Mad Hedge Technology Letter

April 7, 2025

Fiat Lux

Featured Trade:

(THE NEW NORMAL FOR SEARCH ENGINES)

(GOOGL), (TRIP)

Mad Hedge Technology Letter

April 7, 2025

Fiat Lux

Featured Trade:

(THE NEW NORMAL FOR SEARCH ENGINES)

(GOOGL), (TRIP)

Mad Hedge Technology Letter

July 13, 2022

Fiat Lux

Featured Trade:

(HOT INFLATION NUMBER BODES POORLY FOR TECH STOCKS)

(LYFT), (UBER), (AMZN), (SHOP), (GOOGL), (SNAP), (META), (TWTR), (MELI), (EXPE), (TRIP)

Fed swaps now fully price in 150 basis points of hikes over the next two meetings after awful inflation numbers came in showing inflation heading in the wrong direction.

The 9.1% inflation print was an acceleration of the 8.6% which was what we got last time.

I don’t want to beat a dead horse, but inflation accelerating and beating the expectations of 8.8%, is paramount to the trajectory of tech shares.

The awful number also underscores the magnitude of policy mistakes that the U.S. Fed Central Bank has overseen.

This is the only thing that matters because macro liquidity drives the trajectory of equities in the short term.

These clowns aren’t serious about tackling inflation, as I said a few times already and this proves it!

Itty bitty rate rises won’t stamp out 9.1% inflation and in fact, encourages it.

The Fed would need to raise the Fed Funds rate by 7.35% to 9.1% immediately from the current 1.75% for the real inflation rate to be non-inflationary.

According to the official Fed website, the Fed targets 2% inflation because they call this level “healthy.”

By their own measure, to achieve this 2% inflation, they would still need to raise rates by 5.35% immediately, but they absolutely won’t because Powell simply has no interest in doing his job, period.

These core expenses skyrocketing is why I keep and kept mentioning that Americans have less money to splurge on tech gadgets and software and again, this inflation report validates my thesis.

Think about pitiful tech stocks that didn’t work in bull markets like ride chauffeurs Lyft (LYFT) and Uber (UBER), I fully expect these companies to perform terribly over the next 6 months amid a rising rate backdrop.

Not only are they growth tech, but their business is directly tied to energy prices.

They are the poster boys for the pain tech companies will feel from hyperinflation.

The outlook is quite poor for technology in the short term, and we are still waiting to form a bottom. It will come back but we need a capitulation.

The accelerated rate of inflation means that we push back the big recovery in tech stocks.

Ecommerce stocks will suffer like Amazon (AMZN), Shopify (SHOP), and MercadoLibre (MELI) because of the decline in discretional spending for the consumer.

Digital ad giants like Google (GOOGL), Snap (SNAP), Meta (META), and Twitter (TWTR) will need to reckon with smaller ad budgets from 3rd party ad purchasers as companies cut back on marketing spend.

Don’t need to increase marketing spend when people have no money to spend on products.

Travel tech stocks like Expedia (EXPE) and Tripadvisor (TRIP) can expect summer to mark peak travel as Americans get more concerned about food and oil budgets after the summer of travel revenge from the arbitrary lockdowns.

It also means there will be a meaningful next leg down for tech stocks as many CFOs are now furiously crunching the new revenue and margin downgrades to reflect this heightened risk.

The new re-rating isn’t reflected yet in tech shares.

It’s already been a few months on the trot where many analysts say this is the top, they have been inaccurate every time.

Even if it is the top, inflation will stay higher for longer and stagflation is the consensus for 2023.

The clowns at the Fed not doing their job means that economic cycles will be shorter and a great deal more volatile because the smoothing effect of moderated inflation is now stripped out of calculations. This effectively means a contracted boom-bust trajectory for tech stocks which is unequivocally what we are seeing in market behavior.

Mad Hedge Technology Letter

November 18, 2020

Fiat Lux

Featured Trade:

(HOT TECH STOCKS GOING INTO THE RECOVERY)

(YELP), (EXPE), (TRIP)

It’s hard to be net short these days when we are staring at an imminent recovery and by this, I mean not a recovery like the past 6 months where extreme optimism was surrounded by the ceaseless spreading of the virus.

Multiple companies such as Moderna and Pfizer have announced the successful creation of Covid-19 vaccine meaning that consumer behavior and the global economy will come back to normal earlier than first thought.

This is great news for a digital ad company like Yelp (YELP) because they rely on the high volume of businesses open.

Their model is based on consumers offering free reviews and they sell digital ad space on their platform.

With one fell swoop, the virus crushed their business model which was why shares halved during the worst bits of the pandemic.

Sentiment has revered and Yelp stock has been on a remarkable tear, gaining ground for nine straight days and rallying 53% in the process.

The rally started a few days ahead of the company’s better-than-expected third-quarter earnings report, gained momentum when the numbers were released.

Yelp is one of the tech sector’s most outsized profit chances on the reopening of the economy—and investors have jumped aboard.

In my estimation, Yelp is a $40 stock masquerading at $30 today.

Travel-related internet stocks given the potential for a Covid-19 vaccine will feel the same tailwinds and stocks that come to mind are Expedia Group, Inc. (EXPE) and TripAdvisor, Inc. (TRIP).

The beaten-up cyclicals have re-rated over the last several days, Yelp is a standout as a name that should have a clear path towards both multiple and estimate upside from here.

In fact, Yelp’s revenue decline hasn’t been as bad as that of the travel sector, thanks in part to stronger-than-expected restaurant demand.

Even though we have experienced stringent lockdowns, Europeans largely traveled in the summer inside of Europe and Americans still found a way to domestically travel even if more localized.

If the market supports a return post-vaccine for the travel industry, it is clearly confirmation that Yelp’s business will recover fast even if not to the peak of summer 2019.

At these price levels, Yelp has a relatively attractive valuation and improving fundamentals.

When a Covid-19 vaccine is developed and comes available, the company should benefit substantially in terms of foot traffic for businesses on its platform as well as its app volume.

Yelp recently reported a net loss of $1 million, or 1 cent a share, compared with profit of $1 million, or 14 cents a share, in the year-earlier period, and although down, it could have been much worse.

Revenue dropped 16% to $220.8 million from $262.4 million.

"Yelp’s third-quarter results demonstrate our business’s considerable resilience, highlighted by positive year-over-year revenue growth in two key areas of our long-term strategy: home and local services and our self-serve sales channel," Co-Founder and Chief Executive Jeremy Stoppelman said in a statement.

Even though travel and retail outlets were affected, Stoppelman indicated new businesses are being created to serve this new type of economy where the home is the center of businesses.

No doubt there will a surge of new services that will support technological infrastructure for the home and home maintenance.

Yelp’s strong balance sheet and increased sales efficiency will allow Yelp to return to sustainable growth in the new year while still managing the impacts of the pandemic.

The company has clearly shown they are on top of the ball, they use their agility to morph with their times and at this price level, Yelp is an unequivocal buy.

Mad Hedge Technology Letter

January 27, 2020

Fiat Lux

Featured Trade:

(HOW TO PLAY THE CHINESE PANDEMIC)

(TRIP), (TCOM), (GOOGL), (EXPE)

Am I going to rant about Peloton today?

No, I’ll save that for another day.

Let’s get straight to the chase – the epidemic from Wuhan is crushing tech stocks.

If you want a way to play the Chinese coronavirus outbreak, then look no further than Trip.com Group Limited (TCOM).

This company owns a series of reputable Chinese travel apps from Trip.com, Skyscanner, and Ctrip.com.

The Mad Hedge Technology Letter doesn’t tend to do tech alerts on Chinese companies listed in America as American depository receipts.

We rather not expose readers to the high risk of one of them suddenly being kicked off of one of the exchanges.

American investors have zero rights of recouping any losses if Alibaba or Baidu delists or even announces to switch its listing on the Shenzhen tech exchange.

Remember that founder of Alibaba Jack Ma signed over the PayPal of China Alipay to himself without even telling Yahoo about it.

Yahoo was also locked out of any profits from the decision as well even though they were seed investors in Alibaba.

That is China in a nutshell for you!

So what’s happening now? Tourists are staying home in droves and the ones that support the economy which are the Chinese ones during the peak travel season of Chinese New Year.

Cities are getting quarantined left and right in China and the mainland has ordered all travel agencies to suspend sales of domestic and international tours.

Chinese shares have felt the pain with shares of China Southern Airlines Co. – the carrier most exposed to the site of the outbreak – cratering 20% since the second death from the virus was confirmed.

If the situation unfolds like the SARS outbreak of 2003, things could turn bleak quickly.

Remember that in just one month of the SARS outbreak, Chinese air passenger traffic fell 71%, and Trip.com was rerated and has fell off the face of the earth.

I am predicting the same type of devastating numbers to the online travel world.

Trip.com has struggled to keep up with competition from digital rivals like Meituan Dianping and Alibaba, and even if the virus is conquered, business might never come back.

Despite the trade war and Hong Kong’s protests, the world has been held up by the Chinese tourist.

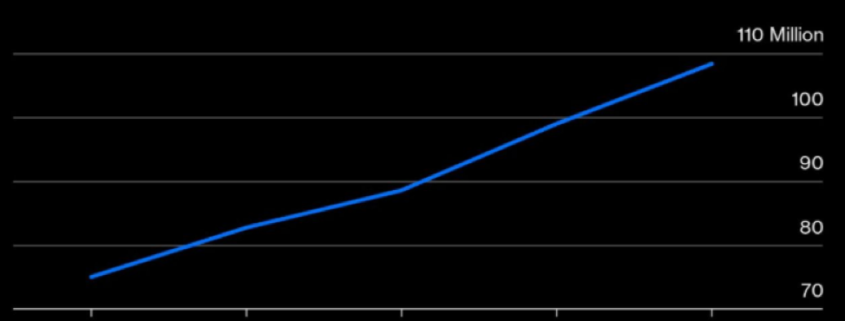

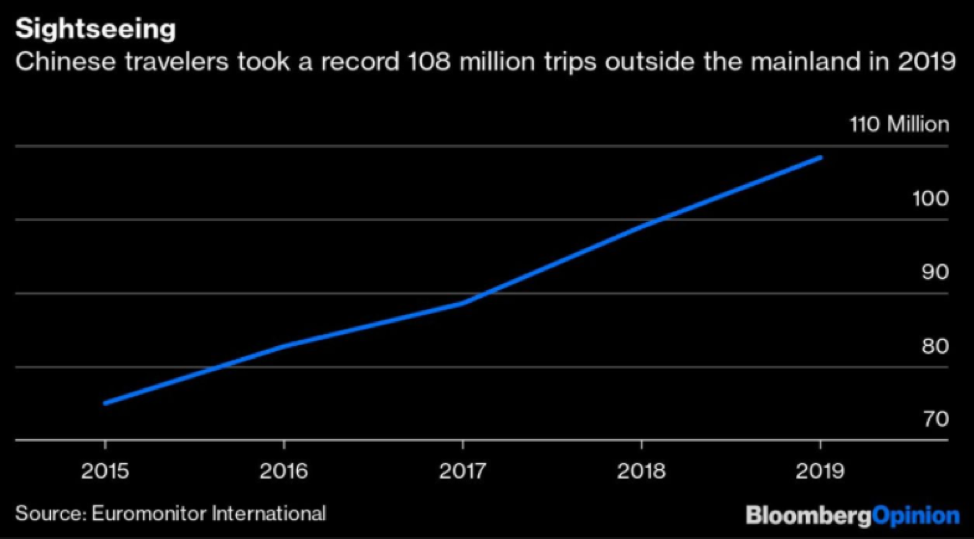

108.39 million Chinese overseas trips were taken last year, a 9.5% gain, after surging 11.7% in 2018.

Flight volume was brimming along nicely until the virus, but the hotel-booking sector is getting crowded.

Meituan Dianping has recently overtaken Trip.com as China’s top site, and now has 47% of China's market, 13% higher than Trip.com.

Now, Meituan is moving further onto Trip.com’s turf with luxury hotels, while chains like Marriott International Inc. are pushing for direct booking on their China websites.

Alibaba said part of the $13 billion it raised from its Hong Kong listing in November would go toward fliggy.com, its online travel group site.

The way the Mad Hedge Technology Letter is playing the sudden drop in overseas travel confidence is through the travel app I dislike the most – TripAdvisor (TRIP).

I actually don’t have a personal problem with the functionality, but the business behind it is terrible.

That was the main reason I strapped on a put spread and I can’t see TripAdvisor outperforming dramatically in the next few weeks in the face of a global pandemic.

This was a short-term trade that TripAdvisor won’t rise 11% in 30 day

I didn’t like this company before the coronavirus and now that Chinese tourists are home sitters for the Chinese New Year, this could put a dent into TripAdvisor’s new China initiative.

Trip.com Group had taken the lead in the day-to-day running of TripAdvisor China. It owns the majority share, with TripAdvisor claiming a 40 percent stake.

Chinese were supposed to increasingly travel the world while its customer base is also becoming more global, in particularly with Trip.com and Skyscanner.

But that is all on hold now.

Yes, it is possible that there could be a dead cat bounce in shares if the virus is tamed, but the 2-week travel season is something you can’t get back once it’s over for TripAdvisor.

I believe this will come out in the numbers along with details about Google’s algorithms further destroying TripAdvisor’s relevancy in the online travel industry.

Then take into account that the company just announced a 200-employee purge for the explicit reason of increased competition from Google and things seem to be going from bad to worse.

The company has done a proverbial deal with the devil by positioning itself to be utterly tied to Google’s search algorithm while Google is going head-to-head with them.

Google has upgraded its travel search tools recently to turn the screws on several trip booking websites like TripAdvisor, Booking.com and Priceline.

In its last earnings release, TripAdvisor noted that Google has placed ads at the top of its search results, forcing companies like it to buy more ads.

The company had a rough last quarter, reporting adjusted earnings of 58 cents a share, down from 72 cents a year earlier and short of analysts’ estimates of 69 cents.

Rhetoric from management was equally as disappointing with them saying, “Google (is) pushing its own hotel products in search results and siphoning off quality traffic that would otherwise find TripAdvisor via free links and generate high margin revenue in our hotel click-based auction.”

“Google has got more aggressive. We’re not predicting that it’s going to turn around.” TripAdvisor CEO Stephen Kaufer said at the time and I don’t see how our put spread will lose money in the short-term.

I will advise readers to take profits when the time comes. Be aware that TripAdvisor also has an earnings report coming up in 2 weeks that could gyrate the stock.

I expect broad-based weakness in guidance and poor performance last quarter in the report.

Mad Hedge Technology Letter

November 8, 2019

Fiat Lux

Featured Trade:

(WANDERLUST TAKES A HIT),

(TRIP), (EXPE)

I have slaughtered travel tech nonstop for quite a while now and today is the day that the bearishness turned ugly.

Let’s take a look at why.

I believe travel tech is a vulnerable group waiting to be taken to the emergency room.

We are approaching the dying embers of the economic bull cycle for better or worse, mostly the latter.

Europe is already mired in a recessionary-like environment and hiring has ground to a halt.

When German automobile manufacturers aren’t doing well, usually the rest of the continent follows suit.

No new jobs mean no new money to travel with and austerity usually whacks off luxuries like hotel stays and cross border travel.

Reading the tea leaves, it’s hard not to think that travel tech could be in for a rough next year with revenue growth sliding like Expedia’s vacation rental business in the third quarter.

The company is signaling slowed momentum in its high growth category leading to a lowered profit forecast for 2020.

The short-term rental unit reported revenue growth of 14% to $467 million, lower than the 17% rate in the previous period and missed analysts’ estimates of $462.4 million.

Total revenue grew 8.6% to $3.56 billion, in line with consensus but as we turn the page, there’s not much to like.

Expedia attempts to juice up home-sharing division, VRBO, in a quest to unseat rivals Airbnb Inc. and Booking Holdings Inc. in the booming home-share market will fall flat.

While VRBO is strong in the U.S. for purely vacation rentals, Airbnb and Booking capture a much larger share of the broader global $34 billion alternative accommodation market, which also includes non-traditional hotels and home-sharing.

Expedia is now set for 2020 adjusted Ebitda growth of 5% to 9%, down from a previous forecast of 15% growth.

VRBO only pulls in just over 10% of Expedia’s overall revenue, but its growth prospects revolve around this one asset.

To reach its targets, Expedia will need a greater dependence on higher-cost marketing channels in a secular flat hotel ADR (average daily rate) environment while grappling with the uncertainty around VRBO weathering a change in brand name.

Many tech companies are finding out that now is the wrong time to champion growth at any costs and travel tech is grossly reliant on exorbitant marketing costs to drive incremental home-sharing revenue.

I can’t say what TripAdvisor (TRIP) is doing is much better than Expedia because it is certainly not.

They have just announced a joint venture and global licensing agreement with China’s Trip.com Group which includes assets Ctrip, Trip.com, Qunar, and Skyscanner.

This is probably the worst time in the past 30 years for an online travel company to dive straight into China.

As I read through the detail, there was one red flag that stood out and that was the bit about “sharing inventory.”

I am doubtful that TripAdvisor is able to have an enforceable mechanism for misbehavior.

For example, if a hotel booked through TripAdvisor China is rerouted into the Trip.com portfolio and executed by the Chinese mainland array of digital assets, how would TripAdvisor respond?

There are too many lurking risks that could easily result in Trip.com Group gaming this agreement to tilt the benefits in their favor.

A cynical part of me tells me that this is just a ruse for Trip.com Group to use TripAdvisor’s brand name which dominates in western developed countries to siphon away foreign tourism revenue.

On a personal level, I have found that Trip.com Group has subsidized its prices which is a boon to consumers but is a way to undercut and pervert competition.

TripAdvisor can’t operate freely in China as it stands, but I wouldn’t desperately decide on a joint venture just to get a shoe in the door.

Better off looking elsewhere or keeping their ammunition dry.

Whether its weakness in VRBO in Expedia or a poor licensing agreement between TripAdvisor and China’s Trip.com Group, there is a lack of good ideas since Airbnb created this industry out of thin air.

Probably better to wait for Airbnb to go public if you want to get into travel tech, they have revolutionized the industry and are profitable or invest in Google who is stealing market share from the old guard.

The higher competition will certainly lead to higher marketing costs, lower growth, and a race to zero commissions.

Mad Hedge Technology Letter

May 15, 2019

Fiat Lux

Featured Trade:

(TRUE COST OF THE CHINA TRADE WAR)

(EXPE), (TRIP), (GOOGL), (CTRP)