Global Market Comments

January 25, 2019

Fiat Lux

Featured Trade:

(JANUARY 9 BIWEEKLY STRATEGY WEBINAR Q&A),

(TSLA), (EDIT), (NTLA), (CRSP), (SJB), (TLT), (FXB), (GLD),

(THE PRICE OF STARDOM AT DAVOS)

Global Market Comments

January 25, 2019

Fiat Lux

Featured Trade:

(JANUARY 9 BIWEEKLY STRATEGY WEBINAR Q&A),

(TSLA), (EDIT), (NTLA), (CRSP), (SJB), (TLT), (FXB), (GLD),

(THE PRICE OF STARDOM AT DAVOS)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader January 23 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Would you buy Tesla (TSLA) right now?

A: It’s tempting; I’m waiting to see if we take a run at the $250-$260 level that we saw at last October’s low. If so, it’s a screaming buy. Tesla is one of a handful of stocks that have a shot at rising tenfold in the next ten years.

Q: CRISPR stocks are getting killed. I know you like the science—do you have a bottom call?

A: What impacted CRISPR stocks was the genetic engineering done on unborn twins in China that completely freaked out the entire industry and killed all the stocks. That being said, CRISPR has a great long-term future. They will either become ten-baggers or get taken over by major drug companies. The first major CRISPR generated cure will take place for childhood blindness later this year. The ones you want to own are Editas (EDIT), Intellia Therapeutics (NTLA), and CRISPR Therapeutics (CRSP).

Q: Do you ever reposition a trade and add contracts?

A: I very rarely double up. I’d rather go on to a new trade with different strike prices. A bad double up can turn a small loss into a big one. Sometimes I will do a “roll down,” or buy back one spread for a loss to earn back that loss with a spread farther in-the-money.

Q: For us newbies, can you please explain your trading philosophy regarding purchasing deep in the money call spreads and how that translates to risk management?

A: I did a research piece in Global Trading Dispatch yesterday on deep in-the-money call spreads, and today on deep-in-the-money put spreads. The idea is to have a position where you make money whether the market goes up, down, or sideways. Your risk is defined, and you always have time decay working for you, writing you a check every day. Here are the links: Vertical Bull Call Spread and Vertical Bear Put Spread.

Q: What’s the risk reward of floating rate corporate debts?

A: Number one: interest rates go down—if we go into recession, rates will fall. That wipes out the principal value of the security. Number two: with corporate debts, you run the risk of the corporation going bankrupt or having their business severely impacted in the next recession and their credit rating cut. It’s far safer to invest in a bank deposits yielding 2-2.5% right now. Some smaller banks are offering certificates of deposit with 4% yields.

Q: What are your thoughts on the British pound (FXB)?

A: I think Brexit will fail eventually and the pound will increase 25%; so play from the long side on the (FXB). It would be economic suicide for Britain to leave the EC and eventually people there will figure this out. If the Brexit vote were held today, it would lose and that may be how they eventually get out of this.

Q: Is it a bear market for bonds (TLT)?

A: Yes, it’s back on again. I expect we will visit $112 in the (TLT) sometime this year, down from the current $121. That brings us back up to the 3.25% yield on the ten-year US Treasury bond. That is down nine points from here, so it’s certainly worth taking a bite out of.

Q: What’s the best time to buy the ProShares Short High Yield (SJB)?

A: At the top of the next equity market run. It rose a whopping 10% during the December stock market meltdown so that gives you a taste of what can happen. Junk bonds are called “junk” for a reason.

Q: How do you see gold (GLD)?

A: Take profits now and buy back on the next dip. If we dip 5%-10% in gold, that would be a good entry point for a larger move later on in the year. To get a real move in gold, we need to see real inflation and that will eventually come. Another stock market crash will also gain you another 10% in gold.

Q: When will the government shutdown end?

A: I think it will go a lot longer than anyone realizes because Trump needs a deal worse than the Democrats do. Trump is basically saying pay for my wall or I’ll keep shooting another of MY supporters in the head every day. The Democrats can wait a really long time in that circumstance. Trump’s standing in the polls has also collapsed to new lows. By the way, the Chinese are using the same approach in the trade talks so that could be a long wait as well.

Q: There’s been a big shift in the MHFT Profit Predictor in the last 30 days—does this mean we should not be adding any positions?

A: Absolutely; this is a terrible place to be adding any new positions. The index went from 2 to 57 which shows you how valuable it is at calling market bottoms. Now we are at the top end of the middle of the range. All markets are now dead in the middle of very wide trading ranges which means the best thing you can do is take profits on existing positions, which I have been doing. Or watch Duck Dynasty and Pawn Stars replays. As for me, I am an Antiques Roadshow guy.

Q: What percentage should you be invested in the market now?

A: I’ve gone from 60% to 30% and have only 3 weeks left on my remaining position. I’m looking to go 100% cash as long as we’re stuck in the middle of this range. Better to sit on your hands than chase a high risk/low return trade.

Did I mention that we have had the best start to a New Year in a decade?

Mad Hedge Technology Letter

January 22, 2019

Fiat Lux

Featured Trade:

(HOW TO PLAY TECHNOLOGY STOCKS IN 2019),

(NFLX), (AAPL), (TSLA), (STT), (BLK)

In the past week, the tech sector has received information allowing investors to sketch a concise roadmap of what to expect in the tech sector for the rest of 2019.

One – the bull story in technology isn’t dead and the December sell-off in tech growth stocks was overdone.

Two – the path to tech profits is filled with more booby traps than in year’s past.

Three – the migration to digital is becoming more pronounced by the millisecond.

If you go back about a month ago when tech stocks were at their trough, traders were pricing in about a 60% chance of a recession in 2019 or early 2020 and the data didn’t support it.

What people were confusing themselves with was slowing growth instead of a lack of growth.

Then we got the disastrous news from Apple (AAPL) indicating business in China was petering out forcing them to change tactics cutting iPhone prices.

The tech market went into full-on panic mode and the revelation of weak China data did not help either.

Netflix (NFLX) reported and the online streaming app offered some respite with outperforming growth numbers.

Netflix has been a favorite of the Mad Hedge Technology Letter since its inception but the caveat with Founder and CEO of Netflix Reed Hastings brainchild is that the extreme volatility makes it difficult to trade around on a short-term basis.

The stock is up 50% from its nadir and its growth story is solid and will perpetuate.

The next bastion of juiced-up growth for Netflix is the international audience and these numbers are examined closely with a fine-tooth comb by investors attempting to understand the direction of the company.

The company audaciously added 8.8 million in new international subscribers last quarter which handily beat the 7.6 million estimates by 1.2 million.

Netflix also announced a few days earlier that it would raise the price of a monthly subscription between 13%-18%, and investors treated the news with celebratory shots of tequila.

It has been consensus for years that Netflix was severely underpricing their premium content, and analysts have been screaming and kicking trying to get Hastings to push up their monthly prices.

The price hike coincides with a year where I believe Netflix can grow revenue over 30%.

The mix of these two developments illuminate a few things about Netflix.

Netflix has the content that consumers want and even if competition rears its ugly head, they aren’t even in the same ballpark in terms of breadth and potency of content.

They are the king of contents and I don’t see anyone knocking them off their elevated perch in 2019.

In many ways, the Netflix long-term thesis mirrors the tech industry’s long-term thesis emphasizing supercharged growth by any means possible.

Even though this strategy is risky, it is working for Netflix and the capital isn’t drying up to go after the best content producers money can buy.

This earnings report should put to rest the growth warning sirens for now, tech will grow this year, but earnings results will be more of a mixed bag with the occasional miss.

This is in stark comparison to early 2018 where every tech company and their mother were scorching earnings forecasts by a magnitude of two or three.

Last September, the tech market looked above its head and saw a few boulders about to crush the herd, but investors shrugged it off.

As we move forward, the tech sector and the overall market is inching closer to a recession.

The low-hanging fruit has been pocketed and incremental gains aren’t no-brainers anymore – this can be gleaned from Tesla (TSLA) curtailing their workforce by 7%.

This news was delivered by a letter from CEO of Tesla Elon Musk noting that these decisions have been made with the goal of “increasing the Model 3 production rate and making many manufacturing engineering improvements in the coming months.”

Basically, Musk has telegraphed that staff needs to perform better, identify efficiencies that will save costs which in turn will boost profit margins.

This doesn’t mean that the era of tech growth is over, but this signals that tech companies are becoming more fidgety about loss-making operations and have ultimately targeted profits which shout at investors' late-cycle economics.

Musk needs to turn Tesla into a perennial profit machine to prove naysayers wrong, and now is the time to turn the page and max out his rocket fuel.

If the recession hits, investors could turn against Tesla and capital could dry up.

This newfound modesty towards the e-car business model is, in no doubt, exacerbated by the ratcheting up of fierce competition from the traditional automobile makers.

Tesla is in the e-car lead for battery technology, revolutionary production processes, and have a treasure trove of data that German companies would do anything to get their hands on.

Musk knows Tesla has fought this hard to get to this point, and he'd rather have the ball in his hands with 10 seconds left and a tie game just like Michael Jordan of the Chicago Bulls did.

Shaving off the excess has meant removing the customer referral program that was too costly that included benefits like half a year of free charging.

Part of this also has to do with Tesla losing their tax credit at the end of the year as well as giving more impetus to trimming costs.

Becoming a mass-market car manufacturer means it is important to price the car at affordable price points and that will be extremely difficult.

The goal is to deliver a $35,000 e-car that performs comparably to the rest of the fleet but produced with 7% less hands.

Can Musk do it?

I wouldn’t bet against him.

Musk means business and is hellbent for revenge against his arch enemies – the Tesla short community who he has habitually dragged under the bus through the media.

Piggybacking on this tougher profit-making climate is Boston-based finance company State Street Corporation’s (STT) announcement reducing headcount by 1,500 amounting to 6% of the global workforce.

The firm cited the urgent need to automate processes that will give the company a bigger foothold into the digital sphere.

The same theme was echoed at BlackRock Inc. (BLK), the world’s largest asset manager, who will eliminate 3% of its global workforce, or 500 people, amid an existential threat from the temporary ineffectiveness of passive investing.

In a rising market, it is guaranteed that assets at these types of funds almost always go up.

However, with an injection of recent volatility, passive investors have seen their balances dwindle with the market spawning abrupt outflows.

The need to zig and zag with the market is now painfully obvious and using technology to plug in the gaps will be cheaper and more appropriate for late cycle price action.

This is a suitable segue way into the third point – the fluid follow-through of the digital migration and the debacle of Sears prove my point.

Hedge fund manager Eddie Lampert and his firm ESL have navigated this famous American retailer into the ground.

This is what happens when the entire retail industry goes online when you don’t.

To make matters worse, Lampert has probably never set foot into his own investment.

Each time I roam the aisles of Sears, it’s about as crowded as a mortuary at midnight – an elementary story of a mismanaged enterprise.

Sears is an example of digital ignorance and it’s not the only one.

Gymboree Group, the baby clothing company, is another one to put on the list – the firm filed for Chapter 11 bankruptcy protection.

The company will close more than 800 Gymboree and Crazy 8 stores, this is the second time they have filed for bankruptcy protection in the past two years.

Unsurprisingly, the firm cited a sudden decrease in mall traffic and a surge in online alternatives as the reason for the economic softness.

The economy does not operate in a vacuum and any analog company who voluntarily misses the pivot to digital is voluntarily digging their own grave.

These three trends will only become more exaggerated moving forward threatening companies like Apple who fail to innovate after more than a decade of selling the same product, other companies don’t have the balance sheets to handle the same weakness.

Global Market Comments

January 17, 2019

Fiat Lux

Featured Trade:

(WHAT HAPPENED TO THE DOW?)

($INDU), (EK), (S), (BS), (CVX), (DD), (MMM),

(FBHS), (MGDDY), (FL), (GE), (TSLA), (GM)

(WHY YOUR OTHER INVESTMENT NEWSLETTER IS SO DANGEROUS)

Mad Hedge Technology Letter

January 14, 2019

Fiat Lux

Featured Trade:

(THE TECH DARLING OF 2019),

(TWLO), (MSFT)

Mad Hedge Technology Letter

January 10, 2019

Fiat Lux

Featured Trade:

(HERE’S THE CANARY IN THE COAL MINE FOR APPLE),

(AAPL), (SWKS), (AMZN), (TSLA)

A tech company in the jaws of the trade war dilemma is one to keep tabs on because this company leads Apple’s stock price.

Many industry analysts say that the market cannot recover unless Apple participates.

Paying homage to the sheer size of Apple is one thing, and the gargantuan size means that many other companies are positioned to feed off of Apple revenue model and rely on the iPhone maker for the bulk of their contracts.

Is this a dangerous game to play?

Yes.

But its better than having no business at all.

No stock epitomizes this strategic position better than niche chip stock Skyworks Solutions (SKWS) who extract 83% of total revenue from China.

Apple announced slashing production to its latest iPhone model by 10% in the first quarter due to weak sales.

Apple has also trimmed forecast for total iPhone production from about 48 million to between 40 and 43 million.

The company also failed to meet its latest projected forecast selling a disappointing 46.9 million in the fourth quarter of fiscal 2018, significantly lower than analysts’ expectation of 47.5 million units.

Then when you thought the bottom was in, President of the United States Donald Trump announced an escalation of tariffs from 10% to 25% on Chinese goods that could siphon off 10% of Apple’s revenue from China-produced iPhones.

All this means is that Skyworks Solutions (SWKS) is now the most oversold stock in the tech sector going from $123 about a year ago to about $63.

The avalanche of grumpy news has halted Apple in its track, but Skyworks Solutions is truly ground zero, the metaphorical canary in the coal mine.

The uncertainty that pervades this part of tech does what tech stocks abhor - puts a cap on Skyworks Solutions ceiling and the whole industry which peaked last year.

Containment is the absolute worst description of a tech because it tears apart any remnant of a growth narrative which tech firms need to justify the accelerating investment.

This is evident in how CEO of Tesla (TSLA) Elon Musk ran his business. If he didn’t convince and mesmerize the public with his antics and chutzpah, he might not have cultivated the star power to have pushed through a loss-making enterprise for so long.

Now the loss-making enterprise is history and Musk is finally turning a profit.

Now let’s turn to the chip sector – sling and arrows have been fired with some direct hits.

Samsung reported earnings and scared off investors with a dud.

Management presides over a huge drop in earnings making China and weak sales as the scapegoats.

Samsung’s first profits decline for 2 years could be a sign of things to come.

Chip momentum and earnings are decelerating. There is no getting around that.

Investors will need management to flush out the chip glut and need confirmation that prices have bottomed to really flesh out a legitimate turnaround later this fiscal year.

Samsung curtailed sales estimates by 10% and expect operating profits to sink 28.7% in 2019.

The walking wounded Korean chaebol has also been the recipient of a massive price war against Chinese smartphones, the end result being that consumers are favoring lower-priced Chinese substitutes that match Samsung’s Galaxy 80% of the way.

Remember that when you battle China tech companies – it’s a fight against the Chinese state who subsidizes these behemoths and have access to unlimited loans at favorable interest rates.

Apple has had the same problem, as well as Huawei and Xiaomi, have started producing premium smartphones. Second tier Chinese smartphone makers Oppo and Vivo have also picked up market share at the marginal buyer level.

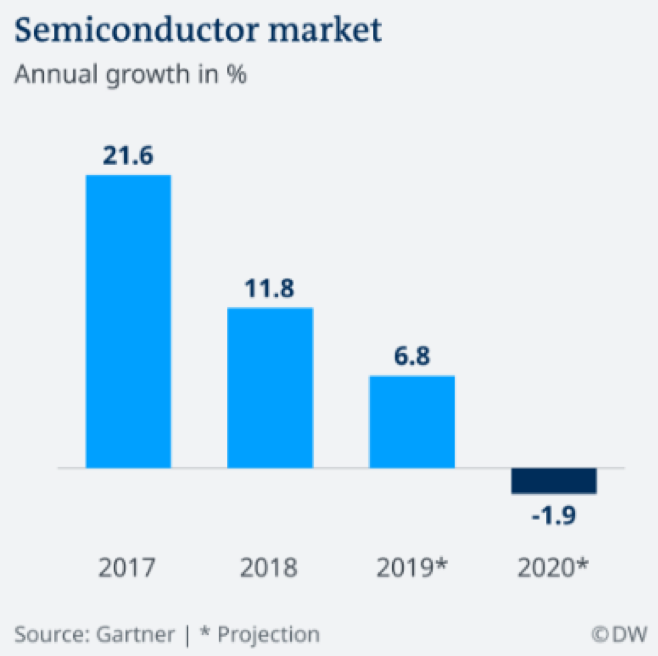

Semiconductor annual growth in 2018 held up quite well even though a far cry from 2017 when the semiconductor industry expanded 21.6%.

However, this year forecasts to only eke out 6.8% growth and then 2020 will turn negative with growth contracting 1.9%.

These dismal numbers could signal total revenue downshifting below total revenue numbers not seen since 2016.

In short, the chip industry is going backwards and backwards quickly.

I wouldn’t want to bet the ranch on any chip names now because the short-term prospects are grim.

The perfect storm of market saturation, overproduction, facetious geopolitics, weak demand, and unparallel competition is not a good cocktail of drivers towards accelerating earnings growth.

This is, in fact, a recipe for disaster.

And when you look at mobile, the phenomenon has been a true gamechanger and success but let’s face the facts, its already onto its 15th year and petering out.

There is only so much juice you can squeeze from a lemon.

Mobile will last for the time being until something better comes along which is absolutely what the tech markets are screaming for.

Tech companies have monetarily benefitted from this massive migration to mobile and there are still some hot croissants to take home from the bakery but I would estimate that 80% of the low-hanging fruit is off the tree.

That leads me to double down on my recent rant of a lack of innovation.

Google is still making most of its revenue from ad search and going 18 years strong, there will be no plans to stop even in year 30 and beyond.

Apple has been making iPhones for over 12 years.

Oracle is still selling the same dinosaur database software that has barely changed for a generation, except for the prettified front end.

Amazon is the only company that is brimming with innovation and that is the very reason why all companies must react to the Amazon threat because they set the terms of engagement.

The pipeline is fertile to the point its hard to keep track of all the new products coming out of the company.

Bezos has stayed head and shoulders ahead of the competition because the competition has gotten comfortable, content with above average market positioning, and gobbling up the profits.

Once companies start behaving this way, it is the beginning of the end.

Then there is Skyworks Solution.

Can you imagine if Apple ever announced a ground-breaking new product that would see them stop making iPhones?

Skyworks Solution would go out of business.

This elevated existential risk has nudged up the beta on this stock and it trades accordingly.

Apple’s price action lags Skyworks Solution’s, but the chip companies' booms and busts are more exaggerated.

On cue, Skyworks Solutions announced a cut in guidance from $1 billion in revenue to $970 million in 2019.

EPS would drop from an estimated $1.91 to $1.81-$1.84.

Skyworks president and CEO Liam Griffin said they were “impacted by unit weakness across our largest smartphone customers.”

A bottom looks to be forming unless the trade war turns for the worse again.

The silver lining is that Skyworks Solutions is in queue for some hefty 5G contracts for the upcoming network upgrade.

This would be Skyworks Solutions' chance to jump out of the ring of fire and attach themselves to alternative revenue that doesn’t shred their share price in a growing piece of the tech industry.

If Skyworks Solutions manages to successfully pivot to 5G and specifically IoT products, management will finally be able to wipe away the sweat bullets because welding yourself to Apple’s story hasn’t been heavenly as the global smartphone market has calcified.

Global Market Comments

January 10, 2019

Fiat Lux

Featured Trade:

(JANUARY 9 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (UUP), (FXE), (FXY), (FXA), (AAPL), (GLD), (SLV), (FCX), (SOYB), (USO), (MU), (NVDA), (AMD), (TLT), (TBT), (BIIB), (TSLA)

(TESTIMONIAL)

Due to technical problems, I was unable to read your questions. However, I was able to get a print out after the fact.

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader January 9 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader.

Q: Is the bottom in for stocks?

A: It is for six months to a year. A price earnings multiple at 14X seems to be the line in the sand. The Christmas Eve massacre, which took us down to a (SPY) of $230, was the final capitulation bottom of the entire down move. We may try a few more retests of the lows on bad tweets or data points. But from here on, you’re trying to buy the dip. That’s why I cut my vacation short a week and issued eight emergency trade alerts, five for Global Trading Dispatch and three for the tech letter. By the way, I hope you appreciate those trade alerts because I had to call back staff from vacations in four different countries to get them done. But it was worth it. We’ve had the strongest start to a New Year in a decade, up 5.75%. We made back all our Q4 losses in two days!

Q: Is the strong dollar play (UUP) over? Is it time to start buying Euro (FXE) and Yen (FXE)?

A: Yes, it is. The Fed flipping from hawk to dove sounds the death knell for the dollar. With the expansion of the yield spread between the buck and other currencies stopped dead in its tracks, a massive short covering rally will drive the currencies higher. That’s why I bought the Euro on Monday for the first time in more than a year (FXE). The Japanese yen where the biggest shorts has already moved too far, up 8%. That’s where hedge fund typically finance positions because yen yields have been at zero forever.

Q: How about the Aussie (FXA)? Do we have a shot now?

A: I think so. But the bigger driver with Aussie is the trade war with China. That said, I believe that will get resolved soon too unless Trump wants to run for reelection during a recession. The Aussie also has relatively high-interest rates so it should soar.

Q: Is the government shutdown starting to hurt the economy?

A: Yes, it is. Estimates on the damage the shutdown is doing range from 0.5% to 1% a week. That means at a minimum of 20-week shut down cuts 2019 GDP growth by 1%. If your assumption for growth this year is only 2%, that brings us perilously close to a recession. However, with the big stock market rally of the past week investors clearly believe the shutdown will be over in a week. Buy “Wall” stocks.

Q: What’s the biggest risk to the market now?

A: Companies announced great earnings in October and the stocks promptly collapsed. Q4 earnings start in a few weeks, except this time, the earnings will be smaller. The big one, Apple (AAPL) is reporting on January 29 and will be especially exciting since they already announced a major disappointment. If we get a repeat, you could get another meltdown in February just like we saw last year.

Q: Do you still like gold (GLD)?

A: I did in Q4 as a hedge for a collapsing stock market. Now that stocks are on fire again, I think gold and silver (SLV) will take a rest. You’re not going to get a serious move in gold until we see higher inflation and that is a while off.

Q: Is the bear market in commodities over?

A: I think so, with a flattening interest rate picture and a weakening dollar, the entire commodity complex is looking better. That includes copper (FCX), energy (USO), and the ags (SOYB). What do you buy in an expensive market? Cheap stuff, and all of these are at seven-year lows. I think people are ready to give paper assets a rest. All we need now for these to work is inflation. My cleaning lady just asked for a raise so there’s hope.

Q: The semiconductors have just had a good move. Is it time to get in?

A: You want to buy the semis, like Micron Technology (MU), NVIDIA (NVDA), and Advanced Micro Devices (AMD) when they’ve just had a BAD move. Market conditions have improved, but not to the extent you want to buy the most volatile stocks in the market. That said, if we get another crushing move in February you might dip your toe in with some semis on capitulation day. If you want to buy semis in this environment, you might have a gambling addiction.

Q: If the Fed has stopped raising rates, are you still bearish on the (TLT) and bullish on the (TBT)?

A: I think what governor Jay Powell’s dovish comments will do is put bonds in a six-month range, say 2.45%-3.0% in yield. All of my future bond alerts will trade around those levels. In the option world, we will be setting up a short strangle, betting that interest rates don’t move out of this range for a while. In that case, our two bond positions will be OK, with the nearest money one expiring in only seven trading days.

Q: Is it too late to get into biotech (BIIB)?

A: No, along with technology, biotech will be one of the two leading sectors in the entire market for the next ten years. However, me being an eternal cheapskate, I want to get in again on a decent dip. This is the industry that will cure cancer over the next decade and that will be worth a trillion dollars in profits.

Q: You’ve kept us out of Tesla (TSLA) for a couple of years. Is it time to go back in?

A: I think I would. If production can ramp up from 7,000 to 10,000 a week, the stock should do the same. The ten-year view for this stock is that it goes from today’s $330 to $2,500. That said, this is a notorious trading stock so it is very important to buy it on a dip. Wait for the next tweet from Elon Musk.

Q: If we enter a bear market in May 2019, what would be the appropriate long-term investments at that time?

A: Nothing beats cash, especially now that you are actually getting paid something decent. You can find cash equivalents now yielding all the way up to 4%. In a bear market, stocks either go down a lot, or a whole lot, so there is nothing worth keeping. The only reason to stay in is to avoid a monster tax bill (my cost on Apple is 25 cents) or you still work for the company.