TSLA stock was once the darling of tech that could do no wrong.

The stock fetched a high premium punching above its weight.

That was then and this is now.

Then CEO of Tesla Elon Musk bought Twitter and everything changed.

He took a financial hit from the acquisition and investors are still not sure this purchase will weigh down his other companies.

Even more concerning is Musk’s entrance into American cultural wars and political punditry where he has tweeted fiercely about controversial topics lately.

This area is a black hole for tech entrepreneurs.

Losing half of a customer base is not a good business strategy and Musk is finding this out the hard way.

He has tweeted that the reason for his behavior is to “save mankind” or “nothing else matters.”

Try telling that to owners of Tesla shares.

They have been losing money hand over fist lately as Tesla shares have cratered while other tech stocks experience a mild renaissance.

Tesla has deflated by half a billion dollars in market cap lately.

Tech shares lurched upwards yesterday fueling a strong rally after weak inflation data.

However, there was one stock that was noticeably lagging big time.

Tesla was down 4% as investors used it as a good reason to dump the stock. Tesla shares are down again today – it’s almost like Groundhog Day.

There has also been a massive uptick in Democrats dumping Tesla shares and posting their actions on Instagram while claiming to have sold their Tesla car.

Musk alienating Tesla owners’ way of thinking and way of life spells lower future revenue.

Musk is simply shutting off the path for more Joe Biden-loving investors, and that’s bad news for the stock short-term since most owners of Tesla shares are Democrats.

There are also other issues percolating under the hood.

Slumping demand in China is forcing the electric-vehicle maker to slow production and delay hiring at its Shanghai factory.

Activist Tesla investor, Ross Gerber, is calling for the board to add a director who would represent retail shareholders.

This is after news reports of Musk sleeping at San Francisco’s Twitter headquarters.

Investors also feel that part of the reason Tesla shares have sold off is because the CEO isn’t paying attention to Tesla while he works on Twitter.

Musk reiterated that he “continues to oversee both Tesla & SpaceX, but the teams there are so good that often little is needed from me.”

“Tesla Team has done incredibly well, despite extremely difficult times,” he said earlier in the day, citing the European energy crisis, real estate downturn in China, and US interest rates as macroeconomic challenges.

The volatile recent stretch muddies the close of a year in which Tesla is still expected to achieve record sales and retain its crown as the world’s largest EV maker.

It hasn’t been immune, however, from the slowdown in China’s car market and recessionary conditions in Europe.

Tesla expects to come up just short of the 50% growth in vehicle deliveries that the company has repeatedly said it’s expecting over several years.

Tesla’s plant in Austin, Texas is scaling slower than expected, with a new form of lithium-ion battery cells not yet ready for volume production.

In China, Tesla plans to cut production on the Model Y and Model 3 production lines in Shanghai by about 20%.

There are some silver linings.

The company recently started delivering its long-awaited Semi truck several years late and plans to finally start producing its first pickup, the Cybertruck.

Tech investors need to be careful about TSLA for the time being and understand that it doesn’t command a hefty premium like it once did.

I believe that there are plenty of other tech companies to focus on when tech stocks start to buck the negativity of 2022.

Profitable software stocks with a strong balance sheet should be at the top of your list.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-12-14 16:02:282022-12-29 15:15:52Tesla In Trouble

Last week, I spoke about the “smart” market and the “dumb” market.

Looking across asset class behavior over the last couple of years, it’s become evident, there is another major driver.

Liquidity.

Hedge fund legend George Soros was an early investor in my hedge fund because he was looking for a pure Japan play. But I learned a lot more from him than he from me.

No shocker here: it’s all about the money.

Follow the flow of funds and you will always know where to invest. If you see a sustainable flow of money into equities, you want to own stocks. The same is true with bonds.

There is a corollary to this truism.

The simpler an idea, the more people will buy it. One can think of many one or two-word easy-to-understand investment themes that eventually led to bubbles: the Nifty Fifty, the Dotcom Boom, Fintech, Crypto Currencies, and oil companies.

Spot the new trend, get in early, and you make a fortune (like me and Soros). Join in the middle, and you do OK. Join the party at the end and it always ends in tears, as those who joined crypto a year ago learned at great expense.

If I could pass on a third Soros lesson to you, it would be this. Anything worth doing is worth doing big. This is why you have seen me frequently with a triple position in the bond market, or the double short I put on with oil companies two weeks ago, clearly just ahead of a meltdown.

Which brings me back to liquidity.

There are only two kinds of markets: liquidity in and liquidity out. Liquidity was obviously pouring into markets from 2009. This is why everything went up, including both stocks and bonds. That liquidity ended on January 4, 2022. Since then, liquidity has been pouring out at a torrential rate and everything has been going down.

So, what happened on October 14, 2022?

The hot money, hedge funds, and you and I started betting that a new liquidity in cycle will begin in 2023 and continue for five, or even ten years. This is why we have made so much money in the past two months.

Notice that liquidity out cycles are very short when compared with liquidity in cycles, one to two years versus five to ten years. That’s because populations expand creating more customers, technology advances creating more products and services, and economies get bigger.

When I first started investing in stocks, the U.S. population was only 189 million, the GDP was $637 billion, and if you wanted a computer, you had to buy an IBM 7090 for $3 million. Notice the difference with these figures today: $25 trillion for GDP, a population of 335 million, and $99 for a low-end Acer laptop, which has exponentially more computer power than the old IBM 7090.

What did the stock market do during this time? The Dow Average rocketed by 54 times, or 5,400%. And you wonder why I am so long term bullish on stocks. The people who are arguing that we will have a decade of stock market returns are out of their minds.

Which reminds me of an anecdote from my Morgan Stanley days, in my ancient, almost primordial past. In September 1982, I met with the Head of Investments at JP Morgan Bank (JPM), Mr. Carl Van Horn. I went there to convince him that we were on the eve of a major long term bull market and that he should be buying stocks, preferably from Morgan Stanley.

Every few minutes he said, “Excuse me” and left the room to return shortly. Years later, he confided in me that whenever he left, he placed an order to buy $100 million worth of stock for the bank’s many funds every time I made a point. That very day proved to be the end of a decade-long bear market and the beginning of an 18-year bull market that delivered a 20-fold increase in share prices.

But there is a simpler explanation. Liquidity in markets are a heck of a lot more fun than liquidity out ones, where your primary challenge is how to spend your newfound wealth.

I vote for the simpler explanation.

Yes, this is how markets work.

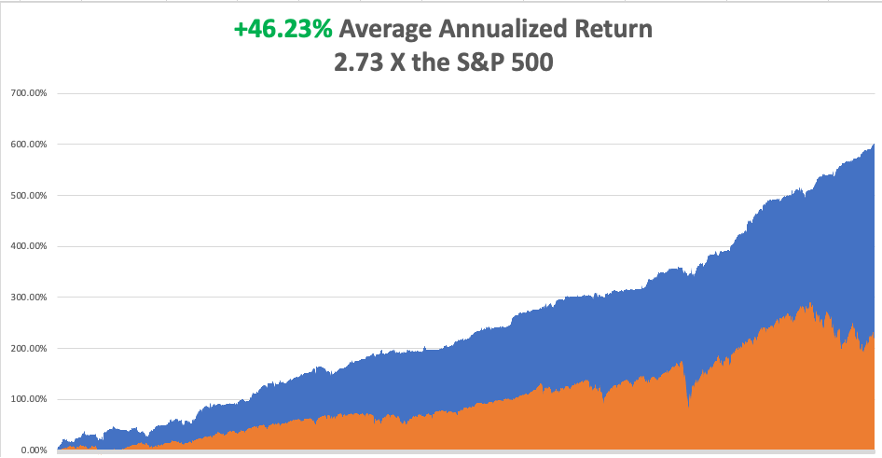

My performance in December has so far tacked on another robust +4.85%. My 2022 year-to-date performance ballooned to +88.53%, a spectacular new high. The S&P 500 (SPY) is down -17.0% so far in 2022.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +92.92%.

That brings my 14-year total return to +601.09%, some 2.73 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +46.23%, easily the highest in the industry.

I took profits in my oil shorts in (XOM), (OXY), (SPY), and (TSLA). I am keeping one long in (TSLA), with 90% cash for a 10% long position.

Producer Prices Come in High, up 0.3% in November, driven by rising prices for services. It sets up an exciting CPI for Tuesday morning.

Emerging Markets Saw Massive Inflows in November, some $37.4 billion, the most since June 2021. Chinese technology stocks were two big beneficiaries, down 80%-90% from their highs. This could be one of the big 2023 performers if the US dollar and interest rates continue to fall. Buy (EEM) on dips.

Oil is in Free Fall, with 57 fully loaded Russian tankers about to hit the market. Nobody wants it ahead of a recession. All mad hedge short plays in energy are coming home. When will the US start refilling the Strategic Petroleum Reserve?

Turkey Blocks Russian Oil at the Straights of Bosporus, checking insurance papers, which are often turning out to be bogus. Insurance Russian tankers are now illegal in western countries. Many of these tankers are ancient, recently diverted from the scrapyard and in desperate need of liability insurance. Oil spills are expensive to clean up. Just ask any Californian.

Tesla Cuts Production in China, some 20% at its Shanghai Gigafactory for its Model Y SUV, or so the rumor goes. The short sellers are back! These are the kind of rumors you always hear at market bottoms.

US Unemployment to Peak at 5.5% in Q3 of 2023, according to a survey from the University of Chicago Business School. A tiny handful expects a higher 7.0% rate. Some 85% of economists polled expect a recession next year. After that, the Fed will take interest rates down dramatically to bring unemployment back down. No room for a soft landing here.

Home Mortgage Demand Plunges in another indicator of a sick housing market, which is 20% of the US economy. New applications are down a stunning 86% YOY despite a dive in the 30-year rate to 6.41%, but nobody is selling. Refis are now nonexistent.

Gold Continues on a Tear, hitting new multi-month highs. With interest rates certain to plummet in 2023 as the Fed reacts to a recession, Gold could be one of the big trades for next year. Buy (GLD), (GDX), and (GOLD) on dips.

Services PMI Hits New Low for 2022 at a recessionary 46.2. Nothing but ashes in this Christmas stocking. It didn’t help bonds, which sold off two points yesterday.

Demand Collapse Hits China (FXI), with US manufacturing there down 40% and many factories closing early for the New Year. Container traffic from the Middle Kingdom is down 21% over the past three months, astounding ahead of Christmas.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, December 12 at 8:00 AM, the Consumer Inflation Expectations for November is published.

On Tuesday, December 13 at 8:30 AM EST, the Core Inflation Rate for November is out

On Wednesday, December 14 at 11:00 AM EST, the Federal Reserve Interest rates decision is announced. The Press Conference follows at 11:30.

On Thursday, December 15 at 8:30 AM EST, the Weekly Jobless Claims are announced. Retail Sales for November are printed.

On Friday, December 16 at 8:30 AM EST, the S&P Global Composite Flash PMI for December is disclosed. At 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, in 1978, the former Continental Airlines was looking to promote its Air Micronesia subsidiary, so they hired me to write a series of magazine articles about their incredibly distant, remote, and unknown destinations.

This was the only place in the world where jet engines landed on packed coral runways, which had the effect of reducing engines lives by half. Many had not been visited by Westerners since they were invaded, first by the Japanese, then by the Americans, during WWII.

That’s what brought me to Tarawa Atoll in the Gilbert Islands, and island group some 2,500 miles southwest of Hawaii in the middle of the Pacific Ocean. Tarawa is legendary in the US Marine Corps because it is the location of one of the worst military disasters in American history.

In 1942, the US began a two-pronged strategy to defeat Japan. One assault started at Guadalcanal, expanded to New Guinea and Bougainville, and moved on to Peleliu and the Philippines.

The second began at Tarawa, and carried on to Guam, Saipan, and Iwo Jima. Both attacks converged on Okinawa, the climactic battle of the war. It was crucial that the invasion of Tarawa succeed, the first step in the Mid-Pacific campaign.

US intelligence managed to find an Australian planter who had purchased coconuts from the Japanese on Tarawa before the war. He warned of treacherous tides and coral reefs that extended 600 yards out to sea.

The Navy completely ignored his advice and in November 1943 sent in the Second Marine Division at low tide. Their landing craft quickly became hung up on the reefs and the men had to wade ashore 600 yards in shoulder-high water facing withering machine gun fire. Heavy guns from our battleships saved the day but casualties were heavy.

The Marines lost 1,000 men over three days, while 4,800 Japanese who vowed to keep it at all costs, fought to the last man.

Some 35 years later, it was with a sense of foreboding that I was the only passenger to debark from the plane. I headed for the landing beaches.

The entire island seemed to be deserted, only inhabited by ghosts, which I proceeded to inspect alone. The rusted remains of the destroyed Marine landing craft were still there with their twin V-12 engines, black and white name plates from “General Motors Detroit Michigan” still plainly legible.

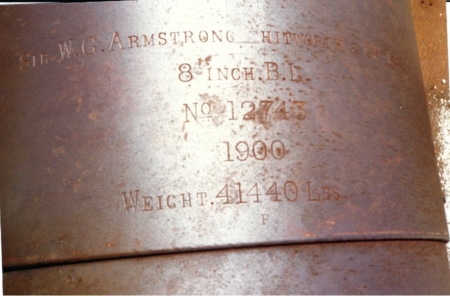

Particularly impressive was the 8-inch Vickers canon the Japanese had purchased from England, broken in half by direct hits from US Navy fire. Other artillery bore Russian markings, prizes from the 1905 Russo-Japanese War transported from China.

There were no war graves, but if you kicked at the sand human bones quickly came to the surface, most likely Japanese. There was a skull fragment here, some finger bones there, it was all very chilling. The bigger Japanese bunkers were simply bulldozed shut by the Marines. The Japanese are still in there. I was later told that if you go over the area with a metal detector it goes wild.

I spend a day picking up the odd shell casings and other war relics. Then I gave thanks that I was born in my generation. This was one tough fight.

For all the history buffs out there, one Marine named Eddie Albert fought in the battle who, before the war, played “The Tin Man” in the Wizard of Oz. Tarawa proved an expensive learning experience for the Marine Corps, which later made many opposed landings in the Pacific far more efficiently and with far fewer casualties. And they paid much attention to the tides and reefs, developing Underwater Demolition Teams, which later evolved into the Navy Seals.

The true cost of Tarawa was kept secret for many years, lest it speak ill of our war planners, and was only disclosed just before my trip. That is unless you were there. Tarawa veterans were still in the Marine Corps when I got involved during the Vietnam War and I heard all the stories.

As much as the public loved my articles, Continental Airlines didn’t make it and was taken over by United Airlines (UAL) in 2008 as part of the Great Recession airline consolidation.

Tarawa is still visited today by volunteer civilian searchers looking for soldiers missing in action. Using modern DNA technology, they are able to match up a few MIAs with surviving family members every year. I did the same in Guadalcanal.

As much as I love walking in the footsteps of history, sometimes the emotional price is high, especially if you knew people who were there.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Tarawa November 1943

Broken Japanese Cannon

Armstrong 8-Inch Cannon 1900

US Landing Craft on the Killer Reef

How to Get to Tarawa

Roving Foreign Correspondent on Tarawa in 1978

Second Marine Division WWII Patch

https://www.madhedgefundtrader.com/wp-content/uploads/2022/12/japanese-cannon-e1670867621973.jpg305450Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-12-12 10:02:252022-12-12 15:43:55The Market Outlook for the Week Ahead, or How Markets Work

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE GOOD MARKET AND THE BAD MARKET)

(TLT), (XOM), (OXY), (TSLA), (SPY), (BABA), (BIDU), (KBH), (PHM), (LEN), (AAPL)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-12-05 09:04:592022-12-05 13:01:09December 5, 2022

I usually write my Monday strategy letters in the middle of the night in my mind, from 2:00 AM to 3:00 AM, because my feet are too hot, too cold, or because my hip hurts. Then I go back to sleep. If I remember half of it the next morning, then I get a great letter.

I often like to refer to old proven market nostrums and show how true they really are. One of my favorites is the concept of the “good” market and the “bad” market.

The good market is the one for bonds. Vastly more research goes into bonds than stocks because that’s where the respectable, safe, widows and orphan money goes. Global bond markets are also far bigger, worth about $120 trillion. Bond traders usually began their journey at Harvard or Wharton, speak with clipped upper-class accents, and belong to exclusive private clubs that would never let you in for lunch, even with an invitation from a member.

Suffice it to say that the bond market is always right. Their relaxed lifestyle can be explained by the fact that they really only have two variables to look at, Fed policy and the actual supply and demand for money. Working in the bond market is almost like a sinecure, sending you a paycheck every month because you are entitled to it.

The stock market is the complete opposite.

While the bond market was polishing the teacher’s apple at the head of the class, the stock market was smoking cigarettes in the bathroom, endlessly catching detention. The stock market is also smaller, worth about $50 trillion. While bond traders are attending their Rotary meetings, stock traders binge drink and tear up the roads with their new Porsches and Ferraris.

Needless to say, stock traders are always wrong.

That’s because they face a hopeless dilemma. While bond traders have to contemplate only two variables, stock traders have to deal with millions. They have to cope with the hundreds of input variables per company that affect their earnings, and there are over 3,000 companies that trade in the US alone.

To illustrate the point, look at the recent market action.

Both markets have been driven by the same massive liquidity created by the government since 2009. The bond market peaked in August 2020 when it saw the free lunch of ultra-low interest rates soon ending. Stocks didn’t peak until January 2021, some 17 months later. It’s clear that stock traders suffer from a severe learning disorder.

And they’re doing it again.

After a 49% swan dive over two years plus, bonds bottomed on October 14. Stocks may not finally bottom until the spring, six months after bonds. Bonds are now betting that the recession has already begun, we just haven’t seen it in the data yet. Stocks are betting that the recession doesn’t start until 2023, if at all. That’s why it’s been going up.

As for me, I have traded both stocks AND bonds. That’s because before there were stocks, there were bonds as the only thing to trade. As you may recall, stocks were moribund in the 1970s. On top of that, you can add foreign exchange, precious metals, commodities, and volatility. There essentially isn’t anything I haven’t traded.

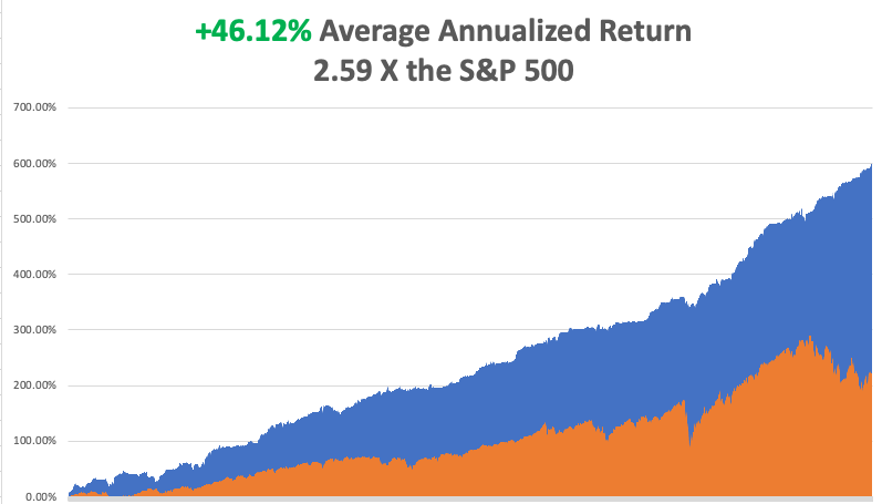

My performance in December has so far tacked on another robust +3.37%. My 2022 year-to-date performance ballooned to +87.05%, a spectacular new high. The S&P 500 (SPY) is down -13.61% so far in 2022.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +104.88%.

That brings my 14-year total return to +599.61%, some 2.60 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +46.12%, easily the highest in the industry.

I took profits in my triple weighting in bonds last week (TLT), booking some serious profits. All my remaining positions are profitable, shorts in (XOM), (OXY), (TSLA), (SPY), and one long in (TSLA), with 50% cash for a 30% net short position. We’ve just had a great run and the time to pay the piper is fast approaching.

With an +87.05% profit in hand this year, I don’t get a lot of complaints. However, I have been getting some lately because my trade alerts can be hard to get into.

Of course, it can be challenging to execute when 6,000 subscribers are trying to get into the same position at the same time. But when the entire world joins in, that raises the difficulty to a whole new level.

That is what happened with my trade alert to BUY the (TLT) on November 18. It was the trade alert around the world and the next day, bonds rocketed by $3.50. I laddered in with more positions with higher strike prices getting to a triple long in the bond market. When your trade alerts have a 95% success rate, that is what happens. It is the price of being right, which is better than the alternative.

When I first entered this trade, I thought the ten-year US Treasury yield would plunge from 4.46% to 2.50% by June 2023, taking the (TLT) from $91 to $120.

With the (TLT) at $108 on Friday and the ten-year yield at 3.50%, we are already halfway there. If I AM right and bond yields drop to 2.50%, the 30-year fixed mortgage rate will also drop below 4.00% and you can forget about any real estate crash. That's why the homebuilders (LEN), (KBH), and (PHM) are up 30%-40% since October.

With the ballistic moves in some Chinese stocks over the last two weeks (Alibaba (BABA) up 58%, Baidu ((BIDU) adding 47%, I have received a surge in inquiries about the prospects of the US going to war with the Middle Kingdom.

I have been asked this question continuously for the last 50 years, by several Presidents of the United States on down, and my answer is always the same.

There is not a chance.

The reason is very simple. The Chinese can’t feed themselves. They have not been able to do so for 100 years. With a population of 1.2 billion, the Chinese will never be able to feed themselves.

That means the Chinese are highly dependent on international trade to finance their food imports. When trade is vibrant, China prospers.

When it doesn’t, they start stacking up the bodies like cordwood for mass cremation, as happened when China suffered its last major famine. I know because I was there in the 1970s, and I’ll never forget that smell. As you quickly learn during a famine, there is no substitute for food.

So, what are the chances of China bombing their food supply? I’d say zero. A disruption of even a few months and people start to go hungry. Will they bluff, bluster, and obfuscate for domestic consumption? Every day of the year and that is what they are doing now.

As for buying Chinese stocks, I think I’ll pass for now. There are just too many great American ones on sale. The Chinese moves above are only taking place after horrific declines, 78% for (BABA), and 81% for (BIDU).

And before I go on to the data points, I want to recall a funny story.

One day in London 40 years ago, one of my junior traders at Morgan Stanley walked in with a big smile on his face. He had just gotten a great deal on a Ferrari Testarossa, which then retailed at $360,000, a lot of money for a 25-year-old East Ender in those days.

I thought to myself, “There are no great deals on Ferraris.”

A few months later, he totaled the Ferrari after a late night of binge drinking and racing on London’s damp streets, breaking the vehicle cleanly in half. The insurance company determined that his car was in fact two different Ferraris with two different VIN numbers that had been welded together. The car had split apart at the welds.

Some clever entrepreneur took the intact front end of a rear-ended car and the pristine back half of a car with destroyed hood and made one whole good Ferrari. Since my trader had only insured one car and not two, the insurance company refused to honor the claim.

All I can say is “Beware of friends bearing false Ferraris.”

Nonfarm Payroll Report Comes in Hot in November at 263,000, socking markets for 500 points. A December rate hike of 75 basis points has been firmly put back on the table. The Headline Unemployment Rate stays at a near-record high 3.7%. Average Hourly Earnings were up an inflationary 0.6%. Wages are up 5.1% YOY. The dollar soared on the prospect of higher rates for longer.

JOLTS Job Openings Report Comes in Weaker at 10.33 million in October, down 353,000 from September. High interest rates are finally taking their toll. There are still 1.7 job openings per applicant.

Key Inflation Read Drops, the Personal Consumption Expenditures Price Index falling 0.2% in October, excluding food and energy. It sets up a weak CPI on December 13, which would be very stock market positive.

Powell Turns Dovish, well, sort of, indicating that smaller interest rate hikes could start in December. The comments were made at a Brookings Institution meeting on Wednesday. Stocks rallied big on the news.

US to Ease Venezuela Sanctions, allowing Chevron to resume pumping there for six months after a three-year hiatus. It’s an out-of-the-blue big negative for oil prices. Venezuelan oil production has plunged from 2.1 million barrels a day to only 679, 000 thanks to gross mismanagement of the economy. But beggars can’t be choosers on the energy front. Good thing I’m running a double short in the sector. It’s the last think OPEC plus wanted to hear.

Don’t Expect a Housing Crash, as the financial system was vastly stronger than it was in 2008. A mild recession is already priced in, and bank balance sheets are rock solid. Buy the homebuilders on the next dips now coming off from horrific earnings, (KBH), (PHM), and (LEN).

Don’t Expect an iPhone 14 for Christmas, as pandemic-driven production shutdowns and Foxconn riots in China crimp supplies. It could be a longer wait if you want the new deep purple color. Avoid (AAPL) for now. I expect another big tech dive in 2023.

China Riots Tank Market, raising the specter of extended supply chain problems, especially for Apple (AAPL). Oil was especially hard hit as China is its largest buyer, hitting a two-year low and giving up all 2022 gains. China seems to be sacrificing its older generation, not giving them priority for vaccinations which don’t work anyway. This isn’t going away in a day. Transition to India will take a decade.

Case Shiller Plunges, the National Home Price Index Taking a 1.2% hit in September to 10.6%. Miami, Tampa, and Charlotte, NC showed the biggest YOY increases. You know the reasons why.

Home Rentals to Stay Sticky at Record Levels, with gains at 25-35% over the past 24 months. Homebuyers frozen out of the market by record-high interest rates are forced to rent at any price.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With the economy decarbonizing and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, December 5 at 8:00 AM EST, the ISM Nonmanufacturing PMI for November is out.

On Tuesday, December 6 at 8:30 AM, the Mad Hedge Traders & Investors Summit begins. Click hereto register.

On Wednesday, December 7 at 7:30 AM, the Crude Oil Stocks are announced. It’s pearly Harbor Day.

On Thursday, December 8 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Producer Price Index for November.

On Friday, December 9 at 8:30 AM, the Producer Price Index for November. At 2:00, the Baker Hughes Oil Rig Count is out.

As for me, I am sitting here in front of the fire at my place in the Berkeley Hills and it is freezing cold and pouring rain outside. Heaven knows we need it.

I’m going to San Francisco later today to do some Christmas shopping. It’s not the ideal time but in my hopelessly busy schedule, this was the only day this year allocated for this chore.

For some reason, last night I recalled my days as an Ivy League Princeton professor, which I hadn’t thought about for decades.

When Morgan Stanley was a private partnership, before it went public in 1987, the firm represented the cream of the US establishment. There wasn’t anyone in business, industry, or politics you couldn’t reach through one of the company’s endless contacts. We referred to it as the “golden Rolodex.”

One day in the early 1980s, a managing director asked me a favor. Since he had landed me my job there, I couldn’t exactly say no. He had committed to teaching a graduate night class in International Economics at his alma mater, Princeton University, but a scheduling conflict had prevented him from doing so.

Since I was then the only Asian expert in the firm, could I take it over for him? If I had extra time to kill, I could always spend it in the Faculty Club.

I said “sure.”

So, the following Wednesday found me at Penn Station boarding a train for the leafy suburb about an hour away. On the way down, I passed the locations of several Revolutionary War battles. When we pulled into Princeton, I realized why they called these places “piles”. The gray stone ivy-covered structures looked like they had been there a thousand years.

My students were whip-smart, spoke several Asian languages, and asked a ton of questions. Many came from the elite families who owned and ran Asia. I understood why my boss took the gig.

I turned out to be pretty popular at the faculty Club, with several profs angling for jobs at Morgan Stanley. Rumors of the vast fortunes being made there had leaked out.

Princeton was weak in my field, DNA research. But as the last home of Albert Einstein, it was famously strong in math and physics. Many of the older guys had worked with the famed Berkeley professor, Robert Oppenheimer, on the Manhattan Project.

I was still a mathematician of some note those days, so someone asked me if I’d like to meet John Nash, the inventor of Game Theory, which won him a Nobel Prize in Economics in 1994. Nash’s work on partial differential equations became the basis for modern cryptography. I was then working on a model using Game Theory to predict the future of stock markets. It still works today and is the basis the Mad Hedge Market Timing Algorithm.

Weeks later found me driven to a remote converted farmhouse in the New Jersey countryside. On the way, I was warned that Nash was a bit “odd,” occasionally heard voices speaking to him, and rarely came to the university.

I later learned that his work in cryptography had driven him insane, given all the paranoia of the 1950s. Having worked in that area myself, that was easy to understand. His friends hoped that by arguing against his core theories, he would engage.

When I was introduced to him over a cup of tea, he just sat there passively. I realized that I was going to have to take the initiative so as a stock market participant, I immediately started attacking Game Theory. That woke him up and started the wheels spinning. It hadn’t occurred to him that game theory could be used to forecast stock prices.

His friends were thrilled.

I later went on to meet many Nobel Prize winners, as the Nobel Foundation was an early investor in my hedge fund. Whenever a member of the Swedish royal family comes to California, I get an invitation to lunch for the Golden State’s living Nobel laureates. It turns out that 20% of all the Nobel Prizes awarded since its inception live here. Last time, I sat next to Milton Friedman, and I argued against HIS theories.

The other thing I remembered about my Princeton days is my discovery of the “professor's dilemma.” Sometimes a drop-dead gorgeous grad student would offer to go home with me after class. I was happily married in those days with two kids on the way, so I respectfully declined, despite my low sales resistance.

No away games for me.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

The Nobel Prize

https://www.madhedgefundtrader.com/wp-content/uploads/2022/12/nobel-prize-e1670258573258.png393400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-12-05 09:02:492022-12-05 13:01:21The Market Outlook for the Week Ahead, or the Good Market and the Bad Market

Below please find subscribers’ Q&A for the November 30 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: You keep mentioning December 13th as a date of some significance. Is this just because the number 13 is unlucky?

A: December 13th at 8:30 AM EST is when we get the next inflation report, and we could well get another 1% drop. Prices are slowing down absolutely across the board except for rent, which is still going up. Gasoline has come down substantially since the election (big surprise), which is a big help, and that could ignite the next leg up in the bull market for this year. So, that is why December 13 is important. And we could well flatline, do nothing, and take profits on all our positions before that happens, because whatever it is you will get a big move one way or another (and maybe both) on December 13.

Q: I’m a new subscriber, and I am intrigued by your structuring of options spreads. Why do you do debit spreads instead of credit spreads?

A: It’s really six of one and a half dozen of the other—the net profit is pretty much the same for either one. However, debit spreads are easier to understand than credit spreads. We have a lot of beginners coming into this service as well as a lot of seasoned old pros. And it’s easier to understand the concept of buying something and watching it go up than shorting something and watching it go down. Now, doing the credit spreads—shorting the put spread—gives you a slight advantage in that it creates cash which you can then use to meet margin requirements. However, it’s only a small amount of cash—only the potential profit in that position. And guess what? All the big hedge funds actually kind of like easy-to-understand trade alerts also, so that’s why we do them.

Q: I have a lot of exposure in NVIDIA (NVDA), so is it worth trading out of it and coming back in at a lower rate?

A: NVIDIA is one of the single most volatile stocks in the market—it’s just come up 50%. But it could well test the lower limits again because it is so volatile, and the chip industry itself is the most volatile business in the S&P 500. If your view is short-term, I would take profits now, and look to go back in next time we hit a low. If you’re long-term, don’t touch it, because NVIDIA will triple from here over the next 3 years. I should caution you that if you do try the short-term strategy, most people miss the bottom and end up paying more to get back into the stock; and that's the problem with all these highly volatility stocks like Tesla (TSLA), NVIDIA (NVDA) and Advanced Micro Devices (AMD) unless you’re a professional and you sit in front of a screen all day long.

Q: Would you buy now and step in to make it long-term?

A: I think we get a couple more runs at the lows myself. We won’t get to the old lows, but we may get close. Those are your big buying points for your favorite stocks and also for LEAPS. And I’m going to hold back on new LEAPS recommendations—we’ve done 12 in the last two months for the Concierge members, and maybe half of those went out to Global Trading Dispatch before they took off again. So, that would be my approach there.

Q: How much farther can the Fed raise interest rates until they reverse?

A: 1%-2%, unless they get taken over by the data—unless suddenly the economy starts to weaken so much that they panic and reverse like crazy. I think that's actually what’s going to happen, which is why we went hyper-aggressive in October on the long side, especially in bonds (TLT). You drop rates on the ten-year from 4.5% to 2.5% in six months—that’s an enormous move in the bond market. That is well worth running a triple long position in it; I think that’s what's going to happen. That’s where we will make out the first 30% in 2023.

Q: Should I short the cruise lines here, like Royal Caribbean (RCL)?

A: They do have their problems—they have massive debts they ran up to survive the pandemic when all the ships were mothballed, so it is an industry with its major issues. The stock has already doubled since the summer so I wouldn’t chase it up here. I’m not rushing to short anything here right now though unless it’s really liquid or has horrendous fundamentals like the oil industry, which everyone seems to love but I hate—right now the haters are winning for the short term, until December 16, which is all I care about.

Q: Is the diesel shortage going to affect farmers and all other industries like the chip?

A: As the economy slows down, you can expect shortages of everything to disappear, as well as all supply chain issues, which is a positive for the economy for the long term.

Q: What about the 2024 iShares 20 Plus Year Treasury Bond ETF (TLT) 95—is that not a trade?

A: That’s a one-year position with a 100% potential profit. That is worth running to expiration unless we get a huge 20-point move up in the next 3 months, which is possible, and then there won’t be anything left in the trade—you’ll have 95% of the profit in hand at which point you’ll want to sell it. So, with these one-year LEAPS or two-year LEAPS, run them one or two years unless the underlying suddenly goes up a lot, and then grab the money and run; that's what I always tell people to do. Because if you sell your position, they can’t take the money away from you with a market correction.

Q: Is the current US economy the best economy in the world?

A: It is. If you look at any other place in the world, it’s hard to find an economy that's in better shape, and it’s because we have the best management in the world and hyper-accelerating technology which everyone else begs and borrows. Or steals. People who are predicting zero return on stocks for 10 years are out of their minds. You don’t short the best economy in the world. If anything, technology is accelerating, and that will take the stock market with it in the next year or so.

Q: Do you see the Dow ($INDU) outperforming the other indexes until the Fed positive pivots?

A: Absolutely yes, because the S&P 500 (SPY) has a very heavy technology weighting and technology absolutely sucks right now. That would probably be a good 3-month trade—buy the Dow, and short the S&P 500 in equal amounts. Easy to do—you might pick up 10% on a market-neutral trade like that.

Q: Do you see a Christmas rally this year?

A: Actually, I do, but it won’t start until we get the next inflation report on December 13, at which point I'm going 100% cash. I’ve made enough money this year, and this is a problem I had when I ran my hedge fund: when you make too much money, nobody believes it, so there's really no point in making more than 50% or 60% a year because people think it’s fake. This is true in the newsletter business as well. Markets also have a nasty habit of completely reversing in January; this year, we had one up day in January, and then it was bombs away and we just piled on the shorts like crazy, so you have to wait for the market to first give you the fake move for the year, and then the real one after that. The best way to take advantage of that is to be 100% cash, and that’s why I usually do.

Q: What indicators do you see that give you the most confidence that inflation has peaked?

A: There's one big one, and that’s real estate. Real estate is absolutely in a recession right now and has the heaviest weighting of any individual industry in the inflation calculation. If anybody thinks house prices are going up, please send me an email and tell me where, because I’d love to know. The general feeling is they’re down 10-15% over the last six months. New homes are only being sold with massive buydowns in interest rates and free giveaways on upgrades. It is an industry that is essentially shut down, with interest rates having gone from 2.75% to 7.5% in a year, so there’s your deflation, but unfortunately, real estate is also the slowest to price in in the Fed’s inflation calculation, so we have to go through six months of torture until the Fed finally sees proof that inflation is falling. So, welcome to the stock market because it's just one of those factors. Just for fun, I got a quote on financing an investment property. The monthly payment would have been double for half the house that I already have.

Q: Are LEAPS a buy with the CBOE Volatility Index (VIX) this low?

A: No, you want to look at stocks first, and then the VIX; and with all the stocks sitting on top of 30-50% rises, it’s a horrible place to do LEAPS. LEAPS were an October play—we bought the bottom in a dozen LEAPS in October, and those were great trades, except for Tesla (TSLA) and Rivian (RIVN) which still have two years left to run. Up here, you’re basically waiting on a big selloff before you go into these one to two-year options positions.

Q: Why does Biden keep extending student loans? Will this catch up at some point?

A: He’s going to take it to the Supreme Court, and if he loses at the Supreme Court, which is likely, then he’ll probably give up on any loan extensions. At this point, the loan extensions on student loans are something like 2 or 2.5 years. The reason he’s doing this is to get 26 million people back into the economy. As long as you have giant student loan balances, you can’t get credit, you can’t get a credit card, you can’t buy a house, you can’t get a home loan. Bringing that many new people into the economy is a huge positive for not only them but for everyone else because it strengthens the economy. That has always been the logic behind forgiving student loans—and by the way, the United States is virtually the only country in the world that makes students pay back their loans after 30 or 40 years. The rest give college educations away either for free or give some interest-free break on repayments until they can get a salary-paying job.

Q: Does the budget deficit drop impact the stock market?

A: Yes, but it impacts the bond market first and in a much bigger way. That’s one of the reasons that bonds have rallied $13 points in six weeks because less government borrowing means lower interest rates—it’s just a matter of supply and demand. This has been the fastest deficit reduction since WWII, and markets will discount that.

Q: Will the US dollar (UUP) crash?

A: Yes, it will. You get rid of those high interest rates and all of a sudden nobody wants to own the US dollar, so we have great trades setting up here against everything, except maybe the Yuan where the lockdowns are a major drag.

Q: Is silver (SLV) a buy now?

A: No, it’s just had a big 10% move; I would wait for any kind of dip in silver and gold (GOLD) before you go into those trades. And when/if you do, there are better ways to do it.

Q: How is the Ukraine war going?

A: It’ll be over next year after Ukraine retakes Crimea, which they’ve already started to do. Russia is running out of ammunition, and so are we, by the way. However, the United States, as everybody learned in WWII, has an almost infinite ability to ramp up weapons production, whereas Russia does not. Russia is literally using up leftover ammunition from WWII, and when that’s gone, they’ve got nothing left, nor the ability to produce it in any sizable way. All good reasons to sell short oil companies ahead of a tsunami of Russian oil hitting the market. By the way, oil is now down for 2022.

Q: What's the number one short in oil (USO)?

A: The most expensive one, that would be Exxon Mobile (XOM).

Q: What’s going to happen to the markets in January?

A: After this Christmas rally peters out, I’m looking for profit-taking in January.

Q: When is a good time to buy debit spreads on oil?

A: Now. Look at every short play you can find out there; I just don’t see a massive spike up in oil prices ahead of a recession. And by the way, if the war in Ukraine ends and Russian oil comes back on the market, then you’re looking at oil easily below $50.

Q: What is the best way to invest in iShares Silver Trust (SLV) in the long term?

A: A two-year LEAP on the Silver (SLV) $25-$26 call spread—that gets you a 100%-200% return on that.

Q: Is lithium a good commodity trade?

A: Lithium will move in sync with the EV industry, which seems to have its own cycle of being popular and unpopular. We’re definitely in the unpopular phase right now. Long term demand for lithium will be increasing on literally hundreds of different fronts, so I would say yes, lithium is kind of the new copper. Look at Albemarle (ALB), Societe Chemica Y Minera de Chile (SQM), and FMC Corp. (FMC).

Q: If we do a LEAPS on Crown Castle Incorporated (CCI), you won’t get the dividend right?

A: No, you won’t, it’s a dividend-neutral trade because you’re long and short in a LEAPS. You have to buy the stock outright and become a registered shareholder to earn the dividend which, these days, is a hefty 4.50%. That said, if you’re looking for a high dividend stock-only play, buying the (CCI) down here is actually a great idea. For the stock-only players, this would be a really good one right now.

Q: Do you know people who are selling because of large capital gains?

A: The only people I know who are selling have giant tax bills to pay because of all the money they made trading options this year. I happen to know several thousand of those, as it turns out. So yes, I do know and that could affect the market in the next couple of weeks, which is why I went with the flatlined scenario for the next two weeks. Most tax-driven selling will be finished in the next two weeks, and after that, it kind of clears the decks for the markets to close on a high note at the end of the year.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING or DISPATCH TECHNOLOGY LETTER as the case may be, then click on WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2022/12/john-thomas-TA-418.jpg600864Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-12-02 13:02:582022-12-02 14:01:23November 30 Biweekly Strategy Webinar Q&A

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or LOOKING FOR BIG FOOT),

(NVDA), (VIX), (TLT), (TSLA), (XOM),

(OXY), (TSLA), (SPY), (MA), (V), (AXP)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-11-28 09:04:262022-11-28 13:56:10November 28, 2022

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.