Global Market Comments

November 18, 2022

Fiat Lux

Featured Trade:

(NOVEMBER 16 BIWEEKLY STRATEGY WEBINAR Q&A),

(TSLA), (JNK), (HYG) or (TLT), (UUP), (FXE), (FXC), (FXA), (ALB), (FCX), (PYPL), (FXI), (GLD), (CCJ), (BHP), (RCL)

Global Market Comments

November 18, 2022

Fiat Lux

Featured Trade:

(NOVEMBER 16 BIWEEKLY STRATEGY WEBINAR Q&A),

(TSLA), (JNK), (HYG) or (TLT), (UUP), (FXE), (FXC), (FXA), (ALB), (FCX), (PYPL), (FXI), (GLD), (CCJ), (BHP), (RCL)

Below please find subscribers’ Q&A for the November 16 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: What do you see Tesla (TSLA) moving to from here until next year?

A: Not much; I mean if you’re lucky, Tesla won’t move at all. The problem is Twitter is looking like a disaster of huge proportions—firing half the staff on day one? Never good for building a business. Tesla has also been tied to the rest of big tech, which has been in awful condition and may not see a continuous move upward until the Fed actually starts lowering interest rates in the second quarter of next year. Tesla could be dead money here for a while; eventually, a company growing at 50% a year will go up—especially when it’s just had a 50% decline in the share price. As to when that is, I don’t know, and asking me 15 more times will get you just the same answer.

Q: Should we start piling into iShares 20 Plus Year Treasury Bond ETF (TLT) longs now or wait?

A: You go now. Every day you waited meant paying one point more in TLT. I think the bottom is in; we have a 20-30 point move ahead of us. Everybody in the world is now trying to get into this trade, just like I spent all this year trying to get out of it. And if anything, November CPI could be a long term-term top in inflation, especially if we came in with another cold number. So, I would start scaling in now, even though we’re over $100 in the (TLT) today and I first recommended this around $95.

Q: If the Fed keeps raising interest rates, will the US Treasury market fall?

A: Probably not because the Fed only has control of overnight interest rates—the discount rate, the interbank rate—whereas the (TLT) is a 10-to-20-year maturity bond. No matter what short term rates do, the inversion will just keep getting bigger, but in fact, the bond market itself was yielding 4.46%, yielding 8% with junk, has bottomed and will probably start going up from here. So that is the difference between the Fed and what the actual market does.

Q: Do you prefer Junk (JNK), (HYG), or (TLT)?

A: I always go for the highest risk. Junk has about an 8% yield here compared to 3.75% for the TLT. By the way, if you want to do one trade and go to sleep, buy the junk on 2 to 1 margin, get your 16% yield next year, and just take a one-year vacation. That’s what some people do.

Q: When you say the dollar is going to go down what do you mean?

A: I mean the US dollar, while Canadian (FXC) and Australian dollars (FXA) will go up.

Q: What is the best time to buy US dollars?

A: Maybe in five years, as it could go down for five or 10 years from here, now that it’s going to imminently give up its yield advantage.

Q: What's the forecast for casinos?

A: I think casinos do better. Las Vegas was absolutely packed, you couldn’t get into the best hotels—people are spending money like crazy.

Q: What’s the best way to play (TLT)?

A: With a one-year LEAP. I put out the $95/$100 last week for my concierge members. Here, you probably want to do the $100/$105; that’ll still give you a one-year return of 100%.

Q: How do you short the dollar?

A: There are loads of short dollar ETFs out there, or you can just sell short the Invesco DB US Dollar Index Bullish Fund (UUP), which is the dollar basket, or buy the (FXA) or (FXE).

Q: Freeport McMoRan (FCX) just went from 25 to 38; is it time to take a profit and re-enter at a lower point?

A: Short term yes, long term no. My long-term target for (FCX) is $100 because of the exponential growth of copper demand caused by EV production going from 1.5 million to 20 million a year in the next 10 years. Each EV needs 200 pounds of copper, so by 2030, annual copper demand for EVs only will be 20 billion pounds. In 2021, the total annual global copper production was 46.2 billion pounds. In order words, global copper production has to double in eight years just to accommodate EV growth only.

Q: Do you think there’ll be a rail worker strike?

A: I have no idea, but it will be a disaster if there is. There’s your recession scenario.

Q: What strike prices do you like for a Tesla LEAP?

A: Anything above here really. You could be cautious and do something like a $200/$210 two years out—that has a double in it. Or you could be more adventurous and go for a 400% return with like a $250/$260 in two years. I’m almost sure that we’ll have a major recovery in Tesla within two years.

Q: What’s your opinion on PayPal (PYPL) and Albemarle (ALB)?

A: I’m trying to stay away from the fintech area, partly because it’s tech and partly because the banks are recapturing a lot of the business they were losing to fintech a couple of years ago by moving into fintech themselves. That is the story and we’re clearly seeing that in the share prices of both banks and PayPal. I like Albemarle because the demand for lithium going forward is almost exponential.

Q: What’s your thought on the Australian dollar (AUD)?

A: Buy it with both hands as it is going to parity. Australia is a great indirect play on trade with China (FXI), gold (GLD), uranium (CCJ), and iron ore (BHP). It’s a great play on the recovery of the global economy, which will start next year.

Q: What do you think about Royal Caribbean Cruises Ltd (RCL)?

A: Probably a buy but remember all the cruise lines will be impaired to some extent by the massive debts they had to take on to survive two years of shutdown with the pandemic. I took the Queen Victoria last July on their Norwegian Fjord cruise, and it had not been operated for two years. None of the staff had any idea what to do. I had to show them.

Q: Will big tech have a good second half?

A: Probably, but it’s going to be a slow first quarter, and I think if we start getting actual cuts in interest rates, then it’s going to be off to the races for tech and they’ll all go to all-time highs as they always do.

Q: How come you haven’t issued any trade alerts yet on the currencies?

A: Calling a five-year turnaround is a big job. Now that we have the turnaround in play, we’re in dip-buying mode. So, you will see these in the future. But I also have to look at what currency trades are offering compared to other trades in other asset classes. And for the last year or two, the big opportunities have all been in stocks. You had volatility constantly visiting the mid $30s, you didn’t get that in the currencies, and more money was to be made in stock trades than foreign currency trades. That is changing now; let's see if we have a sustainable trend and if we get a good entry point. There’s a lot that goes into these trade alerts that you don’t always get to see. We only get a 95% success rate by being very careful in sending out trade alerts and that means long periods of doing nothing when the risk/reward is mediocre at best, which is right now. The services that guarantee you a trade alert every day all lose money.

Q: What is the recommended minimum portfolio size to amortize the cost of the concierge service?

A: I tell people to have a half a million in assets because we want people who are financially sophisticated to understand what we’re telling them. That said, we do have people with as little as 100,000 in the concierge service and they usually make the money back on the first trade. This is a very sophisticated high-return, very active service. You get my personal cell phone number and all that, plus your own dedicated website, and specific concierge-only research. It’s a much higher level of service. It’s by application only and we currently have no places available for new concierge members. However, if you’re interested, we can put you on the waitlist so that when another millionaire retires, we can open up a space.

Q: Despite recent moves, the algo looks bearish. There are lots of mixed signals.

A: Yes, it does. And yes, that’s often the case when the market timing index hangs around 50.

Q: Do concierges go for short term moves?

A: No, concierges are looking for the big, long-term trades that they can just buy and forget about. That is where the big money is made. At least 90% of the people that try day trading lose money but make all the brokers rich.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or Technology Letter, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

November 14, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE TOP FIVE TECHNOLOGY STOCKS OF 2023),

(RIVN), (ROM), (ARKK), (PANW), (CRM), (FXE), (FXY), (FXA), (LEN), (KBH), (DHI), (TLT), (UUP), (META), (TSLA), (BA), (JNK), (HYG), (BRKB), (USO)

The year 2022 has been driven by rising interest rates, a strong dollar, a weak economy, a bear market in stocks.

A massive reversal is about to take place. 2023 will gain the benefit of gale force macroeconomic tailwinds for the right stocks.

So far this year, Mad Hedge earned an astounding 77.20% profit cashing in on this year’s trends. We could earn the same return taking advantage of next year’s trends.

If you want to ride along on my coattails next year, that is fine with me. But it requires you to take a leap of faith.

I refer you to the motto of Britain’s Special Air Service: “Qui audet adipiscitur,” or “Who dares wins.”

For it only makes sense that the worst stocks of 2022 will be the best performers of 2023.

I have no doubt that tech stocks will bottom out sometime in 2023. Those who get in early will build some of the largest fortunes of this century. Those who miss the boat will spend their retirement years working at Taco Bell.

The reasons are very simple.

*Ultra-high interest rates will force a mild recession in early 2023. Then suddenly, inflation will plummet. We know this has already started because the largest element in the inflation calculation is housing costs, which are in free fall.

*The Fed will panic and deliver 2023 the sharpest DECLINE in interest rates in American history.

*Plunging interest rates will bring a crash in the US dollar.

*Foreign currencies like the Euro (FXE), the Japanese Yen (FXY), and the Australian dollar (FXA) will soar.

*And guess who gets the bulk of their earnings from abroad, sometimes up to two-thirds? The technology industry.

Kaching!

If you think I’m out of my mind, just look at the top performers of the historic stock market rally last week.

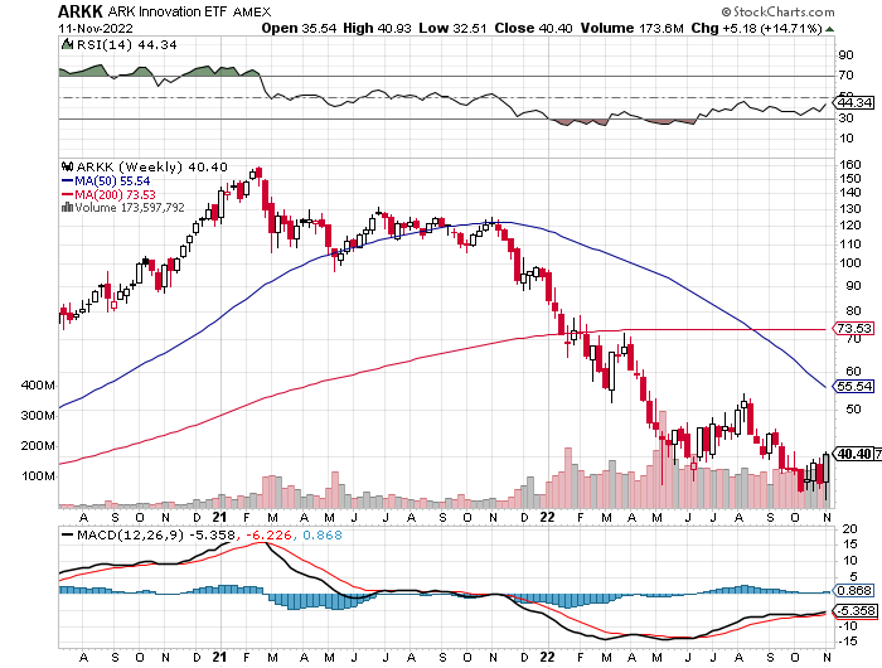

All the interest rate-sensitive sectors caught on fire. Technology stocks took off like a scalded cat, with Cathie Woods’ Ark Innovation Fund (ARKK) up an astounding 14% in a single day.

Bank shares soared. Homebuilders (LEN), (KBH), (DHI) caught a strong bid for the first time in ages. Junk bonds went bid only. US Treasury Bonds had their best day in 20 years (TLT), while the greenback (UUP) had its worst.

The bottom line here is so clear that I’ll write it on a wall for you. Falling interest rates will be the primary driver of stock prices for 2023 and 2024.

Of course, there is a better way to play this than buying the first technology index you stumble across.

So, let me boil this strategy down to just five names, close your eyes, and buy them.

Rivian (RIVN) – ($34) - Rivian is widely believed to be the next Tesla (TSLA). Some 25% owned by its largest customer, Amazon (AMZN), Rivian produces three types of EVs: the R1T pickup truck, the R1S SUV, and Amazon's EDV (electric delivery van). Its R1 vehicles start at under $70,000 and can travel more than 300 miles on a single charge. To learn more about Rivian, please click here.

To say that Rivian is the hot car of the day would be a vast understatement. New cars are trading for double list on the grey market. Owners complain of getting mobbed with gawkers whenever they hit the beach or the ski slopes. The buzz has led to an outstanding order book of an impressive 98,000, or four years of current production. The obvious cool factor allows enormous pricing power.

And here is the key to buying Rivian at this time. At 25,000, it is right at the mass production point where Tesla shares went ballistic all those years ago. And it already has an 80% decline in the price, in the rear-view mirror.

In 2024, Rivian plans to open its second plant in Georgia. After it fully expands its Illinois plant, it expects its annual production capacity to reach 600,000 vehicles.

Inflation Reduction Act passed this summer greatly accelerated rollout of the entire EV industry, which created a $7,500 per vehicle tax credit on top of state benefits.

Yes, this company offers venture capital-type risks. But it offers venture capital-type returns as well, up 10X-50X from here.

Ark Innovation Fund (ARKK) – ($40) – Cathie Woods’ high-tech fund was the proverbial red-headed stepchild of this bear market. It fell a gut-punching 80% from the 2021 top until last week. Just to get back to its old high, likely over the next five years, it has to rise by 400%. Its largest holdings are a real rollcall of the severely abused, Tesla (TSLA), Roku (ROKU), Exact Sciences (EXAS), Intellia (INTL), and Teladoc Health (TDOC), which Woods actively trades. But they are also a valuable insight into the future, EVs, CRISPR technology, robotic surgery, and molecular diagnostics. To learn more about the Ark Innovation Fund, please click here.

ProShares Ultra Technology ETF (ROM) – ($27) – This is a 2X long technology ETF that gives you an extremely aggressive position across the tech sector. It has 19% of its holdings in Apple (AAPL), 16% in Microsoft (MSFT), 10% in Alphabet (GOOGL) and Google (GOOG), at 3.5% in NVIDIA (NVDA), and 120 other smaller names. (ROM) shares are down a breathtaking 67% just in the past year. To learn more about the (ROM), please click here.

Palo Alto Networks (PANW) - $165 – Hacking is one of the fastest-growing sectors in technology, it is recession-proof and immune to the economic cycle. As a result, spending on the defense against hacking is absolutely exploding. Palo Alto Networks, Inc. is an American multinational cybersecurity company with headquarters in Santa Clara, California. Its core products are a platform that includes advanced firewalls and cloud-based offerings that extend those firewalls to cover other aspects of security. I have already earned a tenfold return over the past decade and expect to make another 10X in the coming years. You won’t find any dips in this stock as too many people are trying to get into it. To learn more about the Palo Alto Networks, please click here.

Salesforce (CRM) - $157 – The baby of tech genius Mark Benioff, this company is the dominant player in customer relationship management. If you want to do any business in the cloud, and almost all big companies do, you are up to your eyeballs in customer relationship management. Salesforce is the largest San Francisco-based cloud-oriented software company with virtually all of the Fortune 500 as its customer list. It provides customer relationship management software and applications focused on sales, customer service, marketing automation, analytics, and application development. Salesforce shares have been the target of a haymaker, down 55% in a year. To learn more about Salesforce, please click here.

You know what? I can do better than this.

I can create customized options LEAPS for you that will deliver a tenfold return on whatever performance these ultra-high beta stocks deliver. If the shares of one of my picks rise by 100%, you will make 1,000%.

This is an investment strategy that will enable you to retire early, real early. Tired of punching a time clock or logging into the next Zoom meeting on time?

Those will become a distant memory if you pursue my Mad Hedge Investment strategy for 2023.

As a result, my November month-to-date performance went off to the races, already achieving a hot +2.20%.

That leaves me with a very rare 100% cash position. With midterm election results out on Wednesday and the next report on the Consumer Price Index on Thursday, that sounds like a prudent place to be.

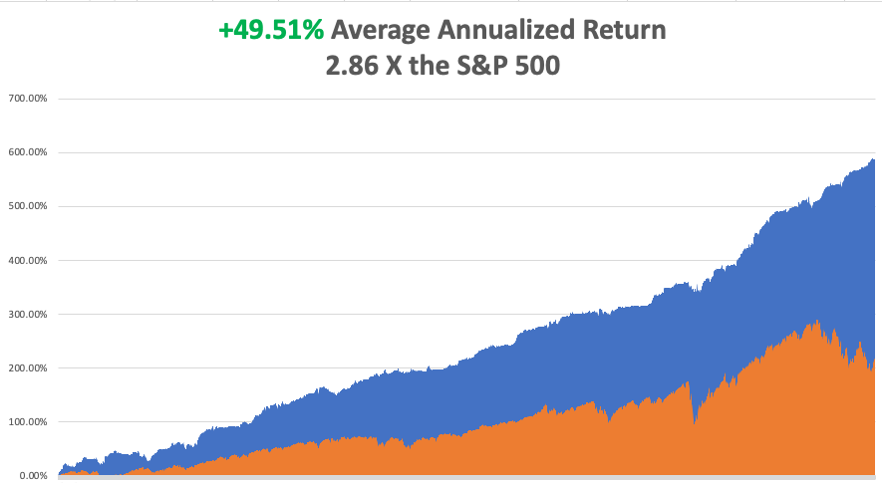

My 2022 year-to-date performance ballooned to +77.57%, a new high. The Dow Average is down -11.85% so far in 2022.

It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high +75.53%.

That brings my 14-year total return to +590.13%, some 2.86 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to +49.51%, easily the highest in the industry.

Bonds Clock Best Day in Years, taking the ten-year US Treasury bond fund up $3.64. All low interest rate plays had monster days. Junk bond ETFs (JNK) and (HYG) were up two points. 30-year fixed rate mortgages dropped 60 basis points to 6.60%, the biggest drop in history. Long bonds will be THE big trade of 2023.

US Dollar has Worst Day in 20 Years, driven by plunging interest rates. Big tech, which gets a major share from overseas sales, rocketed. Apple alone was up $12. Cathy Wood’s Ark Innovation Fund (ARKK) was up an incredible 14%. It vindicates my view that tech will turn when interest rates and the dollar fall.

Oil Companies (USO) Book Record $200 Million Profit this year, using the Ukraine War to double your cost of gasoline. If we have a recession next year, or the war ends, energy share prices should be peaking around here. Even if they don’t, the risk-reward here is terrible. It means we will have to pay a much higher price to decarbonize the economy at a later date.

Wells Fargo Gets Hit with $1 Billion Fine for its many regulatory transgressions over the last decade. Looting of customer accounts with bogus fees has been a recurring problem. Use any selloffs to buy (WFC) on dips.

Berkshire Hathaway's 20% Profit Increase YOY and buys back another $1 billion worth of stock. However, they did take a $10 billion loss on stocks in Q3 during the market meltdown. Keep buying (BRKB) stock and LEAPS on dips.

$1.5 trillion in Homeowners Equity Lost Since May, thanks to interest rates at 20-year high and a shrinking money supply. Since July, the median home price has dropped by $11,560. The average borrower has lost $30,000 in equity. It’s not a great time to rent either as prices there are soaring. Residential housing could remain weak for another 12-24 months, compared to the six-year drawdown we had from 2006.

Boeing Orders Rise in October, but deliveries fall. The company is finally out of the penalty box, up 40% since October 1. Don’t buy (BA) up here.

The Red Wave Fails to Show, with control of congress still too close to call. Republican House control has shrunk from an expected 60 seats six months ago to maybe two today. Donald Trump threw the election for his party, picking unelectable extremist candidates and campaigning where he wasn’t wanted. A pro-life Supreme Court brought out millions of women voters across the country. If the Republicans can’t win with inflation at 8.7%, they are toast in 2024 when it drops back down to 2%.

Market Dives 646 Points on Democratic Win, with technology stocks taking the biggest hit. The red wave no-show was a black swan traders were not looking for. Energy was the worst performing sector because they aren’t getting the air cover they paid for with a red wave. The result was much as I expected, which is why I went into November 8 with a rare 100% cash position waiting to buy the next low. It turns out that rights are more important than prices.

Elon Musk Sells More Tesla Shares and Warns of a Twitter Bankruptcy, some $3.9 billion worth, bringing this year’s total to $36 billion. Musk is raising money to head off a bankruptcy of Twitter now that major advertisers are fleeing en masse. This certainly is a distress sale. If Musk was looking to build a real business, re-tweeting fringe conspiracy theories was the worst thing he could have done. Endorsing the Republican party will cost him half of his customers. Is this Musk’s Waterloo, or his Dien Bien Phu?

Facebook to Lay Off 11,000, about 13% of its total employees. Zuckerberg admits the error of pushing the company into the metaverse too far too fast. With the stock down 77%, there are not a lot of happy campers at One Hacker Way. Avoid (META) for now, but it may be a 2023 play when we get closer to a new final product.

FTX Becomes an Epic Bankruptcy, with $9.5 billion missing from its balance sheet, in one of the biggest blowups of the crypto age. Losses are expected to reach $50-$60 billion, with the bankruptcy of 130 affiliated companies. It is also a potential Dept of Justice target. All affiliated tokens and coins have gone to zero. So, placing your money with a fresh-faced kid in the Bahamas wearing baggy shorts and with no financial background was not such a great idea after all. It’s amazing how many serious people were sucked in on this one. At least Sam Bankman-Fried said he was sorry.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With the economy decarbonizing and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side will be far more efficient and profitable than the old. Dow 240,000 here we come!

On Monday, November 14 at 8:00 AM, the Consumer Inflation Expectations for October are released.

On Tuesday, November 15 at 8:30 AM, the Producer Price Index for October is released.

On Wednesday, November 16 at 8:30 AM, Retail Sales for October are published.

On Thursday, November 17 at 8:30 AM, Weekly Jobless Claims are announced. Housing Starts and Permits for October are also out.

On Friday, November 18 at 10:00 AM, the Housing Starts for October are printed. At 2:00 the Baker Hughes Oil Rig Count is out.

As for me, I am often told that I am the most interesting man people ever met, sometimes daily. I had the good fortune to know someone far more interesting than myself.

When I was 14, I decided to start earning merit badges if I was ever going to become an Eagle Scout. I decided to start with an easy one, Reading Merit Badge, where you only had to read four books and write one review.

I was directed to Kent Cullers, a high school kid who had been blind since birth. During the late 1940s, the medical community thought it would be a great idea to give newborns pure oxygen. It was months before it was discovered that the procedure caused the clouding of corneas and total blindness. Kent was one of these kids.

It turned out that everyone in the troop already had Reading Merit Badge and that Kent had exhausted our supply of readers. Fresh meat was needed.

So, I rode my bicycle over to Kent’s house and started reading. It was all science fiction. America’s Space Program had ignited a science fiction boom and writers like Isaac Asimov, Jules Verne, Arthur C. Clark, and H.G. Welles were in huge demand. Star Trek came out the following year, in 1966. That was the year I became an Eagle Scout.

It only took a week for me to blow through the first four books. In the end, I read hundreds to Kent. Kent didn’t just listen to me read. He explained the implications of what I was reading (got to watch out for those non-carbon-based life forms).

Having listened to thousands of books on the subject, Kent gave me a first class education and I credit him with moving me towards a career in science. Kent is also the reason why I got an 800 SAT score in math.

When we got tired of reading, we played around with Kent’s radio. His dad was a physicist and had bought him a state-of-the-art high-powered short-wave radio. I always found Kent’s house from the 50-foot-tall radio antenna.

That led to another merit badge, one for Radio, where I had to transmit in Morse Code at five words a minute. Kent could do 50. On the badge below the Morse Code says “BSA.” In those days, when you made a new contact, you traded addresses and sent each other postcards.

Kent had postcards with colorful call signs from more than 100 countries plastered all over his wall. One of our regular correspondents was the president of the Palo Alto High School Radio Club, Steve Wozniak, who later went on to co-found Apple (AAPL) with Steve Jobs.

It was a sad day in 1999 when the US Navy retired Morse Code and replaced it with satellites. However, it is still used as beacon identifiers at US airfields.

Kent’s great ambition was to become an astronomer. I asked how he would become an astronomer when he couldn’t see anything. He responded that Galileo, the inventor of the telescope, was blind in his later years.

I replied, “good point”.

Kent went on to get a PhD in Physics from UC Berkely, no mean accomplishment. He lobbied heavily for the creation of SETI, or the Search for Extra Terrestrial Intelligence, once an arm of NASA. He became its first director in 1985 and worked there for 20 years.

In the 1987 movie Contact written by Carl Sagan and starring Jodie Foster, Kent’s character is played by Matthew McConaughey. The movie was filmed at the Very Large Array in western New Mexico. The algorithms Kent developed there are still in widespread use today.

Out here in the west aliens are a big deal, ever since that weather balloon crashed in Roswell, New Mexico in 1947. In fact, it was a spy balloon meant to overfly and photograph Russia, but it blew back on the US, thus its top secret status.

When people learn I used to work at Area 51, I am constantly asked if I have seen any spaceships. The road there, Nevada State Route 375, is called the Extra Terrestrial Highway. Who says we don’t have a sense of humor in Nevada?

After devoting his entire life to searching, Kent gave me the inside story on searching for aliens. We will never meet them but we will talk to them. That’s because the acceleration needed to get to a high enough speed to reach outer space would tear apart a human body. On the other hand, radio waves travel effortlessly at the speed of light.

Sadly, Kent passed away in 2021 at the age of 72. Kent, ever the optimist, had his body cryogenically frozen in Hawaii where he will remain until the technology evolves to wake him up. Minor planet 35056 Cullers is named in his honor.

There are no movies being made about my life…. yet. But there are a couple of scripts out there under development.

Watch this space.

Stay healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

![]()

![]()

Global Market Comments

November 10, 2022

Fiat Lux

Featured Trade:

(TEN MORE TRENDS TO BET THE RANCH ON),

(AAPL), (AMZN), (GOOGL), (TSLA), (CRSP), (EDIT), (NTLA)

Mad Hedge Technology Letter

November 9, 2022

Fiat Lux

Featured Trade:

(RISKY BUSINESS)

(ARKK), (SARK), (ROKU), (TSLA)

Tech growth is a sub-sector that readers really need to stay away from right now.

It’s toxic for the time being.

We are still right in the middle of the Fed Funds rate hike cycle and the pounding has been relentless with former tech darlings breaking records for lower lows.

The poster child for the excesses in tech growth is Cathie Wood who is the CEO of ARK (ARKK) innovation funds.

She has completely ignored “market timing” and has used every brash sell-off to go big without doing much research.

This strategy has proven to be highly unsuccessful, as many of her top holdings like Tesla are again in free fall.

CEO of Tesla Elon Musk just sold $4 billion of stock to divert into his new company Twitter which lost a massive amount of advertising revenue when he took over.

Yesterday, crypto experienced an unbelievable meltdown when the 2nd largest exchange FTX once valued around $35 billion was and still is on the brink of bankruptcy.

The same day Wood bet the ranch on crypto exchange Coinbase (COIN) adding 420,949 shares of COIN to the current 7.7 million that ARK Investment Management currently holds.

Bitcoin is down 13% at the time of this writing, representing yet another giant flop for Wood.

Wood is performing highly risky moves at the peak of turmoil in an industry that many think is a Ponzi scheme.

Her exploits are so infamous that it now has an inverse ETF that tracks the opposite of what she decides and performance has been stellar.

That ETF, called AXS Short Innovation Daily ETF (SARK), has soared more than 111% since launching a year ago. That’s the second best performance among the nearly 450 ETFs that launched over the past year.

Wood’s second biggest position is ad tech firm Roku (ROKU) which has gone from $460 to $48 today.

SARK’s first-year performance is among the 20 best of all-time measured against funds that are still trading.

Wood’s poor performance represents the pitfalls of choosing an investment adviser when they are one-dimensional and unable to acknowledge initial mistakes.

Instead of adjusting a flawed strategy, she has used it as the impetus to double down on a bad strategy.

The best hedge fund managers know when they are wrong and quickly reverse course or cut their losses.

Wood’s failures are quickly dealt with by blaming others, routinely saying that others “don’t do their research.”

Wood’s propensity to hype up tech like there is no tomorrow is now directly working against her.

She views any and every selloff as a brilliant entry point while ignoring broader market fundamentals.

In short, the day Cathie Wood is bearish is the day to go big into tech shares, because there are likely no more incremental buyers willing to hold the bag.

Truth be told, the Nasdaq currently sits 35% down from its November 2021 peak a year on.

I would call that pretty good, considering we are deleveraging from the biggest man-made financial bubble that was ever created in financial markets.

The bubble has caused the US Federal government to shoulder more than $31 billion of government debt that needs to be serviced with constant interest payments.

The only reason why tech shares are down 35% is because every investor believes the US Central Bank will kick the can down the road and save corporate America when push comes to shove.

This is precisely why recent bear market rallies have been epic, and any scintilla of interest rate loosening talk is met with thunderous buying.

If investors were more scared of the Fed, tech shares would be down at least 60% by now.

Global Market Comments

November 4, 2022

Fiat Lux

Featured Trade:

(NOVEMBER 2 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (LLY), (TSLA), (GOOG), (GOOGL), (JPM), (BAC), (C), (BRK), (V), (TQQQ), (CCJ), (BLK), (PHO), (GLD), (SLV), (UUP)

Below please find subscribers’ Q&A for the November 2 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley in California.

Q: The country is running out of diesel fuel this month. Should I be stocking up on food?

A: No, any shortages of any fuel type are all deliberately engineered by the refiners to get higher fuel prices and will go away soon. I think there was a major effort to get energy prices up before the election. If that's the case, then look for a major decline after the election. The US has an energy glut. We are a net energy exporter. We’re supplying enormous amounts of natural gas to Europe right now, and natural gas is close to a one-year low. Shortages are not the problem, intentions are. And this is the problem with the whole energy industry, and the reason I'm not investing in it. Any moves up are short-term. And the industry's goal is to keep prices as high as possible for the next few years while demand goes to zero for their biggest selling products, like gasoline. I would be very wary about doing anything in the energy industry here, as you could get gigantic moves one way or the other with no warning.

Q Is the SPDR S&P 500 ETF (SPY) put spread, correct?

A: Yes, we had the November $400-$410 vertical bear put spread, which we just sold for a nice profit.

Q: I missed the LEAPS on J.P. Morgan (JPM) which has already doubled in value since last month, will we get another shot to buy?

A: Well you will get another shot to buy especially if another major selloff develops, but we’re not going down to the old October lows in the financial sector. I believe that a major long-term bull move has started in financials and other sectors, like healthcare. You won’t get the October lows, but you might get close to them.

Q: I’m waiting for a dip to get into Eli Lilly (LLY), but there are no dips.

A: Buy a little bit every day and you’ll get a nice average in a rising market. By the way, I just added Eli Lilly to my Mad Hedge long-term model portfolio, which you received on Thursday.

Q: Any thoughts about the conclusion of the Twitter deal and how it will affect tech and social media?

A: So far all of the indications are terrible. Advertisers have been canceling left and right, hate speech is up 500%, and Elon Musk personally responded to the Pelosi assassination attempt by trotting out a bunch of conspiracy theories for the sole purpose of raising traffic and not bringing light to the issue. All indications are bad, but I've been with Elon Musk on several startups in the last 25 years and they always look like they’re going bust in the beginning. It’s not even a public stock anymore and it shouldn’t be affecting Tesla (TSLA) prices either, which is still growing 50% a year, but it is.

Q: In terms of food commodities for 2023, where are prices headed?

A: Up. Not only do you have the war in Ukraine boosting wheat, soybean, and sunflower prices, but every year, global warming is going to take an increasing toll on the food supply. I know last summer when it hit 121 degrees in the Central Valley, huge amounts of crops were lost due to heat. They were literally cooked on the vine. We now have a tomato shortage and people can’t make pasta sauce because the tomatoes were all destroyed by the heat. That’s going to become an increasingly common issue in the future as temperatures rise as fast as they have been.

Q: Do I trade options in Alphabet (GOOG) or Alphabet (GOOGL)?

A: The one with the L is the holding company, the one without the L is the advertising company and the stock movements are really identical over the long term, so there really isn’t much differentiation there.

Q: Why can’t inflation be brought down by increasing the supply of all goods?

A: Because the companies won’t make them. The companies these days very carefully manage output to keep prices as high as possible. It’s not only the energy industry that does that but also all industries. So those in the manufacturing sector don’t have an interest in lowering their prices—they want high prices. If they see the prices fall, they will cut back supply.

Q: What do you think about growth plays?

A: As long as interest rates are rising, growth will lag and value will lead, and that has been clear as day for the last month. This is why we have an overwhelming value tilt to our model portfolio and our recent trade alerts. They’ve all been banks—JP Morgan (JPM), Bank of America (BAC), Citigroup (C), plus Berkshire Hathaway (BRK) and Visa (V) and virtually nothing in tech.

Q: I don’t know how to execute spread trades in options so how do I take advantage of your service?

A: Every trade alert we send out has a link to a video that shows you exactly how to do the trade. I have to admit, I’m not as young as I was when I made the videos, but they’re still valid.

Q: Is the US housing market about to crash?

A: There is a shortage of 10 million houses in the US, with the Millennials trying to buy them. If you sell your house now, you may not be able to buy another one without your mortgage going from 2.75% to 7.75%—that tends to dissuade a lot of potential selling. We also have this massive demographic wave of 85 million millennials trying to buy homes from 65 million gen x-ers. That creates a shortage of 20 million right there. That's why rents are going up at a tremendous rate, and that's why house prices have barely fallen despite the highest interest rates in 20 years.

Q: If we get good news from the Fed, should we invest in 3X ETFs such as the ProShares UltraPro QQQ (TQQQ)?

A: No, I never invest in 3X ETFs, because they are structured to screw the investor for the benefit of the issuer. These reset at the close every day, so do 2 Xs and not more. If you're not making enough money on the 2Xs, maybe you should consider another line of business.

Q: Do you think BlackRock Corporate High Yield Fund (HYT) will show the pain of slights because of their green positioning?

A: No I don’t, if anything green investing is going to accelerate as the entire economy goes green. And you’ll notice even the oil companies in their advertising are trying to paint themselves as green. They are really wolves in sheep’s clothing. They’ll never be green, but they’ll pretend to be green to cover up the fact that they just doubled the cost of gasoline.

Q: Where do you find the yield on Blackrock?

A: Just go to Yahoo Finance, type in (BLK), and it will show the yield right there under the product description. That’s recalculated by algorithms constantly, depending on the price.

Q: Do you like Cameco (CCJ)?

A: Yes, for the long term. Nuclear reactors have been given an extra five years of life worldwide thanks to the Russian invasion of Ukraine. Even Japan is opening theirs.

Q: Should I short the US dollar (UUP) here?

A: The answer is definitely maybe. I would look for the dollar to try to take one more run at the highs. If that fails, we could be beginning a 10-year bear market in the dollar, and bull market in the Japanese yen, Australian dollar, British pound, and euro. This could be the next big trade.

Q: What is your outlook on Real Estate Investment Trusts (REITs) now?

A: I think it looks great. REITs are now commonly yielding 10%. The worst-case scenario on interest rates has been priced in—buying a REIT is essentially the same thing as buying a treasury bond, but with twice the leverage, because they have commercial credits and not government credits. We’ll be doing a lot more work on REITS. We also have tons of research on REITS from 12 years ago, the last time interest rates spiked. I'll go in and see who’s still around, and I'll be putting out some research on it.

Q: How do you see the price development of gold (GLD)?

A: Lower—the charts are saying overwhelmingly lower. Gold has no place in a rising interest rate world. At least silver (SLV) has solar panel demand.

Q: Do you have any fear of Korea going into IT?

A: Yes, they will always occupy the low end of mass manufacturing, and you can see that in the cellphone area; Samsung actually sells more phones than Apple, but they’re cheaper phones with lower-end lagging technology, and that’s the way it’s always going to be. They make practically no money on these.

Q: When can we get some more trade alerts?

A: We are dead in the middle of my market timing index, so it says do nothing. I’m looking for either a big move down or big move up to get back into the market. This is a terrible environment to chase trades when you're trading, so I'm going to wait for the market to come to me.

Q: What about water as an investment? The Invesco Water Resources ETF (PHO)?

A: Long term I like it. There’s a chronic shortage of fresh water developing all over the world, and we, by the way, need major upgrades of a lot of water systems in the US, as we saw in Jackson, MS, and Flint, MI.

Q: Will REITs perform as well as buying rental properties over the next 10 to 20 years?

A: Yes, rental properties should do very well, as long as you’re not buying any city that has rent control. I have some rental properties in SF and dealing with rent control is a total nightmare, you’re basically waiting for your tenants to die before you raise the rent. I don’t think they have that in Nevada. But in Las Vegas, you have the other issue that is water. I think the shortage of water will start to drag on real estate prices in Las Vegas.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log on to www.madhedgefundtrader.com go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

It’s Been a Tough Market

Global Market Comments

October 24, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or MY SECRET MARKET INDICATOR),

(SPY), (USO), (TSLA), (TBT), (NFLX), (FXY), (SNAP)