Global Market Comments

April 25, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE ESCALATOR UP AND THE WINDOW DOWN)

($INDU), (SPY), (TLT), (WFC), (JPM),

(TSLA), (TWTR), (FCX), (NFLX), (GLD)

Global Market Comments

April 25, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE ESCALATOR UP AND THE WINDOW DOWN)

($INDU), (SPY), (TLT), (WFC), (JPM),

(TSLA), (TWTR), (FCX), (NFLX), (GLD)

On Friday, we saw the worst day in the market since October 2020. And it won’t be the last such meltdown day.

The big question for the market now is how far it can fall without actually having a recession. The answer is 20%, and we are down 8.6% so far.

The economy is as strong as ever and everyone that is predicting a recession is using outdated, useless models. If I have to wait nine months for the delivery of my sofa demand is still off the charts.

Spoiler Alert!

I have to do some math here to explain the current situation. So, don’t run down the street screaming with your hair on fire. Math is your friend, not your enemy.

With an average estimated $227.33 forecast earnings for the S&P 500, we are currently trading at a multiple of 19.29X ($4,386 divided by $227.33). At the November high, we were trading at 24X. At the 2009 Financial Crisis low, we saw 9.5X for a few nanoseconds. There’s our range, 9.5X to 24X.

So, stocks are still historically expensive. They won’t start to approach cheap until we drop to 15X, a level we haven’t seen in nearly a decade. That is another 4.29 multiple points lower, or down 22.23%.

How do we get to cheap?

Since November, the S&P 500 has earned another $60, or 1.36X multiple points. We’ll probably pick up another $55, or 1.25X multiple points in Q2. That gets us halfway there.

The (SPX) is down 8.6% so far in 2022, or $414. If Q2 earnings come in as expected, then the (SPX) only has to fall by another 1.68X multiple points, or 8.72% to $4,004 to get to our 15X downside target.

I hasten to remind you that this was exactly 10% below my downside forecast of an H1 loss of 10% in my 2022 Annual Asset Class Review (click here)for the link.

The Ukraine War and the third oil shock, neither of which I, or anybody else, predicted, account for the second 10% loss.

How long will it take to reach these new, enhanced downside targets? My guess is by the summer.

And you wondered why I was still 100% in cash….until Thursday?

So what does the Federal Reserve make of all this? Even though they say they don’t care about the stock market, it really does, especially when it is crash-prone.

Some 2.50% in expected interest rate hikes are already discounted by the futures market. The market has already done the Fed’s work, and we were short all the way, via the (TLT). We will likely get aggressive half-point rate hikes through April to June, especially if inflation goes double-digit, which it might.

At that point, the Fed may be ahead of the curve. If we get the slightest backtrack in inflation, even just for one month, the Fed may well back off a bit on its tightening strategy and skip a meeting, igniting a monster stock market rally in the second half.

Poof! Your inflation fears have gone away.

Jay Powell Thrust a Dagger into the heart of the Stock Market, sending the Dow down 1,000. At this point, the only question is whether we get two back-to-back 50 basis point rate hikes coming, or two back-to-back 75 basis point rate hikes. 75 basis points is becoming the new 25 basis points.

TINA is dead (there is no alternative to stocks) with virtually all fixed income securities offering a 3.00% yield and junk bonds paying 6%. These kinds of yields have started sucking money out of stocks into bonds, which is why I am long bonds.

There is one other sparkly asset class that is worthy of attention here. Gold, the yellow metal, the barbarous relic (GLD), may have just entered a long-term structural bull market. By evicting Russia from the global financial system, we have driven it out of dollars and into gold and Bitcoin for good. Take a look at the Gold Miners ETF (GDX).

And Russia is not alone in pouring its revenues into gold, which can’t be seized by foreign governments, so is every other country that might be subject to future sanctions, like China. This adds up to a heck of a lot of new gold buying and could take the barbarous relic to my old long-term target of $3,000 an ounce.

Bonds Crash Again, with ten-year US Treasury bond yields topping 3.02% overnight, a three-year high. Those who took my advice to buy the (TBT) in November are now up 44%. The market is now oversold in the extreme and could rally $5-$10 at any time. This could happen right around the next Fed meeting on April 28.

Tesla Earnings Soar by 87% YOY, taking the stock up $90. Musk is still predicting that 50% YOY growth in sales will continue as far as the eye can see and could reach 2 million this year if they can get the lithium. There is a one-year wait for a Tesla now. With gasoline at $6.00 a gallon everyone who bought a Tesla in the last 12 years is looking like a genius. $10,000 a share here we come! Keep buying (TSLA) on dips, as I have been begging you do to for the last 12 years.

Netflix Gets Destroyed, on horrific earnings and falling subscribers. Disney and Amazon are clearly eating their lunch. Hedge fund manager Bill Ackman dumped his position with a $400 million loss. At this point, (NFLX) is a high risk, high return trade than may take years to play out, not my cup of tea.

Corn Hits Nine-Year High, above $8 a bushel. Russia’s invasion of Ukraine may take one-third of the global wheat supply off the market and cause Africa to starve. Who is the world’s largest food importer? China, which may be why the yuan has seen a rare selloff.

Weekly Jobless Claims Fall to 184,000, why the unemployed hit a 52-year low. No need for stimulus here. It’s clear that fear of interest rate rises is not scaring off companies from hiring. Fifty basis points here we come. The unemployment rate may hit an all-time low with the April report on May 6.

Twitter Adopts Poison Pill, to fight off Elon Musk’s takeover attempt. Musk’s offer is a generous 20% higher than the Friday close. If the poison pill is successful then Musk will dump his 9.9% holding, cratering the stock. The battle of the century is on! Incredibly, the stock is up today. (TWTR) holders should take the money and run.

Investor Optimism Hits 30-Year Low, according to the Association of Individual Investors. Now only 15.8% of investors are bullish, down 9% in a week. A lot of pros are starting to see this as a “BUY” signal.

World Bank Cuts Global Growth Outlook on Russian War, from 4.1% in January to 3.2%. This compares to 5.7% in 2021. Europe and central Asia are taking the big hits.

Natural Gas Hits 13-Year High, to $7.80 per MM BTU, up 100% YTD. American exports are rushing to fill the gap in Europe. With the war showing no end in sight, prices will go higher before they go lower.

Copper is Facing a Giant Short Squeeze, and the world rushes into alternative energy, says Freeport McMoRan (FCX) CEO Richard Adkerson. World copper output will have to triple just to accommodate Tesla’s long-term target of 20 million vehicles a year. Buy (FCX) on dips, like this one.

US Housing Starts Hit 15 Year High, up 0.3% in March to 1.79 million. Applications to build top 1.87 million. The US has a structural shortage of 10 million homes caused by the large number of small builders that went under during the financial crisis and never came back.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still historically cheap, oil peaking out soon, and technology hyper-accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

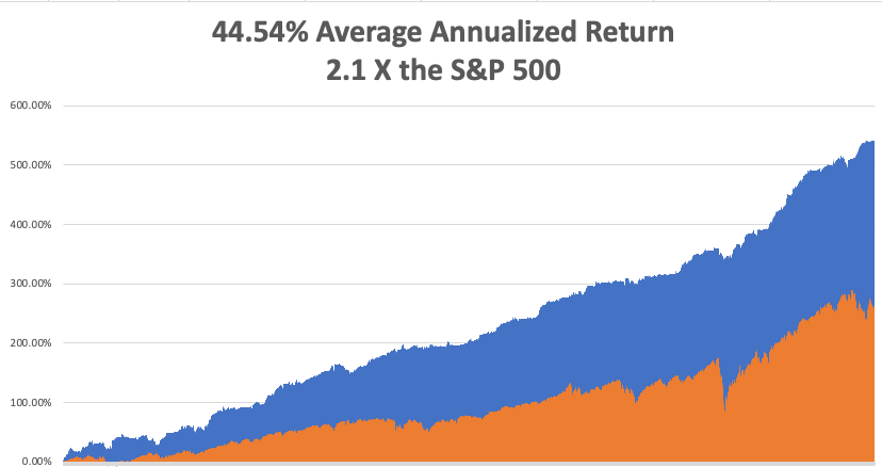

My March month-to-date performance retreated to a modest 2.58%. My 2022 year-to-date performance ended at a chest-beating 29.28%. The Dow Average is down -6.8% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high 71.86%.

On the next capitulation selloff day, which might come with the April Q1 earnings reports, I’ll be adding long positions in technology, banks, and biotech. I am currently in a rare 100% cash position awaiting the next ideal entry point.

That brings my 13-year total return to 541.94%, some 2.10 times the S&P 500 (SPX) over the same period. My average annualized return has ratcheted up to 44.54%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 80.6 million, up only 300,000 in a week, and deaths topping 988,000 and have only increased by 3,000 in the past week. Wow, we only lost the equivalent of eight Boeing 747 crashes in a week! Great news indeed. You can find the data here. Growth of the pandemic has virtually stopped, with new cases down 98% in two months.

The coming week is a big one for tech earnings.

On Monday, April 25 at 8:30 AM EST, the Chicago Fed National Activity Index for March is out. Activision Blizzard Reports (ATVI).

On Tuesday, April 26 at 8:30 AM, US Durable Goods for March are printed. At 9:00 AM the S&P Case Shiller National Price Index is announced. Alphabet (GOOGL) and Microsoft (MSFT) report.

On Wednesday, April 27 at 8:30 AM, the Pending Homes Sales for March are released. Qualcomm and Meta (FB) report.

On Thursday, April 28 at 8:30 AM, the Weekly Jobless Claims are printed. We also get the first look at Q1 GDP. Apple (AAPL), Amazon (AMZN) and Intel (INTC) report.

On Friday, April 29 at 8:30 AM, the Personal Income and Spending for March are disclosed.At 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, when you are a guest of the KGB in Russia, you get treated like visiting royalty par excellence, no extravagance spared. That was the setup I walked into when I was sent by NASA to test fly the MiG 25 in 1993.

Far a start, I was met at Moscow’s Sheremetyevo Airport by Major Anastasia Ivanova, who was to be my escort and guide for the week. She had a magic key that would open any door in Russia and gave me a tour worthy of a visiting head of state.

Anastasia was drop-dead gorgeous. She topped 5’11” with light blonde hair, and was statuesque with chiseled high cheekbones and deep blue eyes. She could easily have taken a side job as a Playboy centerfold. But I could tell from her hands she was no stranger to martial arts and was not to be taken lightly. And wherever we went people immediately tensed up. They knew.

For a start, I was met on the tarmac by a black Volga limo. No need for customs or immigration here. Anastasia simply stamped my passport and welcomed me to Russia, whisking me off to the country’s top Intourist hotel.

The next morning, I was given a VIP tour of the Kremlin and its thousand-year history. I was shown a magnificent yellow silk 18th century ball gown worn by Catherine the Great. I asked her if the story about the horse was true, and she grimaced and said yes.

In a side room were displayed the dress uniforms of Adolph Hitler. I asked what happened to the rest of him and she said he was buried under a parking lot in Magdeburg, East Germany.

Out front, I was taken to the head of the line to see Lenin’s Tomb, which looked like he was made of wax. I think he has since been buried. In front of the Kremlin Armory, I found the Tsar Cannon, a gigantic weapon meant to fire a one-ton ball.

There was only one decent restaurant in Moscow in those days and Anastasia took me out to dinner both nights. Suffice it to say that the Beluga caviar and Stolichnaya vodka were flowing hot and heavy. The service was excellent. We were never presented with a bill. I guess it just went on the company account.

After my day in the capital, I was whisked away 200 miles north to the top secret Zhukovky Airbase to fly the MiG 25. A week later, Anastasia was there in her limo to take me back to Moscow.

The next morning Anastasia was knocking on my door. “Get dressed,” she said. “There’s something you want to see.”

She drove me out to a construction site on the southwestern outskirts of the city. As Moscow was slowly westernizing, suburbs were springing up to accommodate a rising middle class. One section was taped off and surrounded by the Moscow Police. That’s where we headed.

While digging the foundation for a new home, the builders had broken into a bunker left from WWII. Moscow had grown to reach the front lines of the 1942 Battle of Moscow. In Berlin during the 1960s, I worked with a couple of survivors of this exact battle. I was handed a flashlight and we ventured inside.

There were at least 30 German bodies inside in full uniform, except that only the skeletons were left. They still wore their issued steel helmets, medals, belt buckles, and binoculars. There were also dozens of K-98 8 mm rifles, an abundance of live ammunition and potato mashers (hand grenades), and several MG-42’s (yes, I know my machines guns).

The air was dank and musty. My guess was that the bunker had taken a direct hit from a Soviet artillery shell and had remained buried ever since. As a cave in threatened, we got the hell out of there in a few minutes.

Then Anastasia continued with our planned day. Since it was Sunday, she took me to the Moscow Flea Market. Russia was suffering from hyperinflation at the time, and retirees on fixed incomes were selling whatever they had in order to eat.

Everything from the Russian military was for sale for practically nothing, including hats, uniforms, medals, and night vision glasses. I walked away with a pair of very high-powered long-range artillery binoculars for $5. I paused for a moment at an 18th century German bible printed in archaic fraktur. But then Anastasia said I might get hung up by Russia’s antique export ban on my departure.

Anastasia and I kept in touch over the years. I sent him some pressed High Sierra wildflowers, which impressed her to no end. She said such a gesture wouldn’t even occur to a Russian man.

We gradually lost contact over the years, given all the turmoil in Russia that followed. But Anastasia left me with memories I will never forget. And I still have those binoculars to use at the Cal football games.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

April 22, 2022

Fiat Lux

Featured Trade:

(APRIL 20 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPX), (TSLA), (TBT), (TLT), (BAC), (JPM), (MS),

(BABA), (TWTR), (PYPL), (SHOP), (DOCU),

(ZM), (PTON), (NFLX), (BRKB), (FCX), (CPER)

Below please find subscribers’ Q&A for the April 20 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley.

Q: Should I take profits on the ProShares UltraShort 20+ Year Treasury ETF (TBT), or will it go lower?

A: Well, you’ve just made a 45% profit in 4 months; no one ever gets fired for taking a profit. And yes, it will go lower, but I think we’re due for a 5 -10% rally in the (TBT) and we’re seeing some of that today.

Q: Do you think the bottom is in now for the S&P 500 Index (SPX)?

A: No, I think the 50 basis point rate hikes will put the fear of God into the market and prompt another round of profit-taking in stocks. So will another ramp up or expansion in the Ukraine War, and so could another spike in Covid cases. And interest rates are getting high enough, with a ten-year US Treasury (TLT) at 2.95% and junk at 6.00% that they will start to bleed off money from stocks.

So there are plenty of risks in this market that I don’t need to chase thousand point rallies that fail the following week.

Q: What would cause a rally in the iShares 20 Plus Year Treasury Bond ETF (TLT)?

A: Everyone in the world is short, for a start. And secondly, we’ve had a $36 point drop in the market in 4 ½ months—that is absolutely screaming for a short-covering rally. It would be typical of the market to get everybody in the world short one thing, and then ramp it right back up. You can bet hedge funds are just gunning for that trade. So those are two big reasons. Another big reason is getting a slowdown in the economy. Fear of interest rate rises and yield curve inversions are certainly going to scare people into thinking that.

Q: Where to buy Tesla (TSLA)?

A: We had a $1,200 all-time high at the end of last year, then sold off to $700—that was your ideal entry point, on that one day when the market was down $1,000 and they were throwing out Tesla stock like there was no tomorrow. We have since rallied back to the 1100s, so I'd say at this point, anything you could get under just above the $200-day moving average at $900 would be a gift because the sales are happening and they’re making tons of money. They’re so far ahead of the rest of the world on EV technology that no one will ever be able to catch up. A lot of the biggest companies like Ford (F) and (GM) are still unable to mass produce electric cars, even though they’re all talking about these wonderful models they're bringing out in 2024 and 2025. So, I think Tesla is just so far ahead in the market that no one will catch them. And the stock will have to reflect that by trading at a higher premium.

Q: I Bought the ProShares UltraShort 20+ Year Treasury ETF (TBT) at your advice at $14, it’s now at 425. Time to take the money and run?

A: Yes, so that you’re in position to rebuy the (TBT) at $22, or even $20.

Q: I bought some bank LEAPS such as Bank of America (BAC), JP Morgan (JPM), and Morgan Stanley (MS) just before earnings; they’re doing well so far.

A: That will definitely be one of my target sectors on any recovery; because the only reason the stock market recovers is because recession fears have been put away, and the only reason the banks have been going down is because of recession fears. Certainly, the yield curve inversion has been helping them lot, as are absolute higher interest rates. So yes, zero in on the banks, I’m holding back waiting for better entry points, but for those who are aggressive, there’s no problem with scaling in here.

Q: If Putin uses a tactical nuclear weapon in the Ukraine, what would be the outcome?

A: Well, I don't think he will, because you don’t want to use nukes on your neighbors because the wind tends to blow the radiation back into your own country. It also depends on when he does this; if Ukraine joins NATO, joins the EC, and NATO troops enter Ukraine, and then they use tactical nukes, France and England also have their own nuclear weapons. So, attacking a nuclear foe and risking bringing in the US, who could wipe out the whole country in minutes, would not be a good idea.

Q: Would you get into Chinese stocks here?

A: Not really; China seems to have changed its business model permanently by abandoning capitalism. The Mad Hedge Technology Letter is currently running a short position in Alibaba (BABA) which has proved highly successful. Although these things are stupidly cheap, they could get cheaper before they turn around. Also, there’s the threat of delisting on the stock exchanges facing them in a year or two, and the trade tensions which continue with China. China doesn’t seem friendly anymore or is interested in capitalism. You don't want to own stocks anywhere in that situation. And by the way, Russia has also banned all foreign stock listings. China could do the same—not good if you’re an owner of those stocks.

Q: How would you play Twitter (TWTR) now?

A: I think it’s a screaming short, myself. If the board doesn’t accept Elon’s offer, which seems to be the case with their poison pill adoption, there are no other buyers of Twitter; and Elon has already said he’s not going to pay up. So you take Elon Musk’s shareholding out of the picture, and you’re looking at about a 30% drop.

Q: Many of the biggest Covid beneficiaries are near or below their March 2020 lows, such as PayPal (PYPL), Shopify (SHOP), DocuSign (DOCU), Zoom (ZM), Peloton (PTON), Netflix (NFLX), etc. Are these buys soon or are there other new names joining them?

A: I think this will continue to be a laggard sector. I think any recovery will be led by big tech, and once big tech peaks out after a 6-month run, then you may get the smaller ones catching up—especially if they're still down 80% or 90%. So that’s a no-touch for me; too many better fish to fry.

Q: Do you think inflation is transitory or are we headed toward double digits over the long term?

A: The transitory argument got thrown out the window the day Russia invaded Ukraine; they are one of the world’s largest producers of both energy and wheat. So that definitely set those markets on fire and really could end up adding an extra 5% in our inflation numbers before we peak out. I think we will see the highs sometime this year, could be as low as 4% by the end of this year. But we may have a double-digit print before we top out, and that could be next month. So, if you’re looking for another reason for stocks to sell out, that would be a good one.

Q: If the EU could limit oil purchases from Russia, then the war would be over in a month since Russia has no borrowing power or reserves.

A: The problem is whether they actually could limit oil purchases, which they can’t do immediately. If you could limit them in a year or cut them down by like 80%, we could come up with the other 20%, that is possible. Then, the war would end and Russia would starve; but Russia may starve anyway. Even with all the rubles in the world, they can’t buy anything overseas. Basically, Russia makes nothing, they only sell commodities and use those proceeds to buy consumer goods from abroad, which have all been completely cut off. They’re in for an economic disaster no matter what happens, and they have no way of avoiding it.

Q: What are your thoughts on supply chain problems?

A: I actually think they’re getting better; I watch the number of ships at anchor in San Francisco Bay, and it’s actually down by about half over the last 3 months. People are slowly starting to get things that they ordered nine months ago, used car prices are starting to roll over…so yes, it’s going to be a very slow process. It took one week to shut down the global economy, it’ll take three years to get it fully reopened. And of course, that’s extended by the Ukraine War. Plus, as long as there are supply chain problems and huge prices being paid for parts and labor, you’re not going to have a recession, it’s impossible.

Q: What’s your outlook on tech stocks?

A: I see them bottoming in the current quarter, and then going on to new all-time highs in the second half.

Q: What about covered calls?

A: It’s a really good idea, allowing you to get long a stock here, and reduce your average cost every month by writing calls against your position until they eventually get called away. Not too long ago, I wrote a piece on covered calls, so I could rerun that again to get people familiar with the concept.

Q: If Warren Buffet retires, what happens to Berkshire Hathaway (BRKB) stock?

A: It drops about 5% one day, then goes on to new highs. The concept of a 90-year-old passing away in his sleep one night is not exactly revolutionary or new. Replacements for Buffet have been lined up for so long that now the replacements are retiring. I think that’s pretty much baked in the price.

Q: Any plans to update the long-term portfolio?

A: Yes it’s on my list.

Q: Too late to buy Freeport McMoRan (FCX)?

A: Yes I’m afraid so. We’ve had a near double since September when it started moving. However, I would hold it if you already own it and add on any substantial selloff. Freeport McMoRan announced fabulous earnings today, and the stock promptly sold off 9%. It was a classic “buy the rumor, sell the news” type move. This is despite the fact that the United States Copper Fund ETF (CPER), in which (FCX) is a major holding, is up on the day. Please remember that I told you earlier that each Tesla needs 200 pounds of copper, that Tesla sales could double to 2 million this year, and that they could sell 4 million if they could make them. It sounds like a bullish argument of me, of which (FCX) is the world’s largest producer.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

April 20, 2022

Fiat Lux

Featured Trade:

(TESTIMONIAL),

(TEN MORE TRENDS TO BET THE RANCH ON),

(AAPL), (AMZN), (GOOGL), (TSLA), (CRSP), (EDIT), (NTLA)

Global Market Comments

April 18, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or GET READY TO SELL IN MAY)

($INDU), (SPY), (TLT), (WFC), (JPM), (TSLA), (TWTR)

So when you are supposed to “Sell in May and go away”, what are you supposed to be doing on April 18?

Not much.

War, inflation, disease, runaway energy prices, and soaring interest rates are usually not a good backdrop for trading stocks. When the wind is blowing against me with gale-force winds instead of behind me, I tend to quit. I only like playing games that are rigged in my favor, or in yours.

Retreating to fight another day sounds like a good strategy to me because it’s much easier to dig out of a small hole than a large one. And it’s impossible to recover if you lost all your money chasing marginal low-quality trades. That 100-day cruise around the world that Cunard is offering right now looks pretty good. If the central bank says it is set on slowing the economy, believe it. The free Fed put is a distant memory.

But whatever Armageddon we are facing out there, it will be a modest one. We now have an unemployment rate of 3.6%, but there are still 11 million open jobs. That means there are more jobs in the US right now than workers, a first in history.

There are in fact several big positives the markets are ignoring right now because it is fashionable to do so. You know these supply chain problems? They’re slowly going away. You see this in falling freight rates for US truckers.

The Cass Freight Index measure of domestic shipping demand edged up a bare 0.6% in March from the month before, an unseasonable slowing of growth at the end of the quarter. From where I sit, the number of Chinese container ships at anchor in San Francisco Bay is on a definite decline.

Going into real recessions, consumers usually baton down the hatches, don their hard hats, and reign in spending. And while they tell pollsters they are worried about the economy, they act like they believe in the opposite, spending with reckless abandon. Wells Fargo (WFC) has seen spending on credit cards soaring by 33% in Q1, while it has jumped by an impressive 29% at JP Morgan (JPM).

There is also a great positive out there which is being completely ignored by the market. The pandemic is gone. Daily cases have dropped from one million to only 20,000 in two months, a record drop in the history of epidemiology. Masks are now only required at mass events like rock concerts and the San Francisco Ballet.

So I will endeavor to entertain you with my stories long enough to keep you from getting bored until trading stocks becomes the slam dunk no-brainer affair it once was. That would be in anything from 2-5 months.

Elon Musk makes $53 billion takeover bid for Twitter in a move that gobsmacked Wall Street. He made the offer in a 281-character tweet to the board of directors. His goal will be to end all censorship, which means bringing back the crazies and the violent. If they don’t accept his premium offer, then he will sell the 9.9% of shares that he already owns and the board will get sued to death by shareholders.

Inflation jumps to 8.5% YOY, a 40-year high, with half of the increase coming from gasoline prices. Stocks and bonds were up on a “buy the rumor, sell the news” move. Unless oil prices completely collapse, next month will be worse.

Producer Price Index rockets by 11.2%, an 11-year high. This is on the heels of yesterday’s red hot Core Inflation report. It makes a half-point rate hike on April 29 a sure thing.

Retail Sales jumped 0.5% in March, and up 6.9% YOY, while import prices hit an 11-year high.

Bonds hit new three-year lows, with yields soaring to 2.81% overnight. The market is transitioning from a Fed that is raising rates from a quarter point at each meeting to a half point. We may be reaching the end of this leg down, off $9.00 in weeks. Only sell the big rallies. (TLT) LEAPS holders are sitting pretty.

Mortgage Refis down 67% YOY, thanks to a 30-year fixed rate mortgage that has topped 5.0%. It looks like the loan sharks won’t be grabbing as much in fees. This market won’t recover for several years. If you didn’t refi last year at century low rates, you’re screwed.

NVIDIA downgraded from outperform to neutral and the price target was chopped from $360 to $225 by Baird & Co. It’s a bold move as (NVDA) has long been a Mad Hedge favorite and 70-bagger over the last five years. Baird cites cancellations driven by a combination of excess GPUs, or graphics processing unit in Western Europe and Asia, as well as a slowdown in consumer demand, especially in China. Slowing consumer demand for GPUs was evident in the continuing reduction in graphics card pricing. I believe any slowdowns are temporary and you should keep buying (NVDA) on dips.

Used Car Sales take a hit, as affordability becomes a major issue. Carmax just reported a 6.5% plunge in Q4. I can sell my Tesla Model X for more than I paid three years ago because it takes a year to get a new one.

Weekly Jobless Claims hit 185,000, up 18,000 from the previous week. The stock market may be worried about a coming recession but the jobs market sure isn’t.

Morgan Stanley blows away earnings. Equity trading came in a hot $3.2 billion and bond trading $2.9 billion. The shares popped 7% on the news. Buy (MS) on dips.

Mercedes breaks 600 miles range on a single charge with its EQXX prototype, driving from Stuttgart to the French Riviera. But the cost per watt is still double Tesla’s. Mercedes plans to go all-electric by the end of the decade.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still historically cheap, oil peaking out soon, and technology hyper accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

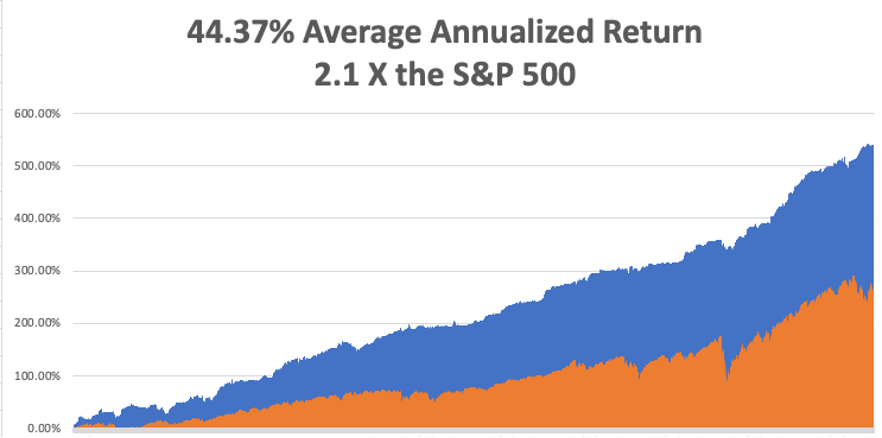

My March month-to-date performance retreated to a modest 0.38%. My 2022 year-to-date performance ended at a chest-beating 27.23%. The Dow Average is down -5.1% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high 68.55%.

On the next capitulation selloff day, which might come with the April Q1 earnings reports, I’ll be adding long positions in technology, banks, and biotech. I am currently in a rare 100% cash position awaiting the next ideal entry point.

That brings my 13-year total return to 539.79%, some 2.10 times the S&P 500 (SPX) over the same period. My average annualized return has ratcheted up to 44.36%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 80.6 million, up only 300,000 in a week and deaths topping 988,000 and have only increased by 3,000 in the past week. You can find the data here. Growth of the pandemic has virtually stopped, with new cases down 98% in two months.

On Monday, April 18 at 7:00 AM EST, the NAHB Housing Market Index is out. Bank of America (BAC) reports.

On Tuesday, April 19 at 8:30 AM, Housing Starts for March are published. Netflix (NFLX) reports.

On Wednesday, April 20 at 8:30 AM, the Existing Home Sales for March are printed. Tesla (TSLA) reports.

On Thursday, April 22 at 7:30 AM, the Weekly Jobless Claims are printed. Union Pacific (UNP) reports.

On Friday, April 23 at 8:30 AM, the S&P Global Composite Flash PMI is disclosed. American Express (AXP) reports. At 2:00 PM, the Baker Hughes Oil Rig Count are out.

As for me, the call from Washington DC was unmistakable, and I knew what was coming next. “How would you like to serve your country?” I’ve heard it all before.

I answered, “Of course, I would.”

I was told that for first the first time ever, foreign pilots had access to Russian military aircraft, provided they had enough money. You see, everything in the just collapsed Soviet Union was for sale. All they needed was someone to masquerade as a wealthy hedge fund manager looking for adventure.

No problem there.

And can you fly a MiG29?

No problem there either.

A month later, I was wearing the uniform of a major in the Russian Air Force, my hair cut military short, sitting in the backseat of a black Volga limo, sweating bullets.

“Don’t speak,” said my driver.

The guard shifted his Kalashnikov and ordered us to stop, looked at my fake ID card and waved us on. We were in Russia’s Zhukovky Airbase 100 miles north of Moscow, home of the country’s best interceptor fighter, the storied Fulcrum, or MiG-29.

I ended up spending a week at the top-secret base. That included daily turns in the centrifuge to make sure I was up to the G-forces demand by supersonic flight. Afternoons saw me in ejection training. There in my trainer, I had to shout “eject, eject, eject,” pull the right-hand lever under my seat, and then get blasted ten feet in the air, only to settle back down to earth.

As a known big spender, I was a pretty popular guy on the base, and I was invited to a party every night. Let me tell you that vodka is a really big deal in Russia, and I was not allowed to leave until I had finished my own bottle, straight.

In 1993, Russia was realigning itself with the west, and everyone was putting their best face going forward. I had been warned about this ahead of time and judiciously downed a shot glass of cooking oil every evening to ward off the worst effects of alcohol poisoning. It worked.

Preflight involved getting laced into my green super tight gravity suit, a three-hour project. Two women tied the necessary 300 knots, joking and laughing all the while. They wished me a good flight.

Next, I met my co-pilot, Captain A. Pavlov, Russia’s top test pilot. He quizzed me about my flight experience. I listed off the names: Laos, Cambodia, Thailand, Israel, Croatia, Serbia, Bosnia, Kuwait, Iraq, and Saudi Arabia. It was clear he still needed convincing.

Then I was strapped into the cockpit.

Oops!

All the instruments were in the Cyrillic alphabet….and were metric! They hadn’t told me about this, but I would deal with it.

We took off and went straight up, gaining 50,000 feet in two minutes. Yes, fellow pilots, that is a climb rate of an astounding 25,000 feet a minute. They call them interceptors for a reason. It was a humid day, and when we hit 50,000 feet, the air suddenly turned to snowflakes swirling around the cockpit.

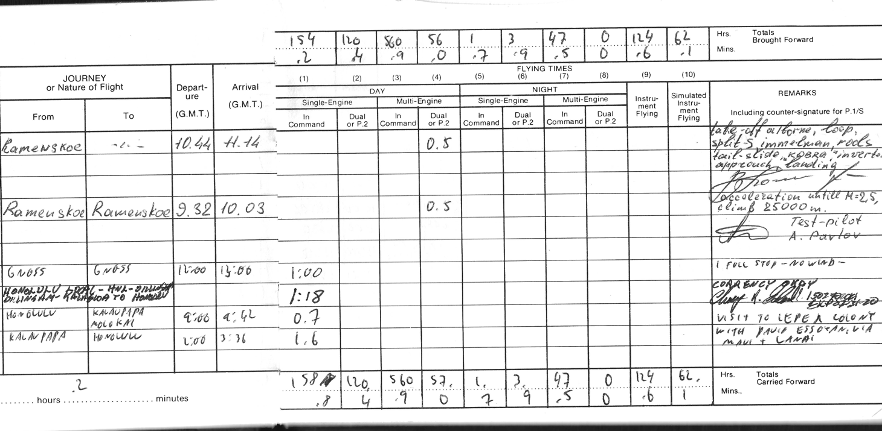

Then we went through a series of violent spins, loops, and other evasive maneuvers (see my logbook entry below). Some of them seemed aeronautically impossible. I watched the Mach Meter carefully, it frequently danced up to the “10” level. Anything over ten is invariably fatal, as it ruptures your internal organs.

Then Pavlov said, “I guess you are a real pilot, and he handed the stick over to me. I put the fighter into a steep dive, gaining the maximum handbook speed of March 2.5, or 2.5 times the speed of sound, or 767.2 miles per hour in seconds. Let me tell you, there is nothing like diving a fighter from 90,000 feet to the earth at 767.2 miles per hour.

Then we found a wide river and buzzed that at 500 feet just under the speed of sound. Fly over any structure over the speed of sound and the resulting shock wave shatters concrete.

I noticed the fuel gages were running near empty and realized that the Russians had only given me enough fuel to fly for an hour. That’s so I wouldn’t hijack the plane and fly it to Finland. Still, Pavlov trusted me enough to let me land the plane, no small thing in a $30 million aircraft. I made a perfect three-point landing and taxied back to base.

I couldn’t help but notice that there was a MiG-25 Foxbat parked in the adjoining hanger and asked if it was available. They said “yes”, but only if I had $10,000 in cash on hand, thinking this was an impossibility. I said, “no problem” and whipped out my American Express gold card.

Their eyes practically popped out of their heads, as this amounted to a lifetime of earnings for the average Russian. They took a picture of the card, called in the number, and in five minutes I was good to go.

They asked when I wanted to fly, and as I was still in my gravity suite I said, “How about right now?” The fuel truck duly back up and in 20 minutes I was ready for takeoff, Pavlov once again my co-pilot. This time, he let me do the takeoff AND the landing.

The first thing I noticed was the missile trigger at the end of the stick. Then I asked the question that had been puzzling aeronautics analysts for years. “If the ceiling of the MiG-25 was 90,000 feet and the U-2 was at 100,000 feet, how did the Russians make up the last 10,000 feet?

“It’s simple,” said Pavlov. Put on full power, stall out at 90,000 feet, then fire your rockets at the apex of the parabola to make up the distance. There was only one problem with this. If your stall forced you to eject, the survival rate was only 50%. That's because when the plane in free fall hit the atmosphere at 50,000 feet, it was like hitting a wall of concrete. I told him to go ahead, and he repeated the maneuver for my benefit.

It was worth the risk to get up to 90,000 feet. There you can clearly see the curvature of the earth, the sky above is black, you can see stars in the middle of the day, and your forward vision is about 400 miles. We were the highest men in the world at that moment. Again, I made a perfect three-point landing, thanks to flying all those Mustangs and Spitfires over the decades.

After my big flights, I was taken to a museum on the base and shown the wreckage of the U-2 spy plane flown by Francis Gary Powers shot down over Russia in 1960. After suffering a direct hit from a missile, there wasn’t much left of the U-2. However, I did notice a nameplate that said, “Lockheed Aircraft Company, Los Angeles, California.”

I asked, “Is it alright if I take this home? My mother worked at this factory during WWII building bombers.” My hosts looked horrified. “No, no, no, no. This is one of Russia’s greatest national treasures,” and they hustled me out of the building as fast as they could.

It's a good thing that I struck while the iron was hot as foreigners are no longer allowed to fly any Russian jets. And suddenly I have become very popular in Washington DC once again.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Russian Test Pilot A. Pavlov

Entries in my Logbook (Notice visit to leper colony on line 9)

U-2 Spyplane

Mad Hedge Technology Letter

April 11, 2022

Fiat Lux

Featured Trade:

(SMALL EV PLAYERS HIT HARD)

(RIVN), (TSLA), (NIO)

A killer tornado is coming for the global EV sector in the short-term and smaller firms like Rivian (RIVN) will bear the brunt of the damage.

That’s not to say that leaders like Tesla (TSLA) have a slam dunk situation as well.

It’s been rough going of late as the already well-documented spiking inflationary pressures could be followed by even worse inflationary gut punches.

How do I know this?

China.

China’s zero covid policy has made the country incredible successful at defending the health of their population against the novel coronavirus.

The Middle Kingdom has only recorded around 4,000 deaths and they are by far the most successful country partly due to their mass lockdown policies.

However, when large swaths of the population are on the subs bench, the vaunted Chinese manufacturing sector is out of order as well.

Tesla’s Shanghai Giga factory was only supposed to shut down for 4 days, but that has been extended as Shanghai’s spread of the virus has expanded to all parts of the city.

This particular factory is Tesla’s most successful and efficient factory producing 16,000 Teslas every week.

A week’s work usually consists of 6,000 Model 3s and 10,000 Model Ys.

As it stands, Tesla’s Gigafactory in Shanghai was supposed to open this Monday, but again, that date has been pushed back yet again bringing a painstaking wait to 17 days.

That means, in total, an opportunity cost of 40,000 units of Shanghai Teslas that were unable to be completed.

Tesla will again, try to open on April 14th which would represent a full 3 weeks of delays and 48,000 cars unable to be produced.

Elon Musk was a legendary genius to build a Gigafactory in Shanghai and avoiding all US raw material import tariffs.

Romanticizing about a cheap source of labor and reduced building construction costs by 75% definitely help companies stay ahead.

In practice, life as an American corporation in an authoritarian country has its downsides.

Ironically enough, Musk was always unhappy about California’s hostile take on allowing his enterprise to run free from covid restrictions.

I wonder what his thoughts are about cooperating with the Chinese communist party, and does he believe they will cave on the covid restrictions?

Maybe California isn’t so bad for Elon.

The news comes on the heels of another EV firm Nio (NIO) announcing they would stop production because of supply chain issues.

Nio’s supplier partners in several cities including Jilin, Shanghai and Jiangsu suspended production making it impossible to finish the cars in production.

Nio also has a large part of the production process placed in Shanghai such as the testing sites and its factory.

Shanghai is home to the country's greatest number of EV-related companies, totaling 18,200.

This is a gargantuan setback for the global EV sector and this Shanghai lockdown is poised to shake out the bottom line of many of these companies who are exposed to China.

The situation is on the verge of spiraling out of control as another Chinese megacity, famous for its industrial prowess, Guangzhou is now in the early stages of initiating a full-scale zero lockdown as well.

These Chinese supply bottlenecks aren’t just a one-off for the EV players, the Eastern European military conflict has forced Rivian to reduce forecasts and lower expectations for a company that is supposed to become the new Tesla.

Large issues such as shortages of critical parts like semiconductors and other materials and equipment necessary for vehicle production have forced it to make changes to its internal processes that have only increased its expenses.

Skyrocketing bills for essential materials such as nickel, lithium, cobalt, and aluminum have hamstrung RIVN.

The price spikes have forced the EV sticker price to spike as well and an uproar ensued as RIVN even raised prices to customers who pre-booked and already paid their initial deposit.

Rivian later walked back the price hikes to the existing purchases and settled for the price hikes for future RIVN purchase.

Ripping off the first swath of customers is bad management.

In the EV world, we are closely approaching the levels of meaningful demand destruction as many consumers could start balking at extortionate pricing especially when RIVN is already struggling to ramp up production and also when RIVN has yet to prove their quality to the median EV buyer.

Ultimately, the headwinds are real for an upstart like Rivian and they have pulled back production targets of 40,000 this year to 25,000 representing a massive blow to the growth trajectory of the company.

Even the 25,000-unit forecast could get another cut to 15,000 if Chinese zero lockdowns persist, and the Eastern European military conflict unleashes another level of inflationary contagion which is highly plausible.

With Tesla producing record quarterly units, that appears as if it will represent a short-term high-water mark for the EV industry as the fracturing of global supply chains forces many of these companies to go into survival mode.

In the short term, I am highly bearish on NIO and RIVN, but TSLA has more tools at its disposal to find better solutions while having the magic of Elon Musk. Shorting TSLA never makes sense from a trading perspective, but other EV firms do.

Global Market Comments

April 11, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD,

or WATCH OUT FOR THE RECESSION WARNINGS)

(TLT), (TSLA), (FB), (CRSP), (TDOC), (GILD), (EDIT), (SQ), (INDU), (NVDA), (GS)