Global Market Comments

November 19, 2021

Fiat Lux

Featured Trade:

(NOVEMBER 17 BIWEEKLY STRATEGY WEBINAR Q&A),

(RIVN), (WMT), (BAC), (MS), (GS), (GLD), (SLV), (CRSP), (NVDA),

(BAC), (CAT), (DE), (PTON), (FXI), (TSLA), (CPER), (Z)

Global Market Comments

November 19, 2021

Fiat Lux

Featured Trade:

(NOVEMBER 17 BIWEEKLY STRATEGY WEBINAR Q&A),

(RIVN), (WMT), (BAC), (MS), (GS), (GLD), (SLV), (CRSP), (NVDA),

(BAC), (CAT), (DE), (PTON), (FXI), (TSLA), (CPER), (Z)

Below please find subscribers’ Q&A for the November 17 Mad Hedge Fund Trader Global Strategy Webinar broadcast from the safety of Silicon Valley.

Q: Even though your trading indicator is over 80, do you think that investors should be 100% long stocks using the barbell names?

A: Yes, in a hyper-liquidity type market like we have now, we can spend months in sell territory before the indexes finally rollover. That happened last year and it’s happening now. So, we can chop in this sort of 50-85 range probably well into next year before we get any sell signals. Selling apparently is something you just do anymore; if things go down, you just buy more. It’s basically the Bitcoin strategy these days.

Q: What do you think about Rivian's (RIVN) future?

A: Well, with Amazon behind them, it was guaranteed to be a success. However, we mere mortals won't be able to buy any cars until 2024, and they have yet to prove themselves on mass production. Moreover, the stock is ridiculously expensive—even more than Tesla was in its most expensive days. And it’s not offering any great value, just momentum so I don’t want to chase it right here. I knew it was going to blow up to the upside when the IPO hit because the EV sector is just so hot and EVs are taking over the global economy. I will watch from a distance unless we get a sudden 40% drawdown which used to happen with Tesla all the time in the early days.

Q: Are you worried about another COVID wave?

A: No, because any new virus that appears on the scene is now attacking a population that is 80-90% immune. Most people got immunity through shots, and the last 10% got immunity by getting the disease. So, it’s a much more difficult population for a new virus to infect, which means no more stock market problems resulting from the pandemic.

Q: Is investing in retail or Walmart (WMT) the best way to protect myself from inflation?

A: It’s actually quite a good way because Walmart has unlimited ability to raise prices, which goes straight through to the share price and increases profit margins. Their core blue-collar customers are now getting the biggest wage hikes in their lives, so disposable income is rocketing. And really, overall, the best way to protect yourself from inflation is to own your own home, which 62% of you do, and to own stocks, which 100% of the people in this webinar do. So, you are inflation-protected up the wazoo coming to Mad Hedge Fund Trader. Not to mention we buy inflation plays like banks here.

Q: Why are financials great, like Bank of America (BAC)?

A: Because the more their assets increase in value, the greater the management fees they get to collect. So, it’s a perfect double hockey stick increase in profits.

*Interest rates are rising

*Rising interest rates increase bank profit margins

*A recovering economy means default rates are collapsing

*Thanks to Dodd-Frank, banks are overcapitalized

*Banks shares are cheap relative to other stocks

*The bank sector has underperformed for a decade

*With rates rising value stocks like banks make the perfect rotation play out of technology stocks.

*Cryptocurrencies will create opportunities for the best-run banks.

Q: Do you think the market is in a state of irrational exuberance?

A: Yes. Warning: irrational exuberance could last for 5 years. That’s what happened when Alan Greenspan, the Fed governor in 1996, coined that phrase and tech stocks went straight up all the way up until 2000. We made fortunes off of it because what happens with irrational exuberance is that it becomes more irrational, and we’re seeing that today with a lot of these overdone stock prices.

Q: Should I hold cash or bonds if you had to choose one?

A: Cash. Bonds have a terrible risk/reward right now. You’re getting like a 1% coupon in the face of inflation that's at 6.2%. It’s like the worst mismatch in history. In fact, we made $8 points on our bond shorts just in the last week. So just keep selling those rallies, never own any bonds at all—I don’t care what your financial advisor tells you, these are worthless pieces of paper that are about to become certificates of confiscation like they did back in the 80s when we had high inflation.

Q: What’s your yearend target for Nvidia (NVDA)?

A: Up. It’s one of the best companies in the world. It’s the next trillion dollar company, but as for the exact day and time of when it hits these upside targets, I have no idea. We’ve been recommending Nvidia since it was $50, and it’s now approaching $400. So that’s another mad hedge 20 bagger setting up.

Q: What about CRISPR Therapeutics (CRSP)?

A: The call spread is looking like a complete write-off; we missed the chance to sell it at $170, it’s now at $88. So, I’m just going to write that one-off. Next time a biotech of mine has a giant one-day spike, I am selling. What you might do though with Crisper is convert your call spread to straight outright calls; that increases your delta on the position from 10% to 40% so that way you only need to get a $20 move up in the stock price and you’ll get a break-even point on your long position. So, convert the spreads to longs—that’s a good way of getting out of failed spreads. You do not need a downside hedge anymore, and you’ll find those deep out of the money calls for pennies on the dollar. That is the smart thing to do, however, you have to put money into the position if you’re going to do that.

Q: Would you buy a LEAP in Tesla (TSLA) at this time?

A: No, it’s starting a multi-month topping out process, then it goes to sleep for 5 months. After it’s been asleep for 5 months then I go back and look at LEAPS. Remember, we had a 45% drawdown last year. I bet we get that again next year.

Q: Will inflation subside?

A: Probably in a year or so. A lot depends on how quickly we can break up the log jam at the ports, and how this infrastructure spending plays out. But if we do end the pandemic, a lot of people who were afraid of working because of the virus (that’s 5 or 10 million people) will come back and that will end at least wage inflation.

Q: When is the next Mad Hedge Fund Trader Summit?

A: December 7, 8, and 9; and we have 27 speakers lined up for you. We’ll start emailing probably next week about that.

Q: Are gold (GLD) and silver (SLV) getting close to a buy?

A: Maybe, unless Bitcoin comes and steals their thunder again. It has been the worst-performing asset this year. The only gold I have now is in my teeth.

Q: Morgan Stanley (MS) is tanking today, should I dump the call spread?

A: I’m going to see if we hold here and can close above our maximum strike price of $98 on Friday. But all of the financials are weak today, it’s nothing specific to Morgan Stanley. Let’s see if we get another bounce back to expiration.

Q: Where can I view all the current positions?

A: We have all of our positions in the trade alert service in your account file, and you should find a spreadsheet with all the current positions marked to market every day.

Q: What is the barbell strategy?

A: Half your money is in big tech and the other half is in financials and other domestic recovery plays. That way you always have something that’s going up.

Q: Is Elon Musk selling everything to avoid taxes from Nancy Pelosi?

A: Actually, he’s selling everything to avoid taxes from California governor Gavin Newsom—it’s the California taxes that he has to pay the bill on, and that’s why he has moved to Texas. As far as I know, you have to pay taxes no matter who is president.

Q: Will the price of oil hit $100?

A: I doubt it. How high can it go before it returns to zero?

Q: Is it time to buy a Caterpillar (CAT) LEAP?

A: We’re getting very close because guess what? We just got another $1.2 billion to spend on infrastructure. Not a single job happens here without a Caterpillar tractor or a tractor from Komatsu for John Deere (DE).

Q: Will small caps do well in 2022?

A: Yes, this is the point in the economic cycle where small caps start to outperform big caps. So, I'd be buying the iShares Russell 2000 ETF (IWM) on dips. That's because smaller, more leveraged companies do better in healthy economies than large ones.

Q: Is it too late to buy coal?

A: Yes, it’s up 10 times. The next big move for coal is going to be down.

Q: Peloton (PTON) is down 300%; should I buy here?

A: Turns out it’s just a clothes rack, after all, it isn't a software company. I didn’t like the Peloton story from the start—of course, I go outside and hike on real mountains rather than on machines, so I’m biased—but it has “busted story” written all over it, so don’t touch Peloton.

Q: Will spiking gasoline prices cause US local governments to finally invest in Subways and Trams like European cities, or is this something that will never happen?

A: This will never happen, except in green states like New York and California. A lot of the big transit systems were built when labor was 10 cents a day by poor Irish and Italian immigrants—those could never be built again, these massive 100-mile subway systems through solid rock. So if you want to ride decent public transportation, go to Europe. Unfortunately, that’s the path the United States never took, and to change that now would be incredibly expensive and time-consuming. They’re talking about building a second BART tunnel under the bay bridge; that’s a $20 billion, 20-year job, these are huge projects. And for the last five years, we’ve had no infrastructure spending at all, just lots of talk.

Q: Would Tesla (TSLA) remains stable if something happened to Elon Musk?

A: Probably not; that would be a nice opportunity for another 45% correction. But if that happened, it would also be a great opportunity for another Tesla LEAPS. My long-term target for the stock is $10,000. Elon actually spends almost no time with Tesla now, it’s basically on autopilot. All his time is going into SpaceX now, which he has a lot more fun with, and which is actually still a private company, so he isn’t restricted with comments about space like he is with comments about Tesla. When you're the richest man in the world you pretty much get to do anything you want as long as you're not subject to regulation by the SEC.

Q: How realistic is it that holiday gatherings will trigger a huge wave of COVID in the United States forcing another lockdown and the Fed to delay a rise in interest rates?

A: I would say there’s a 0% chance of that happening. As I explained earlier, with 90% immunity in much of the country, viruses have a much harder time attacking the population with a new variant. The pandemic is in the process of leaving the stock market, and all I can say is good riddance.

Q: What about the Biden meeting with President Xi and Chinese stocks (FXI)?

A: It’s actually a very positive development; this could be the beginning of the end of the cold war with China and China’s war on capitalism. If that’s true, Chinese stocks are the bargain of the century. However, we’ve had several false green lights already this year, and with stuff like Microsoft (MSFT) rocketing the way it is, I’d rather go for the low-risk high-return trades over the high-risk, high return trades.

Q: What’s your opinion of Zillow (Z)?

A: I actually kind of like it long term, despite their recent disaster and exit from the home-flipping business.

Q: Do you like copper (CPER) for the long term?

A: Yes, because every electric car needs 200 lbs. of copper, and if you’re going from a million units a year to 25 million units a year, that’s a heck of a lot of copper—like three times the total world production right now.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

An Old Fashioned Peloton (a Mountain)

Mad Hedge Technology Letter

November 17, 2021

Fiat Lux

Featured Trade:

(THE TESLA OF PICK-UP TRUCKS)

(RIVN), (AMZN), (TSLA)

Rivian Automotive Inc. (RIVN), the California-based EV company, touched $153 billion in market valuation making Rivian the largest U.S. company with zero revenue.

Exuberance can take you this far, but the company will need to show investors sales after the pixie dust wears off.

I understand that part of the narrative is that this could be the next Tesla (TSLA), and back of the napkin math shows us if it is a certain percentage of Tesla going forward then it would be certain billions of dollars.

The $150 billion valuation is too fast too soon, but when traders grab a hold of this rocket, all they need to do is add a little fuel.

It does speak loudly to investors that there is excess liquidity ebbing and flowing in the financial system where a stock can go this high just based on potential.

Let’s see the damn car first!

Granted, the car looks fantastic based on internet reviews, and if they do become the Tesla of pickup trucks, then anything that means reversion in the stock will be muted.

Word on the street is that only employees are driving the truck around now and the greater public should start receiving their Rivian orders at the end of 2021 or 2022.

EV peer Lucid Group Inc. also rallied intensely closing up 24% and eclipsing the valuation of Ford in the process. Lucid is now a $91 billion company, compared to Ford’s $79 billion.

Rivian will also need to compete with the upcoming European EV behemoths with Volkswagen that is Europe’s largest automaker with about 10 million vehicle deliveries per year, making it the global number two behind Toyota Motor Corp.

Rivian’s trucks are called the R1T and an electric SUV — R1S.

They forecast annual production will hit 150,000 vehicles at its main facility by late 2023.

At one point, Rivian was worth more than almost 90% of S&P 500 companies, including stocks like Goldman Sachs Group Inc., Boeing Co., Citigroup Inc., Starbucks Corp.

Rivian also benefited from Tesla’s Founder Elon Musk selling big tranches of stock which gave EV investors the green light to pile into Rivian even if it’s not for the long term.

Pricing for Rivian’s models starts around $70,000, and each features a base driving range of more than 300 miles on a full charge.

The hope is that mass affluent truck shoppers won’t be able to get enough of Rivian. Remember, the Ford F-150 is the best-selling vehicle in the country. In fact, the top six automobiles in the U.S. by sales are either pickup trucks or SUVs.

Amazon’s 20% stake in the company is the stamp of approval for many investors on the fence and they have already ordered 100,000 units for delivery by the end of 2030.

I could easily see Amazon ramping up orders quickly if they like the quality of the first two models.

Whether the stock should be $150 billion with 0 sales or not, is not really the full story of Rivian.

With only a narrow snapshot of what’s really going on, the high valuation is more a story of the momentum of the market in November that has seen big tech rejuvenate.

Rivian merely just got caught up in the updraft.

I am not diminishing the company, but they will need to demonstrate consistent earnings to build those long-term holders of the stock and I do believe they can do it.

The specs of the car look and feel like a Tesla and if they can replicate 80% of the quality with their first iterations, socially, they could catch on fire and become the new hip car to the masses.

This does set the stage for a critical first earnings report where the first sales will be thoroughly dissected with a fine-tooth comb and possible offer an entry point to investors after people realize this isn’t a $150 billion company yet.

Remember that it took Tesla years to stabilize their volatile stock, and Rivian might have to go through the same right of passage to be legit.

Rivian has the potential to become the #2 behind Tesla and that’s worth $90 billion right there, it’ll be interesting to see what pans out after that.

As for buying the stock, wait for a big sell-off then slowly scale in.

Global Market Comments

November 15, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or PROFITING FROM INFLATION),

($INDU), (TLT), (TBT), (MS), (GS), (BAC), (BRKB), (TSLA)

Worried about inflation?

I’m not. That’s because I know how to trade inflation, which we had in spades during the 1970s when it reached a horrific 18% rate. Those who figured out the game early made fortunes. Those who didn’t got killed.

And what is the best protection against inflation? You own stocks and homes, as much as you can get your hands on.

That’s because in an inflationary environment, companies can raise their prices faster than the inflation rate, which they have been doing since the summer. That’s why we have just seen the best earnings quarter in recent memory and all-time high stock indexes.

Homes do well because there are still 85 million millennials chasing a housing stock that is easily short ten million homes and are given free money to chase prices upward.

I asked a local real estate agent when home prices would slow down and she answered, “it might slow down on Christmas eve and Christmas day, and after that, it will take off again.”

I think home prices will continue to rise for another decade, but not at this year’s ballistic rate.

What about impending rising interest rate, you may ask? They will rise but not enough to hurt either stocks or homes. The pandemic vastly accelerated technology, which we all know is the greatest price destroyer of all time. So, inflation will go up, but from zero to 3%-4%, not the 18% of yore.

And yes, prices are rising for the working classes, those least able to pay them. But the same minimum wage workers are getting the biggest pay hikes in history, up to 100% in some cases, more than offsetting inflation.

And while stocks and homes see rising inflation, bonds don’t. My feeling is that the bond market will stumble across it in the dark some nights and prices will crash. Bonds will keep ignoring inflation until they can’t. The bond vigilantes will then return with a vengeance and are doing their stretching exercises as we speak.

One of the odder things about the past week is that each of the three announcements heralding sharply higher inflation trigger sharp moves up in bonds when they were supposed to go down. That worked until Thursday when the worst 30-year Treasury bond auction since 1990 prompted a $5.00 selloff.

Another bizarre development is that call options are trading at greater premiums than put options, an exceedingly rare event. That means that the consensus for stocks is now almost universally up.

It also means that the at-the-money long-dated LEAPS call option spreads I have been pelting my Concierge members with have become massively profitable. Six months out you can earn eye-popping 100% returns, and 200% in some of the more volatile names, like (ROM) and (MSTR).

The bottom line is that goldilocks is moving in for the long term and might advance to senior citizenship on this watch.

That works for me, so I’m going on a long hike.

The $1.2 Trillion Infrastructure Budget Passes, adding another 6% in GDP growth for the next two years. Construction detours are about to break out all over the country, and the domestic recovery play is on fire. Lost along the way was $550 million in social spending. No increase in corporate taxes sets up a perfect storm for stocks the next several months. Stay fully invested as I begged you to do weeks ago.

The US Reopens, provided you have two Covid shots and a test within the last three days. Got to keep those pesky diseased foreigners out! Hotels, airlines, casinos, and cruise lines took off like a scalded chimp, taking the indexes to new all-time highs. Buy (ALK) and (LUV) on dips.

The Bitcoin Rally Continues, with new all-time highs for both (BITO) and (ETHE). Concerns about the monetary health of the US are rising ahead of a major debt ceiling fight in Congress in December.

Inflation Soars with a Red Hot 6.2% CPI Print in October, the highest in 31 years. Energy, rent, and car costs led the gains. Bitcoin (BITO) and Ethereum (ETHE) jumped to new all-time highs in response. This is only going to get better. You can now count on a Fed interest rate hike in June.

The Disappearing Worker Trend Continues, with a record 4.4 million quitting in September. Workers are taking advantage of the labor shortage to switch jobs for higher wages. This will get worse before it gets better. Good luck trying to hire anyone.

US Consumer Sentiment Hits Ten-Year Low, down from 71.7 to 68.6 in October, according to the University of Michigan. Inflation at a 30-year high 6.2% is starting to hit consumers hard.

Elon Musk Tesla Sales Top $5.1 billion, to pay off Uncle Sam. That must be one hell of a tax bill. At this rate, the market is rapidly running out of the sole seller. Buy (TSLA) on dips.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch saw a massive +8.95% gain in October, followed by a decent 4.42% so far in November. My 2021 year-to-date performance moved to a new high of 92.97%. The Dow Average is up 18.00% so far in 2021.

After the recent ballistic move in the market, we got a week of consolidation which brought some generalized bitching, moaning, and wining.

I am continuing to run my longs in. Those include (MS), (GS), (BAC), (BRKB), and a short in the (TLT). The (TLT) short brought some hair-raising moments when we got a $3.00 spike up in the wake of the red hot 6.2% CPI release. I knew it was a complete BS move and successfully stared it down, watching it all reverse the next day. I don’t do this very often.

All positions are now approaching their maximum profit point and we have nothing left but time decay to capture. So, I am going to run these into the November 19 expiration in 4 trading days and capture all the accelerated time decay.

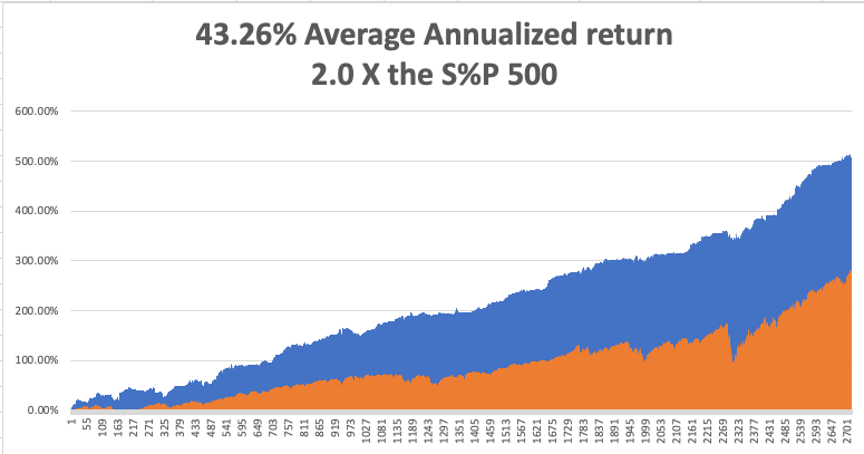

That brings my 12-year total return to 515.52%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return has ratcheted up to 43.26%, easily the highest in the industry.

My trailing one-year return popped back to positively eye-popping 112.08%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 47 million and rising quickly and deaths topping 763,000, which you can find here.

The coming week will be all about the inflation numbers.

On Monday, November 15 at 9:00 AM, the New York Empire State Manufacturing Index for November is released. WeWork reports.

On Tuesday, November 16 at 8:30 AM, US Retail Sales for October are printed. Home Depot (HD) and Walmart (WMT) report.

On Wednesday, November 17 at 8:30 AM, the Housing Starts and Building Permits for October are published. NVIDIA (NVDA) and Cisco Systems (CSCO) report.

On Thursday, November 18 at 8:30 AM, Weekly Jobless Claims are announced. The Philadelphia Fed Manufacturing Index is printed. Macy's (M) and Alibaba (BABA) report.

On Friday, November 19 at 2:00 PM, the Baker Hughes Oil Rig Count are disclosed.

As for me, I am sitting in the Centurion Lounge in San Francisco Airport waiting for a United flight to Las Vegas where I have to speak at an investment conference. I have time to kill so I will reach back into the deep dark year of 1968 in Sweden.

My trip to Europe was supposed to limit me to staying with a family friend, Pat, in Brighton, England for the summer. His family lived in impoverished council housing.

I remember that you had to put a ten pence coin into the hot water heater for a shower, which inevitably ran out when you were fully soaped up. The trick was to insert another ten pence without getting soap in your eyes.

After a week there, we decided the gravel beach and the games arcade on Brighton Pier were pretty boring, so we decided to hitchhike to Paris.

Once there, Pat met a beautiful English girl named Sandy, and they both took off for some obscure Greek island, the ultimate destination if you lived in a cold, foggy country.

That left me stranded in Paris.

So, I hitchhiked to Sweden to meet up with a girl I had run into while she was studying English in Brighton. It was a long trip north of Stockholm, but I eventually made it.

When I finally arrived, I was met at the front door by her boyfriend, a 6’6” Swedish weightlifter. That night found me bedding down in a birch forest in my sleeping bag to ward off the mosquitoes which hovered in clouds.

I started hitchhiking to Berlin, Germany the next day. I was picked up by Ronny Carlson in a beat-up white Volkswagen bug to make the all-night drive to Goteborg where I could catch the ferry to Denmark.

1968 was the year that Sweden switched from driving English style on the left to the right. There were signs every few miles with a big letter “H”, which stood for “hurger”, or right. The problem was that after 11:00 PM, everyone in the country was drunk and forgot what side of the road to drive on.

Two guys on a motorcycle driving at least 80 pulled out to pass a semi-truck on a curve and slammed head on to us, then were thrown under the wheels of the semi. The driver was killed instantly, and his passenger had both legs cut off at the knees.

As for me, our front left wheel was sheared off and we shot off the mountain road, rolled a few times, and was stopped by this enormous pine tree.

The motorcycle riders got the two spots in the only ambulance. A police car took me to a hospital in Goteborg and whenever we hit a bump in the road, bolts of pain shot across my chest and neck.

I woke up in the hospital the next day, with a compound fracture of my neck, a dislocated collar bone, and paralyzed from the waist down. The hospital called my mom after booking the call 16 hours in advance and told me I might never walk again. She later told me it was the worst day of her life.

Tall blonde Swedish nurses gave me sponge baths and delighted in teaching me to say Swedish swear words and then laughing uproariously when I made the attempt.

Sweden had a National Healthcare system then called Scandia, so it was all free.

Decades later, a Marine Corp post-traumatic stress psychiatrist told me that this is where I obtained my obsession with tall, blond women with foreign accents.

I thought everyone had that problem.

I ended up spending a month there. The TV was only in Swedish, and after an extensive search, they turned up only one book in English, Madame Bovary. I read it four times but still don’t get the ending.

The only problem was sleeping because I had to share my room with the guy who lost his legs in the accident. He screamed all night because they wouldn’t give him any morphine.

When I was released, Ronny picked me up and I ended up spending another week at his home, sailing off the Swedish west coast. Then I took off for Berlin to get a job since I was broke.

I ended up recovering completely. But to this day whenever I buy a new Brioni suit in Milan, they have to measure me twice because the numbers come out so odd. My bones never returned to their pre-accident position and my right arm is an inch longer than my left. The compound fracture still shows upon X-rays.

And I still have this obsession with tall, blond women with foreign accents.

Go figure.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Brighton 1968

Ronny Carlson in Sweden

Global Market Comments

November 5, 2021

Fiat Lux

Featured Trade:

(NOVEMBER 3 BIWEEKLY STRATEGY WEBINAR Q&A),

(BRKB), (COIN), (IWM), (GOOGL), (MSFT), (MS), (GS), (JPM),

(BABA), (BIDU), (JD), (ROM), (PYPL), (FXE), (FXA), (FXB), (CRSP), (TSLA), (FXI), (BITO), (ETHE), (TLT), (TBT), (BITO), (CGW)

Below please find subscribers’ Q&A for the November 3 Mad Hedge Fund Trader Global Strategy Webinar broadcast from the safety of Silicon

Valley.

Q: Have you considered buying Coinbase (COIN)?

A: Yes, we actually recommended it as part of our Bitcoin service in the early days back in July. It’s gone up 62% since then, right along with the Bitcoin move itself. So yeah, buy (COIN) on dips—and there will be dips because it will be at least triple the volatility of the main market. And be sure to dollar cost average.

Q: Do you think the breakout in small caps (IWM) will hold and, if so, should we focus on small-c growth?

A: Yes it will hold, but no I would focus on the big cap barbells, which will lead this rally for the next 6 months. And there you’re talking about the best of tech which is Google (GOOGL) and Microsoft (MSFT), and the best of financials which is Morgan Stanley (MS), Goldman Sachs (GS), and JP Morgan (JPM).

Q: Why not time the webinar for after the FOMC? What will be the market reaction?

A: Well, first of all, we already know what they’re going to say—it’s been heavily leaked in the last week. The market reaction will be initially a potential sharp down move that lasts a few minutes or hours, and then we start a grind up for the next two months. So that's why I wanted to be 80% leverage long going into this. Second, we have broadcast this webinar at the same time for the last 13 years and if we change the time we will lose half our customers.

Q: Why do you always do debit spreads?

A: They’re easier for beginners to understand. That’s the only reason. If you’re sophisticated enough to do a credit spread, the results will be the same but the liquidity will be slightly better, and you can also apply that credit to meet your margin requirements. We have a lot of basic beginners signing up for our service in addition to seasoned pros and I always encourage people to do what they're most comfortable with.

Q: Are you still comfortable with the Morgan Stanley (MS) and Berkshire Hathaway (BRKB) positions?

A: I expect both to go up 10-20% by March, so that’s pretty comfortable. By the way, if you have extremely deep in the money call spreads on Goldman Sachs or Morgan, consider taking profits on those and rolling your strikes up. If you have like the $360-$380 vertical bull call spread in Goldman Sachs, realize that gain and roll up to the $420-$430 March position in Goldman Sachs—that will give you another 100% profit by March. With the $360-$ 380s, you have like 97% of the profit already in the price, there’s no leverage left and no point in continuing, you can only go down.

Q: What should I do with my China position?

A: Sell all your positions in China, realize all the losses now so you can offset those with all the huge profits on all your other positions this year. There I’m talking about Ali Baba (BABA), Baidu (BIDU), and (JD), which have been absolutely hammered anywhere from down 50% to down 70%. And do it now before everyone else does it for the same reasons.

Q: Thoughts on Paypal (PYPL) lately?

A: The stock is out of favor as money is moving out of PayPal into newer fintech stocks. The move down is totally unjustified and screaming long term buy here, but for the short-term investors are going to raid the piggy bank, sell the PayPal, and go into the newer apps. This has been my biggest money-losing trade personally this year because PayPal long-term has a great story.

Q: Will earnings fall off next year due to prior year comparisons or supply chain?

A: No, if anything, earnings are accelerating because supply chain problems mean you can charge customers whatever you want and therefore increase margins, which is why the stock market is going up.

Q: Long term, what would your wrong strikes be?

A: I would say don’t get greedy. I’m doing the ProShares Ultra Technology (ROM) $120-$125 call spread for May expiration—the longest expiration they offer. That gives you about 100% return in 6 months; 100% is good enough for me because then I’ll do the same thing again in May and get another 100%. What’s 100% x 100%? It’s 400% because you’re reinvesting a much larger capital base the second time around. If a 100% profit in six months is not enough for you then you are in the wrong line of business.

Q: Do you think Ethereum (ETHE) has long-term potential upside?

A: Yes, is a 10X move enough? We just had a major new high in Ethereum because they made moves to limit the production of new Ethereum. Ethereum is the superior technology because its architecture avoids the code repeats that Bitcoin does and therefore only uses a third of the electricity to create. But Bitcoin is attracting the big institutional cash flows because they have an early mover advantage. By the way, how much electricity does crypto mining consume? The entire consumption of Washington state in a year, so it’s a big deal.

Q: What should I do about Crisper Therapeutics (CRSP)?

Crispr Therapeutics (CRSP) is my other disaster for this year because ignored the move up to $170—we’re now back into the $90’s again. So, I have 2023 LEAPS on that; I’m going to keep them, I’ve already suffered the damage, but the next time it goes up to $170 I’m selling! Once burned, twice forewarned. And part of the problem with the whole biotech sector is we are now in the back end of the pandemic and anything healthcare-related will get hit, except for the vaccine stocks like Pfizer (PFE) which are still making billions and billions of dollars.

Q: I bought Baidu (BIDU) and Alibaba (BABA) years ago at a much lower price and I'm still up quite a lot; what should I do?

A: If you have the big cushion, I would keep them and look for #1 recovery in the Chinese economy next year and #2 for the government to back off from their idiotic anticapitalism strategy because it’s costing them so much money.

Q: Is Robinhood (HOOD) a good LEAP candidate?

A: Only on a really big dip, and then you want to go out two years. With a stock that’s volatile as hell like Robinhood and could drop by half on no notice, so you only buy the big dips. It’s not a slowly grinding upward stock like Goldman Sachs (GS) and Morgan Stanley (MS) where you can add LEAPS now because you know it’s going to keep grinding up.

Q: How can Morgan Stanley go up when the chief strategist is bearish?

A: Their customers aren't listening to their chief strategist—they’re buying. And the volume of the stock, which is where Morgan Stanley makes money, is going through the roof, they’re making record profits there. And I've got Morgan Stanley stock coming out of my ears in LEAPS and so forth.

Q: What are 5 stocks you would buy right now?

A: Easy: Google (GOOGL), Microsoft (MSFT), Morgan Stanley (MS), Goldman Sachs (GS), and JP Morgan (JPM). Buy whatever is down that day. They’re all going up.

Q: Too late to buy Tesla (TSLA) calls?

A: Yes, it is. Tesla has a long history of 40% corrections; we had one that ended in May, and then it doubled (and then some). So yeah, too late to buy the calls here. Go back and read my research from May which said buy the stock and you get a car for free—and that worked again, except this time, you can get three free Tesla’s. A lot of subscribers have sent me pictures of their Teslas they got for free on my advice; I’m probably the largest salesman for Tesla for the last 10 years and all I got out of it was a free Powerwall (the red one)..

Q: How much higher do you think semiconductor companies will go?

A: Higher but it’s impossible to quantify. You’re getting very speculative short-term buying in there. So, I think it continues to the rest of the year, but with chips, you never know.

Q: Would you be buying Crispr Therapeutics (CRSP) at these levels?

A: Yes, but I would either just buy the stock and not be dependent on the calendar or buy a 2 ½ year LEAP and get an easy double on that.

Q: What about the currencies?

A: I don’t see much action in the currencies as long as the US is raising interest rates. I think the Euro (FXE), the Aussie (FXA), and the British pound (FXB) will be dead for the time being. Nobody wants to sell them but nobody wants to buy them either when you’re looking at a potential short term rise in the dollar from rising interest rates.

Q: What stable coins are the right answer for cryptocurrency?

A: The US dollar stable coin, but for price appreciation, you’re really looking at Bitcoin and Ethereum. Stable coins are stable, they don’t move; you want stuff that’s going to go up 5, 10, or 20 times over the next 10 years like Bitcoin (BITO) and Ethereum (ETHE). That is my crypto answer.

Q: What should I do about the iShares 20 Plus Year Treasury Bond ETF (TLT) $135-$140 put spread expiring in January?

A: If we get another run down to the $141 level that we saw last month, I would come out of all short treasury positions because you’re starting to run into time decay problems with the January expirations. And in case we remain in a range for some reason, I would be taking profits at the bottom end of the range. It was my mistake that I didn’t grab those profits when we hit $141 last time. So don’t let profits grow hair on them, they tend to disappear. We lost six months on this trade due to the delta virus and the mini-recession it brought us.

Q: Will there be accelerated tech selling in December because of the new tax rates?

A: What new tax rates? There has been no new tax bill passed and even if there were, I think people wouldn’t tax sell this year because the profits are enormous. They would rather do any selling in January at higher prices and then defer payment of those taxes by 18 months. I don’t think there will be any tax issues this year at all.

Q: What’s your return on solar power investments?

A: My break-even was four years because our local utility, PG&E, went bankrupt and the only way they're getting out of bankruptcy is raising electricity prices by 10% a year. It turns out that as a result of global warming, the panels have operated at a higher efficiency as well, so we’re getting a lot more power output than originally expected. Now I get free electricity for the remaining 20-year life of the panels which is great because with two Tesla’s and all-electric heating and air conditioning I use a lot of juice. My monthly bill is a sight to behold. I also power the 20 surrounding houses and for that PG&E pays me $1,800 a month.

Q: Do you see China (FXI) invading Taiwan as a potential threat to the market?

A: China will never invade Taiwan. They own many of the companies they're already in, they de facto control Taiwan government from a distance; they would not risk the international consequences of an actual invasion. And we have the US seventh fleet there to stop exactly that. So, they can make all the noise they want but nothing will come of it. I’ve been watching this for 50 years and nothing has ever happened.

Q: Would you buy ProShares Ultrashort 20+ Treasury ETF (TBT) here?

A: Absolutely, with both hands, all I can get.

Q: Can you recommend any water ETF opportunity?

A: Yes there is one I wrote a piece on last month. It’s the Claymore S&P Global Water Index ETF (CGW).

Q: How long can you hold the (TBT) before time decay hurts?

A: It doesn’t hurt, the cost of the TBT is two times the 10-year rate. So that would be 3%, plus 1% a year for management fees, and that’s your slippage on the TBT in a year right now—it’s 4%. Remember if you’re short the bond market, you have to pay the coupon when you’re short. Double the bond market and you have to pay double the coupon.

Q: Is the ProShares Bitcoin Strategy ETF (BITO) a good alternative to buying bitcoin?

A: I would say yes because I’ve been watching the tracking on that very carefully and it’s pretty damn close. Plus there’s a lot of liquidity there, so yeah, buy the (BITO) ETF on dips and dollar cost average.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

November 1, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or LET THE GAMES BEGIN!)

(MS), (GS), (BLK), (JPM), (BAC), (TLT), (TSLA), (AAPL), (MSFT), (GOOGL), (AMZN), (ROM)

Welcome to the first day of November, when the seasonals swing from negative to positive. The hard six months are over. The next six should be like shooting fish in a barrel.

At least that’s what happened in the past. The period from November 1 to May 31 has delivered the highest stock returns for the past 75 years.

So how do we play a hand that we have already been dealt full of aces and kings?

Load the boat with financials, like (MS), (GS), (BLK), (JPM), and (BAC). Notice that when we had the sharpest rise in interest rates in a year, financials barely moved when they should have crashed? That means they will soon start going up again.

You might have also observed that technology stock has been flat-lining when rising rates should have floored them. That means their torrid 20% earnings growth will keep floating their boats.

It gets better. We just learned that the GDP growth rate plunged in Q3 from a rip-roaring 6% rate to only 2%. What happens next? That 4% wasn’t lost, just deferred into 2022. The rip-roaring 6% growth rate returns. That’s why stocks are pushing up to new all-time highs right now.

So, buy the dips. We may have seen our last 5% correction of 2021. The only unknown is how markets will react to a Fed taper, which could come as early as Wednesday. But on the heels of that, we will get a $1.75 billion rescue package, the biggest in 50 years. One will cancel out the other, and then some.

Take a look at the ProShares Ultra Technology Fund (ROM), the 2X long ETF. I just analyzed its 30 largest holdings. Half are tech stocks that have been trash and are down 30% or more. The other half are at all-times highs, like Microsoft (MSFT) and Alphabet (GOOGL).

What happens next when the seasonals are a tailwind? The tech stocks that are down will rally because they are cheap, while the high stocks keep going because they are best of breed. I think (ROM) has $150 written all over it by March.

You’ve got to love Elon Musk, whose net worth is approaching $300 billion. When the pandemic broke, every automaker cancelled their chip orders for the rest of the year while Tesla took them all. Today, Detroit has millions of cars built but in storage because they are all missing chips. In the meantime, Tesla is snagging orders for 100,000 cars at a time.

Like I say, you gotta love Musk. Hey, Elon, call me! Why don’t you just buy the entire US coal industry and shut it down. It would only cost $5 billion, as market caps are so low. That would have more impact on the environment than another million Teslas. Worst affected would be China, where 70% of US coal now goes.

A continued major driver of the bull case for stocks is profit margins of historic proportions.

Q1 saw a 13% margin, Q2 13.5% and Q3 12.3%, and Q3 had to carry the dead weight of a delta impaired GDP growth rate of only 2.0%. Imagine what companies can do in Q4 when the growth rate is returning to a torrid 6% rate.

This has been one of my basic assumptions for the entire year and it seems it was I was alone in having it. This is where the 90% year-to-date performance comes from.

Inflation is Here to Stay, says top investing heavyweights, at least 4% through 2022. That means high inflation, higher financial shares, and higher Bitcoin prices. It’s going to take two years to unwind the mess at the ports that is driving prices.

Covid is Getting Knocked Out by a One-Two Punch, via a new round of booster shots and imminent childhood vaccinations. It could take new cases to zero in a year and give us a booming economy.

S&P Case Shiller is Still Rocketing, the National Home Price Index up 19.8% YOY in August. Phoenix (33.3%), San Diego (26.2%), and Tampa (25.9%) were the hot cities. This will continue for a decade but as a slower rate.

New Home Sales Pop, to 800,000. Annual median prices jump at an annual 18.7% to $408,000. The share of homes selling over $1 million increased from 5% to 9% in a year. It cost $500,000 to get a starter home in an Oakland slum these days. Homebuilders Sentiment Soars to 80. Buy (KBH), (PUL), and (LEN) on dips.

Bonds Melt Up, creating one of the best trade entry points of the year. A successful 30-year auction this week that took yields from 1.71% down to 1.52% in a heartbeat. It makes no sense. Buying bonds here is like buying oil in the full knowledge that someday it will go to zero. I am doubling my short position here. Look at the (TLT) December 2022 $150-$155 vertical bear put spread LEAPS which is offering a 14-month return of 54%. This is the month when the Fed has promised to begin the first of six interest rate hikes. Just buy it and forget about it.

Proof that the Roaring Twenties is Here. It’s demand that is spiking, the greatest ever seen, not supplies that are drying up in the supply chain issue. It should continue for a decade and the bull market in stocks that follows it. You heard it here first. Dow 240,000 here we come.

Apple Blows it in Q3, with millions of its phones lost at sea and no idea when unloads are possible, costing it $6 billion in sales. Revenues were up a ballistic 29% YOY. Buy (AAPL) on dips. I see $200 a year next year.

Amazon Craters, with both shrinking revenues and profits. Supply chain problems about with several billion of inventory trapped at sea off the coast of Long Beach. It plans to hire 275,000 to handle the Christmas rush. The stock hit a one year low. There is a time to buy (AMZN) on the dip, but not quite yet.

My Ten Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch saw a massive +8.95% gain in =October. My 2021 year-to-date performance maintained 88.55%. The Dow Average is up 17.06% so far in 2021.

After the recent ballistic move in the market, I am continuing to run my longs in Those include (MS), (GS), (BAC), and a short in the (TLT). All are approaching their maximum profit point and we have nothing left but time decay to capture. So, I am going to run these into the November 19 expiration in 14 trading days. It’s like have a rich uncle write you a check one a day.

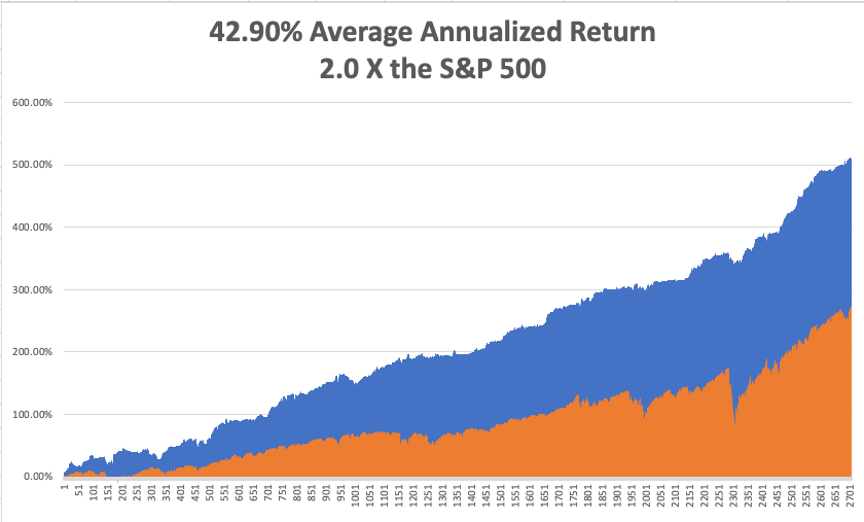

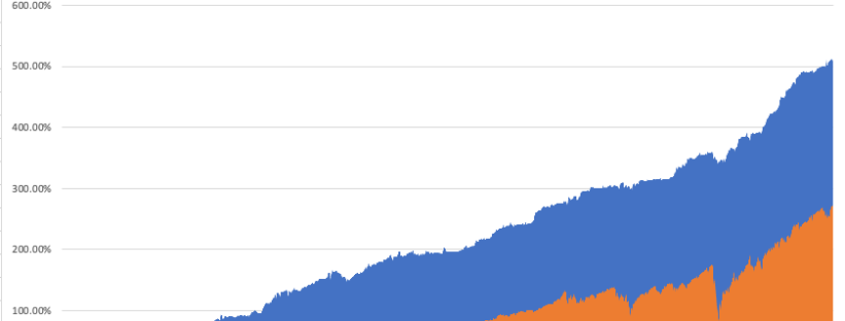

That brings my 12-year total return to 511.10%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 42.90%, easily the highest in the industry.

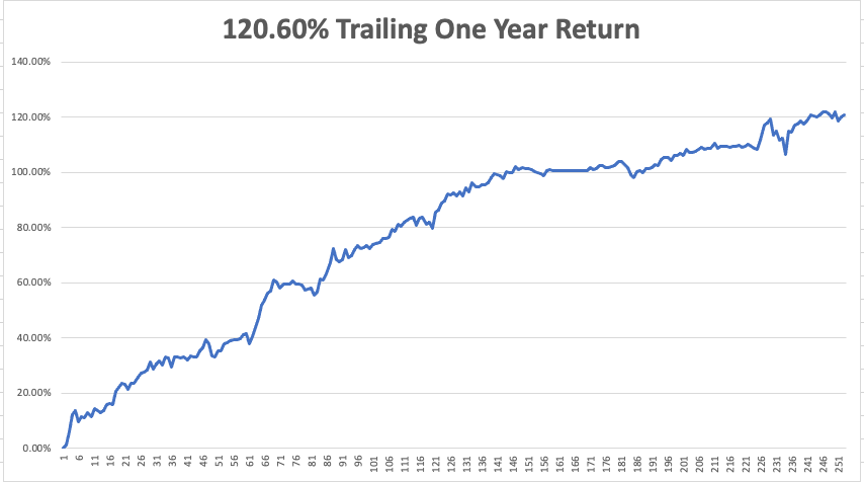

My trailing one-year return popped back to positively eye-popping 120.60%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 46 million and rising quickly and deaths topping 746,000, which you can find here.

The coming week will be slow on the data front.

On Monday, November 1 at 7:00 AM, the ISM Manufacturing PMI for October is out. Avis (CAR) Reports.

On Tuesday, November 2 at 1:30 PM, the API Crude Oil Stocks are released. Pfizer (PFE) reports.

On Wednesday, November 3 at 7:30 AM, the Private Sector Payroll Report is published. Etsy (ETSY) reports. At 11:00 AM, the Federal Reserve interest rate decision is announced, followed by a press conference.

On Thursday, November 4 at 8:30 AM, Weekly Jobless Claims are announced. Airbnb reports (ABNB).

On Friday, November 5 at 8:30 AM, The October Nonfarm Payroll Report is released. DraftKings (DKNG) reports. At 2:00 PM, the Baker Hughes Oil Rig Count are disclosed.

As for me, I have been known to occasionally overreach myself, and a trip to the bottom of the Grand Canyon a few years ago was a classic example.

I have done this trip many times before. Hike down the Kaibab Trail, follow the Colorado River for two miles, and then climb 5,000 feet back up the Bright Angle Trail for a total day trip of 27 miles.

I started early, carrying 36 pounds of water for myself and a companion. Near the bottom, there was a National Park sign stating that “Being Tired is Not a Reason to Call 911.” But I wasn’t worried.

The scenery was magnificent, the colors were brilliant, and each 1,000 foot descent revealed a new geologic age. I began the long slog back to the south rim.

As the sun set, it was clear that we weren’t going to make to the top. I was passed by a couple who RAN the entire route who told me “better hurry up.” I realized that I had erred in calculating the sunset, it'staking place an hour earlier in Arizona than in California.

By 8:00 PM it was pitch dark, the trail had completely iced up, and it was 500 feet straight down over the side. I only had 500 feet to go but the batteries on my flashlight died. I resigned myself to spending the night on the cliff face in freezing temperatures.

Then I saw three flashlights in the distance. Some 30 minutes later, I was approached by three Austrian Boy Scouts in full dress uniform. I mentioned I was a Scoutmaster and they offered to help us up.

I grabbed the belt of the last one, my companion grabbed my belt, and they hauled us up in the darkness. We made it to the top and I said, “thank you”, giving them the international scout secret handshake.

It turned out that I wasn’t in great shape as I thought I was. In fact, I hadn’t done the hike since I was a scout myself 30 years earlier. I couldn’t walk for three days.

Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Happy Halloween!