Global Market Comments

March 23, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WELCOME TO THE GREAT DEPRESSION),

(INDU), (SPY), (GS), (MS), (FXI), (USO), (TSLA)

Global Market Comments

March 23, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WELCOME TO THE GREAT DEPRESSION),

(INDU), (SPY), (GS), (MS), (FXI), (USO), (TSLA)

The neighborhood is alive with power tools.

These are the implements that were given as Christmas presents to dads years ago. But to afford life in the San Francisco Bay Area said dads have to work 12 hours a day and weekends. Now, suddenly they have all the free time in the world and those ancient gifts are coming out of decade-old original packaging.

I’ve noticed something else about my neighborhood. People have suddenly started to turn gray. Beauty salon appointments have been banned for weeks, not designated essential businesses.

The GDP forecasts released by Goldman Sachs (MS) last week have been turning a lot of other people gray as well. Q1 is thought to show a -6% annualized shrinkage and Q2 is expected to come in at -24%. The unemployment rate will peak at 9%. Not to be outdone, Morgan Stanley (MS) cut their Q2 forecast to -30%.

That means America’s GDP will shrink to the 2016 level of $18.62 trillion, down enormously from today’s $21.5 trillion. Yes, three years of economic growth will be gone in a puff of smoke. These are far worse than the last Great Recession when the worst two quarters came in at -2% and -8%. That’s double the worst figures of the Great Recession.

In the meantime, vast swaths of the American economy are moving online, never to return.

The good news is that growth will return at a historic 12% rate in Q3. That sets up an exaggerated “V” for the stock market. How soon should you start buying stocks if this economic scenario plays out? Probably a month, if not weeks, but only if you have the courage to do so.

The numbers from China (FXI) this week are very encouraging, showing no increase in new cases. In February, they enacted the kind of severe lockdown which California enacted a week ago.

Hopefully, that means we will get the Chinese results in a month or two. But the problem is that these are Chinese numbers that may be intended more to please the government than shed light on the truth.

The first real look we get at the effectiveness of lockdown may be in Italy in a few weeks, which has been quarantined since February.

In the US, the states have abandoned all hope of help from Washington and are leading the charge with the most aggressive measures. In California, it is now illegal for 40 million people to go outside unless it is a trip to the grocery store, the pharmacy, or the doctor.

The Golden State is now on a WWII footing. Tesla (TSLA) is switching production to ventilators. The state national guard is setting up field hospitals in parks. I am growing my own victory garden in the back yard.

The state is seeking to double the number of hospital beds to 20,000 within weeks. It just bought an entire hospital in Oakland, Seton Hospital. It went bankrupt last year and the administrators couldn’t give it away. The state i taking control of abandoned college dormitories and leasing empty hotels and cruise ships.

I expect food rationing to hit in a month. The distribution system is strained but working now. It may start to fail in April or May when large numbers of workers get sick.

The good news is that shelter in place should work, possibly by May. Kids are out of school until August.

With Trump refusing to put the entire country on lockdown that raises the specter of those in red states dying, while those in blue ones live. The big blue states of New York, California, New Jersey, Connecticut, and Illinois were the first to order shelter-in-place and will certainly see lower and sooner peaks in disease and fatalities.

And guess who has a one-month supply of Chloroquine, along with antibiotics widely believed to be a cure for the Coronavirus? That would be me, who bought them to fight off malaria for my trip to Guadalcanal six weeks ago. I was planning on going back in June to collect more dog tags for the Marine Corps, so I have an extra supply. As long as you can read, I’ll still be writing.

There is one more unexpected aspect of the pandemic and the shelter-in-place orders. I expect a baby boom to ensue in about nine months, thanks to all this enforced togetherness. The US birth rate has been falling for decades and is now well below the replacement rate. It’s about time we found a way to turn it around. Just don’t count me in on this one. I already have five kids.

So, you’re still asking for a market bottom.

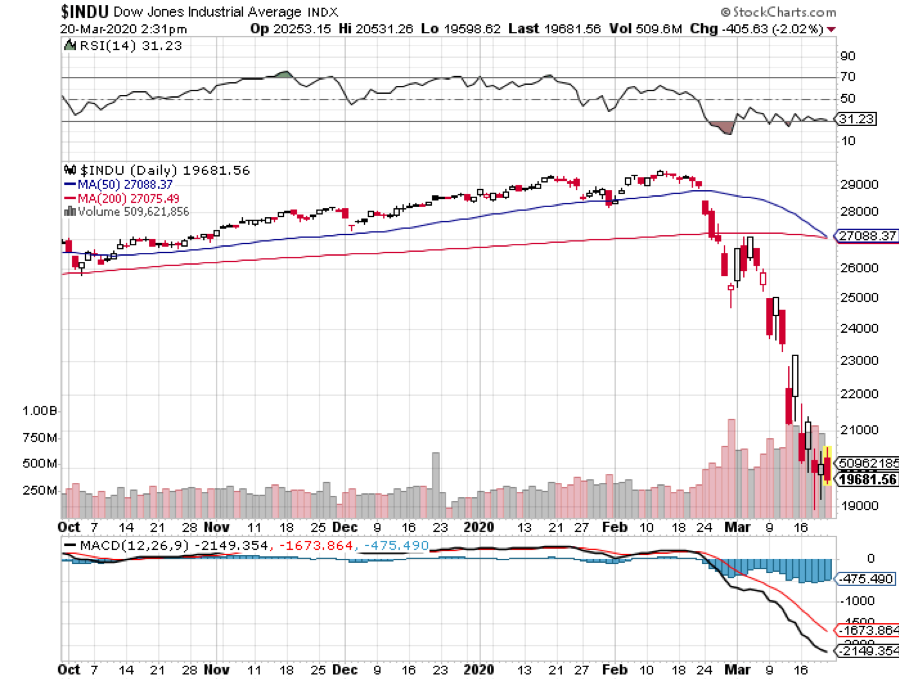

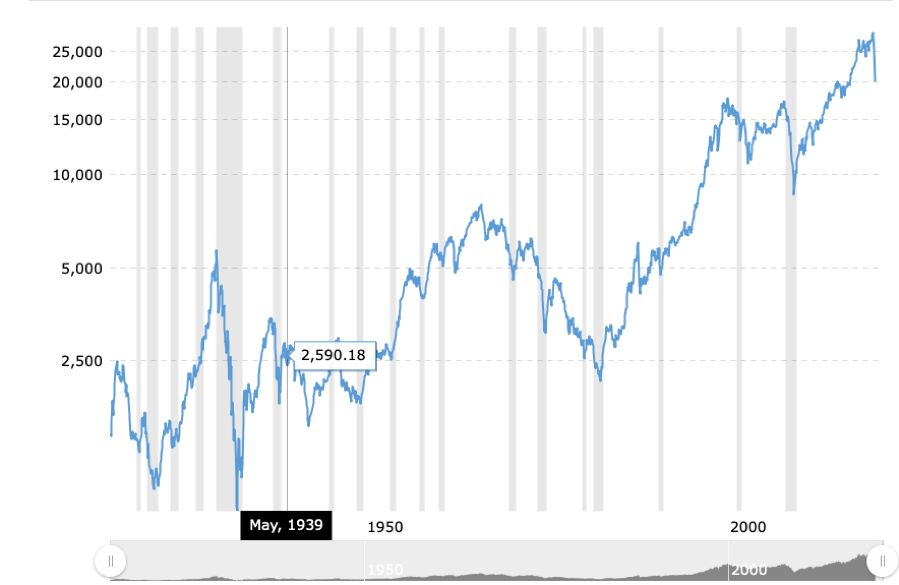

The futures in Asia are limit down as I write this, just above the Dow Average 17,000 handle (INDU), thanks to the Senate failure to pass a virus rescue bill. Near 15,000 seems within range, down 49% from the February high. Modern history is no longer relevant here. We have to go back to 1929 to see numbers this extreme. I’ll be doing the research on that in the coming days.

The 1987 crash was already revisited a week ago, with a 3,000-point plunge in the Dow Average, or 12%. Some 33 years ago, we saw a 20% single day haircut, which I remember too well. This is with the Federal Reserve throwing everything at the stock market but the kitchen sink. I never thought I’d live long enough to see another one of these.

The Fed took interest rates to zero to stave off a depression, but the stock market crashes in overnight trading anyway. That brings the total to 150 basis points in cuts in five days. The Treasury is to buy an eye-popping $700 billion in mortgage securities to clear out the refi market for the first time in a decade. The Fed has just fired its last bullets to save stocks.

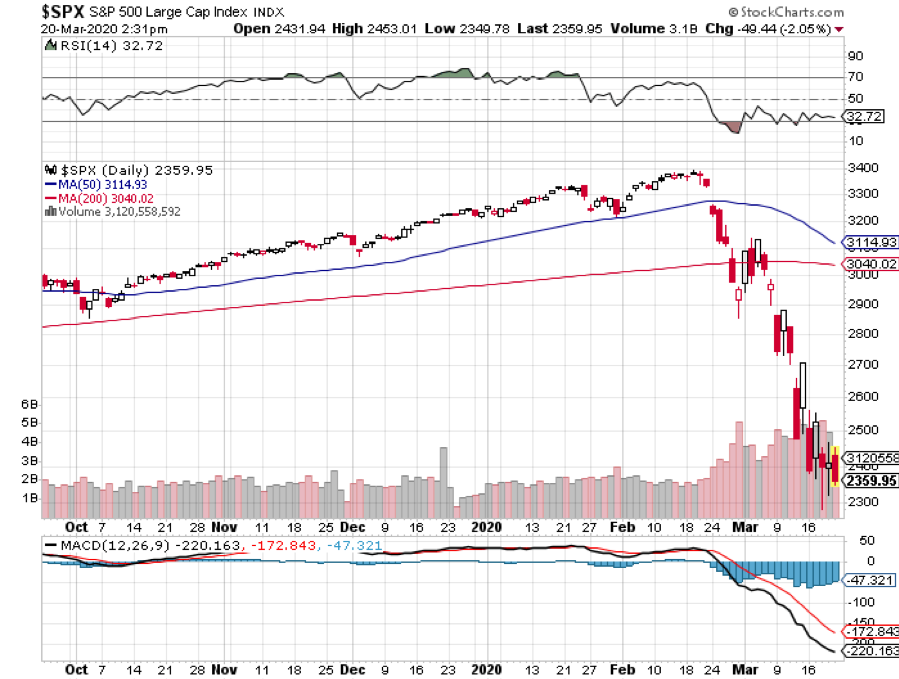

Goldman Sachs is targeting 2,000 in the (SPX), down 10% from here and 41% from the top. That is a 14X multiple on a 2020 S&P 500 earnings decline from $165 to $143. Yes, it’s just a guess. Investors could care less now about fundamentals or technicals. Cash is king.

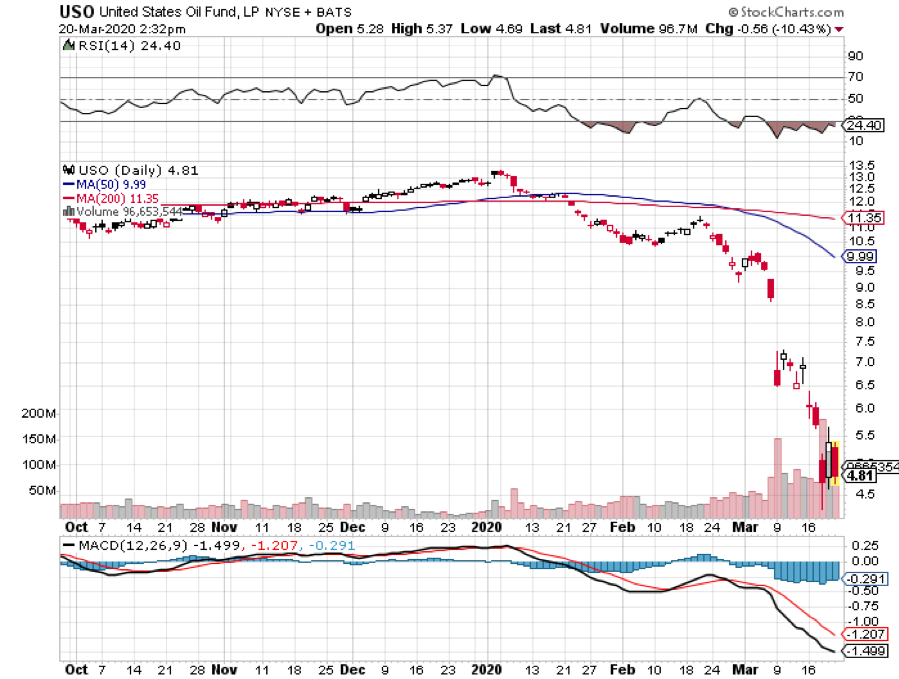

Oil (USO) is headed for the teens. Saudi Arabia is ramping up production to a record 13 million barrels a day. The recession is collapsing US demand from 20 to 15 million b/d, half of which is consumed by transportation.

Russian national income has just collapsed by 75%. Will there by a second Russian Revolution? The 3% of the US market capitalization accounted for by energy stocks will drop below 1%. Fill her up! Avoid energy, even though some are going for pennies on the dollar.

The only data point that counts now is the daily real-time Corona tally of cases and deaths from Johns Hopkins, (click here). All other economic data is now irrelevant. Right now we are at 335,997 cases worldwide and 14,641 deaths. The US is at a frightening 33,276 cases as of writing.

Insider buying is exploding, with CEOs picking up their own stocks at 50%-70% discounts. Charles Scarf, president of Wells Fargo, just bought $5 million worth of (WFC) down 52% from the recent top. This is a legendary indicator that we may be within weeks of a market bottom.

The New York Stock Exchange closes its floor trading operations last week after several members tested positive for the Corona virus. Online trading will continue, where 95% of the business migrated years ago. It’s really just a TV stage now.

It’s all about hedge funds, triggering the massive volatility of the past month. They have been unwinding massive positions with up to 13X leverage in illiquid markets that can’t handle the massive volume.

When the last hedge fund is liquidated, the market will go up and the (VIX) will collapse. They may have started and the (VIX) plunged an incredible 25 points in hours.

Trump asked states to keep unemployment data secret to minimize market impact. Just what we need, less information, not more. The Weekly Jobless Claims were a bombshell, adding 70,000 to 271,000, the sharpest increase in a decade. Look for far worse to come in coming weeks as whole industries are shut down, and state unemployment computers explode from the weight of applications. Jobless Claims over 2 million are imminent!

Existing Home Sales soared by a stunning 6.5% in February, a 13-year high. The West saw an amazing 17% increase. The median home price jumped by 8% YOY. While the data is great, it’s all pre-Corona. It is illegal for people to go out to look at homes in many states, and no one wants to sell to keep strangers out of the house.

When we come out on the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates at zero, oil at $20 a barrel, and many stocks down by three quarters, there will be no reason not to.

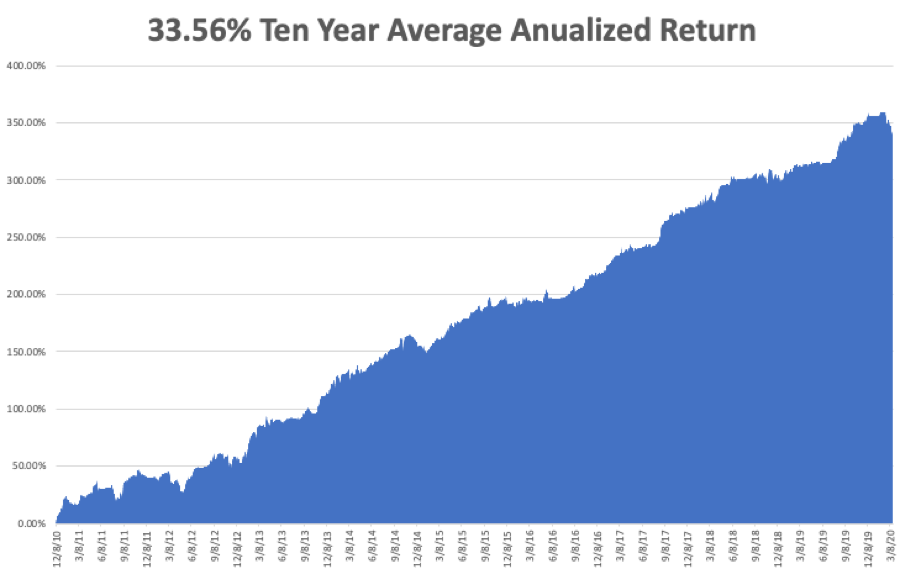

My Global Trading Dispatch performance has had a great week, thanks to the collapse in market volatility, pulling back by -8.22% in March, taking my 2020 YTD return down to -11.14%. That compares to an incredible loss for the Dow Average of -37% at the Friday low. My trailing one-year return was pared back to 31.68%. My ten-year average annualized profit shrank to +33.56%.

I have been fighting a battle for the ages on a daily basis to limit my losses. My goal here is to make it back big time when the market comes roaring back in the second half.

My short volatility positions have largely recovered. I shorted the (VXX) when the Volatility Index (VIX) was at $35. It then went to an unbelievable $80 before falling back to $55. I was saved by only trading in very long maturity, very deep out-of-the-money (VXX) put options where time value will maintain a lot of their value. Now, we have time decay working in our favor. These will all come good well before their one-year expiration.

At the slightest sign of a break in the pandemic, the economy and shares should come roaring back. Right now, I have a 70% cash position.

On Monday, March 23 at 7:30 AM, the Chicago Fed National Activity Index is out.

On Tuesday, March 24 at 9:00 AM, the New Home Sales for February are released.

On Wednesday, March 25, at 7:30 AM, US Durable Goods for February are published.

On Thursday, March 26 at 7:30 AM, Weekly Jobless Claims are announced. The number could top 1,000,000. The final read on Q4 GDP is announced, although it is ancient history.

On Friday, March 27 at 9:00 AM, the US Personal Income for February is printed. The Baker Hughes Rig Count follows at 2:00 PM.

As for me, I will be in training doing daily ten-mile hikes with a 50-pound backpack. I will be leading the Boy Scouts on a 50-mile hike at Philmont in New Mexico. I expect the epidemic to peak well before then and normalcy to return.

Shelter in place will work. Please stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

March 19, 2020

Fiat Lux

Featured Trade:

(INVESTING ON THE OTHER SIDE OF THE CORONA VIRUS),

(SPY), (INDU), (FXE), (FXY), (UNG),

(EEM), (USO), (TLT), (TSLA)

The Coronavirus has just set up the investment opportunity of the century.

In a matter of three weeks, stocks have gone from wildly overbought to ridiculously cheap. Price earnings multiples have plunged from 20X to 13X, well below the 15.5X long term historical average. The Dow Average is now 5% lower than when Donald Trump assumed the presidency more than three years ago. The world of investing after Coronavirus is looking pretty good.

I believe that as a result of this meltdown, the global economy is setting up for a new Golden Age reminiscent of the one the United States enjoyed during the 1950s, and which I still remember fondly. In other words, when it comes to investing after Coronavirus, we are on the cusp of a new “Roaring Twenties.”

This is not some pie in the sky prediction.

It simply assumes a continuation of existing trends in demographics, technology, politics, and economics. The implications for your investment portfolio will be huge.

For a start, medical science is about to compress 5-10 years of advancement into a matter of months. The traditional FDA approval process has been dumped in the trash. Any company can bring any medicine, vaccine, or anti-viral they want to the market, government be damned. You and I will benefit enormously, but a few people may die along the way.

What I call “intergenerational arbitrage” will be the principal impetus. The main reason that we are now enduring two “lost decades” of economic growth is that 80 million baby boomers are retiring to be followed by only 65 million “Gen Xer’s”.

When the majority of the population is in retirement mode, it means that there are fewer buyers of real estate, home appliances, and “RISK ON” assets like equities, and more buyers of assisted living facilities, healthcare, and “RISK OFF” assets like bonds.

The net result of this is slower economic growth, higher budget deficits, a weak currency, and registered investment advisors who have distilled their practices down to only municipal bond sales.

Fast forward two years when the reverse happens and the baby boomers are out of the economy, worried about whether their diapers get changed on time or if their favorite flavor of Ensure is in stock at the nursing home.

That is when you have 65 million Gen Xer’s being chased by 85 million of the “millennial” generation trying to buy their assets.

By then, we will not have built new homes in appreciable numbers for 20 years and a severe scarcity of housing hits. Residential real estate prices will soar. Labor shortages will force wage hikes.

The middle-class standard of living will reverse a then 40-year decline. Annual GDP growth will return from the current subdued 2% rate to near the torrid 4% seen during the 1990s.

The stock market rockets in this scenario. And this pandemic has just given us a very low base from which to start, making investing after Coronavirus a promising prospect.

Once the virus is beaten, we could see the same fourfold return we saw from 2009 to 2020. That would take us from The Thursday low of 18,917 to 76,000 in only a few years.

If I’m wrong, it will hit 100,000 instead.

Emerging stock markets (EEM) with much higher growth rates do far better.

This is not just a demographic story. The next ten years should bring a fundamental restructuring of our energy infrastructure as well.

The 100-year supply of natural gas (UNG) we have recently discovered through the new “fracking” technology will finally make it to end users, replacing coal (KOL) and oil (USO), so this sort of energy investing after Coronavirus in particular is looking undoubtedly promising.

Fracking applied to oilfields is also unlocking vast new supplies.

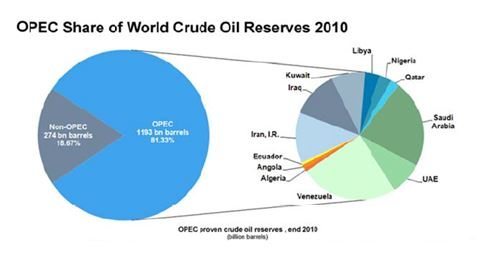

Since 1995, the US Geological Survey estimate of recoverable reserves has ballooned from 150 million barrels to 8 billion. OPEC’s share of global reserves is collapsing.

This is all happening while the use of electric cars is exploding, from zero to 4% of the market over the past decade.

Mileage for the average US car has jumped from 23 to 24.9 miles per gallon in the last couple of years, and the administration is targeting 50 mpg by 2025. Total gasoline consumption is now at a five-year low and collapsing.

Alternative energy technologies will also contribute in an important way in states like California, which will see 100% of total electric power generation come from alternatives by 2030.

I now have an all-electric garage, with a Tesla Model 3 for local errands and a Tesla Model X (TSLA) for longer trips, allowing me to disappear from the gasoline market completely. Millions will follow. Both cars are powered by my rooftop solar system.

The net result of all of this is lower energy prices for everyone.

It will also flip the US from a net importer to an exporter of energy, with hugely positive implications for America’s balance of payments.

Eliminating our largest import and adding an important export is very dollar bullish for the long term.

That sets up a multiyear short for the world’s big energy-consuming currencies, especially the Japanese yen (FXY) and the Euro (FXE). A strong greenback further reinforces the bull case for stocks.

Accelerating technology will bring another continuing positive for investing after Coronavirus.

Of course, it’s great to have new toys to play with on the weekends, send out Facebook photos to the family, and edit your own home videos. But at the enterprise level, this is enabling speedy improvements in productivity that are filtering down to every business in the US, lower costs everywhere.

This is why corporate earnings have been outperforming the economy as a whole by a large margin.

Profit margins are at an all-time high.

Living near booming Silicon Valley, I can tell you that there are thousands of new technologies and business models that you have never heard of under development.

When the winners emerge, they will have a big cross-leveraged effect on the economy.

New healthcare breakthroughs, which are also being spearheaded in the San Francisco Bay area, will make serious disease a thing of the past.

This is because the Golden State thumbed its nose at the federal government 18 years ago when the stem cell research ban was implemented.

It raised $3 billion through a bond issue to fund its own research, even though it couldn’t afford it.

I tell my kids they will never be afflicted by my maladies. When they get cancer in 20 years, they will just go down to Wal-Mart and buy a bottle of cancer pills for $5, and it will be gone by Friday.

What is this worth to the global economy? Oh, about $2 trillion a year, or 4% of GDP. Who is overwhelmingly in the driver’s seat on these innovations? The USA.

There is a political element to the new Golden Age as well. Gridlock in Washington can’t last forever. Eventually, one side or another will prevail with a clear majority.

This will allow the government to push through needed long-term structural reforms, the solution of which everyone agrees on now but nobody wants to be blamed for.

That means raising the retirement age from 66 to 70 where it belongs and means-testing recipients. Billionaires don’t need the maximum $45,480 Social Security benefit. Nor do I.

The ending of our foreign wars and the elimination of extravagant unneeded weapons systems cut defense spending from $755 billion a year to $400 billion, or back to the 2000, pre-9/11 level. Guess what happens when we cut defense spending? So does everyone else.

I can tell you from personal experience that staying friendly with someone is far cheaper than blowing them up.

A Pax Americana would ensue.

That means China will have to defend its own oil supply, instead of relying on us to do it for them for free. That’s why they have recently bought a second used aircraft carrier. The Middle East is now their headache, not ours.

The national debt then comes under control, and we don’t end up like Greece.

The long-awaited Treasury bond (TLT) crash never happens.

The reality is that the global economy will soon spin off profits faster than it can find places to invest them, so the money ends up in bonds instead.

Sure, this is all very long-term, over the horizon stuff. You can expect the financial markets to start discounting a few years hence, even though the main drivers won’t kick in for another decade.

But some individual industries and companies will start to discount this rosy scenario now.

Perhaps this is what the nonstop rally in stocks since 2009 has been trying to tell us.

Needless to say, investing after Coronavirus runs it's course will be a welcome change for both individual investors and the economy as a whole.

Global Market Comments

February 20, 2020

Fiat Lux

SPECIAL FANG ISSUE

Featured Trade:

(FINDING A NEW FANG),

(FB), (AAPL), (NFLX), (GOOGL),

(TSLA), (BABA)

We all love our FANGS.

Not only have Facebook (FB), Apple (AAPL), Netflix (NFLX), and Alphabet (GOOGL) been at the core of our investment performance for the past decade years, we also gobble up their products and services like kids eating their candy stash the day after Halloween.

Three of the FANGs have already won the race to become the first $1 trillion in history, Apple, Amazon, and Microsoft.

In fact, the FANGs are so popular that we need more of them, a lot more. So how do we find a new FANG?

Here is where it gets complicated. None of the four have perfect business models. All excel in many things but are deficient at others.

So, there are at least four different answers as to what makes a FANG. A more accurate answer would probably be 4 squared, or four to the tenth power.

I will list the eight crucial elements that make a FANG.

1) Product Differentiation

In medieval times, location was the most important determinant of business success. If you owned Ye Olde Shoppe at the foot of London Bridge, you prospered.

Then, great distribution was crucial. This occurred during the 19th century when the railroads ran the economy.

Products followed with the automobile boom of the 20th century, when those who dreamed up 18-inch tailfins dominated. This strategy was applied to all consumer products.

The Financial age came next, when cheap money was used to assemble massive conglomerates that was the primary determinant of success.

The eighties and nineties spawned the era of global brands, be it Coca Cola, MacDonald’s, Lexus, or Gucci.

Today, the global economy is ruled by those who can provide the best services. Facebook offers you personal access to a network of 1.5 billion. Apple will sell you a phone that can perform a magical array of tricks.

Netflix will stream any video content imaginable with lightning speed. Alphabet will deliver you any piece of information you want as fast as you can type, but charges advertisers hundreds of billions of dollars to get in your way.

This has created what I call an “Apple” effect. It stampedes buyers to pay the highest premiums for the best products, assuring global dominance.

While Apple accounts for less than 10% of the smart phone market, it captures a stunning 92% of the net profits. Everyone else is just an “also ran.”

Instead of driving my car into a dingy dealership every few months to get ripped off for a tune up, Tesla (TSLA) does it remotely, online, while I sleep, for free.

Unlike battling for a smelly New York taxi cab in a snow storm, a smiling Uber driver will show up instantly, know where to go, automatically bill me at a discount price, and even give me restaurant recommendations in Kabul.

And you all know what Amazon can do. It beats the hell out of looking for a parking space at a mall these days, only to be told they don’t have your size (48 XLT).

2. Visionary Capital

If you have a great vision, you can get unlimited financing free from investors anywhere. That puts those who must pay for expensive external financing for growth at a huge disadvantage.

Have a great vision, and the world is your oyster.

Elon Musk figured this out early with Tesla. By promising a “carbon-free economy,” he has been able to raise tens of billions of equity capital even though his firm has never made a real profit.

Alphabet is “organizing the world’s information”, while Facebook is “connecting the world.”

Chinese Internet giant Alibaba (BABA) invented a holiday from scratch, “Singles Day,” November 11, which has quickly become the most feverish shopping day in history. In 2019, they booked an unbelievable $30.8 billion in sales in a single 24 hours period, up 27% from the previous year.

And you know the great thing about visions? Not only do venture capitalists and consumers love them, so do stock investors.

3) Global Reach

You have to go global or be gone. A company with 7 billion customers will beat one with only 330 million all day long.

Go global, and economies of scale kick in enormously. This is only possible if you digitize everything from the point of sale to the senior management. Some two-thirds of Facebook users are outside the US, although half its profits are homegrown.

By the way, the Mad Hedge Fund Trader is global, with readers in 135 countries. Our marginal cost of production is zero, and the entire firm is run off my American Express card. It’s a great business model. And boy, do I get a ton of frequent flier points! Whenever I board Virgin Atlantic’s nonstop from San Francisco to London, the entire crew stands up to salute.

4) Likeability

Who doesn’t like Mark Zuckerberg, with his ever-present hoodies, skinny jeans, and self-effacing demeanor. And who did Facebook send to Washington to testify about internet regulation but the attractive, razor-sharp, and witty Sheryl Sandberg? The senators ate out of her hand.

Bill Gates and Steve Ballmer? Not so likable. Their arrogance invited a ten-year antitrust suit against Microsoft (MSFT) from the Justice Department which half the legal profession made a living off of.

And here’s the thing. If people like you, so will consumers, regulators, and yes, even equity investors. It makes a big difference to the bottom line and your investment performance.

5) Vertical Integration

Crucial to the success of the FANGs is their complete control of the customer experience through vertical integration.

When FANGs don’t manufacture their own products, as Apple does, they source them, rebrand them, and sell them as their own, like Amazon.

The return on investment for advertising is plummeting. Just ask the National Football League. So, it has become essential for companies to keep a death grip on the customer the second they enter your site.

Some, like Amazon again, will keep chasing you long after you have left their sites with special offers and alternative products. Even if you change computers they will hunt you down.

One of my teenaged daughters used my computer to buy a swimsuit last summer, and let me tell you, booting up in the morning has been a real joy ever since.

This was the genius of the Apple store network. Buy one Apple product and they own you for life, like an indentured servant. They all integrate and talk to each other, a huge advantage for a small business owner. And they are cool.

No pimple-faced geeks wearing horn-rimmed glasses here. Get your iPhone fixed and you don’t talk to a technician, but a “genius.” It’s all about control.

Expect other strong brands to open their own store chains soon.

6) Artificial Intelligence

There is probably no more commonly known but least understood term in technology today. It’s like counting the number of people who have finished Dr. Stephen Hawking’s “A Brief History of Time” (I have).

A trillion-dollar company absolutely must be able to learn from human data input and then use algorithms to analyze it. Data has become the oxygen of the modern economy.

The company then use other algos to predict what you’re most likely buying next and then thrust it in front of your face screaming at the top of its lungs.

This has been evolving for decades.

First, there was demographic targeting. White suburban middle-class guys have all got to like Budweiser, right?

This turned into social targeting. If two friends “liked” the same brand, regardless of their demographics, they should be targeted by same advertisers.

Now we live in the age of behavioral targeting. There is no better predictor of future purchases than current activities. So, if I buy a plane ticket to Paris, offerings of Paris guidebooks, tours, French cookbooks, French dating services, and even seller of discount black berets suddenly start coming out of the woodwork.

It would be a vast understatement to say that behavioral targeting is the most successful marketing strategy ever invented. So, guess what? We’re going to get a lot more of it.

As depressing as this may sound, the number one goal of almost all new technological advancements these days is to get you to buy more stuff.

Better to use the public computer at the library to buy your copy of “50 Shades of Gray.”

7) Accelerant

If you want to throw gasoline on the growth of a company, you absolutely have to have the best people to do it. The companies with the smartest staff can suck in free capital, invent faster, develop speedier services, and always be ahead of the curve when compared to the competition.

This has led to enormous disparities in income. Companies will pay anything for winners, but virtually nothing for losers.

I’ll never forget the first day I walked on to the trading floor at Morgan Stanley (MS). I am 6’4” and am used to towering over those around me. But at Morgan, almost all the salesmen were my height or a few inches shorter.

The company specifically selected these people because they delivered better sales records. Height is intimidating, especially to short customers.

And that’s what the FANGs have, the programming equivalents of a crack all-6’4” sales team.

A few years ago, my son got a job as the head of International SEO at Google. He was rare in that he spoke fluent Japanese and carried three passports, US, British, and Japanese (born in London with a Japanese mom and American dad).

However, when he met his team, they all spoke multiple languages, were binational, and were valedictorians, National Merit Scholars, and Eagle Scouts to boot!

This is why immigration is such a hot button issue in Silicon Valley these days. If you can’t get a work visa for a graduating PhD in Computer Science from Stanford, he’ll just go back to China or India to start a local competitor that may someday eat your lunch.

By the way, if you get a FANG on your resume, even for a short period, you are set for life. Oh, and by the way, Apple gets 100,000 resumes a month!

8) Geography

It all about location, location, location. It’s no accident that Silicon Valley took root near two world class universities, the University of California at Berkeley (my alma mater), and the godless heathens at Stanford across the bay.

When the pioneers moved west in covered wagons in 1849, they came to a fork in the road. The god fearing families went right to the verdant farmland of Oregon, while young men cashing in on the latest get-rich-quick scheme chose left for the gold fields of California. Nothing has changed since.

Cal in particular was the recipient of massive government funding for the Manhattan Project that built the first atomic bomb during WWII. The tailwind lingers to this day. The world’s first cyclotron still occupies a local roundabout.

Universities provide the raw materials essential to create hot house local economies like the San Francisco Bay Area. And as much as every region in the US or country in the world would like to do this, none have been able to.

There is only one place in the world were a company can hire 1,000 engineers from scratch on short notice, and that is the Bay Area.

Also, innovation is city centered. Some two-thirds of future GDP growth will emanate from cities.

So, if you want to move your career forward, you better count on spending some serious time in Silicon Valley, New York, London, and Tokyo.

I’ve done all four and it paid handsomely.

So there you have it. Now we know what makes a FANG. I’ll be addressing who the most likely FANG candidates are in a future letter.

I want to thank my friend, Scott Galloway of New York University’s Stern School of Business for some of the concepts in this piece. His book, “The Four” is a must read for the serious tech investor.

Global Market Comments

February 18, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE TRADE ALERT DROUGHT)

(SPY), (TLT), (MSFT), (BA), (TSLA), (MGM)

Like it or not, we have a trade alert drought on our hands.

I just ran the numbers on 200 potential trades in stocks, bonds, foreign exchange, commodities, precious metals, and real estate, and there was not a single one that was worth executing.

They all had one thing in common: for taking huge risks, there were only paltry profits on offer. Even with a 90% success rate, I would still lose money.

And here is the problem. Massive quantitative easing from the US Federal Reserve is keeping the prices of all assets artificially high. But fears of a global Coronavirus pandemic are keeping all prices capped. The spread between the bid and the offer is only 3%. That is not enough to make an honest living, nor even a dishonest one.

I’ve seen all this before. The US in 1974, Tokyo in 1989, NASDAQ in 1999 presented similar trading dilemmas. The outcome is always the same. Prices always go up much longer than expected and then are followed by horrific crashes. Only when the last dollar is sucked in do trends change.

So, for right now, I would rather do nothing than something. We are in a contest to see who can make the most money with the fewest drawdowns, not to see who can strap on the most trades. The latter makes your broker rich, not you.

Cash is a position, it is an opinion, and it has option value. A dollar at a market top is worth $10 at a market bottom. Opportunity cost is not to be underestimated.

For the time being, everything depends on the Coronavirus. It is universally believed that the Chinese data is wildly inaccurate, possible by tenfold. The risks to the markets are similarly underestimated by US investors.

That became screamingly clear to me after returning from a trip halfway around the world where my temperature was taken every time I crossed a border and planes had to be sterilized before boarding

So, the smart game here is to be patient and learn some discipline. Wait for the market to come to you. This is a year when it will be incredibly difficult to make money and extremely easy to lose it.

All trade alert droughts end. Whether it will be sooner or later is anyone’s guess.

China is planning massive stimulus, to get the economy back on track. GDP could drop from 6% to 0% and maybe -6% thanks to the Coronavirus. A borrowing stampede is underway as shut down companies seek to address hemorrhaging cash flow.

Tesla (TSLA) exploded again to the upside, up 10% at the opening. The company has become a good news factory. The German government stepped in to subsidize a massive Gigafactory there. I won’t touch the stock here, but my long terms target is still $2,500.

Tesla finally took my advice and launched a $2 billion common stock offering at these lofty prices. It should be $5 billion. They can retire all their debt, including the convertible bonds, and with no dividend they can operate at a zero cost of capital. Elon Musk is taking $10 million of the deal. He took $100 million of the last offering. Buy (TSLA) on dips. Losses pile up for the short-sellers. Tesla always does the right thing after trying everything else out first.

The Fed’s Jay Powell cheers the economy but warned that the Coronavirus could become a factor. He also cautioned about a federal deficit that will top $1 trillion this year.

With the economy growing at a 2.2% annual rate, it’s below the Obama era growth. Did anyone notice that he said he would trim back QE by reigning in the repo program initiated last fall? Risk in the stock market is now extremely high.

Apple (AAPL) and Microsoft (MSFT) are now 10% of the entire stock market and are wildly overbought. Such incredible concentration is a typical sign of a topping market. Virtually all the stocks Mad Hedge has been recommending for the last decade are at new all-time highs. Be careful what you wish for.

Household Debt soared hitting a 12-year high. It’s up $601 billion to $14 trillion. It’s pedal to the metal for consumer spending, another classic market-topping indicator. What happens when the bill comes due and interest rates rise?

MGM (MGM) canceled guidance as the Coronavirus upends their business. High-end Chinese gamblers won’t show up to lose gobs of money at the gaming tables if they can’t get here. The epidemic has put the whole gaming industry into turmoil. Call me after new virus cases peak in China. Avoid (MGM).

Boeing had no net deliveries of aircraft in January, the first time since 1962, but the stock rose anyway. That tells me the bottom is firmly in. Buy (BA) on dips. When will the suffering of one of America’s best-run companies, accounting for 3% of GDP, end?

Despite the fact that we may be facing the end of the world, the Mad Hedge Trader Alert Service managed to maintain new all-time highs. I came out of my last position in Boeing (BA) to beat the ex-dividend day and a possible call on my short February $280 calls.

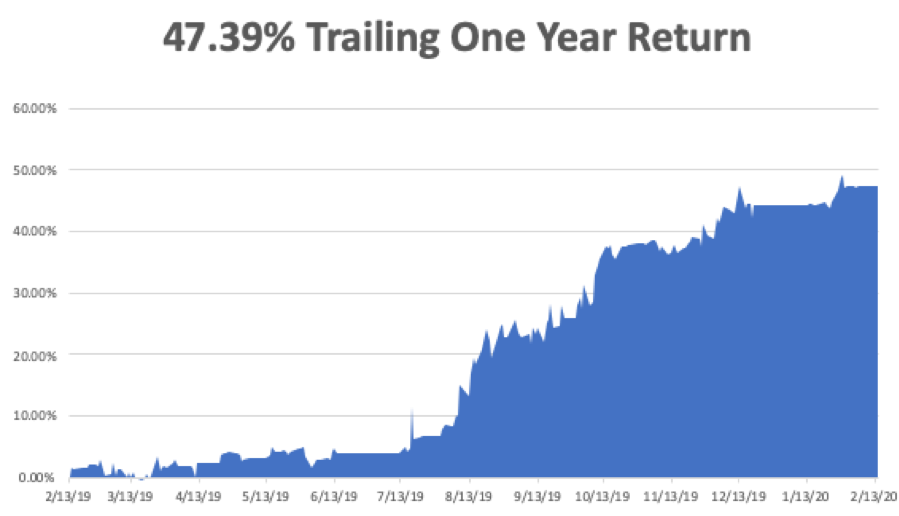

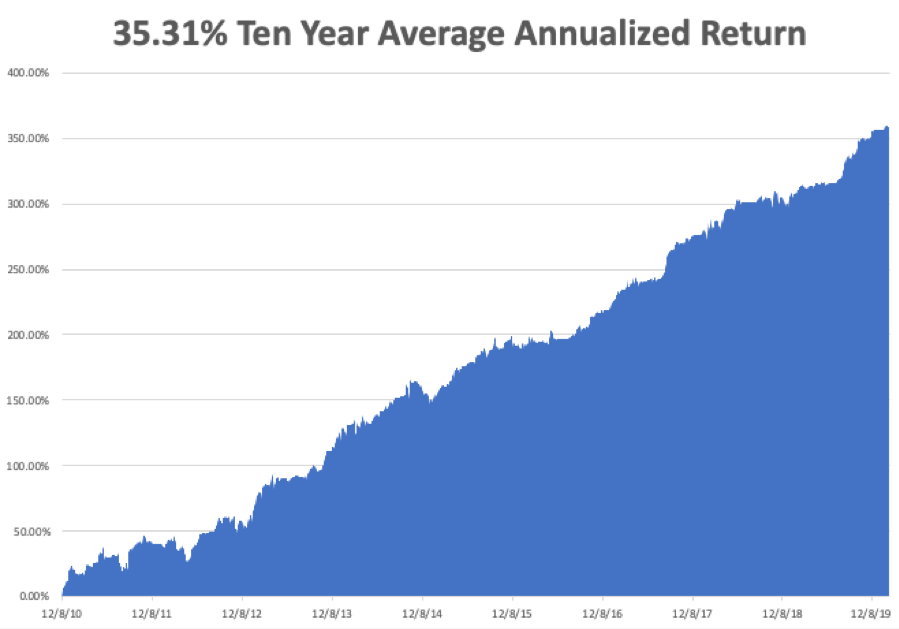

My Global Trading Dispatch performance rose to a new high at +359.00% for the past ten years. February stands at -0.04%. My trailing one-year return is stable at 47.39%. My ten-year average annualized profit ground back up to +35.31%.

All eyes will be focused on the Coronavirus still, with deaths over 1,800. The weekly economic data are virtually irrelevant now. However, some important housing numbers will be released.

On Tuesday, February 18 at 8:30 AM, the NY State Manufacturing Index for February is released.

On Wednesday, February 19, at 9:30 PM, January Housing Starts are out.

On Thursday, February 20 at 8:30 AM, Weekly Jobless Claims come out. The February Philadelphia Fed Manufacturing Index is announced.

On Friday, February 21 at 10:30 AM, January Existing Home Sales are printed. The Baker Hughes Rig Count follows at 2:00 PM.

As for me, I’ll be driving back from Lake Tahoe, where I spent the long weekend catching up on the markets. There was virtually no snow, amazing for February, but great hiking.

Since I will be dropping 7,200 feet from Donner Pass and I have the new expended range Model X, I will be able to make it the 220 miles home on a single charge.

In two years, I’ll be able to make the 440-mile round trip on a single charge when the new Tesla Cyber truck comes out. Of course, people will think I’m nuts and my kids have refused to be seen in the cutting edge vehicle, but when did that ever stop me?

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

February 14, 2020

Fiat Lux

Featured Trade:

(FEBRUARY 12 BIWEEKLY STRATEGY WEBINAR Q&A)

(SQ), (TSLA), (FB), (GILD), (BA), (CRSP), (CSCO), (GLD)

(FEYE), (VIX), (VXX), (USO), (LYFT), (UBER)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader February 12 Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: What do you think about Facebook (FB) here? We’ve just had a big dip.

A: We got the dip because of a double downgrade in the stock from a couple of brokers, and people are kind of nervous that some sort of antitrust action may be taken against Facebook as we go into the election. I still like the stock long term. You can’t beat the FANGs!

Q: If Bernie Sanders gets the nomination, will that be negative for the market?

A: Absolutely, yes. It seems like after 3 years of a radical president, voters want a radical response. That said, I don't think Bernie will get the nomination. He is not as popular in California, where we have a primary in a couple of weeks and account for 20% of total delegates. I think more of the moderate candidates will come through in California. That's where we see if any of the new billionaire outliers like Michael Bloom or Tom Steyer have any traction. My attitude in all of this is to wait for the last guy to get voted off the island—then ask me what's going to happen in October.

Q: When should we come back in on Tesla (TSLA)?

A: It’s tough with Tesla because although my long-term target is $2,500, watching it go up 500% in seven months on just a small increase in earnings is pretty scary. It’s really more of a cult stock than anything else and I want to wait for a bigger pullback, maybe down to $500, before I get in again. That said, the volatility on the stock is now so high that—with the short interest going from 36% down to 20%—if we get the last of the bears to really give up, then we lose that whole 20% because it all turns into buying; and that could get us easily over $1,000. The announcement of a new $2 billion share offering is a huge positive because it means they can pay off debt and operate with free capital as they don’t pay a dividend.

Q: Is Square (SQ) a good buy on the next 5% drop?

A: I would really wait 10%—you don't want to chase trades with the market at an all-time high. I would wait for a bigger drop in the main market before I go aggressive on anything.

Q: What about CRISPR Technology (CRSP) after the 120% move?

A: We’ve had a modest pullback—really more of a sideways move— since it peaked a couple of months ago; and again, I think the stock either goes much higher or gets taken over by somebody. That makes it a no-lose trade. The long sideways move we’re having is actually a very bullish indication for the stock.

Q: If Bernie is the candidate and gets elected, would that be negative for the market?

A: It would be extremely negative for the market. Worth at least a 20% downturn. That said, according to all the polling I have seen, Bernie Sanders is the only candidate that could not win against Donald Trump—the other 15 candidates would all beat Trump in a 1 to 1 contest. He's also had one heart attack and might not even be alive in 6 months, so who knows?

Q: I just closed the Boeing (BA) trade to avoid the dividend hit tomorrow. What do you think?

A: I’m probably going to do the same, that way you can avoid the random assignments that will stick you with the dividend and eat up your entire profit on the trade.

Q: When do you update the long-term portfolio?

A: Every six months; and the reason for that is to show you how to rebalance your portfolio. Rebalancing is one of the best free lunches out there. Everyone should be doing it after big moves like we’ve seen. It’s just a question of whether you rebalance every six months or every year. With stocks up so much a big rebalancing is due.

Q: I have held onto Gilead Sciences (GILD) for a long time and am hoping they’ll spend their big cash hoard. What do you think?

A: It’s true, they haven’t been spending their cash hoard. The trouble with these biotech stocks, and why it's so hard to send out trade alerts on them, is that you’ll get essentially no movement on them for years and then they rise 30% in one day. Gilead actually does have some drugs that may work on the coronavirus but until they make another acquisition, don’t expect much movement in the stock. It’s a question of how long you are willing to wait until that movement.

Q: Is it time to get back into the iPath Series B S&P 500 VIX Short Term Futures ETN (VXX)?

A: No, you need to maintain discipline here, not chase the last trade that worked. It’s crucial to only buy the bottoms and sell the tops when trading volatility. Otherwise, time decay and contango will kill you. We’re actually close to the middle of the range in the (VXX) so if we see another revisit to the lows, which we could get in the next week, then you want to buy it. No middle-of-range trades in this kind of market, you’re either trading at one extreme or the other.

Q: Could you please explain how the Fed involvement in the overnight repo market affects the general market?

A: The overnight repo market intervention was a form of backdoor quantitative easing, and as we all know quantitative easing makes stocks go up hugely. So even though the Fed said this wasn't quantitative easing, they were in fact expanding their balance sheet to facilitate liquidity in the bond market because government borrowing has gotten so extreme that the public markets weren’t big enough to handle all the debt; that's why they stepped into the repo market. But the market said this is simply more QE and took stocks up 10% since they said it wasn't QE.

Q: What about Cisco Systems (CSCO)?

A: It’s probably a decent buy down here, very tempting. And it hasn't participated in the FANG rally, so yes, I would give that one a really hard look. The current dip on earnings is probably a good entry point.

Q: Should we buy the Volatility Index (VIX) on dips?

A: Yes. At bottoms would be better, like the $12 handle.

Q: When is the best time to exit Boeing?

A: In the next 15 minutes. They go ex-dividend tomorrow and if you get assigned on those short calls then you are liable for the dividend—that will eat up your whole profit on the trade.

Q: Do you like Fire Eye (FEYE)?

A: Yes. Hacking is one of the few permanent growth industries out there and there are only a half dozen listed companies that are cutting edge on security software.

Q: What are your thoughts on the timing of the next recession?

A: Clearly the recession has been pushed back a year by the 2019 round of QE, and stock prices are getting so high now that even the Fed has to be concerned. Moreover, economic growth is slowing. In fact, the economy has been growing at a substantially slower rate since Trump became president, and 100% of all the economic growth we have now is borrowed. If the government were running a balanced budget now, our growth would be zero. So, certainly QE has pushed off the recession—whether it's a one-year event or a 2-year event, we’ll see. The answer, however, is that it will come out of nowhere and hit you when you least expect it, as recessions tend to do.

Q: Would you buy gold (GLD) rather than staying in cash?

A: I would buy some gold here, and I would do deep in the money call spreads like I have been doing. I’ve been running the numbers every day waiting for a good entry point. We’re now at a sort of in between point here on call spreads because it’s 7 days to the next February expiration and about 27 days to the March one after that, so it's not a good entry point this week. Next week will look more interesting because you’ll start getting accelerated time decay for March working for you.

Q: When are you going to have lunch in Texas or Oklahoma?

A: Nothing planned currently. Because of my long-term energy views (USO), I have to bring a bodyguard whenever I visit these states. Or I hold the events at a Marine Corps Club, which is the same thing.

Q: Would you use the dip here to buy Lyft (LYFT)? It’s down 10%.

A: No, it’s a horrible business. It’s one of those companies masquerading as a tech stock but it isn’t. They’re dependent on ultra-low wages for the drivers who are essentially netting $5 an hour driving after they cover all their car costs. Moreover, treating them as part-time temporary workers has just been made illegal in California, so it’s very bad news for the stocks—stay away from (LYFT) and (UBER) too.

Q: Is the Fed going to cut interest rates based on the coronavirus?

A: No, interest rates are low enough—too low given the rising levels of the stock market. Even at the current rate, low-interest rates are creating a bubble which will come back to bite us one day.

Q: Household debt exceeded $14 trillion for the first time—is this a warning sign?

A: It is absolutely a warning sign because it means the consumer is closer to running out of money. Consumers make up 70% of the economy, so when 70% of the economy runs out of money, it leads to a certain recession. We saw it happen in ‘08 and we’ll see it happen again.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader