Mad Hedge Technology Letter

July 22, 2019

Fiat Lux

Featured Trade:

(DOES ARTIFICIAL INTELLIGENCE WORK FOR YOU?),

(TSLA), (AMZN), (FB)

Mad Hedge Technology Letter

July 22, 2019

Fiat Lux

Featured Trade:

(DOES ARTIFICIAL INTELLIGENCE WORK FOR YOU?),

(TSLA), (AMZN), (FB)

Anti-A.I. physicist Professor Stephen Hawking was a staunch supporter of preserving human interests against the future existential threat from machines and artificial intelligence (A.I.).

He was diagnosed with motor neuron disease, more commonly known as Lou Gehrig's disease, in 1963 at the age of 21 and sadly passed away March 14, 2018 at the age of 76.

Famed for his work on black holes, Professor Hawking represented the human quest to maintain its superiority against quickly advancing artificial acculturation.

His passing was a huge loss for mankind as his voice was a deterrent to A.I.'s relentless march to supremacy. He was one of the few who had the authority to opine on these issues. Gone is a voice of reason.

Critics have argued that living with A.I. poses a red alert threat to privacy, security, and society as a whole. Unfortunately, those most credible and knowledgeable about A.I. are tech firms. They have shown that policing themselves on this front is remarkably unproductive.

Mark Zuckerberg, CEO of Facebook (FB), has labeled naysayers as "irresponsible" and dismissed the threat. After failing to prevent Russian interference in the last election, he is exhibiting the same defensive posture translating into a de facto admission of guilt. His track record of shirking accountability is becoming a trend.

Share prices will materially nosedive if A.I. is stonewalled and development stunted. Many CEOs who stake careers on doubling or tripling down on A.I. cannot see it die out. There is too much money to lose.

The world will see major improvements in the quality of life in the next 10 years. But there is another side to the coin which Zuckerberg and company refuse to delve into...the dark side of technology.

Defective Amazon (AMZN) Alexa recently produced unexplained laughter because of a mistaken command to start laughing. Despite avoiding calamity, these small events show the magnitude of potential chaos capable of haywire A.I. functions. If one day a user attempts to order a box of tissues and Alexa burns down the house, who is liable?

Tesla's (TSLA) CEO Elon Musk has shared his anxiety about robots flipping the script on humans. Musk acknowledges that A.I. and autonomous vehicles are important factors in the battle for new technology.

The winner is yet to be determined as China has bet the ranch with unlimited resources from Chairman Xi.

The quagmire with China has been squarely centered around the great race for technological supremacy.

A.I. is the ultimate X factor in this race and whoever can harness and develop the fastest will win.

Musk has hinted that robots and humans could merge into one species in the future.

Is this the next point of competition among tech companies? The future is murky at best.

Bill Gates noted that robots should be taxed like humans.

This reflects the bubble in which the ultra-elite reside.

This comment implies that humans and robots are at the same level. It shows a severe lack of empathy for the 40% of working Americans who will be replaced by machines over the next 10 years.

The West is comprised of a deeply hierarchical system of winners and losers. Hawking's premise that evolution has inbuilt greed can be found in the underpinnings of America's economic miracle.

Wall Street has bred a culture that is entirely self-serving regardless of the bigger system in which it finds itself.

Most of us are participating in this perpetual money game chase because our system treats it as a natural part of life.

A.I. will help more people do well in this paper chase to the detriment of the majority.

Quarterly earnings performance is paramount for CEOs.

Return value back to shareholders, or face the sack in the morning.

It's impossible to convince anyone that America's capitalist model is deteriorating in the greatest bull market of all time.

Wall Street has an insatiable hunger for cutting-edge technology from companies that sequentially beat earnings and raise guidance.

Flourishing technology companies enrich the participants creating a Teflon-like resistance to downside market risk.

The issue with Professor Hawking's work is that his timeframe is too far in the future.

Professor Hawking was probably correct, but it will take 25 years to prove it.

The world is quickly changing as science fiction becomes reality.

The year 2020 will signal the real beginning of A.I. in tangible form when autonomous fleets flood main streets and is another step in the direction of human's overreliance on machines.

People on Wall Street are a product of the system in place and earn a tremendous amount of money because they proficiently execute a specialized job.

Traders are busy focusing on how to move ahead of the next guy.

Firms building autonomous cars are free to operate as is.

Hyper-accelerating technology spurs on the development of A.I., machine learning, and enhanced algorithms.

Record profits will topple, and investors will funnel investments back into an even narrower grouping of technology stocks after the weak hands are flushed out.

Professor Hawking said we need to explore our technological capabilities to the fullest in order to avoid extinction.

In 2019, exploring these new capabilities still equals monetizing through the medium of products and services.

This is all bullish for equities as the leading companies associated with A.I. have a red carpet laid out in front of them.

And let me remind you that technology is still the least regulated industry on the planet even if sentiment has pivoted this year.

The only solution is keeping companies accountable by a function of law or creating a third-party task force to regulate A.I.

In 2019, the thought of overseeing robots sounds crazy.

However, by 2020, it might be as normal as uncontrollable laughter from your smart home device.

Global Market Comments

July 8, 2019

Fiat Lux

Featured Trade:

(STANDBY FOR THE COMING GOLDEN AGE OF INVESTMENT),

(SPY), (INDU), (FXE), (FXY), (UNG), (EEM), (USO),

(TLT), (NSANY), (TSLA)

I believe that the global economy is setting up for a new Golden Age reminiscent of the one the United States enjoyed during the 1950s, and which I still remember fondly.

This is not some pie in the sky prediction.

It simply assumes a continuation of existing trends in demographics, technology, politics, and economics. The implications for your investment portfolio will be huge.

What I call “intergenerational arbitrage” will be the principal impetus. The main reason that we are now enduring two “lost decades” of economic growth is that 80 million baby boomers are retiring to be followed by only 65 million “Gen Xers”.

When the majority of the population is in retirement mode, it means that there are fewer buyers of real estate, home appliances, and “RISK ON” assets like equities, and more buyers of assisted living facilities, health care, and “RISK OFF” assets like bonds.

The net result of this is slower economic growth, higher budget deficits, a weak currency, and registered investment advisors who have distilled their practices down to only municipal bond sales.

Fast forward six years when the reverse happens and the baby boomers are out of the economy, worried about whether their diapers get changed on time or if their favorite flavor of Ensure is in stock at the nursing home.

That is when you have 65 million Gen Xers being chased by 85 million of the “millennial” generation trying to buy their assets.

By then, we will not have built new homes in appreciable numbers for 20 years and a severe scarcity of housing hits. Residential real estate prices will soar. Labor shortages will force wage hikes.

The middle-class standard of living will reverse a then 40-year decline. Annual GDP growth will return from the current subdued 2% rate to near the torrid 4% seen during the 1990s.

The stock market rockets in this scenario.

Share prices may rise very gradually for the rest of the teens as long as tepid 2-3% growth persists.

After that, we could see the same fourfold return we saw during the Clinton administration, taking the Dow to 100,000 by 2030.

If I’m wrong, it will hit 200,000 instead.

Emerging stock markets (EEM) with much higher growth rates do far better.

This is not just a demographic story. The next 20 years should bring a fundamental restructuring of our energy infrastructure as well.

The 100-year supply of natural gas (UNG) we have recently discovered through the new “fracking” technology will finally make it to end users, replacing coal (KOL) and oil (USO).

Fracking applied to oilfields is also unlocking vast new supplies.

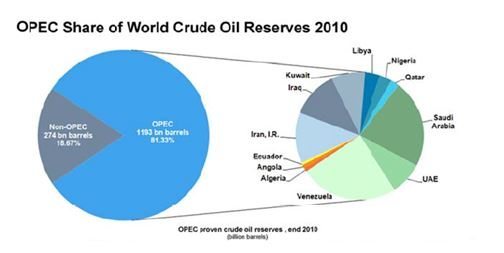

Since 1995, the US Geological Survey estimate of recoverable reserves has ballooned from 150 million barrels to 8 billion. OPEC’s share of global reserves is collapsing.

This is all happening while automobile efficiencies are rapidly improving and the use of public transportation soars.

Mileage for the average US car has jumped from 23 to 24.7 miles per gallon in the last couple of years, and the administration is targeting 50 mpg by 2025. Total gasoline consumption is now at a five-year low.

Alternative energy technologies will also contribute in an important way in states like California, accounting for 30% of total electric power generation by 2020.

I now have an all-electric garage with a Nissan Leaf (NSANY) for local errands and a Tesla Model S-1 (TSLA) for longer trips, allowing me to disappear from the gasoline market completely. Millions will follow.

The net result of all of this is lower energy prices for everyone.

It will also flip the US from a net importer to an exporter of energy with hugely positive implications for America’s balance of payments.

Eliminating our largest import and adding an important export is very dollar-bullish for the long term.

That sets up a multiyear short for the world’s big energy consuming currencies, especially the Japanese yen (FXY) and the Euro (FXE). A strong greenback further reinforces the bull case for stocks.

Accelerating technology will bring another continuing positive. Of course, it’s great to have new toys to play with on the weekends, send out Facebook photos to the family, and edit your own home videos.

But at the enterprise level, this is enabling speedy improvements in productivity that is filtering down to every business in the US, lower costs everywhere.

This is why corporate earnings have been outperforming the economy as a whole by a large margin.

Profit margins are at an all-time high.

Living near booming Silicon Valley, I can tell you that there are thousands of new technologies and business models that you have never heard of under development.

When the winners emerge, they will have a big cross-leveraged effect on economy.

New health care breakthroughs will make serious disease a thing of the past which are also being spearheaded in the San Francisco Bay area.

This is because the Golden State thumbed its nose at the federal government ten years ago when the stem cell research ban was implemented.

It raised $3 billion through a bond issue to fund its own research even though it couldn’t afford it.

I tell my kids they will never be afflicted by my maladies. When they get cancer in 20 years, they will just go down to Wal-Mart and buy a bottle of cancer pills for $5, and it will be gone by Friday.

What is this worth to the global economy? Oh, about $2 trillion a year, or 4% of GDP. Who is overwhelmingly in the driver’s seat on these innovations? The USA.

There is a political element to the new Golden Age as well. Gridlock in Washington can’t last forever. Eventually, one side or another will prevail with a clear majority.

This will allow the government to push through needed long-term structural reforms, the solution of which everyone agrees on now, but nobody wants to be blamed for.

That means raising the retirement age from 66 to 70 where it belongs, and means-testing recipients. Billionaires don’t need the maximum $30,156 annual supplement. Nor do I.

The ending of our foreign wars and the elimination of extravagant unneeded weapons systems cut defense spending from $800 billion a year to $400 billion, or back to the 2000, pre-9/11 level. Guess what happens when we cut defense spending? So does everyone else.

I can tell you from personal experience that staying friendly with someone is far cheaper than blowing them up.

A Pax Americana would ensue.

That means China will have to defend its own oil supply, instead of relying on us to do it for them for free. That’s why they have recently bought a second used aircraft carrier. The Middle East is now their headache.

The national debt then comes under control, and we don’t end up like Greece.

The long-awaited Treasury bond (TLT) crash never happens.

The reality is that the global economy is already spinning off profits faster than it can find places to invest them, so the money ends up in bonds instead.

Sure, this is all very long-term, over the horizon stuff. You can expect the financial markets to start discounting a few years hence, even though the main drivers won’t kick in for another decade.

But some individual industries and companies will start to discount this rosy scenario now.

Perhaps this is what the nonstop rally in stocks since 2009 has been trying to tell us.

Global Market Comments

June 17, 2019

Fiat Lux

Featured Trade:

(THE MARKET OUTLOOK FOR THE WEEK AHEAD, or THE SCARY THING ABOUT THE MARKETS)

(SPY), (TLT), (GLD), (TSLA)

There’s one big scary thing about the markets right now. As I mentioned last week, the major indexes are sitting on a precipice of a right shoulder of a ‘Head and Shoulders” top.

Traders are expecting a trade war settlement and a Fed interest rate cut in July. While the economy in no way needs a rate cut, stock markets desperately do. In fact, they need another dose of steroids just to remain level. It reminds me of a certain recent California governor (I’ll be back).

If we get them, markets will grind up a few percentage points to a new all-time high. If we don’t, the top is in, possibly for this entire economic cycle, and a 25% swan dive is in the cards.

It's what traders call “Asymmetric risk.” If we get the bull case, you make sofa change. If we don’t, you lose dollars. It’s what I call picking up pennies in front of a steamroller. But in the 11th year of a bull market, that’s all you get. The truly disturbing part of this is that this setup is happening with valuation close to a historic high at a 17.5X price earnings multiple.

We’ll get a better read on Wednesday at 2:00 PM EST when the Fed announces its decision on interest rates. The post meeting statement will be more crucial than usual. What’s in a word, Shakespeare might have asked? If the Fed drops the word “Patient”, then a July interest rate cut is a sure thing. The algos reading the release at the speed of light will be the first to know.

It was initially off to the races last Monday when the one-week trade war with Mexico came to an end and some immigration issues were settled.

The tariffs are off, even though the Mexicans say the terms were already agreed to months ago.

There is no big ag buy either. The economy is still sliding into a recession, and the bond market has already discounted three of the next five quarter point rate cuts.

US exports are in free fall, with Long Beach, America’s busiest port, seeing seven straight months of declines in shipping volumes. They were off 19.5% in May alone. Recession indicator no. 199.

Buy bonds (TLT), gold (GLD), and short the US dollar (UUP), says my old friend, hedge fund legend Paul Tudor Jones. He is certainly reading the writing on the wall. The legendary trading billionaire believes that plunging interest rate cuts are going to dominate the scenery for the rest of 2019.

Tanker attacks sent oil soaring. After 50 years of waiting, it finally happened, torpedo attacks against two tankers in the Straits of Hormuz bound for China. Oil rocketed 4%, then gave up the rally, and stocks are amazingly up on the day.

Go figure. A decade ago, this would have been a down 1,000-point day for stocks and Texas tea would have soared to $100. Clearly, tensions in the Middle East are ratcheting up, but with the US now the swing oil producer, why bother?

With US oil production climbing to 17 million barrels a day by 2024, up from 5 million b/d in 2005, the Middle East can blow itself up and nobody cares. The US by then will have created an entire Saudi Arabia’s worth of new oil production over a 20-year period. US troops there are defending China’s oil supply, not ours.

The US budget deficit soared by 38.7% YOY, to $739 billion. It’s the fastest growth in government borrowing since WWII. Much of today’s economic growth in on credit and this can only end in tears. Enjoy the good times while they last.

Major semiconductor maker Broadcom (AVGO) disappointed hugely on earnings, tanking the market, and the stock plunged a heartbreaking 12%. The trade war gets the entire blame. It turns out that Broadcom’s biggest customer is the ill-fated Huawei whose CFO is now sitting in a Canadian jail awaiting extradition to the US. Other semiconductor stocks especially got slammed. The canary in the coal mine just died.

China’s industrial production hit a 17 year low, and yes, it’s because of the trade war, trade war, trade war. When your biggest customers come down with the Asian flu, you at the very least catch a severe cold. Start shopping for Robitussin.

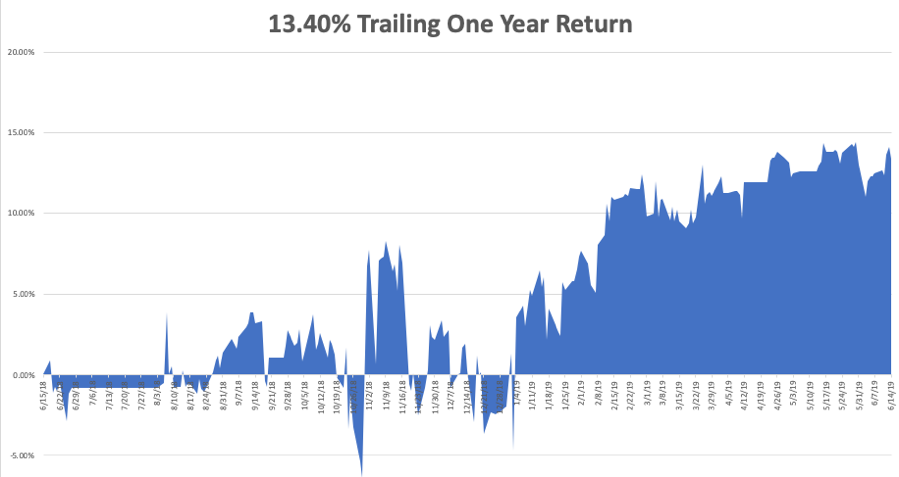

Global Trading Dispatch closed the week up 15.38% year-to-date and is down by -0.34% so far in June. That’s show business. You work your guts out trying to understand this market and it turns out to be for free. Or worse yet, you get a bill without an amount due. This is something that regular salary earners don’t understand.

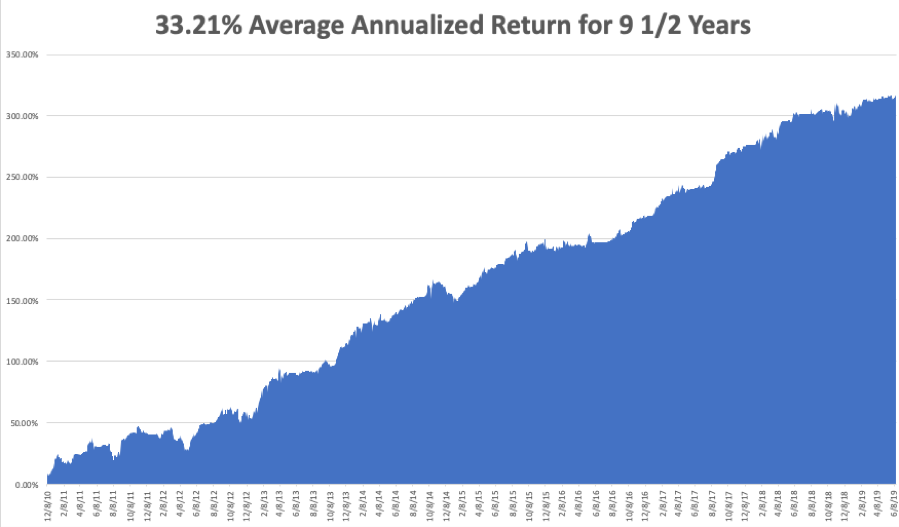

My nine and a half year profit appreciated to +315.52%, pennies short of a new all-time high. I think I’ll be flatlining at a high for a while to create a base from which I can jump to new highs. The average annualized return ticked up to +33.21%. With the trade war with China raging, I am now 100% in cash with Global Trading Dispatch and 100% cash in the Mad Hedge Tech Letter.

My twin bets on Tesla (TSLA) worked out very nicely and I took profits on both. It was an option play whereby I expected that (TSLA) shares would not fall below $150 or rise above $240 by the June 21 option expiration.

Several followers have seen good success using every Tesla dip below $200 to go naked short August $100 or $125 Tesla puts in small quantities for a decent amount of change.

The long view here is to wait for some kind of summer meltdown and then go long into a year-end rally as 2020 election-related turbochargers start to hit the market.

The coming week will be all about waiting for the Fed to jump. We also get some important updates on housing data.

On Monday, June 17 at 8:30 AM EST the Empire State Manufacturing Index is out.

On Tuesday, June 18, 8:30 AM EST, the May Housing Starts are released.

On Wednesday, June 19 at 2:00 PM EST, the Federal Reserve decision on interest rates is announced. Vital is whether the word “Patient” remains in their statement.

On Thursday, June 20 at 8:30 AM, the Weekly Jobless Claims are printed. We also get the Philadelphia Fed Manufacturing Index.

On Friday, June 21 at 10:00 AM, we learn May Existing Home Sales. The Baker Hughes Rig Count follows at 2:00 PM.

As for me, by the time you read this, I will be winging my way somewhere over the Pacific Ocean. It’s a 14-hour flight from California to New Zealand, and the plane carries two crews.

It’s a genuine four movie flight. I’ll take off on Sunday and don’t arrive until Tuesday because I’ll be crossing the International Dateline. When I arrive, I’ll feel like death warmed over. It’s all in the name of research and finding that next great trading idea.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

June 14, 2019

Fiat Lux

Featured Trade:

(WEDNESDAY JUNE 26 BRISBANE, AUSTRALIA STRATEGY LUNCHEON)

(MAY 29 BIWEEKLY STRATEGY WEBINAR Q&A),

(TSLA), (BYND), (AMZN), (GOOG), (AAPL), (CRM), (UT), (RTN), (DIS), (TLT), (HAL), (BABA), (BIDU), (SLV), (EEM)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader June 12 Global Strategy Webinar with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Do you think Tesla (TSLA) will survive?

A: Not only do I think it will survive, but it’ll go up 10 times from the current level. That’s why we urged people to buy the stock at $180. Tesla is so far ahead of the competition, it is incredible. They will sell 400,000 cars this year. The number two electric car competitor will sell only 25,000. They have a ten-year head start in the technology and they are increasing that lead every day. Battery costs will drop another 90% over the next decade eventually making these cars incredibly cheap. Increase sales by ten times and double profit margins and eventually, you get to a $1 trillion company.

Q: Beyond Meat (BYND)—the veggie burger stock—just crashed 25% after JP Morgan downgraded the stock. Are you a buyer here?

A: Absolutely not; veggie burgers are not my area of expertise. Although there will be a large long-term market here potentially worth $140 billion, short term, the profits in no way justify the current stock price which exists only for lack of anything else going on in the market. You don’t get rich buying stocks at 37 times company sales.

Q: Are you worried about antitrust fears destroying the Tech stocks?

A: No, it really comes down to a choice: would you rather American or Chinese companies dominate technology? If we break up all our big tech companies, the only large ones left will be Chinese. It’s in the national interest to keep these companies going. If you did break up any of the FANGS, you’d be creating a ton of value. Amazon (AMZN) is probably worth double if it were broken up into four different pieces. Amazon Web Services alone, their cloud business, will probably be worth $1 trillion as a stand-alone company in five years. The same is true with Apple (AAPL) or Google (GOOG). So, that’s not a big threat overhanging the market.

Q: Is it time to buy Salesforce (CRM)?

A: Yes, you want to be picking up any cloud company you can on any kind of sizeable selloff, and although this isn’t a sizeable selloff, Salesforce is the dominant player in cloud plays; you just want to keep buying this all day long. We get back into it every chance we can.

Q: Do you think the proposed merger of United Technologies (UT) and Raytheon (RTN) will lower the business quality of United Tech’s aerospace business?

A: No, these are almost perfectly complementary companies. One is strong in aerospace while the other is weak, and vice versa with defense. You mesh the two together, you get big economies of scale. The resulting layoffs from the merger will show an increase in overall profitability.

Q: I had the Disney (DIS) shares put to me at $114 a share; would you buy these?

A: Disney stock is going to go up ahead of the summer blockbuster season, so the puts are going to expire being worthless. Sell the puts you have and then go short even more to make back your money. Go naked short a small non-leveraged amount Disney $114 puts, and that should bring in a nice return in an otherwise dead market. Make sure you wait for another selloff in the market to do that.

Q: What role does global warming play in your bullish hypothesis for the 2020s?

A: If people start to actually address global warming, it will be hugely positive for the global economy. It would demand the creation of a plethora of industries around the world, such as solar and other alternative energy industries. When I originally made my “Golden Age” forecast years ago, it was based on the demographics, not global warming; but now that you mention it, any kind of increase in government spending is positive for the global economy, even if it’s borrowed. Spending to avert global warming could be the turbocharger.

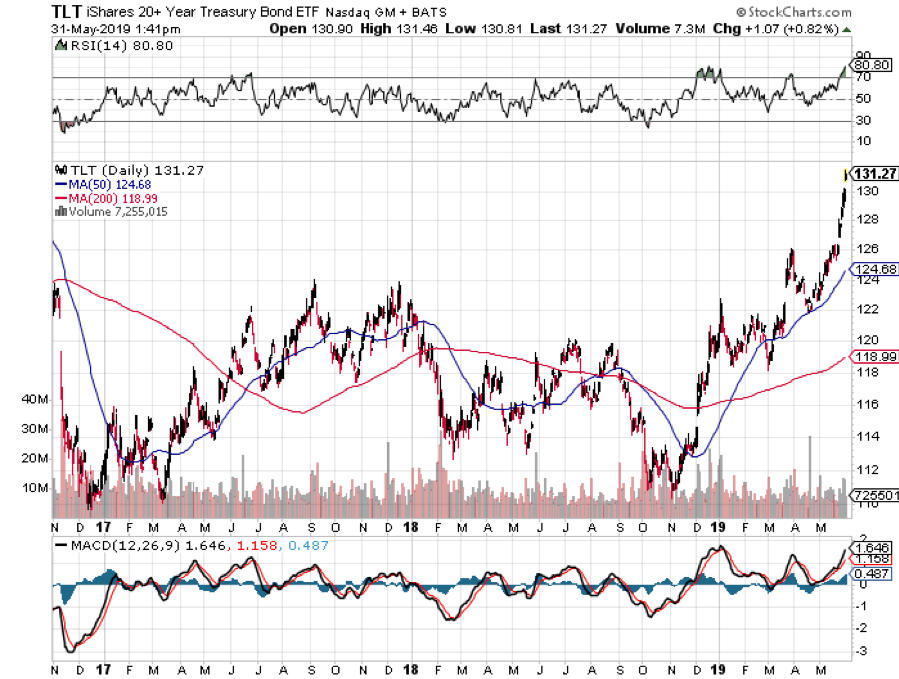

Q: Why not go long in the United States Treasury Bond Fund (TLT) into the Fed interest rate cuts?

A: I would, but only on a larger pullback. The problem is that at a 2.06% ten-year Treasury yield, three of the next five quarter-point cuts are already priced into the market. Ideally, if you can get down to $126 in the (TLT), that would be a sweet spot. I have a feeling we’re not going to pull back that far—if you can pull back five points from the recent high at $133, that would be a good point at which to be long in the (TLT).

Q: Extreme weather is driving energy demand to its highest peak since 2010...is there a play here in some energy companies that I’m missing?

A: No, if we’re going into recession and there’s a global supply glut of oil, you don’t want to be anywhere near the energy space whatsoever; and the charts we just went through—Halliburton (HAL) and so on—amply demonstrate that fact. The only play here in oil is on the short side. When US production is in the process of ramping up from 5 million (2005) to $12.3 million (now), to 17 million barrels a day (by 2024) you don’t want to have any exposure to the price of oil whatsoever.

Q: What about China’s FANGS—Alibaba (BABA) and Baidu (BIDU). What do you think of them?

A: I wanted to start buying these on extreme selloff days in anticipation of a trade deal that happens sometime next year. You actually did get rallies without a deal in these things showing that they have finally bottomed down. So yes, I want to be a player in the Chinese FANGS in expectation of a trade deal in the future sometime, but not soon.

Q: Silver (SLV) seems weaker than gold. What’s your view on this?

A: Silver is always the high beta play. It usually moves 1.5-2.5 times faster than gold, so not only do you get bigger rallies in silver, you get bigger selloffs also. The industrial case for silver basically disappeared when we went to digital cameras twenty years ago.

Q: Does this extended trade war mean the end for emerging markets (EEM)?

A: Yes, for the time being. Emerging markets are one of the biggest victims of trade wars. They are more dependent on trade than any of the major economies, so as long as we have a trade war that’s getting worse, we want to avoid emerging markets like the plague.

Q: We just got a huge rebound in the market out of dovish Fed comments. Is this delivering the way for a more dovish message for the rest of the year?

A: Yes, the market is discounting five interest rate cuts through next year; so far, the Fed has delivered none of them. If they delayed that cutting strategy at all, even for a month, it could lead to a 10% selloff in the stock market very quickly and that in and of itself will bring more Fed interest rate cuts. So, it is sort of a self-fulfilling prophecy. The bottom line is that we’re looking at an ultra-low interest rate world for the foreseeable future.

Good Luck and Good Trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

June 3, 2019

Fiat Lux

Featured Trade:

(MONDAY, JUNE 24 MELBOURNE, AUSTRALIA STRATEGY LUNCHEON)

(MARKET OUTLOOK FOR THE WEEK AHEAD, OR WHAT A WASTE OF TIME!),

(SPY), ($INDU), (JPM), (MSFT), (AMZN), (TSLA)

“Sell in May and go away” has long suffered from the slings and arrows of non-believers, naysayers, and debunkers.

Not this time.

Looking at the trading since April 30, we have barely seen an up day. Since then, the Dow Average has plunged 1,900 points from a 26,700 high, a loss of 7.1%. We are now sitting right at my initial downside target of the 200-day moving average.

The Dow has now given up virtually all its 2019 gains, picking up only 2.0%. In fact, the market is dead unchanged since the end of 2017. If you have been an index investor for the past 17 months, your return has been about zero. In other words, it has been a complete waste of time.

There are a lot of things I would have preferred to do rather than invest in index funds for the past year and a half. I could have hiked the Pacific Crest Trail….twice. I might have taken six Cunard round-the-world cruises and met several rich widows along the way. I might even have become fluent in Italian and Latin. Such is the value of 20-20 hindsight.

You would have done much better investing in the bond market, which has exploded to a new two-year high, taking the ten-year US Treasury yield down to a once unimaginable 2.16%. During the same period, the (TLT) has gained 11 points, or 9.0% plus another 3.0% worth of interest. You did even better if you invested in lower grade credits.

Which leads us to the big question: Will stocks bottom out here, or are we in for a full-on retrace to the December lows?

Unfortunately, recent events have conspired to point to the latter.

The United States has now declared trade wars against all neighbors and allies around the world: China, Mexico, Europe, and Canada. On Friday, it announced 25% punitive tariffs against Mexico before NAFTA 2.0 was even ratified before Congress, thus rendering it meaningless. Businesses are dropping like flies.

As a result, GDP forecasts have been falling off a cliff, down from 3.2% in Q1 to under 1% for Q2. The administration’s economic policy seems to be a pain now, and more pain later. It is absolutely not what stock investors want to hear.

If you are a business owner now, what do you do with the global supply chain being put through a ringer? Sit as firmly on your hands as possible and do nothing, waiting for either the policy or the administration to change. Stock investors don’t want to hear this either. The fact that stock markets entered this cluster historically expensively is the fat on the fire.

Having hummed the bear national anthem, I would like to point out that stocks could rally from here. We enter a new month on Monday. There will be plenty of opportunities to make amends and the G-20 meeting which starts on June 20. This should provide a backdrop for a rally of at least one-third of the recent losses, or about 600 points.

But quite honestly, if that happens, I’ll be a seller. The economy is doing the best impression of going down the toilet that I can recall, and that includes 2008. Only this time, all the injuries are self-inflicted.

As the trade war ramped up, China moved to ban FedEx (FDX) and restrict rare earth exports (REMX) to the US essential for all electronics manufacture. Most modern weapons systems can’t be built without rare earths. The big question in investors' minds becomes “Is Apple next?”

The OECD cut its global growth forecast from 3.9% to 3.1% for 2019 because of you know what. Stock markets are now down for their sixth week as the 200-day moving average comes within striking distance.

There was more bad news for real estate with April Pending Home Sales down 1.5%. If rates this low can’t help it, nothing will. Where are those SALT deductions?

The bear market in home prices continued in March with the Case Shiller CoreLogic National Home Price Index showing a 3.7% annual price gain, down 0.2%. Home price in San Francisco is posting negative numbers. When will those low-interest rates kick in?

The bond market says the recession is already here with ten-year interest rates at 2.16%, a new 2019 low. German bunds hit negative -0.21%. JP Morgan (JPM) CEO Jamie Diamond says the trade war could cause real damage to the US economy.

US Capital Goods fell out of bed in April, down 0.9%, in another important pre-recession indicator. No company with sentient management wants to expand capacity ahead of an economic slowdown.

Despite all the violence and negativity, the Mad Hedge Fund Trader managed to crawl to new all-time highs last week, thanks to some very conservative positioning on the long side in the right names.

Those would include Microsoft (MSFT), Amazon (AMZN), and Tesla (TSLA). All of these names were down on the week, but the vertical bull call spreads were up. You see, there is a method to my madness!

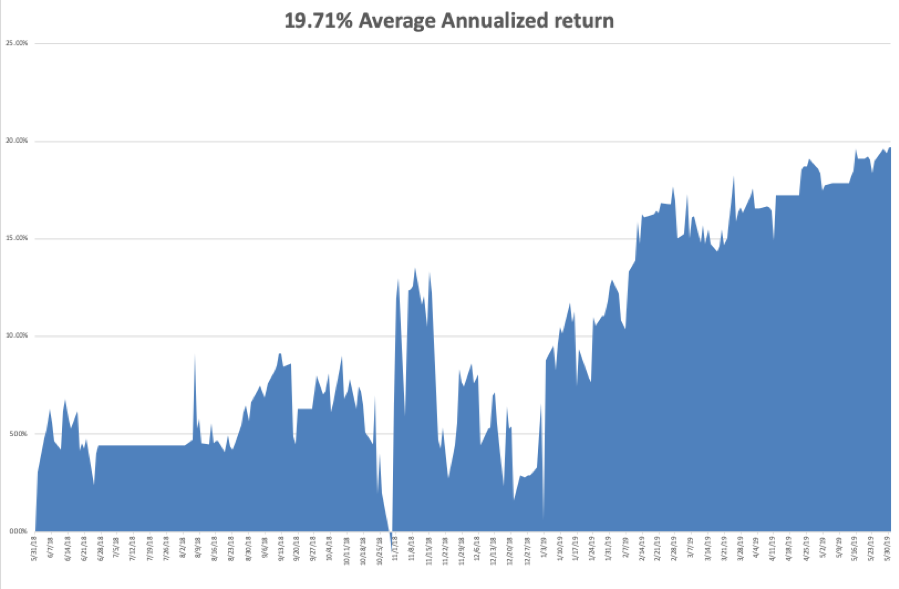

Global Trading Dispatch closed the week up 16.30% year-to-date and is up 0.51% so far in May. My trailing one-year declined to +19.71%.

The Mad Hedge Technology Letter did fine, making money on longs in Microsoft (MSFT) and Amazon (AMZN). Some 10 out of 13 Mad Hedge Technology Letter round trips have been profitable this year.

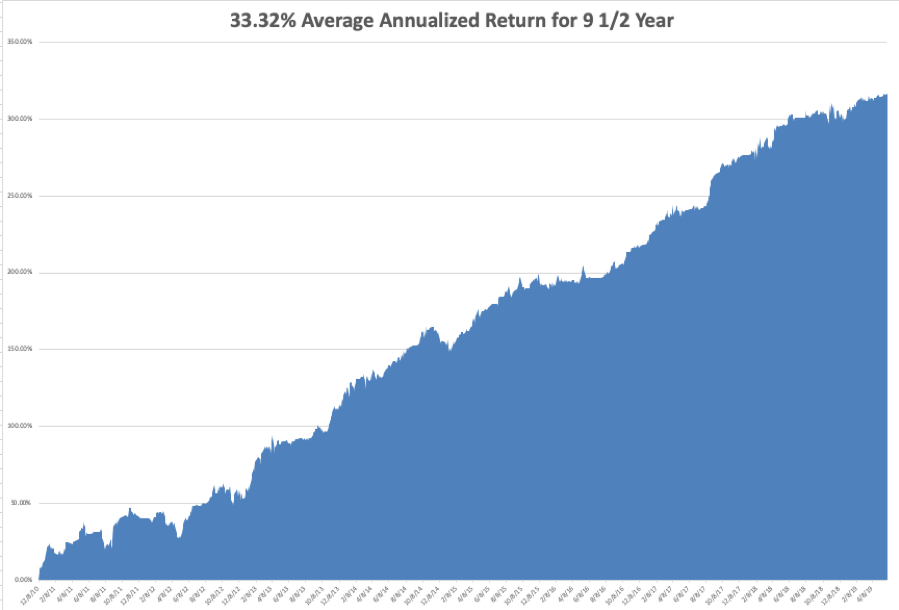

My nine and a half year profit jumped to +316.55%. The average annualized return popped to +33.32%. With the trade war with China raging, I am now 70% in cash with Global Trading Dispatch and 80% cash in the Mad Hedge Tech Letter.

I’ll wait until the markets enjoy a brief short-covering rally before adding any short positions to hedge my longs.

The coming week will be a big one with the trifecta of big jobs reports.

On Monday, June 3 at 7:00 AM, the May US Manufacturing PMI is out.

On Tuesday, June 4, 9:00 AM EST, the April US Factory Orders are published.

On Wednesday, June 5 at 5:15 AM, the May US ADP Employment Report of private hiring trends is released.

On Thursday, June 6 at 5:30 AM, the April US Balance of Trade is printed. At 8:30 Weekly Jobless Claims are published.

On Friday, June 7 at 8:30 AM, we learn the May Nonfarm Payroll Report is announced which lately has been incredibly volatile.

As for me, I am going to be leading the local Boy Scout troop on a 20-mile hike with a 2,500-foot vertical climb in the Oakland Hills. Hey, you never know when Uncle Sam is going to come calling again. I need to stay boot camp-ready at all times.

At least I can still outpace the eleven-year-olds. I’ll be leaving my 60-pound pack in the garage so it should be a piece of cake.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader