Mad Hedge Technology Letter

April 21, 2025

Fiat Lux

Featured Trade:

(DIFFICULTY OF DOING BUSINESS FOR CHIP COMPANIES)

(NVDA), (TSM), (HUAWEI)

Mad Hedge Technology Letter

April 21, 2025

Fiat Lux

Featured Trade:

(DIFFICULTY OF DOING BUSINESS FOR CHIP COMPANIES)

(NVDA), (TSM), (HUAWEI)

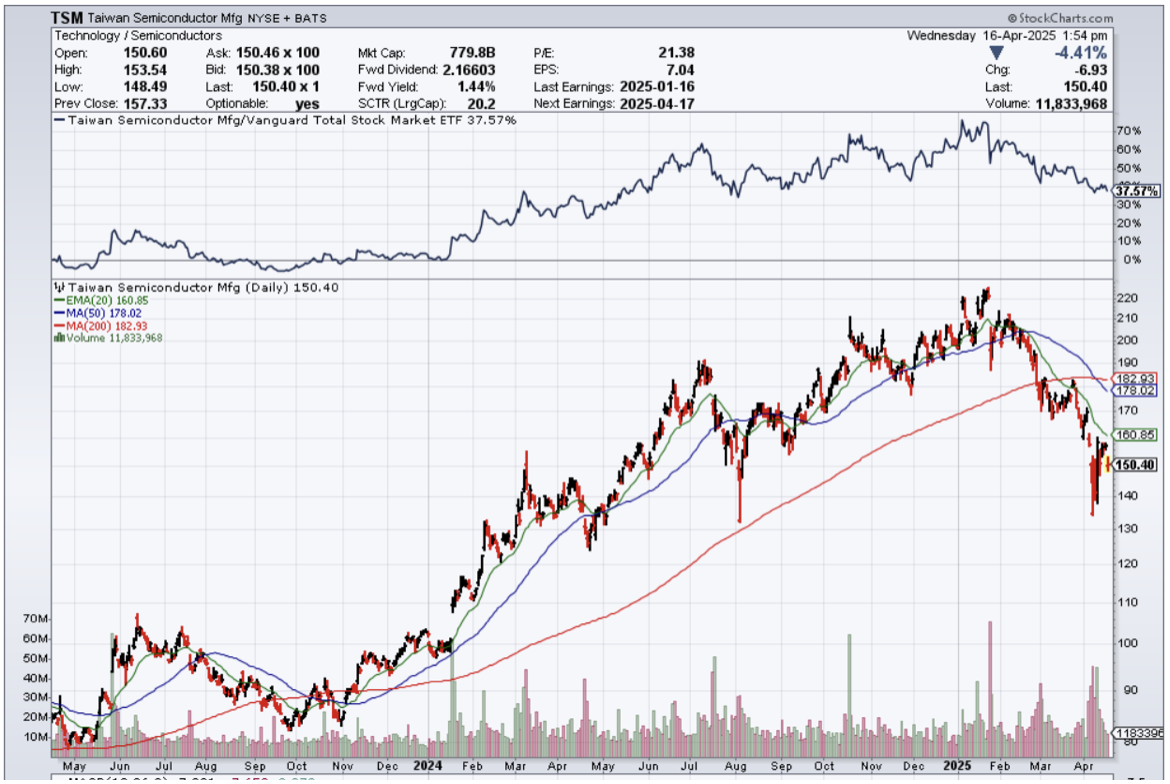

The U.S. appears to have made a massive blunder in its chip control blocking of China.

The U.S. Commerce Department said last week that Nvidia’s H20 graphics processing units — designed to comply with previous U.S. restrictions — would now require export licenses, as would additional chips from AMD. Nvidia says it has already halted exports of the GPUs, resulting in a quarterly charge of approximately $5.5 billion.

Could this be an example of the government getting in its own way?

Examples of these local AI chipmakers include tech powerhouse Huawei and the partially state-owned and publicly listed Cambricon Technologies, which designs GPUs.

Shares of Cambricon were up over 10% in the past five trading days amid news of the latest Nvidia controls. The stock is up over 400% in the past 12 months.

Can China fill the gap?

Huawei is the clear leader in China’s race to find an Nvidia competitor. The U.S.-blacklisted company has been working on its own improvements to compete with the leading technology.

Huawei remains about a generation behind in chips, but that won’t be the case for long.

Because TSMC’s chipmaking equipment includes U.S. technology, the company has complied with U.S. trade restrictions on Huawei and the shipment of advanced chips to China. That has left Chinese companies increasingly reliant on domestic foundries like Semiconductor Manufacturing International Corporation.

Nevertheless, SMIC is under its own export controls, which prevent it from accessing some of the world’s most advanced chipmaking equipment.

Are export controls working?

Chinese chip makers won’t need to immediately fill this H20 demand thanks to stockpiles and previous export exemptions and loopholes.

The U.S. government’s aggressive policy against the semiconductor industry is backfiring.

It is interesting that the Federal government never takes into consideration that loopholes and workarounds are possible and what the aftereffects are.

Sanctions can usually be subverted by using a third country to move the goods, and that is what we are seeing.

The end result is higher prices for all.

In general, an increase in the price of semiconductor chips would result in anything tech-related going up in price, and that is after a generation of deflation made devices cheap.

This also raises the price of doing business in AI. The GPUs needed for AI data centers will become more costly.

I could envision the future where harnessing AI software might be reserved for the well-off, because it won’t be cheap to use.

Each pressing day, the cost of business goes up as the globalization trends from post-World War 2 are being ripped to shreds by the existing administration.

Deglobalization is painful for the average person, but when you add on a tech sector in dysfunction, it really turns the screws on the investors.

What’s the end result?

In the short-term, semiconductor stocks will cool off because government obstruction means it is way harder to do business, let alone at profitable prices.

This restriction, this tariff, this rule, this forced export control, and the circus keep going with corporate management wishing one day to operate in a stable business environment.

Nothing is stable about the business environment now, forcing investment dollars to the sidelines.

In the short-term, sell any bear market rally in chip stocks.

Mad Hedge Technology Letter

April 16, 2025

Fiat Lux

Featured Trade:

(AMERICAN TECH ABLE TO OUTFLANK)

(NVDA), (TSM), (AAPL)

I understand that the U.S. administration wants to bring back American manufacturing, but that will not include Silicon Valley manufacturing.

There is a higher likelihood that if China is a no-go zone, American tech companies will venture out to a low-tariff, cheap labor country to continue their path to profits.

If you look through the numbers, it doesn’t make sense for American tech companies to manufacture goods in America.

The costs are too prohibitive.

Silicon Valley tech firms that are public on the New York markets have a fiduciary responsibility to shareholders to sustain short-term profits.

There is no mandate stating that these American tech companies must be manufactured in any specific sovereign country.

Silicon Valley companies are global, and American jobs lose out because of that.

This is a tough nut to crack because wages in rich Western countries dwarf the nominal amount in more affordable places.

U.S. Commerce Secretary Howard Lutnick said during an interview that the (China tariff) move was temporary.

Instead, he explained, tech products will be tariffed as part of the administration's planned duties on semiconductors, which could be announced later this week.

It's not just about timing. Companies would also need the workers to build devices.

While there's a degree of automation possible and while many of the components needed are made in the US, there's still a need for tens of thousands of trained electronics assemblers willing to work long, arduous hours in highly repetitive tasks.

Companies including Nvidia (NVDA), TSMC (TSM), Apple (AAPL), and others have announced increased investments in the US to win over Trump and avoid tariffs.

Nvidia said it will produce $500 billion in AI infrastructure in the US over the next four years through partners including Foxconn (601138.SS), TSMC, and Wistron (3231.TW).

And while that doesn't take away from the fact that the companies are pouring money into the US, it doesn't exactly support the idea that they're moving vast amounts of their manufacturing capabilities to America.

Even if companies brought their manufacturing bases to the US, they'd still have to deal with importing certain parts from abroad.

It's not just Apple that's contending with manufacturing headwinds; everything from laptop makers to display producers would face the same problems if they were to move to the US.

According to some estimates, prices on devices could double, resulting in demand destruction as consumers seek out less expensive options or hold onto their existing smartphones and computers for longer periods.

While it's unlikely manufacturing is coming back to the US, there's still plenty of uncertainty about how tech companies and consumers navigate the next four years of tariff shocks.

The biggest winners appear to be Vietnam or India, and much of the American tech manufacturing has their sights set on these places to reduce costs.

In short, this won’t destroy American tech and their shares will outperform in the long run, but in the short-term, it hurts, because it puts doubt into where they will produce their gizmos and gadgets.

At the very least, this gets American tech out of China, and I believe the federal government would be happy if businesses migrated to a more neutral country, even if they don’t come back home.

Either way, after this all blows over, there will be a great buying opportunity in American tech companies, which will all be trading at a discount.

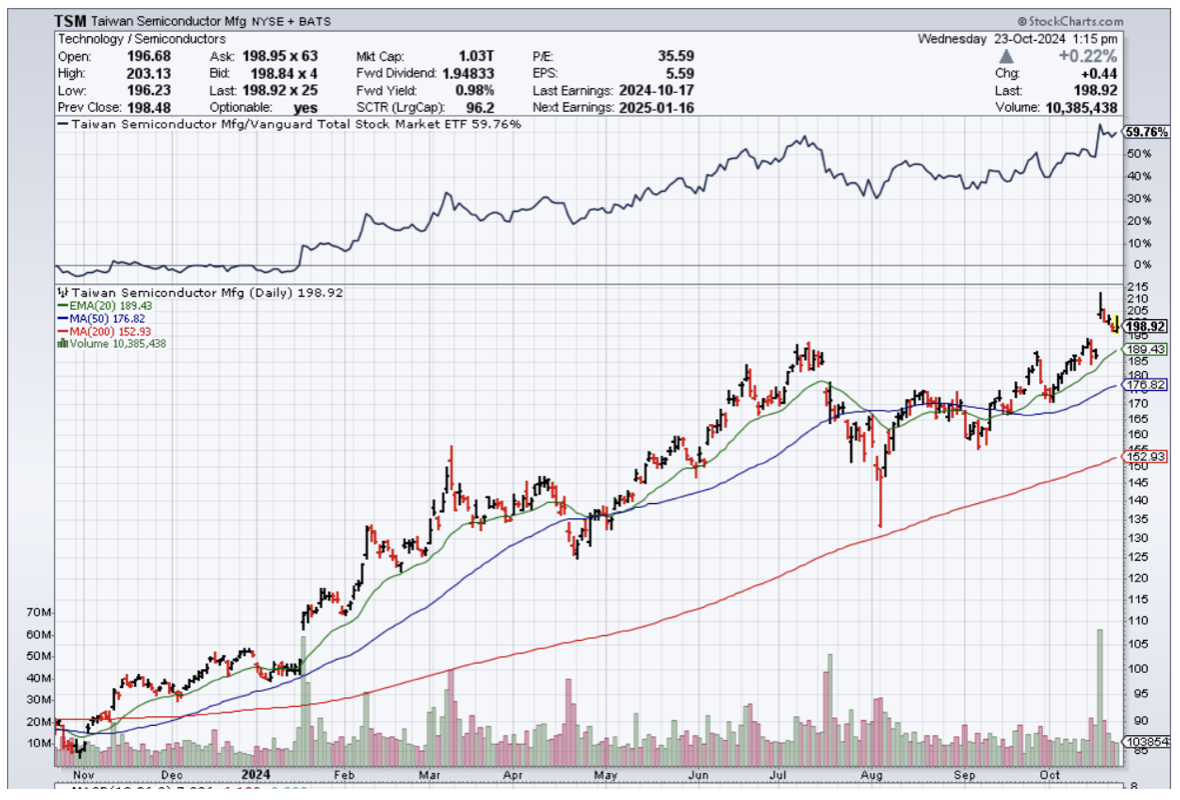

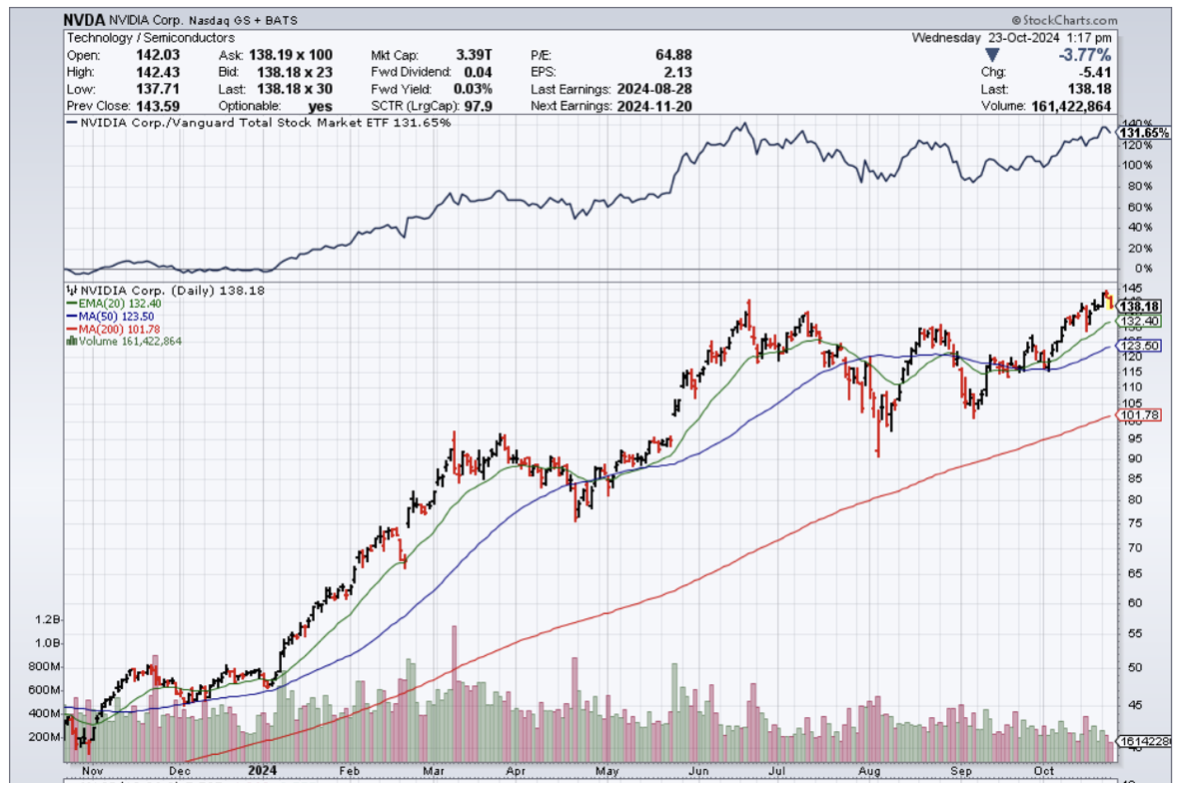

Mad Hedge Technology Letter

October 23, 2024

Fiat Lux

Featured Trade:

(ANOTHER GEM IN THE CHIP INDUSTRY)

(TSM), (NVDA)

The hottest part of the tech industry is the build-out of the AI infrastructure.

Millions of data centers are needed equipped with high-speed chips to facilitate the miracle that is artificial intelligence.

One of the leading companies right in the heat of the battle is Taiwan Semiconductor Manufacturing (TSM).

Why is TSM so important?

Nvidia (NVDA) outsources the manufacturing of its chip designs; TSM is the one doing the building, and that will mean a highly strategic position in AI moving forward.

TSM's other customers include several tech heavyweights like Advanced Micro Devices and Apple.

TSM has carved out a solid advantage in producing leading-edge logic chips used in advanced computing technologies such as AI and 5G mobile networks.

TSM is the world leader in manufacturing these specialized semiconductor chips, with an estimated 90% share of this market.

A key factor in TSM's market dominance is customer demand for chips using its three-nanometer (nm) semiconductor manufacturing process. Referred to as 3nm, this technology creates chips with greater microprocessor speed, lower energy consumption, and exceptional computational power without increasing chip size.

This 3nm tech looks like a game-changer for TSM. The process produces better chips than its older 7nm technology, which was once responsible for over a third of the company's revenue a mere three years ago. Just last year, TSM's 3nm-related revenue was a tiny 6% of third-quarter sales. But the rapid rise of AI drove 3nm income to reach 20% of quarter three revenue this year.

As 3nm-manufactured chips become more widely adopted, TSM's market share in this sector is expected to grow. This is because TSM's 3nm process generates higher yields and power efficiencies compared to those made by such competitors as Samsung.

TSM's 3nm strengths position the firm for revenue growth in the coming years. The market for the technology is forecast to skyrocket from $1.4 billion in 2023 to $26.5 billion by 2032.

With its 3nm process taking off, TSM experienced strong sales in the third quarter as revenue rose 36% year over year to $23.5 billion.

TSM's long-term sales potential looks to get a boost from the expansion of its chip fabrication facilities. Because leading-edge logic chips are needed for advanced computing, the U.S. government is incentivizing TSM to build semiconductor factories in the United States.

The underlying stock has delivered a 92% performance in the first 10 months of the year.

They certainly didn’t get left behind by the success of Nvidia, and I believe as we move forward, their strategic importance to the industry will grow and fortify.

I don’t believe that there is any slowdown in the pipeline coming any time soon.

The rhetoric from the AI chip management has been bragging about the over-demand and undersupply of chips.

This has created a massive surge in the profits for AI chip firms.

In the short term, the only negative that comes to mind would be that chip firms could be the victim of their own success reflected in overheated stock price trends.

We are due for a pullback, and that would certainly constitute as a buy-the-dip moment.

We have not seen the best of TSM yet, the best is yet to come.

Mad Hedge Technology Letter

March 27, 2024

Fiat Lux

Featured Trade:

(TAIWAN IS ON THE MAP)

(AAPL), (TSM)

I know it’s not the sexiest choice but there is a chip company in Taiwan that readers need to look at.

This company has investments all over the world and is the leader in what they do.

They are also involved in AI which lately has been the ticket to riches.

Taiwan Semiconductor Manufacturing Company (TSM) may not seem like a glamorous AI stock, but it's as critical to the AI future.

To understand TSMC's role in AI, you need to understand how we get to end consumer-facing products like ChatGPT, Bard, and other generative AI applications.

For AI to be effective, it must be trained using lots of data -- quantities that must be stored in specialized data centers.

Data centers rely on graphic processing units (GPUs), which are essentially the brains of AI computing systems.

TSMC and the semiconductors it manufactures for its client companies are crucial in this process. These GPUs rely heavily on TSMC's best-in-class manufacturing processes.

This AI knock-on effect hasn't impacted TSMC's financials yet, but management said they expect sales of its AI-related semiconductors to grow at a compound annual rate of 50% for at least the next few years.

By 2027, AI-related semiconductors are expected to be responsible for a large part of the company's revenue.

TSMC will absolutely be additive to the AI ecosystem.

Let’s talk about their products.

TSMC's 3nm fabrication process accounted for 15% of the company's revenue in 2023.

Only one of TSMC's customers used it at the time:

Apple (AAPL).

The three-nanometer product is where it’s at.

Wasn’t it just a year or 2 ago we were at 7 nanometers?

As more customers adopt the manufacturing process, 3nm process nodes will account for a considerably larger share of TSMC's revenue.

This year TSMC's N3-series nodes — including N3B and N3E — will account for over 20% of the foundry's revenue in 2024.

Apple currently exclusively uses TSMC's N3B to make its A17 Pro system-on-chip (SoC) for smartphones, as well as the M3-series processors for iMac desktops and MacBook laptops.

AMD is preparing to launch its new Zen 5-based processors made on 3nm- and 4nm-class process technologies later this year.

Apple's new iPhone 16 series will be equipped with the A18-series processor, and the upcoming M4-series processors for Mac PCs will also be produced using TSMC's 3nm technology.

This marks the first time Intel has entrusted TSMC with the full range of chips for its mainstream consumer platform, the report notes.

This collaboration highlights TSMC's expanding role in serving Intel, which also happens to be the company's rival in the foundry market.

With three major customers using TSMC's 3nm family of process technologies, this company needs to be on readers’ radar.

More companies are expected to adopt TSMC's N3 nodes in 2025, including performance-enhanced N3P, and the report suggests 3nm will account for over 30% of TSMC earnings in 2025.

It’s easy to see with the mushrooming of business for TSMC, how they are a highly sought-after stock.

It also explains why the stock has been on a tear.

It was only just last May they were trading at $82 per share and fast forward to today at the stock sits at $136 per share.

Holding this stock long term has borne fruit and every big should be bought.

They will continue to be the best at what they do.

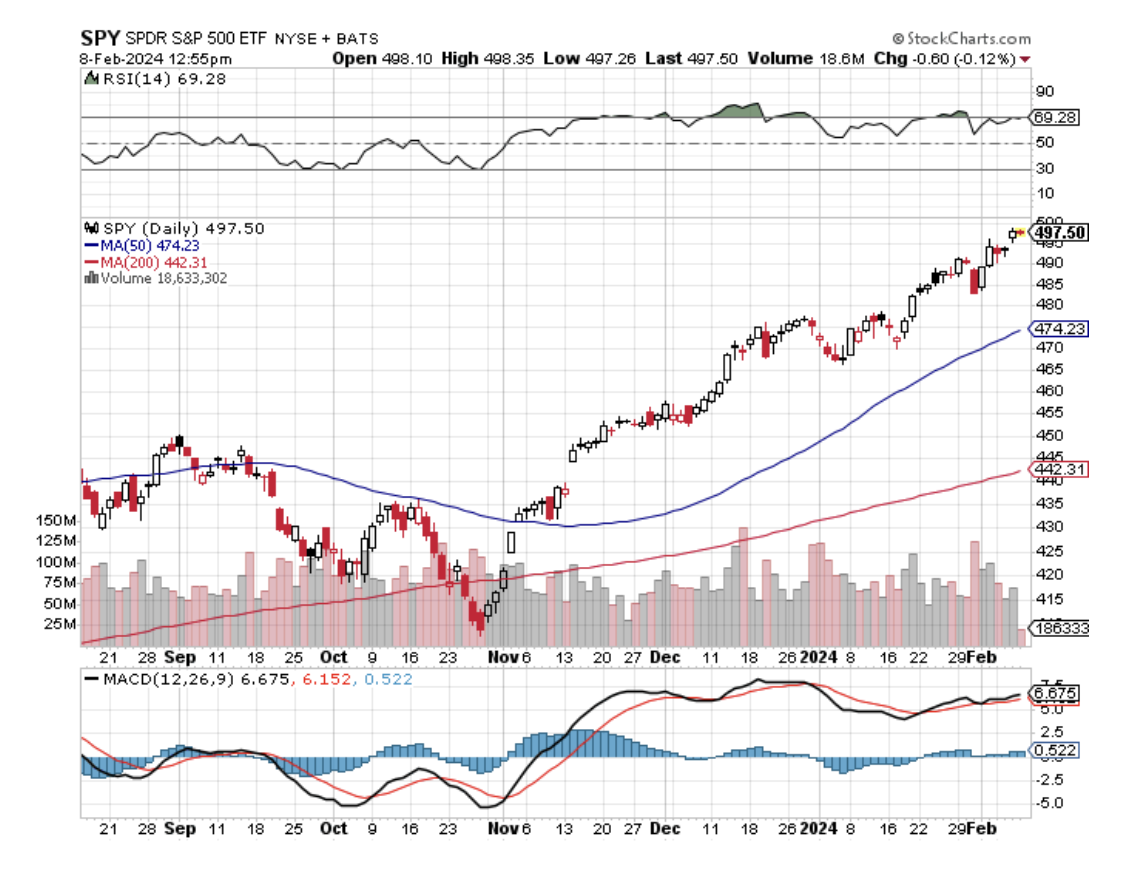

Global Market Comments

February 9, 2024

Fiat Lux

Featured Trade:

(FEBRUARY 7 BIWEEKLY STRATEGY WEBINAR Q&A),

(LLY), (FXI), (TSM), (BABA), (PLTR), (MSBHF), (SMCI), (JPM), (INDY), (INDA), (TSLA), (BYDDF), (NFLX), (META), (UNG)

Below please find subscribers’ Q&A for the February 7 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Silicon Valley, CA.

Q: Have you ever flown an ME-262?

A: There's only nine of the original German jet fighters left from WWII in museums. One hangs from the ceiling in the Deutsches Museum in Munich (click here for the link), I have been there and seen it and it is truly a thing of beauty. You would have to be out of your mind to fly that plane, because the engines only had a 10 hour life. That's because during WWII, the Germans couldn't get titanium to make jet engine blades and used steel instead, and those fell apart almost as soon as they took off. So, of the 1,443 ME-262’s made there’s only nine left. The Allies were so terrified of this plane, which could outfly our own Mustangs by 100 miles per hour, that they burned every one they found. That’s also why there are no Japanese Zeros.

Q: Thoughts on Palantir (PLTR) long term?

A: I love it, it’s a great data and security play. Right now, markets are revaluing all data plays, whatever they are. But it is also overvalued having almost doubled in a week.

Q: What do you make of all these layoffs in Silicon Valley? What does this mean for tech stocks?

A: It means tech stocks go up. The tech stocks for a long time have practiced over-employment. They were growing so fast, they always kept a reserve of about 10% of extra staff so they could be put them to work immediately when the demand came. Now they are switching to a new business model: fire everybody unless you absolutely have to have them right now, and make everybody you have work twice as hard. That greatly increases the profitability of these companies, as we saw with META (META), which had its profits triple—and that seems to be the new Silicon Valley business model. If you're one of the few 100,000 that have been laid off in Silicon Valley, eventually the economy will grow back to where they can absorb you. That's how it's going to play out. In the meantime, go take a vacation somewhere, because you're not going to get any vacations once you get a new job.

Q: I have had shares of Alibaba (BABA) since 2020 and the stock has been in free fall since. Should I take the 80% loss or hold?

A: Well, number one, you need to learn about risk control. Number two, you need to learn about stop losses. I stop out when things go 10% against me; that's a good level. At 80%, you might as well keep the stock. You've already taken the loss and who knows, China may recover someday. It's not recovering now because no foreigners want to invest in China with all the political risk and invasion risk of Taiwan. After all, look at what happened to Russia when they invaded Ukraine—that didn't work out so well for them.

Q: On the Chinese economy (FXI), is the poorer performance due to the decision to move to a war economy? The move in the economic front was described in Xi's speech to the CCP in January of 2023.

A: The real reason, which no one is talking about except me, is the one child policy, which China practiced for 40 years. What it has meant is you now have 40 years of missing consumers that were never born. And there is no solution to that, at least no short-term solution. They're trying to get Chinese people to have more kids now, and you're seeing three and four child families for the first time in 40 years in China. But there is no short-term fix. When you mess with demographics, you mess with economic growth. We warned the Chinese this would happen at the time, and they ignored us. They said if they hadn't done the one child policy, the population of China today would be 1.8 billion instead of 1.2 billion. Well, they’re kind of damned no matter what they do so there was no good solution for them. Of course, threatening to invade your neighbors is never good for attracting foreign investment for sure. Nobody here wants to touch China with a 10-foot pole until there’s a new leader who is more pacifist.

Q: What do you think of Eli Lilly (LLY)?

A: I absolutely love it. If there's a never-ending bull market in fat Americans, which is will go on forever, they're one of two companies that have the cure at $1,000 a month. On the other hand, the stock has tripled in the last 18 months, so it’s kind of late in the game to get in.

Q: Are there any stocks that become an attractive short in the event of a Taiwan invasion, such as Taiwan Semiconductor (TSM)?

A: All stocks become attractive shorts in the event of another war in China. You don't want to be anywhere near stocks and the semis will have the greatest downside beta as they always do. You don't want to be anywhere near bonds either, because the Chinese still own about a trillion dollars’ worth of our bonds. Cash and T-bills suddenly looks great in the event of a third war on top of the two that we already have in Gaza and Ukraine.

Q: What do you think about the prospects of the Japanese stock market now?

A: I think the big move is done; it finally hit a new high after a 34-year wait. The next big move in Japan is when the Yen gets stronger, and that is bad for Japanese stocks, so I would be a little cautious here unless you have some great single name plays like Warren Buffett does with Mitsubishi Corp. (MSBHF). So that's my view on Japan—I'm not chasing it after being out for 34 years. Why return? The companies in the US are better anyway.

Q: What is the deal with Supermicro Computer (SMCI)? It went up 23 times in a year to $669 after not clear $30 for a decade.

A: The answer is artificial intelligence. It is basically creating immense demand for the entire chip ecosystem, including high end servers, which Supermicro makes. It also has the benefit of being a small company with a small float, hence the ballistic move. It was too small to show up on my radar. I’ll catch the next one. There are literally thousands of companies like (SMCI) in Silicon Valley.

Q: Will JP Morgan (JPM) bank shares keep rising, or will they fall when the Fed cuts rates?

A: (JPM) will keep rising because recovering economies create more loan demand, allow wider margins, and cause default rates to go down. It becomes a sort of best case scenario for banks, and JP Morgan is the best of the breed in the banking sector. It also benefits the most from the concentration of the US banking sector, which is on its way from 4,000 banks to 6 with help from the US government.

Q: Is India a good long-term play? Which of the two ETFs I recommend are the better ones?

A: Yes, India is a good long-term play. You buy both iShares India 50 (INDY) and the iShares MSCI India (INDA), which I helped create yonks ago. India is the new China, and the old China is going nowhere. So, yes, India definitely is a play, especially if the dollar starts to weaken.

Q: Do you expect to pull back in your market timing index?

A: Yes, probably this month. Have I ever seen it go sideways at the top for an extended period? No, I haven't. On the other hand, we’ve never had a new thing like artificial intelligence hit the market, nor have we seen five stocks dominate the entire market like we're seeing now. So, there are a lot of unprecedented factors in the market now which no one has ever seen before, therefore they don't know what to do. That is the difficulty.

Q: Does India have an in-country built EV, and what is their favorite EV in India?

A: No, but Tesla (TSLA) is talking about building a factory there. And I would have to say BYD Motors (BYDDF) because they have the world’s cheapest EV’s. There is essentially no car regulation in India except on imports. Car regulation and safety requirements is what keeps the BYDs out of the United States, and it's kept them out for the last 15 years. So that is the issue there.

Q: What do you think about META as a dividend play?

A: I think META will go higher, but like the rest of the AI 5, it is desperately in need of a pull back and a refresh to allow new traders to come in.

Q: Why does Netflix (NFLX) keep going up? I thought streaming was saturated—what gives?

A: Netflix won the streaming wars. They have the best content and the best business strategy; and they banned sharing of passwords, which hit my family big time since it seemed like the whole world was using my Netflix password. And no, I'm not going tell you what my password is. I’ve already paid for Griselda enough times. Seems there is a lot of demand for strong women in my family. Netflix they seem to be enjoying a near monopoly now on profits.

Q: Has the NASDAQ come too far too fast, and does it have more to run?

A: Well it does have more to run, but needs a pull back first. I'm thinking we'll get one this month, but I'm definitely not shorting it in the meantime.

Q: Have you ordered your Tesla (TSLA) Cybertruck?

A: I actually ordered it two years ago and it may be another two year wait; with my luck the order will come through when I'm in Europe and I'll miss it. Some of my friends have already gotten deliveries because they ordered on day one. They love it.

Q: What happened to United States Natural Gas (UNG)?

A: A super cold spell hit the Midwest, froze all the pipes, and nobody could deliver natural gas just when the power companies were screaming for more gas. That created the double in the price which you should have sold into! Usually, people don't need to be told to take a profit when something doubles in 2 weeks, but apparently there are some out there as I've been here getting emails from them. Further confusing matters further is that (UNG) did a 4:1 reverse split right at this time. They have to do this every few years or the 35% a year contango takes the price below $1.00 and shares can’t trade below $1.00 on the New York Stock Exchange.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, select your subscription (GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or Jacquie's Post), then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader