Mad Hedge Technology Letter

February 15, 2023

Fiat Lux

Featured Trade:

(NOT ALL AD TECH FIRMS ARE IN THE DOGHOUSE)

(TTD), (GOOGL), (META)

Mad Hedge Technology Letter

February 15, 2023

Fiat Lux

Featured Trade:

(NOT ALL AD TECH FIRMS ARE IN THE DOGHOUSE)

(TTD), (GOOGL), (META)

Some of the digital ad tech stocks have had a rough go of it lately.

There was Google (GOOGL), whose stock has been threatened because of the new artificial intelligence chat box technology that was debuted by OpenAI called ChatGPT.

Meta (META) has rebounded but the initial sell-off last year was cringe-worthy.

As we see the light at the end of the tunnel, it’s time to explore where to deploy funds to invest in tech, and one option is The Trade Desk (TTD).

The advertising-technology company issued a stronger-than-expected outlook and unveiled a $700 million stock buyback program.

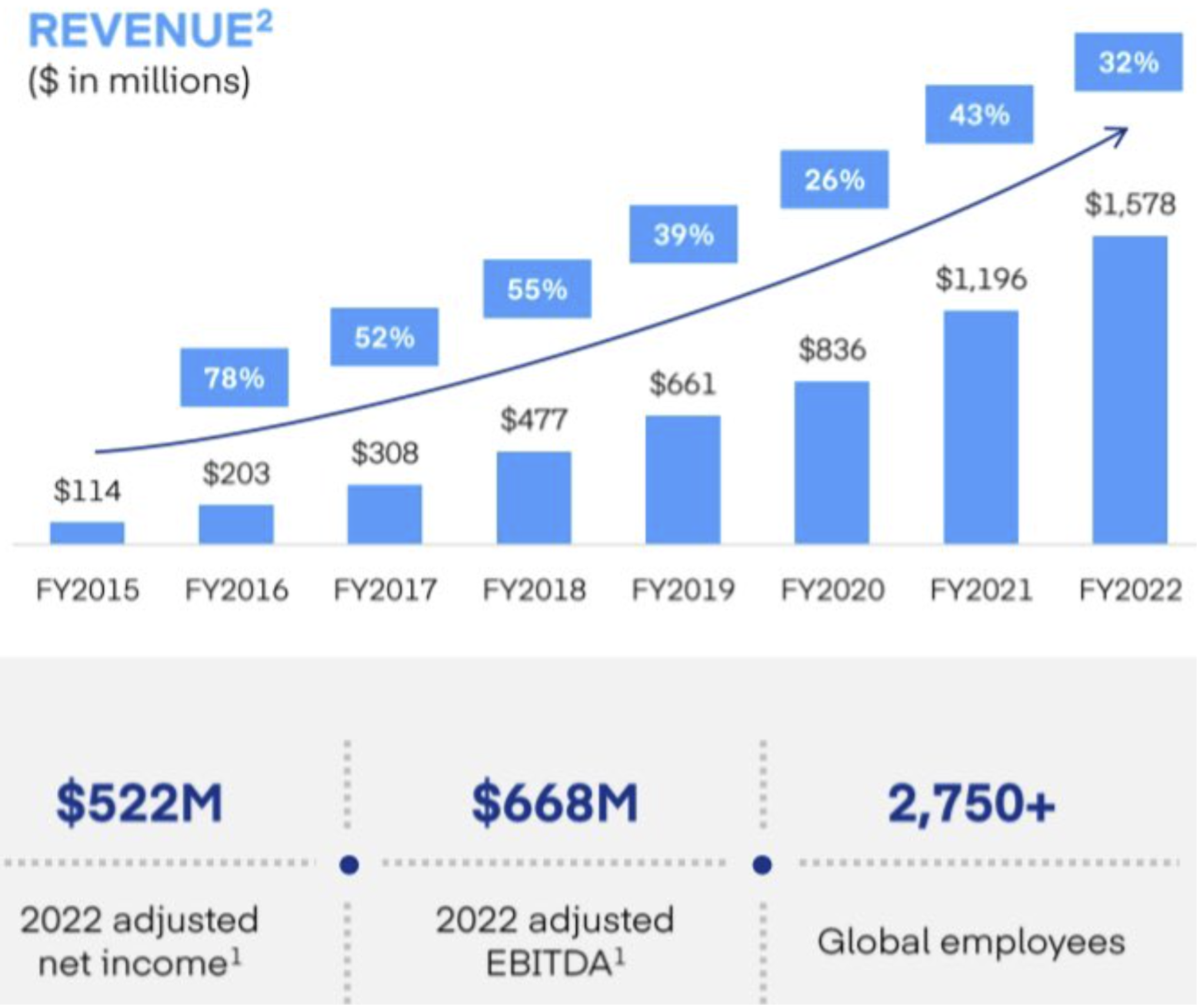

The Trade Desk outpaced nearly all areas of digital advertising in 2022, with 32% revenue growth year over year, and a record $491 million of revenue in the fourth quarter alone.

In addition, management at The Trade Desk made significant operational progress during the first quarter.

For example, Adobe was won as a partner that carries out real-time integration. But a first certified service partner has also been won with the Goodway Group. Growth in the area of programmatic advertising therefore continues.

I can confidently say that they delivered great earnings results once again and that’s a good habit to have in the public markets.

The company's top line didn't beat expectations, but was still impressive, especially considering a macroeconomic environment that weighed on the broader advertising industry.

Analyzing their company, I am confident that they are gaining market share and that their platform continues to gain traction with advertisers.

The numbers strongly back me up.

While the company's sales grew by 24% in the fourth quarter, some of The Trade Desk's biggest competitors were seeing their sales decline.

Another highlight from the quarter is The Trade Desk keeping its customer retention rate above 95%, which it has done for nine consecutive quarters.

The company also said that its Unified ID 2.0 - an online identifier that gives users more privacy than online trackers - continues to be accepted by more companies, including the addition of Paramount Advertising in the quarter.

Management expects Unified ID 2.0 to continue growing as online trackers (called cookies) "become less important" in the ad industry.

I can’t say it has been the golden year for digital ad tech.

The beating it took last year was quite horrendous, but as all rate hikes have mostly been priced into shares, we can expect a positive trajectory to the upside.

It’s quite positive that in the last two days, we received a hot CPI number and hot retail sales, but tech stocks have held up nicely.

I fully expect many growth tech stocks including TTD to become buy-the-dip candidates moving through the bulk of the year.

Sure, higher inflation remains the biggest risk to shares and after the latest numbers, we could go up to 5.25% on the Fed Funds rate but that has largely been quantified and sanitized by the market by now.

Mad Hedge Technology Letter

December 5, 2022

Fiat Lux

Featured Trade:

(A DIGITAL AD COMPANY TO LOOK AT FOR 2023)

(TTD)

We are headed to one of our worst years in tech stocks, but that doesn’t mean it is all bad.

It’s time to look at a digital ad company that could make your portfolio next year.

Many subsectors of tech have not been left unscathed, but I do see pockets of strength and there is one particular company that has done admirably this year even if its stock price has gotten hammered.

Robust tech stock next year will be the ones that had great business models and healthy profitable profiles this year.

Numbers will only improve.

The company I’m thinking about is digital ad company The Trade Desk (TTD).

The massive global advertising industry is not yet done, and it really is the present and future.

Don’t put a fork in it.

Television ads are quite a dinosaur at this point and TTD is in the business of selling digital ad inventory.

However, a number of headwinds this year slowed the stock. Amidst heightened economic uncertainty, many brands are halting marketing budgets.

Another problem that has been extensively chronicled is the collateral damage from Apple's privacy updates.

This allows users to opt out of app activity tracking lowering the value of digital ads on the lucrative iOS operating system.

In general, digital advertising technology will continue to expand and The Trade Desk (TTD) will be a growth element of that expansion.

The Trade Desk has been a best-in-class player in the advertising ecosystem for years.

A demand-side platform that helps marketers purchase ads from publishers, the company champions the "open internet."

It doesn't compete with its customers in the way that Alphabet's Google and other internet and media giants.

In addition, many of its ad marketplace and software solutions are open source allowing marketing agencies and the brands they represent to build their own proprietary systems atop The Trade Desk's platform.

Revenue in the 3rd quarter was up 31% year over year, compounding the 39% year-over-year increase in the same period of 2021.

Another problem tech firms face while their stock price is low is the high cost of stock-based compensation.

Stock-based comp was a drag on earnings per share last quarter as it totaled $121 million compared to $34.5 million last year.

Nevertheless, The Trade Desk remains highly profitable.

The balance sheet remains in pristine condition as well, with $1.32 billion in cash and short-term investments and zero debt as of the end of September.

Although the stock price has halved from the November 2021 peak, the stock is well placed for a positive 2023.

Revenue is growing around a 30% clip during down times and once the Fed starts lowering rates, TTD will be off to the races and you want to be on board.

The weakness in tech shares has been painful for everybody as literally, every force went against tech in 2022.

Growth tech will outperform traditional tech stocks as the liquidity gates start to open and there’s a strong chance the Fed will start to pivot before 2023 is done.

Mad Hedge Technology Letter

October 1, 2021

Fiat Lux

Featured Trade:

(CONNECTED TV IS ON FIRE)

(TTD), (DIS), (FUBO)

One of my favorite ad tech companies has to be The Trade Desk (TTD).

They are a middleman of sorts, using an in-house platform to match the inventory of digital ads with the advertisers themselves.

They have been extremely effective at harnessing data to deliver the right ads to the right people and many major streaming companies and Fortune 500 companies are reaching out to them to figure out how to deploy ads in the most systematic way possible.

Let’s just say there is a lot of slippage going on in the linear industry where wrong ad placement is common.

Performance of late has been strong in TTD — more of the world's top advertisers and their agencies signed up or expanded their use of TTD’s platform, which just continues to validate their business strategy.

Companies are now increasingly embracing the opportunities of the open Internet in contrast to the limitations of walled gardens.

The highlight of last quarter’s performance is led by Connected TV (CTV) and premium video.

What is CTV in advertising? CTV is short form, skippable online advertising targeted to relevant content channels and/or audience groups. Connected TV (CTV) refers to any TV that can be connected to the internet and access content beyond what is available via the normal offering from a cable provider.

The CTV growth coincides with a broad move from broadcast and cable to digital on-demand content that is happening all over the world.

CTV as a percentage of TTD’s business continues to grow very rapidly and is, by far, their fastest-growing channel.

Overall, total revenue was up 101% from a year ago to $280 million, significantly surpassing in-house expectations.

Growth occurred mainly because of TTD’s latest platform launch, Solimar, which is the result of more than two years of engineering work, and it addresses many of the opportunities in front of agencies and brands today.

Just to provide some context on growth in CTV, through just the first half of this year, the number of brands spending more than $1 million in CTV to TTD has already more than doubled year over year.

And it's not just larger advertisers that are taking advantage of CTV anymore. The number of advertisers spending over $100,000 has also doubled. In total, TTD has nearly 10,000 CTV advertisers, up over 50% compared to last year.

That exponential growth speaks to how rapidly the TV landscape is evolving. The accelerated consumer shift to digital video is real, including CTV. And that shows no signs of slowing down.

In fact, TTD reached more households via CTV in the U.S. today than are reachable through linear TV. Today, TTD reaches more than 87 million households. Those trends are now well established.

MoffettNathanson recently reported that the ad-supported video-on-demand market is growing from $4.4 billion in 2020 to about $18 billion as early as 2025.

And every major ad-supported platform, whether it's Disney's Hulu, Peacock, Discovery Plus, ViacomCBS' Paramount and Pluto, FOX's 2B or fuboTV and many others, all are reporting record viewership or ad spend figures.

Broadcasters recognize that the traditional upfront process is a mismatch. It doesn't work in a digital world where data and personalization are required to succeed.

The legacy upfront process is really hard to run in an environment with lots of change and lots of uncertainty. I believe that this year will mark a turning point in how the process is managed. In today's fragmented TV environment, linear audiences continue to erode, linear supply is shrinking and the prices are rising simply because of the scarcity. This year, broadcasters use that scarcity to their advantage and lock up commitments as the demand for growth intensifies.

When compared to parallel linear TV ad campaigns, CTV delivered a 51% incremental reach and a four times improvement when analyzing cost per household reach. These are not isolated cases.

Retail is a point of emphasis this year with Walmart integrating Walmart shopper data on TTD’s platform. This is a leading example of how TTD is working with advertising customers to help unlock the value of retail data estimated at $100 billion to $200 billion market.

This is a highly volatile stock and 2021 has been a year of consolidation.

If TTD comes down to $60 from the $70 today, that should represent an optimal entry point into one of the hottest sub-industries in tech.

Mad Hedge Technology Letter

May 12, 2021

Fiat Lux

Featured Trade:

(THE EXPLODING PROGRAMMATIC AD SPACE)

(TTD)

Annual advertising budgets are often being reset and reconsidered in Q1, but as the economy is roaring back, digital ad deliverers are set to make hay.

The Trade Desk (TTD) specializes in programmatic ad buying.

What is it?

It’s the deployment of software to buy digital advertising.

Previously, the traditional way included requests for proposals, tenders, quotes, and human negotiation, but programmatic buying uses machines and algorithms to purchase display space.

Humans now have more time for the optimization and evolution of ads.

Ad agencies will always need to optimize advertising to meet consumers’ needs on a deeper level.

Programmatic-centric software will deliver a better set of tools to plan, optimize and target advertising effectively.

Since TTD doesn’t make anything physical, margins are usually a lot higher and that certainly showed with Q1 producing adjusted EBITDA of a record $70.5 million.

This Q1 record is on both an absolute basis and a percentage of revenue basis.

As TTD continues to grow and represent more large brands and a larger percentage of ad agencies' brands, they will continue to become an accurate bellwether for the open Internet and advertising spend.

When you consider their performance in the context of the health of the overall advertising industry, you can see how they continue to outperform the industry and gain market share.

WPP's GroupM predicts worldwide advertising revenue will increase 10% in 2021. Publicis Groupe's Zenith expects overall U.S. ad spending to rise 3.2% in 2021, following a drop of 5.4% last year. GroupM also predicts digital advertising will surge 14% to nearly $400 billion.

Almost all major content owners put more premium inventory online.

Today, TV providers are fighting for consumer attention and there is more competition than ever.

The gap in cost-adjusted efficacy between linear and Connected TV (CTV) has stayed strong. However, as advertisers embrace CTV to leverage data and relevance, the power of data-driven targeting is quickly becoming more apparent.

Only effective data-driven targeting can achieve the value sought after by advertisers.

In other words, TV advertisers now have a choice. They have the ability to differentiate between content across channels more than ever. And that's critical to a healthy and competitive CTV market.

Now just to put the CTV market scale in perspective, according to Omdia's latest research, there are now more than 200 million active Advertising-Based Video on Demand (AVOD) users in the U.S. alone.

By 2024, Omdia predicts that annual CTV advertising revenue will top $120 billion, outperforming subscription revenue by more than 20%.

More and more of the world's top advertisers are making programmatic buys a larger component of their upfront commitments.

Advertisers want more data-driven flexibility in TV advertising campaigns. They believe their digital buys should be a core element of their upfront commitment. And the networks are adapting to that demand.

Ultimately, this will lead to the development of a new programmatic forward market for CTV inventory.

Broadcasters are also applying the same innovation focus to the world of identity. Recently, TTD has announced collaborations with OpenAP and Blockgraph.

This discussion on identity is bigger than cookies. It's bigger than any company or any channel. Cookies are not present in CTV. However, a privacy-safe identifier for CTV will be a major factor in driving relevant ads and managing reach and frequency across apps, channels, and devices.

CTV needs this kind of approach in order to maintain pricing power in a way that helps fund the high quality content that has kept most consumers binge-watching during this pandemic.

The current TV content arms race cannot be financially sustained for providers or consumers without relevant ads.

UID or user ID number is the identification number of your user account.

Remember how UID works, consumers sign in once with their email address and then opt-in site by site, just once per site or app, or channel.

This is a significant improvement to the consumer Internet experience today, where intrusive toasts or cookie pop-ups appear on almost every premium content site and seemingly every time you go there.

It's a common ID that can be used by many different advertisers and publishers.

It often originates from publishers with existing sign-on systems.

Consumers can then engage with privacy settings and opt out directly from the services they know.

The Wall Street Journal reported 50 million UID authenticated users in the U.S. a couple of months ago.

There's no point in building walls around it. Brands will, over time, always gravitate to places where they can be deliberate and where they can measure ad impressions across channels.

There are some companies, mostly those with a dominant walled garden approach, that believe the Internet can be controlled by a few.

Then there's the rest who believe that an open, competitive Internet marketplace is the only real viable approach that preserves value and opportunity for all participants.

And that has meant that cord-cutting in linear or cable television has accelerated and that people are looking more and more at Internet-fueled TV.

Because there are also more apps than there have ever been, content discovery is tougher in CTV than it’s ever been.

TTD’s Q1 revenue was $220 million, a 37% increase from a year ago and TTD benefited from improvement in the digital advertising environment from both agencies and brands.

Video, which includes CTV, again, led growth during the quarter followed by audio.

While improving, the travel and entertainment verticals still lag compared to others, but both are showing signs of a rebound so far in Q2. There is still a massive recovery ahead in these segments and starting to see green shoots.

TTD estimates Q2 revenue to be between $259 million and $262 million, which would represent growth of between 86% to 88% on a year-over-year basis because Q2 last year was the nadir of TTD’s Covid problems to the ad buying industry.

That said, in the second half of 2021, TTD expects year-over-year total revenue growth rates to decelerate significantly on a sequential basis because comparable data will be hard to beat from Q3 and Q4.

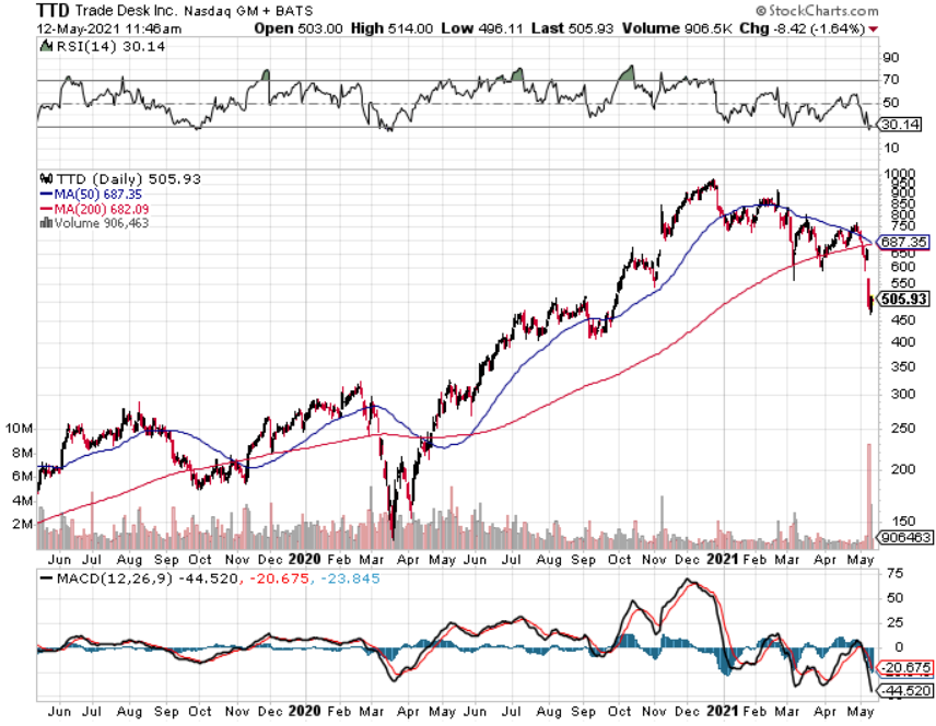

This was the cue for a massive selloff in TTD shares.

Don’t forget that the 2020 U.S. Election produced a tsunami of ad buying in the 2nd half of 2020.

The company is still firing on all cylinders, justifying the move from $160 in March 2020 to $950, but price action in shares is volatile.

The stock has pulled back to around $500 and has technical support at $450, I would look for an entry point around there if the broader market calms down.

Mad Hedge Technology Letter

January 29, 2021

Fiat Lux

Featured Trade:

(THE OTHER STREAMING SERVICE)

(FUBO), (ROKU), (TTD)

I was going to hold off on writing about this streaming service, but the shares are up another 15% this morning on a down day and that has forced my hand.

Streaming platforms have done extremely well during the pandemic and it is a no-brainer to put two and two together because consumers stuck at home would obviously mean more streaming consumption.

But what about those streaming services that you have not heard about?

They do exist and now I am here to tell you about one of them.

Enter fuboTV (FUBO).

FuboTV is an American streaming television service that focuses primarily on channels that distribute live sports, including NFL, MLB, NBA, NHL, MLS, and international soccer, plus sports news, network television series, and movies.

Yes, I must admit that fuboTV isn’t the newest company. The company was established in 2015 and some of the hardcore streamers will see this service pop up on their Roku (ROKU) amongst other platforms.

After a more focused migration into live sports television, a key deal to bring Disney’s ESPN to its platform, and a pair of acquisitions to allow sportsbook operations beginning in 2021.

FUBO has potential and is already showing robust growth backed by the kind of subscriber numbers needed to turn an eventual profit.

November’s third-quarter print showed accelerating subscriber growth from 58% to 72% and sales surging from 71% to 80%.

I am quite positive on FUBO’s ability to monetize traffic at much higher rates than its competitors.

That includes streaming hardware darling Roku, which captures less than one-third of FUBOs per user ad revenue.

FUBO had just 545,000 subscribers entering into 2021, but its free-spending audience that totals an average of four hours a day streaming the platform is a bedroom piece of foundation to this upstart company.

It is generating an average $7.50 in monthly ad revenue per user, and that's on top of the $65 monthly fee for the entry-level plan featuring 118 different channels.

The big selling point for fuboTV is that more than three dozen of those networks are dedicated sports channels.

FUBO’s capture of ESPN last summer was a coup, but it also dropped Turner's sports-heavy properties.

It’s true that it is not the perfect service, and is missing some crucial content.

They are also not carrying Sinclair's regional sports channels.

Cord cutters are helping this stock be hard to bet against after joining the services in droves in 2020.

FUBO actually was laser-focused on European soccer at the beginning but understood they needed to branch out to capture other pro sports fans and widen its audience.

Unlike Netflix, advertising is a key component in the company's revenue. It works with top ad-tech companies like The Trade Desk (TTD) and Magnite, and these partnerships are helping it with growth.

In the third quarter, ad revenue grew 153% year over year.

FUBO's ad business is already far ahead of Roku's, perhaps demonstrating the greater monetization potential of live sports and TV compared to on-demand streaming.

FUBO believes it can generate more than $20 in ARPU after paying the third-party vendors it works with.

A net loss of $402.5 million through the first nine months of 2020 is standard for most teething growth companies and the unprofitability shouldn’t stop investors from this stock.

If you do choose to dip your toe into this stock, then be aware the volatility might make you feel unsteady at night.

The wild swings are a sign of an immature company growing into its investor base.