Global Market Comments

May 6, 2025

Fiat Lux

Featured Trade:

(THEY’RE NOT MAKING AMERICANS ANYMORE)

(SPY), (EWJ), (EWL), (EWU), (EWG), (EWY), (FXI), (EIRL), (GREK), (EWP), (IDX), (EPOL), (TUR), (EWZ), (PIN), (EIS)

Global Market Comments

May 6, 2025

Fiat Lux

Featured Trade:

(THEY’RE NOT MAKING AMERICANS ANYMORE)

(SPY), (EWJ), (EWL), (EWU), (EWG), (EWY), (FXI), (EIRL), (GREK), (EWP), (IDX), (EPOL), (TUR), (EWZ), (PIN), (EIS)

If demographics are destiny, then America’s future looks bleak. You see, they’re just not making Americans anymore.

At least that is the sobering conclusion of the latest Economist magazine survey of the global demographic picture.

I have long been a fan of demographic investing, which creates opportunities for traders to execute on what I call “intergenerational arbitrage”. When the number of middle-aged big spenders is falling, risk markets plunge.

Front run this data by two decades, and you have a great predictor of stock market tops and bottoms that outperforms most investment industry strategists.

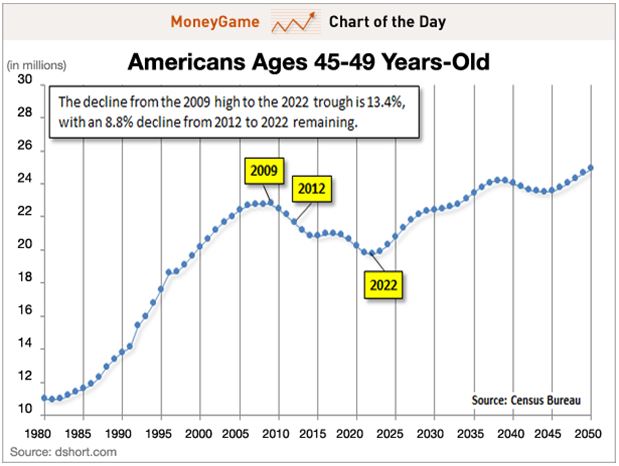

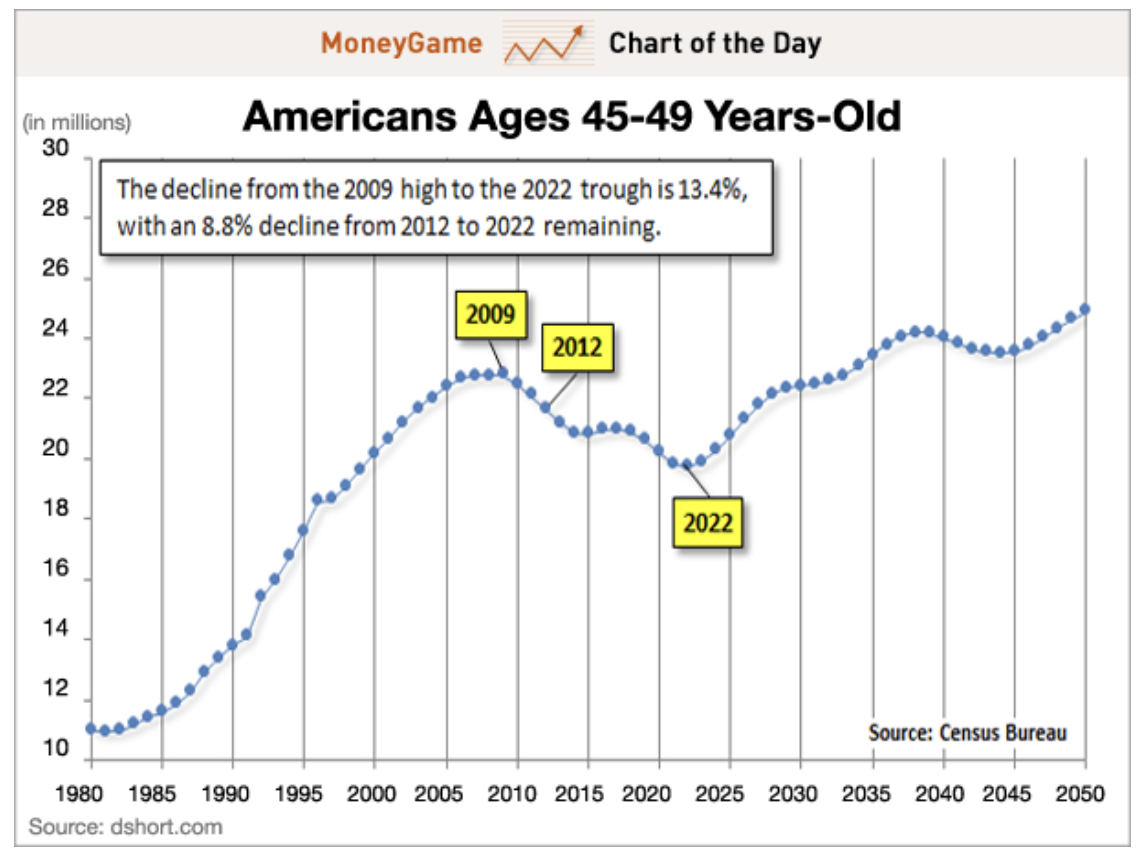

You can distill this even further by calculating the percentage of the population that is in the 45-49 age bracket.

The reasons for this are quite simple. The last five years of child rearing are the most expensive. Think of all that pricey sports equipment, tutoring, braces, SAT coaching, first cars, first car wrecks, and the higher insurance rates that go with it.

Older kids need more running room, which demands larger houses with more amenities. No wonder it seems that dad is writing a check or whipping out a credit card every five seconds. I know, because I have five kids of my own. As long as dad is in spending mode, stock and real estate prices rise handsomely, as do most other asset classes. Dad, you’re basically one generous ATM.

As soon as kids flee the nest, this spending grinds to a juddering halt. Adults entering their fifties cut back spending dramatically and become prolific savers. Empty nesters also start downsizing their housing requirements, unwilling to pay for those empty bedrooms, which in effect, become expensive storage facilities.

This is highly deflationary and causes a substantial slowdown in GDP growth. That is why the stock and real estate markets began their slide in 2007, while it was off to the races for the Treasury bond market.

The data for the US is not looking so hot right now. Americans aged 45-49 peaked in 2009 at 23% of the population. According to US census data, this group then began a 13-year decline to only 19% by 2022.

You can take this strategy and apply it globally with terrific results. Not only do these spending patterns apply globally, but they also backtest with a high degree of accuracy. Simply determine when the 45-49 age bracket is peaking for every country, and you can develop a highly reliable timetable for when and where to invest.

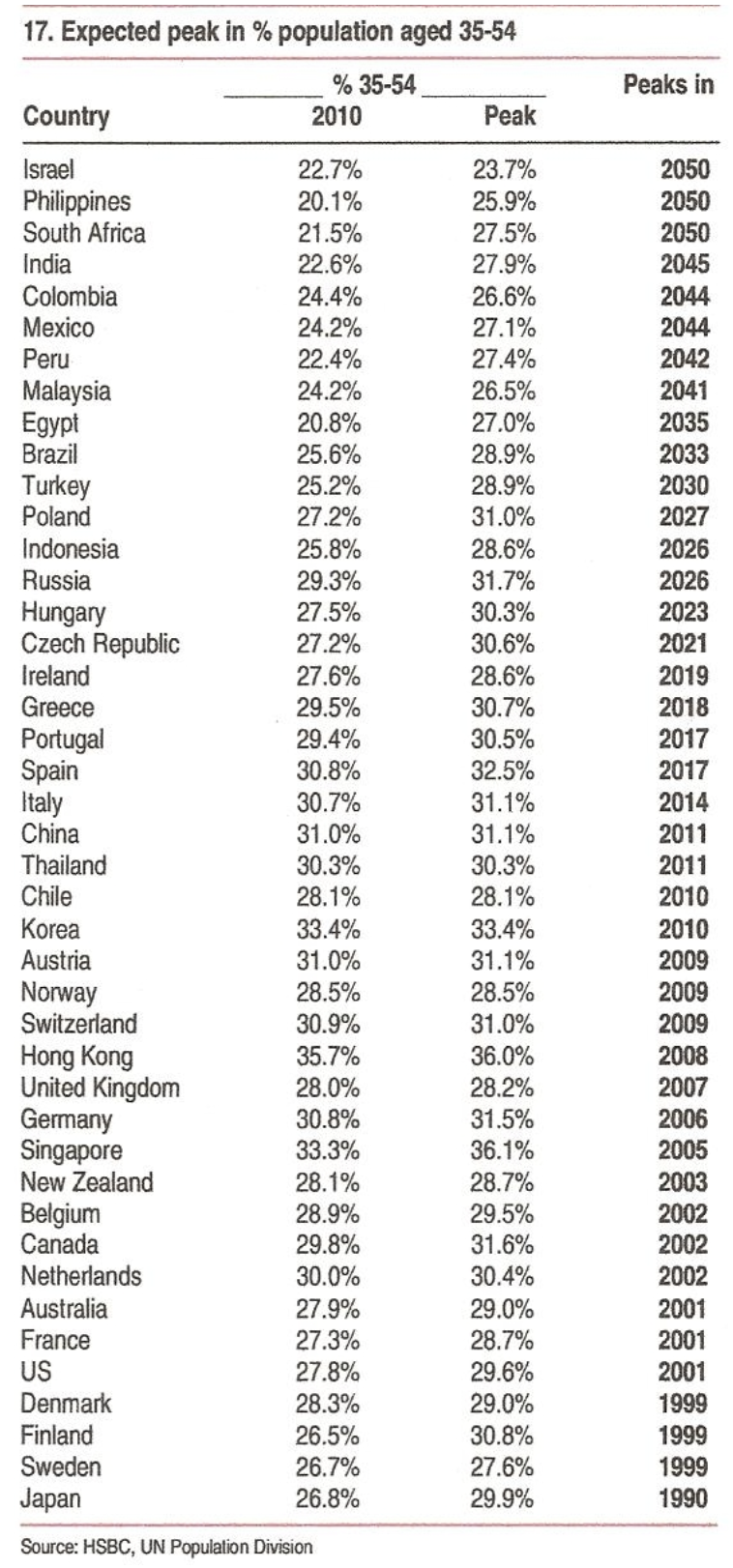

Instead of poring through gigabytes of government census data to cherry-pick investment opportunities, my friends at HSBC Global Research, strategists Daniel Grosvenor and Gary Evans, have already done the work for you. They have developed a table ranking investable countries based on when the 34-54 age group peaks—a far larger set of parameters that captures generational changes.

The numbers explain a lot of what is going on in the world today. I have reproduced it below. From it, I have drawn the following conclusions:

* The US (SPY) peaked in 2001 when our first “lost decade” began.

*Japan (EWJ) peaked in 1990, heralding 32 years of falling asset prices, giving you a nice back test.

*Much of developed Europe, including Switzerland (EWL), the UK (EWU), and Germany (EWG), followed in the late 2,000’s, and the current sovereign debt debacle started shortly thereafter.

*South Korea (EWY), an important G-20 “emerged” market with the world’s lowest birth rate, peaked in 2010.

*China (FXI) topped in 2011, explaining why we have seen three years of dreadful stock market performance despite torrid economic growth. It has been our consumers driving their GDP, not theirs.

*The “PIIGS” countries of Portugal, Ireland (EIRL), Greece (GREK), and Spain (EWP) don’t peak until the end of this decade. That means you could see some ballistic stock market performances if the debt debacle is dealt with in the near future.

*The outlook for other emerging markets, like Indonesia (IDX), Poland (EPOL), Turkey (TUR), Brazil (EWZ), and India (PIN) is quite good, with spending by the middle-aged not peaking for 15-33 years.

*Which country will have the biggest demographic push for the next 38 years? Israel (EIS), which will not see consumer spending max out until 2050. Better start stocking up on things Israelis buy.

Like all models, this one is not perfect, as its predictions can get derailed by a number of extraneous factors. Rapidly lengthening life spans could redefine “middle age”. Personally, I’m hoping 72 is the new 42.

Emigration could starve some countries of young workers (like Japan), while adding them to others (like Australia). Foreign capital flows in a globalized world can accelerate or slow down demographic trends. The new “RISK ON/RISK OFF” cycle can also have a clouding effect.

So why am I so bullish now? Because demographics is just one tool in the cabinet. Dozens of other economic, social, and political factors drive the financial markets.

What is the most important demographic conclusion right now? That the US demographic headwind veered to a tailwind in 2022, setting the stage for the return of the “Roaring Twenties.” With the (SPY) up 27% since October, it appears the markets heartily agree.

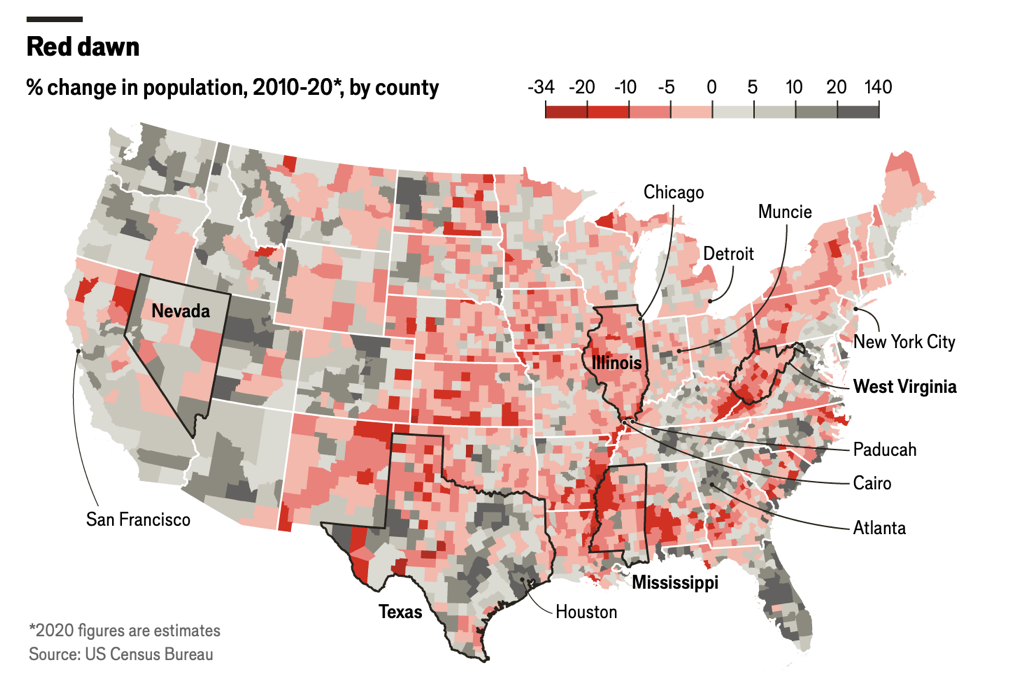

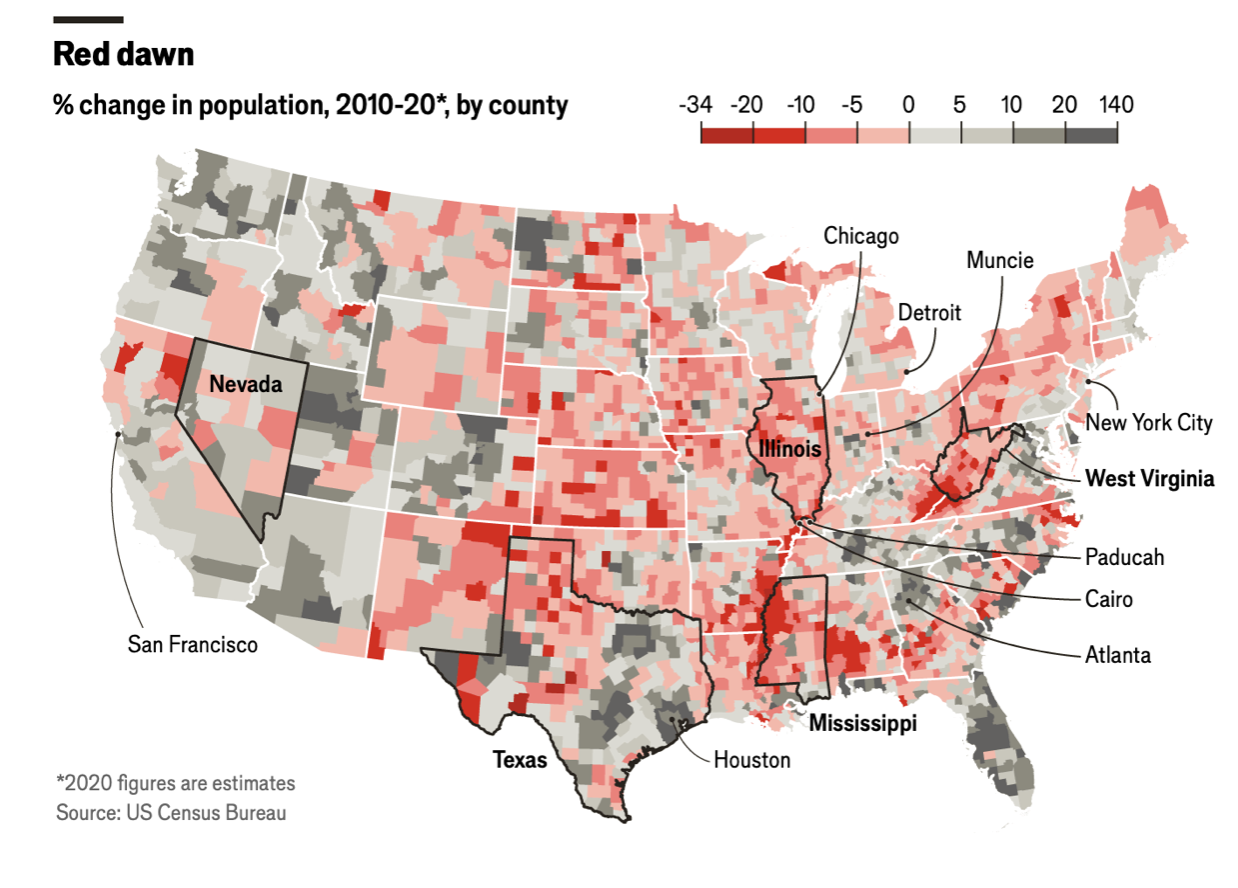

While the growth rate of the American population is dramatically shrinking, the rate of migration is accelerating, with huge economic consequences. The 80-year-old trend of population moving from North to South to save on energy bills is picking up speed, and the Midwest is getting hollowed out at an astounding rate as its people flee to the coasts, all three of them.

As a result, California, Texas, Florida, Washington, and Oregon are gaining population, while Missouri, Iowa, Nebraska, Kansas, and Wyoming are losing it (see map below). During my lifetime, the population of California has rocketed from 10 million to 40 million. People come in poor and leave as billionaires, as Elon Musk did.

In the meantime, I’m going to be checking out the shares of the matzo manufacturer down the street.

Global Market Comments

April 24, 2024

Fiat Lux

Featured Trade:

(THEY’RE NOT MAKING AMERICANS ANYMORE)

(SPY), (EWJ), (EWL), (EWU), (EWG), (EWY), (FXI), (EIRL), (GREK), (EWP), (IDX), (EPOL), (TUR), (EWZ), (PIN), (EIS)

If demographics is destiny, then America’s future looks bleak. You see, they’re not making Americans anymore.

At least that is the sobering conclusion of the latest Economist magazine survey of the global demographic picture.

I have long been a fan of demographic investing, which creates opportunities for traders to execute on what I call “intergenerational arbitrage”. When the numbers of the middle-aged big spenders are falling, risk markets plunge. Front run this data by two decades, and you have a great predictor of stock market tops and bottoms that outperforms most investment industry strategists.

You can distill this even further by calculating the percentage of the population that is in the 45-49 age bracket.

The reasons for this are quite simple. The last five years of child rearing are the most expensive. Think of all that pricey sports equipment, tutoring, braces, SAT coaching, first cars, first car wrecks, and the higher insurance rates that go with it.

Older kids need more running room, which demands larger houses with more amenities. No wonder it seems that dad is writing a check or whipping out a credit card every five seconds. I know, because I have five kids of my own. As long as dad is in spending mode, stock and real estate prices rise handsomely, as do most other asset classes. Dad, you’re basically one generous ATM.

As soon as kids flee the nest, this spending grinds to a juddering halt. Adults entering their fifties cut back spending dramatically and become prolific savers. Empty nesters also start downsizing their housing requirements, unwilling to pay for those empty bedrooms, which in effect, become expensive storage facilities.

This is highly deflationary and causes a substantial slowdown in GDP growth. That is why the stock and real estate markets began their slide in 2007, while it was off to the races for the Treasury bond market.

The data for the US is not looking so hot right now. Americans aged 45-49 peaked in 2009 at 23% of the population. According to US census data, this group then began a 13-year decline to only 19% by 2022.

You can take this strategy and apply it globally with terrific results. Not only do these spending patterns apply globally, they also back-test with a high degree of accuracy. Simply determine when the 45-49 age bracket is peaking for every country and you can develop a highly reliable timetable for when and where to invest.

Instead of pouring through gigabytes of government census data to cherry-pick investment opportunities, my friends at HSBC Global Research, strategists Daniel Grosvenor and Gary Evans, have already done the work for you. They have developed a table ranking investable countries based on when the 34-54 age group peaks—a far larger set of parameters that captures generational changes.

The numbers explain a lot of what is going on in the world today. I have reproduced it below. From it, I have drawn the following conclusions:

* The US (SPY) peaked in 2001 when our first “lost decade” began.

*Japan (EWJ) peaked in 1990, heralding 32 years of falling asset prices, giving you a nice backtest.

*Much of developed Europe, including Switzerland (EWL), the UK (EWU), and Germany (EWG), followed in the late 2000s and the current sovereign debt debacle started shortly thereafter.

*South Korea (EWY), an important G-20 “emerged” market with the world’s lowest birth rate peaked in 2010.

*China (FXI) topped in 2011, explaining why we have seen three years of dreadful stock market performance despite torrid economic growth. It has been our consumers driving their GDP, not theirs.

*The “PIIGS” countries of Portugal, Ireland (EIRL), Greece (GREK), and Spain (EWP) don’t peak until the end of this decade. That means you could see some ballistic stock market performances if the debt debacle is dealt with in the near future.

*The outlook for other emerging markets, like Indonesia (IDX), Poland (EPOL), Turkey (TUR), Brazil (EWZ), and India (PIN) is quite good, with spending by the middle age not peaking for 15-33 years.

*Which country will have the biggest demographic push for the next 38 years? Israel (EIS), which will not see consumer spending max out until 2050. Better start stocking up on things Israelis buy.

Like all models, this one is not perfect, as its predictions can get derailed by a number of extraneous factors. Rapidly lengthening life spans could redefine “middle age”. Personally, I’m hoping 72 is the new 42.

Emigration could starve some countries of young workers (like Japan) while adding them to others (like Australia). Foreign capital flows in a globalized world can accelerate or slow down demographic trends. The new “RISK ON/RISK OFF” cycle can also have a clouding effect.

So why am I so bullish now? Because demographics is just one tool in the cabinet. Dozens of other economic, social, and political factors drive the financial markets.

What is the most important demographic conclusion right now? That the US demographic headwind veered to a tailwind in 2022, setting the stage for the return of the “Roaring Twenties.” With the (SPY) up 27% since October, it appears the markets heartily agree.

While the growth rate of the American population is dramatically shrinking, the rate of migration is accelerating, with huge economic consequences. The 80-year-old trend of population moving from North to South to save on energy bills picking up speed, the Midwest is getting hollowed out at an astounding rate as its people flee to the coasts, all three of them.

As a result, California, Texas, Florida, Washington, and Oregon are gaining population, while Missouri, Iowa, Nebraska, Kansas, and Wyoming are losing it (see map below). During my lifetime, the population of California has rocketed from 10 million to 40 million. People come in poor and leave as billionaires, as Elon Musk did.

In the meantime, I’m going to be checking out the shares of the matzo manufacturer down the street.

Global Market Comments

August 15, 2018

Fiat Lux

Featured Trade:

(WHY BONDS CAN'T GO DOWN),

(TLT), (TBT), ($TNX), (TUR), (TSLA),

(HOW TO MAKE MORE MONEY THAN I DO),

(AMZN), (LRCX), (ABX), (AAPL), (TSLA), (NVDA)

Ho Hum. Another week, another financial crisis. And why did I rush back from the bucolic mountain pastures of Zermatt? To come back to the smoke-laden skies from the Northern California forest fires? It all must be an early sign of dementia.

Trump's foreign policy now seems crystal clear; to destroy the economies of all our allies. That's what he accomplished with NATO member Turkey today by doubling tariffs, triggering an instant 20% devaluation of the Turkish Lira. Turkey has been at war with Russia for 600 years.

Most Turkish companies have their debts in U.S. dollars or Euros (FXE), so you can write them off. That puts European banks at risk of another crisis, which could quickly turn global in nature. The flip side of this move was to take the U.S. dollar (UUP) to a new high for the year, thus crushing our own exporters even further.

Did our stock market care? Well. Actually yes, taking the Dow Average down 300 points. Will it care more than today? Probably not. All we are seeing is profit taking in some of the most overbought high fliers.

That is, unless, you are a soybean farmer, who saw prices collapse yet again. I watch bean prices closely these days, as it is an indicator of the market's expectation of intensifying trade wars.

After four decades of efforts to develop the Chinese markets, those efforts are going up in flames. And that business is not coming back now that the U.S. has proved itself an unreliable partner. As anyone in business will tell you, you only get to offend a customer once.

Markets generally believe that the U.S. trade war against the rest of the world is nothing more than a negotiating ploy. If that is not the case and they go on and on, you can move up the next recession and bear market by a year, like to tomorrow.

Perhaps the most important news of the week was the July Consumer Price Index leaping to 2.9%, a decade high. This is on the heels of the 2.7% pop in Average Hourly Earnings that came with the July Nonfarm Payroll Report.

Yes, ladies and gentlemen, this is called inflation. And while bonds normally get destroyed by such a data point, fixed income markets instead decided to focus on the strong U.S. dollar.

That was enough to entice me to sell short the U.S. Treasury bonds (TLT) for the first time in three months. With the Fed raising interest rates on September 25 by 25 basis points, what could go wrong?

Tesla (TSLA) sucked a lot of the air out of the room this week with its mooted buyout at $420 a share. I think it will happen. There is a global capital glut right now, with trillions of dollars of capital looking for a home. Ownership of Tesla would be a great hedge for Saudi Arabia against falling oil prices, which already owns 4% of the company. And guess who the world's largest per capita buyer of Tesla's is? Norway, which has a $1 trillion sovereign wealth fund of its own. The proposed $82 billion price tag for Tesla would look like pennies on the dollar.

Tip toeing back into the market with two cautious positions has boosted my August performance to 1.32%. My 2018 year-to-date performance has clawed its way up to 26.14% and my nine-year return appreciated to 302.61%. The Averaged Annualized Return stands at 34.91%. The more narrowly focused Mad Hedge Technology Fund Trade Alert performance is annualizing now at an impressive 32.24%.

This coming week will be a very boring week on the data front.

On Monday, August 13, there will be nothing of note to report. It will just be another boring summer day.

On Tuesday, August 14, at 6:00 AM EST, we get the weekly NFIB Small Business Optimism Report.

On Wednesday, August 15, at 9:15 AM, we learn July Industrial Production.

Thursday, August 16, leads with the Weekly Jobless Claims at 8:30 AM EST, which saw a fall of 13,000 last week to 222,000. Also announced are July Housing Starts. At 4:30 PM, we learn the July Money Supply, which we might have to start paying attention to, now that inflation is on the rise.

On Friday, August 17, at 10:00 AM EST, we get Leading Economic Indicators. Then the Baker Hughes Rig Count is announced at 1:00 PM EST.

As for me, I will be stuck indoors this weekend and the government has warned me not to go outside unless absolutely necessary because the air quality is so bad. Maybe I can sneak out to Costco at some point to replenish my empty refrigerator.

Good luck and good trading.

I am writing this to you from the veranda of the presidential suite at the Ciragan Palace Hotel in Istanbul. The former palace of an Ottoman prince, the commerce of the Straights of Bosphorus plays out before me.

Empty supertankers lumber up the narrow waterway to pick up another load of Russian crude at Baku, followed by full containerships loaded with consumer goods to pay for it. Peripatetic ferries rapidly crisscross its course laden with passengers fleeing Istanbul?s traffic nightmare. Amid the mix are dozens of racing yachts, the chief status symbol of Turkey?s new elite.

It?s amazing that you don?t read about more Turkish maritime disasters!

The first thing you learn about Turkey these days is that it is no longer an emerging economy. It has emerged! It now ranks 17th in GDP, and could be tenth in another decade. Per capita income has soared to $11,000, compared to $48,000 in the US and $6,000 in China. Once overly dependent on Europe for trade, Turkey has ramped up its shipment of goods to much of the emerging world.

A runaway property boom has placed it fourth in the world in the number of billionaires, with 28. It is the fourth largest shipbuilder, a major auto manufacturer and boasts an important defense industry. If you are eating cherries, hazelnuts, olives, or figs in Europe, chances are that they came from a farm in Turkey.

Turkey joined the European customs union in 1996. It is now negotiating for full European Community membership, becoming the first Asian member, an event expected to occur in the next 5-10 years.

I have taken great pleasure in recent years returning to old haunts I first saw 46 years ago. That was when I lived on $1 a day, carried my worldly possessions in a Kelty backpack and slept under bridges, in bombed out farmhouses, or the local Youth Hostel. I remember that Istanbul?s had a thriving population of bedbugs and a permanently blocked sewer line.

However, this time around I?m staying at five star hotels, like the Kempinski, and the first decision of the day is whether or not to have French Champagne with my fresh squeezed orange juice.

Buy when there is blood in the streets!

That is the time-honored tradition of traders and investors everywhere when it comes to emerging markets (EEM). I had a friend who reliably bought every coup d?etat in Thailand during the seventies and eighties, and he made a fortune, retiring to one of the country?s idyllic islands off the coast of Phuket.

Blood is certainly flowing in Turkey these days. You have the real kind flowing in Istanbul?s Taksim Gezi Park, the country?s own Democracy Square, where students and labor leaders have been protesting the conservative, mildly Islamic policies of Prime Minister Recep Tayyip Erdogan. The violence led to 3,000 arrests and 11 dead.

The fat then fell into the fire with the latest round of instability in the Middle East.? A new terrorist group called ISIS (Islamic State of Iraq and the Levant), even more violent and extreme than its Al Qaida parent, took over the northern portion of that country.

Iraq is Turkey?s second largest trading partner, supplying services, infrastructure, food and consumer goods in exchange for oil. That business completely ceased, and more than 50 Turkish hostages were taken, mostly truck drivers. The oil price spike that followed delivered yet another blow to an already fragile Turkish economy, which depends heavily on imported energy.

This brought a plunge by two thirds in Turkey?s economic growth, from 4.7% annualized rate in the first quarter of 2014, to only 1.6% in May. That was well off from the heady days of 9% growth seen in 2010-2011, when Turkey was one of the fastest countries to bounce back from the 2008-2009 financial crisis. This does not auger well for the future.

The new civil war in Iraq and the endless fighting in Syria have prompted 1 million refugees to flee to Turkey. You see them everywhere in Istanbul, living in abandoned buildings or trolling the streets for handouts. I gave ten Turkish lira to the children below to take their picture. The resulting burden on the country?s nascent social services is immense.

If this were the only problem the country was facing, you might conclude that the timing was ripe to ramp up your investments here.

Better to lie down and take a long nap first.

Turkey is sitting atop a massive property bubble. While GDP has risen by 400% over the past decade, property prices are up by an incredible 900%, and stocks 1,000%. Much is financed by undercapitalized local Turkish banks or by foreign debt.

That is a huge problem when the Turkish lira is weak, as it leads to rising principal amounts and interest rate payments in dollars, Euros and Swiss francs. You see abandoned construction projects all over the country, the casualties of just such a squeeze.

These conditions are about to worsen. We learned from the general collapse of emerging markets (EEM) last year that they are the most sensitive to US Federal Reserve tightening. That tightening has only just begun.

Fed governor, Janet Yellen, has indicated that the central bank?s monthly Treasury bond buying will get tapered down from a high of $80 billion a month down to zero by October. Actual interest rate increases are likely to follow next year.

This is all likely to suck more money out of Turkish financial markets into US ones, to the detriment of Turkish prices everywhere. This is one of the reasons that the Turkish stock market plunged a gob smacking 50% from its highs last year.

European weakness, far and away Turkey?s largest trading partner, caused the country to run a massive $56.8 billion current account deficit in 2013. A borrowing binge to finance speculative real estate projects was another contributing factor.

Consumer prices are also raging away at 9.2% a year. This is often a problem with what I call the ?advanced? emerging markets. Economic growth brings uncontrolled inflation, which raises its cost of labor in the international marketplace and erodes its competitiveness. You see this in Turkey, China and India.

The only way a country can fight back is to devalue its currency. But that frightens away foreign investors, a large factor in the country?s economic miracle.

This is the conundrum in which the Turkish Central Bank finds itself today: High interest rates, a strong currency, and no growth? Or low interest rates, a weak currency, and no foreign investors. It?s a choice that would vex Solomon.

For the short term, Turkey has clearly chosen the latter, ratcheting up short-term interest rates by a gob smacking 4.75% during one night last winter. That caused the Turkish Lira to rally smartly, some 10%. But ten-year government bond rates now hover just above 9.0%, hardly a business friendly rate, removing yet another leg supporting precarious Turkish real estate prices.

Still, conditions today are a vast improvement over the bad old Turkey of decades ago. For 40 years, the military controlled weak elected governments, and one cruel fact that I have learned over the years is that generals are lousy at running economies.

Perennial financial crises scared off foreign investors and the International Monetary Fund had to come in and bail out the country as often as I change my socks. The US turned a blind eye to these abuses, as Turkey was the only NATO member bordering the old Soviet Union and an unstable Middle East.

The potential was always there. Turkey has a highly positive population pyramid, with a large, dynamic and young population only needing to support a miniscule aging population. All that was needed was leadership and confidence.

Prime Minister Erdogan, riding a wave of popularity with his AKP, or Justice and Development Party, delivered that in spades after his election as prime minister in 2003. Pursuing a no nonsense, technocratic, pro business approach, a Turkish economic revival ensued, delivering meteoric results for the country. Yet, he was just Islamic enough to keep the religious hard liners, the Army and terrorist groups at bay.

I had a chance to hear the prime minster speak, attending what turned into a political rally on the first day of Ramadan, in front of the storied Blue Mosque in Istanbul. The only words I understood were ?God is great.? But his support among his conservative base, who were ebullient over his surprise appearance, is undeniable.

Yet, another problem is that this man behind the curtain who has delivered so much is about to leave the stage. Term limits prevent Erdogan from running for Prime Minister again, so he is seeking the presidency instead, a largely ceremonial post under Turkey?s constitution.

That will likely make the current president the next Prime Minister, Abdullah Gul, a close political ally of Erdogan?s. But he is not the same guy.

Even with his impending diminished status, Erdogan is charging ahead with public works projects, the scale of which would impress Franklin Delano Roosevelt. He wants to build a third bridge connecting Europe with Asia. He is planning a tunnel under the Bosphorus. He wants Istanbul?s airport to become the largest in the world. The price tag for all of this is enormous.

So has Turkey suffered enough?

I have to admit that I came to revisit the exotic playground of my impetuous youth to issue the mother of all Trade Alerts and jump back into the ETF (TUR). What I heard in the bazaars, outside mosques and speaking to local businessmen suggests that the pain has only just begun.

As discretion seems to be the better part of valor this year, I think I?ll pass on that Trade Alert.

The US Dollar?s Ten Year Rise Against the Turkish Lira

The US Dollar?s Ten Year Rise Against the Turkish Lira

For the last couple of nights, I have left my iPhone logged into the Argentina peso market, one of several troubled currencies igniting the emerging market contagion. Whenever the peso losses another handle to the US dollar, an alarm goes off. That gives me a head start on how American markets will behave the next day.

I have not been getting a lot of sleep lately. My poor phone has recently been sounding off like a winning slot machine at a Las Vegas casino.

Take a look at the long-term chart for the peso, and it?s clear that some traders have not gotten any sleep for five years, when the peso cratered 50% against the greenback. An imploding currency, soaring national debt, and sliding economy promise to send it lower.

Incompetent leadership doesn?t help either. You know that things are bad when your ships get seized by creditors when they land at foreign ports.

When I wrote my all asset class forecast for 2014, there was only one thing I knew for sure: this year would be harder than last. That has been my best prediction for 2014 so far.

The guaranteed shorts, those for the Japanese yen (FXY) and the Treasury bond market (TLT), have been rocketing to the upside since the opening bell rang on January 2. The no brainer longs, like financials (XLF) and consumer discretionaries (XLY), have been plummeting.

The heart wrenching 4.3% correction we saw for the S&P 500 (SPY), and the 5% hit for the Dow average this month, the worst weekly draw down in two years, has predictably brought the Armageddon crowd out of the closet once again. All of a sudden, a 10% correction best case, and Dow 3,000 worst case, are on the table once again. Do they have a leg to stand on?

Not really.

To achieve these big numbers on the downside, your really need a global systemic financial crisis. There isn?t one remotely on the horizon. Yes, there are difficulties in Argentina, the Ukraine, and Turkey. But they are locally confined.

Together, these countries account for less than 1% of global GDP. If they disappeared completely, they would barely make a blip in world GDP. They certainly are not important enough to panic you into emptying your ATM at the local mall on your next lunch break.

You also need excessive leverage. But that has been banned by prime brokers since the 2008 crash. An aggressive long today is 20% net long, not 200% as in the bad old days of yore. Nothing systemic there.

Sure, we aren?t getting the juice that we used to from the Federal Reserve. It is likely that they will further reduce the taper from $75 billion to $65 billion of bond buying per month at their 1:00 PM Wednesday press release.

If there were a one in a million chance that this would trigger a real market meltdown, my friend, Fed governor Janet Yellen, would run that release through the shredder as fast as you could say ?Go Bears?, sending markets flying.

Others are accusing a looming financial crisis in China as another culprit. Yes, the economic data has been soggy of late, to be sure. However, that is just the continuation of a four year old trend. You can safely forget about that one.

No country in history ever suffered a financial crisis with $4 trillion in foreign exchange reserves on hand, including over $1 trillion in US Treasury bonds close to all time highs in value. In fact many of the emerging markets said to be in trouble also boast large reserves, the product of running massive trade surpluses with a hyper consuming West for the past decade.

So if we can?t blame emerging markets or the taper for the downside, then what is causing the January swoon? You can blame it all on the hedge funds.

I have seen this time and again. Whenever too many people crowd into one end of a canoe, it rolls over. When the majority of funds have identical positions, they are guaranteed to fail. That is why we have had a looking glass market performance since the beginning of this year.

Except that this time we got a turbocharger. The peaking of concentration in the most popular trades perfectly coincided with the big New Year reallocation trade, taking prices to greater extremes. Much of the selling you are seeing down here is from latecomers who bought stock only three weeks ago and are now puking them out.

Of course, I saw all of this coming a country mile off. This is why I cut my net long from 100% 10 days ago to only 10%. It is why I am maintaining a year to date performance of +5.13%, compared to a Dow that is down -5%. It is one of my best gains relative to the index over a short period ever.

The same is true of my colleague, Mad Day Trader, Jim Parker. He is almost all in cash and is also well up on the year. He stuck his toe in the water with a small position in some calls on the (TBT) last week, but it got bit off by a shark almost immediately. So he quickly stopped out, as is his way. Of course, we have been comparing notes and sharing input throughout the selling. It appears that great minds think alike.

Jim?s proprietary in-house analysis predicts that the (SPX) will bottom out just above 1,730, the market close on the November 15 options expiration. If correct, that would give us a total start to finish correction of only 6.7%, which is in line with every other correction for the past two years. But the bottoming process could last a few weeks, and provide several more gut churning dumps. Fasten your seat belt.

When will this end? Watch for the parallel confirming cross market trends. The Treasury bond market is a big one, which appears to be peaking already, right at its 200 day moving average and the top of a six month trading range.? Announcement of the next taper could spark the selloff we need there. The Japanese yen is also important. A top here could signal a return to the carry trade and ?RISK ON?.

Since Emerging markets were the instigator of the crisis, look there as well for the first signs of a turnaround. Scrutinize the chart below, and you gain some heart.? It shows that we are a scant 70 cents from setting up a potential multiyear triple bottom at $37, and worst-case $36.

More specifically, you want to see Turkey (TUR), another instigator of this crisis, recoil from $39. Expect it to bounce hard there, as long as the world is really not ending.

Then it will be off to the races once more. I?ll be keeping my powder dry until then. Watch this space.

The Argentine Peso Against the US Dollar

The Argentine Peso Against the US Dollar

Time To Keep Your Powder Dry

Time To Keep Your Powder Dry

I am building lists of emerging market ETF?s to snap up during the current sell off, and Turkey popped up on the menu.

The country is only one of two Islamic countries that I consider investment grade, (Indonesia is the other one). The 82 million people of Turkey rank 15th in the world population, and 16th with a GDP of $960 billion. Furthermore, 25% of the population is under the age of 15, giving it one of the planet?s most attractive demographic profiles.

The real driver for Turkey is a rapidly rising middle class, generating consumer spending that is growing by leaps and bounds. Its low waged labor force is also a major exporter to the modestly recovering European Community next door. The present collapse of the Turkish Lira increases that advantage.

I first trod the magnificent hand woven carpets of Istanbul?s Aga Sophia in the late sixties while on my way to visit the rubble of Troy and what remained of the trenches at Gallipoli, a bloody WWI battlefield.

Remember the cult film Midnight Express? If it weren?t for the nonstop traffic jam of vintage fifties Chevy?s on the one main road along the Bosphorus, I might as well have stepped into the Arabian Nights. They were still using the sewer system built by the Romans.

Four decades later, and I find Turkey among a handful of emerging nations on the cusp of joining the economic big league. Exports are on a tear. Prime Minister Erdogan, whose AKP party took control in 2002, implemented a series of painful economic reform measures and banking controls, which have proven hugely successful.

Foreign multinationals like General Electric, Ford, and Vodafone, have poured into the country, attracted by a decent low waged work force and a rapidly rising middle class. The Turkish Lira has long been a hedge fund favorite, attracted by high interest rates.

Still, Turkey is not without its problems. It does battle with Kurdish separatists in the east, and has suffered its share of horrific terrorist attacks. There is a risk that it gets sucked further into the Syrian civil war. Inflation at 7.4% is a worry, but that?s down from 8.88% a year ago.

The play here has long been to buy ahead of membership in the European Community, which it has been denied for four decades. Suddenly, that outsider status has morphed from a problem to an advantage.

The way to get involved here is with an ETF heavily weighted in banks and telecommunications companies, classic emerging market growth industries like (TUR). You also always want to own the local cell phone company in countries like this, which in Turkey is Turkcell (TKC). Turkey is not a riskless trade, and has already had a great run, but is well worth keeping on your radar.

I See A Trade Setting Up Here

I See A Trade Setting Up HereI am building lists of emerging market ETF?s to snap up during any summer sell off, and Turkey popped up on the menu. The country is only one of two Islamic countries that I consider investment grade, (Indonesia is the other one). The 82 million people of Turkey rank 15th in the world population, and 16th with a GDP of $960 billion GDP. Some 25% of the population is under the age of 15, giving it one of the planet?s most attractive demographic profiles.

The real driver for Turkey is a rapidly rising middle class, generating consumer spending that is growing by leaps and bounds. Its low wage labor force is also a major exporter to the European Community next door.

I first trod the magnificent hand woven carpets of Istanbul?s Agia Sophia in the late 1960?s while on my way to visit the rubble of Troy and what remained of the trenches at Gallipoli, a bloody WWI battlefield. Remember the cult film, Midnight Express? If it weren?t for the nonstop traffic jam of vintage fifties Chevy?s on the one main road along the Bosporus, I might as well have stepped into the Arabian Nights. They were still using the sewer system built by the Romans.

Four decades later, and I find Turkey among a handful of emerging nations on the cusp of joining the economic big league. Exports are on a tear, and the cost of credit default swaps for its debt is plunging. Prime Minister Erdogan, whose AKP party took control in 2002, implemented a series of painful economic reform measures and banking controls, which have proven hugely successful.

Foreign multinationals like General Electric, Ford, and Vodafone, have poured into the country, attracted by low costs and a rapidly rising middle class. The Turkish Lira has long been a hedge fund favorite, attracted by high interest rates.

Still, Turkey is not without its problems. It does battle with Kurdish separatists in the east, and has suffered its share of horrific terrorist attacks. Inflation is a worry. The play here long has been to buy ahead of membership in the European Community, which it has been denied for four decades. Suddenly, that outsider status has morphed from a problem to an advantage.

The way to get involved here is with an ETF heavily weighted in banks and telecommunications companies, classic emerging market growth industries like (TUR). You also always want to own the local cell phone company in countries like this, which in Turkey is Turkcell (TKC). June elections could provide us with the trigger to move into this enchanting country. Turkey is not a riskless trade, but is well worth keeping on your radar.

I See A Trade Here