Mad Hedge Technology Letter

November 23, 2020

Fiat Lux

Featured Trade:

(COMMUNICATIONS HAS NEVER BEEN MORE IMPORTANT)

(TWLO), (TWTR), (CRM), (SQ), (AMZN), (OSTK), (W)

Mad Hedge Technology Letter

November 23, 2020

Fiat Lux

Featured Trade:

(COMMUNICATIONS HAS NEVER BEEN MORE IMPORTANT)

(TWLO), (TWTR), (CRM), (SQ), (AMZN), (OSTK), (W)

Growth is not dead as last week’s tech rally shows that tech stocks still have their allure.

One tech growth stock that I am absolutely in-love with is communications-as-a-platform cloud stock Twilio who services Airbnb and Uber as the software that connects the users to their staff.

The ability to communicate with customers in real time has never been more urgent in a fast-paced world, especially in the software-centric economy.

From food delivery to booking hotels, from customer service to password resets, literally anything revolves around the ability to connect reliably and rapidly.

Many people in 2020 still do not even know what Twilio (TWLO) does!

They are the dark horse cloud company that nobody has heard of.

The company provides the software building blocks that lets developers embed Twilio's communication technology in their apps, messaging systems, emails, and more. It also streamlines the process so it can be accomplished in a matter of hours, rather than weeks or months.

Here’s an insanely applicable example: The update you received from Lyft regarding your ride, the text messages and reservation confirmation you got from Airbnb, the customer service interactions with Disney's Hulu, and the booking confirmation from your restaurant via Yelp? These were delivered by Twilio's technology.

In pandemic third quarter, Twilio's revenue climbed 52% year over year, while also avoiding a loss, swinging from a loss in the prior-year quarter.

The company reported 208,000 active customers, up 24% year over year.

There is no mistake that these types of cloud stocks are in the vein of Twitter (TWTR), Salesforce (CRM), Square (SQ), and so on and at the vanguard of the hullabaloo of growth stocks.

Why are growth stocks so popular?

Growth stocks are companies that increase their revenue and earnings faster than average.

A growth company relentlessly develops an innovative product or service or at the top of the pack of fastest-growing industries and unsurprisingly that is technology, and that fact won’t change for generations.

Firms growing faster than average for long periods tend to be rewarded by the market, and this is why there has been a massive migration to growth stocks that has enriched shareholders of Apple (APPL), Facebook (FB), Netflix (NFLX), and so on.

Growth also begets additional growth and the faster they grow, the bigger the returns can be.

They are also more expensive than the average stock in terms of metrics like price-to-earnings, price-to-sales, and price-to-free-cash-flow ratios, but investors look past this in an age of expanding liquidity which is the catalyst that breathes even more momentum into these stocks.

US growth stocks secure a premium just for the possibility they will fulfill their parabolic growth potential.

Capitalizing on powerful long-term trends can grow their sales and profits for many years, and the following are a list of seminal trends that all involve technology data points as the secret sauce.

These powerful trends will last decades giving you plenty of time to claim your share of the profits they create.

Rank growth companies with strong competitive advantages. Otherwise, their business might fail.

Some competitive advantages are:

Pinpointing large addressable markets means a larger opportunity to secure higher revenue and Twilio is occupying a spot at the intersection of generational, long-term trends and almost unfair competitive advantages.

The underlying shares have rocketed this year as communications has never been more important. This is a great buy and hold stock for the long term because trading short term is difficult with its elevated volatility.

Mad Hedge Technology Letter

July 6, 2020

Fiat Lux

Featured Trade:

(WHY AN OFFICE IN BELGRADE MAKES SO MUCH SENSE)

(OKTA), (SPLK), (CRM), (WKDAY), (TWLO), (NOW)

My nephew paid nothing for phone, transport, internet, utilities during the coronavirus. I’ll tell you how he did it and no, he did not live with his parents or anyone else footing the bills. The future and a massive deflationary wave of technology can be found in how my nephew lives his life.

This is a story about James.

His life is the reason why the U.S. economy will never be the same and highlights the level of metamorphosis going on in our newfound home offices.

The usual culprit of the element inciting change is tech with the aftermath a catalyst for another wave of gigantic deflation.

The statisticians need to check what they are doing because nothing adds up in the deflationary world anymore.

This downward pressure on inflation is likely to be relentless, not just transitory offering central banks more flexibility with corporate accommodative policies without threatening to invoke the specter of inflation.

This is part of the reason why the bull market in tech stocks will be infinite.

Many economists and officials are befuddled, and such worries have never been far from the surface in the period after the financial crisis, the Great Recession, and now Covid-19.

The only thing constant right now is uncertainty.

Technologies are spawning “supply side shocks” in many areas of the global economy by permitting a more intense and efficient utilization of resources.

Also, replacement often leads to the betterment of people’s lives as software disrupts and cannibalizes many established goods and services.

One recent example that couldn’t illustrate this better for the “have nots” is car rental company Hertz, who woke up one day and found their business model shattered into oblivion and obsolete.

James has a modest U.S. income of $4,000 per month, which does not get you anywhere in megacities like New York or San Francisco.

After taking into account car maintenance, gas bills, car insurance, utilities, and rent, there might be $1,000 left over if luck is on the right side.

This type of income just doesn’t cut it in many American cities.

James faced a daunting challenge to acquire the quality of life he desired in most American megacities.

James works for a small start-up tech company, and after he proved to management that he was a legitimate contributor, he quickly asserted his leverage by requesting his manager to sanction a move to a full-time remote position.

Management didn’t want to lose him and reluctantly agreed contingent on a rolling 6-month review.

But James didn’t settle on Bakersfield, California, or even Klamath Falls, Oregon where he could significantly cut his bills.

He chose to take his talents to Belgrade, Serbia.

Deflationary impulse is pervasively spread across economic sectors where its presence has been difficult to note and with James’ housing budget now abroad, his dollars are partially taken out of the U.S. financial picture.

How can such “supply-side shock” manifest itself so quickly? Surely, the supply of land is largely fixed, particularly in areas that have already been urbanized.

The answer lies with technology that created additional capacity of the second industrial revolution, such as increasingly taller high-rise buildings.

Fast forward to today.

A company like Airbnb showcases how digital technologies are allowing more intensive resource utilization. There was abundant accommodation capacity hidden in the world’s cities — but it was not accessible until the internet, smartphone adoption, and Airbnb’s founders’ ingenuity unlocked it.

James is taking advantage of these wrinkles cutting his housing and office bill and crashing his monthly budget to the bare minimum.

James didn’t even feel the need to pay a deposit on a 1-year rental lease choosing to forego rental stability for the optionality of movement.

His Belgrade Airbnb space doubled as his home office.

Airbnb usually offers a 28-day discounted price which is classified as a “long stay.”

Many of these discounts are 30% or more, meaning James only paid $350 per 28 days to live in the Belgrade city center and would move around to different neighborhoods he felt were palatable.

He especially liked the Austrian-Hungarian historical district Zemun and the hipster vibe in Dorchol near the Belgrade City Center.

After the coronavirus hit, these “long term” rentals went from $350 to $200 per 28 days as tourists fled the city centers of Europe, and Airbnb prices crashed with cratering demand.

Why doesn’t James pay for internet, phone, and utilities?

Utilities and Wi-Fi are included in the price of the Airbnb covered by the host along with the furniture and amenities like air conditioning, fully equipped kitchen, microwave, dishwasher, iron, and washing machine.

James has substituted his phone bill opting for chat apps WhatsApp, Skype, FaceTime, Signal, and calls over Wi-Fi.

He keeps a Google Fi phone account to maintain a U.S. number, but keeps it permanently “paused” and only uses it to receive security and verification codes from his U.S. bank, IRS to pay taxes, and mortgage service provider to pay his mortgage online.

He manages to log on to these important portals via a virtual private network (VPN) that routes through a U.S.-based server.

He leases his U.S. house, which he owns, out to a tenant who covers 100% of James’ monthly mortgage costs and handed over his property to a local property manager to be managed.

James doesn’t pay for any transport fees because his city center apartment is walking distance to every main artery in Belgrade giving him access to Turkish-style coffee houses, to Cevapi grilled barbecue shops, to designer Hookah lounges all within a 15-minute walk.

The 2 to 3 times he needs to jump on the tram network to attend a party or night event, he borrows his friend’s yearly transit pass or just skips the fare completely. If he needs to pay, it is 75 cents for a 1-way ticket anywhere in Belgrade.

James has been living out of 2 suitcases for as long as I can remember and has never owned a car, despite growing up in the U.S. and graduating high school and university here.

Although many in the family think he is overly extreme, his intensely minimalistic lifestyle is food for thought; even though he was the first I had ever seen live in such a simplistic, draconian way.

The fallout from the coronavirus and the trends of deflationary technology show that James was ahead of his times when nobody knew it and recently accelerating trends validate his life choices.

James has effectively been planning for a pandemic his whole life which is why he has successfully navigated it, while many Millennials his age have been wiped out, drowned into debt they can never get out of.

If the U.S. suddenly gets tens of millions of James living a variation of his life, many services and products just wouldn't sell in the U.S. anymore. And if they are as extreme as James, housing will crash in all American megacities.

The reality is somewhere in between.

Reinvention is the U.S.’s strong point, but now young people are arbitraging literally everything in their lives, applying a global perspective with a good dose of software to support ultimate goals.

I will assume that most goals end up with obtaining a higher life quality.

Moving forward, investors will need to reprogram their technology compasses around firms that support a “James” type of lifestyle simply because there will be more people like this every day.

Software companies that mesh with this overarching thesis are Okta (OKTA), Splunk (SPLK), Salesforce (CRM), Workday (WKDAY), Twilio (TWLO), and ServiceNow (NOW).

The broader conclusion is that high-quality software stocks will outperform any other sub-sector or sector from now until forever.

As for James, I heard he finally decided to cough up money for local phone data which comes in at a mind-boggling $1 per 1 GB in Belgrade only 10% the cost of the same GB in inexpensive western countries.

Mad Hedge Technology Letter

February 26, 2019

Fiat Lux

Featured Trade:

(WHY THE BIG PLAY IS IN SOFTWARE),

(AMZN), (WMT), (ZEN), (FB), (TWLO)

Buy and hold domestic software companies for dear life because that is what the market is giving you.

Take them with both hands.

These revenue models should revolve around developing the lucrative North American digital consumer markets.

Tech is all about giving you pockets of dispersion and my job to herd you into these pockets of opportunity created by pockets of dispersion.

We have once again been delivered a few more poignant indicators allowing us to gauge the market appetite for certain tech barometers.

Incandescent as can be, recent news of hardware companies planning to bring exorbitant foldable phones to market has me profusely shaking my head.

Huawei announced plans to debut the Mate X foldable 5G smartphone with a price tag of a staggering $2,600.

This followed an announcement by Korean behemoth Samsung to roll out the Samsung's Galaxy Fold and the Koreans plan to sell this luxury product for $1,980.

Chinese Huawei Mate X is 5G-supported and can simply fold into a slimmer 6.6-inch smartphone or unfold into an 8-inch tablet.

This is another case of smart manufacturers overreaching for a market that doesn’t exist and shouldn’t exist.

I believe the demand for screen-related smart products at this price point is scant at best.

If you compare foldable phones to a $600 high-tier Samsung Android smartphone with a 6-inch screen, Samsung and Huawei would need to convince consumers the extra $1,500 or in Samsung’s case, $2,200 is worth the extra relative wad of cash.

My bet is that these foldable phones aren’t worth even $300 more of aggregated incremental value let alone $500 and for many consumers like me, it’s worth zilch.

In no way, aside from the gimmick of buying one of these novelties, does buying a foldable phone justify the price.

This is another example of the common-sense factor that has been completely absent from a product cycle.

Product viability and product desirability do not walk hand in hand.

The screen-related smart device market is saturated, evident by the elongated refresh cycle in smartphone usership.

Blame the expensive price tags of over $1,000 and the removal of carrier subsidies that have caused the upgrade cycle to skyrocket from 2.39 years in 2016 to 2.83 years in late 2018.

Then there is the touchy issue of cannibalizing other hardware product lines as many of the potential foldable phone customers might interchange the foldable phone with normal smartphones.

This all screams bad strategy with companies saddled in a glut of inventory.

It takes R&D years to follow through and develop the technology to bring it to market, and it is entirely conceivable this could become a big write-off.

If price cuts happen shortly after the debut, prospects look bleak.

In general, consumer sentiment has soured for more of this type of tech. Many people are just exhausted from screen time and the cycle of the newest hardware screens is failing to excite existing customers bases.

The only conclusion I can make is that tech today is about software, software, and particularly domestic software.

If you compare software to hardware head to head now, software functionality is still increasing 15% YOY juicing up efficiency and productivity.

What will foldable phones offer a digital nomad or working professional?

Not much.

It highlights the absence of a productivity or functionality boost that digital device users are scouring for now.

Stay away from hardware.

Why is domestic software preferred over international software that scales the earth five times around?

Regulation.

It has reared its ugly head again.

The avalanche of negative headlines applied to American big tech is finally becoming a self-fulfilling prophecy.

It was only a matter of time until someone took note, and in this case, various Asian governments have taken note.

In a bid to blunt American tech’s first mover advantage, the Indian government has written up a draft of regulatory measures in order to make the Indian tech landscape a fairer playground.

This will have the intended effect of creating a national powerhouse of tech firms employing local people.

India has effectively taken a page out of China’s playbook using home-field advantage to nurture homegrown talent.

Large American tech companies have made India a playground of binge investments lately with Amazon (AMZN) shelling out $5 billion and Walmart (WMT) brazenly pouring $15 billion into e-commerce heartthrob Flipkart.

This is awful news for them.

They will have to adjust to India’s new-found zeal for digital regulation and a heavy restructuring of the business model could be in the cards in 2019 along with higher costs of running these businesses.

India has followed China in its footsteps demanding data to be localized meaning data centers won’t be able to run and store Indian data abroad.

American participants will have no other choice but to pony up the extra costs.

Readers might forget that India is the current battleground of global tech growth and Amazon will not have unfettered market access like they did breaking into Europe and dominating e-commerce from the start.

Amazon and Walmart can thank Facebook (FB) which has been the main culprit in bringing wave after monstrous wave of heavy criticism on a whole industry.

Facebook has effectively brought forward the regulatory storm that otherwise would have happened a few years later down the road.

In any case, this makes life harder for data-oriented companies who wish to navigate hazardous foreign tech climates.

Domestic angst against local tech has given the rubber stamp for full-on data government mandates abroad from India to Vietnam.

What does this all mean?

In 2019, data regulation could shrink expected growth levers while hardware companies are becoming even more desperate as these Hail Marys could quickly turn into liabilities.

I nailed software picks Zendesk (ZEN) and Twilio (TWLO) amongst others from a strong group of enterprise software stocks.

Twilio’s performance could potentially become my best pick of 2019, it’s on a straight line up even with all this clutter and chaos around the world.

Mad Hedge Technology Letter

February 19, 2019

Fiat Lux

Featured Trade:

(THE SAFE PLACE TO HIDE IN TECH),

(CSCO), (ORCL), (WDAY), (ZEN), (HUBS), (NOW), (PYPL), (VEEV), (TWLO)

Great quarter by Cisco (CSCO).

That was the first thought in my head when perusing their quarterly earnings.

It’s been hit or miss for tech companies lately and at the end of 2018, I stood up and told readers to double down on software companies and specifically enterprise software companies.

Well, Cisco has skin in this software game because corporations cultivating software need the best type of network infrastructure money can buy.

Cisco is the foundational hardware on what current high-end software is built on.

It is all rosy to have a spectacular roof design, but without a solid foundation, we have nothing more than a house of cards.

The great part about Cisco is that they are immune to the software battle taking place inside of industries because they do not build the enterprise software that is built on top of the Cisco infrastructure.

We have seen our fair share of software companies go sideways such as Oracle (ORCL) who have presided over a stale patchwork of database system software created last gen.

However, on the other side of the coin, my prediction of enterprise software companies leading tech has been spot on.

Zendesk (ZEN), HubSpot (HUBS), ServiceNow (NOW), Workday (WDAY), PayPal (PYPL), Salesforce (CRM), Veeva Systems (VEEV), and Twilio (TWLO) are software companies that I was incredibly bullish on as we turned the calendar year and they have not disappointed with nearly all of these names flirting with all-time highs.

All these software companies need Cisco.

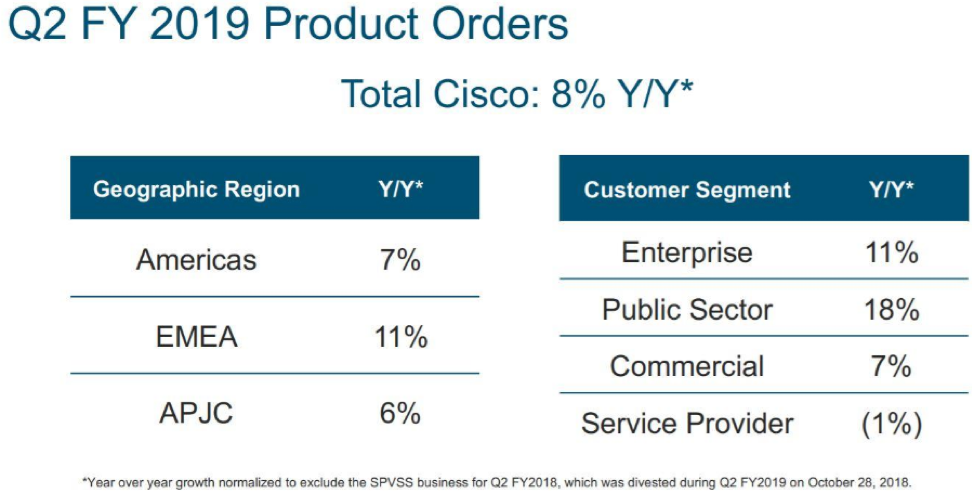

What stood out for me was that public sector orders grew 18% last quarter signaling that not only are the private corporations snapping up Cisco products, but governments are embedding their offices with Cisco’s Internet Protocol-based networking and other products related to the communications and information technology industry.

And if you wanted a general tech stock to capture the migration from analog commerce to digital and stay out of the high stakes online media segment, this would be the stable name that would check all the boxes.

And if you thought this was just a domestic story, once again, the scope is wider with Europe, the Middle East and Africa (EMEA) sales expanding by 11% which eclipsed America sales by 4%.

The only blip on the radar was service revenue slipping by 1% to $3.17 billion, but I do not view that as a pattern of sequential deceleration and pricing mechanisms can be altered to relaunch growth.

If you thought that Cisco doesn’t sell any software – you are wrong.

The software they do sell applies to operating the proprietary hardware that they produce.

Cisco’s wide competitive advantage stems from the industries toweringly high barriers of entry and that they make great products relative to other players.

The infrastructure software that liaises brilliantly with its hardware is succinctly named Cisco ONE Software.

This software suite is molded to face the most relevant use cases in the data center, WAN, and access edge.

CEO of Cisco Chuck Robbins characterized the current geopolitical and overall economic landscape as “complex” but experienced “zero difference” in Chinese revenue giving the company a quarterly victory in the Middle Kingdom.

China’s economy is decelerating faster than we can understand. The latest details of ride-hailing leader Didi sacking 2,000 employees is a warning flare to the rest that open wounds are appearing in the economy and are becoming harder to conceal.

And for Cisco to do a quarter with no significant Chinese downdraft is a good sign that the company can handle the upcoming recession in 2020.

As a sign of further strength, Cisco raised its dividend and boosted stock buybacks which are all the trappings of what great companies do.

Cisco already made $5 billion of repurchases last quarter which was on top of the $6 billion they bought in October 2018.

This method of financial engineering helps put a solid floor under the stock delighting investors and ignites the share price.

And the capital allocation encore means that Cisco will pile $15 billion into its buyback program with this fresh authorization, and the company is forecasted to produce at least $15 billion in free cash flow over the next year.

Cisco’s balance sheet is glistening and even has options to adventure into meaningful M&A if they see something that catches their eye without any real hit to the balance sheet.

These multiple tailwinds in a precarious economic point in the cycle have investors aware that there are worse options out there to invest capital than tech thoroughbred Cisco.

And if you thought the one variable that could turn this earnings report from good to bad was expenses and margins, well, Cisco covered their bases on that one too.

Margins came within the forecasted guidance with gross margins slightly trending down by 1% to 64.1%.

Expenses were reigned in and management saw a small nudge up of 3% causing investors to take a deep sigh of relief.

Cisco is in a superior strategic spot to most tech companies and is a staunch participant of the migration to digital.

Buy shares on the dip.

Winter 2018 was a time to remember as American tech shares were caught up in a perfect storm of a global growth scares, interest rate gyrations, and a political tug of war that sees no end in sight.

All of this made investors run for the hills after a huge run-up of tech shares since the February correction in 2018.

Even after all the chaos, there is one tech stock that has muscled out the noise and is hovering at all-time highs.

Coincidently, this is a name that I recommended last year as a strong 2019 play and I would like to reaffirm my prognosis by doubling down on cloud communications company Twilio.

Twilio will be a darling of 2019 because it seeks to upgrade a whole swath of communications in legacy companies that are scurrying to compete with the rest who have forged ahead.

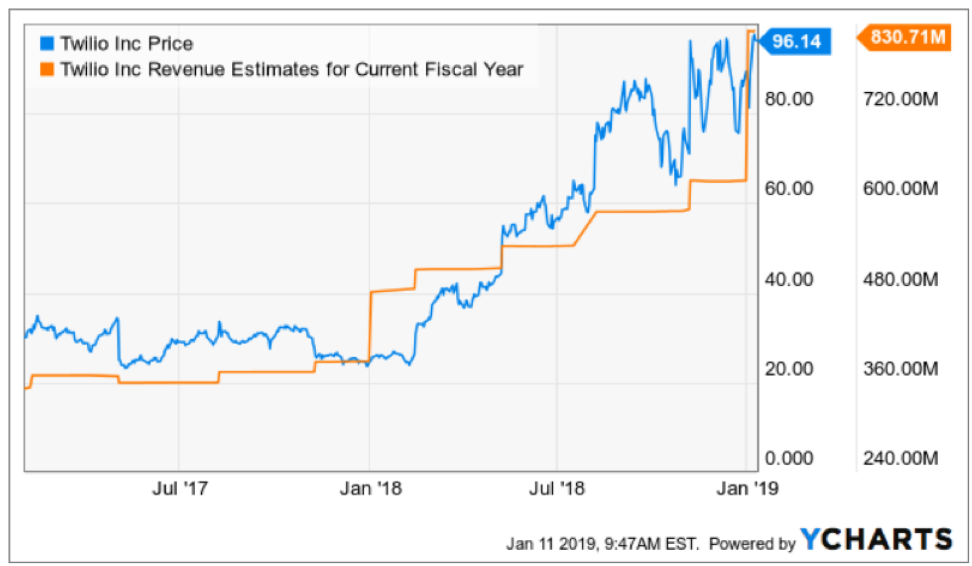

The start of 2019 has been a positive omen for Twilio shares, and are almost 10% higher in this short span of time.

It’s discernable that it is not only me who believes in this company and naysayers are few and far between.

Twilio doesn’t get as much PR as it should because making sure the back-end communication channels are executing at optimum levels is not exactly a sexy part of tech with shiny smartphones and wearable gadgets.

This company produces software and are good at what they do.

Many of you might not have even heard of them but I am sure you have heard of companies such as Uber, Lyft, and Airbnb.

Why do I mention these three private tech companies that are on the verge of going public this year?

Because this trio of unicorns is all powered by Twilio’s communication technology that is best of breed in their genre of cloud software.

More specifically, Twilio is a platform as a service (PaaS) firm offering programmatic phone call functions, can automate sending and receiving text messages, and performs other communication functions using its web service APIs.

When your shaggy-haired Uber driver calls asking you to reveal yourself out of a concrete apartment block or your lavish gated community, this is all facilitated by Twilio’s technology.

At the 2018 Twilio Signal Conference in San Francisco, Twilio indicated that its latest “call center in a box” product called Flex was up and running after announcing in March last year.

Prior to Twilio’s roll-out, this type of call center functionality was only reserved for the Fortune 500 companies that could afford expensive software to serve its minions of customers.

The small guy was left out in the cold as usual.

Twilio has reshaped the call center and, at $1 per hour or $150 per month, has made itself a gamechanger for SMEs who don’t have the manpower or capital to fund exorbitant back-end operations.

Twilio is really going after anyone with a light or bulky-shaped wallet as you see from their all-star lineup of customers. U-Haul, real estate website Trulia, and data analytic firms Scorpion and Centerfield are just a few of their customers proving the incredible flexibility and inclusive nature of the software.

It’s not a shock that this stock has gone ballistic in 2018 surging over 200% and I must admit investors need to wait for this molten hot stock to cool down.

But how can you blame a company that habitually beats any expectations by investors because of its super growth model and rapid broad-based adoption?

From the fourth quarter of last year, revenue accelerated to 48% YOY and Twilio followed that up with a blistering 54% YOY quarter.

Then they pulled a shocker guiding down only expecting 35% to 37% growth but dismantled any whiff of jangling investors' nerves by posting another quarterly growth rate of 54%.

If you average out the three-year sales growth rate, few can topple the 57% Twilio has registered.

Performance has been fantastic, to say the least, and Flex could be the product that widens their industry lead and fortifies the moat around them.

Airbnb, Uber, and Lyft will avoid tinkering with the back end of their operations before their 2019 IPOs boding well for Twilio who are on a hot streak scoring a series of big contracts.

And as their IPO dates creep closer, I firmly believe that the quiet story of Twilio will jump to the fore.

There is only so long this brilliant company can be kept under wraps.

If you take a long-term view of companies, this cloud company will be investor’s ticket to early retirement.

Even though Twilio has failed to become profitable, this year bodes well with EPS growth expected to be over 10%.

This year will be the precursor to 2020 when Twilio really invigorates earnings capability with analysts forecasting over 48% EPS growth in 2020.

Sometimes cloud companies must move mountains and absorb years of losses to finally breach the profitability marker, that time is about to come for Twilio and along with maintaining its riveting growth, the business model will become more sustainable with a vast improvement in cash flow.

Although Twilio’s competitive advantage is not as large as Microsoft (MSFT), this company has the same type of momentum going into 2019.

I believe many institutional investors have yet to hear this name echo around investment offices, and if any tech stock is going to be the darling of 2019, it will be Twilio.

I expect Twilio shares to shortly eclipse the $100 mark and maintain that level with an infusion of zeal that mimics Microsoft’s share price.

Notice that through hell and high water, any massive sell-off that crushes Microsoft swan diving below $100, shares find itself above $100 again in a jiffy.

I expect Twilio to exude similar characteristics, albeit with more volatility.

Twilio has the ability to rise 10% or even 15% on any given day on good news.

Being at all-time highs again only illustrates the attractiveness of the name.

In general, this should really be a software-as-a-service (SaaS) year for investors as the migration to these services picks up speed.

Any meaningful dip that can be attributed to outside forces should be bought because there are no fundamental problems with Twilio.

Don’t chase the stock here because it’s up almost 300% in the past 365 days - wait for it to fall into your wheelhouse.

To add the cherry on top, this company is far away from the geopolitical trade winds.

And even though fundamental differences have yet to be hashed out, at least it debugs one potential headwind to the fundamental story.

Twilio should outperform this year relative to the large tech stocks, it’s up to you if you want to ride on the coattails of this story or try your luck on less qualified names.

And not to toot my own horn, but this stock is already up almost 30% since I urged readers to pile into it.

I am strongly bullish Twilio.

Mad Hedge Technology Letter

January 9, 2019

Fiat Lux

Featured Trade:

(TOP 8 TECH TRENDS OF 2018),

(GOOGL), (FB), (WMT), (SQ), (AMZN), (ROKU), (KR), (FDX), (UPS), (CRM), (TWLO), (ADBE), (PYPL)