Global Market Comments

April 22, 2022

Fiat Lux

Featured Trade:

(APRIL 20 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPX), (TSLA), (TBT), (TLT), (BAC), (JPM), (MS),

(BABA), (TWTR), (PYPL), (SHOP), (DOCU),

(ZM), (PTON), (NFLX), (BRKB), (FCX), (CPER)

Global Market Comments

April 22, 2022

Fiat Lux

Featured Trade:

(APRIL 20 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPX), (TSLA), (TBT), (TLT), (BAC), (JPM), (MS),

(BABA), (TWTR), (PYPL), (SHOP), (DOCU),

(ZM), (PTON), (NFLX), (BRKB), (FCX), (CPER)

Below please find subscribers’ Q&A for the April 20 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Silicon Valley.

Q: Should I take profits on the ProShares UltraShort 20+ Year Treasury ETF (TBT), or will it go lower?

A: Well, you’ve just made a 45% profit in 4 months; no one ever gets fired for taking a profit. And yes, it will go lower, but I think we’re due for a 5 -10% rally in the (TBT) and we’re seeing some of that today.

Q: Do you think the bottom is in now for the S&P 500 Index (SPX)?

A: No, I think the 50 basis point rate hikes will put the fear of God into the market and prompt another round of profit-taking in stocks. So will another ramp up or expansion in the Ukraine War, and so could another spike in Covid cases. And interest rates are getting high enough, with a ten-year US Treasury (TLT) at 2.95% and junk at 6.00% that they will start to bleed off money from stocks.

So there are plenty of risks in this market that I don’t need to chase thousand point rallies that fail the following week.

Q: What would cause a rally in the iShares 20 Plus Year Treasury Bond ETF (TLT)?

A: Everyone in the world is short, for a start. And secondly, we’ve had a $36 point drop in the market in 4 ½ months—that is absolutely screaming for a short-covering rally. It would be typical of the market to get everybody in the world short one thing, and then ramp it right back up. You can bet hedge funds are just gunning for that trade. So those are two big reasons. Another big reason is getting a slowdown in the economy. Fear of interest rate rises and yield curve inversions are certainly going to scare people into thinking that.

Q: Where to buy Tesla (TSLA)?

A: We had a $1,200 all-time high at the end of last year, then sold off to $700—that was your ideal entry point, on that one day when the market was down $1,000 and they were throwing out Tesla stock like there was no tomorrow. We have since rallied back to the 1100s, so I'd say at this point, anything you could get under just above the $200-day moving average at $900 would be a gift because the sales are happening and they’re making tons of money. They’re so far ahead of the rest of the world on EV technology that no one will ever be able to catch up. A lot of the biggest companies like Ford (F) and (GM) are still unable to mass produce electric cars, even though they’re all talking about these wonderful models they're bringing out in 2024 and 2025. So, I think Tesla is just so far ahead in the market that no one will catch them. And the stock will have to reflect that by trading at a higher premium.

Q: I Bought the ProShares UltraShort 20+ Year Treasury ETF (TBT) at your advice at $14, it’s now at 425. Time to take the money and run?

A: Yes, so that you’re in position to rebuy the (TBT) at $22, or even $20.

Q: I bought some bank LEAPS such as Bank of America (BAC), JP Morgan (JPM), and Morgan Stanley (MS) just before earnings; they’re doing well so far.

A: That will definitely be one of my target sectors on any recovery; because the only reason the stock market recovers is because recession fears have been put away, and the only reason the banks have been going down is because of recession fears. Certainly, the yield curve inversion has been helping them lot, as are absolute higher interest rates. So yes, zero in on the banks, I’m holding back waiting for better entry points, but for those who are aggressive, there’s no problem with scaling in here.

Q: If Putin uses a tactical nuclear weapon in the Ukraine, what would be the outcome?

A: Well, I don't think he will, because you don’t want to use nukes on your neighbors because the wind tends to blow the radiation back into your own country. It also depends on when he does this; if Ukraine joins NATO, joins the EC, and NATO troops enter Ukraine, and then they use tactical nukes, France and England also have their own nuclear weapons. So, attacking a nuclear foe and risking bringing in the US, who could wipe out the whole country in minutes, would not be a good idea.

Q: Would you get into Chinese stocks here?

A: Not really; China seems to have changed its business model permanently by abandoning capitalism. The Mad Hedge Technology Letter is currently running a short position in Alibaba (BABA) which has proved highly successful. Although these things are stupidly cheap, they could get cheaper before they turn around. Also, there’s the threat of delisting on the stock exchanges facing them in a year or two, and the trade tensions which continue with China. China doesn’t seem friendly anymore or is interested in capitalism. You don't want to own stocks anywhere in that situation. And by the way, Russia has also banned all foreign stock listings. China could do the same—not good if you’re an owner of those stocks.

Q: How would you play Twitter (TWTR) now?

A: I think it’s a screaming short, myself. If the board doesn’t accept Elon’s offer, which seems to be the case with their poison pill adoption, there are no other buyers of Twitter; and Elon has already said he’s not going to pay up. So you take Elon Musk’s shareholding out of the picture, and you’re looking at about a 30% drop.

Q: Many of the biggest Covid beneficiaries are near or below their March 2020 lows, such as PayPal (PYPL), Shopify (SHOP), DocuSign (DOCU), Zoom (ZM), Peloton (PTON), Netflix (NFLX), etc. Are these buys soon or are there other new names joining them?

A: I think this will continue to be a laggard sector. I think any recovery will be led by big tech, and once big tech peaks out after a 6-month run, then you may get the smaller ones catching up—especially if they're still down 80% or 90%. So that’s a no-touch for me; too many better fish to fry.

Q: Do you think inflation is transitory or are we headed toward double digits over the long term?

A: The transitory argument got thrown out the window the day Russia invaded Ukraine; they are one of the world’s largest producers of both energy and wheat. So that definitely set those markets on fire and really could end up adding an extra 5% in our inflation numbers before we peak out. I think we will see the highs sometime this year, could be as low as 4% by the end of this year. But we may have a double-digit print before we top out, and that could be next month. So, if you’re looking for another reason for stocks to sell out, that would be a good one.

Q: If the EU could limit oil purchases from Russia, then the war would be over in a month since Russia has no borrowing power or reserves.

A: The problem is whether they actually could limit oil purchases, which they can’t do immediately. If you could limit them in a year or cut them down by like 80%, we could come up with the other 20%, that is possible. Then, the war would end and Russia would starve; but Russia may starve anyway. Even with all the rubles in the world, they can’t buy anything overseas. Basically, Russia makes nothing, they only sell commodities and use those proceeds to buy consumer goods from abroad, which have all been completely cut off. They’re in for an economic disaster no matter what happens, and they have no way of avoiding it.

Q: What are your thoughts on supply chain problems?

A: I actually think they’re getting better; I watch the number of ships at anchor in San Francisco Bay, and it’s actually down by about half over the last 3 months. People are slowly starting to get things that they ordered nine months ago, used car prices are starting to roll over…so yes, it’s going to be a very slow process. It took one week to shut down the global economy, it’ll take three years to get it fully reopened. And of course, that’s extended by the Ukraine War. Plus, as long as there are supply chain problems and huge prices being paid for parts and labor, you’re not going to have a recession, it’s impossible.

Q: What’s your outlook on tech stocks?

A: I see them bottoming in the current quarter, and then going on to new all-time highs in the second half.

Q: What about covered calls?

A: It’s a really good idea, allowing you to get long a stock here, and reduce your average cost every month by writing calls against your position until they eventually get called away. Not too long ago, I wrote a piece on covered calls, so I could rerun that again to get people familiar with the concept.

Q: If Warren Buffet retires, what happens to Berkshire Hathaway (BRKB) stock?

A: It drops about 5% one day, then goes on to new highs. The concept of a 90-year-old passing away in his sleep one night is not exactly revolutionary or new. Replacements for Buffet have been lined up for so long that now the replacements are retiring. I think that’s pretty much baked in the price.

Q: Any plans to update the long-term portfolio?

A: Yes it’s on my list.

Q: Too late to buy Freeport McMoRan (FCX)?

A: Yes I’m afraid so. We’ve had a near double since September when it started moving. However, I would hold it if you already own it and add on any substantial selloff. Freeport McMoRan announced fabulous earnings today, and the stock promptly sold off 9%. It was a classic “buy the rumor, sell the news” type move. This is despite the fact that the United States Copper Fund ETF (CPER), in which (FCX) is a major holding, is up on the day. Please remember that I told you earlier that each Tesla needs 200 pounds of copper, that Tesla sales could double to 2 million this year, and that they could sell 4 million if they could make them. It sounds like a bullish argument of me, of which (FCX) is the world’s largest producer.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Stay Healthy

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

April 18, 2022

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or GET READY TO SELL IN MAY)

($INDU), (SPY), (TLT), (WFC), (JPM), (TSLA), (TWTR)

So when you are supposed to “Sell in May and go away”, what are you supposed to be doing on April 18?

Not much.

War, inflation, disease, runaway energy prices, and soaring interest rates are usually not a good backdrop for trading stocks. When the wind is blowing against me with gale-force winds instead of behind me, I tend to quit. I only like playing games that are rigged in my favor, or in yours.

Retreating to fight another day sounds like a good strategy to me because it’s much easier to dig out of a small hole than a large one. And it’s impossible to recover if you lost all your money chasing marginal low-quality trades. That 100-day cruise around the world that Cunard is offering right now looks pretty good. If the central bank says it is set on slowing the economy, believe it. The free Fed put is a distant memory.

But whatever Armageddon we are facing out there, it will be a modest one. We now have an unemployment rate of 3.6%, but there are still 11 million open jobs. That means there are more jobs in the US right now than workers, a first in history.

There are in fact several big positives the markets are ignoring right now because it is fashionable to do so. You know these supply chain problems? They’re slowly going away. You see this in falling freight rates for US truckers.

The Cass Freight Index measure of domestic shipping demand edged up a bare 0.6% in March from the month before, an unseasonable slowing of growth at the end of the quarter. From where I sit, the number of Chinese container ships at anchor in San Francisco Bay is on a definite decline.

Going into real recessions, consumers usually baton down the hatches, don their hard hats, and reign in spending. And while they tell pollsters they are worried about the economy, they act like they believe in the opposite, spending with reckless abandon. Wells Fargo (WFC) has seen spending on credit cards soaring by 33% in Q1, while it has jumped by an impressive 29% at JP Morgan (JPM).

There is also a great positive out there which is being completely ignored by the market. The pandemic is gone. Daily cases have dropped from one million to only 20,000 in two months, a record drop in the history of epidemiology. Masks are now only required at mass events like rock concerts and the San Francisco Ballet.

So I will endeavor to entertain you with my stories long enough to keep you from getting bored until trading stocks becomes the slam dunk no-brainer affair it once was. That would be in anything from 2-5 months.

Elon Musk makes $53 billion takeover bid for Twitter in a move that gobsmacked Wall Street. He made the offer in a 281-character tweet to the board of directors. His goal will be to end all censorship, which means bringing back the crazies and the violent. If they don’t accept his premium offer, then he will sell the 9.9% of shares that he already owns and the board will get sued to death by shareholders.

Inflation jumps to 8.5% YOY, a 40-year high, with half of the increase coming from gasoline prices. Stocks and bonds were up on a “buy the rumor, sell the news” move. Unless oil prices completely collapse, next month will be worse.

Producer Price Index rockets by 11.2%, an 11-year high. This is on the heels of yesterday’s red hot Core Inflation report. It makes a half-point rate hike on April 29 a sure thing.

Retail Sales jumped 0.5% in March, and up 6.9% YOY, while import prices hit an 11-year high.

Bonds hit new three-year lows, with yields soaring to 2.81% overnight. The market is transitioning from a Fed that is raising rates from a quarter point at each meeting to a half point. We may be reaching the end of this leg down, off $9.00 in weeks. Only sell the big rallies. (TLT) LEAPS holders are sitting pretty.

Mortgage Refis down 67% YOY, thanks to a 30-year fixed rate mortgage that has topped 5.0%. It looks like the loan sharks won’t be grabbing as much in fees. This market won’t recover for several years. If you didn’t refi last year at century low rates, you’re screwed.

NVIDIA downgraded from outperform to neutral and the price target was chopped from $360 to $225 by Baird & Co. It’s a bold move as (NVDA) has long been a Mad Hedge favorite and 70-bagger over the last five years. Baird cites cancellations driven by a combination of excess GPUs, or graphics processing unit in Western Europe and Asia, as well as a slowdown in consumer demand, especially in China. Slowing consumer demand for GPUs was evident in the continuing reduction in graphics card pricing. I believe any slowdowns are temporary and you should keep buying (NVDA) on dips.

Used Car Sales take a hit, as affordability becomes a major issue. Carmax just reported a 6.5% plunge in Q4. I can sell my Tesla Model X for more than I paid three years ago because it takes a year to get a new one.

Weekly Jobless Claims hit 185,000, up 18,000 from the previous week. The stock market may be worried about a coming recession but the jobs market sure isn’t.

Morgan Stanley blows away earnings. Equity trading came in a hot $3.2 billion and bond trading $2.9 billion. The shares popped 7% on the news. Buy (MS) on dips.

Mercedes breaks 600 miles range on a single charge with its EQXX prototype, driving from Stuttgart to the French Riviera. But the cost per watt is still double Tesla’s. Mercedes plans to go all-electric by the end of the decade.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still historically cheap, oil peaking out soon, and technology hyper accelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The America coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

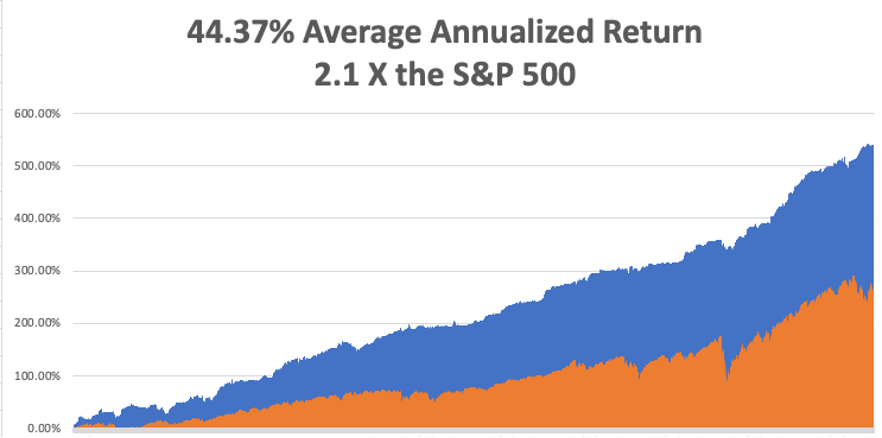

My March month-to-date performance retreated to a modest 0.38%. My 2022 year-to-date performance ended at a chest-beating 27.23%. The Dow Average is down -5.1% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky-high 68.55%.

On the next capitulation selloff day, which might come with the April Q1 earnings reports, I’ll be adding long positions in technology, banks, and biotech. I am currently in a rare 100% cash position awaiting the next ideal entry point.

That brings my 13-year total return to 539.79%, some 2.10 times the S&P 500 (SPX) over the same period. My average annualized return has ratcheted up to 44.36%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 80.6 million, up only 300,000 in a week and deaths topping 988,000 and have only increased by 3,000 in the past week. You can find the data here. Growth of the pandemic has virtually stopped, with new cases down 98% in two months.

On Monday, April 18 at 7:00 AM EST, the NAHB Housing Market Index is out. Bank of America (BAC) reports.

On Tuesday, April 19 at 8:30 AM, Housing Starts for March are published. Netflix (NFLX) reports.

On Wednesday, April 20 at 8:30 AM, the Existing Home Sales for March are printed. Tesla (TSLA) reports.

On Thursday, April 22 at 7:30 AM, the Weekly Jobless Claims are printed. Union Pacific (UNP) reports.

On Friday, April 23 at 8:30 AM, the S&P Global Composite Flash PMI is disclosed. American Express (AXP) reports. At 2:00 PM, the Baker Hughes Oil Rig Count are out.

As for me, the call from Washington DC was unmistakable, and I knew what was coming next. “How would you like to serve your country?” I’ve heard it all before.

I answered, “Of course, I would.”

I was told that for first the first time ever, foreign pilots had access to Russian military aircraft, provided they had enough money. You see, everything in the just collapsed Soviet Union was for sale. All they needed was someone to masquerade as a wealthy hedge fund manager looking for adventure.

No problem there.

And can you fly a MiG29?

No problem there either.

A month later, I was wearing the uniform of a major in the Russian Air Force, my hair cut military short, sitting in the backseat of a black Volga limo, sweating bullets.

“Don’t speak,” said my driver.

The guard shifted his Kalashnikov and ordered us to stop, looked at my fake ID card and waved us on. We were in Russia’s Zhukovky Airbase 100 miles north of Moscow, home of the country’s best interceptor fighter, the storied Fulcrum, or MiG-29.

I ended up spending a week at the top-secret base. That included daily turns in the centrifuge to make sure I was up to the G-forces demand by supersonic flight. Afternoons saw me in ejection training. There in my trainer, I had to shout “eject, eject, eject,” pull the right-hand lever under my seat, and then get blasted ten feet in the air, only to settle back down to earth.

As a known big spender, I was a pretty popular guy on the base, and I was invited to a party every night. Let me tell you that vodka is a really big deal in Russia, and I was not allowed to leave until I had finished my own bottle, straight.

In 1993, Russia was realigning itself with the west, and everyone was putting their best face going forward. I had been warned about this ahead of time and judiciously downed a shot glass of cooking oil every evening to ward off the worst effects of alcohol poisoning. It worked.

Preflight involved getting laced into my green super tight gravity suit, a three-hour project. Two women tied the necessary 300 knots, joking and laughing all the while. They wished me a good flight.

Next, I met my co-pilot, Captain A. Pavlov, Russia’s top test pilot. He quizzed me about my flight experience. I listed off the names: Laos, Cambodia, Thailand, Israel, Croatia, Serbia, Bosnia, Kuwait, Iraq, and Saudi Arabia. It was clear he still needed convincing.

Then I was strapped into the cockpit.

Oops!

All the instruments were in the Cyrillic alphabet….and were metric! They hadn’t told me about this, but I would deal with it.

We took off and went straight up, gaining 50,000 feet in two minutes. Yes, fellow pilots, that is a climb rate of an astounding 25,000 feet a minute. They call them interceptors for a reason. It was a humid day, and when we hit 50,000 feet, the air suddenly turned to snowflakes swirling around the cockpit.

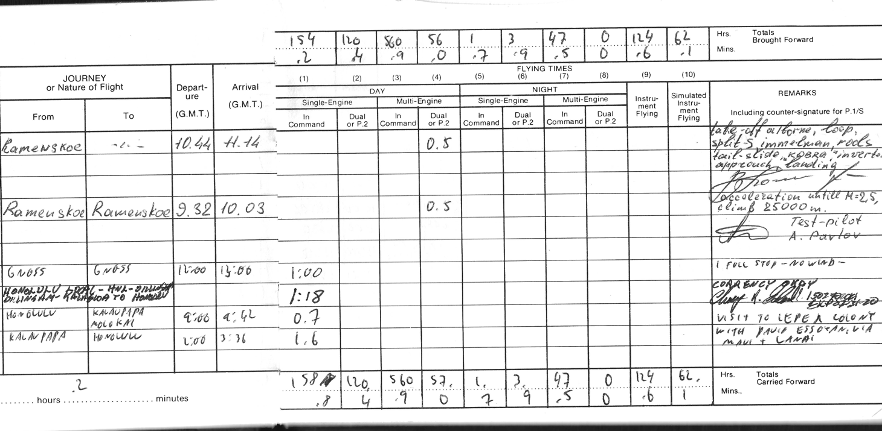

Then we went through a series of violent spins, loops, and other evasive maneuvers (see my logbook entry below). Some of them seemed aeronautically impossible. I watched the Mach Meter carefully, it frequently danced up to the “10” level. Anything over ten is invariably fatal, as it ruptures your internal organs.

Then Pavlov said, “I guess you are a real pilot, and he handed the stick over to me. I put the fighter into a steep dive, gaining the maximum handbook speed of March 2.5, or 2.5 times the speed of sound, or 767.2 miles per hour in seconds. Let me tell you, there is nothing like diving a fighter from 90,000 feet to the earth at 767.2 miles per hour.

Then we found a wide river and buzzed that at 500 feet just under the speed of sound. Fly over any structure over the speed of sound and the resulting shock wave shatters concrete.

I noticed the fuel gages were running near empty and realized that the Russians had only given me enough fuel to fly for an hour. That’s so I wouldn’t hijack the plane and fly it to Finland. Still, Pavlov trusted me enough to let me land the plane, no small thing in a $30 million aircraft. I made a perfect three-point landing and taxied back to base.

I couldn’t help but notice that there was a MiG-25 Foxbat parked in the adjoining hanger and asked if it was available. They said “yes”, but only if I had $10,000 in cash on hand, thinking this was an impossibility. I said, “no problem” and whipped out my American Express gold card.

Their eyes practically popped out of their heads, as this amounted to a lifetime of earnings for the average Russian. They took a picture of the card, called in the number, and in five minutes I was good to go.

They asked when I wanted to fly, and as I was still in my gravity suite I said, “How about right now?” The fuel truck duly back up and in 20 minutes I was ready for takeoff, Pavlov once again my co-pilot. This time, he let me do the takeoff AND the landing.

The first thing I noticed was the missile trigger at the end of the stick. Then I asked the question that had been puzzling aeronautics analysts for years. “If the ceiling of the MiG-25 was 90,000 feet and the U-2 was at 100,000 feet, how did the Russians make up the last 10,000 feet?

“It’s simple,” said Pavlov. Put on full power, stall out at 90,000 feet, then fire your rockets at the apex of the parabola to make up the distance. There was only one problem with this. If your stall forced you to eject, the survival rate was only 50%. That's because when the plane in free fall hit the atmosphere at 50,000 feet, it was like hitting a wall of concrete. I told him to go ahead, and he repeated the maneuver for my benefit.

It was worth the risk to get up to 90,000 feet. There you can clearly see the curvature of the earth, the sky above is black, you can see stars in the middle of the day, and your forward vision is about 400 miles. We were the highest men in the world at that moment. Again, I made a perfect three-point landing, thanks to flying all those Mustangs and Spitfires over the decades.

After my big flights, I was taken to a museum on the base and shown the wreckage of the U-2 spy plane flown by Francis Gary Powers shot down over Russia in 1960. After suffering a direct hit from a missile, there wasn’t much left of the U-2. However, I did notice a nameplate that said, “Lockheed Aircraft Company, Los Angeles, California.”

I asked, “Is it alright if I take this home? My mother worked at this factory during WWII building bombers.” My hosts looked horrified. “No, no, no, no. This is one of Russia’s greatest national treasures,” and they hustled me out of the building as fast as they could.

It's a good thing that I struck while the iron was hot as foreigners are no longer allowed to fly any Russian jets. And suddenly I have become very popular in Washington DC once again.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Russian Test Pilot A. Pavlov

Entries in my Logbook (Notice visit to leper colony on line 9)

U-2 Spyplane

Mad Hedge Technology Letter

April 4, 2022

Fiat Lux

Featured Trade:

(HOW TO BE AN ELITE TRADER?)

(TWTR), (TSLA), (SPACEX)

How to be an elite stock market trader?

Easy.

First, be the richest guy in the world.

Shell out $3B on a 9.2% stake in a publicly-traded tech stock that you often use.

Grab a bag of popcorn and watch the SEC filing announced and the stock soar 26%.

Make an instant $780M appreciation in your purchase, flip it if you want to right away for a profit, or hold it to most likely make another double or triple in your investment.

It seems like it’s that easy for guys like Tesla (TSLA) founder and CEO Elon Musk who announced a monster purchase in the social media messaging company Twitter (TWTR).

Making money isn’t that easy for most people, but Elon isn’t most people.

He has more gunpowder than anyone else and deploying it at this moment is an unequivocal buy signal for tech in the short term.

He usually is the smartest guy in every room and Twitter has been beaten down quite badly in the short-term going from $77 per share down to $31.

Buy low and sell high.

This formula has worked for many people.

Twitter will instantly go from a tech company rough around the edges to now an Elon Musk company.

The brand difference is immense.

First on the cards will most likely be the changing of CEO Parag Agrawal who must be responsible for the acceleration of digital ads you see on Twitter lately.

Agrawal is not Musk’s chosen man and Musk’s decision to dive into Twitter also has an activist investor element to it.

Let me remind readers that it was only just a few days ago that Elon Musk said he is “giving serious thought” to creating a social media platform that would compete with Twitter, saying that the latter has been stifling free speech.

“Free speech is essential to a functioning democracy. Do you believe Twitter rigorously adheres to this principle?” Musk tweeted in a Twitter poll.

The next day, Musk took it a step further, writing: “Given that Twitter serves as the de facto public town square, failing to adhere to free speech principles fundamentally undermines democracy. What should be done?”

In the same thread, a Twitter user asked the Tesla CEO about possibly “building a new social media platform” that would boast “an open-source algorithm.”

The user proposed that the new platform would be one “where free speech and adhering to free speech is given top priority” and where “propaganda is very minimal.”

There will be an inquisition into the “best practices” at Twitter to see who is behind the mechanisms that lead to what Musk believes is the stifling of censorship.

Naturally, it appears that Musk will be hellbent on securing a board seat and this could be the precursor to additional investments into Twitter that might have him secure majority ownership.

Musk will turn Twitter into what he sees is good for democracy and sadly for investors in the short term, which could plausibly be bad for the share price.

However, if this becomes his pet project, he will want it to succeed in the long-term like everything else he touches which turns into gold and failure is not an option.

Just imagine being part of the umbrella that is Twitter management right now, Musk will most likely push for wholesale management changes at every level.

This is also an indictment of how bad Twitter management has been.

Musk is about to remake Twitter in his own image and what does that mean for tech stocks?

In a world of high uncertainties, this offers an ironclad green light to buy tech stocks.

Certainly, Musk wouldn’t buy Twitter at this time because he believes it is at a high point.

I loaded up last Friday in tech and I believe much of the short-term bad news in technology stocks is priced into shares and we have a lull before earnings season in which there is a chance for tech stocks to make up lost ground.

The last nugget I want to throw out to readers is that Twitter could become the vehicle in which Musk develops his passion for cryptocurrency.

This would dovetail nicely with Musk’s tendency to pull workers from Tesla and Space X in order to harness synergies.

Mad Hedge Technology Letter

December 1, 2021

Fiat Lux

Featured Trade:

(TAKE A REST FROM FINTECH)

(PYPL), (SQ), (BNPL), (AMZN), (TWTR), (AAPL)

The fintech trade is tiring — that is what the underperformance of stocks like PayPal (PYPL) and Square (SQ) is telling us.

Jack Dorsey’s Square has retraced around 25% from its peak and is bang on even from where it was 365 days ago.

Not what you want to hear if you’re a fintech trader.

The pullback from PYPL is even more precipitous declining around 40% from its peak.

Certainly, it would be cliché for me to say that the low-hanging fruit is gone from the fintech trade, but that’s exactly what is happening here.

Not only that, but I would also like to point out that most companies without a home-field advantage ecosystem are getting penalized for exactly that — not having an ecosystem.

Wasn’t it weird how the whole tech sector literally gave us a rip-your-face-off selloff the other day yet, Apple was one of the only tech stocks that reacted positively?

As we move into the late stages of the economic cycle, the goalposts are certainly narrowing for the tech companies, and that’s bad news for SQ and PYPL.

Another way to get penalized is to let that moat narrow which is effectively what has happened to PYPL and SQ.

And that’s the thing with PYPL, it’s just a way to pay, and not an ecosystem.

It plays second fiddle to that of wall gardens and the user trapped in it who is spending and can’t find a way out.

Another point I would like to make is that Twitter (TWTR) at these levels is an ideal buy-the-dip candidate precisely because it’s a great walled garden whose potential has yet to be untapped.

And readers shouldn’t let the mismanagement of the company by former CEO Jack Dorsey turn you off from a great long-term investment.

PYPL would kill for a platform like Twitter and instead needs to grovel to other strategic platforms to allow them to use PYPL’s technology.

PYPL is finally exposed, and I guess more accurate would be to say they are getting undercut by stickier technology that is more convenient to the consumer.

And what does that get you in late 2021?

Downgrades and slews of them which cut blocks the stock at its knees.

We just got one from Bernstein the other day and then it almost becomes a self-fulfilling prophecy with other analyst outlets doing the same thing in a copycat league.

Instead of catching a falling knife in SQ and PYPL, traders need to let these stocks breathe and find support where we know buyers will come in to breed confidence in an upward trajectory.

Easier said than done.

What has been all the rage so far denting PYPL and SQ’s model?

Enter Buy Now Pay Later (BNPL).

Naturally, the differentiated mechanism around which this technology revolves around is the delay in paying, which is never a good concept for a fintech player who rather gets paid ASAP.

Delayed payment is one headache, but then the downward force on fees is another monumental concern, if not downright scary.

This will no doubt trounce margin expansion moving forward and evidence of slowed growth in the latest quarter does not portend well for the company, especially as pandemic tailwinds continue to fade.

Another talking point is BNPL’s lack of credit checks meaning the quality of purchasers will naturally decline, may I even say attract fraudsters as well, and the companies will need to build up loss reserves to compensate for a riskier purchaser profile.

Klarna is another major BNPL company, and they were part of this new industry that took in around 20% of all sales on Cyber Monday.

That rather high number bodes poorly for PYPL in the short term.

Reinforcing the strategic hole of a lack of walled garden is that PYPL is desperate to cultivate partnerships like PYPL’s Venmo joining forces with Amazon (AMZN) — Starting next year, you'll be able to use the money anybody Venmo’s you to buy products directly from Amazon — so long as you live in the US.

But again, Amazon is infamous for replacing outside technology with its own in-house solution over time.

PYPL’s counter solution for BNPL is to enter the BNPL lovefest as well which will effectively trigger a race to zero.

Stopgap solutions will inevitably cannibalize its own business model.

Then let’s point to another walled garden — Tim Cook’s Apple with its Apple wallet.

It’s getting better and with the Apple Card, do they ever really need to spend one second considering a partnership with PYPL or SQ.

There is an inquisition going on in the fintech industry and big body blows will need to be landed for some clear-cut solutions that will ultimately lead to consolidation.

In this precarious environment, don’t get too fancy while fintech is getting elbowed out the way, head to higher ground where balance sheets can absorb just about anything.

Mad Hedge Technology Letter

November 29, 2021

Fiat Lux

Featured Trade:

(THE FUTURE LOOKS BRIGHT FOR THIS AD TECH STOCK)

(TWTR), (FB)

Founder Jack Dorsey's stepping down as CEO of Twitter (TWTR) is great news for the stock.

Let’s not beat around the bush — it’s been brewing for some time.

It was only just before the pandemic that he announced his intentions to work remotely from Africa for 6 months.

Who does that?

Part of his job as CEO of a major Silicon Valley company is to deduce the pulse of the industry in real-time, and on the ground while rubbing shoulders with the rest of his kind.

Six-month African Safaris are romantic but don’t cut it when you are a top CEO of a Silicon Valley company and when major hedge funds are relying on advanced expertise to guide the company through a labyrinth of strategic and regulatory issues.

Whether he stepped down by his own will or was effectively forced out by activist shareholders, either way, the future stock price appears prime to shake off the years of mediocrity.

Why does Twitter need change at the helm?

Simply put, the stock has grossly underperformed the broader market for not only the last year but also the past 3 and 8 years.

The stock was trading around $70 in December 2013 and fast forward to today and the stock is around $50.

The underperformance comes under a backdrop of a cyclical bull market in which tech has been the leader with growth constantly reaccelerating.

Not only that, but Twitter also has a unique asset in which it has accrued massive scarcity value because no other technology company has anything like it.

Dorsey has mishandled the operation.

The nail in the coffin was certainly the user growth numbers in which Twitter was only able to grow the user base by 3% last quarter in North America.

Twitter announced earlier this year some major long-term goals in which one of them was to have 315 million monetizable daily active users by the end of 2023.

That number stands at 211 million users reported last quarter and is underwhelming.

Another objective was to surpass annual revenue of $7.5 billion by 2023 and as of last quarter, management said they were still on pace to achieve that, but I do not see that.

I agree they are on pace to hit that revenue target, but Twitter announced a highly disappointing forecast expecting $1.5 billion to $1.6 billion in revenue for the fourth quarter, which will be up 24%.

Twitter will need to maintain revenue growth in the mid-30% to achieve the numbers they promised, and Dorsey has proved that he is prone to botching forecasts.

How many fumbles will management let him get away with?

Granted, Dorsey was forced by activist shareholders to state explicit targets, and true, they were ambitious from the start.

However, much of the nudge in the backside stems from Dorsey largely underachieving as a CEO especially during the golden years of ad tech.

Investors saw when Founder and CEO of Facebook (FB) Mark Zuckerberg was able to release animal spirits for his ad technology platform and it’s fair to question why Dorsey can’t do the same for his company.

Even though harsh, comparing your company to Facebook is not everyone’s cup of tea, but Twitter is in the same exact industry as Facebook deploying the same exact products, so they can’t really complain about comparing.

In the last 10 years, Facebook has returned shareholders 17X their investment and Zuckerberg was agile enough to rotate from a stale Facebook platform to a booming Instagram platform.

The last major Twitter forecast called for a long-term target of 40% to 45% adjusted EBITDA margin.

For the fourth quarter, Twitter is looking for operating income in the $130 million to $180 million range. That would be down 29% the prior year.

Profitability per unit is decelerating.

As it stands, I do not envision Dorsey achieving his 2023 targets if he stayed and on top of that, changes to the iOS system have made ad targeting more difficult to extract the necessary monetizable data.

In an environment where data visibility is reducing, and other regulatory changes could be coming down the pipeline, the shareholders most likely felt they needed a change at the top.

Dorsey is by and large the legacy of what was left over after Twitter was created, and many investors know, it’s hard to kick out these tech CEOs that usually possess super-voting shares which makes it so they must vote themselves out to leave as CEO.

Dorsey didn’t have that level of moat around his position and eventually, the underperformance caught up to him.

Twitter will insert Parag Agrawal, the company’s chief technology officer, as new CEO in hopes of supercharging revenue, user, and margin growth that shareholders have been patiently waiting for.

If Agrawal can fix Twitter, then Twitter is easily an $80 stock.

Remember that Dorsey is still the CEO of Square and hasn’t been shy in expressing his passion for cryptocurrencies, and it’s likely there that he will finally be unshackled from the annoyance of running Twitter and get to focus on his favorite company.

Honestly, he hasn’t seemed interested in Twitter for a while, so it’s a win–win for both companies.