Global Market Comments

March 30, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or COPING WITH CORONA),

(INDU), (VIX), (VXX), (UAL), (WYNN), (CCL), (SSO), (SPXU)

Global Market Comments

March 30, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or COPING WITH CORONA),

(INDU), (VIX), (VXX), (UAL), (WYNN), (CCL), (SSO), (SPXU)

I am sitting in my Lake Tahoe office watching a light snow blanket the surrounding High Sierras. There is a stiff north wind whipping up whitecaps on a cerulean blue lake.

Spring break normally packs the Diamond Peak ski resort at Incline Village, Nevada. This year, it is a ghost town. The resort is closed, the streets deserted and the hotels empty.

Driving up from San Francisco, I had to stop at a Tesla Supercharging station at Rocklin, California next to a huge shopping mall for a top-up to cross Donner Pass. It was bereft of shoppers, looking like everyone had been wiped out by an uncontrollable plague. Of a hundred stores only Subway, Chipotle Mexican Grill (CMG), and Target (TGT) were open. I could almost hear the rent and interest payments ticking on.

And economically, it has.

Let’s do some raw, back-of-the-envelop calculations. Congress has just passed the largest stimulus package in history, some $2 trillion. If Morgan Stanley is right and the US is about to lose 30% of its economic growth on an annualized basis, that means the GDP is about to drop from $21.4 trillion to $19.8 trillion. Get two quarters like this and we fall back to $18.2 trillion, or to the 2016 levels.

That means the government is already $1.2 trillion behind the curve in bridge spending to carry over the economy to the other side of the epidemic. It can come back with another rescue package. If it does, there is no guarantee the money will end up in the right place to have any real effect.

Yes, we have just lost three years of economic growth, and the stock market is reflecting the same.

Of course, there are silver linings behind the clouds. Some 90% of the demand in the economy hasn’t been destroyed, it has been deferred. Cruises not taken, restaurant meals not eaten, and vacations not taken are gone for good.

However, a lot of discretionary purchases, such as for home, car, and computer purchases have simply been delayed until the fall. That's why so many forecasts call for an exploding economy in the second half.

A lot more economic economy isn’t lost, it has simply been rearranged. There has been a vast migration of legacy businesses to online. Most workers in Silicon Valley have adjusted from one to two days of work at home to five or six. The background noise of kids crying, and pets barking during an online meeting has become a normal part of business life.

And let’s face it, a lot of people are being paid for doing nothing. Government employees are receiving paychecks even though their agencies have been closed. Teachers are paid in annual contracts. Those Social Security and pension payments keep coming like clockwork.

I have spent the last week talking to old friends in the scientific community. Realistically, the economy will be shut down until June. You can open it up earlier, but only at the cost of hundreds of thousands of lives. Without restrictions, mathematically, everyone in the United States will be infected with Coronavirus within two months causing 6 million deaths. That’s the worst-case scenario.

Only when the infection rate hits 53% do we start to acquire herd immunity. That happens when there’s greater than 50% chance that the next person the virus contacts is immune.

Also, the greater the number of recovered individuals, the more we can tap for serum to treat existing patients and increase immunity and survival rates. Some 98% of those infected recover and become immune and non-contagious within two weeks.

Shelter-in-place orders and social distancing will greatly reduce those numbers. That’s what China did, and they have had no growth in new cases for two weeks.

My bet is that the epidemic will peak first in the states that sheltered-in-place early, and then peak in the Midwest later. That sets up two big waves of the disease, one in the spring, and a second in the summer and fall. Every state will have its own New York crisis moment sooner or later.

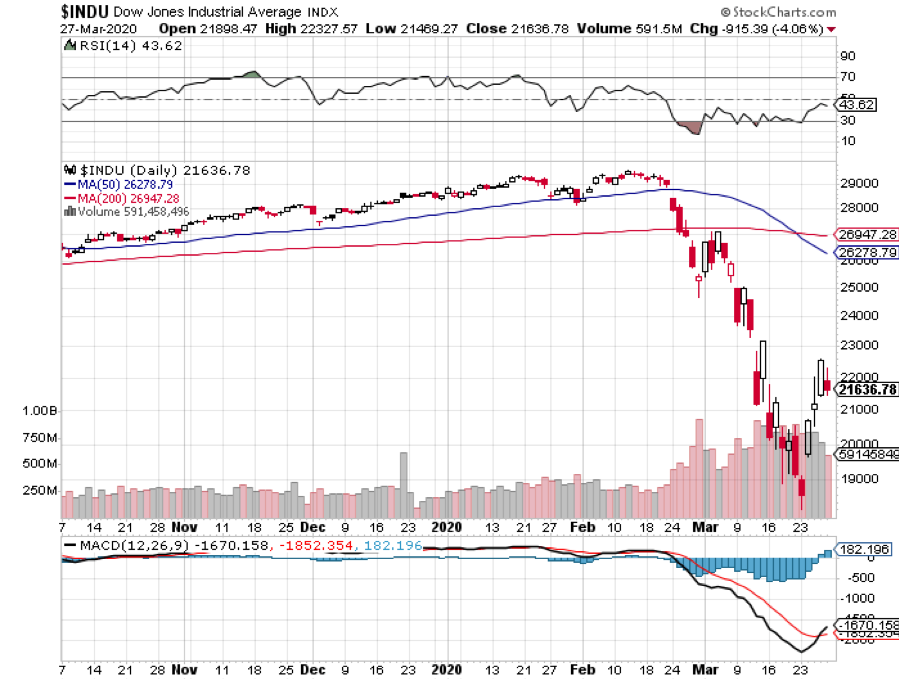

The president has expressed an interest in reopening the economy on April 13. If the stock market (INDU) believes that, then it is in for new lows. There is no point in predicting a final bottom. Once the algorithms get going, they are unstoppable.

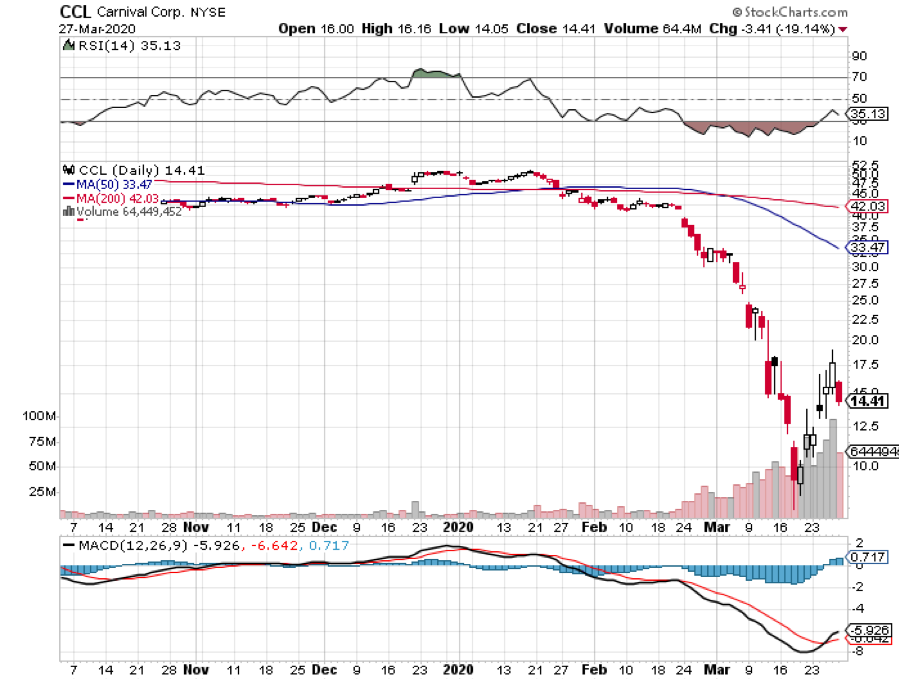

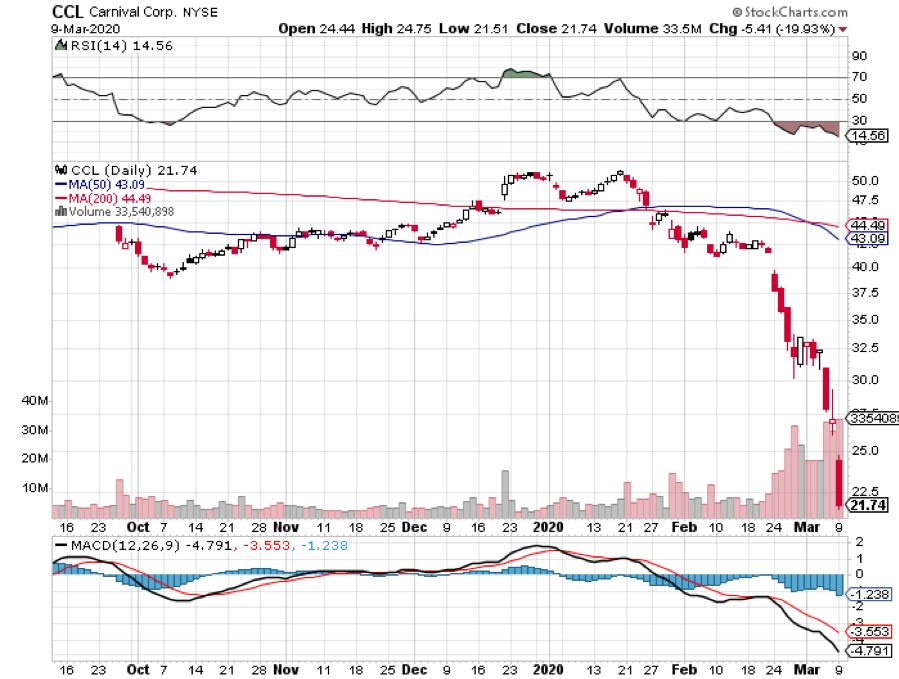

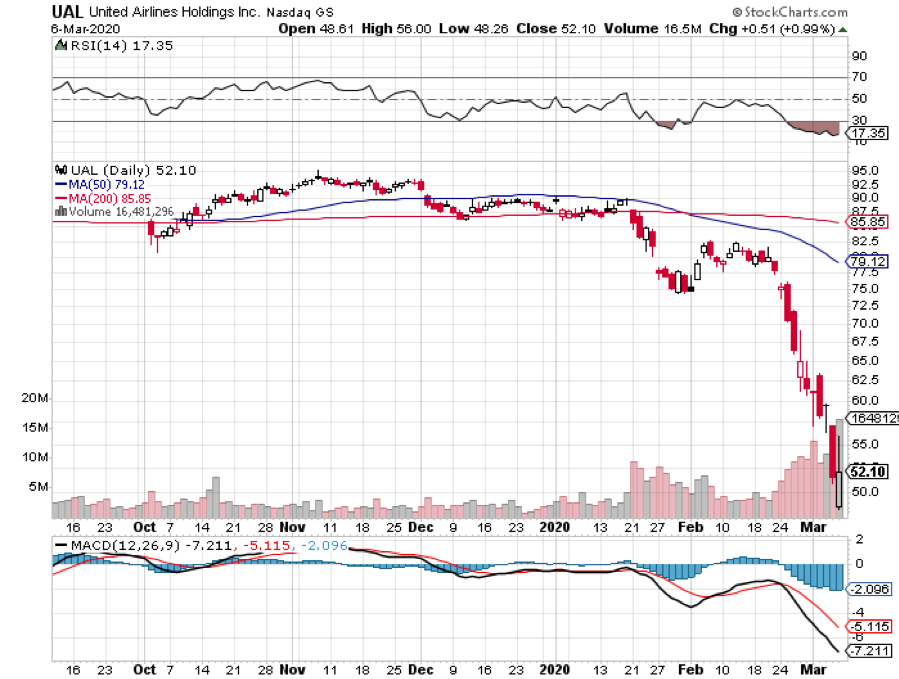

Big companies like United Airlines, Wynn Resorts (WYNN), and Carnival Cruise Lines (CCL), have seen a staggering 90% decline in sales. Yet the wage bills and interest payments mount daily. The cruel math points to disaster on an epic scale.

Face reality. There is no way the stock market can bottom before the number of cases peaks. Front run that at your peril. The consolation is that will likely happen by June. This will be the shortest, sharpest depression in history.

Global Corona cases topped 704,095, and deaths 33,509 (click here for the latest data). Why does the US have 52% more cases than China with one quarter the population? Because the federal government was asleep at the switch and then responded with a test that didn’t work for the first month. That blinded us to an epidemic that was already here in force.

A monster 3.28 million in Weekly Jobless Claims hit the market last week, five times the previous record. That’s normally the total number of jobs you lose in a full recession. This is the number of claims you get from an entire recession.

The number was probably higher as many state websites crashed, limiting applications. This rate of claims will probably increase for two more months. One can only guess what the unemployment rate is, probably over 5%. Next week will be worse. Over 50 million work in retail and most will lose their jobs.

Chicago clearing firm Ronin Capital went under, unable to meet their capital requirements. It was one of the CME’s principal clearings firm, and their problems are stemming from the (VIX) spike to $80 this week. I knew it was totally artificial.

The forced liquidation of their massive holdings probably accounted for the incredible 25-point drop in the (VIX) on Thursday and the last 500 points of the fall in Dow Average on Friday. It sounds terrible, but the loss of several brokerage firms like this often markets a market bottom. This is the second time in two years that (VIX)-related blow-ups roiled the markets. For more about the firm, visit https://www.ronin-capital.com

Internet traffic is up 30% on the week as a massive move to online commerce takes place. There is now a laptop shortage as the government outbids the private sector to get machines for first responders. Phishing attacks are at record highs. Don’t click on any links sent to you, especially from Apple, your credit card company, or the IRS.

The Fed expects a 30% Unemployment Rate in Q2, or so says James Bullard, president of the Federal Reserve Bank of St. Louis. The Great Depression only hit 25% unemployment.

The US Real Estate market is freezing up. If you’re trying to sell a house right now, you’re screwed. Closings are impossible because of the shutdown of notaries and title offices. Open houses are now virtual only. The hit to the US economy will be huge.

Tokyo 2020 Olympics were postponed a year, as the Japanese finally cave to the obvious. Canada and Australia had already withdrawn for Corona reasons. Tokyo is really unluckily with Olympics. They lost the 1940 games to the outbreak of WWII. It will be a big hit for the Japanese economy.

Online Hiring is exploding, up 44% in the past week, a decades-old trend that is now vastly accelerating. Entire school systems have moved online. We are all working now on Zoom, Skype, GoToMeeting, and Google Hangouts. Internet traffic has doubled in some neighborhoods, slowing speeds appreciably.

Target saw a staggering 50% growth in same store sales. Lines go around the block, hours are limited, and the police are on standby to maintain order. This has been one of our favorite retailers for years (click here for “Is Target the Next FANG?”). If they only had more toilet paper! Buy (TGT) on the meltdown.

Blackrock rated US stocks a “Strong Overweight.” The firm believes we won’t see a repeat of 2008. The fiscal and monetary response has been overwhelming. It’s just a matter of time before markets settle down, but not until well after new Corona cases peak. Buy (BLK) on the dip.

Oil falls again, back to $21. Not even all the stimulus in the world can save this structurally impaired industry. Ask John Hamm of Continental Resources (CLR), whose stock has just crashed from $36 to $4. He’s the guy who wrote the billion-dollar divorce check. Avoid the entire industry on pain of death.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates at zero, oil at $20 a barrel, and many stocks down by three quarters, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade.

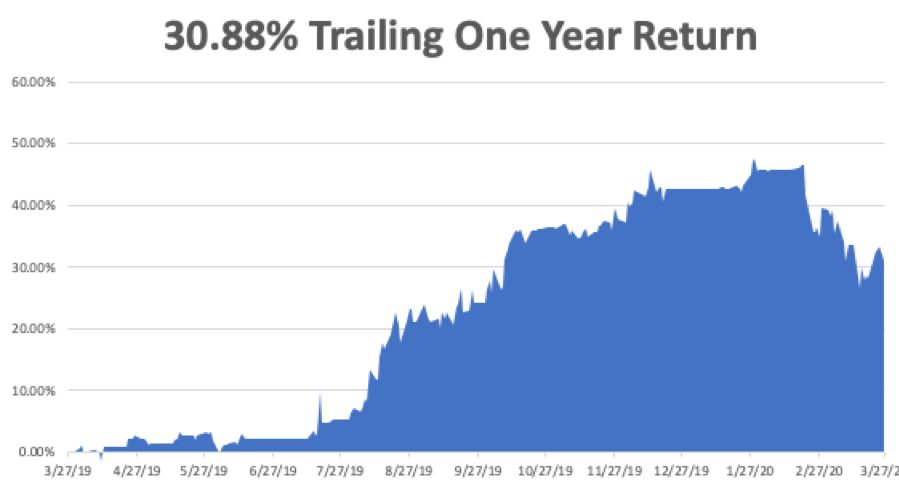

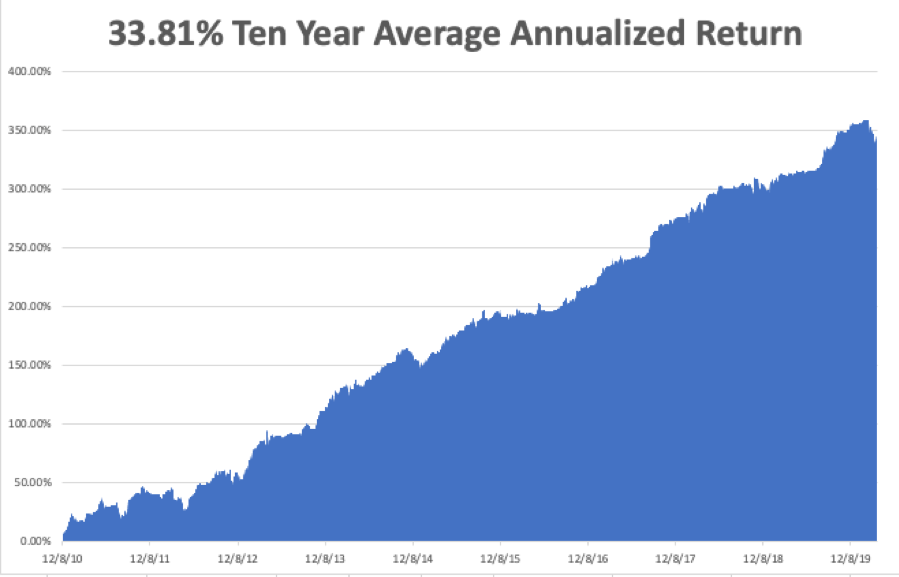

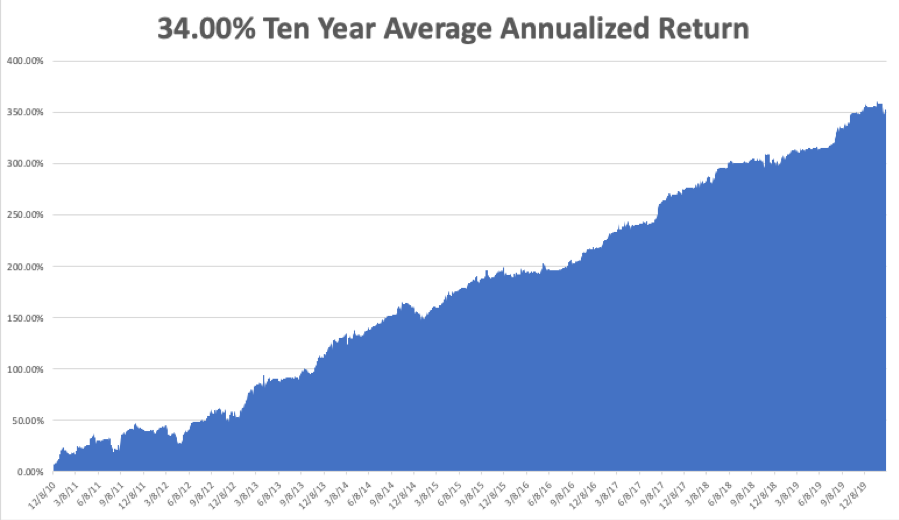

My Global Trading Dispatch performance has had a descent week, pulling back by -8.22% in March, taking my 2020 YTD return down to -11.14%. That compares to an incredible loss for the Dow Average of -37% at the Monday low. My trailing one-year return was pared back to 30.88%. My ten-year average annualized profit recovered to +33.81%.

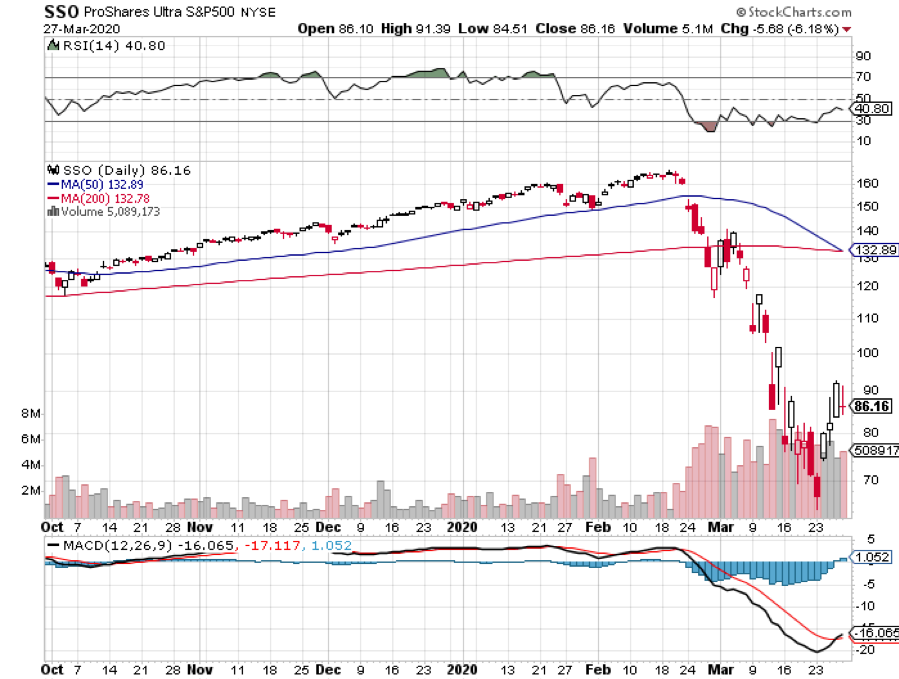

My short volatility positions have held steady. I used the 3,600-point rally in the Dow Average to add enough short positions to hedge out my risk in my exiting short volatility positions (VXX). Now we have time decay working in our big time favor. These will all come good well before their ten month expiration.

At the slightest sign of a break in the pandemic, the economy and shares should come roaring back. Right now, I have a 60% cash position.

This is jobs week and it should be the most tumultuous in history.

On Monday, March 30 at 9:00 AM, the Pending Home Sales for February are released.

On Tuesday, March 31 at 8:00 AM, the S&P Case Shiller National Home Price Index for January is out and should still show a sharp upward trend.

On Wednesday, April 1, at 8:15 AM, the ADP Private Sector Jobs Index is announced.

On Thursday, April 2 at 7:30 AM, Weekly Jobless Claims are announced. The number could top 3,000,000 again.

On Friday, April 3 at 9:00 AM, the March Nonfarm Payroll is printed. The Baker Hughes Rig Count follows at 2:00 PM. Expect these figures to crash as well.

As for me, I am at Lake Tahoe to hide out from the Zombie Apocalypse with my stockpile of Chloroquine and Azithromycin. There are only 536 cases in Nevada, most of which are in Las Vegas, and has a lot more food (click here for the latest updates).

I am building a Corona-sanitizing Station at the front door made of paper towels and isopropyl or ethyl alcohol. It kills the virus on contact.

I hear they even have toilet paper in a few undisclosed places.

Shelter in place will work. Please stay healthy.

As a public service, I am posting “the entire DNA sequence of Covid-19” in its entirety, which I obtained from a lab in China. A scientist friend asked me to publicize it on my website to the widest possible audience. What better place than the Mad Hedge Fund Trader.

Typical of viruses, it is an incredible small genome, one hundred thousandth the size of our own with only 29,000 base pairs. There are only a handful of genes here compared to our 35,000. For the full code click here.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

March 16, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE PANIC IS ON),

(INDU), (SPX), (VIX), (VXX), (GLD), (USO), (TLT), (AAPL), (WYNN), (CCL), (UAL)

I just drove from Carmel, California to San Francisco on scenic Highway 1. I was virtually the only one on the road.

The parking lot at Sam’s Chowder House was empty for the first time in its history. The Pie Ranch had a big sign in front saying “Shut”. The Roadhouse saw lights out. It was like the end of the world.

The panic is on.

The economy has ground to a juddering halt. Most US schools are closed, sports activities banned, and travel of any kind cancelled. All ski resorts in the US are shut down as are all restaurants, bars, and clubs in California. Virtually all public events of any kind have been barred for the next two months. Apple (AAPL) and Nike (NIKE) have closed all their US stores.

The moment I returned from my trip, I learned that the Federal Reserve has cut interest rates by a mind-boggling 1.00% on the heels of last week’s 0.50% haircut. This is unprecedented in history. S&P Futures responded immediately by going limit down for the third time in a week.

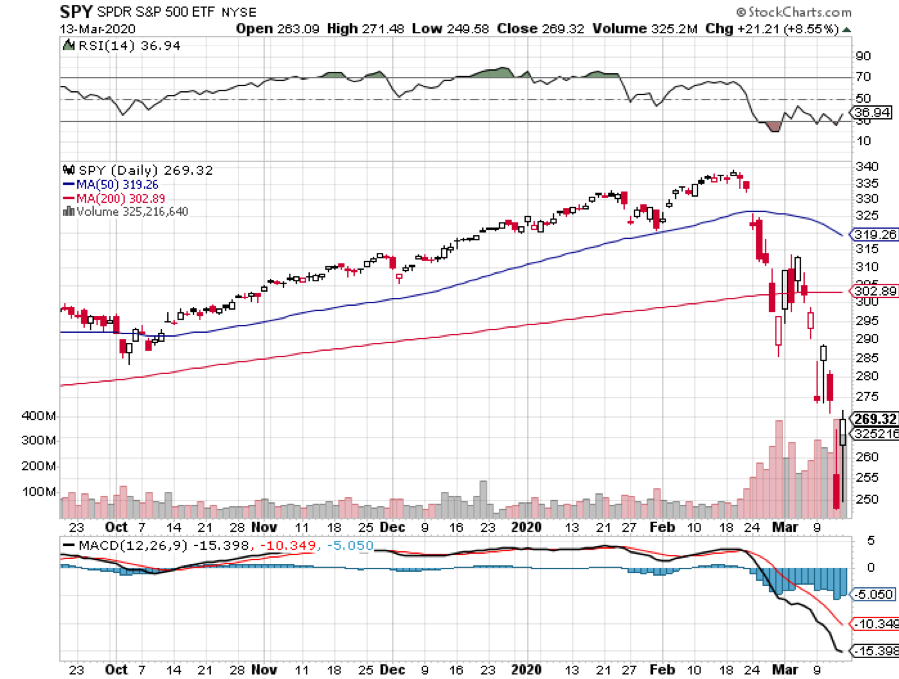

The most pessimistic worst-case scenario I outlined a week ago came true in days. The (SPX) is now trading at 2,500. Goldman Sachs just put out a downside target at 2,000, off 41% in three weeks.

That takes the market multiple down from 20X three weeks ago to 14X, and the 2020 earnings forecast to crater from $165 to $143. These are numbers considered unimaginable only a week ago.

You can blame it all on the Coronavirus. Global cases shot above 160,000 yesterday, while deaths exceeded 5,800. In the US, we are above 3,000 cases with 60 deaths. The pandemic is growing by at least 10% a day. All international borders are effectively closed.

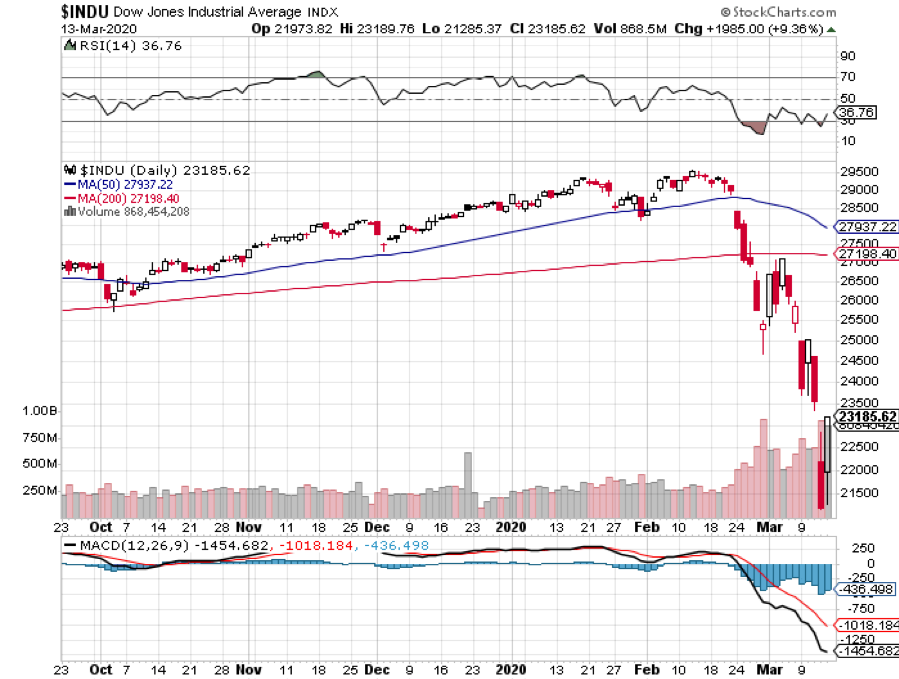

The stock market has effectively impeached Donald Trump, unwinding all stock market gains since his election. At the Thursday lows, the Dow Average ticked below 20,000, less than when he was elected. Economic growth may be about to do the same, wiping out the 7% in economic growth that has taken place during the same time.

Leadership from the top has gone missing in action. The president has told us that the pandemic “amounts to nothing”, is “no big deal”, and a Democratic “hoax.” There is no Fed effort to build a website to operate as a central clearing house for Corona information. In the meantime, the number of American deaths has been doubling every three days.

There have only been 13,500 tests completed in the US so far and they are completely unavailable in my area. The bold action to stem the virus has come from governors of the states of all political parties.

The good news is that all this extreme action will work. If you shut down the economy growth, the virus will do the same. In two weeks, all carriers will become obvious. Then you simply quarantine them. Any dilution of the self-quarantine strategy simply stitches out the process and the market decline.

The hope now is that the recession, which we certainly are now in, will be sharp but short. “An ounce of prevention is worth a pound of cure” is certainly in control now.

When we come out the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates at zero, oil at $25 a barrel, and many stocks down by half, there will be no reason not to.

Oil (USO) crashed, taking Texas tea down an incredible $22 overnight. OPEC collapsed as Saudi Arabia took on Russia in a price war, flooding the market. All American fracking companies with substantial debt have just been rendered worthless. I told you to stay away from MLPs! It’s amazing to see how the effect of one million new electric cars can have on the oil market. Blame it all on Elon Musk.

The oil crash is all about the US. American fracking has added 4 million barrels a day of supply over the last five years and 8 million b/d during the last ten. Saudi Arabia and Russia would love to wipe out the entire US industry.

Even if they do, the private equity boys are lining up to buy assets at ten cents on the dollar and bring in a new generation of equity investors. The wells may not even stop pumping. How do you say “Creative Destruction” in Arabic and Russian? We do it better than anyone else.

Gold (GLD) soared above $1,700, on a massive flight to safety bid bringing the old $1,927 high within easy reach.

Bond yields (TLT) plunged to 0.31% as recession fears exploded. Looks like we are headed to 0% interest rates in this cycle. Corona cases top 4,000 in the US and fatalities are rising sharply. Malls, parking lots, and restaurants are all empty.

Trump triggered a market crash, with a totally nonsensical Corona plan. Banning foreigners from the US will NOT stop the epidemic but WILL cause an instant recession, which the stock market is now hurriedly discounting. This is an American virus now, not a foreign one or a Chinese one. The market has totally lost faith in the president, who did everything he could to duck responsibility. The US is short 100,000 ICU beds to deal with the coming surge in cases. No one has any test kits at the local level. We could already have 1 million cases and not know it.

The US could lose two million people, according to forecasts by some scientists. At 100 million cases with a 5% fatality rate, get you there in three months. That could cause this bear market to take a 50% hit. The US is now following the Italian model, doing too little too late, where bodies are piling up at hospitals faster than they can be buried.

Stocks are back to their January 2017 lows, down 1,000 (SPX) points and 9,500 Dow points (INDU) in three weeks. Yikes! Unfortunately, I lived long enough to see this. We’ve seen 14 consecutive days of 1,000-point moves. The speed of the decline is unprecedented in financial history.

The Recession is on. Look for a short, sharp recession of only two quarters. JP Morgan is calling for a 2% GDP loss in Q2 and a 3% hit in Q3. The good news is that the stock market has already almost fully discounted this. The only way to beat Corona is to close down the economy for weeks.

A two-week national holiday is being discussed, or the grounding of all US commercial aircraft. Warren Buffet has cancelled Berkshire Hathaway’s legendary annual meeting. All San Francisco schools are closed, events and meetings cancelled. The acceleration to the new online-only economy is happening at light speed.

Municipal bonds crashed, down ten points in three days to a one-year low. If you thought that you parked your money in a safe place, think again. Municipalities are seeing tax and fee incomes collapse in the face of the Coronavirus. Brokers are in panic dumping inventories to meet margin calls. There is truly no place to hide in this crisis but cash, which is ALWAYS the best hedge. I would start buying (MUB) around here.

Bitcoin collapsed 50% in two days, to an eye-popping $4,000. So much for the protective value of crypto currencies. I told you to stay away. No Fed help here.

My Global Trading Dispatch performance has gone through a meat grinder, pulling back by -10.36% in March, taking my 2020 YTD return down to -13.28%. That compares to an incredible loss for the Dow Average of -32% at the Friday low. My trailing one-year return was pared back to 35.31%. My ten-year average annualized profit shrank to +33.84%.

I have been fighting a battle for the ages on a daily basis to limit my losses. My goal here is to make it back big time when the market comes roaring back in the second half.

My short volatility positions have been hammering me. I shorted the (VXX) when the Volatility Index (VIX) was at $35. It then went to an unbelievable $76. I was saved by only trading in very long maturity, very deep out-of-the-money (VXX) put options where time value will maintain a lot of their value. These will all come good well before their one-year expiration.

I also took profits in four short position at the market lows in Apple (AAPL) and the three short positions in Corona-related stocks, (CCL), (WYNN), and (UAL), which cratered, picking up an 8% profit there.

At the slightest sign of a break in the pandemic, the economy and shares should come roaring back. As things stand, I can handle a 3,000 point in the Dow Average from here and still have all of my existing positions expire at their maximum profit point with the Friday options expiration.

On Monday, March 16 at 7:30 AM, the New York Empire State Manufacturing Index is out.

On Tuesday, March 17 at 5:00 AM, the Retail Sales for February is released.

On Wednesday, March 18, at 7:30 AM, the Housing Starts for February is printed.

On Thursday, March 19 at 8:30 AM, Weekly Jobless Claims are announced.

On Friday, March 20 at 9:00 AM, the February Existing Home Sales is published. The Baker Hughes Rig Count follows at 2:00 PM.

As for me, I went down to Carmel, California to hole up in a hotel near the most perfect beach in the state and do some serious writing. This is the city where beachfront homes go for $10 million and up, mostly owned by foreign investors and tech billionaires from San Francisco. Locals decamped from here ages ago because it became too expensive to live in.

This is also where my parents honeymooned in 1949, borrowing my grandfather’s 1947 Ford.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

March 11, 2020

Fiat Lux

Featured Trade:

(A NOTE ON ASSIGNED OPTIONS, OR OPTIONS CALLED AWAY),

(AAPL), (BA), (UAL), (CCL), (WYNN), (FB)

Global Market Comments

March 10, 2020

Fiat Lux

Featured Trade:

(RISK CONTROL FOR DUMMIES IN TODAY’S MARKET),

(SPY), (VIX), (VXX), (AAPL), (CCL), (UAL), (WYNN)

Today, we saw the largest point loss in market history, the first use of modern circuit breakers, and individual stocks down up to 40%. Ten-year US Treasury bond yields cratered to 0.39%. Virtually the entire energy and banking sectors vaporized.

What did I do? I did what I always do during major stock market crashes.

I took my Tesla out to get detailed. When I got home, I washed the dishes and did some laundry. And for good measure, I mowed the lawn, even though it is early March and it didn’t need it.

That’s because I was totally relaxed about how my portfolio would perform.

There is a method to my madness, although I understand that some new subscribers may need some convincing.

I always run hedged portfolio, with hedges within hedges within hedges, although many of you may not realize it. I run long calls and puts against short calls and puts, balance off “RISK ON” positions with “RISK OFF” ones, and always keep a sharp eye on multi-asset class exposures, options implied volatilities, and my own Mad Hedge Market Timing Index.

While all of this costs me some profits in rising markets, it provides a ton of protection in falling ones, especially the kind we are seeing now. So, while many hedge funds are blowing up and newsletters wiping out their readers, I am so relaxed that I could fall asleep at any minute.

Whenever I change my positions, the market makes a major move or reaches a key crossroads, I look to stress test my portfolio by inflicting various extreme scenarios upon it and analyzing the outcome.

This is second nature for most hedge fund managers. In fact, the larger ones will use top of the line mainframes powered by $100 million worth of in-house custom programming to produce a real-time snapshot of their thousands of positions in all imaginable scenarios at all times.

If you want to invest with these guys feel free to do so. They require a $10-$25 million initial slug of capital, a one-year lock-up, charge a fixed management fee of 2% and a performance bonus of 20% or more.

You have to show minimum liquid assets of $2 million and sign 50 pages of disclosure documents. If you have ever sued a previous manager, forget it. The door slams shut. And, oh yes, the best performing funds are closed and have a ten-year waiting list to get in. Unless you are a major pension fund, they don’t want to hear from you.

Individual investors are not so sophisticated, and it clearly shows in their performance, which usually mirrors the indexes less a large haircut. So, I am going to let you in on my own, vastly simplified, dumbed-down, seat of the pants, down and dirty style of risk management, scenario analysis, and stress testing that replicates 95% of the results of my vastly more expensive competitors.

There is no management fee, performance bonus, disclosure document, lock up, or upfront cash requirement. There’s just my token $3,000 a year subscription fee and that’s it. And I’m not choosy. I’ll take anyone whose credit card doesn’t get declined.

To make this even easier, you can perform your own analysis in the excel spreadsheet I post every day in the paid-up members section of Global Trading Dispatch. You can just download it and play around with it whenever you want, constructing your own best-case and worst-case scenarios. To make this easy, I have posted this spreadsheet on my website for you to download by clicking here. You have to be logged in to access and download the spreadsheet.

Since this is a “for dummies” explanation, I’ll keep this as simple as possible. No offense, we all started out as dummies, even me.

I’ll take Mad Hedge Model Trading Portfolio at the close of March 9, 2020, the date of a horrific 2,000 down day in the Dow Average. This was the day when margin clerks were running rampant, brokers were jumping out of windows, and talking heads were predicting the end of the world.

I projected my portfolio returns in three possible scenarios: (1) The market collapses an additional 5.3% by the March 20 option expiration, some 8 trading days away, (2) the S&P 500 (SPX) rises 10% by March 20, and (3) the S&P 500 trades in a narrow range and remains around the then-current level of $2,746.

Scenario 1 – The S&P 500 Falls Another 5.3% to the 2018 Low

A 5.3% loss would take the (SPX) down to $2,600, to the 2018 low, and off an astonishing 800 points, or 23.5% down from the recent peak in a mere three weeks. In that situation the Volatility Index (VIX) would rise maybe to $60, the (VXX) would add another point, but all of our four short positions (AAPL), (UAL), (CCL), and (WYNN) would expire at maximum profit points.

In that case, March will end up down -3.58%, and my 2020 year-to-date performance would decline to -6.60%, a pittance really compared to a 23.5% plunge in the Dow Average. Most people would take that all day long. We live to buy another day. Better yet, we live to buy long term LEAPs at a three-year market low with my Mad Hedge Market Timing Index at only 3, a historic low.

Also, when the market eventually settles down, volatility will collapse, and the value of my (VXX) positions double.

Scenario 2 – S&P 500 rises 10%

The impact of a 10% rise in the market is easy to calculate. All my short positions expire at their maximum profit point because they are all so far in the money, some 20%-40%. It would be a monster home run. I would go back in the green on the (VXX) because of time decay. That would recover my March performance to +1.50% and my year-to-date to only -1.42%

Scenario 3 – S&P 500 Remains Unchanged

Again, we do great, given the circumstances. All the shorts expire at max profits and we see a smaller increase in the value of the (VXX). I’ll take that all day long, even though it cost me money. When running hedge funds, you are judged on how you manage your losses, not your gains, which are easy.

Keep in mind that these are only estimates, not guarantees, nor are they set in stone. Future levels of securities, like index ETFs, are easy to estimate. For other positions, it is more of an educated guess. This analysis is only as good as its assumptions. As we used to say in the computer world, garbage in equals garbage out.

Professionals who may want to take this out a few iterations can make further assumptions about market volatility, options implied volatility or the future course of interest rates. And let’s face it, politics is a major influence this year. Thanks Joe Biden for that one day 1,000 point rally to sell into, when I established most of my shorts and dumped a few longs.

Keep the number of positions small to keep your workload under control. Imagine being Goldman Sachs and doing this for several thousand positions a day across all asset classes.

Once you get the hang of this, you can start projecting the effect on your portfolio of all kinds of outlying events. What if a major world leader is assassinated? Piece of cake. How about another 9/11? No problem. Oil at $10 a barrel? That’s a gimme.

What if there is an American attack on Iranian nuclear facilities to distract us from the Coronavirus and stock market carnage? That might take you all two minutes to figure out. The Federal Reserve launches a surprise QE5 out of the blue? I think you already know the answer.

Now that you know how to make money in the options market, thanks to my Trade Alert service, I am going to teach you how to hang on to it.

There is no point in being clever and executing profitable trades only to lose your profits through some simple, careless mistakes.

The first goal of risk control is to preserve whatever capital you have. I tell people that I am too old to lose all my money and start over again as a junior trader at Morgan Stanley. Therefore, I am pretty careful when it comes to risk control.

The other goal of risk control is the art of managing your portfolio to make sure it is profitable no matter what happens in the marketplace. Ideally, you want to be a winner whether the market moves up, down, or sideways. I do this on a regular basis.

Remember, we are not trying to beat an index here. Our goal is to make absolute returns, or real dollars, at all times, no matter what the market does. You can’t eat relative performance, nor can you use it to pay your bills.

So the second goal of every portfolio manager is to make it bomb-proof. You never know when a flock of black swans is going to come out of nowhere or another geopolitical shock occurs causing the market crash.

Global Market Comments

March 9, 2020

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or SEARCHING FOR A BOTTOM),

(SPX), (VIX), (VXX), (CCL), (UAL), (WYNN)

OK, I’ll give it to you straight.

If the American Coronavirus epidemic stabilizes at current levels of infection, the double bottom in the S&P 500 (SPX) at 2,850 will hold, down 16% from the all-time high two weeks ago.

If it gets worse, it won’t, possibly taking the index down another 8.8% to 2,600, the 2018 low. Not only have we lost the 2019 stock market performance, we may be about to lose 2018 as well.

Of course, the problem is testing kits, which the government has utterly failed to provide in adequate numbers. The president is relying on disease figures provided by Fox News and ignoring those of his own experts at the CDC. And the president told us that the governor of Washington state, the site of the first US Corona hot spot, is a “snake,” and that the outbreak on the Diamond Princess is not his fault.

It’s not the kind of leadership the stock market is looking for at the moment. It amounts to an economic and biological “Pearl Harbor” where the government slept while the disease ran rampant. Until we get the true figures, markets will assume the worst. The real number of untested cases could be in the hundreds of thousands or millions, not the 350 reported. And stock prices will react accordingly.

There is an interesting experiment going on at the Grand Princess 100 miles off the coast of San Francisco right now which will certainly affect your health. Of the 39 showing Corona symptoms, 21 were found to have the disease and 19 of these were crew.

That means ALL of the passengers who took the last ten cruises were exposed, about 30,000 people, 90% of whom are back ashore. The Grand Princess may turn out to be the “Typhoid Mary” of our age.

You can see these fears expressed in the volatility index, which hit a decade high on Friday at $55, although it closed at $42. We live in a world now were all economic data is useless, earnings forecasts are wildly out of date, and technical analysis is ephemeral at best. Airlines, restaurants, and public events are emptying out everywhere and the deleterious effects on the economy will be extreme.

That is kind of hard to trade.

The good news is that this won’t last more than a couple of months. By June, the epidemic will be fading, or we’ll all be dead. All of the buying you see now is of the “look through” kind where investors are picking up once in a decade bargains in the highest quality companies in expectation of ballistic moves upward out the other side of the epidemic.

Enormous fortunes will be made, but at the cost of a few sleepless nights over the next few weeks. The bear market will end when everyone who needs tests get them and we obtain the results.

The Fed cut interest rates by 50 basis points taking the overnight rate down to 1.25%. They may cut again in two weeks. Traders were looking for some kind of global stimulus to head off a global recession. Markets are in “show me” mode and were down 300 prior to the announcement.

Quantitative Easing has become the cure for all problems. So, if it doesn’t work, try, try again? The Fed has now used up all its dry powder levitating the stocks, with the market already at a 1.00% yield for ten-year money. We need a vaccine, not a rate cut. New York schools close on virus fears.

The Beige Book says Corona is a worry, in their minutes from the last Fed meeting six weeks ago, mentioning it 48 times in yesterday’s report. No kidding? Travel and leisure are the hardest hit, and international trade is in free fall. The presidential election is also arising as a risk to the economy. Worst of all, the new James Bond movie has been postponed until November. The report only applies to data collected before February 24.

The next recession just got longer and deeper, as the Fed gives away the last of its dry powder. It’s the first time the central bank was used to fight a virus. It only creates more short selling and volatility opportunities for me down the line. Thanks Jay!

Gold ETF assets hit all-time high, both through capital appreciation and massive customer inflows. Fund values have exceeded the 2012 high, when gold futures reached $1,927. They saw 84 metric tonnes added to inventory in February. The barbarous relic is a great place to hide out for the virus. I expect a new all-time high this year and a possible run to $3,000.

Biotech & healthcare are back! Bernie’s thrashing last week in ten states takes nationalization of health care off the table for good. Biden should sweep most of the remaining states. There’s nothing left for Bernie but Michigan and Florida. Buy Health Care and Biotech on the dip!

The Nonfarm Payroll was up 273,000 in February, much higher than expectations. At least we HAD a good economy. The headline unemployment rate was 3.5%%. As if anyone cares. The only number right now that counts is new Corona infections. This may be the last good report for a while, possibly for years.

Private Payrolls were up 183,000, says the February ADP Report. No Corona virus here. Do you think companies believe this is a short-term ephemeral thing? What if they gave a pandemic and nobody came?

Mortgage Applications were up 26%, week on week, as free money keeps the housing market on fire. Don’t expect too much from the banks though. Mine offered a jumbo loan at 3.6%. Banks are not lining up to sell at the bottom.

The OPEC Meeting was desperate to stabilize prices and they failed utterly. But if they fail to deliver at least 1 million barrels a day in production slowdowns at their Friday Vienna meeting, Texas tea could reach the $30 a barrel handle in days.

The airline industry will lose $113 billion from the virus, says IATA, the International Air Transport Association. All events everywhere have been cancelled, even my Boy Scout awards dinner for Sunday night and my flight to a wedding in April. Lufthansa just cancelled half of all it flights worldwide. Who knows where the bottom is for this industry? I bet you didn’t know that airline ticket sales account for 8% of all credit card purchases. Keeping my short in United Airlines (UAL).

My Global Trading Dispatch performance took a shellacking, pulling back by -4.41% in March, taking my 2020 YTD return down to -7.33%. That compares to a return for the Dow Average of -16% at the Friday low. My trailing one-year return is stable at 48.44%. My ten-year average annualized profit ground back up to +34.00%.

I took my hit of the year on Friday, losing 4.4% on my bond short. A 9-point gap move has never happened in the long history of the bond market. Fortunately, my losses were mitigated by a five-point dip I was able to use to get out, a hedge within my bond position, and three short positions in Corona related-stocks, (CCL), (WYNN), and (UAL), which cratered.

All eyes will be focused on the Coronavirus still, with deaths over 3,000. The weekly economic data are virtually irrelevant now. This is usually the weakest week of the month on the data front.

On Monday, March 9 at 10:00 AM, the Consumer Inflation Expectations is out.

On Tuesday, March 10 at 5:00 AM, the NFIB Business Optimism Index is released.

On Wednesday, March 11, at 7:30 AM, the Core Inflation Rate for February is printed.

On Thursday, March 12 at 8:30 AM, Initial Jobless Claims are announced. Core Producer Price Index for February is also out.

On Friday, March 13 at 9:00 AM, the University of Michigan Consumer Sentiment Index is published. The Baker Hughes Rig Count follows at 2:00 PM.

As for me, I’ll be shopping for a cruise this summer. I am getting offered incredible deals on cruises all over the world. Suddenly, every cruise line in the world is having sales of the century.

Shall it be a Panama Canal cruise for $99, a trip around the Persian Gulf for $199, or a voyage retracing the route of the HMS Bounty across the Pacific for $299. Of course, the downside is that I may be subject to a two-week quarantine on a plague ship on my return.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

![]()

Global Market Comments

February 28, 2020

Fiat Lux

Featured Trade:

(FEBRUARY 26 BIWEEKLY STRATEGY WEBINAR Q&A),

(VIX), (VXX), (SPY), (TLT), (UAL), (DIS), (AAPL), (AMZN), (USO), (XLE), (KOL), (NVDA), (MU), (AMD), (QQQ), (MSFT), (INDU)