Mad Hedge Technology Letter

April 29, 2019

Fiat Lux

Featured Trade:

(A TESLA ENTRY POINT IS FINALLY OPENING UP)

(TSLA), (LYFT), (UBER)

Mad Hedge Technology Letter

April 29, 2019

Fiat Lux

Featured Trade:

(A TESLA ENTRY POINT IS FINALLY OPENING UP)

(TSLA), (LYFT), (UBER)

CEO of Tesla Elon Musk touting his company’s ability to deploy robo-taxis in the next 12 months miffed many industry analysts.

Few tech CEOs would have the balls to get on stage and put themselves out there in that type of manner.

But many tech CEOs aren’t Elon Musk.

I believe Musk calling for these bold predictions will help bend the world in his favor, maybe not right away, but before Tesla burns through their horde of cash.

Of course, there is no way in hell he could pull this off today, regulatory hurdles and in-house capability are two severe constraints.

But confidently proclaiming audacious initiatives that become self-fulfilling prophecies is a smart way to align the stars in the way you want.

Musk certainly believes the scent is in the air for the wolves to go in for the killer blow, he just needs a few miracles and a tad bit of luck on his side.

Tesla is now on record hyping up a custom-made robo-taxi capable of running about a million miles using a single battery pack, with all the sensors and computing power for full autonomy, costing less than $38,000 to produce.

They believe this will come out in 2020.

The combination of low vehicle cost, low maintenance cost and an expected powertrain efficiency of 4.5 miles per kWh should make this the lowest cost of ownership and will be the most profitable autonomous taxi on the market.

Using this state of the art robo-taxi to build a ride-sharing service business would effectively mean an Uber or Lyft without drivers.

Tesla would receive 30% of each fare, with the other 70% sent to Tesla owners that would deploy their own cars into the ride-sharing network.

I respect that Musk can feel sentiment behind Tesla's brand slipping away after heavy criticism, personal backlash from a spat with the SEC, and a boatload of competition hoping to smash him in the mouth.

Musk needed to shift the narrative into Tesla’s brand being the most innovative and publicly letting investors know there are more irons in the fire that will entrench Tesla supporters further while giving the Tesla haters more fodder to terrorize Musk.

Tesla is a luxury brand and constructed in the image of Elon Musk - making the impossible possible ethos needed a facelift and Musk gave what his supporters wanted in spades.

His showmanship is not misplaced and is part of who he is. But more importantly, if Tesla makes serious headway in the robo-taxi business in the next 12 months, Musk will be able to stand on the podium to whip up enough support needed to nudge this over the line.

Musk is very much from the mold of build it and they will come, and he has what few other CEOs have – vision.

The vision comes with a pricey premium.

And Musk must nurture this vision and urge believers to keep believing to carry on this act.

I was surprised that one of the most applicable pieces of news in the shareholder letter was something that nobody excavated.

Tesla will build a second-generation Model 3 line in China that projects to be at least 50% cheaper per unit of capacity than the Model 3-related lines in Fremont and at Gigafactory 1.

The cost to produce Model 3's is about to crash all while Tesla is still considered a premium, luxury vehicle.

This will free up space at the Reno Gigafactory and Fremont to focus on the robo-taxi challenge.

The latest news in Shanghai was an explosion at the half-built Gigafactory parking lot, but not much will come of that.

For investors on the sideline, the nadir of Tesla stock is approaching, another more shakeout might give investors the green light for a trade, that is if they aren’t already long-time holders.

Tesla mentioned they had trouble delivering new Teslas to foreign countries because of headwinds putting the logistics in place for the first time.

This one-off write-down will come off the balance sheet in next quarter’s earnings report and more information on the Shanghai Gigafactory will start to filter in aside from its boost to Tesla being able to produce 500,000 cars in 2019 once it comes online.

The Shanghai Gigafactory will unlock substantial value for shareholders once it's fully operational and finishing the construction ahead of time would be a boon.

Part of the plan to go into China results from snapping up more of a battery supply which Musk feels is the Achilles heel right now in Reno.

He continues to fault Panasonic for not delivering enough cells which, in turn, is holding back the power wall business creating a backlog in orders.

Many of the talking heads appearing on major networks were too trigger-happy in tearing Musk to shreds because of the way he speaks in hyperbole.

Musk even came out with another zinger that could pick up traction - an insurance product to marry up with Tesla vehicle purchases because Tesla believed Tesla owners are being price gouged by insurance companies.

As the impact of higher deliveries and cost reduction take full effect, Tesla expects to return to profitability in Q3 and significantly reduce losses in Q2.

Most of the bad news is baked into the stock and there could be another leg-down before this stock starts to look compelling.

Whether you love them or hate them, visionary tech CEOs get a lot of slack because the upside is so lucrative for shareholders.

That is part of why it is excruciating trading the stock led by a moody visionary with a larger-than-life persona, better to buy and hold if you are a Tesla believer.

Mad Hedge Technology Letter

April 17, 2019

Fiat Lux

Featured Trade:

(ALPHABET DOMINATES WITH GOOGLE MAPS)

(GOOGL), (AMZN), (YELP), (UBER)

Remember Google Maps?

Google will start monetizing it, let me tell you about it.

The web mapping service developed by Google gifting access to satellite imagery, aerial photography, street maps, 360° panoramic views of streets has been around since the beginning of this generation of big tech and is what I would consider legacy technology.

Legacy technology is often associated with failure as the out of date nature isn’t applicable to the tech scene and the commercialization of it today.

In a candid letter, Jeff Bezos wrote to shareholders that Amazon will “occasionally have multibillion-dollar failures.”

Silicon Valley tech will have its share of implosions stemming from ill-fated industry decisions correlating to heavy losses.

Google Maps won’t be one of these slip-ups.

However, a whole catalog of instances can be chronicled from Microsoft’s purchase of Nokia’s handset division to Google’s social media foray in Google Plus.

It hasn’t gone all pear-shaped for Alphabet in 2019. I strongly believe they are one of the companies of the year harnessing YouTube in ways consumers never imagined.

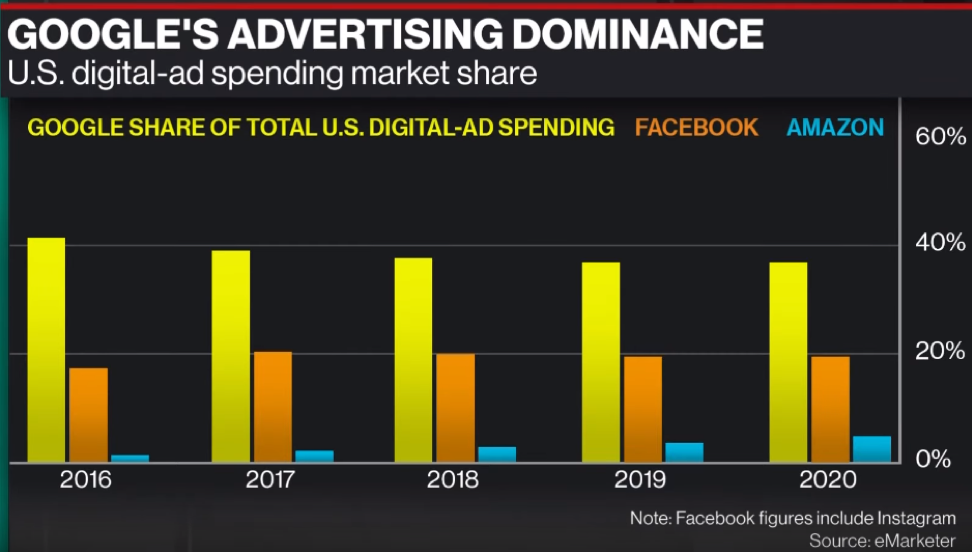

Adding color to the story, any remnant of apprehension to any bearish feelings about Alphabet should vanish once investors understand how lucrative Google Maps will become.

Google has spent decades and billions of capital honing the application and in terms of market share they have cultivated a monopoly.

Uber’s S-1 filing shined some light on Google Maps characterizing it as a must-have input into their business saying, “We do not believe that an alternative mapping solution exists that can provide the global functionality that we require to offer our platform in all of the markets in which we operate.”

Uber sunk $58 million integrating Google Maps into its services from 2016-2018 along with continuous payments to its Google Cloud arm to host Uber’s data.

The strong relationship with Uber shows how Alphabet is adept at milking 3rd party apps for what they are worth.

Alphabet’s stake in Uber is projected to be $5 billion from the $250 million investment in Uber in 2013.

The party doesn’t stop there with Uber paying Alphabet $631 million from 2016-2018 in digital marketing services and another $70 million for technology infrastructure.

To say that Google firmly has its tribal marks tattooed into Uber’s skin is an understatement.

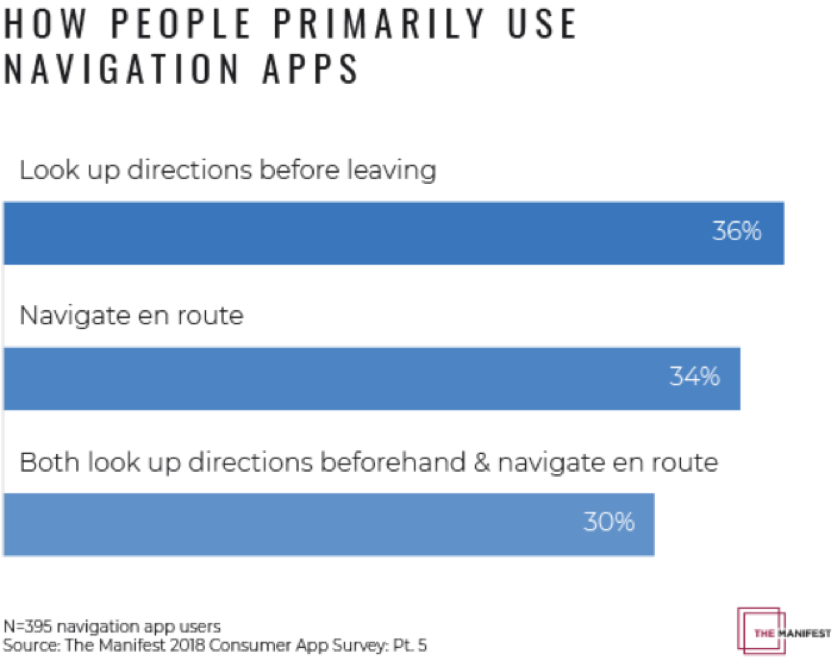

Almost 80% of smartphone users regularly use navigation apps.

Google Maps is the most popular navigation app by a country mile with 67% of market share.

One billion people consistently use Google Maps.

It is the go-to navigation app for nearly 6x more people compared to the runner up app Waze with 12% market share.

The superior performance of the app has allowed it to branch off into a Yelp-like hybrid app accumulating reviews of businesses and institutions that are conveniently dotted around its map.

Multi-functional terrain was integrated to make the maps more 3D and route navigation from point A to B routes has steadily improved since its inception.

The increasing detail showing even roofs of sheds and the Google street view offering a point of view vantage point boosting the reliability of the app.

The result of making the app better is that navigators can easily discern locations and follow routes clearly.

Most would concede that they use the app to look up specific street routes.

By implementing digital ads into the experience, product and service offers will possibly populate in real time as the user glances at the app’s directions.

A vast amount of services such from food to personal grooming to even cannabis club ads could be applicable and ad companies will pay top dollar to post on Google Maps.

Google could also offer personalized recommendations to users and collect an affiliate fee if the user clicks on an attached link transferring the customer to a 3rd party landing page.

They already benefit from this strategy on Google Flights.

Google might even be tempted to implement a Groupon model with group discounts on services positioned on Google Maps.

Google Maps is hands down the most underappreciated app and most under monetized tech asset in the world.

Another possible revenue generation avenue would be the advent of Google Maps voice ads en route to a destination that would promote a 5 or 10 second voice commercial of a businesses that the user is physically passing by.

The unintended effects of Google’s audacious transformation of their proprietary Map service spells doom for Yelp’s business model.

Google’s move into digital ads of maps effectively means that Yelp will be relegated to an inferior version of Google Maps without the map technology.

Google has accumulated enough personal data to draw up any type of profile for particularly Android users voraciously consuming data on Gmail, Google Maps, Google Search and Google Chrome.

These four data generators will allow Google to formulate a shadow profile based on individual tastes with daily use of these four Google properties.

Alphabet has a time-honored model of building assets that become utilities and once they monopolize the utility, they sprinkle the digital ad pixie-dust effectively monetizing the asset that was once free of charge.

They have followed the same road map for Gmail, Google Search, YouTube, and if Waymo can become a utility, prepare from Google digital ads inside the screens of Waymo autonomous cars.

When many sulked that this could be one of those billion-dollar failures that Bezos whined about, Google has decided to supercharge Google Maps by cross-pollinating the power of Google maps with its digital advertising knowhow.

This powerful cocktail of forces working in tandem will accelerate its revenue growth along with the resurgence of its YouTube digital ad revenue.

I believe this new lever of revenue growth isn’t priced into Alphabet shares yet, and withstanding any random black swan shocks to the broader economy, Alphabet is poised to outperform the rest of the trading year.

Short Yelp on any and every rally - Google has made their business model redundant.

Mad Hedge Technology Letter

April 16, 2019

Fiat Lux

Featured Trade:

(UBER’S DARK AND DIRTY SECRETS)

(UBER), (LYFT)

The granddaddy of IPOs awaits us – Uber has filed an S-1 with the SEC detailing plans to go public.

Uber can’t do this any sooner as they preside over a decelerating ride-share operation and its high margin Uber eats division, food delivery business, that has experienced slowing margins.

Once helmed by swashbuckling entrepreneur Travis Kalanick, Uber was infamous for its cultural problems that played out in real time in the media with sexual harassment accusations amongst other things.

They were castigated for its environment of testosterone overload that current CEO Dara Khosrowshahi has rooted out.

Khosrowshahi is pinning the blame on the past leadership in the S-1 filing explaining they are still fine-tuning these problems and its inherent risk could be detrimental to the growth model.

The Iranian-American CEO needs as many outs as he can find because Uber is a high-risk, high-reward model that has revealed no possible way to becoming profitable.

Sequentially, Uber’s core growth has stagnated with revenues last quarter of 2018 coming in at $2.314 billion, decelerating from $2.315 billion in the third quarter.

This is a sensitive spot for Uber because it correlates to 91% of its revenue.

Its Uber Eats division has also presided over two sequential quarters of deceleration indicating the low-hanging fruit has been picked.

The company is shifting towards higher volume, lower margin restaurants in more competitive locations hinting that the gangbuster years of high margin food delivery service growth is over.

The proposed $90 billion IPO also marks the high-water mark to the Silicon Valley IPO parade with only smaller fish from the sea debuting after them.

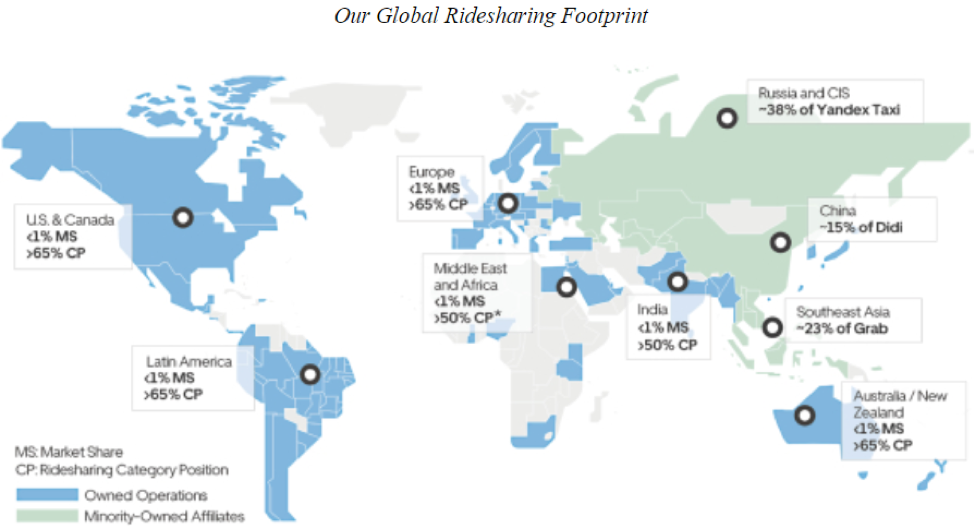

Uber has altered economic and consumer habits as we know it and the size of the business means it’s no Lyft (LYFT) – Uber is global, and its revenues are six times larger than its American competitor.

Becoming an enormous start-up also means heavier losses, the company had $3 billion in operating losses last year while its smaller competitor Lyft had only $911 million.

Lyft is solely focused on the ride-share industry capping upside potential while Uber has more gunpowder to load if it wants to ammo up in the business world.

One direction Uber hopes to explore is under the banner of Uber Freight which plans to monetize the deeply fragmented logistic industry.

It can take sometimes days for suppliers to deliver shipments with most of the process conducted over the phone or by fax.

Uber Freight mitigates logistical risks by providing an on-demand platform to automate and accelerate logistics transactions end-to-end.

The software smoothly connects carriers with the most appropriate shipments available, and offers carriers upfront, transparent pricing and the ability to book a shipment with the touch of a button.

As of the end of 2018, Uber Freight delivered $125 million in annual revenue and they hope to ameliorate many of the same logistical pain points that occur around the world.

This division of Uber is one that Lyft lacks, thus Uber should be granted a higher multiple when shares go public.

A huge addressable market awaits Uber Freight, but as many know, logistic routes have been formed over many years, and disruptors won’t be able to come in overnight and sign up new contracts.

Revenue should be slow but steady, and not the sugar high rush of revenue management is wishing for.

Uber’s heavy cash burning enterprise needs to offer some glimmer of hope of becoming profitable in the future whether it's five or twenty years out.

Without this x-factor of potential profitability, committed capital could become strained as investor will shy away knowing that a solid balance sheet might be a pie in the sky.

Since 2015, Uber has paid drivers $78.2 billion in renumeration - Uber will need to curtail heavy costs like these to raise operating margins.

One upside to its model is that its software platform possesses synergetic effects cutting costs for rolling out newer software for Uber Freight and Uber Eats.

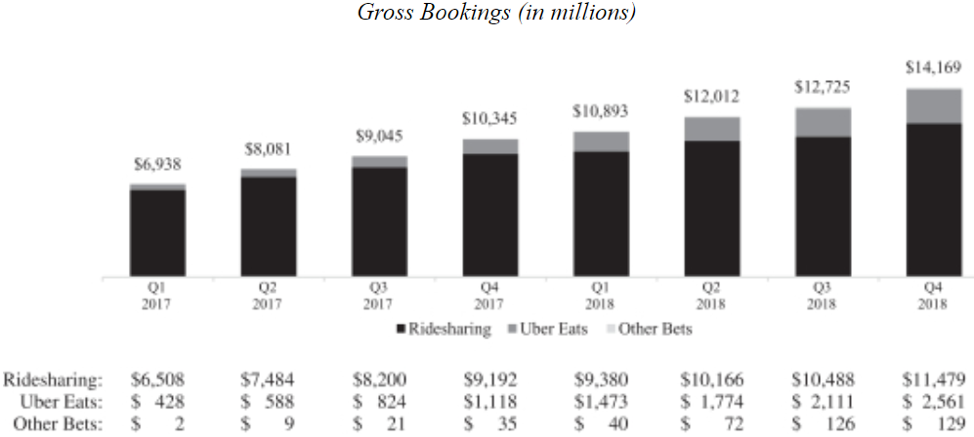

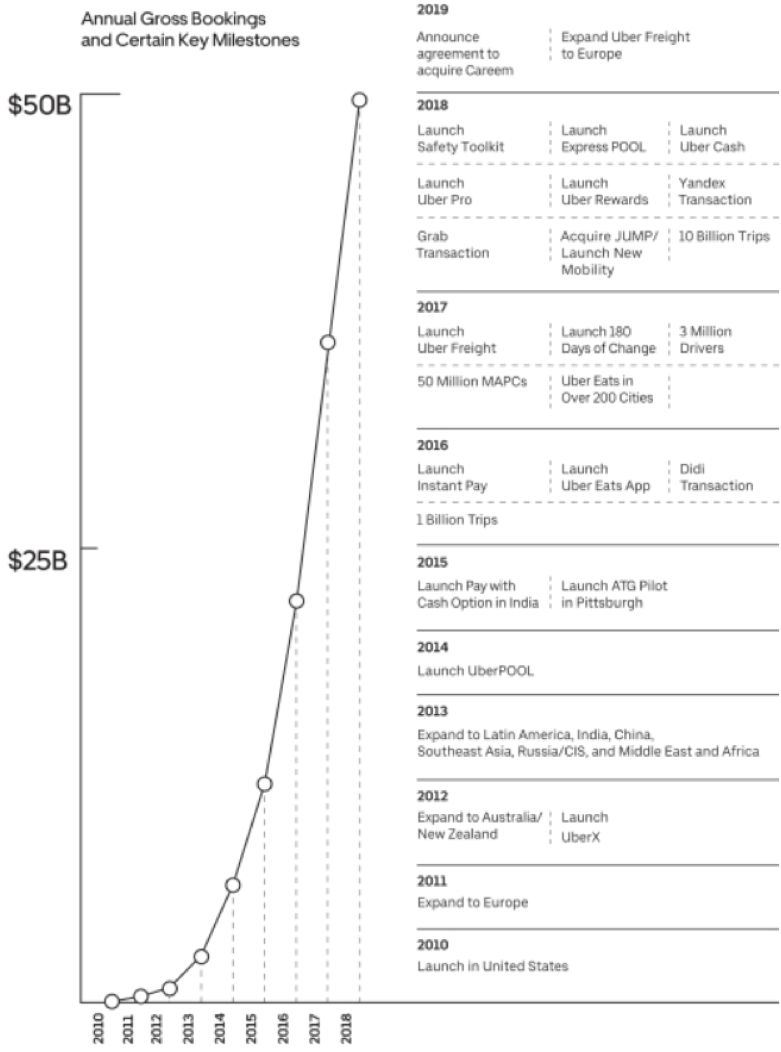

Uber is still growing, albeit at a slower rate, 2018 Gross Bookings grew to $49.8 billion, up 45% from $34.4 billion in 2017.

The growth contributed to revenues of $11.3 billion in 2018. While a mammoth number, Uber still needs to absorb capital hits from M&A when they acquired Careem, the Uber of Middle East, North Africa, and Pakistan, for $3.1 billion last year.

Uber clearly choreographed a future strategy in the S-1 filing saying, “Our strategy is to create the largest network in each market so that we can have the greatest liquidity network effect, which we believe leads to a margin advantage.”

Details of this strategy include more drivers, more riders, more rides per hour, lower fares, and smaller waiting times.

I believe Uber is biting off more than they can chew on this front.

To overcome the regulatory hurdles and the social backlash while offering cheaper fares and simultaneously increasing driver payout will be impossible unless drivers start shuttling around 5 or 6 people in one ride.

I do acknowledge that Uber has massive scale, first move advantage, and a handsome margin advantage working on their side.

But will this be enough if Uber adds more drivers and effectively piles more money into the same strategy?

I would say no and that could mean that growth rates could slip severely which leads me to suggest that Uber has a problem with the quality of growth.

On the bright side, the business model with be compensated by enhancements in the routing algorithms, payment technologies, in-car user experience, and user interface.

These incremental gains won’t help offset the relative weakness in the growth numbers that possess less and less quality in them.

The overarching theme of what to do when the low-hanging fruit is picked off the branch is a tough one, because any further incremental gain is negated by higher costs or competition.

Uber’s get out of jail free card is the eventual paradigm shift to aerial ride sharing, and if they are the leaders in that transition, it could offer another massive pay day and steeper growth trajectory that would propel the company into a realm of many more possibilities.

Whether Uber can complete this tectonic shift is too far away to predict, time could become a significant headwind in this case since mainstream adoption of autonomous driving has been relatively sluggish.

Expect heightened volatility as the main characteristics of Uber’s price action - it’s certain to be a bumpy ride.

Abstaining from Uber shares would be the smart play here while some more detective work can be deployed.

Mad Hedge Technology Letter

April 1, 2019

Fiat Lux

Featured Trade:

(THE NEXT TECH BUBBLE TOP HAS STARTED)

(LYFT), (PIN), (UBER), (AAPL), (JPM), (FB)

Don't go chasing rainbows.

That is what the current tech IPO environment is hinting.

Even though market conditions are frothy, that doesn't mean I'm calling a market top today, hardly so.

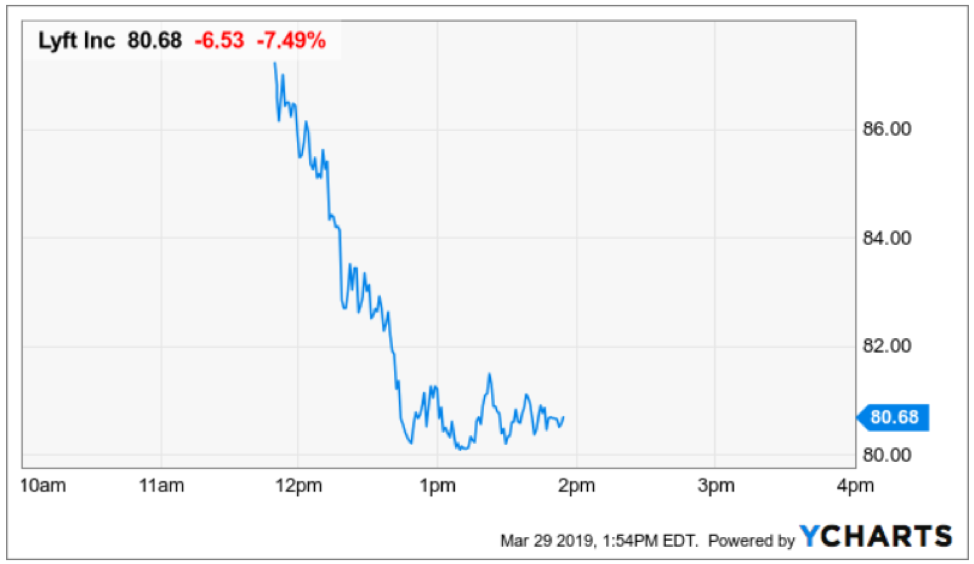

I predicted that Lyft (LYFT) would storm out of the gate like a bull on ecstasy, and I was vindicated when the stock flirted intraday with the $87 mark.

The scarcity value of these gig economy companies is hard to quantify.

Examples Uber unduly promise ambition and innovation leading to hopes of a possible air transport service and sharing network that I would need to see to believe.

The built-up expectations smell of over-promising and under-delivering, the majority won’t be able to deliver merely half of what their manifestos promulgate

As I put my analyst hat on, the 2019 IPO frenzy coming online has some of the same fingerprints of the infamous dot com bust of 2001.

The two main trends symbolic of the last time the tech industry disentangled were overly generous valuation, pricing in revenue expansion of 80% for the next five years when the leader of the pack Microsoft (MSFT) only grew at 50%.

A tantalizing clue was the utterly deficient cash flow generated back then.

The underlying premise revolved around putting the network effect on a pedestal irrespective of understanding that the network effect should have caused cash flow to accelerate which was conspicuously absent.

Losing money and losing a lot of it does lead to paralysis, examples were rife, for instance, priceline.com losing $30 on each air ticket sold.

Even more hard to fathom was that Priceline was stretching itself to the limits on the open market filling ticket orders because of a dearth of inventory steepening losses.

Priceline gushed about a unique business model of collecting excess ticket inventory that airlines couldn't sell at low cost and reskinning them to a digital audience hoping to take advantage of this price dispersion.

But in reality, this wasn’t always the case.

Priceline was on a suicide mission and expanding from 50 employees to 300 employees based upon misleading growth was madness.

In a nutshell, investors bypassed pragmatic arithmetic and were lifted by the fumes of exuberance that had manifested around the euphoria of the tech bubble.

Lyft is not revolutionary, they are a broker which occupy a low position in the spectrum of tech intellectual property.

Exploiting drivers, compensating them per hour, and letting them figure out their own cost structures for car insurance, fuel costs, and opportunity cost while offering zero benefits is a court battle waiting to happen in California.

And if your response was the way they craft value is by way of a proprietary app, well, Google, Apple, or even Netflix can produce the same type of app and quality of app in a few weeks with their legendary phalanx of top-tier engineering talent.

To Lyft’s credit, they have at least collected the treasure trove of data the app has compiled which is extraordinarily valuable.

The top of the tech bubble means that big tech is overreaching into any revenue they can get their hands on like a heroin addict yearning for the next syringe.

The environment has transformed into an eerily zero-sum game, such as Apple (AAPL) cooperating with JPMorgan Chase (JPM) to create Apple pay, and then instantly flipping around to compete with JPMorgan Chase in the credit card space with Apple Pay being an accomplice.

Big tech has sown the seeds of discord by quietly attempting to trample on any analog business they can get near.

Leveraging the network effect of billions of users in a proprietary walled garden to extract the incremental dollar for a new service is impossible to compete with for analog companies without a similar embedded on-demand audience.

Lyft co-founder and CEO Logan Green mentioned in an interview that in the next five year, he plans to deploy a subscription service coined as transportation-as-a-service like a software-as-a-service option which cloud platforms sell.

A fight to the bottom with Uber will cause major disruption in the pricing mechanisms of the subscription service and could force Lyft to earn less revenue per ride than the current pricing system.

Investors need to remember that Uber is bigger than Lyft and possessed more ammunition.

At the end of the day, the race to the bottom is never good for profitability or sustainability, and Lyft has yet to provide any substantial clues on how they will navigate through this quagmire.

My guess is that Lyft will have to do a deal with the devil of sorts to slang its branded broker app onto the cresting wave of Waymo as Waymo motors ahead and starts to materially monetize its self-driving program.

Remember that Alphabet already has a small stake in Lyft and these two could partner up with Alphabet dictating terms.

Lyft cannot compete with the holy grail of tech - self-driving technology – they are way down the tech value chain.

If we look at the bigger picture, the broader market has been riding the coattails of Federal Reserve Chairman Jerome Powell’s 180-degree turn from winter’s statement that interest rate tightening was on “autopilot.”

Now, there is only a 27% chance given by the market that the Fed will raise rates at all in 2019.

The market responded with strength begetting strength allowing the bull run to continue and even whispers of a possible rate cut later this year.

Sentiment will not change until we get to the point when earnings can’t surpass the expectation which have been lowered substantially.

I bet this won’t happen until late this year or next year.

This is inning 8 or 9 of the bull crusade, the closer is warming up in the bullpen.

Lyft’s opening day gallop is just one of the side effects from a market that is toppy.

Mad Hedge Technology Letter

March 20, 2019

Fiat Lux

Featured Trade:

(LYFT), (UBER), (GRUB), (POSTMATES), (DOORDASH), (GOOGL)

The imminent launch of the Lyft IPO is telling investors that the next era of technology is upon us.

Does that mean that you should go out and buy Lyft shares as soon as they hit the market?

Yes and no.

30 million shares are up for grabs and the price of the IPO appears to be pinpointed between $62 and $68.

Even though this company is a huge cash burning enterprise, the fact is that they have been catching up to industry leader Uber and snatching away market share from the incumbent.

It was only in January 2017 that Lyft had accumulated 27% of the domestic market share, and in the recent filing for the IPO, that number had exploded to 39%.

If Lyft can start to gnaw into Uber's lead even more, shares will be prime to rise beyond the likely $62 to $68 level.

Let's remember that one of the main reasons for Uber giving up ground in this 2-way race is because of the toxic work environment embroiling many of the upper management and the subsequent damage to its broad-based public image.

If you wanted the definition of a public relations disaster, Uber was the poster boy.

Story after story leaked detailing payment problems to Uber drivers, a huge data leak revealing millions of lost personal information, and even a crude video of the founder berating a driver went viral.

There might be no Cinderella ending for this ride-hailing operation as litigious time bombs stemming from an aggressive high-risk, high-reward strategy skirting local taxi laws have flaunted the feeling of corporate invincibility in the face of government.

Being the first of its kind to hit the market, I do believe the demand will outstrip the supply.

There is a scarcity value at play here that cannot be quantified.

And an initial pop from the low-to-mid $60 range to about $80 is a real possibility in the short-term.

However, expect any robust price action to be met with rip-roaring volatility, meaning there is a legitimate chance that shares will consolidate back to $50 before they head up to $100.

Some of my favorite picks have echoed this same price action with fintech juggernaut Square (SQ) and streaming platform Roku (ROKU) mimicking heart-stopping price action with 10% moves up or down on any given day.

This doesn't mean that these are bad companies, but they do become harder to trade when entry points and exit points become harder to navigate around because of the extreme beta attached to the package.

The big winner of this IPO is ultimately self-driving technology.

Let's not skirt around the issue - Lyft loses a lot of money and so does Uber and that needs to stop.

It has been customary for tech companies to go public in order for the initial venture capitalists to cash out so they can rotate capital into different appreciating assets.

When companies are on the verge of ex-growth, maintaining the same growth trajectory becomes almost impossible without even more incremental cash burn relative to sales.

This leads to an even more arduous pursuit of revenue acceleration with stopgap solutions calling for riskier strategies.

What this means for Lyft is that they will need to double down on their self-driving technology because they are incentivized to do so, otherwise face an existential crisis down the road.

The most exorbitant cost for Uber and Lyft is by far employing, servicing, and paying out the drivers that shuttle around passengers.

I cannot envision these companies becoming profitable unless they find a way to eliminate the human driver and automate the driving function.

I will say that Uber benefitting from the Uber Eats business has been a high margin bump to the top line.

Yet, food delivery is not the main engine that will spur on these IPO darlings.

This part of the business is getting more saturated with margins getting chopped down every day.

What food delivery mainstays like Doordash and GrubHub don't have, is the proprietary self-driving technology that at some point will be present in every vehicle in the United States and the world.

What we are seeing now is a race to perfect, optimize, and implement this technology in order to further license it out to food delivery operations and other logistic heavy business that focus on the last mile.

The licensing portion out of self-driving technology will become a massive revenue driver eclipsing anything that the actual ride-hailing revenue from passengers can inject.

Well, that is at least the hope.

And because Lyft going public might force the company to remove the subsidies provided to the lift operators, this could translate into higher costs per unit.

The pathway is a no-brainer – Lyft needs self-driving technology more than the technology needs them.

And even though Google is head and shoulders the industry leader with Waymo, Lyft and Uber don't have a world-famous search engine that they can fall back on if the sushi hits the fan.

I believe Lyft passengers will have to pay more for rides in the future because of the demand for meeting short-term targets incentivizing management to raise fares.

Going public first will allow them to set the industry standards before Uber can participate in the discussion gifting a tactical advantage to Lyft.

That is why Uber is attempting to go public as fast as possible because every day that Lyft is a public company is every day that they can push their unique narrative and standardize what is a nascent industry that never existed 20 years ago with their new capital.

If high risk is your cup of tea, then buy shares when you get the first crack at it, otherwise, take a backseat with a bag of popcorn and watch history unfold.

This trade is not for the faint of heart and until we can get some more color on the business model and the ability or not of management to meet quarterly or annual expectations, there will be many moving parts with cumbersome guesswork involved.

To read up on Lyft’s IPO filing on the SEC website, please click here.