Mad Hedge Technology Letter

March 26, 2021

Fiat Lux

Featured Trade:

(AVOID THIS KOREAN ECOMMERCE COMPANY)

(CPNG), (AMZN), (GRUB), (UBER), (JD), (SHOP), (MELI)

Mad Hedge Technology Letter

March 26, 2021

Fiat Lux

Featured Trade:

(AVOID THIS KOREAN ECOMMERCE COMPANY)

(CPNG), (AMZN), (GRUB), (UBER), (JD), (SHOP), (MELI)

I might characterize Coupang (CPNG) as something akin to China’s JD.com.

It's an e-commerce company that has fulfillment solutions, not dissimilar to Amazon (AMZN) Fulfillment. They also have storefronts that they provide for businesses, which isn't dissimilar to say, a Shopify (SHOP).

Even combining aspects of Amazon and Shopify are there but they don’t have the powerful AWS cloud business.

Similar to JD.com (JD), which is a Chinese e-commerce platform, Coupang has differentiated itself by owning its entire logistics and delivery system.

What is different about Coupang versus the other players in Korean e-commerce is that they own their own inventory for the most part.

That means that they have inventory sitting on their balance sheets.

They have responsibility for pushing that through. But it also means, since they directly negotiate with the manufacturers of these items, they're able, for the most part, to get lower prices.

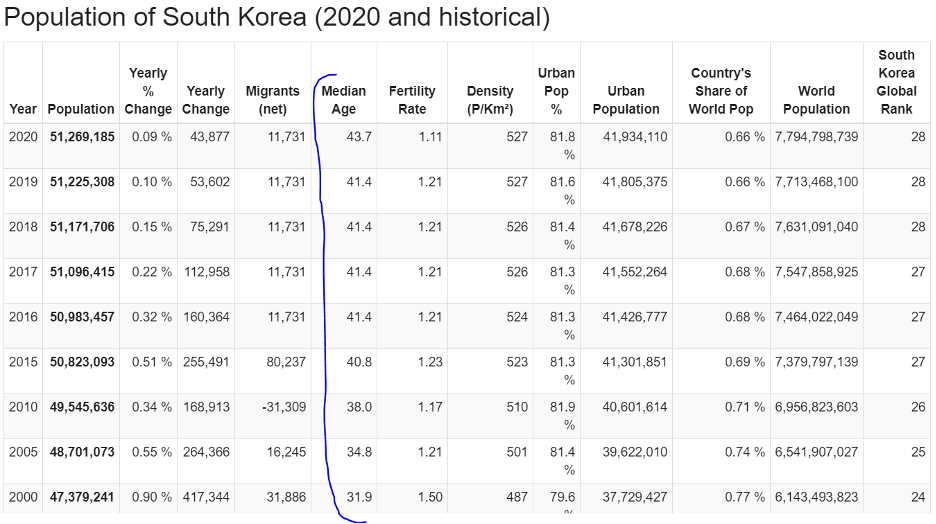

Total Korean e-commerce spend was $128 billion in 2019, which is expected to grow to $206 billion by 2024, implying a CAGR of approximately 10%.

This is where Coupang has a chance but in a rising interest rate environment and with competition on the New York exchanges from Amazon (AMZN), Shopify (SHOP), even MercadoLibre (MELI), I don’t believe Coupang is more attractive than these 3 in its current form as it relates to American investors pouring money into their stock.

Is it an advantage if 70% of Koreans live within seven miles of the Coupang logistic centers?

Certainly, there is that train of thought.

The massive investments into fulfillment centers mean they can surpass the delivery speed of many of its competitors because South Korea is essentially one capital city with millions upon millions hovering on top of each other like many other parts of Asia.

The problem I can have with this scenario is that margins could suffer because a busy Korean lifestyle doesn't lend itself to things like in-store shopping as readily as it does in the United States, and it could manifest itself with Koreans tapping into higher frequency in which they buy online which will push up total spend, but margins will decrease because you are buying stuff that won’t move the needle higher because you've paid for the service.

I can easily see someone just buying one item for delivery in the morning and doing that seven days per week.

Now I need a set of tweezers, I'm going to order that. Tomorrow, I need cotton pads, I’m going to order that.

Over time, operating margin will get butchered with a business like this.

And what do you know? I’m right, they have been losing billions upon billions the past few years with no end in sight.

How long will the external investors subsidize their losses?

At a broader level, mobile phone penetration is already at 96% of Koreans and 40% of Koreans order groceries online, so it’s hard for me to digest where the addressable market can expand from here because they have already collected so much of the available harvest.

This IPO does feel a little bit like an ex-growth dump on the retail investor and that’s not saying shares can’t appreciate at all, but investors believing this is the next Amazon are sorely mistaken.

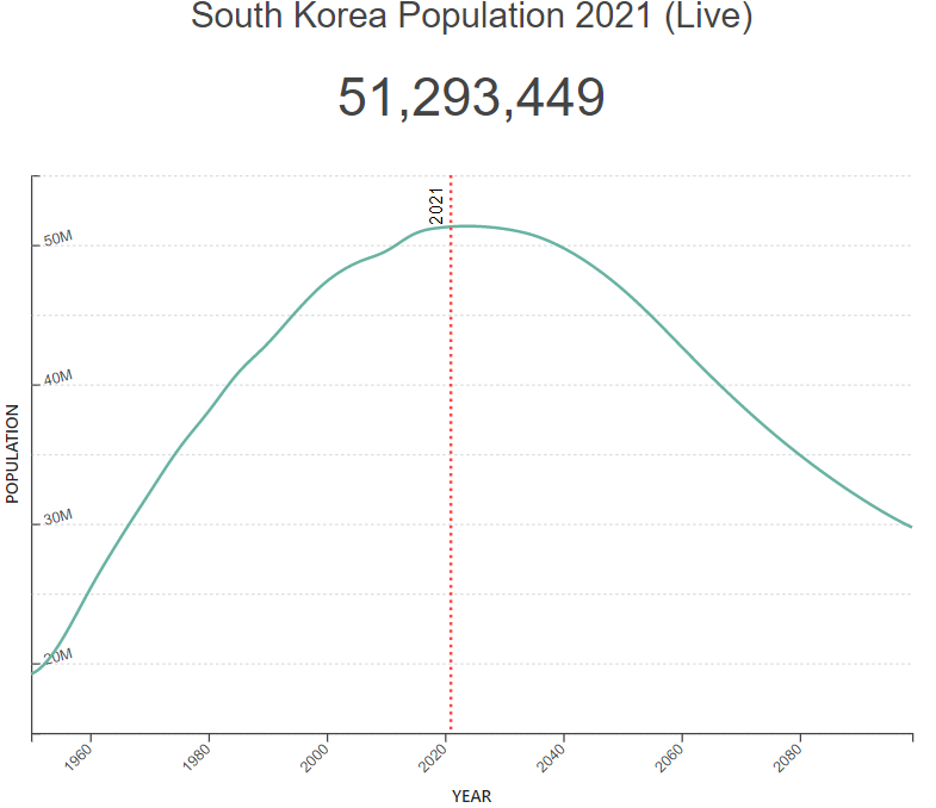

They are not Amazon, not even close, and they are also confined to one small market where the population has peaked and will start decreasing in numbers.

The population is only 15% of the U.S. and incomes in the U.S. are vastly higher, so how does Coupang become an Amazon without the AWS business?

Just as disturbing, the median age in Korea has ballooned from 31.9 in 2000 to 43.7 in 2020 and this cohort doesn’t strike me as the group in the glory years of family formation, peak spend, or technological know-how.

As the Korean population starts to decline in 2025 and the median age creeps up from 43.7 to 50, then aside from adult diapers, where does the incremental growth come from in Korea?

I just don’t see it.

Personal incomes are going to rise at an annualized rate of about 3% every year and I believe much of the total spend will be fought out attempting to woo the big buyers which offer a point of attack for competition that should come around in the next 2 to 3 years.

They also have Coupang Eats, not dissimilar to Grubhub (GRUB) or Uber (UBER) Eats. They have grocery delivery, and even an integrated payment processor. All of these things that took Amazon much longer to build out, admittedly, were a little before their time there, Coupang has already integrated that into the platform.

For this, I give them credit, but they are still nothing like Amazon in terms of potency and scale.

In 2019, active customers rose 34% and that’s what a prototypical growth company should do.

It’s not shocking.

Then an analyst would think that with covid and all that public chaos pinning consumers at home, surely, Coupang would grow active customers by 50% of even 60% in 2020, right?

But active customers only grew 18% in 2020, and they provided zero insight about why active customer growth slowed nearly in half year-over-year, and that for me shows, Coupang is severely limited by what Korea can offer in terms of growth and total spend.

If readers want to get into the Korean economy then I would advise to wait on other Korean homegrown entrepreneur-led startups with IPOs in the pipeline by Krafton Inc., the creator of hit game PUBG, and the country’s biggest mobile-only bank Kakao Bank. Unlike Coupang, those firms are profitable.

Ultimately, total e-commerce spend for all Internet buyers in Korea is expected to grow from approximately $2,600 in 2019 to approximately $4,300 in 2024 on a per buyer basis and Coupang will take advantage of that but I don’t foresee the 30% annual rise in underlying shares that others do.

I can definitely visualize a grind up with periodical substantial selloffs because of missed targets and disappointing forecasts.

That’s not the type of price action I want to see.

The signs point to Coupang maturing immediately and the executive management creating a special clause to allow them to dump shares right after the IPO illustrates that this tech company will stall out moving forward.

Normally, management must wait 6 months after going public before the lock-up period ends.

Highly unusual and can you believe it? They even gave stock shares to their courier drivers at the IPO, making me pause, then come to the conclusion that I rather invest in a tech company returning incremental value to the shareholders and not the manual labor that is paid by an hourly wage. How bizarre!

Avoid Coupang like the plague.

Global Market Comments

March 23, 2021

Fiat Lux

Featured Trade:

(NOW THE FAT LADY IS REALLY SINGING FOR THE BOND MARKET),

(JPM), (BAC), (C), (FCX), (TLT), (UBER)

Mad Hedge Technology Letter

February 10, 2021

Fiat Lux

Featured Trade:

(UBER GETS ANOTHER MULLIGAN)

(UBER)

Great news for tech investors – Uber (UBER) is getting a pass on its almost historic loss-making 2020!

A highly bullish indicator is the broader tech market able to absorb an almost $7 billion annual loss with ease.

This all bodes well for the health of the tech market in 2021 – we should finish this year clearly higher than we are now today albeit with no black swans.

The tech market is iron clad right now with multiple external forces pushing up multiples to historic levels.

Imagine there are copious amounts of better tech companies out there that are actually turning a profit and are even at the vanguard of all the latest tech trends, and Uber definitely isn’t one of them.

Yet, I believe Uber shares will roar higher!

A Nasdaq index brimming with liquidity is the one way to explain this phenomenon because the bar has been set so low for tech companies to jump over that unless there is a bankruptcy or systemic risk, shares will rip higher.

Remove the liquidity subsidy and Uber shares would be headed into the gutter in a flinch.

But here we sit with tech shares going parabolic after a robust breakout.

If this carries on, we will see more abnormal side-effects and I believe the GameStop phenomenon was precisely the precursor to much weirder activity that is about to happen.

I must divulge that part of the narrative driving firms like Uber is the re-opening theme of increased consumer behavior if the population is theoretically inoculated driving a surge in economic activity.

The boom in outdoor consumerism would catapult Uber’s loss-making ride share division which performed poorly grossing only $6.79 billion, down 50% from a year ago.

As many might have guessed, Uber’s pitiful performance in ridesharing in a pandemic was met conversely by heightened food delivery gross volume of $10.05 billion, up 130% from a year ago.

What does this mean?

Uber is turning into a loss-making food deliverer from a loss-making ridesharing company and are still losing vast sums of money.

Their strategy of acquiring other food deliverers like alcohol delivery app Drizly for a deal valued at $1.1 billion in stock and cash combined will scale well and offer cost savings but is no panacea.

They also sealed a deal for a $2.65 billion acquisition of delivery service competitor Postmates in December to help build out its delivery capabilities.

However, where is the light at the end of the tunnel?

Where is that iPhone or YouTube – that game-changing asset?

There is no growth asset here and I still see no proprietary technology other than an app that matches drivers to passengers and a food delivery app that gets a car to its hungry customers.

To Uber’s credit, they revealed 20% improvement in net losses amounting to $6.77 billion, from a jaw-dropping $8.51 billion loss in 2019, and I will agree there is headway to make with such lousy numbers.

As long as Uber is afforded such a long leash and incentivized to perform badly, they can incrementally reign in the net losses and still claim victory.

But I scratch my head thinking how they will finally overcome that “last mile” problem of making this company a true tech giant and not one just brandishing below-average intellectual property and partying for losses that aren’t as bad as expected type of model.

At the end of the day, we can only trade the market we have, and not the one we want.

The broader tech market has given its implicit nod to Uber and this company remains an attractive buy on the dip tech growth company even though I listed a myriad of risks and concerns about its underlying model.

Mad Hedge Technology Letter

February 8, 2021

Fiat Lux

Featured Trade:

(VENTURE CAPITALISTS SHARE THE CLUES TO THE TECH MARKET)

(NVDA), (OTCMKTS: SFTBY), (GOOGL), (BABA), (AMZN), (UBER), (FB)

To gain a glimpse into the current psyche of tech investing, we need to take a raw snapshot of the state of Softbank’s Vision Fund.

The Vision Fund is the brainchild of the Japanese telecom company’s founder Softbank Masayoshi Son and is the world’s largest technology-centric venture capital fund with over $100 billion in capital.

The torrent of bullish price action of late has meant that SoftBank recorded a record quarterly profit in its Vision Fund as a gangbusters’ stock market lifted the value of its portfolio companies.

However, the significant gains accrued in equity were also substantially offset by painful derivatives losses as Son attempted to parlay his winnings into leverage directional bets in the short-term.

The Vision Fund’s $8 billion profit in the December quarter is a stark change from the prior March when the pandemic was in full gear and the Fund booked major losses amid embarrassing flops like office space sharing company WeWork.

As 2020 came to a close, tech growth firms like Uber (UBER) stock exploded higher and DoorDash (DASH) gave the Vision Fund a nice payday going public at the end of the year in stellar fashion.

On the options trading front, things didn’t go so rosy.

SoftBank posted a 285.3 billion yen or $2.7 billion derivatives loss in the period.

I understand “hedging your bets” but for Son to create this massive loss undeniably has to infuriate deep-pocketed investors from Arab nations that have stuck with him through tumultuous events.

The staggering option losses was why the asset management arm registered a loss of 113.5 billion yen or $1.08 billion, up from losses of 85.2 billion yen in the previous three-month period.

Experiencing wonderful gains only to have the narrative wiped out because of high stakes option bets is perhaps a sign of the times as phenomena like the Gamestop (GME) have moved to the forefront indicating that players have access to too much liquidity at this point in the market cycle.

Some 15 companies have gone public from the Vision Fund so far, and Son does have a long list of busts and winners.

However, one might assume that he won’t hit on every company as he revealed that his Vision Fund 1 and Vision Fund 2 have invested in a total of 131 companies. In the case of DoorDash, SoftBank invested about $680 million for a stake now worth about $9 billion while its $7.7 billion investment in Uber is worth $11.3 billion.

There are still shining stars on the balance sheet.

Another six more portfolio companies are planning IPOs this year and bringing this volume model to the public markets is logical considering even zombie companies are getting funded out the wazoo at this point.

Tech is also still holding its perch as the darling of the market and Son is simply delivering to market what investors want which is growth tech and more of it.

Other issues on Softbank’s list are to sell off its interests in Alibaba, T-Mobile US Inc., and SoftBank Corp., the Japan telecommunications unit. SoftBank also announced a deal to sell its chip designer Arm to Nvidia (NVDA) for $40 billion.

On top of the risky growth companies, Softbank has also parked its capital in a who’s who of tech firms such as a $7.39 billion investment in Amazon.com (AMZN), $3.28 billion in Facebook (FB). and $1.38 billion in Alphabet or Google (GOOGL). The operation is managed by its asset management subsidiary SB Northstar, where Son personally holds a 33% stake.

Son labeled his options debacle as a “test-drive stage” hoping to play down the fact that he should have made a lot more with the massive ramp-up in tech demand in 2020.

It’s not all smooth for Son with the chaos at Alibaba (BABA), Son’s most exotic investment success to date and SoftBank’s largest asset, tanked 20% last quarter amid a Chinese government clampdown on Alibaba Founder Jack Ma.

This has to worry Son’s future tech investing prospects in China (P.R.C.).

SoftBank’s own sale of Arm to Nvidia (NVDA) is still making the rounds through the EU approval process. The United Kingdom and European Union are both preparing to launch probes into the deal.

All in all, a mixed bag for the Vision Fund where profits should have been higher and most of the damage was self-inflicted.

At some point, throwing massive amounts of capital to juice up tech growth firms will backfire, but the generous access to liquidity that Son has makes this strategy work while even affording him some massive failures.

In short, the Vision Fund should be many times more profitable and it’s a reminder that these leveraged bets aren’t going away which should mean enough liquidity out there to take the markets higher.

We should also be aware that the eventual “market mistake” could give us 10% tech corrections, which are no brainer buying opportunities if the same liquidity volume persists.

Then consider that many tech companies have done well in the recent earnings season and combine that with the eventual reestablishment of buybacks and the neutral observer must think that tech has more room to run in 2021.

Mad Hedge Technology Letter

November 9, 2020

Fiat Lux

Featured Trade:

(UBER BACK FROM PURGATORY)

(UBER), (LYFT), (GRUB)

The most impacted tech company in 2020 is most likely ridesharing company Uber and is highly likely to become the new “buy the dip” tech stock.

I’ll tell you why and how they managed to turn it around.

Foundationally, two important data points from their earnings report have to be total revenue declining 18% year-over-year and delivery revenue growing 125% year-over-year.

The good news is that delivering food is turning out to be a monumental growth engine and the bad news is that the core business is hamstrung by the current conditions stemming from the global health crisis.

Even with their core business declining, Uber benefits from a silver lining of the macroeconomy recovering from summer lows and this will follow through into its ride-sharing operations.

The initial recovery from terrible to bad is usually the greatest in terms of percentages similar to recent quarterly GDP numbers.

I am definitely observing positive movement in Uber’s direction, especially as consumers feel less comfortable taking mass transit during the pandemic.

This development is clearly much better than a mass lockdown where Uber is unable to deliver on any rideshare volume whatsoever.

Management has also indicated that the overall environment is starting to considerably improve over the coming quarters with Q2 marking a clear trough in volumes and fundamentals.

Another potential tailwind is that the consumer element is becoming commonplace across cities both in the US and internationally and their preference will steer them away from mass transportation given health concerns.

This could result in an incremental demand driver for ridesharing vendors over the next few quarters and beyond.

Structurally, Uber will get to the other end of the health crisis intact and as a healthy corporation.

That speaks volumes compared to corporates floundering in damaged industries like energy and retail.

But the elephant in the room was finally addressed with the passage of California’s Proposition 22, a measure that exempts it, along with rival Lyft (LYFT) and businesses like Instacart and GrubHub (GRUB), from having to pay drivers like in-house employees.

This is the feather in their cap they needed to become the newest buy the dip tech stock because it essentially means they won’t have to pay drivers much to drive for Uber instead of doling out proper employment contracts.

The passage of the proposition legitimizes Uber’s business model at a time where the global economic environment is precarious, and we could be walking straight into legislative gridlock and an inadequate fiscal stimulus package.

This obviously means putting less dollars in consumers’ pockets to pay for Uber Eats and Uber rideshares.

This was essentially an existential issue for Uber in the state of California and without a win, Uber and Lyft threatened to pull out of California entirely.

This has happened before like in Austin, Texas, which Uber deserted in 2016 after the city passed a measure calling for stricter background checks and fingerprinting for drivers.

Fortunately for Uber, Texas State Legislature overruled Austin, and Uber and Lyft returned to the city.

The current ballot count is 58.4% in favor of Prop 22 and 41.6% in opposition meaning Californian citizens overwhelmingly voted to pass this measure.

Californians, no doubt, were scared to lose their cheap way of getting around the suburban sprawl that is California.

Even if Uber’s company creates a traffic snarl of drivers meaninglessly idling around for more rides – that is a moot point right now.

Gig workers will continue to be classified as independent contractors in the state.

It also essentially makes these gig companies exempt from AB-5, the gig worker bill that went into law at the beginning of the year that forces gig companies to pay sub-contractors like regular workers.

That is off the table and a massive win for Uber.

On the back of this legislative success, Uber will now take this win and go after other states to pass similar types of legislation.

This political template for future anti-labor, corporate law-making is pro-capital to the extreme extent of the law for better or mostly worse in my eyes if you aren’t a corporate shareholder.

This perhaps could open up all corporations in California to never pay health or social security benefits in the future to employees.

If Uber doesn’t have to, then why does Google, Facebook, or Apple need to share the burden of paying for medical and social security benefits?

Labor groups are considering potentially lobbying the newly elected Biden administration’s Department of Labor for improved federal laws for worker classification.

Biden has pledged to narrow economic inequalities and Uber’s win could be in his crosshairs because the result is a massive setback for labor laws in California and potentially around the United States.

Intervention would take some balls by the Biden administration and the most likely scenario is him giving Uber a pass.

Gig Workers Rising, a campaign supporting and educating app and platform workers, had this to say, “Billionaire corporations just hijacked the ballot measure system in California by spending millions to mislead voters. The victory of Prop 22, the most expensive ballot measure in U.S. history, is a loss for our democracy that could open the door to other attempts by corporations to write their own laws.”

Yes, this is terrible for Uber drivers but highly positive for shareholders of Uber’s stock.

The cost of doing business is effectively passed on to the guy at the bottom – sub-contracted drivers.

Like it or not, it will be enshrined into Californian law and this makes serious inroads to Uber’s business model actually becoming profitable which has been the big knock on this company.

At the very minimum, this will give a stop-gap measure for the 10 or so years Uber needs to get to autonomous driving technology where they can just never pay the driver again.

Not only does the path to autonomous driving technology look optimistic, but the excess liquidity circulating in the market effectively means that zombie companies will be funded infinitely.

Although not a zombie company, Uber has really had a hard time making up the numbers to prove a viable path to sustainability and that basically doesn’t matter anymore.

The existential threat is now out of the window and with several structural tailwinds powering Uber, the stock and the company have never had a brighter future and any medium-sized pullback should be bought.

This one is going higher.

Mad Hedge Technology Letter

August 10, 2020

Fiat Lux

Featured Trade:

(SCRAPING THE BOTTOM OF THE TECH BARREL WITH UBER)

(UBER), (LYFT), (FB), (AMZN), (GOOGL), (NFLX), (AAPL), (MSFT)