The coronavirus and the resulting effects from it have had the single most sway on tech companies since the 2001 tech bust.

Marginal tech companies or even quasi-fraudulent ones have been exposed for what they are, while the secondary effects from the virus have supercharged the behemoths of the industry.

The stock market has no earnings growth in the past 5 years without the earnings from Microsoft (MSFT), Facebook (FB), Apple (AAPL), Google (GOOGL), Amazon (AMZN), and Netflix (NFLX). That means that without the Republican corporate tax cut, there has been negative earnings growth in the past five years.

One of those tech companies at the bottom of the barrel has been chauffeur service company Uber (UBER) and their latest earnings report is a glaring indictment of a shoddy business model that operates in a gray area.

The only reason this stock is at $33 is because of the piles of easy money printed by the central bank.

Uber needs all the help they can get, and shares are still trading 20% below the IPO price.

Competitor chauffeur service Lyft (LYFT) is doing even worse registering a 50% decline since the IPO.

Let’s do a little snooping around to see why these companies are doing so poorly and why you shouldn’t even think about investing in these companies long-term.

No matter how you dice it up, Uber’s core business, the one where they refuse to properly compensate their drivers, had a disaster of a quarter with gross ride volumes down 73% year-over-year.

Before we go any further with this one, I would like to point out yes, other areas of the business grew substantially, the problem is that the “other” part of the business is only 30% of total revenue.

Therefore, when 70% of your business that relies on pure volume to scale out crashes by 73%, it doesn’t really matter what else is in the report.

The only sensible idea now is capturing a snapshot of the silver linings, of which there were a few.

Delivery volumes through Uber Eats were up 49%, but the problem here is that first, it’s not profitable per delivery and second, it’s still a small part of the business.

Uber acquired Postmates who is another loss-making delivery service and the idea behind this is to achieve significant cost savings by scaling out these powerful assets.

The problem here is that it is essentially throwing good money on top of bad money because it’s proven that deliveries don’t make money per ride and that won’t change in the near future.

CEO of Uber Dara Khosrowshahi is on record saying Uber will become “profitable on an adjusted earnings basis before interest, taxes, depreciation, and amortization before the end of the year.”

This is almost like saying we won’t lose as much money as before and ironically, Dara Khosrowshahi has withdrawn this statement as the ride-sharing model has been repudiated by the consumer during the coronavirus.

Nowhere in the earnings report is the explanation of how Dara Khosrowshahi plans to attract people to share a car ride with a stranger during a global pandemic.

He didn’t share a solution because there isn’t one, hence the 73% decline in ride volumes.

If we assume this company is semi-fraudulent, then the silver lining would be that ride volumes didn’t decline by 100%.

That is where we are now with U.S. corporate companies such as the airlines that fired their employees but have subsidized them to stick around even though there is no work.

Instead of re-imagining itself through bankruptcies, the Fed has encouraged many marginal companies by breathing life into their finances through cheap loans.

This gives failing firms a last chance to enrich management with the capital and “cash out” before they hand the business off to someone who will essentially plan to do the same.

I will say that traders might have a trade or two in this one, because it’s hard to imagine Uber posting another 73% loss in ride volume and a dead cat bounce trade could be in the cards.

Long term investors should steer clear of this one and allow Uber to struggle on its own and just maybe in 5 or 10 years, it might just be “profitable on an adjusted earnings basis before interest, taxes, depreciation, and amortization before the end of the year.”

With so many high-quality tech companies and even one that is about to add super growth elements like TikTok into its portfolio, there are so many superior names to deploy capital in the tech ecosphere.

Either you must be galvanized by a gambler’s mentality to invest in Uber, or losing money is something that is habitual in your routine.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-08-10 10:02:102020-08-10 15:57:53Scraping the Bottom of the Tech Barrel with Uber

To understand the unintended consequences of the Fed’s helicopter money to U.S. capitalism, we can put a magnifying glass over Uber’s (UBER) recent takeover attempt of Grubhub (GRUB) as what’s in store for not only the tech sector but the wider public markets.

Zombie companies parade around Europe and Japan because of an era of low interest rates and cozy bank relationships that keep these companies from dying out.

To read more about Allianz Economic Advisor Mohamed El-Erian’s take on zombie companies – click here.

It’s not a surprise that Japan and Europe are highly unproductive, and innovation ceases to exist when capital is being tied up in marginal companies with management happy to let capital slosh about without adding extra added value.

I get it that the Fed is trying to “save” the wider U.S. economy by bringing out the bazookas and even by buying junk-graded debt which was once seen as heresy.

But what we have now are inferior companies that will never turn a profit masquerading as real companies that would be on life support if not for cheap capital.

In almost every instance, the only winners are the executive management who pillage the system and cash out when they are allowed to sell their stock.

U.S. Representative for Rhode Island David Cicilline hit the nail on the head when he described the fluid situation by focusing on two of the bad apples, saying “Uber is a notoriously predatory company that has long denied its drivers a living wage. Its attempt to acquire Grubhub — which has a history of exploiting local restaurants through deceptive tactics and extortionate fees — marks a new low in pandemic profiteering.”

Uber is a taxi service that undercompensates its highest expense - the driver, and Grubhub delivers restaurant food but rips off the restaurants in doing it.

I defined exorbitant delivery fees as up to 40% which Grubhub is infamous for charging.

Yes, even with predatory practices, they cannot turn a profit.

Now, in this new normal of coronavirus, it would be a miracle to make any operational headway.

Uber’s attempted market grab is a giant red flag.

My guess is that they are doing this in order to jazz up the balance sheet and concoct some ridiculous new metric showing a pathway to growth.

By adding growth to revenue, Uber would be able to preach “growth” even if it’s of bad quality.

I thought the tech market was done looking through to grow by essentially killing off the “WeWork model.”

However, Uber is going for a model that is one notch above that model and repurposing it as something actually meaningful, which of course, it’s not.

They are already in litigious hell regarding driver’s remuneration, and that will not die down and could even destroy Uber.

Uber has in fact ignored California state orders to reclassify its drivers as employees and have appealed the court’s decision.

The New York state government has validated my theory of these fly-by-night delivery outfits being a net negative for business and society.

The New York City Council compared food ordering apps Grubhub and UberEats to blood-sucking parasites this week before passing emergency legislation aimed at helping struggling restaurants lower delivery costs during a precarious time.

During the state of emergency, a new vote passed capping food ordering and delivery app fees at 15% in delivery fees and 5% “other” takeout order fees.

To read more about this decision by the New York City Council – click here.

This was done to give some power back to the restaurants that have been getting fleeced.

The balance sheet shows the whole story with Uber's net loss totaling more than $8.5 billion in 2019 and in February, they reported a net loss of $1.1 billion in the fourth quarter.

Let me remind readers that Grubhub posted a net income loss of $27.7 million for the last reported quarter as well.

As it turned out, Grubhub rejected Uber’s offer believing it didn’t meet their valuation of the company.

It would appear natural that a predatory company with no competitive advantage would set a market premium that would align with their borderline extortionate ways.

Do not own either one of these companies – there are far better ones out there in tech and no need to scrounge at the bottom of the barrel.

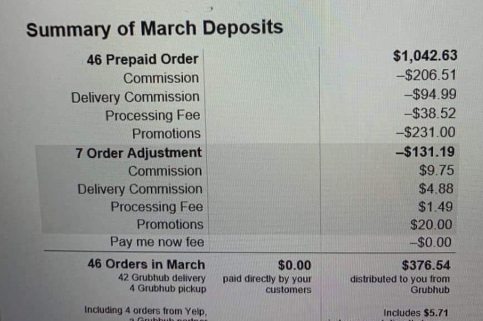

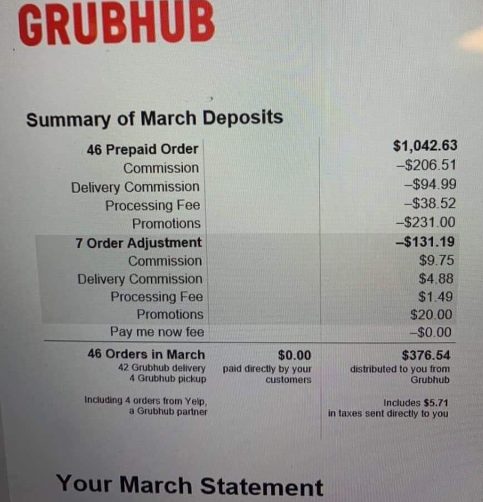

Monthly Grubhub bill for Chicago Pizza Boss During the Epidemic

https://www.madhedgefundtrader.com/wp-content/uploads/2020/05/grubhub-may15.png502483Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-05-15 10:02:362020-06-15 12:14:38Why Uber Tried to Buy Grubhub

Nimble tech firms like online taxi company Lyft will be penalized in the coronavirus economy as it de-globalizes for a period of time.

If you read the Mad Hedge Technology Letter, you already know that I believe rideshare business models will never become profitable.

Fast forward to today and ask yourself how can these companies make profitability headway when the state mandates shelter in place policies?

The answer is they cannot.

It is not exactly the type of foundational policy that promotes more ride-sharing volume, so bad news for Uber and Lyft.

Uber CEO Dara Khosrowshahi told investors that ride volume has gone down by as much as 60%-70% in ground zero cities like Seattle, and that’s before you consider the pauses in some of its secondary services and the dubious distinction of becoming one of the earliest proof-of-concepts of just how fluid this virus really is.

But Khosrowshahi also told investors that Uber is “well-positioned” to ride the troubles out even in the worst-case scenario of rides down by 80% for the year. And even as ride volume crashes, it is also considering leveraging its network for delivering other things, such as medicine or basic goods.

Basically, Uber specializes in losing money and lots of it.

Then imagine how demoralizing it is for the inferior version of Uber, it’s little brother Lyft.

Lyft has no “other” businesses such as food delivery service Uber Eats, leading me to conclude that this massive retracement in shares must be a bear market rally that will run out of steam.

Finding entry points to short growth stocks is an imprecise endeavor but I do believe that poor revenue reports in the upcoming earnings season is going to cap this bear market rally in Lyft’s shares.

What do we know already?

A global and tech recession will be sharp and it will be worse than the global financial crisis possibly by a factor of 4.

Investors still cannot wrap their head around whether this contagion will spill over into being a depression.

Tech investors will need to respect the “new, new normal” following the pandemic, in which corporates make aggressive cuts to their spending side-- again, bad news for Uber and Lyft.

This type of scenario is especially problematic for Lyft who must spend illogically just to stay in business.

Lyft burned $463.5 million in the third quarter of 2019, which was almost twice the amount that the company lost over the same period of time the previous year.

The fourth quarter net loss includes $246.1 million of stock-based compensation and related payroll tax expenses as well as $86.6 million related to changes to the liabilities for insurance.

That translates into an adjusted net loss of $121.6 million, which is better than the adjusted loss of $245.3 million over the same period last year.

Considering the elevated amount of cash burn to Lyft’s model pre-virus and aware that nobody knows how long the cash burn will accelerate beyond Lyft’s earnings – investors are staring into a black hole of infinite losses moving forward as Lyft’s business model looks worse every day.

I must conclude that the post-coronavirus economy is highly likely to not be kind to marginal companies like Lyft who is a glorified taxi service.

Uber controls about 60% of the ride-sharing market in the US and managed to accomplish this by losing $5.2 billion in the Q2 2019.

Lyft has already slashed its R&D budget by deleting the autonomous vehicle development program.

Yes, the very program that was supposed to be the x-factor in its quest for real profits.

Laughably, Lyft’s executives emphasized that they believed the company will turn a profit in the fourth quarter of 2021, a year earlier than they had previously projected, but that forecasts looks foolish in hindsight.

The one miniscule silver lining for Lyft - fewer discounted rides than it did a year ago.

Lyft is also trying to boost the number of more-profitable rides, which are premium trips such as “airport” or “business” trips.

It’s a shame these premium trips have gone to zero.

The narrative has quickly pivoted to “grow at all costs” to “survive at all costs” and it’s not surprising to see Lyft grossly underperform the Nasdaq index in relative terms and most quality cloud stocks are in the midst of a v-shaped recovery.

Lyft is a sell on a rally type of stock.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-04-17 09:02:462020-05-19 11:33:44Why You Should Sell the Uber Rally

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader March 25Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Since we flipped the off button on the economy, I don’t see how we can simply flip the on button and have a V-shaped recovery. It seems much more unlikely that it will get back to pre-recession levels.

A: Actually, all we really need is confidence. Confident people can go outside and not get sick. Once we start seeing a dramatic decline in the number of new cases, the shelter-in-place orders may be cancelled, and we can go outside and go back to work. It’s really that simple. So, we will get an initial V-shaped recovery probably in the third quarter, and after that, it will be a slower return spread over several quarters to get back to normal. Everybody wants to get back to normal and let's face it, there's an enormous amount of deferred consumption going on. I have hardly spent any money myself other than what I’ve spent online. All of those purchases get deferred, so in the recovery, there's going to be a massive binge of entertainment, shopping, and travel that is all being pent up now—that will get unleashed once the airlines start flying again and the shelter-in-place orders are cancelled. We’re not losing so much of this growth, we’re just deferring it. Obviously, some of the growth is gone permanently; you can forget about any kind of vacation in the next couple of months. I would say, the great majority of consumption in the US—and thus growth and thus stock appreciation—is just being deferred, not cancelled outright.

Q: Other than the ProShares Ultra Technology ETF (ROM), do you have any other leveraged sectors coming into the recovery?

A: There is a 50/50 chance the Roaring 20s started 2 days ago, on Monday, March 23 at the afternoon lows. We may go back and test those lows one more time, which at this point is 3,700 points below here, but we are clocking 1,000 points a day. It doesn’t take much, like a bad non-farm payroll number, to go back and test those lows. The good news is out; they're not going to spend any more money other than the $10 trillion they're putting in now.

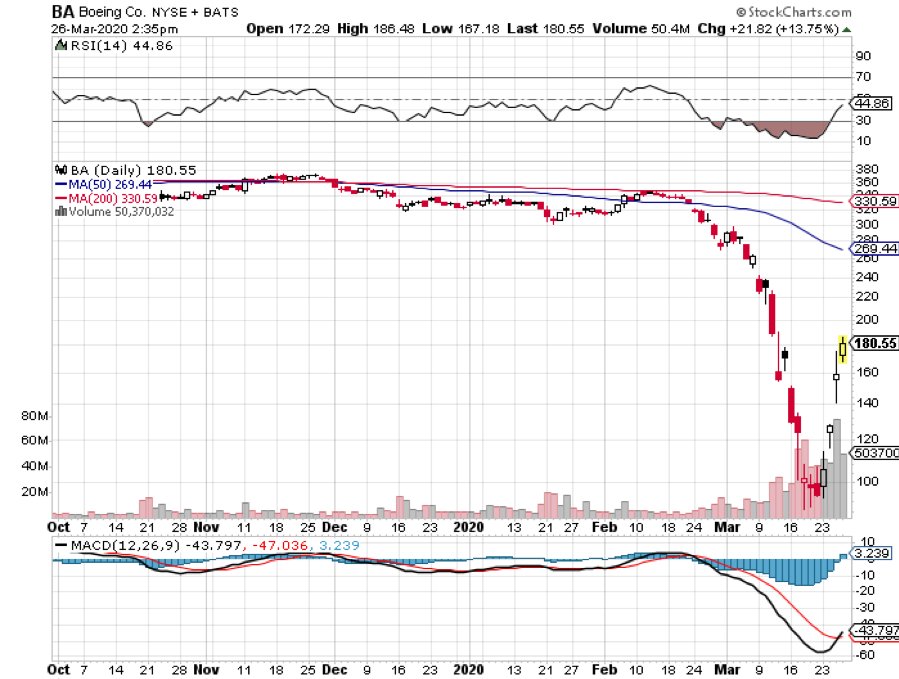

Q: Would you buy Boeing (BA) here? Is this the bottom?

A: The bottom was at $94 on Monday; we went up 100% in three days and now we’re at $180. Incredible moves, and a total lack of liquidity. One reason I haven't added any positions lately is that they have closed the New Yok Stock Exchange floor and its not clear that of I send out a trade alert, it could get done. We have gone totally online, so I just want to see what happens as a result of that. I don’t want to be putting out trade alerts that no one can get in or out of, heaven forbid.

Q: What do you mean by “The spike to $80 in the Volatility Index (VIX) was totally artificial?”

A: When you have a series of cascading shorts triggered by margin calls, that is artificial. I have seen this happen many times before, both on the upside and the downside. This happened twice in the (VIX) in the last two years. When you go from a (VIX) of $25 to $80 and back down to $39 in days, which is what we did, you know it was a one-time-only spike and we are not going to visit the $80 level again— at least not until the next financial crisis because those positions are gone and are never coming back. A (VIX) of $80 means we are going to have 1,000 point move in the Dow Average for the next 30 days.

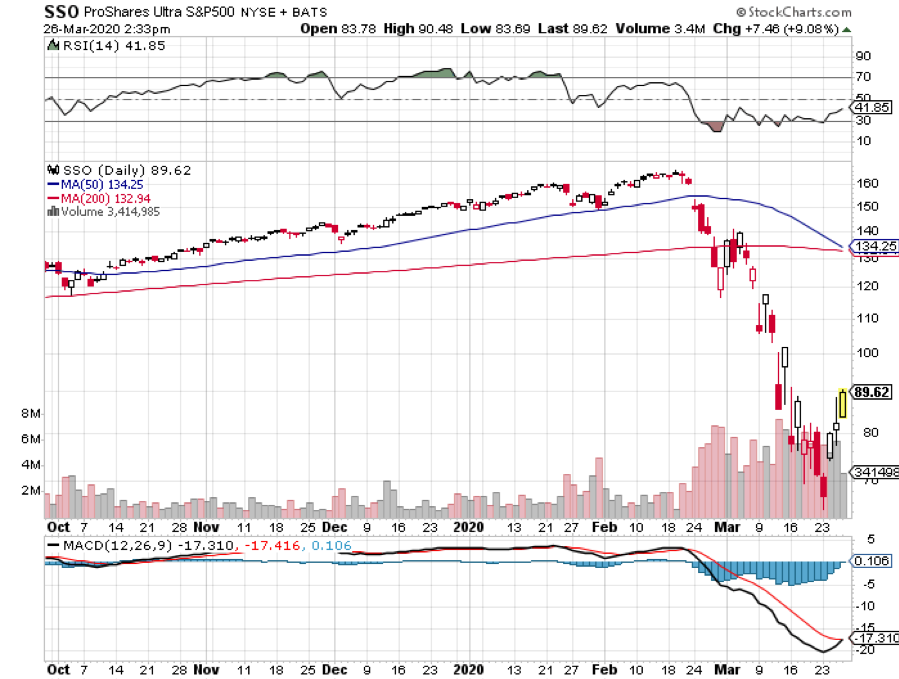

Q: I bought some ProShares Ultra Pro ETF (UPRO) which is the 3x long the S&P 500 at $1,829. Do I take profits by selling calls or just hold longer?

A: I would just sell the whole position outright. The (UPRO) is so incredibly volatile that you are rewarded heavily for just coming out completely and then reopening fresh positions on these big meltdown days. We will probably be doing trade alerts on (UPRO) or its cousin, the 2x long ProShares Ultra S&P 500 (SSO) sometime in the near future.

Q: With 2-year LEAPs, would you go at the money or out of the money?

A: This is the golden opportunity to go way out of the money because the return goes from 100% to 500%, or even 1000% if you go, say, 30%-50% out of the money. A lot of these stocks are ripe for very quick 30% bouncebacks, especially the (ROM). So yes, you want to do out of the money 20% to 30%. It will easily recover those losses in weeks if you are picking the right stocks. Over a two-year view, a lot of these big tech stocks could double by the time your LEAP expires, and then you will get the full profit. The rule of thumb is: the farther out of the money you go, the bigger the profit is. But I wouldn’t go for more than a 1000% profit in 2 years; you don't want to get greedy, after all.

Q: You called the Dow to hit 15,000. Is that still possible? We got down to the 18 handle.

A: Yes, if the coronavirus data gets worse, which is certain, we could get another panic selloff. How will the market handle 100,000 US deaths, given the exponential rise in cases we are seeing? With cases doubling every three days that is entirely within range. So, I would say, there is a 50% chance we hit the bottom on Monday at 18,000, and 50% chance we go lower.

Q: Do you know anything about the coronavirus stocks like Regeneron (REGN)?

A: Actually, I do, it's covered by the Mad Hedge Biotech & Health Care Letter, click here for the link. If you get the Biotech Letter, you already know all about stocks like Regeneron. Regeneron literally has hundreds of drugs in testing right now to work as vaccines or antivirals, and some of them, like their arthritis drug, have already been proven to work. So, we just have to get through the accelerated trials and testing to unleash it on the market. But for anybody who has a drug, it's going to take a year to mass-produce enough to inoculate the entire country, let alone the world. So, don't make any big bets on getting a vaccine any time soon—it's a very long process. Even in normal times, some of these drugs take months to manufacture.

Q: Are there any ventilator stocks out there?

A: There are; a company called Medtronic (MDT), which the Mad Hedge Biotech & Healthcare Letter also covers. They are the largest ventilator company in the US. Their normal production is 100 machines a week. Now, they are increasing that to 500 a week as fast as they can, but it isn’t enough. We need about 100,000 ventilators. China is now selling ventilators to the US. Elon Musk from Tesla (TSLA) just bought 1,000 ventilators in China and had them shipped over to San Francisco at his own expense, and Virgin Atlantic just flew over a 747 full of ventilators and masks and other medical supplies from China. So yes, there are stocks out there to play these things, they have already had large moves. We liked them anyway, even before the pandemic, so those calls were quite good. And China thinks their epidemic is over, so they are happy to sell us all the medical supplies they can make.

Q: Why did 30-year mortgage rates just go up instead of down? I thought the Fed rate cuts were supposed to take them down; am I missing something?

A: In order to get 30-year mortgage rates down, you have to have buyers of 30-year loans, and right now there are buyers of nothing. The lending that is happening is from banks lending their own money, which is only a tiny percentage of the total loan market. When the Fed moves into the mortgage market, you will see those yields move to the 2% range. The other problem is how to get a loan if all the banks are closed. They are running skeletal staff now, and you can’t close on real estate deals because all the notaries and title offices are closed; so essentially the real estate industry is going to shut down right now and hopefully, we’ll finish that in a month.

Q: Do you think Uber (UBER) and Lyft (LYFT) will go bankrupt?

A: It is a possibility because one to one human contact inside a car is about the last situation you want to be in during a pandemic. Their traffic was down 25% according to a number I saw. It’s very heavily leveraged, very heavily indebted, and those are the companies that don’t survive long in this kind of crisis. So, I would say there is a chance they will go under. I never liked these companies anyway; they are under regulatory assault by everybody, depend on non-union drivers working for $5 an hour, and there are just too many other better things to do.

Q: Is this the end of corporate buybacks?

A: To some extent, yes. A future Congress may make it either illegal or highly tax corporate buybacks, in some fashion or another because twice in 12 years now, we have had companies load up on buying back their own stock, boosting CEO compensation to the hundreds of millions—if not billions—and then going broke and asking for government bailouts. Something will be done to address that. If you take buybacks out of the market (the last 10,000-point gain in the Dow were essentially all corporate buybacks), we may not see a 20X earnings multiple again for another generation. Individuals were net sellers of stock for those two years. We only reached those extreme highs because of buybacks, so you take those out of the equation and it's going to get a lot harder to get back to the super inflated share prices like we had in January.

Q: How long before an Italian bank collapses, and will they need a bailout?

A: I don’t think they will get a collapse; I think they will be bailed out inside Italy and won’t need all of Europe to do this. But the focus isn't on Europe right now, it's on the US.

Q: Do you think this virus is really subsiding in China based on their past history of dishonest reporting?

A: Yes, that is a risk, and that's why people aren’t betting the ranch right now—just because China is reporting a flattening of cases. And China could be hit with a second wave if they relax their quarantine too soon.

Q: What's your opinion on how the Fed is doing and Steve Mnuchin in this crisis?

A: I think the Fed is doing everything they possibly can. I agree with all of their moves—this is an all-hands-on-deck moment where you have to do everything you can to get the economy going. Notice it’s Steve Mnuchin doing all the negotiating, not the president, because nobody will talk to him. For a start, he may be a Corona carrier among other things, and you’re not seeing a lot of social distancing in these press conferences they are holding. About which 50% of the information they give out is incorrect, and that's the 50% coming from Donald Trump.

Q: What do you think about no debt and no pension liability?

A: That’s why Tech has been leading the upside for the last 10 years and will lead for the next 10. You can really narrow the market down to a dozen stocks and just focus on those and forget about everything else. They have no net debt or net pension fund liabilities.

Q: Why have we not heard from Warren Buffet?

A: I'm sure negotiations are going on all over the place regarding obtaining massive stakes in large trophy companies that he likes, such as airlines and banks. So that will be one of the market bottom indicators that I mentioned a couple of days ago in my letter on “Ten Signs of a Market is Bottoming.”

Q: What’s the outlook for gold?

A: Up. We just had to get the financial crisis element out of this before we could go back into gold, so I would be looking to buy SPDR Gold Shares ETF (GLD), the gold miners like Barrick Gold (GOLD) and Newmont Mining (NEM), the Van Eck Vectors Gold Miners ETF (GDX), and the 2X long ProShares Gold ETF (UGL).

Q: Does the Fed backstop give you any confidence in the bond market?

A: Yes, it does. I think we finally may be getting to the natural level of the market, which is around an 80-basis point yield. Let’s see how long we can go without any 50-point gyrations.

Q: Do you foresee a depression?

A: We are in a depression now. We could hit a 20% unemployment rate. The worst we saw during the Great Depression was 25%. But it will be a very short and sharp one, not a 12-year slog like we saw during the 1930s.

Good Luck and Good Trading and stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

It’s Been a Tough Month

https://www.madhedgefundtrader.com/wp-content/uploads/2019/04/john-thomas-3.png391522Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-03-27 06:02:112020-05-11 14:48:11March 25, 2020 - Biweekly Strategy Webinar Q&A

Mass layoffs are on the horizon, thanks to the tech market slowdown sapping vitality for risk in the IPO market, and the widening contagion stemming from the coronavirus.

At a moment in Silicon Valley’s history where the market is rethinking its appetite for risk, it is customary for the loftiest and hottest growth names to drop the most in times like this.

For instance, Tesla (TSLA) was rocked by 32% and ride-hailing app Uber (UBER) gave up 25% in an epic downturn.

In general, tech that isn’t integral to the intricate global supply chain will also be penalized because of cratering overall business demand.

The vacuum of demand isn’t applied to only digital products but most others, as the world literally becomes a walled garden of self-quarantine areas.

The odds are still high that this global phenomenon squeaks by, but the far reach of the virus worries even experts and making crucial decisions on how to cut losses is becoming a pressing and imminent issue.

Airlines have been first to announce a potential readjustment to staff numbers such as Finland’s flagship airline Finn Air, but mass layoffs will start to trickle in from Silicon Valley.

Front-running the layoff parade was online travel tech company Expedia (EXPE) who expects to say adiós to 3,000 employees and network infrastructure company Cisco (CSCO) who announced restructuring plans because they expect revenue to fall between 1.5%-3.5% in Fiscal 2020.

I have been unwavering in my core thesis that tech procuring revenue from Mainland China is nothing more than a short-term Faustian bargain, and now the downsides of that bargain are finally appearing and frankly uncontainable.

The viral coronavirus is escalating on the heels of a new round of layoffs from Silicon Valley’s startups who just don’t know how to make money such as robot pizza startup Zume and car-sharing company Getaround who slashed more than 500 jobs.

Online DNA testing company 23andMe, logistics startup Flexport, Firefox internet browser Mozilla and social platform Quora restructured staff as well.

The “disruptors” are finally getting disrupted out of existence because of a sudden referendum on the health of balance sheets.

The situation turned ugly just before the coronavirus and this health crisis just adds fuel on the fire.

In total, more than 30 startups have cut over 8,000 jobs over the past four months with aggressive venture capital investments pulling back significantly.

The latest to flop at the starting line was Casper Sleep (CSPR) who marketed themselves as the “Nike of sleep” only because they sell online mattresses.

Mr. Market is purging these marginal businesses that over-promise, over-hype, and under-deliver.

The IPO pricing was underwhelming with Casper taking down the price range to the point where it went public at over $13.

The stock is now at $8.

No doubt that some of this negative sentiment was stoked by office-sharing company WeWork, who had an epic fall from grace and cut its valuation by 80% late last year while permanently shelving an IPO.

Now the coronavirus is on the verge of scoring the empty net goal as companies go into full-blown crisis mode.

SoftBank bet two ranches on Uber and WeWork, then poured money into Colombian delivery startup Rappi and Indian hotel startup Oyo.

All have sputtered with mass firings recently.

Poor investment decisions led SoftBank to report a $2 billion operating loss in the last quarter of 2019 from their venture capitalist arm named the Vision Fund.

After Nasdaq flourished in a memorable 10-year run post the financial crisis, flip the parabola upside down and markets are tanking with many experts already contrasting the coronavirus sell-off to the dot-com bust of 2001.

Irrational optimism is part of the DNA of San Francisco.

Entrepreneurs are quietly preparing to change the world, but the climate has soured so quickly that many investors believe many of these current entrepreneurs are unlucky.

The rules of the game deem unprofitable models temporarily obsolete in the current market environment.

In the land where spending money in uneconomic ways is a time-honored tradition, turning to more “responsible” models is gut-check time.

Talent is forgoing chances to enter the start-up world too, instead opting for big box corporates who provide a lower ceiling but higher salary and benefits.

Café X, which operated robot coffee shops and raised $14.5 million in venture funding, fired its own robots and closed three stores in San Francisco recently.

The brightest stars of the IPO pipelines might be able to go public this year, but at a cut-rate price which is a tough pill to swallow for Airbnb and online delivery platform DoorDash.

With no new blood going live on the public tech markets, we focus on the ones already there and recent news is alarming.

Apple whose 42 stores in China have been closed since January and Foxconn, which produces Apple products, are running at around 30%-40% capacity, then it’s ring-the-alarm time.

The most likely scenario is that big tech will need to write off this quarter until the public health crisis improves setting up a bullish second half of 2020.

Even that could get stopped in its tracks.

The only silver lining is that the run-up in shares in January means that the best of tech has only returned one month of share appreciation, but for the weaker companies, they aren’t afforded those types of luxuries in malicious trading conditions and have returned 4-6 months of share appreciation already.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-03-02 04:02:312020-05-11 13:16:35Tech's Big Corona Hit

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-02-14 04:04:392020-02-13 17:36:49February 14, 2020

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.