Global Market Comments

May 15, 2018

Fiat Lux

Featured Trade:

(FRIDAY, JUNE 15, 2018, DENVER, CO, GLOBAL STRATEGY LUNCHEON)

(GET READY FOR THE COMING GOLDEN AGE),

(SPY), (INDU), (FXE), (FXY), (UNG), (EEM), (USO),

(TLT), (NSANY), (TSLA)

Global Market Comments

May 15, 2018

Fiat Lux

Featured Trade:

(FRIDAY, JUNE 15, 2018, DENVER, CO, GLOBAL STRATEGY LUNCHEON)

(GET READY FOR THE COMING GOLDEN AGE),

(SPY), (INDU), (FXE), (FXY), (UNG), (EEM), (USO),

(TLT), (NSANY), (TSLA)

I believe that the global economy is setting up for a new golden age reminiscent of the one the United States enjoyed during the 1950s, and which I still remember fondly.

This is not some pie in the sky prediction. It simply assumes a continuation of existing trends in demographics, technology, politics, and economics. The implications for your investment portfolio will be huge.

What I call "intergenerational arbitrage" will be the principal impetus. The main reason that we are now enduring two "lost decades" of economic growth is that 80 million baby boomers are retiring to be followed by only 65 million "Gen Xers."

When the majority of the population is in retirement mode, it means that there are fewer buyers of real estate, home appliances, and "RISK ON" assets such as equities, and more buyers of assisted living facilities, health care, and "RISK OFF" assets such as bonds.

The net result of this is slower economic growth, higher budget deficits, a weak currency, and registered investment advisors who have distilled their practices down to only municipal bond sales.

Fast forward six years when the reverse happens and the baby boomers are out of the economy, worried about whether their diapers get changed on time or if their favorite flavor of Ensure is in stock at the nursing home.

That is when you have 65 million Gen Xers being chased by 85 million of the "millennial" generation trying to buy their assets.

By then we will not have built new homes in appreciable numbers for 20 years and a severe scarcity of housing hits. Residential real estate prices will soar. Labor shortages will force wage hikes.

The middle-class standard of living will reverse a then 40-year decline. Annual GDP growth will return from the current subdued 2% rate to near the torrid 4% seen during the 1990s.

The stock market rockets in this scenario. Share prices may rise very gradually for the rest of the teens as long as tepid 2% growth persists. A 5% annual gain takes the Dow to 28,000 by 2019.

After that, after a brief dip, we could see the same fourfold return we saw during the Clinton administration, taking the Dow to 100,000 by 2030. If I'm wrong, it will hit 200,000 instead.

Emerging stock markets (EEM) with much higher growth rates do far better.

This is not just a demographic story. The next 20 years should bring a fundamental restructuring of our energy infrastructure as well.

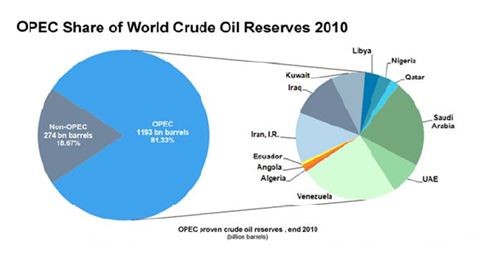

The 100-year supply of natural gas (UNG) we have recently discovered through the new "fracking" technology will finally make it to end users, replacing coal (KOL) and oil (USO). Fracking applied to oilfields is also unlocking vast new supplies.

Since 1995, the United States Geological Survey estimate of recoverable reserves has ballooned from 150 million barrels to 8 billion. OPEC's share of global reserves is collapsing.

This is all happening while automobile efficiencies are rapidly improving and the use of public transportation soars.

Mileage for the average U.S. car has jumped from 23 to 24.7 miles per gallon in the past couple of years, and the administration is targeting 50 mpg by 2025. Total gasoline consumption is now at a five-year low.

Alternative energy technologies will also contribute in an important way in states such as California, accounting for 30% of total electric power generation by 2020, and 50% by 2030.

I now have an all-electric garage, with a Nissan Leaf (NSANY) for local errands and a Tesla Model S-1 (TSLA) for longer trips, allowing me to disappear from the gasoline market completely. Millions will follow. The net result of all of this is lower energy prices for everyone.

It will also flip the U.S. from a net importer to an exporter of energy, with hugely positive implications for America's balance of payments. Eliminating our largest import and adding an important export is very dollar bullish for the long term.

That sets up a multiyear short for the world's big energy consuming currencies, especially the Japanese yen (FXY) and the Euro (FXE). A strong greenback further reinforces the bull case for stocks.

Accelerating technology will bring another continuing positive. Of course, it's great to have new toys to play with on the weekends, send out Facebook photos to the family, and edit your own home videos.

But at the enterprise level this is enabling speedy improvements in productivity that are filtering down to every business in the U.S., lowering costs everywhere.

This is why corporate earnings have been outperforming the economy as a whole by a large margin.

Profit margins are at an all-time high. Living near booming Silicon Valley, I can tell you that there are thousands of new technologies and business models that you have never heard of under development.

When the winners emerge, they will have a big cross-leveraged effect on economy.

New health care breakthroughs will make serious disease a thing of the past, which are also being spearheaded in the San Francisco Bay area.

This is because the Golden State thumbed its nose at the federal government 10 years ago when the stem cell research ban was implemented. It raised $3 billion through a bond issue to fund its own research, even though it couldn't afford it.

I tell my kids they will never be afflicted by my maladies. When they get cancer in 20 years they will just go down to Wal-Mart and buy a bottle of cancer pills for $5, and it will be gone by Friday.

What is this worth to the global economy? Oh, about $2 trillion a year, or 4% of GDP. Who is overwhelmingly in the driver's seat on these innovations? The USA.

There is a political element to the new golden age as well. Gridlock in Washington can't last forever. Eventually, one side or another will prevail with a clear majority.

This will allow the government to push through needed long-term structural reforms, the solution of which everyone agrees on now, but for which nobody wants to be blamed.

That means raising the retirement age from 66 to 70 where it belongs and means-testing recipients. Billionaires don't need the maximum $30,156 annual supplement. Nor do I.

The ending of our foreign wars and the elimination of extravagant unneeded weapons systems cuts defense spending from $800 billion a year to $400 billion, or back to the 2000, pre-9/11 level. Guess what happens when we cut defense spending? So does everyone else.

I can tell you from personal experience that staying friendly with someone is far cheaper than blowing them up.

A Pax Americana would ensue.

That means China will have to defend its own oil supply, instead of relying on us to do it for them. That's why they have recently bought a second used aircraft carrier. The Middle East is now their headache.

The national debt then comes under control, and we don't end up like Greece.

The long-awaited Treasury bond (TLT) crash never happens. The Fed has already told us as much by indicating that the Federal Reserve will only raise interest rates at an infinitesimally slow rate of 25 basis points a quarter.

Sure, this is all very long-term, over-the-horizon stuff. You can expect the financial markets to start discounting a few years hence, even though the main drivers won't kick in for another decade.

But some individual industries and companies will start to discount this rosy scenario now.

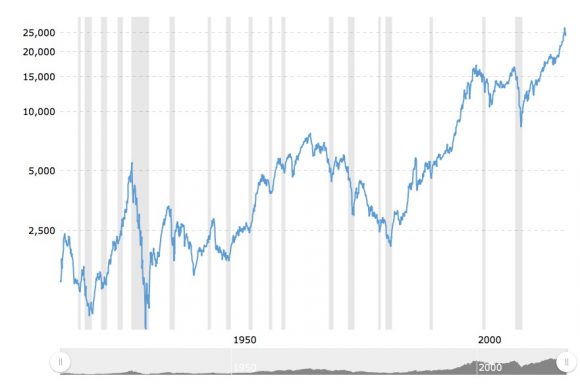

Perhaps this is what the nonstop rally in stocks since 2009 has been trying to tell us.

Dow Average 1908-2018

Another American Golden Age is Coming

Given that my friend, former Texas Governor, Rick Perry, was nominated for the position of Secretary of Energy yesterday, I thought I would recount a dinner I had with him.

The irony is great since Rick promised to close down the agency while campaigning for president in 2012.

It confirms my suspicion that many of the people Trump is appointing have the mission to destroy the agencies they will head.

As a precondition to joining a dinner with the former Texas governor, I had to promise a few things.

I was not allowed to bring up the fact that he shoots coyotes while jogging. I couldn?t mention statistics proving that 70% of the jobs created in his state during his 12-year tenure as governor were government, not private.

Having agreed to all of that, I was told, ?Sure, come along, we?d love to hear your questions and your insights.?

Perry was making his 12th?visit to the Golden State in the past two years to convince local companies, plagued with onerous taxes, stringent regulations and high operating costs, to pull up stakes and move camp to the Lone Star State.

When I first shook hands with the governor, I was surprised at how short he was. But then he wasn?t wearing the three-inch heeled cowboy boots that normally elevated him at home.

Then I mentioned my secret words: ?Go Aggies.? He recoiled.

?How did you know?? he demanded.

I told him that during the early 1970s, I drove my sister from California to his home state so she could attend Texas A&M University. Perry was a cadet then, and I speculated that they had probably dated.

He answered, ?Nah, I didn?t play around much in those days.?

Probably not.

But after that, he melted, only engaging me in serious conversation, while sticking to canned, stock answers to questions from everyone else.

I was Rick Perry?s new best friend.

As he spoke, I realized that he was much more reasonable in his views than when appealing to his ultra conservative base back home. That is simply the mark of a savvy and successful politician.

Perry said that the country needs both states to lead change and succeed, and that he rooted for California to do well.

The governor was still basking in the glow of Toyota?s recent announcement that it was moving 3,000 jobs from Long Beach, California to Texas.?

It has been a controversial win for him, as his state is paying $10,000 in subsidies per person to lure the white-collar work force.

I spoke to Toyota USA CEO, Jim Lentz, about this recently. He said the real reason had to do with working in the same time zone as the company?s large manufacturing facilities in Kentucky and Tennessee.

A lower cost of living, cheaper rents, and discount labor costs were also issues. Lower taxes were at the bottom of a list of ten priorities.

Past experience has shown that most departing workers, fleeing from California, return after three years. It seems the summer heat and humidity kill them.?

Thus chastened, they are more than willing to pay a premium for the lifestyle here, despite the higher taxes and earthquakes.

Perry says the US needs an ?all of the above? solution to its energy problems. It is not a good idea to be dependent on foreign energy sources, especially from unstable countries.

Despite its stereotype as an oil-based economy, Texas was now the top producer of wind power in the country. The installed base there now exceeds 12 gigawatts, making it the fifth largest in the world.

My friend, T. Boone Pickens, has been a major investor in wind power generation there.

An aggressive approvals process made possible the construction of long distance transmission lines needed to send it to other states and eventually to California itself, thus creating a national market for wind power.

The governor says that Texas will become a major exporter for liquefied natural gas within the next two years. Cheniere Energy (LNG), the front-runner in the field, has been a favorite recommendation of mine for the past five years, and? Trade Alert followers have chased the shares up from $6 to $70.

Despite the controversy over fracking wells polluting fresh water supplies, Perry says there has not been a single incidence of this occurring in Texas. This is no doubt a result of the state?s ferocious regulation of the energy industry, of which I, myself, have no small amount of experience.

Thanks in part to new federal regulations, air pollution has fallen dramatically in Texas. Ozone emissions have dropped by 23% since 2000, while nitrous oxides are off by 57%.

These, and other measures have enabled the US to cut its dependence on foreign oil imports from 33% to 15% since 2000. During the same period, natural gas production, which produces half the carbon of oil based fuels, has soared by 57%.

At that point, another guest raised his hand and asked his stance on gay rights. Perry opined that sexuality was a choice that could be controlled, and that gay marriage would never get his support. An audible hiss was heard in the roomwhich Perry stonily ignored.

That invited the question about the legalization of marijuana. He simply said that it would never be legalized in his state, and, ?If people want to get high, they can go to Colorado.?

Finally, a woman at the table asked about reproductive rights. When Perry said that he was proud to sign a Texas law limiting termination to the first five months of pregnancy, murmurs were heard. The law is not expected to survive a pending challenge at the Supreme Court.

Another attendee queried his view of Hillary Clinton. I braced myself. He then surprised me by saying that he thought she was ?a very capable Secretary of State and a great public servant.?

That spoke volumes to me. It meant that with access to all his private polling data, Rick Perry thought that Hillary would win the 2016 presidential election. As the astute politician that he is, Perry doesn?t want to burn his bridges.

Perry likes to tell people that he is probably the last governor who used an outhouse on a dry cotton farm near Abilene, West Texas.

He became an Eagle Scout and I confirmed this with the secret scout handshake.

He earned a degree in animal science at Texas A&M where he was also a Corps Cadet and a yell leader. His first part-time job was as a door-to-door salesman. When he graduated, he joined the Air Force and became a C-130 pilot.

Perry originally started in politics as a Democrat, getting elected to the Texas House of Representatives in 1984.

He worked on Al Gore?s presidential campaign in 1988. This was back when Southern Democrats were more conservative than the right wing of the Republican Party.Perry became a Republican in 1989.

He moved up to the governorship in 2000, when sitting governor George W. Bush was elected president. Perry has been reelected three times, making him the longest tenured Texas governor in history.

Perry said that his time spent as the front runner in the 2012 presidential election ?were the three most exhausting hours of my life.?

He then repeated his ?Oops? moment when, if elected, he couldn?t remember the third government department he would close (it was the Department of Commerce, in addition to Energy and Education). That was probably to head off someone else bringing it up first.

I told the governor I knew two facts about our respective states which I bet he didn?t know. He asked what they were.

I responded that California and Texas were the only two states that had been independent countries before joining the Union. California had been the Bear Flag Republic for six months until mid 1848, while the Republic of Texas stood on its own for a decade, until 1846. Texans have been regretting joining the Union ever since.

Today, the two states make up 19.1% of America?s GDP, and 20.4% of its population.

The other mystery fact was that while Texas was independent, it maintained an embassy in London, England on St. James Street.Today, the space is occupied by a pub and is across the street from the Ritz Hotel and next door to my old office at The Economist?magazine headquarters. Perry said he?d check it out on his next visit there.

As the dinner wound down, I asked the governor if he had ever driven a Tesla Model S-1. He said he hadn?t. I asked if he would like to because my own high performance model was conveniently parked out front. He said he?d love to.

At that point, the plain clothed Texas Rangers who accompany him as bodyguards noticeably tensed up.

I have some experience providing quick tutorials for the uninitiated on how to drive this incredible electric car from the future. My chassis number is 125 out of a fleet of 45,000 and is one of the oldest S-1s around.

Newcomers invariably underestimate the car?s power and acceleration, which works out to about 450 horsepower in the carbon world. This can be unexpectedly dangerous for newbies.

With some careful coaching, Perry gingerly drove the car a few times around San Francisco?s Huntington Park, atop Nob Hill with two nervous, but heavily armed, Rangers in the back seat.

When we carefully turned back onto California Street and came to a stop in front of the Mark Hopkins Hotel, Perry pronounced the vehicle ?a marvelous piece of technology?.

With that, Perry invited me to visit the governor?s mansion the next time I visited Austin, Texas.

I said I?d be honored, and silently drove my Tesla off into the night, thus christened by a true Texan.

You Want Me to Do What?

I am once again writing this report from a first class sleeping cabin on Amtrak?s California Zephyr.

By day, I have two comfortable seats facing each other next to a panoramic window. At night, they fold into bunk beds, a single and a double. There is a shower, but only Houdini could get in and out of it.

I am not Houdini, so I go downstairs to use the larger public showers.

We are now pulling away from Chicago?s Union Station, leaving its hurried commuters, buskers, panhandlers, and majestic great halls behind. I love this building as a monument to American accomplishment.

I am headed for Emeryville, California, just across the bay from San Francisco. That gives me only 56 hours to complete this report.

I tip my porter, Raymond, $100 in advance to make sure everything goes well during the long adventure, and to keep me up to date with the onboard gossip.

The rolling and pitching of the car is causing my fingers to dance all over the keyboard. Spellchecker can catch most of the mistakes, but not all of them.

Thank goodness for small algorithms.

As both broadband and cell phone coverage are unavailable along most of the route, I have to rely on frenzied searches during stops at major stations along the way to chase down data points.

You know those cool maps in the Verizon stores that show the vast coverage of their cell phone networks? They are complete BS.

Who knew that 95% of America is off the grid? That explains a lot about our country today. I have posted many of my better photos from the trip below, although there is only so much you can do from a moving train and an iPhone 6.

After making the rounds with strategists, portfolio managers, and hedge fund traders, I can confirm that 2015 was one of the toughest to trade for careers lasting 30, 40, or 50 years. Even the stay-at-home index players had their heads handed to them.

With the Dow gaining 3.1% in 2015, and S&P 500 almost dead unchanged, this was a year of endless frustration. Volatility fell to the floor, staying at a monotonous 12% for eight boring consecutive months before spiking repeatedly many times to as high as 52%. Most hedge funds lagged the index by miles.

My Trade Alert Service, hauled in an astounding 38.8% profit, at the high was up 48.7%, and has become the talk of the hedge fund industry.

If you think I spend too much time absorbing conspiracy theories from the Internet, let me give you a list of the challenges I see financial markets facing in the coming year:

The Four Key Variables for 2016

1) Will the Fed raise interest rates more or not?

2) Will China?s emerging economy see a hard or soft landing?

3) Will Japanese and European quantitative easing increase, or remain the same?

4) Will oil bottom and stay low, or bounce hard?

Here are your answers to the above: no, soft, more later, bounce hard later.

There you go! That?s all the research you have to do for the coming year. Everything else is a piece of cake.

The Ten Highlights of 2015

1) Stocks will finish higher in 2016, almost certainly more than the previous year, somewhere in the 5% range and 7% with dividends. Cheap energy, a recovering global economy, and 2-3% GDP growth, will be the drivers. However, this year we have a headwind of rising interest rates and falling multiples.

2) Expect stocks to take a 15% dive. That gives us a -15% to +5% trading range for the year. Volatility will remain permanently higher, with several large spikes up. That means you are going to have to pedal harder to earn your crust of bread in 2016.

3) The Treasury bond market will modestly grind down, anticipating the next 25 basis point rate rise from the Federal Reserve, and then the next one after that.

4) The yen will lose another 5% against the dollar.

5) The Euro will fall another 5%, doing its best to hit parity with the greenback, with the assistance of beleaguered continental governments.

6) Oil stays in a $30-$60 range, showering the economy with hundreds of billions of dollars worth of de facto tax cuts.

7) Gold finally bottoms at $1,000 after one more final flush, then rallies $250. (My jeweler was right, again).

8) Commodities finally bottom out, thanks to new found strength in the global economy, and begin a modest recovery.

9) Residential real estate has made its big recovery, and will grind up slowly from here for years.

10) The 2016 presidential election will eat up immense amounts of media and research time, but will have absolutely no impact on financial markets. Give your money to charity instead.

The Thumbnail Portfolio

Equities - Long. A rising but high volatility year takes the S&P 500 up to 2,200. Technology, biotech, energy, solar, consumer discretionary, and financials lead. Energy should find its bottom, but later than sooner.

Bonds - Short. Down for the entire year, but not by much, with long periods of stagnation.

Foreign Currencies - Short. The US dollar maintains its bull trend, especially against the Yen and the Euro, but won't gain nearly as much as in 2015.

Commodities - Long. A China recovery takes them up eventually.

Precious Metals - Buy as close to $1,000 as you can. We are overdue for a trading rally.

Agriculture - Long. El Nino in the north and droughts in Latin American should add up to higher prices.

Real estate - Long. Multifamily up, commercial up, single family homes up small.

1) The Economy - Fortress America

I think real US economic growth will come in at the 2.5%-3% range.

With a generational demographic drag continuing for five more years, don?t expect more than that. Big spenders, those in the 46-50 age group, don?t return in larger numbers until 2022.

But this negative will be offset by a plethora of positives, like hyper-accelerating technology, global expansion, and the lingering effects of the Fed?s massive five year quantitative easing.

US corporate profits will keep pushing to new all time highs. But this year we won?t be held back by the collapsing economies of Europe, China, and Japan, which subtracted about 0.5% from American economic growth, nor weak energy.

US Corporate earnings will probably come in at $130 a share for the S&P 500, a gain of 10% over the previous year. During the last six years, we have seen the most dramatic increase in earnings in history, taking them to all-time highs.

Technology and dramatically lower energy costs are the principal sources of profit increases, which will continue their inexorable improvements. Think of more machines and software replacing people.

You know all of those hundreds of billions raised from technology IPO?s in 2015? Most of that is getting plowed right back into new start ups, increasing the rate of technology improvements even further, and the productivity gains that come with it.

We no longer have the free lunch of zero interest rates. But the cost of money will rise so slowly that it will barely impact profits. Deflation is here to stay. Watch the headline jobless rate fall below 5% to a full employment economy.

Keep close tabs on the weekly jobless claims that come out at 8:30 AM Eastern every Thursday for a good read as to whether the financial markets will head in a ?RISK ON? or ?RISK OFF? direction.

A Rocky Mountain Moose Family

A Rocky Mountain Moose Family2) Equities (SPX), (QQQ), (AAPL), (XLF), (BAC), (EEM),(EWZ), (RSX), (PIN), (FXI), (TUR), (EWY), (EWT), (IDX)

For the first time in seven years, earnings multiples are going to fall, but not by much. That is the only possible outcome in a world with rising interest rates, however modestly.

If multiples fall by 5%, from the current 18X to 17.1X, profits increase by 10%, and you throw in a 2% dividend, you should net out a 7% return by the end of the year.

S&P 500 earnings fell by 6% in 2015, but take out oil and they grew by 5.6%. In 2016, energy will be a lesser drag, or not at all. That makes my 10% target doable.

That is not much of a return with which to take on a lot of risk. But remember, in a near zero interest rate world, there is nothing else to buy.

This is not an outrageous expectation, given the 10-22 earnings multiple range that we have enjoyed during the last 30 years.

The market currently trades around fair value, and no market in history ever peaked out here. An overshoot to the upside, often a big one, is mandatory. Yet, that is years off.

After all, my friend, Janet Yellen, is paying you to buy stock with cheap money, so why not? Borrowing money at close to zero and investing in 2% dividend paying stocks has become the world?s largest carry trade.

Rising interest rates will have one additional worrying impact on stock prices. They will pare back mergers and acquisitions and corporate buy backs in 2016.

Together these were the sources of all new net buying of stocks in 2015, some $5.5 trillion worth. Call it financial engineering, but the market loves it.

Although energy looks terrible now, it could well be the top-performing sector by the end of the year, to be followed by commodities.

Certainly, every hedge fund and activist investor out there is undergoing a crash course on oil fundamentals. After a 13-year expansion of leverage in the industry, it is ripe for a cleanout.

Solar stocks will continue on a tear, now that the 30% federal investment tax subsidy has been extended by five more years. Look at Solar City (SCTY), First Solar (FSLR), and the solar basket ETF (TAN). Revenues are rocketing and costs are falling.

After spending a year in the penalty box, look for small cap stocks to outperform. These are the biggest beneficiaries of cheap energy and low interest rates.

Share prices will deliver anything but a straight-line move. Expect a couple more 10% plus corrections in 2015, and for the Volatility Index (VIX) to revisit $30 multiple times. The higher prices rise, the more common these will become.

Frozen Headwaters of the Colorado River

Frozen Headwaters of the Colorado River 3) Bonds ?(TLT), (TBT), (JNK), (PHB), (HYG), (PCY), (MUB), (HCP), (KMP), (LINE)

Amtrak needs to fill every seat in the dining car, so you never know who you will get paired with for breakfast, lunch, and dinner.

There was the Vietnam vet Phantom jet pilot who now refused to fly because he was treated so badly at airports. A young couple desperate to get out of Omaha could only afford seats as far as Salt Lake City, sitting up all night. I paid for their breakfast.

A retired British couple was circumnavigating the entire US in a month on a ?See America Pass.? Mennonites returning home by train because their religion forbade airplanes.

I have to confess that I am leaning towards the ?one and done? school of thought with regards to the Fed?s interest rate policy. We may see a second 25 basis point rise in June, but only if the economy takes off like a rocket and international concerns disappear, an unlikely probability.

If you told me that US GDP growth was 2.5%, unemployment was at a ten year low at 5.0%, and energy prices had just plunged by 68%, I would have pegged the ten-year Treasury bond yield at 6.0%. Yet here we are at 2.25%.

We clearly are seeing a brave new world.

Global QE added to a US profit glut has created more money than the fixed income markets can absorb.

Virtually every hedge fund manager and institutional investor got bonds wrong last year, expecting rates to rise. I was among them, but that is no excuse.

Fixed income turned out to be a winner for me in 2015, as I sold short every bond price spike from the summer onward. It worked like a charm.

You might as well take your traditional economic books and throw them in the trash. Apologies to John Maynard Keynes, John Kenneth Galbraith, and Paul Samuelson.

The reasons for the debacle are myriad, but global deflation is the big one. With ten year German bunds yielding a paltry 62 basis points, and Japanese bonds paying a paltry 26 basis points, US Treasuries are looking like a steal.

To this, you can add the greater institutional bond holding requirements of Dodd-Frank, a balancing US budget deficit, a virile US dollar, the commodity price collapse, and an enormous embedded preference for investors to keep buying whatever worked yesterday.

For more depth on the perennial strength of bonds, please click here for ?Ten Reasons Why I?m Wrong on Bonds?.

Bond investors today get an unbelievable bad deal. If they hang on to the longer maturities, they will get back only 80 cents worth of purchasing power at maturity for every dollar they invest a decade down the road.

But institutions and individuals will grudgingly lock in these appalling returns because they believe that the potential losses in any other asset class will be worse.

The problem is that driving eighty miles per hour while only looking in the rear view mirror can be hazardous to your financial health.

While much of the current political debate centers around excessive government borrowing, the markets are telling us the exact opposite.

A 2% handle on the ten-year yield is proof to me that there is a Treasury bond shortage, and that the government is not borrowing too much money, but not enough.

There is another factor supporting bonds that no one is looking at. The concentration of wealth with the 1% has a side effect of pouring money into bonds and keeping it there. Their goal is asset protection and nothing else.

These people never sell for tax reasons, so the money stays there for generations. It is not recycled into the rest of the economy, as conservative economists insist. As this class controls the bulk of investable assets, this forestalls any real bond market crash, at lest for the near term.

So what will 2016 bring us? I think that the erroneous forecast of higher yields I made last year will finally occur this year, and we will start to chip away at the bond market bubble?s granite edifice.

I am not looking for a free fall in price and a spike up in rates, just a move to a new higher trading range.

We could ratchet back up to a 3% yield, but not much higher than that. This would enable the inverse Treasury bond bear ETF (TBT) to reverse its dismal 2015 performance, taking it from $46 back up to $60.

You might have to wait for your grandchildren to start trading before we see a return of 12% Treasuries, last seen in the early eighties. I probably won?t live that long.

Reaching for yield suddenly went out of fashion for many investors, which is typical at market tops. As a result, junk bonds (JNK) and (HYG), REITS (HCP), and master limited partnerships (AMLP) are showing their first value in five years.

There is also emerging market sovereign debt to consider (PCY). If oil and commodities finally bottom, these high yielding bonds should take off on a tear.

This asset class was hammered last year, so we are now facing a rare entry point.

There is a good case for sticking with munis. No matter what anyone says, taxes are going up, and when they do, this will increase tax-free muni values.

The collapse of the junk bond market suddenly made credit quality a big deal last year. What is better than lending to the government, unless you happen to live in Puerto Rico or Illinois.

So if you hate paying taxes, go ahead and buy this exempt paper, but only with the expectation of holding it to maturity. Liquidity could get pretty thin along the way, and mark to markets could be shocking.

Be sure to consult with a local financial advisor to max out the state, county, and city tax benefits.

One question I always get asked at lunches, conferences, and lectures is what is going to happen to the budget deficit?

The short answer is that it disappears in 2018 with no change in current law, thanks to steady growth in tax revenues and no big new wars.

And Social Security? It will be fully funded by 2030, thanks to a huge demographic tailwind provided by the addition of 86 million Millennials to the tax rolls.

A bump up in US GDP growth from 2% to 4% during the 2020?s will also be a huge help, again, provided we don?t start any more wars.

It looks like I am going to be able to collect after all.

A Visit to the 19th Century

A Visit to the 19th Century4) Foreign Currencies (FXE), (EUO), (FXC), (FXA), (YCS), (FXY), (CYB)

Without much movement in interest rates in 2016, you can expect the same for foreign currencies.

Last year, we saw never ending expectations of aggressive quantitative easing by foreign central banks, which never really showed. What we did get, was always disappointing.

The decade long bull market in the greenback continues, but not by much. You can forget about those dramatic double digit gains the dollar made against the Euro at the beginning of last year, which we absolutely nailed.

The fundamental play for the Japanese yen is still from the short side. But don?t expect movement until we see another new leg of quantitative easing from the Bank of Japan. It could be a long wait.

The problems in the Land of the Rising Sun are almost too numerous to count: the world?s highest debt to GDP ratio, a horrific demographic problem, flagging export competitiveness against neighboring China and South Korea, and the world?s lowest developed country economic growth rate.

The dramatic sell off we saw in the Japanese currency since December, 2012 is the beginning of what I believe will be a multi decade, move down. Look for ?130 to the dollar sometime in 2016, and ?150 further down the road.

I have many friends in Japan looking for an overshoot to ?200. Take every 3% pullback in the greenback as a gift to sell again.

With the US having the world?s strongest major economy, its central bank is, therefore, most likely to continue raising rates the fastest.

That translates into a strong dollar, as interest rate differentials are far and away the biggest decider of the direction in currencies. So the dollar will remain strong against the Australian and Canadian dollars as well.

For a sleeper, use the next plunge in emerging markets to buy the Chinese Yuan ETF (CYB) for your back book. Now that the Yuan is an IMF reserve currency, it has attained new respectability.

But don?t expect more than single digit returns. The Middle Kingdom will move heaven and earth in order to keep its appreciation modest to maintain their crucial export competitiveness.

5) Commodities (FCX), (VALE), (MOO), (DBA), (MOS), (MON), (AGU), (POT), (PHO), (FIW), (CORN), (WEAT), (SOYB), (JJG)

There isn?t a strategist out there not giving thanks for not loading up on commodities in 2015, the preeminent investment disaster of the year. Those who did are now looking for jobs on Craig?s List.

It was another year of overwhelming supply meeting flagging demand, both in Europe and Asia. Blame China, the one big swing factor in the global commodity.

The Middle Kingdom is currently changing drivers of its economy, from foreign exports to domestic consumption. This will be a multi decade process, and they have $3.5 trillion in reserves to finance it.

It will still demand prodigious amounts of imported commodities, especially, oil, copper, iron ore, and coal, all of which we sell. But not as much as in the past. This trend ran head on into a decade long expansion of capacity by the industry.

The derivative equity plays here, Freeport McMoRan (FCX) and Companhia Vale do Rio Doce (VALE), have all taken an absolute pasting.

The food commodities were certainly the asset class to forget about in 2015, as perfect weather conditions and over planting produced record crops for the second year in a row, demolishing prices. The associated equity plays took the swan dive with them.

Not even the arrival of one of the biggest El Nino events in history could bail them out.

However, the ags are still a tremendous long term Malthusian play. The harsh reality here is that the world is making people faster than the food to feed them, the global population jumping from 7 billion to 9 billion by 2050.

Half of that increase comes in countries unable to feed themselves today, largely in the Middle East. The idea here is to use any substantial weakness, as we are seeing now, to build long positions that will double again if global warming returns in the summer, or if the Chinese get hungry.

The easy entry points here are with the corn (CORN), wheat (WEAT), and soybean (SOYB) ETF?s. You can also play through (MOO) and (DBA), and the stocks Mosaic (MOS), Monsanto (MON), Potash (POT), and Agrium (AGU).

The grain ETF (JJG) is another handy fund. Though an unconventional commodity play, the impending shortage of water will make the energy crisis look like a cakewalk. You can participate in this most liquid of assets with the ETF?s (PHO) and (FIW).

Snow Angel on the Continental Divide

Snow Angel on the Continental Divide6) Energy (DIG), (RIG), (USO), (DUG), (DIG), (UNG), (USO), (OXY), (XLE), (X)

You are now an oil trader, even if you didn?t realize it. Yikes!

The short-term direction of the price of Texas tea will be the principal driver for the prices of all asset classes, as it was for the 2015.

The smartest thing I did in 2015 was to ignore the professional traders, who called the bottom in oil monthly, based on key technical levels.

Instead, I hung on every word uttered by my old drilling buddies in the Barnett Shale, who only saw endless supply.

Guess whom I?ll be paying attention to this year?

I expect oil to bottom in 2016, and then launch a ferocious short covering rally. But when and where is anyone?s guess.

If energy legends John Hamm, John Arnold, and T. Boone Pickens have no idea where the absolute low will be, who am I to second-guess them?

When that happens, a trillion dollars will pour out of the sidelines into this troubled sector. Energy shares should be top-performers in 2016.

That makes energy Master Limited Partnerships, now yielding 10%-15%, especially interesting in this low yield world. Since no one in the industry knows which issuers are going bankrupt, you have to take a basket approach and buy all of them.

The Alerian MLP ETF (AMLP) does this for you in an ETF format (click here for details). At its low this fund was down by 41% this year. The last printed annualized yield I saw was 10%. That kind of return will cover up a lot of sins.

Our train has moved over to a siding to permit a freight train to pass, as it has priority on the Amtrak system. Three Burlington Northern engines are heaving to pull over 100 black, brand new tank cars, each carrying 30,000 gallons of oil from the fracking fields in North Dakota.

There is another tank car train right behind it. No wonder Warren Buffet tap dances to work every day, as he owns the railroad.

Who knew that a new, younger Saudi king would ramp up production to once unimaginable levels and crush prices, turning the energy world upside down?

They aren?t targeting American frackers, who at 1 million barrels a day in a 92 million barrel a day demand world barely move the needle. Their goal is to destroy the economies of enemies Iran, Yemen, Russia, and of course ISIS, which need high prices to stay in business.

So far, so good.

Cheaper energy will bestow new found competitiveness on US companies that will enable them to claw back millions of jobs from China in dozens of industries.

At current prices, the energy savings works out to an eye popping $550 per American driver per year!

This will end our structural unemployment faster than demographic realities would otherwise permit.

We have a major new factor this year in considering the price of energy. The nuclear deal with Iran promises to add 500,000 to 1 million barrels a day to an already glutted global market. Iraq is ramping up production as well.

We are also seeing relentless improvements on the energy conservation front with more electric vehicles, high mileage conventional cars, and newly efficient building. Anyone of these inputs is miniscule on its own. But add them all together and you have a game changer.

Enjoy cheap oil while it lasts because it won?t last forever. American rig counts are already falling off a cliff and will eventually engineer a price recovery.

As is always the case, the cure for low prices is low prices. But we may never see $100/barrel crude again.

Add to your long term portfolio (DIG), Exxon Mobil (XOM), Cheniere Energy (LNG), the energy sector ETF (XLE), Conoco Phillips (COP), and Occidental Petroleum (OXY).

Skip natural gas (UNG) price plays and only go after volume plays, because the discovery of a new 100-year supply from ?fracking? and horizontal drilling in shale formations is going to overhang this subsector for a very long time.

It is a basic law of economics that cheaper prices bring greater demand and growing volumes, which have to be transported. However, major reforms are required in Washington before use of this molecule goes mainstream.

These could be your big trades of 2016, but expect to endure some pain first, nor to get much sleep at night.

7) Precious Metals (GLD), (DGP), (SLV), (PPTL), (PALL)

The train has added extra engines at Denver, so now we may begin the long laboring climb up the Eastern slope of the Rocky Mountains.

On a steep curve, we pass along an antiquated freight train of hopper cars filled with large boulders. The porter tells me this train is welded to the tracks to create a windbreak. Once, a gust howled out of the pass so swiftly that it blew a train over on to its side.

In the snow filled canyons we sight a family of three moose, a huge herd of elk, and another group of wild mustangs. The engineer informs us that a rare bald eagle is flying along the left side of the train. It?s a good omen for the coming year.

We also see countless abandoned 19th century gold mines and the broken down wooden trestles leading to them, relics of previous precious metals busts. So it is timely here to speak about precious metals.

As long as the world is clamoring for paper assets like stocks and bonds, gold is just another shiny rock. After all, who needs an insurance policy if you are going to live forever?

We have already broken $1,040 once, and a test of $1,000 seems in the cards before a turnaround ensues. There are more hedge fund redemptions and stop losses to go. The bear case has the barbarous relic plunging all the way down to $700.

But the long-term bull case is still there. Gold is not dead; it is just resting.

If you forgot to buy gold at $35, $300, or $800, another entry point is setting up for those who, so far, have missed the gravy train. The precious metals have to work off a severely, decade old overbought condition before we make substantial new highs.

Remember, this is the asset class that takes the escalator up and the elevator down, and sometimes the window.

If the institutional world devotes just 5% of their assets to a weighting in gold, and an emerging market central bank bidding war for gold reserves continues, it has to fly to at least $2,300, the inflation adjusted all-time high, or more.

This is why emerging market central banks step in as large buyers every time we probe lower prices. China and India emerged as major buyers of gold in the final quarter of 2015.

They were joined by Russia, which was looking for non-dollar investments to dodge US economic and banking sanctions.

For me, that pegs the range for 2016 at $1,000-$1,250. ETF players can look at the 1X (GLD) or the 2X leveraged gold (DGP).

I would also be using the next bout of weakness to pick up the high beta, more volatile precious metal, silver (SLV), which I think could hit $50 once more, and eventually $100.

What will be the metals to own in 2015? Palladium (PALL) and platinum (PPLT), which have their own auto related long term fundamentals working on their behalf, would be something to consider on a dip.

With US auto production at 18 million units a year and climbing, up from a 9 million low in 2009, any inventory problems will easily get sorted out.

Would You Believe This is a Blue State?

Would You Believe This is a Blue State?8) Real Estate (ITB)

The majestic snow covered Rocky Mountains are behind me. There is now a paucity of scenery, with the endless ocean of sagebrush and salt flats of Northern Nevada outside my window, so there is nothing else to do but write.

My apologies to readers in Wells, Elko, Battle Mountain, and Winnemucca, Nevada.

It is a route long traversed by roving banks of Indians, itinerant fur traders, the Pony Express, my own immigrant forebears in wagon trains, the transcontinental railroad, the Lincoln Highway, and finally US Interstate 80.

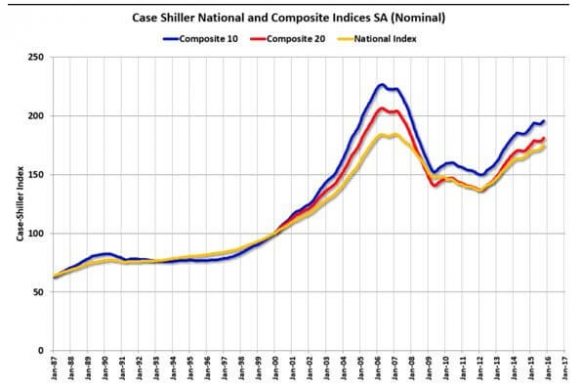

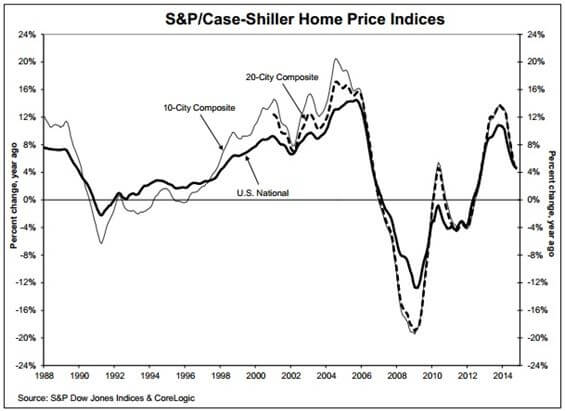

There is no doubt that there is a long-term recovery in real estate underway. We are probably 5 years into a 17-year run at the next peak in 2028.

But the big money has been made here over the past two years, with some red hot markets, like San Francisco, soaring. If you live within commuting distance of Apple (AAPL), Google (GOOG), or Facebook (FB) headquarters in California, you are looking at multiple offers, bidding wars, and prices at all time highs.

While the sales figures have recently been weak, it is a shortage of supply that is the cause. You can?t sell what you don?t have, at least in the real estate business.

From here on, I expect a slow grind up well into the 2020?s. If you live in the rest of the country, we are talking about small, single digit gains. The consequence of pernicious deflation is that home prices appreciate at a glacial pace.

At least, it has stopped going down, which has been great news for the financial industry.

There are only three numbers you need to know in the housing market for the next 20 years: there are 80 million baby boomers, 65 million Generation Xer?s who follow them, and 86 million in the generation after that, the Millennials.

The boomers have been unloading dwellings to the Gen Xer?s since prices peaked in 2007. But there are not enough of the latter, and three decades of falling real incomes mean that they only earn a fraction of what their parents made. That's what caused the financial crisis.

If they have prospered, banks won?t lend to them. Brokers used to say that their market was all about ?location, location, location?. Now it is ?financing, financing, financing?.

Banks have gone back to the old standard of only lending money to people who don?t need it. But expect to put up your first-born child as collateral, and bring in your entire extended family in as cosigners if you want to get a bank loan.?

There is a happy ending to this story. Millennials, now aged 21-37 are already starting to kick in as the dominant buyers in the market. They are just starting to transition from 30% to 70% of all new buyers in this market. The Great Millennial Migration to the suburbs has begun.

As a result, the price of single family homes should rocket tenfold during the 2020?s, as they did during the 1970?s and the 1990?s, when similar demographic influences were at play.

This will happen in the context of a coming labor shortfall and rising standards of living. Inflation returns.

Rising rents are accelerating this trend. Renters now pay 35% of the gross income, compared to only 18% for owners, and less when multiple deductions and tax subsidies are taken into account.

Remember too, that by then, the US will not have built any new houses in large numbers in 10 years. We are still operating at only a quarter of the peak rate. Thanks to the Great Recession, the construction of five million new homes has gone missing in action.

That makes a home purchase now particularly attractive for the long term, to live in, and not to speculate with.

You will boast to your grandchildren how little you paid for your house, as my grandparents once did to me ($18,000 for a four bedroom brownstone in Brooklyn in 1922).

Quite honestly, of all the asset classes mentioned in this report, purchasing your abode is probably the single best investment you can make now.

If you borrow at a 3% 5/1 ARM rate, and the long-term inflation rate is 3%, then over time you will get your house for free.

How hard is that to figure out?

Crossing the Bridge to Home Sweet Home

Crossing the Bridge to Home Sweet Home9) Postscript

We have pulled into the station at Truckee in the midst of a howling blizzard.

My loyal staff have made the 20 mile trek from my beachfront estate at Incline Village to welcome me to California with a couple of hot breakfast burritos and a chilled bottle of Dom Perignon Champagne, which has been resting in a nearby snowbank. I am thankfully spared from taking my last meal with Amtrak.

After that, it was over legendary Donner Pass, and then all downhill from the Sierras, across the Central Valley, and into the Sacramento River Delta.

Well, that?s all for now. We?ve just passed the Pacific mothball fleet moored in the Sacramento River Delta and we?re crossing the Benicia Bridge. The pressure increase caused by an 8,200 foot descent from Donner Pass has crushed my water bottle.

The Golden Gate Bridge and the soaring spire of the Transamerica Building are just around the next bend across San Francisco Bay.

A storm has blown through, leaving the air crystal clear and the bay as flat as glass. It is time for me to unplug my Macbook Pro and iPhone 6, pick up my various adapters, and pack up.

We arrive in Emeryville 45 minutes early. With any luck, I can squeeze in a ten mile night hike up Grizzly Peak and still get home in time to watch the opener for Downton Abbey's final season.

I reach the ridge just in time to catch a spectacular pastel sunset over the Pacific Ocean. The omens are there. It is going to be another good year.

I?ll shoot you a Trade Alert whenever I see a window open on any of the trades above.

Good trading in 2016!

John Thomas

The Mad Hedge Fund Trader

The Omens Are Good for 2016!

The Omens Are Good for 2016!

You wanted clarity in understanding the current state of play in the global financial markets? Here?s your #$%&*#!! clarity.

You should expect nothing less for this ridiculously expensive service of mine.

But maybe that is the cabin fever talking, now that I have been cooped up in my Tahoe lakefront estate for a week, engaging in deep research and grinding out the Trade Alerts, devoid of any human contact whatsoever.

Or, maybe it?s the high altitude.

I did have one visitor.

A black bear broke into my trash cans last light and spread garbage all over the back yard. He then left his calling card, a giant poop, in my parking space.

Judging by the size of the turds, I would say he was at least 600 pounds. This is why you never take out the trash at night in the High Sierras.

Ah, the delights of Mother Nature!

We certainly live in a confusing, topsy-turvy, tear your hair out world this year. Good news is bad news, bad news worse, and no news the worst of all.

The biggest under performing week of the year for stocks is then followed by the best. Net net, we are absolutely at a zero movement, and lots of clients complaining about poor returns on their investment.

I tallied the year-on-year performance of every major assets class and this is what I found.

+16% - Hedged Japanese Stocks (DXJ)

+15% - Hedged European stocks (HEDJ)

+13% - US dollar basket (UUP)

+10% - My house

0% - Stocks (SPY)

0% -? bonds (TLT)

-5% - Japanese Yen (FXY)

-11% - Euro (FXE)

-12% - Gold (GLD)

-18% -? Oil (USO)

-27% -? Commodities (CU)

-27% - Natural Gas (UNG)

There are some sobering conclusions to be drawn from these numbers.

There were very few opportunities to make money this year. If you were short energy, commodities, and foreign currencies, you did very well.

Followers of the Mad hedge Fund Trader can?t help but know and love these ticker symbols. They?ll notice that our long plays were found among the asset classes with the best performance, while our short bets populated the losers.

The problem with that is most financial advisors are not permitted to place client funds in the sort of inverse or leveraged ETF?s that most benefit from these kinds of moves (like the (YCS), (EUO), and (DUG)).

That left them reading about the success of others in the newspapers, even when they knew these trends were unfolding (through reading this letter).

How frustrating is that?

What was one of my best investments of 2015?

My San Francisco home, which has the additional benefit in that I get to live in it, have a place to stash all my junk, and claim big tax deductions (depreciated home office space, business use of phone, blah, blah, blah).

Of course, I do have the advantage of living in the middle of one of the greatest technology and IPO booms of all time. Every time one of these ?sharing? companies goes public, the value of my home rises by a few hundred grand.

The real problem here is that investing since the end of the Federal Reserve?s quantitative easing program ended a year ago has become a real uphill battle.

While the government was adding $3.9 trillion in funds to the economy we traders enjoyed one of the greatest free lunches of all time. It made us all look like freakin? geniuses!

Just maintaining their present $3.9 trillion balance sheet, not adding to it, has left almost every asset class dead in the water.

Heaven help us if they ever try to unwind some of that debt!

Janet has promised me that she isn?t going to engage in such monetary suicide.

The Fed is continuing with Ben Bernanke?s plan to run all of their Treasury bond holdings into expiration, even if it takes a decade to achieve this. And with deflation accelerating (see charts below), the need for such a desperate action is remote.

Still, one has to ponder the potential implications.

It all kind of makes my own 43% Trade Alert gain in 2015 look pretty good. But I don?t want to boast too much. That tends to invite bad luck and losses, which I would much rather avoid.

What! No QE?

I am constantly asked if there are any ways investors can take advantage of the current collapse in natural gas prices.

You don?t want to touch the gas producing companies, like Chesapeake (CHK) and Devon (DVN), because prices for natural gas are probably going to stay down for years.

Good firms that benefit from the increased volume of gas pumped are few and far between. Unless you are a large consumer of this despised molecule, such as an electric power company or a petrochemical plant, it is tough to find a profitable niche.

However, there is one company that delivers a narrow rifle shot that will do extremely well in coming years, and that is Cheniere Energy (LNG).

I first started following (LNG) two decades ago when I was still wildcatting for CH4 in the Texas Barnet Shale.

Back when natural gas was trading at a lofty $5/MBTU, Qatar invested $50 billion in developing its own massive gas resources.

The plan was to liquefy the gas at -256 degrees Fahrenheit in the Middle East, ship it to the US in a fleet of specialized LNG carriers, and have Cheniere convert it back into gas at its Sabine River plant for distribution to an energy hungry US market through the Creole Trail pipeline.

It all looked like a great plan, and (LNG) shares traded up to $45.

Then ?fracking? technology came along and blew up the entire model. The discovery of a new 100-year supply of gas under our feet caused gas prices to crash from a post Amaranth peak of $17/MMBTU down to $2/MMBTU.

Any plans to import LNG from the other side of the world were rendered utterly worthless. Qatar ended up selling its gas to Europe insteadto help offset that continent's over reliance on imports from Russia.

Chenier?s billion-dollar investment in a gasification plant was now worth only so much scrap metal. (LNG) shares plumbed to low single digits as the firm flirted with bankruptcy.

Enter China.

The Middle Kingdom?s voracious demand for energy in this recovery has caused the price of oil (USO) to soar from a 2008 low of $30 to $112.

Despite accounting for an overwhelming share of the world?s new energy purchases, Chinese cities are suffering from brown outs due to power shortages.

This is why China is resisting immense American pressure to quit buying Texas tea from Iran.

Enter the arbitrage. While oil has been plummeting, gas has been falling even more. Gas is now selling at 25% of the cost of oil on an adjusted BTU basis.

Another way of saying this is that you can buy oil for $12 a barrel instead of $48. It only takes a second with an abacus to understand the appeal of such a disparity.

Gas also has the additional benefits in that it is much cleaner burning than crude, lacks the sulfur and nitrogen dioxides, and produces half the carbon dioxide. That?s a big deal in Beijing where the air is so thick you can cut it with a knife on a bad day.

It is also important to know that many states, like California have decided to use natural gas as a bridge fuel until more economic and scalable alternatives are developed.

Enter the long-term contracts. During the 1960?s and 1970?s Japan entered into huge long term contracts to buy LNG from Australia and Indonesia to feed their own economic miracle of the day.

Because it is very expensive and hard to get, offshore supplies were tapped, the price was set at $16/MBTU. Those contracts are now expiring.

Do you think they?ll renew at the old price, or go to Cheniere for the $4 stuff? Gee, let me think about that one for a bit.

Enter Fukushima. The nuclear meltdown on March, 2011 prompted Japan to shut down 49 of 54 nuclear power plants that accounted for 25% of the country?s electric power generation. The brownouts that followed forced a sweltering summer on millions as the government urged consumers to shut off air conditioners to save juice.

Power companies there have been scrambling to obtain conventional energy supplies, and cheap gas supplies from the US would meet this demand nicely.

The trigger.

Cheniere obtained US government permission to export 2.2 billion cubic feet a day for 20 years. That would require it to convert the existing gasification plant to a liquefaction plant, something that can be done with some expensive re-engineering. A second plant is in the approval process.

It has already found several large international buyers to take delivery of the new end product. All that was missing was the money to finish the plant.

My hedge fund buddies have been accumulating this stock when it bottomed at $3, expecting an angel investor to appear. But it was one of those ?someday, it might happen? kind of stories better left to long-term players.

Then Blackstone jumped in with a beefy $2 billion investment in Cheniere. That will enable them to obtain an additional $3 billion in debt financing needed to finish the first of two export facilities. They are now expected to come online in 2016.

How does Cheniere stack up as an investment? Frankly, it is kind of scary. The market cap is only $11.3 billion, it has no earnings yet, and it pays no dividend. When the current spate of deals are done, it will have $5 billion in debt.

I first got followers into (LNG) at $5. We then had a great run all the way up to $85, and we took profits. In the current melt down, it has backed off all the way down to $45, a 47% hickey.

And these facilities are dangerous to operate. One blew up in Texas in 1937 and killed 300 schoolchildren.

As a result, local permits for these are very hard to come by. Anyone who thinks Texas is an unregulated paradise should try drilling for natural gas.

But as you can see a whole host of geopolitical, technology and economic strands reach a nexus in this one company, all of which are extremely positive for the share price.

If the story comes true, as Blackstone hopes, then there could be a double or triple in the shares for the patient. To learn more about Cheniere Energy, please go to their website: http://www.cheniere.com.

Did Somebody Light a Match?

Did Somebody Light a Match?

When is the Mad Hedge Fund Trader a genius, and when is he a complete moron?

That is the question readers have to ask themselves whenever their smart phones ping, and a new Trade Alert appears on their screens.

I have to confess that I wonder myself sometimes.

So I thought I would run my 2014 numbers to find out when I was a hero, and when I was a goat.

The good news is that I was a hero most of the time, and a goat only occasionally. Here is the cumulative profit and loss for the 75 Trade Alerts that I closed during calendar 2014, listed by asset class.

Profit by Asset Class

Foreign Exchange 15.12%

Equities 12.52%

Fixed Income 7.28%

Energy 1.4%

Volatility -1.68%

Total 37.64%

Foreign exchange trading was my big winner for 2014, accounting for nearly half of my profits. My most successful trade of the year was in my short position in the Euro (FXE), (EUO).

I piled on a double position at the end of July, just as it became apparent that the beleaguered European currency was about to break out of a multi month sideway move into a pronounced new downtrend.

I then kept rolling the strikes down every month. Those who bought the short Euro 2X ETF (EUO) made even more.

The fundamentals for the Euro were bad and steadily worsening. It helped that I was there for two months during the summer and could clearly see how grotesquely overvalued the currency was. $20 for a cappuccino? Mama mia!

Nothing beats on the ground, first hand research.

Stocks generated another third of my profits last year and also accounted for my largest number of Trade Alerts.

I correctly identified technology and biotech as the lead sectors for the year, weaving in and out of Apple (AAPL) and Gilead Sciences (GILD) on many occasions. I also nailed the recovery of the US auto industry (GM), (F).

I safely stayed away from the energy sector until the very end of the year, when oil hit the $50 handle. I also prudently avoided commodities like the plague.

Unfortunately, I was wrong on the bond market for the entire year. That didn?t stop me from making money on the short side on price spikes, with fixed income chipping a healthy 7.28% into the kitty.

It was only at the end of the year, when the prices accelerated their northward trend that they started to cost me money. My saving grace was that I kept positions small throughout, doubling up on a single occasion and then coming right back out.

My one trade in the energy sector for the year was on the short side, in natural gas (UNG), selling the simple molecule at the $5.50 level. With gas now plumbing the depths at $2.90, I should have followed up with more Trade Alerts. But hey, a 1.4% gain is better than a poke in the eye with a sharp stick.

In which asset class was I wrong every single time? Both of the volatility (VIX) trades I did in 2014 lost money, for a total of -1.68%. I got caught in one of many downdrafts that saw volatility hugging the floor for most of the year, giving it to me in the shorts with the (VXX).

All in all, it was a pretty good year.

What was my best trade of 2014? I made 2.75% with a short position in the S&P 500 in July, during one of the market?s periodic 5% corrections.

And my worst trade of 2014? I got hit with a 6.63% speeding ticket with a long position in the same index. But I lived to fight another day.

After a rocky start, 2015 promises to be another great year. That is, provided you ignore my advice on volatility.

Here is a complete list of every trade I closed last year, sorted by asset class, from best to worse.

|

Date |

Position |

Asset Class |

Long/short |

? |

? |

? |

? |

? |

? |

|

7/25/14 |

(SPY) 8/$202.50 - $202.50 put spread |

equities |

long |

? |

? |

? |

? |

? |

2.75% |

|

10/16/14 |

(GILD) 11/$80-$85 call spread |

equities |

long |

? |

? |

? |

? |

? |

2.57% |

|

5/19/14 |

(TLT) 7/$116-$119 put spread |

fixed income |

long |

? |

? |

? |

? |

? |

2.48% |

|

4/4/14 |

(IWM) 8/$113 puts |

equities |

long |

? |

? |

? |

? |

? |

2.38% |

|

7/10/14 |

(AAPL) 8/$85-$90 call spread |

equities |

long |

? |

? |

? |

? |

? |

2.30% |

|

2/3/14 |

(TLT) 6/$106 puts |

equities |

long |

? |

? |

? |

? |

? |

2.27% |

|

9/19/14 |

(IWM) 11/$117-$120 put spread |

equities |

long |

? |

? |

? |

? |

? |

2.26% |

|

10/7/14 |

(FXE) 11/$127-$129 put spread |

foreign exchange |

long |

? |

? |

? |

? |

? |

2.22% |

|

9/26/14 |

(IWM) 11/$116-$119 put spread |

equities |

long |

? |

? |

? |

? |

? |

2.21% |

|

4/17/14 |

(TLT) 5/$114-$117 put spread |

fixed income |

long |

? |

? |

? |

? |

? |

2.10% |

|

8/7/14 |

(FXE) 9/$133-$135 put spread |

foreign exchange |

long |

? |

? |

? |

? |

? |

2.07% |

|

10/2/14 |

(BAC) 11/$15-$16 call spread |

equities |

long |

? |

? |

? |

? |

? |

2.04% |

|

4/9/14 |

(SPY) 5/$191-$194 put spread |

equities |

long |

? |

? |

? |

? |

? |

2.02% |

|

10/15/14 |

(DAL) 11/$25-$27 call spread |

equities |

long |

? |

? |

? |

? |

? |

1.89% |

|

9/25/14 |

(FXE) 11/$128-$130 put spread |

foreign exchange |

long |

? |

? |

? |

? |

? |

1.86% |

|

6/6/14 |

(JPM) 7/$52.50-$55.00 call spread |

equities |

long |

? |

? |

? |

? |

? |

1.81% |

|

4/4/14 |

(SPY) 5/$193-$196 put spread |

equities |

long |

? |

? |

? |

? |

? |

1.81% |

|

3/14/14 |

(TLT) 4/$111-$114 put spread |

fixed income |

long |

? |

? |

? |

? |

? |

1.68% |

|

10/17/14 |

(AAPL) 11/$87.50-$92.50 call spread |

equities |

long |

? |

? |

? |

? |

? |

1.56% |

|

10/15/14 |

(SPY) 11/$168-$173 call spread |

equities |

long |

? |

? |

? |

? |

? |

1.51% |

|

7/3/14 |

(FXE) 8/$138 put spread |

foreign exchange |

long |

? |

? |

? |

? |

? |

1.51% |

|

10/9/14 |

(FXE) 11/$128-$130 put spread |

foreign exchange |

long |

? |

? |

? |

? |

? |

1.48% |

|

9/19/14 |

(FXE) 10/$128-$130 put spread |

foreign exchange |

long |

? |

? |

? |

? |

? |

1.45% |

|

10/22/14 |

(SPY) 11/$179-$183 call spread |

equities |

long |

? |

? |

? |

? |

? |

1.44% |

|

5/29/14 |

(TLT) 7/$118-$121 put spread |

fixed income |

long |

? |

? |

? |

? |

? |

1.44% |

|

2/24/14 |

(UNG) 7/$26 puts |

energy |

long |

? |

? |

? |

? |

? |

1.40% |

|

2/24/14 |

(BAC) 3/$15-$16 call spread |

equities |

long |

? |

? |

? |

? |

? |

1.39% |

|

6/23/14 |

(SPY) 7/$202 put spread |

equities |

long |

? |

? |

? |

? |

? |

1.37% |

|

9/29/14 |

(SPY) 10/$202-$205 Put spread |

equities |

long |

? |

? |

? |

? |

? |

1.29% |

|

5/20/14 |

(AAPL) 7/$540 $570 call spread |

equities |

long |

? |

? |

? |

? |

? |

1.22% |

|

9/26/14 |

(SPY) 10/$202-$205 Put spread |

equities |

long |

? |

? |

? |

? |

? |

1.22% |

|

5/22/14 |

(GOOGL) 7/$480-$520 call spread |

equities |

long |

? |

? |

? |

? |

? |

1.16% |

|

5/19/14 |

(FXY) 7/$98-$101 put spread |

foreign exchange |

long |

? |

? |

? |

? |

? |

1.14% |

|

1/15/14 |

(T) 2/$35-$37 put spread |

equities |

long |

? |

? |

? |

? |

? |

1.08% |

|

3/3/14 |

(TLT) 3/$111-$114 put spread |

fixed income |

long |

? |

? |

? |

? |

? |

1.07% |

|

1/28/14 |

(AAPL) 2/$460-$490 call spread |

equities |

long |

? |

? |

? |

? |

? |

1.06% |

|

4/24/14 |

(SPY) 5/$192-$195 put spread |

equities |

long |

? |

? |

? |

? |

? |

1.05% |

|

6/6/14 |

(CAT) 7/$97.50-$100 call spread |

equities |

long |

? |

? |

? |

? |

? |

1.04% |

|

7/23/14 |

(FXE) 8/$134-$136 put spread |

foreign exchange |

long |

? |

? |

? |

? |

? |

0.99% |

|

8/18/14 |

(FXE) 9/$133-$135 put spread |

foreign exchange |

long |

? |

? |

? |

? |

? |

0.94% |

|

11/4/14 |

(BAC) 12/$15-$16 call spread |

equities |

long |

? |

? |

? |

? |

? |

0.88% |

|

4/9/14 |

(SPY) 6/$193-$196 put spread |

equities |

long |

? |

? |

? |

? |

? |

0.88% |

|

7/25/14 |

(SPY) 8/$202.50 -205 put spread |

equities |

long |

? |

? |

? |

? |

? |

0.88% |

|

6/6/14 |

(MSFT) 7/$38-$40 call spread |

equities |

long |

? |

? |

? |

? |

? |

0.87% |

|

10/23/14 |

(FXY) 11/$92-$95 puts spread |

foreign exchange |

long |

? |

? |

? |

? |

? |

0.86% |

|

7/23/14 |

(TLT) 8/$117-$120 put spread |

fixed income |

long |

? |

? |

? |

? |

? |

0.81% |

|

3/5/14 |

(DAL) 4/$30-$32 Call spread |

equities |

long |

? |

? |

? |

? |

? |

0.76% |

|

4/10/14 |

(VXX) long volatility ETN |

equities |

long |

? |

? |

? |

? |

? |

0.76% |

|

1/30/14 |

(UNG) 7/$23 puts |

equities |

long |

? |

? |

? |

? |

? |

0.66% |

|

4/1/14 |

(FXY) 5/$96-$99 put spread |

foreign currency |

long |

? |

? |

? |

? |

? |

0.60% |

|

1/15/14 |

(TLT) 2/$108-$111 put spread |

equities |

long |

? |

? |

? |

? |

? |

0.47% |

|

3/6/14 |

(EBAY) 4/$52.50- $55 call spread |

equities |

long |

? |

? |

? |

? |

? |

0.24% |

|

10/14/14 |

(TBT) short Treasury Bond ETF |

fixed income |

long |

? |

? |

? |

? |

? |

0.22% |

|

3/28/14 |

(VXX) long volatility ETN |

equities |

long |

? |

? |

? |

? |

? |

0.20% |

|

7/17/14 |

(TBT) short Treasury Bond ETF |

fixed income |

long |

? |

? |

? |

? |

? |

0.08% |

|

3/26/14 |

(VXX) long volatility ETN |

equities |

long |

? |

? |

? |

? |

? |

0.06% |

|

7/8/14 |

(TLT) 8/$115-$118 put spread |

fixed income |

long |

? |

? |

? |

? |

? |

-0.18% |

|

4/28/14 |

(SPY) 5/$189-$192 put spread |

equities |

long |

? |

? |

? |

? |

? |

-0.45% |

|

3/5/14 |

(GE) 4/$24-$25 call spread |

equities |

long |

? |

? |

? |

? |

? |

-0.73% |

|

4/28/14 |

(VXX) long volatility ETN |

volatility |

long |

? |

? |

? |

? |

? |

-0.81% |

|

4/24/14 |

(TLT) 5/$113-$116 put spread |

fixed income |

long |

? |

? |

? |

? |

? |

-0.87% |

|

4/28/14 |

(VXX) long volatility ETN |

volatility |

long |

? |

? |

? |

? |

? |

-0.87% |

|

6/6/14 |

(IBM) 7/$180-$185 call spread |

equities |

long |

? |

? |

? |

? |

? |

-1.27% |

|

9/30/14 |

(SPY) 11/$185-$190 call spread |

equities |

long |

? |

? |

? |

? |

? |

-1.51% |

|

10/9/14 |

(TLT) 11/$122-$125 put spread |

fixed income |

long |

? |

? |

? |

? |

? |

-1.55% |

|

9/24/14 |

(TSLA) 11/$200 call spread |

equities |

long |

? |

? |

? |

? |

? |

-1.62% |

|

2/27/14 |

(SPY) 3/$189-$192 put spread |

equities |

long |

? |

? |

? |

? |

? |

-1.67% |

|

3/6/14 |

(BAC) 4/$16 calls |

equities |

long |

? |

? |

? |

? |

? |

-2.01% |

|

10/14/14 |

(SPY) 10/$180-$184 call spread |

equities |

short |

? |

? |

? |

? |

? |

-2.13% |

|

11/14/14 |

(BABA) 12/$100-$105 call spread |

equities |

short |

? |

? |

? |

? |

? |

-2.38% |

|

10/20/14 |

(SPY) 11/$197-$202 call spread |

equities |

short |

? |

? |

? |

? |

? |

-2.72% |

|

7/3/14 |

(GM) 8/$33-$35 call spread |

equities |

long |

? |

? |

? |

? |

? |

-2.91% |

|

3/7/14 |

(GM) 4/$34-$36 call spread |

equities |

long |

? |

? |

? |

? |

? |

-2.96% |

|

11/25/14 |

(SCTY) 12/47.50-$52.50 call spread |

equities |

long |

? |

? |

? |

? |

? |

-3.63% |

|

10/20/14 |

(SPY) 11/$197-$202 call spread |

equities |

short |

? |

? |

? |

? |

? |

-4.22% |

|

4/14/14 |

(SPY) 5/$188-$191 put spread |

equities |

long |

? |

? |

? |

? |

? |

-6.63% |

What a Year!

What a Year!

I am once again writing this report from a first class sleeping cabin on Amtrak?s California Zephyr. By day, I have two comfortable seats facing each other next to a broad window. At night, they fold into bunk beds, a single and a double. There is a shower, but only Houdini could get in and out of it.

We are now pulling away from Chicago?s Union Station, leaving its hurried commuters, buskers, panhandlers, and majestic great halls behind. I am headed for Emeryville, California, just across the bay from San Francisco. That gives me only 56 hours to complete this report.