Mad Hedge Biotech and Healthcare Letter

May 20, 2025

Fiat Lux

Featured Trade:

(HEALTHCARE’S FALLING KNIFE)

(UNH), (CI), (CVS), (LLY), (VRTX), (SGRY), (AAPL), (AMZN)

Mad Hedge Biotech and Healthcare Letter

May 20, 2025

Fiat Lux

Featured Trade:

(HEALTHCARE’S FALLING KNIFE)

(UNH), (CI), (CVS), (LLY), (VRTX), (SGRY), (AAPL), (AMZN)

Global Market Comments

May 19, 2025

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or FULL SPEED AHEAD TOWARDS THE CLIFF),

(FL), (DKS), (UNH), (GLD), (SPY), (MSTR), (AAPL), (QQQ), (TLT)

Global Market Comments

May 16, 2025

Fiat Lux

Featured Trade:

(MAY 14 BIWEEKLY STRATEGY WEBINAR Q&A),

(TSLA), (BLK), (SPY), (TLT), (WMT), (LLY), (UNH), (KKR), (NVDA), (ABNB), (GLD)

Global Market Comments

February 24, 2025

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE DOWNSIDE OF DOGE, plus THE LAST GLASS OF KOOL-AID)

(SPY), (TLT), (GS), (VST), (TSLA), (WMT), (UNH)

Mad Hedge Biotech and Healthcare Letter

December 10, 2024

Fiat Lux

Featured Trade:

(THE INSURANCE COMPANY ALWAYS RINGS TWICE)

(UNH), (CI), (CVS), (HUM), (AMGN), (BIIB), (GILD)

Got an interesting call yesterday from an old college buddy - let's call him Bob. We go way back to our UCLA days, before I headed to Tokyo and he went into tech.

He was fuming because UnitedHealth (UNH) just denied his family's third claim this year, something about an "experimental treatment" for his daughter's rare condition.

Coming from a guy who just cashed out of his third startup, hearing him rant about insurance bureaucracy was pretty rich.

Still, his situation got me thinking. After hanging up, I dug into what's really happening with insurance stocks, and the picture isn't pretty.

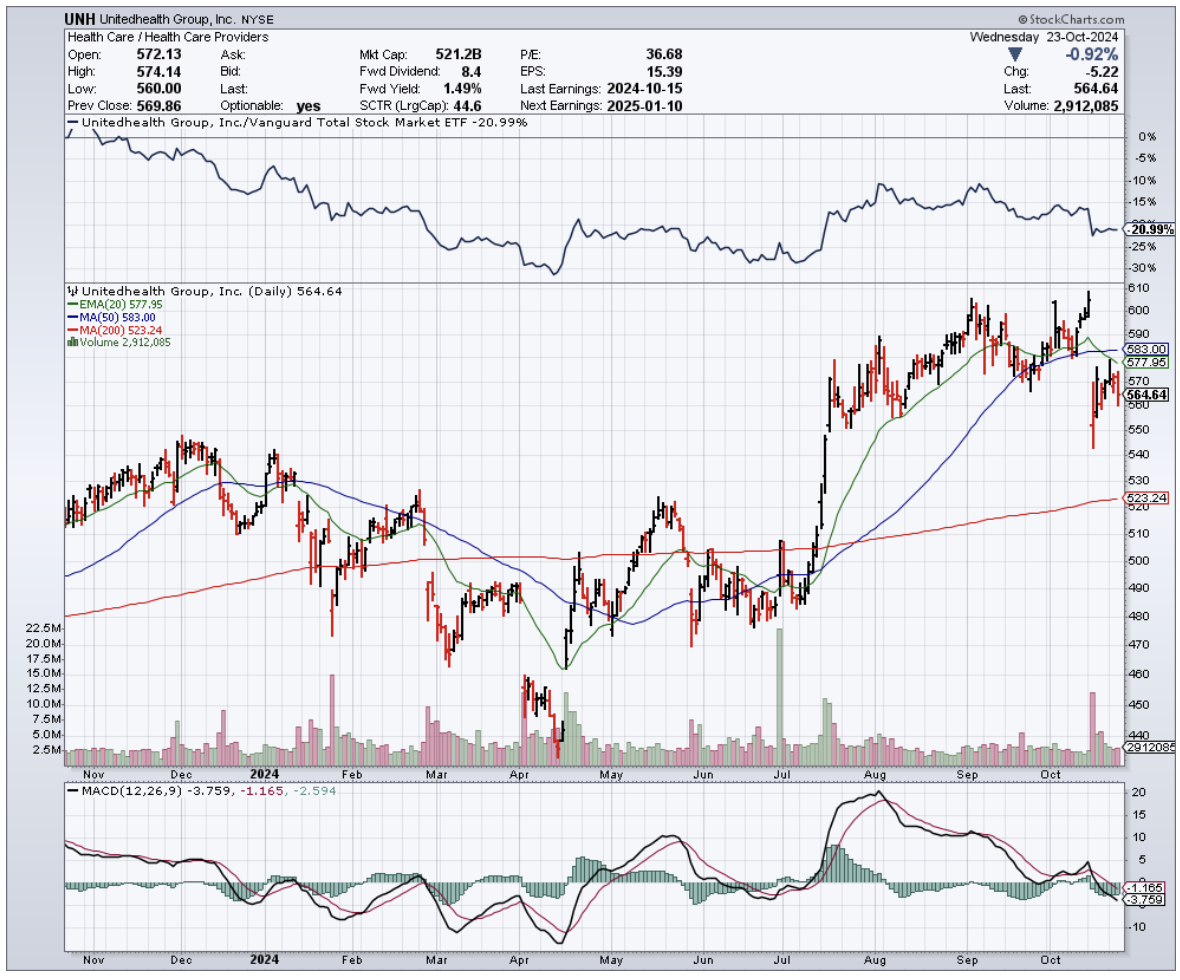

UnitedHealth Group, our nation's biggest health insurer, just had its worst week in years - dropping 9.5% after one of their executives was tragically murdered, which sparked an unexpected spotlight on their claims practices.

Cigna (CI) and CVS Health (CVS) caught the same downdraft, falling 4.5% and 5% respectively.

But here's what really caught my attention: UnitedHealthcare's denial rate for Medicare Advantage claims has more than doubled since 2020, hitting 22.7% last year.

Interestingly, this spike happened right as they rolled out new automation processes. Funny how that works, isn't it?

Experian Health's latest report shows this isn't isolated - 73% of healthcare providers are reporting more denials than ever, with processing times stretching longer and longer.

The cost of this trend? The Council for Affordable Quality Healthcare estimates $31 billion annually in administrative expenses alone.

Meanwhile, biotech companies find themselves in an awkward position. They're developing treatments that cost more than a house in the Hamptons and then need these very same insurers to make them accessible.

Amgen's (AMGN) been crushing it with their human therapeutics portfolio, pulling in $28.2 billion in revenue last year.

Biogen's (BIIB) making serious moves in neurological treatments, though their path has been rockier - just ask anyone who followed the Aduhelm saga.

Gilead Sciences (GILD), our antiviral champions, have managed to stay above the fray, partly because their HIV and hepatitis treatments have become standard of care.

But even these giants must wonder:: as insurers tighten their prior authorization screws, what happens to patient access?

These biotechs spend billions developing breakthrough treatments - Amgen alone dropped $4.4 billion on R&D last year - only to face the insurance industry's equivalent of "computer says no."

The irony isn't lost on anyone: insurers need innovative treatments to justify their premiums, while biotech needs insurance coverage to justify their R&D spending.

It's a delicate dance that's worked reasonably well so far, but these rising denial rates have everyone on edge. Just last quarter, we saw several biotech earnings calls dominated by questions about insurance coverage rather than clinical trials.

So what should we do? Well, I say UnitedHealth and Cigna are "holds" right now - the current turbulence needs time to settle.

CVS Health is showing broader operational challenges that suggest it might be wise to consider selling. But Humana (HUM), with their strong Medicare Advantage presence, looks promising.

On the biotech side, Gilead looks like an excellent stock to buy on the dip. Its leadership in antivirals and solid pipeline make it compelling.

Amgen and Biogen? Keep them on your watch list while they try to find their footing in this situation.

Bob texted me again this morning - turns out he's filing an appeal with help from one of Silicon Valley's top healthcare attorneys. Typical Bob, bringing a cannon to a knife fight.

But maybe that's exactly what this sector needs right now - some heavy artillery to shake up the status quo.

For those willing to dodge the crossfire, there might just be some spoils of war worth picking up. After all, fortune favors the bold—and sometimes, the heavily armed.

Mad Hedge Biotech and Healthcare Letter

October 24, 2024

Fiat Lux

Featured Trade:

(A HEALTHCARE STOCK THAT OWNS TOMORROW)

(UNH), (HUM), (ELV), (CVS)

After decades of watching healthcare stocks, I've learned one immutable truth - demographics always win. And right now, demographics are handing UnitedHealth Group (UNH) the keys to the kingdom.

The numbers tell an impressive story. UnitedHealth just reported Q3 2024 revenue of $100.82 billion, up 9.2% year-over-year. That's a billion dollars above what Wall Street expected, even after weathering a nasty cyberattack on their Change Healthcare unit in February.

Let's put this in perspective. By 2031, America's national health expenditure will hit $7.17 trillion - more than the GDP of Japan and Germany combined. This isn't just another growth story.

Besides, having managed hedge fund money through multiple market cycles, I’d like to think that I know the difference between lucky timing and structural advantage. From the looks of how things are going, UnitedHealth has engineered themselves the latter.

The company's UnitedHealthcare segment tells only part of the story, bringing in $74.85 billion in Q3, up 7.2% from last year.

Their Medicare Advantage enrollment grew from 7.65 million to 7.81 million people, while their U.S. commercial health plans expanded from 27.25 million to 29.73 million members.

Yes, they took a hit on their global numbers after selling their Brazilian business - dropping from 5.48 million to 1.34 million customers. But sometimes the best deals are the ones you don't do.

The real story here is Optum and its aggressive push into value-based care.

While competitors are still figuring out how to merge technology with healthcare delivery, UnitedHealth has already built a fortress. Their $13 billion acquisition of Change Healthcare wasn't just about processing claims - it was about owning the healthcare data highway.

Optum's revenue jumped 12.5% to $63.79 billion, with their pharmacy division surging 18.5% to $34.21 billion. They processed 410 million prescriptions in Q3 alone - that's 30 million more than last year.

What Wall Street is missing is UnitedHealth's positioning for the post-COVID healthcare landscape. They're not just riding the telehealth wave - they're reshaping it.

Their OptumRx digital platform now handles 80% of all prescription transactions, while their virtual care visits have grown tenfold since 2019.

In fact, the regulatory environment plays into their hands.

While smaller players struggle with Medicare Advantage rate adjustments and value-based care requirements, UnitedHealth's scale and technology infrastructure turn these challenges into opportunities.

Their compliance systems and data analytics capabilities give them a moat that gets wider every quarter.

Wall Street expects Q4 revenue between $100.48 billion and $104.14 billion. Their P/S ratio of 1.41x looks rich compared to Humana (HUM) at 0.29x and Elevance Health (ELV) at 0.57x. But in this market, scale and execution command a premium.

Looking ahead, I see UnitedHealth hitting $552 billion in revenue by 2028. The catalysts are clear: aging demographics, rising chronic disease management post-COVID, and the unstoppable march toward value-based care.

Their Q3 non-GAAP EPS of $7.15 beat estimates by 12 cents. By 2028, I expect EPS to reach $44, with their P/E ratio dropping from 22.75x to 12.99x.

Their balance sheet remains rock solid - net debt/EBITDA ratio below 1.5x, with investment-grade ratings from S&P Global (SPGI), Fitch, and Moody's (MCO).

UnitedHealth also keeps growing its dividend by double digits, maintains a predictable business model, and outperforms competitors like CVS Health (CVS) and Humana on ROE.

Admittedly, they slightly lowered their 2024 adjusted EPS guidance, spooking some traders. But in my experience, Wall Street's short-term panic creates long-term opportunities.

So, what’s the play here? I suggest you build a position in UnitedHealth now while the stock has pulled back. Scale in gradually if you're concerned about timing, but don't miss this opportunity.

Remember, in the end, this isn't just about healthcare - it's about owning a piece of America's unstoppable demographic destiny. And that's a trend even a skeptic like me can believe in.

Mad Hedge Biotech and Healthcare Letter

August 13, 2024

Fiat Lux

Featured Trade:

(THE RISE OF THE STEADY EDDIES)

(CNC), (UNH), (PFE), (JNJ), (ABBV), (LLY), (BIO), (UHS), (WAT), (AMGN), (REGN), (VRTX), (CRSP), (MRNA)

Think of the market as a body fighting off an infection. Tech stocks might be the flashy antibodies, but healthcare is the steady, reliable immune system, keeping things stable when the going gets tough. And right now, that immune system is looking stronger than ever.

Skeptical? I get it. We've heard the hype about healthcare before. But this time, it's different.

The Healthcare Select Sector SPDR ETF (XLV) has been on a tear, up 9.3% this year as of Thursday's close. That's nearly keeping pace with the broader S&P 500's 12% gain - a remarkable feat in a market that's been anything but stable.

But what's even more impressive is the turnaround. Back in mid-July, XLV was lagging behind like a three-legged horse in the Kentucky Derby, up only 8.3% while the S&P 500 was showing off with an 18% gain.

In fact, out of the 63 healthcare stocks in the S&P 500, only a dozen have been slacking off since July. The rest? They've been outperforming like it's going out of style.

So what changed?

Well, it wasn't so much that healthcare stocks suddenly discovered the fountain of youth. No, my friends, it was more like the rest of the market decided to take a swan dive off the high board.

You see, while tech stocks were busy doing their best Icarus impression – flying too close to the sun and then plummeting back to earth – healthcare stocks were steady as she goes. It's like the old tortoise and hare story, except in this version, the hare got distracted by shiny objects and ran off a cliff.

Now, let's shine the spotlight on some of the key players driving this healthcare rally.

Remember those health insurers everyone was worried about back in spring? The ones that had investors biting their nails over the future of Medicare Advantage? Well, they've made a comeback.

The S&P 500 Managed Health Care index was down 12% in mid-April, looking about as healthy as a chain smoker with a Big Mac habit. But now? It's up 4.5% since the start of the year.

Companies like Centene (CNC) and UnitedHealth Group (UNH) have bounced back faster than a rubber band on steroids.

And it's not just the insurers. Big Pharma's been flexing, too.

Pfizer (PFE), the company that became a household name faster than you can say "vaccine," is holding steady. Johnson & Johnson (JNJ) is up 2.2%, probably thanks to all that baby powder they're not selling anymore.

Meanwhile, AbbVie’s (ABBV) up 11% since July. These guys are like the Energizer Bunny of the pharma world – they just keep going and going.

But the real showstopper? Eli Lilly (LLY). This biopharma has been on a tear since the beginning of 2024. Up 45% on the year at one point, they've been climbing faster than a squirrel up a tree with a dog in hot pursuit.

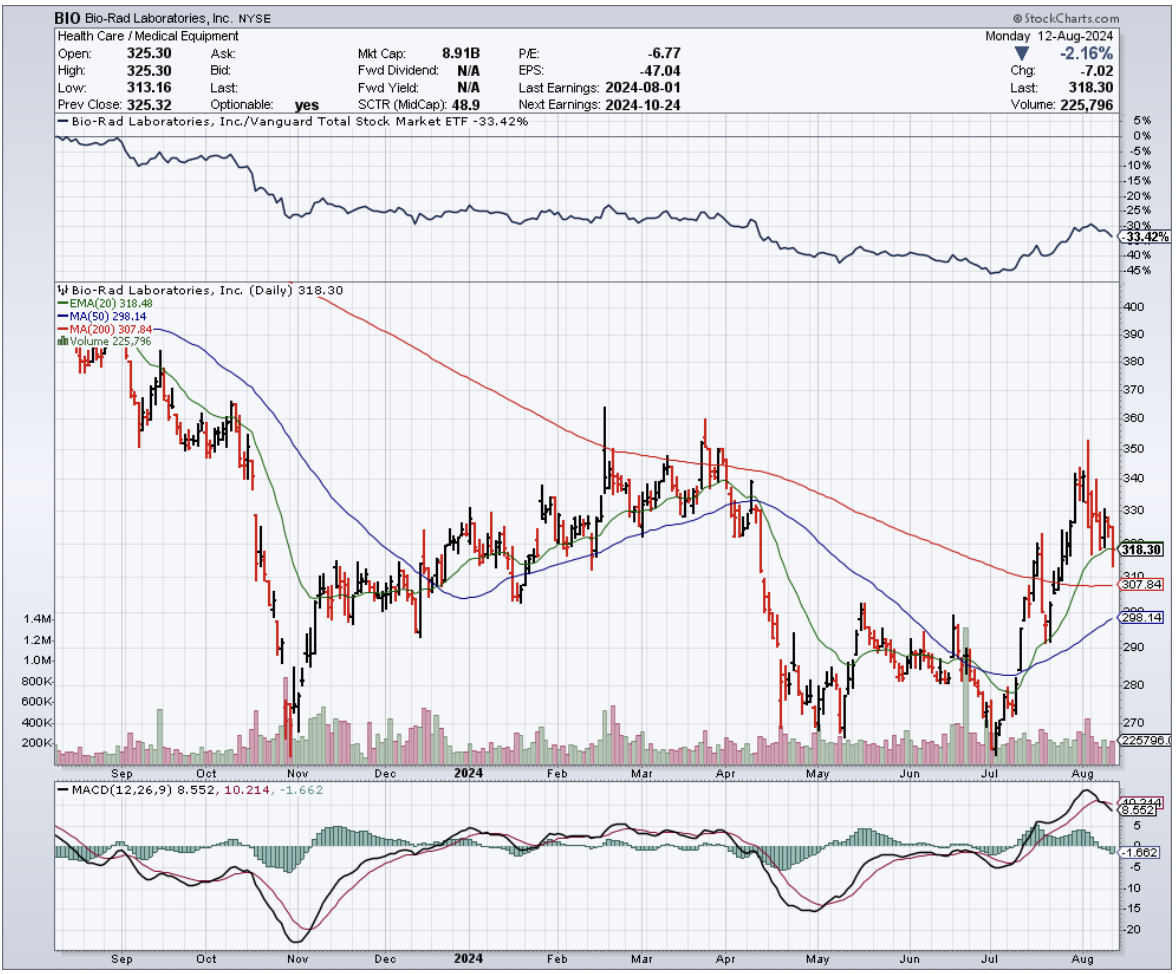

Then, there are companies like Bio-Rad Laboratories (BIO), up 20% since July. Universal Health Services (UHS)? Up 18% since July. Waters (WAT), the life sciences tools folks? Up 15%.

Even the biotechs are out to impress.

Amgen (AMGN), the granddaddy of biotech, is up 10% year-to-date. They're selling drugs like Prolia and Enbrel faster than hotcakes at a lumberjack convention.

And Amgen’s pipeline? It’s packed with potential blockbusters, setting the stage for further expansion in the future.

Gilead Sciences (GILD)? Up 15% year-to-date. Turns out, their COVID-19 treatment, Remdesivir, is back in vogue like bell-bottom jeans. And their HIV and hepatitis C drugs? They're still growing stronger.

But the real rock star of biotech? That'd be Regeneron Pharmaceuticals (REGN). These guys are up over 30% year-to-date. They're treating everything from eye diseases to cancer to inflammation.

Vertex Pharmaceuticals (VRTX) is another one to watch. Up 12% this year, they've got the cystic fibrosis market cornered. And they're not stopping there – they're expanding faster thanks to their collaboration with the likes of Crispr Therapeutics (CRSP).

Now that I’ve mentioned gene therapy, I know you're wondering about Moderna (MRNA). After all, weren’t they the darlings of the COVID era? Well, yes and no.

Their stock's down about 35% year-to-date, but don't count them out just yet. Their mRNA technology is hotter than a jalapeño popper fresh out of the fryer. They might be down, but they're definitely not out.

So, what's the takeaway here? I suggest you keep your eyes peeled on the biotechnology and healthcare sectors. After all, in this market, the best offense might just be a good defense – and what's more defensive than betting on the sector that keeps us all alive and kicking?