Mad Hedge Bitcoin Letter

January 13, 2022

Fiat Lux

Featured Trade:

(THE TURKISH LIRA AND THE DEATH CROSS COME INTO PLAY)

(BTC), (LIRA), (ETH), (USD)

Mad Hedge Bitcoin Letter

January 13, 2022

Fiat Lux

Featured Trade:

(THE TURKISH LIRA AND THE DEATH CROSS COME INTO PLAY)

(BTC), (LIRA), (ETH), (USD)

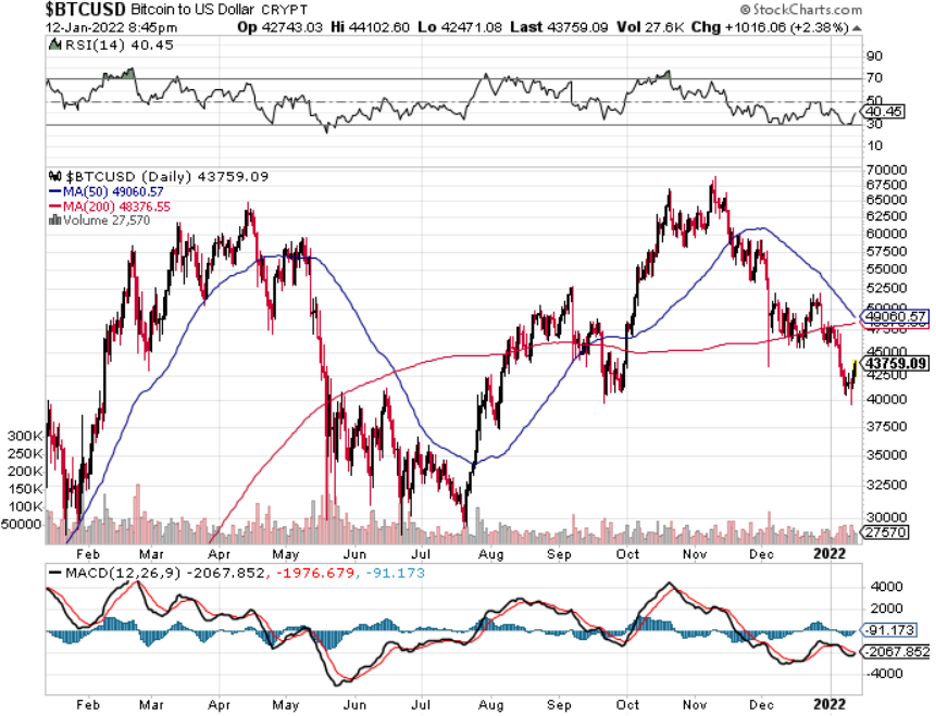

The infamous Death Cross is just around the corner again staring us in the face as another potential liquidity event could drive us lower or higher.

Even if you don’t fancy dealing with this phenomenon, algorithms lap it up and these technical events signal short-term price momentum and the direction of it.

To get even more exact, the death cross is the situation in which an asset's average price over the last 50 days drops below that of its 200-day moving average, an indication that its momentum is toast.

And this event is even more scrutinized after Bitcoin’s disgusting start to the year that has left it languishing in the lower $40,000s.

Not exactly the start we wanted and lots of complaints about the dufus called Fed Chair Jerome Powell and his handling of monetary policy.

Now, we should zone in on the big whales — the ones that hold massive amounts of Bitcoin and by that, I don’t mean 1 BTC or 1.2333 BTC.

All eyes are on them, many have said they will hold until infinity, but that’s easier when you bought BTC 10 years ago and not at $60,000 per unit which is what many retail traders did last year.

As we inch towards the vaunted death cross, will this trigger a 10% escape hatch that deadens the asset?

So far in 2022, Bitcoin has outperformed for just a few days and has been under relentless selling pressure.

To make matters worse, Ethereum appears to be forming a death cross as well.

The macro turning putrid has had a meaningful effect on the drop of Bitcoin prices, and if BTC can get through this death cross quagmire by holding onto the $40,000 level, then that could signal greener pastures ahead in the mid-term.

Speculative investments like Bitcoin are being abandoned under such aggressive tightening. Reports show only 5% of the clients surveyed by JPMorgan Chase expect Bitcoin to reach $100,000 per piece by the end of 2022.

Although the "death cross" is a bearish indicator, Bitcoin's historical record surrounding the indicator remains unclear. When the metric appeared last June, Bitcoin’s performance was dismal. But when the metric appeared last March, Bitcoin’s performance was strong. The emergence of this indicator in November 2019 sent Bitcoin lower.

As the U.S. economy is grappling with rip-roaring inflationary prices searing through the consumer prices to home prices, emerging countries are doing so bad with inflation that some are already completely giving up their own fiat currency.

Sure, El Salvador sucked up all the headlines for nationalizing Bitcoin as the de-facto medium of exchange for their citizens, but Turkey and its massive population of 84 million straddling the European continent have comprehensively pivoted towards Bitcoin as hyperinflation wrecks the purchasing power of the Turkish Lira.

The situation in Turkey is what crypto fanatics want to happen in the United States and it also represents what could unfold if the US Federal Reserve neglect doing their job.

Luckily, we are nowhere near that yet.

The Turkish lira has become so unpredictable that bakeries are closing down by the thousands citing a local currency that has lost most of its value.

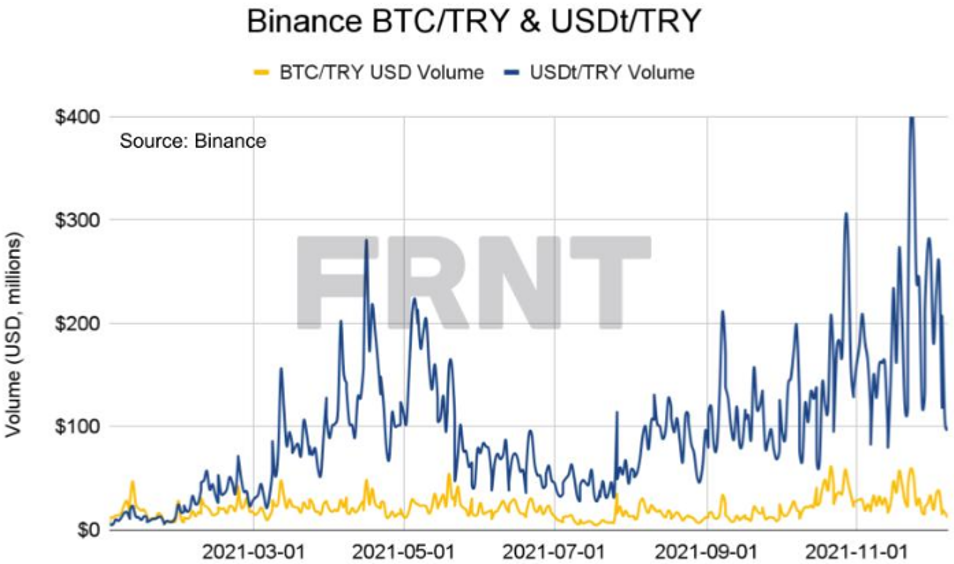

In Turkey, cryptocurrency trading volumes using the lira exploded to an average of $1.8 billion a day across three exchanges, according to blockchain analytics firm Chainalysis.

Turks favor stable coin tether, whose value is pegged to the dollar.

The rise of cryptocurrencies in recent years has presented a unique tool kit in which to store wealth, albeit far more volatile, and the shortage of US dollars circulating has forced the hand of the average Turk.

The Turkish lira has lost 40% of its value against the U.S. dollar in the past 5 months.

In the capital Istanbul, on the ground level, the local bazaars are accepting Bitcoin as standard currency over their own Turkish Lira.

This trend could mirror the future for some of these marginal economies that are run into the ground by renegade dictators.

Although the U.S. Federal Reserve has been irresponsible, the degree of policy mistake in Washington is nowhere near as atrocious as the events in Turkey.

There are numerous countries whose population could resort to crypto as a store of wealth including every ex-Soviet republic, big swaths of the Middle East, and major areas of Central and South America along with all of Africa.

My guess is that over time Bitcoin gets elevated as the de facto third currency behind the U.S. dollar and Euro. At this point, Bitcoin is too big to fail and too big to get rid of.

In a time of desperate need and no access to dollars and euros, Bitcoin is giving hope to large parts of the world as the pandemic and omicron inches closer to their shores.

Wait out this sideways correction then we march higher.

The blockbuster nonfarm payroll on Friday, coming in at a heady 288,000 has certainly removed any doubt that the US economy will reaccelerate in the fall. Earlier months were substantially revised up.

Monthly job growth of 200,000 plus now seems to be the new norm, after five consecutive months of such prints.

The headline unemployment rate plunged to 6.1%, a new six year low. American H2 GDP growth of 4% or more now seems to be firmly back on the table.

The gob smacking data has left many hedge fund managers confused, befuddled, and questioning the meaning of life. Loads have been playing the short bond, short equity trade all year, to the unmitigated grief of their investors.

Is smart now the new dumb?

As for me, I have been on the long equity side for almost the entire year, except for a few fleeting moments of mental degradation here and there. After spending most of June unwinding a sizeable US equity position into the rally, I now have little choice but to slap some new positions back on.

Still, there is a way to stay invested in the market and sleep at night. That is to focus on sectors and companies that, so far, have been left at the station during the 2014 bull market.

This is why I charged into a long in General Motors (GM) on Friday, the stock, until now, weighed down by past management?s unfortunate proclivity for killing off their customers.

The housing stocks (ITB), inhabitants of the doghouse for the past year, also look pretty interesting here. May pending home sales came in at a robust 6.1%, the best in four years, while pending home sales (contracts signed) leapt a positively eye popping 18.1%, a six year apex.

Revival of a moribund housing market is another piece of the puzzle that gets us to 4% GDP growth this year.

Bonds seemed to sniff out the great things coming by rolling over two days ahead of the June payroll news, diving some two points. Did they have advance notice, or are bond guys just smarter than we dullards in the equity world (true!)?

Rising US interest rates, a byproduct of a strengthening economy, will certainly lead to one thing: a more virile Uncle Buck and a sagging Euro. Interest rate differentials are the primary driver of foreign exchange movements.

So, you always want to be long the currency with rising rates (ours), and short the one with falling rates (theirs). So I am happy to sell short the beleaguered European currency here.

We saw the multi month selloff in the Euro going into the European Central Bank?s announcement of interest rate cuts and quantitative easing last month. Since then we have seen a classic ?buy the rumor, sell the news? short covering rally that has taken the euro up a counterintuitive two points.

The second move is just about to run out of steam.

Weakening data from the European economy, which is trailing that of the US, Japan, Australia, and even China, suggests that the Euro zone will see more easing before it experiences a tightening.

In proposing the Currency Shares Euro Trust (FXE) August, 2014 $136-$138 in-the-money bear put spread, I have been devious in the selection of my strikes. The near $136 put strike that I am shorting here against the long $138 put is exactly 50% of the move down from the double top at the March and May highs.

It also helps that the (FXE) was firmly rejected from the 50 day moving average on the charts.

We are getting a further assist from the calendar, which is giving us an unusually short monthly expiration on August 15. Most of Europe will be closed until then, not a bad time to be short Euro volatility.

I was also in a rush to get these out before the long July 4 weekend sucks out what little premium is left in the options market.

For those who don?t have options coursing through their veins, the ProShares Ultra Short Euro ETF (EUO) makes an ideal second choice. This 2X leveraged fund rises when the Euro falls, not by two times, but enough to make it worth the trouble. Or you can just sell short the 1X Currency Shares Euro Trust ETF (FXE).

Finally, if you are looking for another way to slumber like a baby with your long equity position, you can use a short position in the Euro to partially hedge your stock portfolio as well. US stock market weakness generally triggers a strong dollar and a weak Euro, as financial assets rush into a flight to safety mode.

The Time to Dump the Euro is Here

The Time to Dump the Euro is Here

The Time to Dump the Euro is Here

The Time to Dump the Euro is Here

I have been pounding the table trying to get readers out of gold since early December. Now, my friend at stockcharts.com, Mike Murphy, has produced a stunning series of charts showing that this may be more than just a short-term dip and another buying opportunity.

Mike explains that a number of traditional chart, technical, and intermarket signs are flashing serious warning signals. At the very least, we are going to test $1,500 an ounce sometime soon. If that doesn?t hold, then $1,250 is in the cards.

To make matters particularly fiendish for traders, we may see a false breakdown through $1,500 first, well into the 1,400?s, that sucks in tons of capitulation sellers before an uptrend resumes. It is a scenario that will be enough to test even the most devoted of gold bugs.

At risk is nothing less than the end of a bull market that is entering its 12th year. The shares of gold miners suggest that the demise of the bull market is already a foregone conclusion. The index for this group (GDM) has breached major support once again and is looking for a new four year low. Since this index usually correlates very highly with the barbarous relic, the grim writing is on the wall.

A strong dollar does not auger well for gold either. Look at the chart below, and you see the dollar basket (UUP) has punched through to an eight month high. Until two weeks ago, this was primarily a weak yen story. But since then, both the euro (FXE) and Sterling (FXB) have collapsed, adding fuel to the fire. And it is not just gold that is feeling the heat. The entire commodities space has been the pain trade, including oil (USO), copper (CU), and other hard assets.

There are a host of reasons why the yellow metal has suddenly become so unloved. The largest holder of the gold ETF (GLD), John Paulson, is getting big redemptions in his hedge fund, forcing him to sell. This is why the selling is so apparent in the paper gold markets, like the ETF?s, but not the physical.

India has suddenly seen its currency, the rupee, drop against the greenback. That reduces the buying power of the world?s largest gold importer. With years of pernicious deflation ahead of us, who needs a traditional inflation hedge like the yellow metal?

Here is the final nail in the coffin for gold. Look at the last chart of the Federal Reserve Bank of St. Louis?s measurement of the broader monetary base. It shows that it has exploded to the upside in recent months. In the past, gold matched the rise in the money supply step for step. Now it?s not. If a market can?t rally on fabulous news, which it has obviously failed to do since the last QE was launched in September, then you sell the daylights out of it. That is what most traders believe.

The screaming conclusion here is that traders are pouring their money into stocks instead of gold. Now, paper trumps gold. Conditions for the barbarous relic will, therefore, probably get worse before they get better.

Ben Bernanke affirmed as much last week when he told Congress that quantitative easing would continue unabated for the foreseeable future. That means rising stocks and flat bonds, all of which are bad for gold. The bottom line here is that when gold makes its first run at $1,500, I am not going to jump in as a buyer.

Weekly December, 2011 to February, 2013

Adjusted Monetary Base

Reserve Bank of St. Louis

Suddenly Going Out of Style

Panic is on deck, to use the baseball terminology that my foreign readers are often attempting to decipher. That is the only conclusion one can reach after getting gob smacked by the price action this morning. Copper got spanked for eight cents, oil burned $2, gold shed another $26, and silver puked 70 cents.

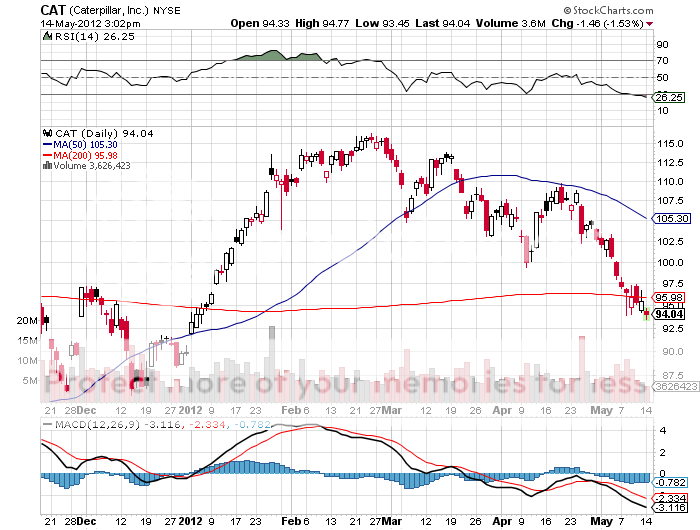

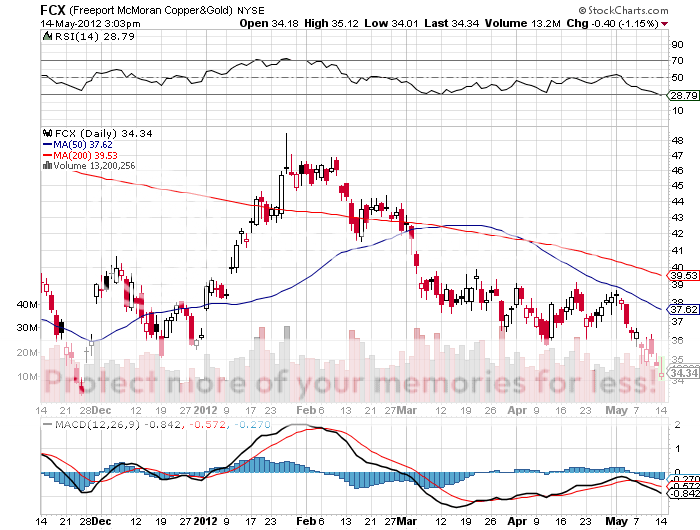

The tantrum like stock behavior in producing and equipment companies, like Freeport McMoRan (FCX) and Caterpillar (CAT) has been atrocious. How many of you out there know that JP Morgan (JPM) is the largest holder of futures contracts in the silver market and just got hit with a massive margin call? Why is all this happening on the 100 year anniversary of the sinking of the HMS Titanic?

Blame it all on Uncle Buck, whose recent steroid treatments has enabled him to unload the pounds, shed the fat, and adopt a new, more virile attitude towards life. Every other currency now looks like a 98 pound weakling. We now awake each morning to be greeted by the latest disastrous headline from Europe that accelerates the capital flight from the continental currency.

The Euro (FXE), (EUO), is deteriorating from bad to worse, with the foreign exchange community now clearly gunning for the next short term support at $1.26. Look at a ?10 note these days and it has recently printed upon it ?Abandon hope all ye who enter here.?

Traditional diversification currencies, like the Australian (FXA) and Canadian dollars (FXC) are now biting the hands that fed them, dragged down by their export commodities? pitiful performance. Hard as it is to imagine, the Ausie has been the world?s worst performing major currency this year, even underperforming the dreadful euro. Australian readers who followed my advice to pay for their summer vacations in advance at the $1.10 that prevailed at the beginning of the year are smiling. Those they didn?t are now looking for a discount caravan at a remote, dingo plagued campsite somewhere in the Outback.

The Japanese yen, the currency that everyone loves to hate, has perked up to a flight to safety bid while the rest of the world goes to hell in a hand basket. We are currently in between Bank of Japan quantitative easings there, so don?t expect this to last much longer. The tipping point into hyper debt driven, economic Armageddon there creeps ever forwards with each passing day on the calendar.

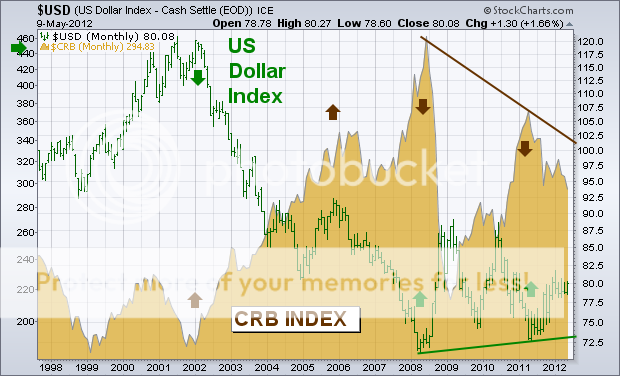

Take a look at the charts below for the US Dollar Index and it is obvious that things may soon get a whole lot worse. For starters, the dollar has only rallied back to the midpoint of a multiyear range. To get back up to the top of that range it needs to appreciate another 10%. To understand why this is a problem, look at the second chart that proves a tremendous inverse correlation between the dollar and commodities. A strong dollar always leads to falling demand for the hard stuff.

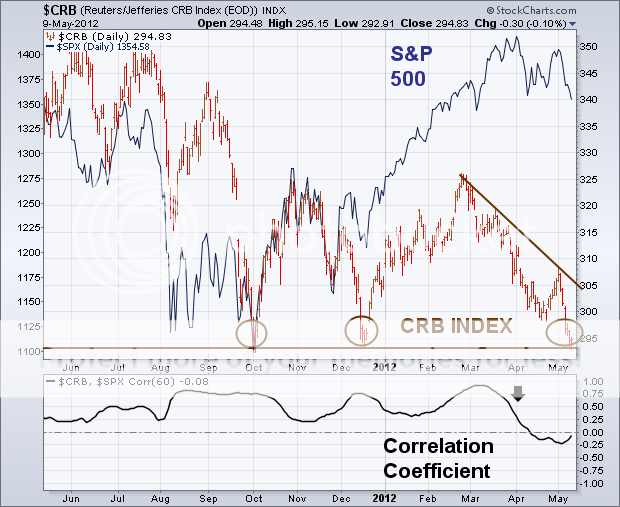

The third chart suggests that the other grotesquely overvalued asset class, US stocks, is also cruising for a bruising. Commodities led equities in this downturn by three months, as they usually do. If they break support here, then they will easily drag the (SPX) down to my medium term target of 1,275, off a heart thumping 10.3% from the recent top. If the economic data continues to worsen on a daily basis, as I have been chronicling on a daily basis for the last two months ad naseum and ad absurdum, then we have a clear shot at the fall, 2011 low at 1,060.

Oops, There Goes My Equity Portfolio