(MARKET OUTLOOK FOR THE WEEK AHEAD, or PARACHUTING WITHOUT A PARACHUTE), (AAPL), (SPY), (MSFT), (TLT), (TBT), (TDOC), (NFLX), (DIS), (VALE), (FCX), (USO), (JPM), (WFC), (BAC), (TSLA), (AMZN), (NVDA)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-01-24 09:04:462022-01-24 16:50:43January 24, 2022

It has been the worst New Year stock market opening in history.

After a two-day fake-out to the upside, stocks rolled over like the Bismarck and never looked up. NASDAQ did its best interpretation of flunking parachute school without a parachute, posting the worst month since 2008.

Markets can’t hold on to any rally longer than nanoseconds, and the last hour of the day has turned into one from hell.

What is even more confusing is that stocks are now trading like commodities, with massive one-way moves, while commodities, like oil (USO), copper( FCX), and iron ore (VALE) have resumed a steady grind up.

We had a lovefest going on here at Incline Village, Nevada for Technology and Bitcoin researcher Arthur Henry has been staying with me for the week to plot market strategy.

Once the market showed its hand, I sold short Microsoft (MSFT), which elicited torrents of complaints from readers. Then Arthur sold short Netflix (NFLX), inviting refund demands. Then I sold short Apple (AAPL), prompting accusations of high treason. Then Arthur sold short Teledoc (TDOC). There wasn’t a lot of talking, but frenetic writing and emailing instead.

Followers cried all the way to the bank.

In a mere two weeks, the price earnings multiple for the S&P 500 plunged from 22X to 20X. A lot of traders were only buying stock because they were going up. Take out the “up” and Houston we have a problem.

The entire streaming industry seems to have gone up in smoke and ex-growth practically overnight. Netflix (NFLX) delivered a gob smacking 29.5% swan dive in the wake of disappointing subscriber growth forecasts. Walt Disney (DIS), which ate the Netflix lunch, was dragged down 10% through guilt by association.

It is often said that the stock market has discounted 12 of the last six recessions. It is currently pricing in one of those non-recessions. What we are seeing is a sudden growth scare of the first order.

Despite last week’s carnage, stocks are still the most attractive asset class in the world, offering a potential 10% return in 2022. The problem is that they may make that 10% profit starting from 10% lower than here.

Despite all the red ink, big tech stocks are still on track to see a 30% earnings growth this year, and they account for a hefty 28% of the market.

Let’s look at Apple’s past declines for guidance on this meltdown.

Steve Jobs’ creation gave back 60% in the 2008 Great Recession, 34% during the 2015 growth scare, 48% during the great 2018 Christmas collapse, and 28% in the 2020 pandemic crash. So, the good news is that you won’t get killed by this selloff, you’ll just lose an arm and a leg. But they’ll grow back.

Remember, it’s always darkest just before it goes completely black. This correction is survivable, although it may not seem so at the moment.

It does vindicate my 2022 view that the first half will be about survival and that big money can be had in the second half.

So far, so good.

The Market is De-Grossing Big Time. That means cutting total market exposure and selling everything, regardless of stock or sector. The market is discounting a recession and bear market that isn’t going to happen, which occurs often. When it ends in a few weeks, interest rate sensitives, especially the banks, will bounce back hard, but tech won’t. Buy (JPM), (WFC), and (BAC) on bigger dips.

The Bond Collapse Goes Global, with German 10-year bunds going positive for the first time in three years, up 40 basis points in a month. Yes, inflation is finally hitting the Fatherland, home of post-WWI billion percent inflation. Eurozone inflation just topped 5%, well above its 2% target. British inflation hit a 30-year high. The move has lit a fire under all Euro currencies. Methinks the down move in (TLT) has more to go.

Fed to Raise Rates Eight Times, says Marathon Asset Management. That’s what will be needed to curb the current runaway inflation now at 7.0% and still rising. Personally, I think it will be 12 quarter-point increments to peak out at a 3 ¼% overnight rate. Any more and Powell might bring on a recession.

NASDAQ is Officially in Correction, down 10%, in the wake of poor performance this month. It’s the fourth one since the pandemic began two years ago. Tesla (TSLA), Amazon (AMZN), and NVIDIA (NVDA) have been leading the swan dive, all felled by rapidly rising interest rates. This could go on for months.

Weekly Jobless Claims Hit 286,000, a four-month high, as omicron sends workers fleeing home.

Goldman Sachs (GS) Gets Crushed, down 8%, on disappointing earnings. Tough market conditions are fading trading volumes while 2021 bonuses were through the roof. The move is particularly harsh in that buyers were flooding in right at support at the 200-day moving average.

China GDP (FXI) Grows 8.1% YOY but is rapidly slowing now, thanks to Omicron. China was first in and first out with the pandemic but is getting hit much harder in this round. That has prompted new mass lockdowns which will make out own supply chain problems worse for longer. In Chinese, “lockdown” means they weld your door shut, unlike here. Harsh, but it works.

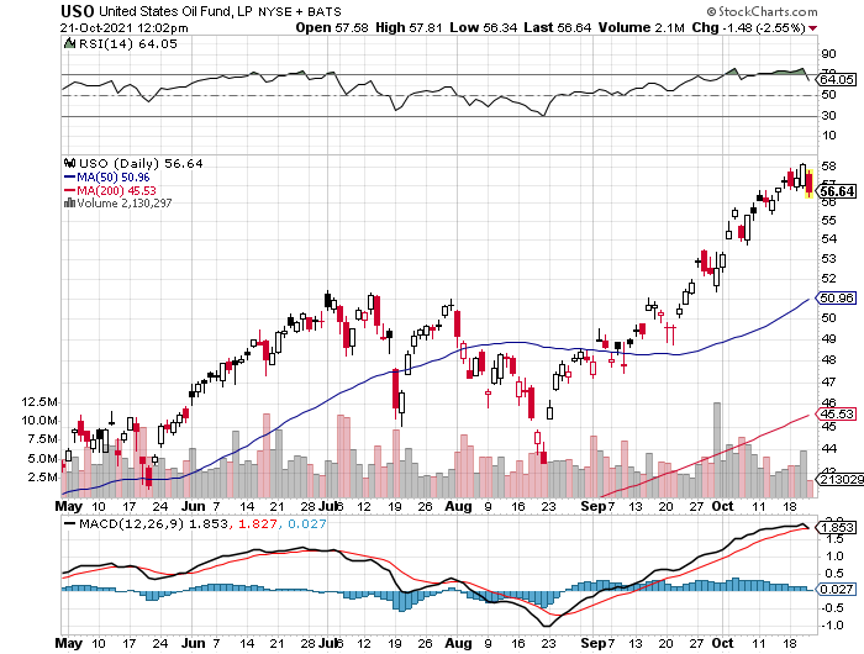

Oil (USO) Hits Seven-Year High, as inventories hit a 21-year low. No new capital is entering the industry, crimping supplies as old fields play out. The threat of a Russian invasion of the Ukraine is prompting advance stockpiling. Russia is the world’s second-largest oil exporter.

Existing Homes Sales Hit a 15-Year High, at 6.12 million, the best since 2006. December fell 4.6%. Extreme inventory shortage is the issue, with only 910,000 homes for sale at the end of the year, an incredibly low 1.8-month supply. You can’t find anything on the market now, to buy or rent. The median price of a home sold in December was $358,000, a 15.8% gain YOY.

Bitcoin (BITO) Crashes, decisively breaking key support at $40,000. Non-yielding assets of every description are getting wiped. Bail on all crypto options plays asap.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

With the pandemic-driven meltdown on Friday, my January month-to-date performance bounced back hard to 5.05%. My 2022 year-to-date performance also ended at 5.05%. The Dow Average is down -6.12% so far in 2022.

Once stocks went into free fall, I piled on the short positions as fast as I could write the trade alerts, including in Microsoft (MSFT), Apple (AAPL), and a double short in the S&P 500 (SPY). I also increased my shorts in the bond market (TLT) to a triple position. When prices became the most extreme, when the Volatility Index (VIX) hit $30, I bought both (SPY) and (TLT).

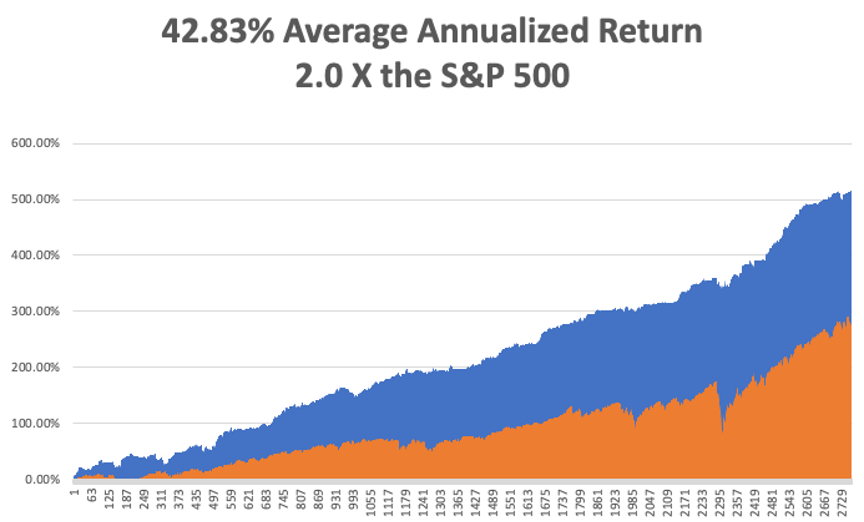

If everything goes our way, we should be up 14.26% by the February 18 options expiration.

That brings my 12-year total return to 517.61%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return has ratcheted up to 42.82% easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 71 million and rising quickly and deaths topping 866,000, which you can find here.

On Monday, January 24 at 6:45 AM, The Market Composite Flash PMI for January is out. Haliburton (HAL) reports.

On Tuesday, January 25 at 6:00 AM, the S&P Case Shiller National Home Price Index for November is released. American Express (AXP) reports.

On Wednesday, January 26 at 7:00 AM, the New Home Sales for December are published. At 11:00 AM The Federal Reserve interest rate decision is announced. Tesla (TSLA), Boeing (BA), and Freeport McMoRan (FCX) report.

On Thursday, January 27 at 8:30 AM the Weekly Jobless Claims are disclosed. We also get the first look at US Q4 GDP. Alaska Air (ALK) and US Steel (X) report.

On Friday, January 28 at 5:30 AM EST US Personal Income & Spending is printed. Caterpillar (CAT) reports. At 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, when I drove up to visit my pharmacist in Incline Village, Nevada, I warned him in advance that I had a question he never heard before: How good is 80-year-old morphine?

He stood back and eyed me suspiciously. Then I explained in detail.

Two years ago, I led an expedition to the South Pacific Solomon Island of Guadalcanal for the US Marine Corps Historical Division (click here for the link). My mission was to recover physical remains and dog tags from the missing-in-action there from the epic 1942 battle.

Between 1942 and 1944, nearly four hundred Marines vanished in the jungles, seas, and skies of Guadalcanal. They were the victims of enemy ambushes and friendly fire, hard fighting, malaria, dysentery, and poor planning.

They were buried in field graves, in cemeteries as unknowns, if not at all left out in the open where they fell. They were classified as “missing,” as “not recovered,” as “presumed dead.”

I managed to accomplish this by hiring an army of kids who knew where the most productive battlefields were, offering a reward of $10 a dog tag, a king's ransom in one of the poorest countries in the world. I recovered about 30 rusted, barely legible oval steel tags.

They also brought me unexploded Japanese hand grenades (please don’t drop), live mortar shells, lots of US 50 caliber and Japanese 7.7 mm Arisaka ammo, and the odd human jawbone, nationality undetermined.

I also chased down a lot of rumors.

There was said to be a fully intact Japanese zero fighter in flying condition hidden in a container at the port for sale to the highest bidder. No luck there.

There was also a just discovered intact B-17 Flying Fortress bomber that crash-landed on a mountain peak with a crew of 11. But that required a four-hour mosquito-infested jungle climb and I figured it wasn’t worth the malaria.

Then, one kid said he knows the location of a Japanese hospital. He led me down a steep, crumbling coral ravine, up a canyon and into a dark cave. And there it was, a Japanese field hospital untouched since the day it was abandoned in 1943.

The skeletons of Japanese soldiers in decayed but full uniform laid in cots where they died. There was a pile of skeletons in the back of the cave. Rusted bottles of Japanese drugs were strewn about, and yellowed glass sachets of morphine were scattered everywhere. I slowly backed out, fearing a cave-in.

It was creepy.

I sent my finds to the Marine Corps at Quantico, Virginia, who traced and returned them to the families. Often the survivors were the children or even grandchildren of the MIAs. What came back were stories of pain and loss that had finally reached closure after eight decades.

Wandering about the island, I often ran into Japanese groups with the same goals as mine. My Japanese is still fluent enough to carry on a decent friendly conversation with the grandchildren of their veterans. It turned out I knew far more about their loved ones than they. After all, it was our side that wrote the history. They were very grateful.

How many MIAs were they looking for? 30,000! Every year, they found hundreds of skeletons, cremated in a ceremony, one of which I was invited to. The ashes were returned to giant bronze urns at Yasakuni Ginja in Tokyo, the final resting place of hundreds of thousands of their own.

My pharmacist friend thought the morphine I discovered had lost half of its potency. Would he take it himself? No way!

As for me, I was a lucky one. My dad made it back from Guadalcanal, although the malaria and post-traumatic stress bothered him for years. And you never wanted to get in a fight with him….ever.

I can work here and make money in the stock market all day long. But my efforts on Guadalcanal were infinitely more rewarding. I’ll be going back as soon as the pandemic ends, now that I know where to look.

Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

True MIAs, the Ultimate Sacrifice

My Collection of Dog Tags and Morphine

My Army of Scavengers

Dad on Guadalcanal (lower right)

https://www.madhedgefundtrader.com/wp-content/uploads/2022/01/dog-tags-morphine.png428570Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-01-24 09:02:122022-01-24 16:51:22The Market Outlook for the Week Ahead, or Parachuting Without a Parachute

Below please find subscribers’ Q&A for the January 5 Mad Hedge Fund Trader Global Strategy Webinar broadcast from Incline Village, Nevada.

Q: What’s a good ETF to track the Russell 3,000 (RUA)?

A: I use the Russell 2,000 (IWM) which is really only about the Russell 1500 because 500 companies have been merged or gone bankrupt and they haven't adjusted the index yet. This is the year where value plays and small caps should do better, maybe even outperforming the S&P500. These are companies that do best in a strong economy.

Q: Should I focus on value dividends growth, or stick with the barbell?

A: I think you have to stick with the barbell if you’re a long-term investor. If you’re a short-term trader, try and catch the swings. Sell tech now, buy it back 10% lower. Keep financials; when they peak out you, dump them and go back into tech. It’ll be a trading year, but if a lot of you are just indexing the S&P500 or doubling up through a 2x ETF like the ProShares ultra S&P 500 (SSO), it may be the easiest way to go for this year.

Q: Will higher rates sabotage tech, particularly smaller companies?

A: They’ve already done so with PayPal (PYPL) down 44% in six months—I’d say that’s sabotaged. Same with Square (SQ) and a lot of the other smaller tech companies. So that has happened and will continue to happen a bit more, but we’re really getting into the extreme oversold levels on a lot of these companies.

Q: Should we cash out on the iShares 20 Plus Year Treasury Bond ETF (TLT) summer 150/155 put spread LEAPS?

A: No, because you haven't even realized half of the profit in that yet since there is so much time value left in those options. As long as you stay below $150 in the (TLT), which I'm pretty sure we will, you will get your full 100% profit on that position. On the six month and one year positions, they don’t really move very much because they have so much time value in them. Once you get into the accelerated time decay, which is during the last 3 months before expiration, they catch like a house on fire. So, if you're willing to keep a safe long-term position, this thing will write you a check every day for the next six months or a year to expiration. I know we have absolutely everybody in these deep in the money TLT puts; some people even did $165-$170’s—you know, my widows and orphans crowd—and they are doing well, but not as much as if you’d had a front month.

Q: What scares you most for the next 12 months?

A: Another variant that is more fatal than either Delta or Omicron. Unlikely, but not impossible.

Q: Do you expect Freeport McMoRan (FCX) to break out to the upside?

A: I do, I did the numbers over the vacation for copper production to meet current forecast demands for electric vehicle production. Global copper has to increase 11 times, and that can’t be done, so prices are going to have to go up a lot. One of my concerns with these lofty EV projections (that even I make) is that there aren’t enough commodities in the world to make all these cars with the current infrastructure. And you’re not going to find a replacement for copper—it's just too perfect of an electrical conductor. So, that means higher prices to me—you increase demand 11 times on a stable supply, and it takes 10 years to bring a new copper mine online.

Q: Do you have any open trades?

A: No, and one reason is that I figured they would probably crash the market on the last trading day of the year, which they did. If I had positions, they would have crushed them on the last year and my performance. And all hedge fund traders do this; they try to go 100% cash at the end of the year to avoid these things. And whatever you lost on Friday you made back on Monday morning at the expense of last year's performance. But you have to wait 15 months to get paid on today's performance, and, that is the reason I do that. So, looking for higher highs to sell, lower lows to buy.

Q: Should I be buying NVIDIA (NVDA) and Tesla (TSLA) on the dip?

A: Absolutely yes, but Tesla's prone to 45% corrections—we had one last year and the year before—and Nvidia tends to have 25% corrections. So yes, NVIDIA could well be the stock of the decade, but you don’t want to buy it right now. It’s starting to lose steam already.

Q: Will ProShares Ultra Technology (ROM) be under pressure?

A: Keep your position small now, take some profits, look to buy on a bigger dip. If the big techs drop 10%, (ROM) will drop 20% and get you below $100.

Q: Do you offer trade alerts on small caps for short term traders?

A: No, because you can’t execute those trades. A lot of them are just so illiquid, you can’t even trade one share unless you want to pay a huge spread. Keep in mind, when I worked at Morgan Stanley (MS), I covered the Rockefeller Foundation, the Ford Foundation, George Soros, Paul Tudor Jones, the government of Abu Dhabi, California State Pension Fund, and a lot of other huge funds; and the last thing they’re interested in is short term trades for the small-cap stocks. So, I don't really know much about those, but they tend to change the names every year anyway. And it really is a beginner trader type area because the volatility is so enormous. You can get 10x moves one day going to zero the next. It is also an area full of scams, cons, and pump and dump schemes.

Q: What is your advice when it comes to the ProShares UltraShort 20+ Year Treasury (TBT)?

A: Short term, take the profits—you just got a $14 point rally in your favor. Short term traders, take profits on bonds here, cover your shorts. Long term investors keep it, the cost of carry is only about 4% right now, not that high, so I would keep it for a great year-end move for 2.5% yields on the ten-year.

Q: I hate oil (USO) because it’s going to zero. Should I keep trading in it?

A: Very few are nimble enough to trade oil, it’s really an insider’s game. No new capital is moving into the oil industry and oil companies themselves won’t invest in their own businesses anymore.

Q: Would you put on a new position on the iShares 20 Plus Year Treasury Bond ETF (TLT) today?

A: No, you don’t sell short things after they move down $14 points. You put them on before that. If I were to do a short-term trade in (TLT) I would be a buyer, I’d maybe buy it for a countertrend rally of maybe $4 or $5 points.

Q: What should I do with my FCX 2023 LEAP?

A: There is enough time on it, so I would keep running it along as is—don’t get greedy. Keep the LEAPS you have and you should do well by it.

Q: Could the iShares 20 Plus Year Treasury Bond ETF (TLT) bottom out in the near term?

A: Yes, it could, on a short-term basis. $141 is the nine-month low for the (TLT), so a great place to take short term profits. (TLT) is right now at $142.56, so we’re approaching that $141 handle closely. Every technical trader on the market’s going to cover their shorts on the $141 or $142 handle, so just congratulate yourself going into this move short, and take the money and run. You take every $14 point move in your favor in the (TLT); and let it rally 5 points and then reestablish, that’s how you trade.

Q: Do you think there will be a delay in the first interest rate hike due to COVID?

A: Yes, Jay Powell is the ultra-dove—any excuse to delay rate hikes, he’ll do it. And the way you’ll know is he’ll delay the end of other things which you don’t see, like daily mortgage bond purchases, daily US Treasury purchases, and other backdoor forms of QE. We’ll know well in advance if he’s going to raise or not by March or even June. We watch this stuff every day, we talk to people at the Fed every week. And remember, the Treasury Secretary Janet Yellen is a good friend of mine, I get a good handle on these things; this is why 99% of my bond trades make money.

Q: What if I have the $135-$140 put spread in January?

A: Sell it now, take what you can, take the hit; because that’ll expire at zero unless we break down to new lows on the (TLT) in the next ten days or so. That's not a good bet, especially on top of a $14 point drop. Capture what you can on that one and keep the cash for a better entry point. That’s exactly what I did—I sold all my January positions yesterday no matter what they were, because when you get to two weeks to expiration the moves become random.

Q: Do you think inflation will last longer than expected?

A: No, I think it will last shorter than expected because I think at least half of the inflation rate, if not more, are caused by supply chain problems which will end within the next six months, and therefore lead to the over-order problem that I was talking about earlier.

Q: What’s your outlook on energy this year?

A: It could go higher. On the way to zero, you’re going to have several double, tripling’s, even 10x increases in the price of oil, like we saw in the last 18 months. We went from negative numbers to 80, and what happens is oil becomes more volatile as the supply becomes more variable, that's a natural function. But trading this is not for non-professionals.

Q: Since sector rotation is happening, do you think we should sell all tech positions?

A: Short term yes, long term no. Tech will still lead with earnings, and even if they have a bad five months coming, they have a terrific long-term view. For the last 30 years, every sale of tech has been a mistake, especially in Apple (AAPL). So if you’re a trader, yes, you should have been selling since November. If you’re a long-term investor, keep them all.

Q: Is the ProShares UltraShort S&P 500 (SDS) a good position to buy up when the market timing index goes into sell territory?

A: Yes it is, and that will probably work better this year than it did last year because narrow range volatile markets are much more technically oriented than straight-up markets or long term bull markets. Pay close attention to those markets, you could make a lot of money trading them.

Q: Do Teslas have good car heaters for climates up North in -25 or -30?

A: You plug them in. When it gets below zero you actually get a warning message on your Tesla app telling you to plug it in, and then the car heats itself off of the power input. Otherwise, if you get to below zero, the range on the car drops by half. If you have a 300-mile range car like I do and then you freeze it, it drops to like 150 miles. In Tahoe, I keep my car plugged in all the time when I'm not using it, just to keep it warm and friendly.

Q: Is Zoom (ZM) a good buy here?

A: No, I think they’re going to keep punishing these overpriced small cap techs like they have been. We’re a long way from value on small tech. That was a 2020 story.

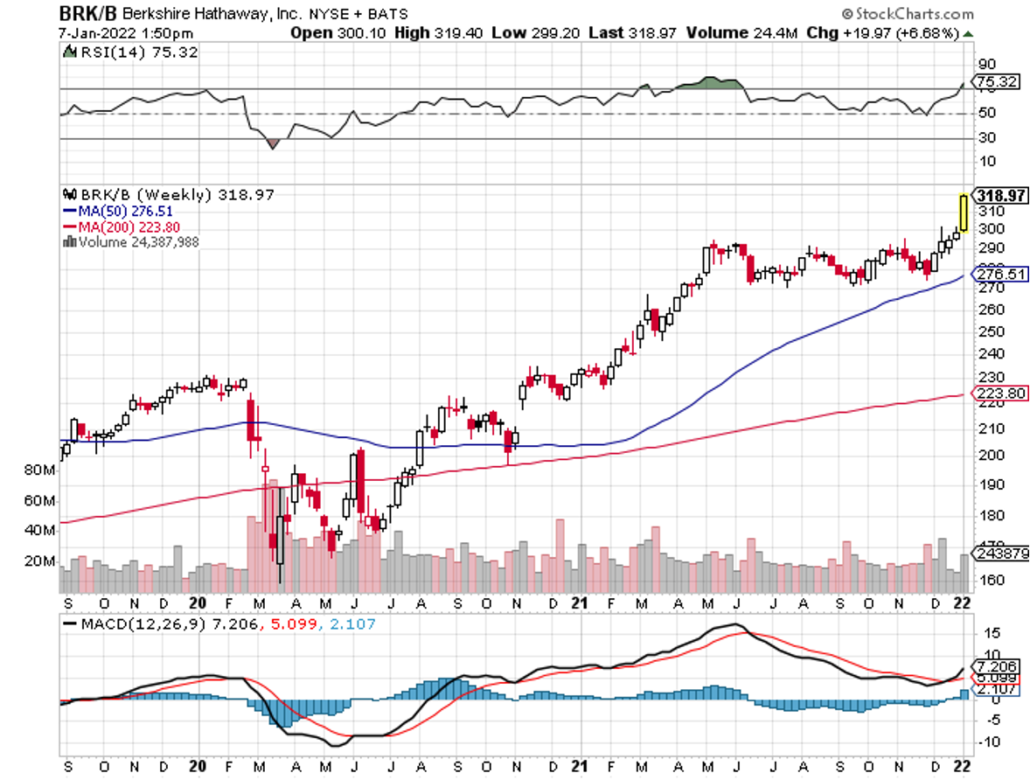

Q: What about Berkshire Hathaway (BRKB)?

A: Berkshire Hathaway is doing a major breakout because they own financials up the wazoo and they’re all breaking out. And YOU should be long up the wazoo on these things because I’ve been recommending them for the last 4 months.

Q: What do you think of Robinhood (HOOD)?

A: Robinhood I like long term, but it is high risk, high volatility. It is down 78% from the IPO so it is busted. Kind of tempting down here, but again, all the non-earning overvalued stocks are getting their clocks cleaned right here; I'm not in a rush to get involved.

Q: When you enter a LEAP, is the straight call or call spread?

A: It’s a call spread. You finance the high cost of one-year options by selling short a call option against it further out of the money. And that way you can get enormous leverage for practically nothing, 10 or 20 times in some cases, depending on how you structure the strikes.

Q: Best stock to play Copper?

A: Freeport McMoRan (FCX). I’ve been recommending it since it was $4.00.

Q: Oil is the pain train until EVs actually take over.

A: That’s true, and they haven’t. EVs have about a 6% market share now of new car sales worldwide, but that could rapidly accelerate given all the subsidies that EVs are getting. Also, we have many future recessions to worry about, during which oil could easily drop 290% like it did last year. If you can hack that kind of volatility, go for it, but I find better things to do quite honestly. And I think my next oil trade will be a short, especially if we go over $100.

Q: What about Bitcoin?

A: It could go sideways in a range for a while. If we can’t hold the 200-day, we’re going back down to the high 30,000s, where we were at the start of the year—we could give up the entire year of 2021. Bitcoin also suffers from rising interest rates since they don’t yield anything.

Q: Is this recorded?

A: Yes, the webinar recording goes out in about 2 hours. Log into the madhedgefundtrader.com website and go to my account, where you’ll find it with all the different products you’ve purchased.

Q: I just closed out my (TLT) 150 put option for the biggest single trade profit in my life; I just made 20% of my annual salary alone today. Thank you, John!

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2022/01/john-thomas-pilot-e1661438842642.png354450Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-01-07 15:02:552022-01-07 15:49:48January 5 Biweekly Strategy Webinar Q&A

I am once again writing this report from a first-class sleeping cabin on Amtrak’s legendary California Zephyr.

By day, I have two comfortable seats facing each other next to a panoramic window. At night, they fold into two bunk beds, a single and a double. There is a shower, but only Houdini could navigate it.

I am anything but Houdini, so I go downstairs to use the larger public hot showers. They are divine.

We are now pulling away from Chicago’s Union Station, leaving its hurried commuters, buskers, panhandlers, and majestic great halls behind. I love this building as a monument to American exceptionalism.

I am headed for Emeryville, California, just across the bay from San Francisco, some 2,121.6 miles away. That gives me only 56 hours to complete this report.

I tip my porter, Raymond, $100 in advance to make sure everything goes well during the long adventure and to keep me up-to-date with the onboard gossip. The rolling and pitching of the car is causing my fingers to dance all over the keyboard. Microsoft’s Spellchecker can catch most of the mistakes, but not all of them.

As both broadband and cell phone coverage are unavailable along most of the route, I have to rely on frenzied Internet searches during stops at major stations along the way to Google obscure data points and download the latest charts.

You know those cool maps in the Verizon stores that show the vast coverage of their cell phone networks? They are complete BS.

Who knew that 95% of America is off the grid? That explains so much about our country today.

I have posted many of my better photos from the trip below, although there is only so much you can do from a moving train and an iPhone 12X pro.

Here is the bottom line which I have been warning you about for months. In 2022, you are going to have to work twice as hard to earn half as much money with double the volatility.

It’s not that I’ve turned bearish. The cause of the next bear market, a recession, is at best years off. However, we are entering the third year of the greatest bull market of all time. Expectations have to be toned down and brought back to earth. Markets will no longer be so strong that they forgive all mistakes, even mine.

2022 will be a trading year. Play it right, and you will make a fortune. Get lazy and complacent and you’ll be lucky to get out with your skin still attached.

If you think I spend too much time absorbing conspiracy theories or fake news from the Internet, let me give you a list of the challenges I see financial markets are facing in the coming year:

The Ten Key Variables for 2022

1) How soon will the Omicron wave peak?

2) Will the end of the Fed’s quantitative easing knock the wind out of the bond market?

3) Will the Russians invade the Ukraine or just bluster as usual?

4) How much of a market diversion will the US midterm elections present?

5) Will technology stocks continue to dominate, or will domestic recovery, and value stocks take over for good?

6) Can the commodities boom get a second wind?

7) How long will the bull market for the US dollar continue?

8) Will the real estate boom continue, or are we headed for a crash?

9) Has international trade been permanently impaired or will it recover?

10) Is oil seeing a dead cat bounce or is this a sustainable recovery?

The Thumbnail Portfolio

Equities – buy dips Bonds – sell rallies Foreign Currencies – stand aside Commodities – buy dips Precious Metals – stand aside Energy – stand aside Real Estate – buy dips Bitcoin – Buy dips

1) The Economy

What happens after a surprise variant takes Covid cases to new all-time highs, the Fed tightens, and inflation soars?

Covid cases go to zero, the Fed flip flops to an ease and inflation moderates to its historical norm of 3% annually.

It all adds up to a 5% US GDP growth in 2022, less than last year’s ballistic 7% rate, but still one of the hottest growth rates in history.

If Joe Biden’s build-back batter plan passes, even in diminished form, that could add another 1%.

Once the supply chain chaos resolves inflation will cool. But after everyone takes delivery of their over orders conditions could cool.

This sets up a Goldilocks economy that could go on for years: high growth, low inflation, and full employment. Help wanted signs will slowly start to disappear. A 3% handle on Headline Unemployment is within easy reach.

The weak of heart may want to just index and take a one-year cruise around the world instead in 2022 (here's the link for Cunard).

So here is the perfect 2022 for stocks. A 10% dive in the first half, followed by a rip-roaring 20% rally in the second half. This will be the year when a big rainy-day fund, i.e., a mountain of cash to spend at market bottoms, will be worth its weight in gold.

That will enable us to load up with LEAPS at the bottom and go 100% invested every month in H2.

That should net us a 50% profit or better in 2022, or about half of what we made last year.

Why am I so cautious?

Because for the first time in seven years we are going to have to trade with a headwind of rising interest rates. However, I don’t think rates will rise enough to kill off the bull market, just give traders a serious scare.

The barbell strategy will keep working. When rates rise, financials, the cheapest sector in the market, will prosper. When they fall, Big Tech will take over, but not as much as last year.

The main support for the market right now is very simple. The investors who fell victim to capitulation selling that took place at the end of November never got back in. Shrinking volume figures prove that. Their efforts to get back in during the new year could take the S&P 500 as high as $5,000 in January.

After that the trading becomes treacherous. Patience is a virtue, and you should only continue new longs when the Volatility Index (VIX) tops $30. If that means doing nothing for months so be it.

We had four 10% corrections in 2021. 2022 will be the year of the 10% correction.

Energy, Big Tech, and financials will be the top-performing sectors of 2022. Big Tech saw a 20% decline in multiples in 2022 and will deliver another 30% rise in earnings in 2022, so they should remain at the core of any portfolio.

It will be a stock pickers market. But so was 2021, with 51% of S&P 500 performance coming from just two stocks, Tesla (TSLA) and Alphabet (GOOGL).

However, they are already so over-owned that they are prone to dead periods as long as eight months, as we saw last year. That makes a multipronged strategy essential.

Amtrak needs to fill every seat in the dining car to get everyone fed on time, so you never know who you will share a table with for breakfast, lunch, and dinner.

There was the Vietnam Vet Phantom Jet Pilot who now refused to fly because he was treated so badly at airports. A young couple desperately eloping from Omaha could only afford seats as far as Salt Lake City. After they sat up all night, I paid for their breakfast.

A retired British couple was circumnavigating the entire US in a month on a “See America Pass.” Mennonites are returning home by train because their religion forbade automobiles or airplanes.

The national debt ballooned to an eye-popping $30 trillion in 2021, a gain of an incredible $3 trillion and a post-World War II record. Yet, as long as global central banks are still flooding the money supply with trillions of dollars in liquidity, bonds will not fall in value too dramatically. I’m expecting a slow grind down in prices and up in yields.

The great bond short of 2021 never happened. Even though bonds delivered their worst returns in 19 years, they still remained nearly unchanged. That wasn’t good enough for the many hedge funds, which had to cover massive money-losing shorts into yearend.

Instead, the Great Bond Crash will become a 2022 business. This time, bonds face the gale force headwinds of three promised interest rates hikes. The year-end government bond auctions were a complete disaster.

Fed borrowing continues to balloon out of control. It’s just a matter of time before the last billion dollars in government borrowing breaks the camel’s back.

That makes a bond short a core position in any balanced portfolio. Don’t get lazy. Make sure you only sell a rally lest we get trapped in a range, as we did for most of 2021.

For the first time in ages, I did no foreign exchange trades last year. That is a good thing because I was wrong about the direction of the dollar for the entire year.

Sometimes, passing on bad trades is more important than finding good ones.

I focused on exploding US debt and trade deficits undermining the greenback and igniting inflation. The market focused on delta and omicron variants heralding new recessions. The market won.

The market won’t stay wrong forever. Just as bond crash is temporarily in a holding pattern, so is a dollar collapse. When it does occur, it will happen in a hurry.

5) Commodities (FCX), (VALE), (DBA)

The global synchronized economic recovery now in play can mean only one thing, and that is sustainably higher commodity prices.

The twin Covid variants put commodities on hold in 2021 because of recession fears. So did the Chinese real estate slowdown, the world’s largest consumer of hard commodities.

The heady days of the 2011 commodity bubble top are now in play. Investors are already front running that move, loading the boat with Freeport McMoRan (FCX), US Steel (X), and BHP Group (BHP).

Now that this sector is convinced of an eventual weak US dollar and higher inflation, it is once more the apple of traders’ eyes.

China will still demand prodigious amounts of imported commodities once again, but not as much as in the past. Much of the country has seen its infrastructure build out, and it is turning from a heavy industrial to a service-based economy, like the US. Investors are keeping a sharp eye on India as the next major commodity consumer.

And here’s another big new driver. Each electric vehicle requires 200 pounds of copper and production is expected to rise from 1 million units a year to 25 million by 2030. Annual copper production will have to increase 11-fold in a decade to accommodate this increase, no easy task, or prices will have to ride.

The great thing about commodities is that it takes a decade to bring new supply online, unlike stocks and bonds, which can merely be created by an entry in an excel spreadsheet. As a result, they always run far higher than you can imagine.

Accumulate commodities on dips.

Snow Angel on the Continental Divide

6) Energy (DIG), (RIG), (USO), (DUG), (UNG), (USO), (XLE), (AMLP)

Energy may be the top-performing sector of 2022. But remember, you will be trading an asset class that is eventually on its way to zero.

However, you could have several doublings on the way to zero. This is one of those times.

The real tell here is that energy companies are drinking their own Kool-Aid. Instead of reinvesting profits back into their new exploration and development, as they have for the last century, they are paying out more in dividends.

There is the additional challenge in that the bulk of US investors, especially environmentally friendly ESG funds, are now banned from investing in legacy carbon-based stocks. That means permanently cheap valuations and shares prices for the energy industry.

Energy stocks are also massively under-owned, making them prone to rip-you-face-off short squeezes. Energy now counts for only 3% of the S&P 500. Twenty years ago it boasted a 15% weighting.

The gradual shut down of the industry makes the supply/demand situation more volatile. Therefore, we could top $100 a barrel for oil in 2022, dragging the stocks up kicking and screaming all the way.

Unless you are a seasoned, peripatetic, sleep-deprived trader, there are better fish to fry.

The train has added extra engines at Denver, so now we may begin the long laboring climb up the Eastern slope of the Rocky Mountains.

On a steep curve, we pass along an antiquated freight train of hopper cars filled with large boulders.

The porter tells me this train is welded to the tracks to create a windbreak. Once, a gust howled out of the pass so swiftly, that it blew a passenger train over on its side.

In the snow-filled canyons, we saw a family of three moose, a huge herd of elk, and another group of wild mustangs. The engineer informs us that a rare bald eagle is flying along the left side of the train. It’s a good omen for the coming year.

We also see countless abandoned 19th century gold mines and the broken-down wooden trestles leading to them, relics of previous precious metals booms. So, it is timely here to speak about the future of precious metals.

Fortunately, when a trade isn’t working, I avoid it. That certainly was the case with gold last year.

2021 was a terrible year for precious metals. With inflation soaring, stocks volatile, and interest rates going nowhere, gold had every reason to rise. Instead, it fell for almost all of the entire year.

Bitcoin stole gold’s thunder, sucking in all of the speculative interest in the financial system. Jewelry and industrial demand was just not enough to keep gold afloat.

This will not be a permanent thing. Chart formations are starting to look encouraging, and they certainly win the price for a big laggard rotation. So, buy gold on dips if you have a stick of courage on you.

Would You Believe This is a Blue State?

8) Real Estate (ITB), (LEN)

The majestic snow-covered Rocky Mountains are behind me. There is now a paucity of scenery, with the endless ocean of sagebrush and salt flats of Northern Nevada outside my window, so there is nothing else to do but write.

My apologies in advance to readers in Wells, Elko, Battle Mountain, and Winnemucca, Nevada.

It is a route long traversed by roving banks of Indians, itinerant fur traders, the Pony Express, my own immigrant forebearers in wagon trains, the transcontinental railroad, the Lincoln Highway, and finally US Interstate 80, which was built for the 1960 Winter Olympics at Squaw Valley.

Passing by shantytowns and the forlorn communities of the high desert, I am prompted to comment on the state of the US real estate market.

There is no doubt a long-term bull market in real estate will continue for another decade, although from here prices will appreciate at a 5%-10% slower rate.

There is a generational structural shortage of supply with housing which won’t come back into balance until the 2030s.

There are only three numbers you need to know in the housing market for the next 20 years: there are 80 million baby boomers, 65 million Generation Xer’s who follow them, and 86 million in the generation after that, the Millennials.

The boomers have been unloading dwellings to the Gen Xers since prices peaked in 2007. But there are not enough of the latter, and three decades of falling real incomes mean that they only earn a fraction of what their parents made. That’s what caused the financial crisis.

If they have prospered, banks won’t lend to them. Brokers used to say that their market was all about “location, location, location.” Now it is “financing, financing, financing.” Imminent deregulation is about to deep-six that problem.

There is a happy ending to this story.

Millennials now aged 26-44 are now the dominant buyers in the market. They are transitioning from 30% to 70% of all new buyers of homes.

The Great Millennial Migration to the suburbs and Middle America has just begun. Thanks to Zoom, many are never returning to the cities. So has the migration from the coast to the American heartland.

That’s why Boise, Idaho was the top-performing real estate market in 2021, followed by Phoenix, Arizona. Personally, I like Reno, Nevada, where Apple, Google, Amazon, and Tesla are building factories as fast as they can.

As a result, the price of single-family homes should rocket during the 2020s, as they did during the 1970s and the 1990s when similar demographic forces were at play.

This will happen in the context of a coming labor shortfall, soaring wages, and rising standards of living.

Rising rents are accelerating this trend. Renters now pay 35% of their gross income, compared to only 18% for owners, and less, when multiple deductions and tax subsidies are taken into account. Rents are now rising faster than home prices.

Remember, too, that the US will not have built any new houses in large numbers in 13 years. The 50% of small home builders that went under during the crash aren’t building new homes today.

We are still operating at only a half of the peak rate. Thanks to the Great Recession, the construction of five million new homes has gone missing in action.

That makes a home purchase now particularly attractive for the long term, to live in, and not to speculate with.

You will boast to your grandchildren how little you paid for your house, as my grandparents once did to me ($3,000 for a four-bedroom brownstone in Brooklyn in 1922), or I do to my kids ($180,000 for a two-bedroom Upper East Side Manhattan high rise with a great view of the Empire State Building in 1983).

That means the major homebuilders like Lennar (LEN), Pulte Homes (PHM), and KB Homes (KBH) are a buy on the dip.

Quite honestly, of all the asset classes mentioned in this report, purchasing your abode is probably the single best investment you can make now. It’s also a great inflation play.

If you borrow at a 3.0% 30-year fixed rate, and the long-term inflation rate is 3%, then, over time, you will get your house for free.

How hard is that to figure out? That math degree from UCLA is certainly earning its keep.

Crossing the Bridge to Home Sweet Home

9) Bitcoin

It’s not often that new asset classes are made out of whole cloth. That is what happened with Bitcoin, which, in 2021, became a core holding of many big institutional investors.

But get used to the volatility. After doubling in three months, Bitcoin gave up all its gains by year-end. You have to either trade Bitcoin like a demon or keep your positions so small you can sleep at night.

By the way, right now is a good place to establish a new position in Bitcoin.

10) Postscript

We have pulled into the station at Truckee in the midst of a howling blizzard.

My loyal staff has made the ten-mile trek from my beachfront estate at Incline Village to welcome me to California with a couple of hot breakfast burritos and a chilled bottle of Dom Perignon Champagne, which has been resting in a nearby snowbank. I am thankfully spared from taking my last meal with Amtrak.

After that, it was over legendary Donner Pass, and then all downhill from the Sierras, across the Central Valley, and into the Sacramento River Delta.

Well, that’s all for now. We’ve just passed what was left of the Pacific mothball fleet moored near the Benicia Bridge (2,000 ships down to six in 50 years). The pressure increase caused by a 7,200-foot descent from Donner Pass has crushed my plastic water bottle. Nice science experiment!

The Golden Gate Bridge and the soaring spire of Salesforce Tower are just around the next bend across San Francisco Bay.

A storm has blown through, leaving the air crystal clear and the bay as flat as glass. It is time for me to unplug my Macbook Pro and iPhone 13 Pro, pick up my various adapters, and pack up.

We arrive in Emeryville 45 minutes early. With any luck, I can squeeze in a ten-mile night hike up Grizzly Peak and still get home in time to watch the ball drop in New York’s Times Square on TV.

I reach the ridge just in time to catch a spectacular pastel sunset over the Pacific Ocean. The omens are there. It is going to be another good year.

I’ll shoot you a Trade Alert whenever I see a window open at a sweet spot on any of the dozens of trades described above.

Good luck and good trading in 2022!

John Thomas

The Mad Hedge Fund Trader

The Omens Are Good for 2022!

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-01-05 13:00:512022-01-05 18:26:592022 Annual Asset Class Review

Below please find subscribers’ Q&A for the October 20 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from the safety of Silicon Valley.

Q: Why are stocks so high? Won’t inflation hurt companies?

A: Inflation hurts bonds (TLT), not companies, which is why we are short the bond market and have been short for most of this year. Inflation actually helps companies because it allows them to raise prices at a faster rate. The ability to raise prices is the best that it’s been in 45 years, and that is enabling them to either maintain or increase profit margins.

Q: Where is all this liquidity coming from to drive the stocks high after the Fed ends Quantitative easing?

A: In the last 20 years, the liquidity of the US has gone from 6% of GDP to 47% of GDP. That is an enormous increase, and most of that money has gone into stocks and real estate, which is why both have been on a tear for the last 11 years. And I expect that to continue; the Fed isn’t even hinting at taking liquidity out of the system until well into 2023. On top of that, you have corporate profit exploding from $2 trillion last year to $10 trillion this year, adding another $8 trillion to the system, and outpacing any Fed taper by a five to one margin. Corporations alone are using these profits to buy back more than $1 trillion of their own stock this year.

Q: I’m hearing so much about the supply chain problems these days. Is that just a short-term fixable problem or a long-term structural one?

A: Absolutely it’s short-term. This actually isn’t a pandemic-related problem but a private capital investment one. It’s being caused by the record growth of the US economy which is sucking in more imports than it has ever seen before. We’ve actually exceeded pre-pandemic levels of imports a while ago. Import infrastructure isn’t big enough to handle it. If it was there wouldn’t be enough truckers to handle it. We had a shortage of 50,000 truckers before the pandemic, now we’re short 100,000. Some of these guys are making up to $100,000 a year, not bad for a high school level education. Expect it to get worse before it gets better, but it will get better eventually. That is why Amazon is having trouble, because supply chain problems may bring a weak Christmas, which is the most profitable time of year for them. If we get any big selloff at Amazon for this reason, you want to buy that bottom because it’ll double again in 3 years.

Q: Walt Disney (DIS) has pretty much sideways the whole year around $70, is this going down or should I buy?

A: I would look to buy but I would buy an in-the-money LEAPS, like a $150-$170 one year out. Disney’s been hit with a lot of slowdowns lately, slowdowns with park reopening, movie releases, new streaming customers. But these are all temporary slowdowns and will pick up again next year. Disney is the classic reopening play, so you will get another bite at the apple with a second reopening. Maybe “bite of the mouse” is a better metaphor.

Q: Global growth is down because of China (FXI) with their PMI under 50; do you think they will drag down the entire global economy in 2022?

A: No, if we recover, their largest customer, they will recover too. Remember their pandemic cases are only a tiny fraction of what ours were, some 4,000 or so, and their economy is still export-driven. You can't have major port congestion in Los Angeles and a weak economy in China, those are just two ends of one chain. I would look for a recovery in China next year. As for the stocks, I don’t know because that’s an entirely political issue; Baidu (BIDU), (JD), and Alibaba (BABA) are still getting beaten like a redheaded stepchild. We don’t know when that’s going to end; it’s an unknown. So, stand aside on Chinese plays, especially when the stuff at home is so much better with all these financials and tech stocks to invest in.

Q: What do you think about meme stocks?

A: I think you should avoid them like the plague. When there are so many good quality stocks with long term uptrends, why bother dumpster diving? You’re better off buying a lottery ticket.

Q: Which US bank should I invest in?

A: If you want the gold standard, you buy JP Morgan (JPM) which just announced blowout earnings. If you want a broker, go for Morgan Stanley (MS), which also just announced blowout earnings last week. And I want you to make my monthly pension payment secure, as it comes from Morgan Stanley. Keep those checks coming!

Q: Are we headed to $150 oil (USO)?

A: No, what we’re seeing here is a short-term spike in prices due to supply chain problems, OPEC discipline, a booming economy, and Russia trying to squeeze Europe on energy supplies. I don’t see it continuing much per year as the stocks could be popping out, so avoid oil and energy plays. The solar plays, like (TAN), (FSLR), and (SPWR) on the other hand, all look like they have miles to go.

Q: You said in your Webinar that you can still get a 50% Return on the United States Treasury Bond Fund (TLT) LEAPS. Can you give me the specifics?

A: If you went a year out on Tuesday when I recorded this webinar, you could buy the (TLT) October 2022 $150-$150 vertical bear put spread for $3.40 for a maximum profit on expiration at $5.00 of $47%. That’s where you buy the $155 put and sell short the $150 put against it. Since then, bonds have fallen by $3.00, and it is now trading at $3.60 giving you a 39% return. Try to establish this position on the next (TLT) rally.

Q: What is your yearend target for Bitcoin?

A: Now that we have broken the old high at $66,000, we should be able to make it to $100,000 by January. The SEC approving that new ProShares Bitcoin Strategy ETF (BITO) ETF unlocks trillions of dollars which can now go into Bitcoin, those regulated by the Investment Company Act of 1940. Crypto is now the fastest-growing segment of the financial markets. It’s inflation that driving this, and the Fed is throwing fuel on the fire by taking no action in the face of a red hot 5.4% Consumer Price Index. Even if the Fed does taper, the action will be more than offset by the massive $8 trillion increase in corporate profits. Companies are not only buying their own stocks, they are also using these profits to buy Bitcoin. I see this as a Bitcoin node myself. Be sure to dollar cost average your position by putting in a little bit of money every day because Bitcoin is wildly volatile, up 140% since August 1. By the way, it’s not too late to subscribe to the Mad Hedge Bitcoin Letter, which we are taking down from the store on Monday for a major upgrade by clicking here. We are raising prices after that.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on the paid service you are currently in (GLOBAL TRADING DISPATCH, TECH LETTER, or BITCOIN LETTER), then select WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good luck and stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2020/07/John-Thomas-bull2.png514454Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-10-22 11:02:452021-10-22 11:52:17October 20 Biweekly Strategy Webinar Q&A

Below please find subscribers’ Q&A for the September 22 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from the safety of Silicon Valley.

Q: When’s the United States US Treasury bond fund (TLT) going to go down?

A: When J. Powell tapers, which will be either today or in 6 weeks. That's the time frame we’re looking at now, and people are positioning now for the taper—that's why financials are taking off like a rocket. Buy those financials and don't expect too much from your tech stocks for the next few months.

Q: What do you think of adding corporate or municipal bonds to my portfolio?

A: Don’t do that on pain of death please; you will lose money. Corporate bonds will get slaughtered the second interest rates turn because they have the most exposure from a credit point of view to any downgrades resulting from rising interest rates. Better to keep your money in cash than buy bonds here. It was a great idea 10 years ago, but a terrible idea today. Just buy cash or buy extremely deep-in-the-money LEAPS which will get you a 10-20% per year return.

Q: What are the chances that the government defaults?

A: Zero, because corporate profits this year will increase from $2 trillion to $10 trillion, spinning off massive tax revenues for the government. The deficit will come down substantially in the future as a result. Keep expecting upwards surprises in profits and taxable revenues. That may be why the (TLT) is staying so high.

Q: I need a customized LEAPS on a stock.

A: We do those for our concierge customers. If you’re interested, then email Filomena at customer support at support@madhedgefundtrader.com.

Q: What brand of shot did you get?

A: Pfizer (PFE).

Q: The Government is showing no sign of balancing a budget and the hole will only get deeper; what are your thoughts?

A: I agree, and that’s why I'm short the (TLT). All we need is a taper to really get some juice under that trade; we really don’t need that much. Ten-year US Treasury yields are now around 1.30% and we only need the yield to get up to about 1.70% for us to make a maximum profit on our positions. One taper hint and it could get us up to those levels.

Q: Why is Visa (V) dropping so much?

A: Fear of being replaced by Bitcoin. This is the big thing dragging all three credit card companies down, including American Express (AXP) and master Card (MA). That's why I have not added a Visa position among my financials in this go around.

Q: How can the Fed unwind their balance sheet and normalize interest rates to a historical average of 4-5%?

A: Quite easily: quit buying bonds. They’re still buying $120 billion/month worth. Technology has accelerated with the pandemic and we all know this is highly deflationary. I expect the next peak in interest rates to be only 3% or 3.5%, not the 6% we saw in the last peak in interest rates in the 2000s. So yeah, bonds are going to go down but not back to 2000’s level.

Q: Thoughts on the Johnson & Johnson (JNJ) shot?

A: No thank you. If you get to choose, Moderna (MRNA) is now producing the best immunity data on a year-to-date basis if you’re starting out from scratch. Some people are mixing, they start out with Pfizer and then get Moderna. They get a worse reaction because the Moderna initial reaction shot sees the Pfizer vaccine as a new virus, so you may get a small flu as a result of that.

Q: What is the put spread you’re recommending on the TLT?

A: The May 2022 $150-$155 vertical put spread. That is the sweet spot now on the short side on (TLT) LEAPS. You should earn a 115% profit in eight months on this trade if interest rates remain unchanged or fall.

Q: Do you expect the ProShares Ultra Short 20 year+ Treasury ETF (TBT) to make it to $20 this year?

A: Yes, I do; $16 to $20 isn’t that much of a move. Remember, the (TBT) is a two times short ETF.

Q: Are you recommending bank stocks?

A: Yes, Morgan Stanley (MS) and JP Morgan (JPM) are two of the best. They will lead the yearend rally starting from here.

Q: When do you expect the semiconductor shortage to end?

A: End of next year, or maybe even 2023, because what all the analysts keep underestimating is that the end of shortages is based on companies getting the chips they want today. The actual issue is that companies are designing billions of chips into their products at an exponential rate, and what they’ll need in a year from now is far higher than most people realize. The semiconductor shortage is much more structural than people realize—that's my theory. They don’t throw up a $2 billion fab overnight. So, this will keep going on for a while and be a drag on economic growth.

Q: Are you sure we won’t see $100 oil (USO)?

A: With oil, you're never sure about anything, although I highly doubt it. We’d have to have monster economic growth in China to get oil up to $100 a barrel. Right now, China is going the other way.

Q: What’s your view on the debt ceiling? Will it give us a good buying opportunity?

A: Probably not, our good buying opportunity was yesterday or Monday. These debt crises are always one minute before midnight solutions. They always get solved. Never underestimate the ability of Congressmen to spend money in their own district. So, I don’t think that would create a stock market crash like it might have done 20 years ago.

Q: What about Freeport McMoRan (FCX)?

A: It’s taking a dip here because of a possible real estate crash in China, and of course China is the world’s largest buyer of copper for apartment construction. I’m kind of taking a break here on Freeport McMoRan and US Steel (X) until we learn a little more about the China situation. They did move to start a bailout today. Let’s see if that continues.

Q: When will the airlines come back?

A: They’ll come back when business travel returns, which I think could be next year. If you eliminate the virus completely, these things double easily. That's the bet you’re making. Let’s see if the covid boosters work, the childhood shots work, and then you can take another look at Delta (DAL) and Alaska (ALK).

Q: If Bitcoin gains mass adoption, does that put banks out of business just like electric vehicles are making oil obsolete?

A: No, not if the banks go into the Bitcoin business. And the banks actually have the cash, resources, and infrastructure to take over the Bitcoin area once the technology matures. And the corollary to that is that the oil industry is that the majors have the infrastructure, the manpower, and the capital to take over the alternative energy business if they choose to do so and oil goes to zero, which it eventually will. The proof of that is the largest investor in all the Silicon Valley energy startups are Saudi Arabian venture capital funds. They’re huge investors in solar here. If Saudi Arabia has a lot of oil, they have even more solar. Believe me, I’ve been there.

Q: Will a lack of inventory and rising interest rates end the bidding wars on houses soon?

A: Only if you consider 10 years soon. That is how long it will take for the sizes of different generations to come into balance, the Millennials (85 million) versus the Gen Xers (45 million). That’s when the housing bubble will end, but that won’t be for another decade. We still have a structural shortage of new home construction (about 5 million units a year) because all the home builders who went bust in the financial crisis in 2008/2009 and never came back—all of that new construction is still missing. And the surviving ones haven’t increased production to meet that shortfall because they want to manage their risk. Eventually, they will and that probably will be the next top, but that’s really 2030 type business.

Q: What about Federal Express (FDX)?

A: Labor shortages. It's hitting (UPS), (FDX), the Post Office, and DHL too—all the couriers.

Q: When do you think gold (GLD) and silver (SLV) rise back to 2,000?

A: I am avoiding gold and silver as long as Bitcoin has buyers. The action in Bitcoin is 10x the movement you get in gold and that’s attracted all the speculative capital in the market, draining all interest from gold, which hit a new six-month low just last week.

Q: What’s your buy target for Apple (AAPL)?

A: I would say if you can get it at $135, that would be a gift. We did get close to $140 at the lows this week; that’s when you start nibbling, and then you double up again at $135. I doubt Apple is going down more than 10% in this cycle. There are too many people still trying to get into it. And they’re still the largest buyer of stock in the world. They only buy one stock, their own.

Q: I never got any IPath Series B S&P 500 VIX Short Term Futures ETN (VXX) alerts.

A: That's because we never sent any out. (VIX) has become an incredibly difficult game to play, accumulating positions for months and then trying to get out on a one-day spike that lasts a few minutes. The insiders have too much of a house advantage here, who only play from the short side. There are too many better fish to fry.

Q: What about the Apple electric vehicle?

A: I’ll believe it when I see it; I've been hearing about this for something like seven years. My guess is that Apple is more likely to supply consoles and parts to other EV makers and help them get into the game with software and so on. I think that will be Apple's role in all of this.

Q: How much has China Evergrande Group stock fallen?

A: It’s a really illiquid stock in China so we never got involved in it. I think it’s down more than half. Even the professional short-sellers like Jim Chanos and Kyle Bass, have been targeting that stock for 10 years are now screaming they’re vindicated. Of course, they lost fortunes in the meantime. So, I'll pass on that one.

Q: What about stop losses on LEAPS trades?

A: I don’t really run LEAPS portfolios or issue stop losses. The idea is to run these into expiration, and we’ve never had one expire out of the money, although I may break that record if TLT doesn’t turn around in the next three months.

Q: How would autonomous trucking impact rail transportation?

A: They’re two totally different things. Trucking companies like Yellow Corporation (YELL) carry smaller cargo for local deliveries or small long-distance deliveries. 7Some 70% of all railroad traffic is coal going to China, and the rest is bulk commodities like wood chips, iron ore, etc. Trucks don’t carry any of that, so they’re totally separate businesses. But, if we went totally autonomous on trucking, it would make all the main trucker companies massively profitable, as they get rid of their drivers. Right now, every trucking company in the US has a driver shortage.

Q: United Airlines (UAL) pilots are now ordered to get vaccinated.

A: I think within months to hold a job anywhere in the US, you will have to get vaccinated. They do not want you in the office without a vaccination. Jobs are not worth risking lives, and we hit 2,000 deaths again yesterday. The corporations are taking the lead, not the government. The exception will be the politically motivated companies, like the My Pillow Guy; I doubt they'll ever require vaccinations at My Pillow. And there are a few other companies such as Hobby Lobby that are also anti-vaxers. But all public transport companies, hospitals, etc., are going to say get vaccinated or get out—it’s very simple.

Q: Should I buy Berkshire (BRKB) here?

A: Yes, it’s a great entry point, even if you can't get my price. Go higher in the strikes or go farther out in maturity.

Q: Is copper metal (CPER) a buy here?

A: Probably long term, but short term will be subject to the whims of the Chinese real estate crisis if there is one.

Q: Won’t Natural Gas (UNG) outperform in the power grid since all EVs must be charged?

A: Not if the grid is 100% electric. Natural gas still has carbon in it, although only half as much as oil or gasoline. I think even natural gas eventually gets phased out because you can expect solar panels to improve by 80% over the next ten years. At that point, any other energy source won’t be able to compete—oil, natural gas, you name it. And that is why you don’t see any long-term money going into carbon energy sources.

Q: Iron ore has just gone from $200 to $100, why are you bullish?

A: Yes, Because it has just gone from $200 to $100. Eventually, China recovers, despite a short-term financial and housing crisis. Buy low, sell high—that’s my revolutionary new strategy.

Q: What are your thoughts on Bitcoin vs Ethereum?

A: I think Ethereum will outperform Bitcoin because it has a more modern technology. It’s only six years old, vs 12 years for Bitcoin. It’s also more efficient, using less energy in its production. In fact, we did get a double in Ethereum in August as opposed to only a 50% move in Bitcoin.

Q: Do you have any concerns on holding the financials through earnings in October?

A: No, I think the results will be fantastic, and I want to be long going into those.

Q: What does the current situation with China mean for Alibaba (BABA)?

A: Keep your stocks, you’ve already taken the hit—down 53%. The next surprise is that China quits beating up on capitalism and these things will all recover bigtime. However, any options you may have could expire before that happens. So, keep the stocks, get rid of the options, salvage whatever time value you can, and then wait for China to start doing the right thing.

Q: What are the best solar stocks?

A: First Solar (FSLR) and SunPower (SPWR), which have both done great.

Q: If bonds are a no-no, and governments are getting more indebted than ever, who will buy them?

A: Governments. The only buyers of bonds now are non-economic buyers. Those would be governments, central banks, and banks who are required by law to own certain amounts of bonds to meet regulatory capital requirements. No individual in their right mind is buying any bonds here at all, nor is any financial advisor recommending them.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2019/03/tootsie.png331522Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-09-24 09:02:442021-09-24 11:19:08September 22 Biweekly Strategy Webinar Q&A

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.