Below please find subscribers’ Q&A for the September 8 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from the safety of Silicon Valley.

Q: Do you think we’ll see the under $130 in the United States Treasury Bond Fund (TLT) before January 2022?

A: I don’t think so; I think we could go below $140, maybe below $135. But $130 would be a brand new low in the move and would be a stretch. We basically lost 4 months on this trade due to the countertrend rally, which just ended. I would come out of your (TLT) $130-$135 vertical bear put spreads right here while they still have time value, but keep the $135-$ 140s, the $140-$145’s, and especially the $150-$155’s. The idea was that you just keep averaging up and up until the market turns, and then you make back any loss. We move into accelerated time decay on those deep out of the money put spreads in December, so I would take the money and then offset it with the gains you made in those positions.

Q: Does Palantir (PLTR) look like it’ll hit $100 by year-end?

A: No, the stock has been dead, and management has not been doing anything to promote it. We did get a move up to $45 but it failed. It’s still a great long-term idea as they are growing at 50% a year. Also, they did buy $50 million worth of gold bars as a hedge. But as a short-term trader, Palantir isn’t working. If you have an options position on that I would probably get out of it or roll it forward to 2023.

Q: PayPal (PYPL) is fluctuating up and down with Bitcoin. Do you like PayPal?

A: Absolutely, but it obviously is being dragged down by Bitcoin. It is a temporary down move caused by a one-time-only event in El Salvador. Buy the dip in PayPal. It is a leader in the whole move into a digital financial system.

Q: When is Freeport McMoRan (FCX) likely to move up?

A: As soon as we shift out of the tech trade into the domestic recovery trade, which could be in weeks or months at the latest. We’ll switch from one side of the barbell to the other.

Q: Where do you see Tesla (TSLA)?

A: It keeps going up, so my guess is we top $800 by the end of the year, and maybe $850. The big news here is that Tesla has gone into the chip business, making its own chips in-house which is easy for them to do in Silicon Valley. But it does make them the first global car maker that is also a chip maker, and therefore the stock deserves a higher premium. The stock went up $30 on the news and is great for all Tesla holders. I hope you have the 2023 LEAPS.

Q: Too late to buy Tesla LEAPS?

A: Unless you’re really deep in the money, with something like a $600-$650; but the return on that will only be about 50% in 2 years.

Q: The Biden administration just set a goal of 45% solar by the end of 2050. Which solar stock should I buy here?

A: The problem with solar is as soon as Biden started winning primaries, every solar stock took off like a rocket, figuring he’d win, which he did. All of them went up 6-fold or more as a result of that, then gave up one-third of their gains and are now moving sideways. So if you look at the charts, the classic one to buy here is the Invesco Solar ETF (TAN), a basked of the top solar companies. All of these peaked in February and have been doing sideways “time” corrections since then, which means they eventually want to go higher. The other two that have charts that look like they’re finally starting to break out to the upside are First Solar (FSLR) and SunPower (SPWR) after 8 months of consolidation.

Q: Why is the second half of September almost always bad? Is it due to institutional repositioning?

A: Not really, the cash comes into the market at certain times of the year, like end of the year, beginning of the year, and end of each quarter. September seems like the month where they kind of just run out of money. But there's actually also a historical reason for that. For most of American history, we had an agricultural economy. Farmers were more than half the population, and the period of maximum distress for farmers is September, where they put all the money into seed and fertilizer and labor into the field, but they haven't harvested it yet. So, traditionally, they always did a lot of borrowing in September, which caused a cash squeeze and interest rate spike, and a stock market panic as a result. So that's the history behind weak Septembers and Octobers. Once the farmers get the crops in and sell them, that resolves the cash squeeze, interest rates fall, and it’s straight up for stocks for the rest of the year most of the time.

Q: SPACs (Special Purpose Acquisition Companies) seem to be losing interest. Do you recommend any or stay away?

A: Stay away—they’re all rip-offs and are simply a means by which managers can increase their fees from 2% to 20%. That's what they did with virtually all of them. This will end in tears.

Q: What's your feeling about satellite internet phone service replacing current internet cell service in the future?

A: It’s in the future, but it may be 10 years off in the future. If it happens sooner, it’s because Elon Musk was able to deliver cheap rocket service. He already has 20,000 satellites in the sky for his own Starlink global cell phone service for internet access.

Q: How does one buy a Bitcoin stock?

A: Well first of all, I highly recommend you buy the Mad Hedge Bitcoin Letter, which you can get in our store. But there's also the Greyscale Bitcoin Trust (GBTC) which allows you to buy a Bitcoin proxy very easily. I’ll even honor the discounted $995 price for my Bitcoin Letter for another day by clicking here.

Q: Is Warren Buffet and his value philosophy something I should be following, or is he outdated?

A: I have to say, buying stocks cheap with high cash flow will never go out of style. Currently, Warren’s big holdings are domestic industrials, banks, and Apple. All of those look like they will do well moving forward. Buffet’s Berkshire Hathaway (BRKB) has a built-in barbell element to it and is the subject of one of our LEAPS recommendations which has already been hugely successful.

Q: Is Home Depot (HD) at $330 a bargain?

A: Well, we just had a selloff and it bounced hard, and now we’re waiting for the domestic post delta recovery. It's hard to imagine both Home Depot and Lowes not doing well in this scenario.

Q: What will happen to tech when interest rates rise?

A: My bet is they go sideways to down small until you get another peak in interest rates (the next peak will be at 1.76% in the ten year US Treasury bond, the 2021 high) and once you hit that, then tech will take off like a rocket again, and in the meantime, you play the domestics while interest rates are rising. That is the game and will continue to be the game for a couple of years.

Q: Should I buy IBM (IBM) on a turnaround story?

A: No, I've been waiting for IBM to turn around for 10 years. They just don’t seem to get it. What they do is whenever a division starts to make money, they sell it and get cash like they did with the PC division and this year with its infrastructure business called Kyndryl. So, they’re not leaving any growth for the actual IBM holders.

Q: Do you like Square (SQ) at $256?

A: Yes, and that would be a great 2023 LEAPS candidate. All of the digital settlement payment systems are going to do well in the Bitcoin future. They also own quite a lot of Bitcoin. They are leading the charge into a digitized financial system.

Q: What’s a good Ethereum ETF?

A: The Greyscale Ethereum Trust (ETHE) is just the ticket.

Q: So you avoid energy, meaning oil and gas?

A: Yes, alternative energy we like, but it’s had an enormous run already so after a 7-month time correction it’s probably safe to get into solar. Traditional oil and gas (USO) is in a long-term secular bear market that started 13 years ago and will eventually go to zero. Last year’s visit to negative futures prices is just a start. Since 2020, the energy market weighting has gone from 15% to 2%.

Q: Is Natural Gas the only rational core fuel for the grid?

A: No, natural gas (UNG) still produces carbon even though it’s only half the amount of oil. This all gets replaced by solar in the next ten years. That’s why I tell people to stay away from energy like the plague. Would you rather buy natural gas at $4.50/btu or get solar electricity for free? Those are basically going to be the choices in ten years.

Q: Who is the biggest Aluminum producer?

A: Alcoa (AA) which we are a buyer on dips. By the way, if we do have to build 200,000 miles of long-distance transmission lines to cover the electrification of the US energy supply, all of that has to be made of aluminum. You don't use copper for long distances, you use aluminum (aluminum for you Brits).

Q: Would you buy Uber (UBER) at $40 today?

A: Probably, yes; it had a nice 40% correction. However, you are buying into the battle over gig workers—whether they should be treated as full-time or part-time workers. That is going to be a continuing drag on the stock until they win.

Q: What do you think of meme stocks?

A: You're better off buying a lottery ticket. Even with a low payoff, you get a 1:10 chance of winning on a $1 lottery ticket. Meme stocks could double or go to zero with no warning whatsoever—there’s no logic to this market at all.

Q: What do you think of Uranium?

A: Three words come to mind: Chernobyl, Fukushima, and Three Mile Island. I think uranium's time has passed, even though China is building a hundred nuclear power plants. It’s just too expensive to compete against solar on a large scale and impossible to insure. If you still like Uranium though, the Uranium Royalty Corp. (UROY) has had a nice pop recently. But the issue is that nuclear technologies can’t keep up with solar and digital. And they blow up.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/09/john-thomas-roller-coaster.png696424Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-09-10 10:02:392021-09-10 12:21:53September 8 Biweekly Strategy Webinar Q&A

Below please find subscribers’ Q&A for the August 25 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from The Atlantis Casino Hotel in Reno, NV.

Q: How does a 2X ProShares Ultra Technology ETF (ROM) February 2022 vertical bull call spread on the ROM look? Would you do $110-$115 or $115-$120?

A: I would do nothing here at $112.50 because we’ve just gone up 10 points in a week. I’d wait for some kind of pullback, even just $5 or $10 points, and then I would do the $110-$115. I’m leaning towards more conservative LEAPS these days—bets that the market goes sideways to up small rather than going ballistic, which it has done for the last 18 months. Think at-the-money strikes, not deep out-of-the-money on your LEAPS from here on for the rest of this economic cycle. The potential profits are still enormous. The only problem with (ROM) is that the longest maturities on the options are only six months.

Q: How do you recommend entering your long-term portfolio?

A: I would use the one-third rule: you put on ⅓ now, ⅓ higher or lower later on, and ⅓ higher or lower again. That way you get a good average price. Long term, everything goes up until we hit the next recession, which is probably several years off.

Q: I keep reading that the Delta variant is a market risk, but I don’t think that investors will look through this. Is Delta already priced into the shares?

A: Yes, what is not priced into the shares is the end of Delta, the end of the pandemic—and that will lead to my “everything” rally that I’ve been talking about for a month now. And we have already seen the beginning of that, especially with the price action this week. So yes, Delta in: dead market; Delta out: roaring market.

Q: Do you think there will eventually be a rotation into emerging markets (EEM), or has the virus battered these markets too much to even consider it?

A: Sometime in our future—not yet—the emerging markets will be our core holding. And the trigger for that will be the collapse of the dollar, which is hitting an interim high right now. When the greenback rolls over and dies, you can expect emerging markets, especially China, to take off like a rocket. That’s going to be our next big trade. I don't know if it will be this year or next year but it’s coming, so start doing your emerging market research now, and keep reading my newsletter.

Q: Is the coming tax hike a problem for the stock market?

A: No, I don’t think so. First off, I don’t think they’re going to do a tax bill this year; they don’t want anything to interfere with the 2022 election, so it may be next year’s business. Also, any new taxes are going to be overwhelmingly focused on billionaires, carried interest, offshoring, and large corporations. The middle class, people who make less than $400,000 a year, will not see any tax hike at all, possibly even getting some tax cuts via restored SALT deductions. So, I don't really see it affecting the stock market at all.

Q: What do you think about Chinese stocks (FXI)?

A: Long-term they’re okay, short term possibly more downside. Interestingly, the bigger risk may not be China itself and how the government is beating up its own tech companies, but the SEC. It has indicated they don’t really like these offshore vehicles that have been listed on the New York Stock Exchange, and they may move to ban them. I’m not rushing into China right now, only because there are just so many better opportunities in the US stock market for the time being. I may go back in the future—it’s a case where I’d rather buy them on the way up than trying to catch a falling knife on China right now.

Q: Do you expect any market impact from the Jackson Hole meeting?

A: Yes, whatever J Powell says, even if he says nothing, will have a market impact. And it will have a bigger impact on the bond market than it will on the stock market, which is down a full point this morning. So yes, but not yet. I imagine we’ll hear something very soon.

Q: September and October tend to be volatile; do you see us having a 5% or 10% pullback in those months?

A: I don’t see any more than 5%, with the hyper liquidity that we have in the system now. There just aren’t any events out there that could trigger a pullback of 10%—no geopolitical events, and the economy will be getting stronger, not worse. So yes, an “everything rally” doesn’t give you many long side entry points, so I just don’t see 10% happening.

Q: What about a Walt Disney (DIS) January 2022 $180-$220 LEAPS?

A: I would do the $180-$200. I think you can afford to be tighter on your spread there, take some more risk because I think it’s just going to go nuts to the upside once we get a drop in COVID cases. By the way, Disney parks are only operating at 70% capacity, so if you go back up to 100% that's a near 50% increase in profits for the company. And it’s not just Disney, but Netflix (NFLX), Amazon (AMZN), and everybody else that’s about to have the greatest number of blockbuster movies released of all time. They’re holding back their big-ticket movies for the end of the pandemic when people can go back into theaters. We’ll start seeing those movies come out in the last quarter of this year, and I’m particularly looking forward to the next James Bond movie, a man after my own heart.

Q: Are EV car charging companies like ChargePoint Holdings (CHPT) going to do as well as the car companies?

A: No. They’re low margin business, so it’s not a business model for me. I like high-profit margins, huge barriers to entry, and very wide moats, which pretty much characterizes everything I own. The big profits in EVs are going to be in the cars themselves. Charging the cars is a very capital-intensive, highly regulated, and low-margin business.

Q: Would a Fed taper cause a 10% pullback?

A: Absolutely not; in fact, I think a taper would make the market go up because Jay Powell has been talking it into the market all year. And that’s his goal, is to minimize the impact of a taper so when they finally do it, they say ho-hum and “okay you can take that risk out of the market.” That’s the way these things work.

Q: What is your yearend target for United States Treasury Bond Fund (TLT)?

A: $132. Call it bold, but I'm all about bold. I think the first stop will be at $144, then $138, then bombs away!

Q: What will it take for (TLT) to dip below $130?

A: Another year of hot economic growth, which Congress seems hell-bent on delivering us.

Q: What are your ProShares Ultra Short 20+ Year Treasury ETF (TBT) targets?

A: When we were at 1.76% on the 10-year bond, the (TBT) made it all the way back to 22 ½. Next year we go higher, probably to $25, maybe even $30.

Q: What’s your 10-year view on the (TBT)?

A: $200. That’s when you get interest rates back to 10% in 10 years on the 10-year bond. So yes, that’s a great long-term play.

Q: How long can we hold (TBT)?

A: As long as you want. Ten years would be a good time frame if you want to catch that $17 to $200 move. The (TBT) is an ETF, not an option, therefore it doesn’t expire.

Q: Are you working on an electrification stock list?

A: I am not, because it’s such a fragmented sector. It’s tough to really nail down specific stocks. I think it’s safe to say that the electric power grid is going to change beyond all recognition, but they won’t necessarily be in high margin companies, and I tend to prefer high-profit-margin, large-moat companies which nobody else can get into, like Apple (AAPL) or Google (GOOG).

Q: What about gas pipelines with high yields?

A: They have a high yield for a reason; because they’re very high risk. If you're going to a carbon-free economy, you don’t necessarily want to own pipelines whose main job is moving carbon; it’s another buggy whip-type industry I would avoid. I’ve seen people get wiped out by these things more times than I could count. If you remember Master Limited Partnerships, quite a few of them went bankrupt last year with the oil crash, so I would avoid that area. These tend to be very highly leveraged and poorly managed instruments.

Q: Best play on silver (SLV)?

A: Wheaton Precious Metals (WPM) is the highest leveraged silver play out there, and a great LEAPS candidate. Go out 2 years and triple your money.

Q: Geopolitical oil (USO) risks?

A: No, nobody cares about oil anymore—that’s why we’re giving up on Afghanistan. China is buying 80% of the Persian Gulf oil right now. We don’t really need it at all, so why have our military over there to protect China’s oil supply?

Q: What about Freeport McMoRan (FCX)?

A: I absolutely love it. Any big economic recovery can’t happen without copper, and you have a huge tailwind there from electric cars which need 200 pounds of copper each, as opposed to 20 pounds in conventional cars.

Q: I see AMC Entertainment Holdings (AMC) is up 20% today; should everyone be chasing this stock?

A: No, absolutely not. (AMC) and all the meme stocks aren’t investments, they’re gambling, and there are better ways to gamble.

Q: Should I buy the lumber dip?

A: Yes. I think the slowdown on housing is temporary because it will take 10 years for supply and demand in the housing market to come back into balance because of all the millennials entering the housing market for the first time. So, that would be a yes on lumber and all the other commodities out there that go into housing like copper, steel, and aluminum.

Q: Should I put money into Canadian Junior Gold Miners (GDX)?

A: No, I would rather go out and take a long nap first. These are just so high risk, and they often go bankrupt. The liquidity is terrible, and the dealing spreads are wide. I would stick with the bigger precious metal plays like Newmont Mining (NEM), Barrick Gold (GOLD), and Wheaton Precious Metals (WPM).

Q: Is Boeing (BA) a buy here?

A: Yes, we’re back at the bottom end of the trading range for the stock. It’s just a matter of time before they get things right, and the 737 Max orders are rolling in like crazy now that there’s an airplane shortage.

Q: What do you think about Robinhood (HOOD)?

A: I like it quite a lot; I got flushed out of my long position on Friday with a 10% down move. Of course, 90% of my stop losses end up expiring at their maximum profit points, but I have to do it to keep the volatility of the portfolio down. So yes, I’ll try to buy it again on the next dip. The trouble is it’s kind of a quasi-meme stock in its own right, hence the volatility; so I would say on the next 10% down day, you go into Robinhood, and I probably will too.

Q: How are the wildfires around Tahoe?

A: They’re terrible and there are three of them. I did a hike two days ago there, and out of a parking lot with 100 spaces, I was the only one there. It’s the only time I’d ever seen Tahoe deserted in August. With visibility of 500 yards, it's just terrible. Fortunately, I was able to hike without coughing my guts out—it’s not so thick that you can’t breathe.

Q: What do you think of US Steel (X)?

A: I like it, I think the whole industrial commodity complex rallies like crazy going into the end of the year.

Q: As a new member, where is the best place to start? It’s just kind of like drinking from a fire hose.

A: Wait for the trade alerts; they only happen at sweet spots and you may have to wait a few days or weeks to get one since we only like to enter them at good points. That’s the best place to enter new positions for the first time. In the meantime, keep reading all the research, because when these trade alerts do come out, they’re not surprises because I’m pumping out research on them every day, across multiple fronts. Be patient— we are running a 93% success rate, but only because we take our time on entering good trades. The services that guarantee a trade alert every day lose money hand over fist.

Q: If they do delist Chinese stocks, will US investors be left holding the bag?

A: Yes, and that will be the only reason they don’t delist them, that they don’t want to wipe out all current US investors.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER (whichever applies to you), then select WEBINARS and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2021/08/john-thomas-wine-1.png812562Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-08-27 10:02:412021-08-27 11:03:48August 25 Biweekly Strategy Webinar Q&A

Below please find subscribers’ Q&A for the April 28 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from Silicon Valley, CA.

Q: There is talk of digital currencies being launched in the US. Is there any truth to that? How would that affect the dollar?

A: There is no truth to that; there is not even any serious discussion of digital currency at the US Treasury. My theory has always been that once Bitcoin works and is made theft-proof, the government will take it over and make that the digital US dollar. So far, Bitcoin has existed regulation-free; in fact, the IRS is counting on a trillion dollars in capital gains being taxed going forward in helping to address the budget deficit.

Q: If you have a choice, what’s the best vaccine to get?

A: The best vaccine is the one you can get the fastest. I know you’re a little slow on the rollout in Canada. Go for Pfizer (PFE) if you’re able to choose. You should avoid Moderna (MRNA) because 15% of people getting second shots have one-day symptoms after the second shot. But basically, you don’t get to choose, only kids get to choose because only Pfizer has done trials on people under the age of 21. So, if you take your kids in, they will all get Pfizer for sure.

Q: Should I buy Freeport McMoRan (FCX) here or wait for a bigger dip?

A: Freeport has just had a 25% move up in a week. I wouldn’t touch that. We put out the trade alert when it was in the mid $30s, and it's essentially at its maximum profit point now. So, you don't need to chase—wait for a bigger dip or a long sideways move before you get in.

Q: How do I trade copper if I don't do futures?

A: Buy (FCX), the largest copper producer in the US, and they have call options and LEAPS. By the way, if we do get another $5 dip in Freeport, which we just had, I would really do something like the (FCX) $45-$50 2023 LEAP. You can get 5 times your money on that.

Q: Time to buy oil stocks (USO) for the summer?

A: No, the big driver of oil right now is the pandemic in India. They are one of the world's largest consumers—you find out that most poor countries are using oil right now as they can’t afford the more expensive alternative sources of power. And when your biggest customer is looking at a billion corona cases, that’s bad for business. Remember, when you trade oil, you’re trading against a long-term bear trend.

Q: Would you buy Delta Airlines (DAL) at today’s prices?

A: Yes, I’m probably going to go run the numbers on today's call spread; I actually have 20% of cash left that I could spend. So that looks like a good choice—summer will be incredible for the entire airline industry now that they have all staved off bankruptcy. Ticket prices are going to start rising sharply with an impending severe aircraft shortage.

Q: What are your thoughts on the Buffet index which shows that stocks are more stretched vs GDP at any time vs 2000?

A: The trouble with those indicators is that they never anticipated A) the Fed buying $120 billion a month in US Treasury bonds, B) the Fed promising to keep interest rates at zero for three years, and C) an enormous bounce back from a once-in-a-hundred-year pandemic. That's why not just the Buffet Index but virtually all technical indicators have been worthless this year because they have shown that the market has been overbought for the last six months. And if you paid attention to your indicators, you were either left behind or you went short and lost your shirt. So, at a certain point, you have to ignore your technical indicators and your charts and just buy the damn market. The people who use that philosophy (and know when to use it, and it’s not always) are up 56% on the year.

Q: What trade categories are getting fantastic returns? It’s certainly not tech.

A: Well, we actually rotated out of tech last September and went into banks, industrial plays, and domestic recovery plays. And you can see in the stocks I just showed you in our model portfolio which one we’re getting the numbers from. Certainly, it was not tech; tech has only performed for the last four weeks and we jumped right back in that one also with positions in Microsoft (MSFT). So yes, it’s a constantly changing game; we’re getting rotations almost daily right now between major groups of stocks. The only way to play this kind of market is to listen to someone who’s been practicing for 52 years.

Q: I am 83 years old and have four grandchildren. I want to invest around $20,000 with each child. I was thinking of your bullish view on Tesla (TSLA) on a long-term investment. Do you agree?

A: If those were my grandchildren, I would give them each $20,000 worth of the ProShares Ultra Technology Fund (ROM), the 2x long technology ETF. Unless tech drops 50% from here, that stock will keep increasing at twice the rate of the fastest-growing sector in the market. I did something similar with my kids about 20 years ago and as a result, their college and retirement funds for their kids have risen 20 times. So that’s what I would do; I would never bet everything on a single stock, I would go for a basket of high-tech stocks, or the Invesco QQQ NASDAQ Trust (QQQ) if you don’t want the leverage.

Q: Do you like Amazon (AMZN) splitting?

A: I don’t think they’ll ever split. Jeff Bezos worked on Wall Street (with me at Morgan Stanley) and sees splits as nothing more than a paper shuffle, which it is. It’s more likely that he’ll break up the company into different segments because when they get to a $5 trillion market cap, it will just become too big to manage. Also, by breaking Amazon up into five companies—AWS, the store, healthcare, distribution, etc., —you’re getting a premium for those individual pieces, which would double the value of your existing holdings. So, if you hold Amazon stock, you want it to face an antitrust breakup because the flotation will double the value of your total holdings. That has happened several times in the past with other companies, like AT&T (T), which I also worked on.

Q: When is Tesla going to move and why is it going up with earnings up 74%?

A: Well, the stock moved up a healthy 46% going into the earnings; it’s a classic sell the news market. Most stocks are doing that this quarter and they did so last quarter as well. And Tesla also tends to move sideways for years and then have these explosive moves up. I think the next double or triple will come when they announce mass production of their solid-state batteries, which will be anywhere from 2 to 5 years off.

Q: How can I renew my subscription?

A: You can call customer support at 347-480-1034 or email support@madhedgefundtrader.com and I guarantee you someone will get back to you.

Q: Top gene-editing stock after CRISPR Therapeutics (CRSP)?

A: There are two of them: one is Intellia (NTLA); it’s actually done better than CRISPR lately. The second is Editas (EDIT) and you’ll find out that the same professionals, including the Nobel prize winner Jennifer Doudna here at Berkeley, rotate among all three of these, and the people who run them all know each other. They were all involved in the late 2000's fundamental research on CRISPR, and they’re all frenemies. So yes, it's a three-company industry, kind of like the cybersecurity industry.

Q: What about PayPal (PYPL)?

A: I would wait for the earnings since so many companies are selling off on their announcements. See if they sell off 3-5%, then you buy it for the next leg up. That is the game now.

Q: Do you like any 3D printing stocks like Faro Technologies (FARO)?

A: No, that’s too much of a niche area for me, I’m staying away. And that's becoming a commodity industry. When they were brand new years ago, they were red hot, now not so much.

Q: Do you see the chip companies continuing their bull run for the next few months?

A: I do. If anything, the chip shortage will get worse. Each EV uses about 100 chips, and they’re mostly the low-end $10 chips. Ford (F) said production of a million cars will be lost due to the chip shortage. Ford itself has 22,000 cars sitting in a lot that are fully assembled awaiting the chips. Tesla alone has $300 worth of chips just in its inverters, and there are two inverters in every car. So, when you go from production of 500,000 cars to a million in one year, that's literally billions of chips.

Q: The airlines are packed; what are your thoughts?

A: Yes, one of the best ways to invest is to invest in what you see. If you see airlines are packed, buy airline stocks. If you can’t hire anyone, you know the economy is booming.

Q: What about the Russel 2000 (IWM)?

A: We covered it; it looks like it wants to break out to new highs from here. By the way, there are only 1,500 stocks left in the Russell 2000 after the pandemic, mergers, and bankruptcies.

Q: Are there other ways to play copper out there like (FCX)?

A: Yes; one is the (COPX)— a pure copper futures ETF. However, be careful with pure metal ETFs of any kind because they have huge contangos and you could get a 50% move up in your commodity while your ETF goes down 50% over the same time. This happens all the time in oil and natural gas, and to a lesser degree in the metals, so be careful about that. Before you get into any of these alternative ETFs, look at the tracking history going back and I think you'll see you're much better off just buying (FCX).

Q: How long do you typically hold onto your 2-year LEAPS? Based on my research, the time decay starts to accelerate after about 3 months to one year on LEAPS.

A: Actually, with LEAPS, the reason I go out to two years is that the second year is almost free, there's almost no extra cost. And it gives you more breathing room for this thing to work. Usually, if I get my timing right, my LEAP stocks make big moves within the first three months; by then, the LEAP has doubled in value, and then you have to think about whether you should keep it or whether there are better LEAPS out there (which there almost always are). So, you sell it on a double, which only took a 30% move in the stock, or you may be committed to the company for the long term, like a Microsoft or an Amazon. And then you just run it through the expiration to get a 400% or 500% profit in two years. That is how you play the LEAP game.

Q: Are these recorded?

A: Yes, we record these and we post them on the website after about 2 hours. Just log into the site, go to “my account”, then select your subscription type (Global Trading Dispatch or Technology Letter), and “webinars” will be one of the button choices.

Q: Can you also sell calls on LEAPS?

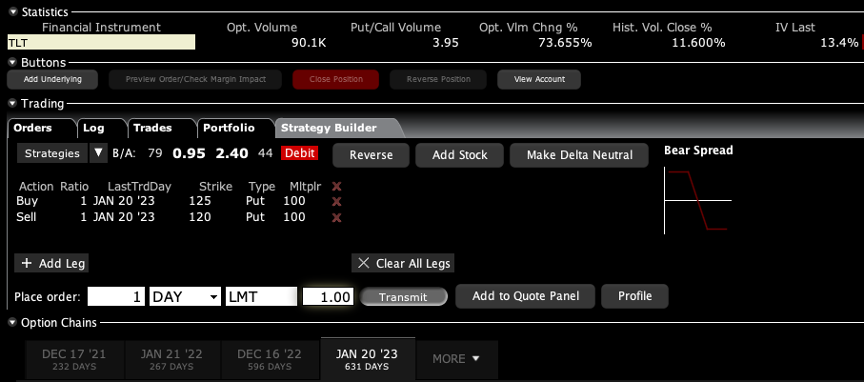

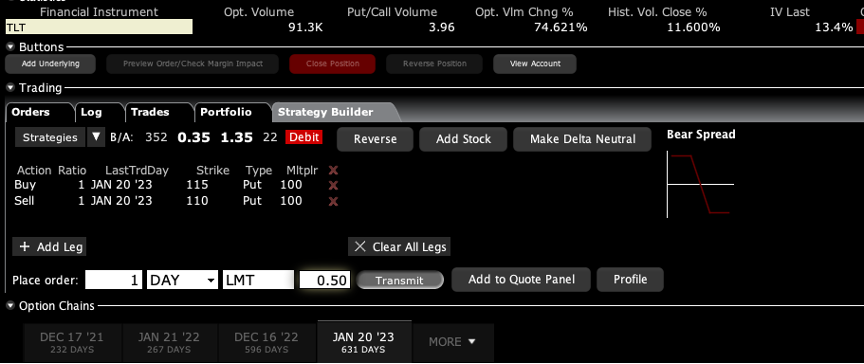

A: Yes and the only place to do that is the US Treasury market (TLT). There you either want to be short calls far above the market, out two years, or you want to be long puts. And by the way, if you did something like a $120-$125 put spread out to January 2023, then you’re looking at making about a 400% gain. That is a bet that 20-year interest rates only go up a little bit more, to 2.00%. If you really want to bet the ranch, do something like a $120-$122 and you might get a 1000% return.

Q: What is the best LEAP to trade for Microsoft (MSFT)?

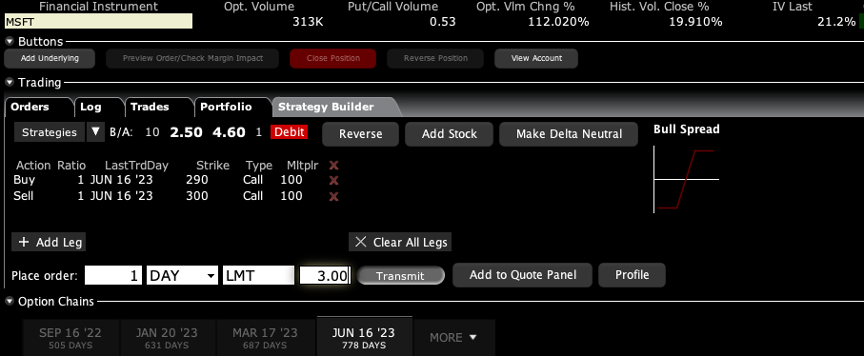

A: If you want to go out two years, I would do something like a June 2023 $290-$300 vertical bull call spread. There is an easy 67% profit in that one on only a 20% rise in the stock. I do front monthlies for the trade alert service, so we always have at least 10 or 20 trade alerts going out every month. And the one I currently have for is a deep in the money May $230-$240 vertical bull call spread which expires in 12 days.

Q: What is the best way to play Google (GOOG)?

A: Go 20% out of the money and buy a January 2023 $2,900-$3,000 vertical bull call spread for $20—that should make about 400%. If you want more specific advice on LEAPS, we have an opening for the Mad Hedge Concierge Service so send an email to support@madhedgefundtrader.com with subject line “concierge,” and we will reach out to you.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

I Think I See Another Winner

https://www.madhedgefundtrader.com/wp-content/uploads/2019/11/john-rifle.png700525Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-04-30 09:02:212021-04-30 12:12:05April 28 Biweekly Strategy Webinar Q&A

Below please find subscribers’ Q&A for the March 17 Mad Hedge Fund TraderGlobal Strategy Webinar broadcast from frozen Incline Village, NV.

Q: I’ve heard that the COVID-19 cases are being understated by 16 million. Do you think this is true?

A: Yeah, I've always argued that the previous government's numbers were vastly underestimating the true number of cases out there for political purposes, but we are on the downslide regardless, so that’s good.

Q: When are tech stocks going to bottom out and when can I buy them?

A: I knew I would get this question. This is the question of the day. Picking bottoms is always tough because these are momentum plays and not valuation plays. I’ll give you a couple of levels though. The tech (QQQ) multiple is now at 25X earnings and the S&P 500 (SPY) is at 22X, so your first bottom will be down about 10% from here, or a 22X multiple. And I don’t think we will get much lower than that because tech stocks are growing at 20-25% a year, versus the (SPY) growing at maybe 10%, and I don’t think tech goes to much of a discount in that situation. So, you’re just waiting for interest rates to top out and start to go down, which will be the other indicator of a tech bottom. We had a slowdown in the rise of rates for just a couple of days this week, and tech stocks took off like a rocket. Those are your two big signals.

Q: With the Fed announcement, are you still in the Invesco QQQ Trust NASDAQ ETF (QQQ) bear put spread?

A: Yes, one of them expires in two days so that’s a piece of cake. The other one expires in a month, but it is way out-of-the-money—the April $240-$245 bear put spread, so I’ll keep that for a real meltdown day. But if it looks like we’re getting a breakout, I will come out of that short position so fast it will make your head spin.

Q: Do you like Palantir (PLTR)?

A: Absolutely yes—screaming LEAP candidate. It traded all the way down to $20 two weeks ago and is trading around $25 now. It’s a huge data firm, lots of CIA and defense work, huge government contracts extending out for years, cutting edge technology, and run by a nut job, so yes screaming buy at this level.

Q: Freeport McMoRan (FCX) is taking some pain here, is this still a buy and hold?

A: Yes, it’s taking the pain along with all the other domestic stocks, which is natural. In their case though, it’s up almost 10x from its bottom a year ago where we recommended it, so yeah I'd say time for a rest. So I’m still a buyer of the metals and (FCX) on dips, but like all other metals, it did get overextended. EV manufacturing is doubling this year, which uses a ton of copper. The same is true with solar panels and Chinese industrial recovery. When all your major markets are doubling in size, it’s usually good for the stock. I peaked at $50 in the last cycle and could touch $100 in this one.

Q: What are your thoughts about the Lucid EV SPAC, Churchill Capital IV (CCIV)?

A: Don’t touch it with a ten-foot pole. They only have 1 or 2 concept vehicles for high-end investors to test drive. The rumor is that their main factory will be in Saudi Arabia where the bulk of the seed capital came from. They’ll never catch up with Tesla (TSLA) on the technology. There's always going to be a few niche $250,000 cars out there, and they have no proof they can actually make these things. When they get to a million vehicles a year, then I might be interested. But they haven't done the hard part yet, which is mass-producing battery packs for a million cars. They've only done the easy part which is designing one sexy prototype to raise money. So, stay away from Lucid, I don’t think they’re going to make it.

Q: What about oil?

A: I am avoiding oil plays like the plague.

Q: When do you anticipate your luncheons to be back?

A: Maybe in 2023. I don’t want to scare off my customers by inviting them to a lunch where they all get COVID-19. If I did have a lunch, I’d have a vaccine requirement and a temperature gun to hit them at the door like everywhere else. I really miss meeting subscribers in person.

Q: Should I buy banks like JP Morgan (JPM) at this level?

A: I would say no. That ship has sailed. Wait for a steeper selloff or just let it run. We’ve already had an enormous move and you don’t want to chase it with a low discipline trade, which is what that would be.

Q: What do you think of silver (SLV)?

A: It’s a buy long term, short term it’s in the grim spiral of death along with the other precious metals, which absolutely hate rising interest rates. A silver long here is the equivalent of a bond (TLT) long. When you do go into silver, buy Wheaton Precious Metals (WPM) for the leveraged long play.

Q: Is 3M (MMM) going to extend the upside?

A: Probably yes, that's a classic American industrial play and a great company. I have friends who work there. How could we live without Post-it notes, Scotch Tape, and Covid-19 N-95 masks?

Q: What about Square (SQ)?

A: I love it in the long term, buy on the dips and buy it through LEAPS (long term equity anticipation securities).

Q: Should I unwind my leveraged financial ETF?

A: I’d say take a piece off, yeah; you never get fired for taking a profit. And they have had a tremendous move. Plus of course, the flip side of taking profits on domestic recovery stocks is to buy tech with that money. And eventually, that's what the entire market will do, it just may still be a little bit early.

Q: What’s a good target for LEAPS for CRISPR (CRSP) and Palantir (PLTR)?

A: Put your first strike 30% higher than today’s stock price and go 2 years out in maturity. I noticed on some names, the June 2023’s are starting to trade, but they’re highly illiquid. But if you put a bid in there and you get a market meltdown, you will get hit.

Q: If the long-term future for oil (USO) is so bad, why is it $65?

A: A few reasons. #1, huge short covering action. #2, economy recovery faster than people expected because of the stimulus. #3, a lot of people, mostly in Texas, Oklahoma, and Louisiana, don’t believe that there will be an all-electric grid in 20 years and think that oil will be in demand forever, including the entire oil industry, so they’re in there buying. And #4, the Saudis have held back with production increases to push the price up, so they’re letting it run so they can sell at a higher price. When they do sell, oil crashes again.

Q: Can we re-watch this presentation?

A: Yes, we post it about 2 hours later on the website so all our people in about 135 countries can access it whenever they like. Just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Q: How often do you have these webinars?

A: Every two weeks, and if you need help accessing it on your account page, email customer support at support@madhedgefundtrader.com.

Q: Is it time to initiate short positions on oil companies?

A: Not yet but keep it in the back of your mind. When some of the super-hot economic data come out after Q2, that may be your short in oil—then we may get into the $70’s a barrel. But not yet, there’s still too much upward momentum.

Q: Do you think we will see the 30-year fix below a 3.00% yield again?

A: Yes, in the next recession, which may be 5 or 10 years off because we’re starting at such a low base.

Q: Regarding copper, EV motors require a ton of copper. Doesn’t that make the metals a BUY?

A: That is true, and why we recommended Freeport McMoRan at $4 a year ago and recommended buying every dip. Each one of these rotor motors on each wheel of a Tesla weighs about 100 lbs—I’ve lifted them. Remember I tore apart a Tesla once just to see what made it tick, and they’re really heavy, and they use a lot of copper, and silver as well. So that has always been the bull market case for copper, as well as the fact that China re-emerged as a major buyer for their industrial buildout. That’s why we had a long in the SPDR S&P Metals and Mining ETF (XME).

Q: Do you foresee a good opportunity to go heavy into margin again?

A: Maybe if we get a decent selloff this summer, but you’ll never get the opportunity we had a year ago when you really wanted to put 100% of your portfolio into 2-year LEAPS. The people who did that made many tens of millions of dollars, which is why I get a free bottle of Bourbon every month. That was a once in 20 years event.

Q: What is your 2021 target for the S&P 500 (SPX)?

A: $4,860. It’s in my strategy letter which I sent out on January 6th, and that is all still posted on the website, click here for it.

Q: How do I renew my subscription with your company, and how do I figure out what I bought?

Q: Do you follow the iShares IBoxx High Yield Corporate Bond ETF (HYG)?

A: Yes, that is the high yield junk bond fund, but I have been avoiding long bond plays, as you may have noticed with my screaming short of the past year. We list (HYG) in these slides in the Bonds section.

To watch a replay of this webinar, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH or TECHNOLOGY LETTER (as the case may be), then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2016/08/John-in-Cap-e1473378948252.jpg400301Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-03-19 10:02:222021-03-19 11:34:22March 17 Biweekly Strategy Webinar Q&A

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-02-19 10:04:152021-02-19 10:28:18February 19, 2021

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.