(LAST CHANCE TO BUY THE NEW MAD HEDGE BIOTECH AND HEALTH CARE LETTER AT THE FOUNDERS PRICE)

(SEPTEMBER 18 BIWEEKLY STRATEGY WEBINAR Q&A),

(SPY), (VIX), (USO), (ROKU), (TLT), (BA), (INDU),

(GM), (FXI), (FB), (SCHW), (IWM), (AMTD)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-10-04 07:06:252019-10-04 07:00:03October 4, 2019

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader October 2Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Would you do the S&P 500 (SPY) bull call spread if you didn’t have time to enter the short leg yesterday?

A: I would, because once again, once the Volatility Index (VIX) gets over $20, picking these call spreads is like shooting fish in a barrel. I think the long position I put on the (SPY) this morning is so far in the money that you will be sufficiently safe on a 12-day and really a 2-week view. There is just too much cash on the sidelines and interest rates are too low to see a major December 2018 type crash from here.

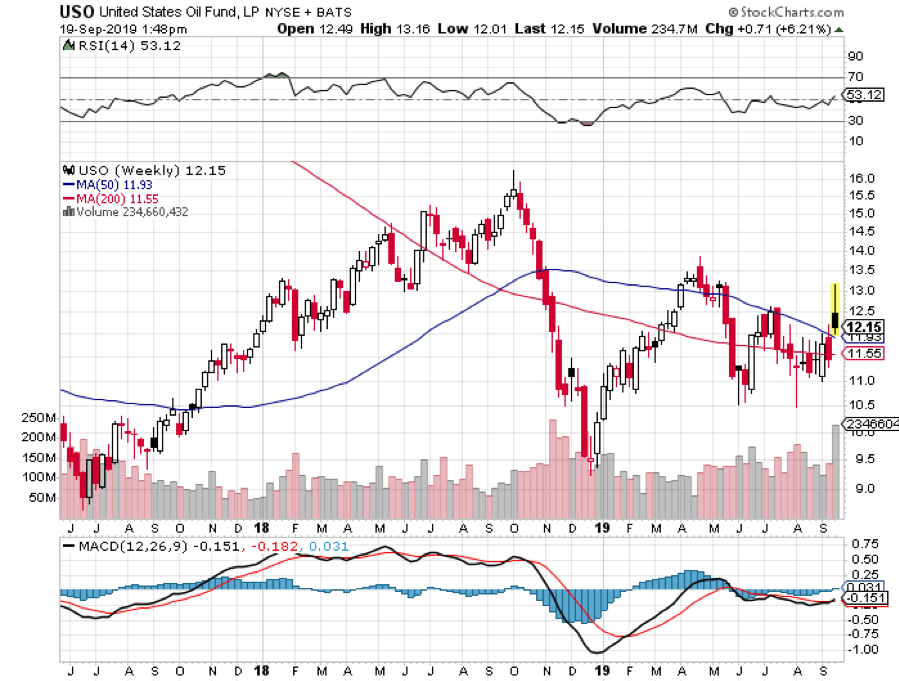

Q: I could not come out of the United States Oil Fund (USO) short position—should I keep it to expiration?

A: Yes, at this point we’re so close to expiration and so far in the money that you’d need a 30% move in oil to lose money on this. So, run it into expiration and avoid the execution costs.

Q: How do you see TD Ameritrade (AMTD) short term?

A: Well, it was down approximately 25% yesterday, so I would buy some cheap calls and go way out of the money so as not to risk much capital—on the assumption that maybe next week into the China trade talks, we get some kind of rally in the market and see a dramatic rise. 25% does seem extreme for a one-day move just because one broker was cutting his commissions to zero. By the way, I have been predicting that rates would go to zero for something like 30 years; that’s one of the reasons I got out of the business in 1989.

Q: Would you consider buying Roku (ROKU) at the present level?

A: Down 1/3 from the top is very tempting; however, I’m not in a rush to buy anything here that doesn’t have a large hedge on it. What you might consider doing on Roku is something like a $60-$70 or $70-$80 long-dated call spread. That is hedged, and it’s also lower risk. Sure, it won’t make as much money as an outright call option but at least you won’t be catching a falling knife.

Q: Will we see a yearend rally in the stocks?

A: Probably, yes. I think this quarter will clear out all the nervous money for the short term, and once we find a true bottom, we might find a 5-10% rally by yearend—and I’m going to try to be positioned to catch just that.

Q: At which price level do you go 100% long position?

A: If we somehow get to last December lows, that’s where you add the 100% long position. And there is a chance, while unlikely, that we get down to about 22,000 in the Dow Average (INDU), and that’s where you bet the ranch. Coming down from 29,000 to 22,000, you’re essentially discounting an entire recession with that kind of pullback. But we’re going to try to trade this thing shorter term; the market has so far been rewarding us to do so.

Q: The United States Treasury Bond Fund (TLT) looks like it’s about to break out. How do you see buying for the November $145 calls targeting $148?

A: We are actually somewhat in the middle of the range for the (TLT), so it’s a bit late to chase. We did play from the long side from the high $130s and took a quick profit on that, but now is a little bit late to play on the long side. We go for the low-risk, high-return trades, and $145 is a bit of a high-risk trade at this point. I would look to sell the next spike in the (TLT) rather than buy the middle where we are now.

Q: Will Boeing (BA) get recertified this year?

A: Probably, yes—now that we have an actual pilot as the head of the FAA—and that will be a great play. But if the entire economy is falling into a recession, nothing is a good play and you want to go into cash if you can’t do shorts. That would give us a chance to buy Boeing back closer to the $320 level, which was the great entry point in August.

Q: Do you expect General Motors (GM) shares to bounce if they settle with the union on their strike?

A: Maybe for a day or two, but that’s it. The whole car industry is in recession already. The union picked the worst time to strike because GM has a very high 45-day inventory of unsold cars which they would love to get rid of.

Q: What are the chances of a deal with China (FXI)?

A: Zero. How hard do the Chinese really want to work to get Trump reelected? My guess is not at all. We may get the announcement of a fake deal that resumes Chinese agricultural purchases, but no actual substance on intellectual property theft or changing any Chinese laws.

Q: Will they impeach Trump?

A: Impeach yes, convict no; and it’s going to take about 6 months, which will be a cloud hanging over the market. The market’s dropped about 1,000 points since the impeachment inquiry has started.

Q: What about the dollar?

A: I'm staying out of the dollar due to too many conflicting indicators and too much contra-historical action going on. The dollar seems high to me, but I’ve been wrong all year.

Q: E*Trade (ETFC) just announced free stock trading—what are your thoughts?

A: All online brokers now pretty much have to announce free trading in order to stay in business, otherwise you end up with the dumbest customers. It’s bad for the industry, but it’s good for you. The fact that all of these companies are moving to zero shows how meaningless your commissions became to them because so much more money was being made on selling your order flow to high frequency traders or selling your data to people like Facebook (FB).

Q: What’s your take on the Canadian dollar (FXC)?

A: It will go nowhere to weak, as long as the US is on a very slow interest rate-cutting program. The second Canada starts raising rates or we start cutting more aggressively is when you want to buy the Loonie.

Q: Fast fashion retailer Forever 21 went bankrupt—is it too late to short the mall stocks?

A: No but be very disciplined; only short the rallies. Last week would have been a good chance to get shorts off in malls and retailers. You really need to sell into rallies because the further these things go down, the more volatility increases as the prices go low. Obviously, a $1 move on a $30 stock is only 3% but a $1 move on a $10 stock is 10%. If you’re the wrong way on that, it can cost you a lot of money, even though the thing’s going to zero.

Q: Comments on defense stocks such as Raytheon (RTN)?

A: This is a highly political sector. If Trump gets reelected, expect an expansion of defense spending and overseas sales to Saudi Arabia, which would be good for defense. If he doesn’t get reelected, that would be bad for defense because it would get cut, and sales to places like Saudi Arabia would get cut off. I stay out of them myself because it’s essentially a political play and we’re very late in the cycle.

Q: Mark Zuckerberg says presidential candidate Elizabeth Warren’s proposal is an existential threat. Do you agree with him and her policies? Will they crash the economy?

A: They would be bad for the economy; however, I think it’s highly unlikely Warren gets elected. The country’s looking for a moderate president, not a radical one, and she does not fit that description. If you did break up the Tech companies, they’d be worth more individually than they are in these great monolithic companies.

Q: Does the Russell 2000 (IWM) call spread look in danger to you?

A: It’s a higher risk trade, however we are hedged with that short S&P 500, so we can hang onto the long (IWM) position hedging it with your short S&P 500 (SPY) trade reducing your risk.

Q: What do you have to say about shrinking buybacks?

A: It’s another recession indicator, for one thing. Corporate buybacks have been driving the stock market for the last 2 years at around a trillion dollars a year. They have suddenly started to decline. Why is that happening? Because companies think they can buy their stocks back at lower levels. If companies don't want to buy their stocks, you shouldn’t either.

Q: When is the time for Long Term Equity Anticipation Securities (LEAPS)?

A: We are not in LEAPS territory yet. Those are long term, more than one-year option plays. You really want to get those at the once-a-year horrendous selloffs like the ones in December and February. We’re not at that point yet, but when we get there, we’ll start pumping out trade alerts for LEAPS for tech stocks like crazy. Start doing your research and picking your names, start playing around with strikes, and then one day, the prices will be so out of whack it will be the perfect opportunity to go in and buy your LEAPS.

Q: Was it a Black Monday for brokerages when Charles Schwab (SCHW) cut their commission to zero?

A: Yes, but it’s been one of the most predicted Black Mondays in history.

Q: Will the Fed save the market?

A: I would think they have no ability to save the market because they really can’t cut interest rates any more than they already have. There really are no companies that need to borrow money right now, and any that does you don’t want to touch with a ten-foot pole. The economy is not starved for cash right now—we have a cash glut all over the world—therefore, lowering interest rates will have zero impact on the economy, but it does eliminate the most important tool in dealing with future recessions. You go into a recession with interest rates at zero, then you’re really looking at a great depression because there’s no way to get out of it. It’s the situation Europe and Japan have been in for years.

Good Luck and Good Trading

John Thomas

CEO $ Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2018/04/John-Thomas-story-2-e1522965508602.jpg321300Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-10-04 07:02:242019-10-04 07:05:16October 2 Biweekly Strategy Webinar Q&A

“May you live in interesting times.” The question is whether this old Chinese proverb is a blessing or a curse.

Our beleaguered lives have certainly been getting more interesting by the day, if not the hour. Trump has been withholding military aid from foreign leaders to fish for dirt on those who may run against him in 2020. The prospects of the Chinese trade negotiations seem to flip flop by the day.

Prospective IPOs for Saudi ARAMCO and WeWork have been stood up against a wall and shot. The Altria (MO) - Philip Morris (PM) merger went up in smoke. Brexit (FXB) has turned into a runaway roller coaster that has lost its brakes. And that was just last week!

All of this is happening with the major indices (SPY), ($INDU) mere inches away from all-time highs, with valuations at the high end of the decade-old band. A worse risk/reward for initiating new positions I can’t imagine. I think I’ll go take a long nap instead.

There are times to trade and there are times to engage in research and this is definitely time for the latter. That means when it is time to strike, you already have a list of short names on which to execute. The worst time to initiate research is when the Dow is down 1,000 points.

I believe the markets are gridlocked until we get a good look at Q3 corporate earnings. If they are as bad as the macro data is suggesting, markets will tank. If they aren’t, we may see a begrudging slow-motion grind up to new highs.

Our launch of the Mad Hedge Biotech and Healthcare Letter was a huge success. Let me tell you, we have some real blockbusters lined up in our newsletter queue. The Tuesday letter will have a link that will enable you to get in at the $997 a year founders’ price. Otherwise, you can find it in our store now for $1,500 a year. Please click here.

The WeWork IPO is on the Rocks, with the CEO soon to be fired for self-dealing. In any case, the company has minimal added value and will not survive the next recession when the bulk of its tenants walk. Don’t touch this one on pain of death, even down three quarters from its original valuation.

Watch out for October, says Goldman Sachs (GS), which will see a volatility (VIX) spike 25%. Shockingly poor Q3 corporate earnings results could be the trigger with almost every company negatively impacted by the trade war. This could set up our next entry point on the long side.

The Saudi ARAMCO IPO is on the skids in the wake of the mass drone attack. Terrorist attacks on your key infrastructure is not a great selling point for new shareholders. It just underlines the high-risk investing in the area. The world’s largest IPO may get cancelled.

A huge killing was made on the Thomas Cook affair. It looks like short sellers raked in $2.7 billion in profits on the collapse. Some 600,000 mostly British travelers were stranded or had future vacations cancelled.

Thomas Cook never figured out the Internet, were destroyed by the collapse of the pound triggered by Brexit and, horror upon horrors, bought an airline. It’s all great news for surviving European tour operators and discount airlines. Airfares are already rising.

The S&P Case Shiller ticked up in July, showing that the National Home Price Index rising 3.2%. It’s the first positive move in more than a year. It’s got to be super-low interest rates finally kicking in. But the real move up won’t start until SALT deductions come back in 18 months.

That went over like a lead balloon. From the moment Trump started speaking at the United Nations, stocks went into free fall, dropping 450 points from top to bottom. It’s trade war against everyone all the time with his withdrawal from globalization. Oh, and if you want to resist America’s incredible military might, we will crush you. It’s not what traders wanted to hear.

In the meantime, the impeachment moved forward, with younger Democrats forcing Pelosi’s hand. The Ukraine scandal, a Trump effort to have candidate Joe Biden arrested, was the stick that broke the camel’s back. Fortunately, the stock market could care less. Stocks rose 20% during the last impeachment in the 1990s.

US Consumer Confidence dove in September from 133 estimated down to 125.1 as trade war concerns take their toll. It’s one of the first September data points to come out and presages worse to come. News fatigue has to be a factor.

BitcoinCrashed 15% to a new three-month low, hitting $7,944. Other cryptos fell 20%. All of the explanations were technical as they always are with this bogus asset class.

The Vaping Crisis demoed the Altria-Philip Morris merger. Suddenly, the crown jewels are toxic and about to be made illegal. The Juul CEO has resigned and the company may be about to go down the tubes. One of the largest mergers in history that would have created a $200 billion company has been tossed on the dustbin of history.

In a rare positive data point, New Homes Sales soared 7.1% in August to a 713,000 annualized rate. Median sales prices rise by 2.2% YOY to $328,400. Inventories drop from 5.9 to 5.5 months. The big numbers are happening in the south and west. Historically low-interest rates are kicking in big time.

The FTC Slammed Match Group (MTCH), the owner of Tinder and OK Cupid, for security lapses and scamming their own customers. Apparently, that gorgeous six-foot blond who speaks six languages who want to meet me if I only subscribed doesn’t actually exist. Oh well.

Q2 GDP final read came in at 2.0% with no change from the last report. Coming quarters will almost certainly be worse as the chickens come home to roost from a global trade war. We may already be in a recession and not know it. Inventories are building at a tremendous rate. Certainly, Fortune 500 CEOs think so.

Tesla deliveries may hit new high in Q3, topping 100,000, according to last week’s leak. The stock is back in play. It looks like I am going to get a new entertainment package upgrade too.

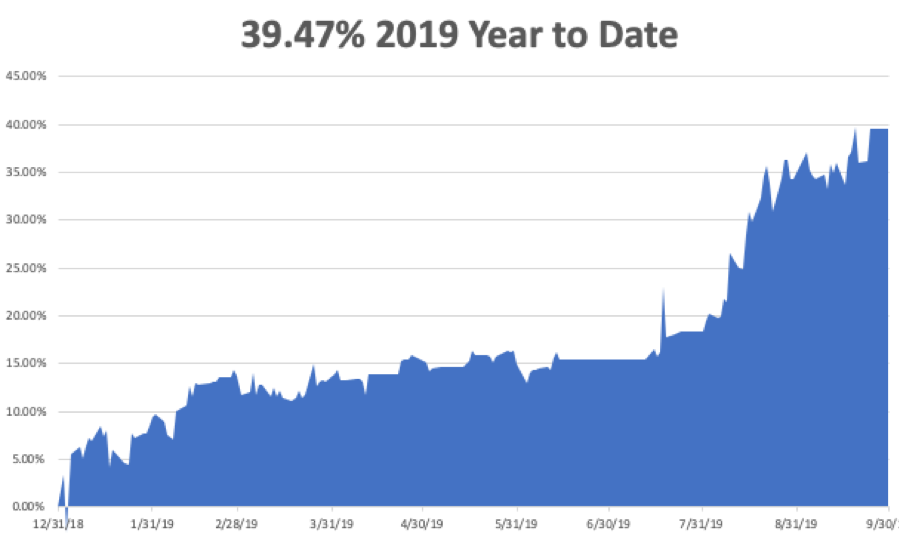

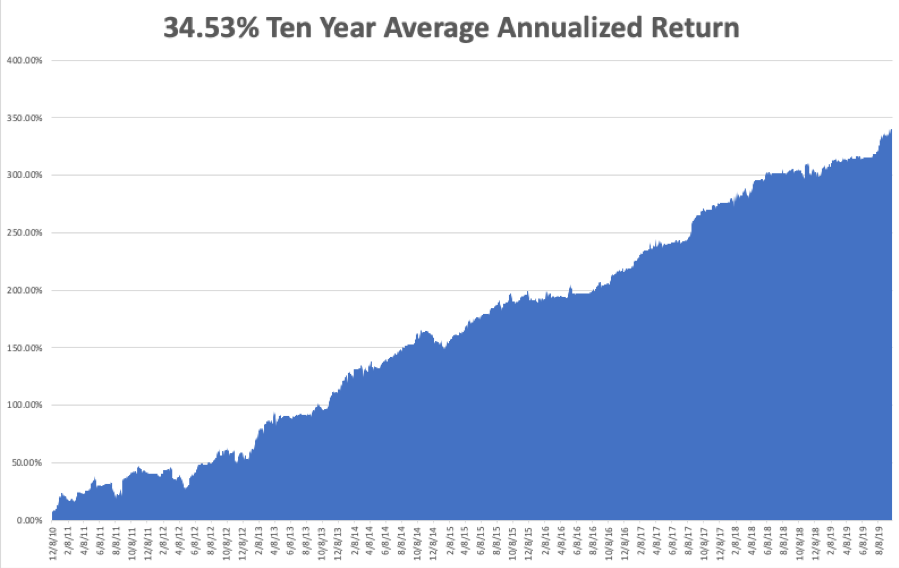

The Mad Hedge Trader Alert Service has blasted through to yet another new all-time high. My Global Trading Dispatch reached new apex of 336.07% and my year-to-date accelerated to +39.47%. The tricky and volatile month of September closed out +3.08%. at My ten-year average annualized profit bobbed up to +34.53%.

Some 25 out of the last 27 trade alerts have made money, a success rate of 92.59%. Under-promise and over-deliver, that's the business I have been in all my life. It works.

I took profits in my short position in oil (USO) earlier in the week, capturing a 12% decline there. That gives me a rare 100% cash position. I’m itching to get back in, but conditions right now are terrible

The coming week is all about the September jobs reports. It seems like we just went through those.

On Monday, September 30 at 9:45 AM, the Chicago Purchasing Managers Index for September is out.

On Tuesday, October 1 at 10:00 AM, the US Construction Spending for August is published

On Wednesday, October 2, at 8:15 AM, we learn the ADP Private Employment Report is out for September.

On Thursday, October 3 at 8:30 AM, the Weekly Jobless Claims are printed. At 3:00 PM, we get US Vehicle Sales for September.

On Friday, October 4 at 8:30 AM, the September Nonfarm Payroll Report is announced. Last month was a big disappointment so this month could set a new trend.

The Baker Hughes Rig Count is released at 2:00 PM.

As for me, I’ll be camping out with 2,500 Boy Scouts at the Solano Fair Grounds to attend Advance Camp. That’s where scouts have the opportunity to earn any of 50 merit badges in a single day.

I will be teaching the Swimming Merit Badge class. The basic idea is that if you throw a scout in the pool and he doesn’t drown, he passes. Personally, I wanted to take the welding class. The bonus is that we get to ride nearby roller coasters at Six Flags for free.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2019/09/john-thomas-4.png441827Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-09-30 05:02:472019-12-09 12:33:17The Market Outlook for the Week Ahead, or Interesting Times are Upon Us

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader September 18Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: What would happen to the United States Treasury Bond Fund (TLT) if the Fed does not lower rates?

A: My bet is that it would immediately have a selloff—probably several points—but after that, recession worries will take bond prices up again and yields down. I don’t think we have seen the final lows in interest rates by a long shot. That’s why I bought the (TLT) last week.

Q: Is it good to buy FedEx (FDX) considering the 13% fall today?

A: I use the 3-day rule on these situations. That's how long it takes for the dust to settle from an earnings shock like this and find the real price. The problem with FedEx is that it’s a great early recession predictor. When the number of delivered packages decreases, it’s always an indicator that the economy as a whole is slowing down, which we know has been happening. It’s one of the most cyclical stocks out there, therefore one of the most dangerous. I wouldn’t bother with FedEx right now. Go take a long nap instead.

Q: Would you be a buyer of Facebook (FB) here, given they seem to have weathered all the recent attacks from Washington?

A: Not here in particular, but I would buy it 20% down when it gets to the bottom edge of its upward channel—it still looks like it’s going crazy. They’re literally renting or buying buildings to hire an additional 50,000 people in San Francisco anticipating huge growth of their business, so that’s a better indicator of the future of Facebook than anything.

Q: Will junk bonds be more in demand now that rates are cratering?

A: Junk bonds (HYG), (JNK) are driven more by the stock market than the bond market, as you can see in the huge rally we just had. Junk bonds are great because their default ratios are usually far below that which the interest rate implies, but you really have to trade them like stocks. Think of them as preferred stocks with really high dividends. When the stock market tops, so will junk bonds. Remember in 2008, junk yields got all the way up to 15% compared to today’s 5.6%.

Q: What will happen to emerging markets (EEM) as rates lower?

A: If lower interest rates bring a weaker US dollar, that would be very positive for emerging markets over the long term and they would be a great buy. However, emerging markets will take the hardest hit if we actually do go into a recession. So, I would pass for now.

Q: What are your thoughts on Alibaba (BABA) and JD.com (JD)?

A: They are great for the long term. However, expect a lot of volatility in the short term. As long as the trade war is going on, these are going to be hard to trade until we get a settlement. (JD) is already up 50% this year but is still down 40% from pre trade war levels. These things will all be up 20-30% when that happens. If you can take the heat until then, they would probably be okay for a long-term portfolio globally diversified.

Q: What do you have to say about the ProShares Ultra Short 20+ Year Treasury ETF (TBT)—the short bond ETF?

A: If you have a position, I’d be selling now. We just had a massive 20%, 4-point rally from $22 to $27 and now would be a good time to take a profit, or at least get out closer to your cost. The zero interest rates story is not over yet.

Q: Would you short the US dollar?

A: I would most likely short it against the euro (FXE), which now has a massive economic stimulus and quantitative easing program coming into play which should be positive for it and negative for the US dollar (UUP). That’s most likely why the euro has stabilized over the last couple of weeks. That said, the dollar has been unexpected high all year despite falling interest rates so I have been avoiding the entire foreign exchange space. I try to stay away from things I don’t understand.

Q: If all our big tech September vertical bull call spreads are in the money, what should we do?

A: You do nothing. They all expire at the Friday close in two trading days. Your broker should automatically use your long call position to cover your short call position and credit your account with the total profit on the following Monday, as well as release the margin for holding that position. After that, we’ll probably wait for another good entry point on all the same names, (AMZN), (FB), (DIS), (MSFT).

Q: If the US fires a cruise missile at Iran, how would the market react?

A: It would selloff pretty big—markets hate wars. And the US wouldn’t send one missile at Iran; it would be more like 100, probably aimed at what little nuclear facilities they have. I doubt that is going to happen. The world has figured out that Trump is a wimp. He talks big but there is never any action or follow through. Inviting the Taliban to Camp David while they were still blowing up our people? Really?

Q: Will the housing market turn on the turbochargers after this dip in rates?

A: It wouldn't turn on the turbochargers, but it might stabilize the market because money is available now at unprecedentedly low interest rates. However, we still have the loss of the SALT deductions—the state and local taxes and real estate taxes that came in with the Trump tax bill. Since then, real estate has been either unchanged or has fallen on both the East and West coast where the highest priced houses are. It’s the most expensive houses that take the loss of the SALT deduction the hardest. Don’t expect any movement in these markets until the SALT deduction comes back, probably in 16 months.

Q: What catalyst do you think would cause a 10% correction in the next 2-3 months?

A: Trump basically saying “screw you” to the Chinese—a tweet saying he’s going to bring another round of tariff increases. That’s worth a minimum of 2,000 points in the Dow Average (INDU), or about 7% percent. Either that or no move in Fed interest rates—that would also create a big selloff. My guess is that and adverse development in the trade war will be what does it. That’s why my positions are so small now.

Q: We have a big short position in the United States Oil Fund (USO) now. Are you going to run this into expiration until October $18?

A: Even though oil has already collapsed by 10% since we put this position on last Friday, premiums in oil options are still close to record levels. So, it pays us to hang on for the time decay. The world is still massively oversupplied in oil and the Saudis were able to bring half of the lost production back on in a day. Oil will keep falling unless there is another attack and it is unlikely we will see one again on this scale. And, we only have 20 more days to go to capture the full 14.8% profit.

Good luck and good trading.

John Thomas

CEO & Publisher

Diary of a Mad Hedge Fund Trader

You Can’t Do Enough Research

https://www.madhedgefundtrader.com/wp-content/uploads/2019/09/john-and-girls.png322345Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-09-20 01:04:442019-12-09 12:38:46September 18 Biweekly Strategy Webinar Q&A

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader September 4Global Strategy Webinar broadcast from Silicon Valley with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: If Trump figures out the trade war will lose him the election; will he stop it?

A: Yes, and that is a risk that hovers over all short positions in the market at all times these days because stocks will soar (INDU) when the trade war ends. We now have 18 months of share appreciation that has been frustrated or deferred by the dispute with China. The problem is that the US economy is already sliding into recession and it may already be too late to turn it around.

Q: Do you see the British pound (FXB) dropping more on the Brexit turmoil? Do you think the UK will stay in the EU?

A: If the UK ends Brexit through an election, then the pound should recover from $1.19 all the way back up to $1.65 where it was before Brexit happened four years ago. If that does happen, it will be one of the biggest trades of the year anywhere in the world, going long the British pound. This is how I always anticipated it would end. I was in England for the Brexit vote and I was convinced that if they held the election the next day, it would have lost. The only reason it won was because nobody thought it would— a lot like our own 2016 election. That brings Britain back into the EEC, saves Europe, and has a positive impact on markets globally. So, this is a big deal. Not to do so would be economic suicide for Britain, and I think wiser heads will prevail.

Q: Do you think it’s a good idea for Saudi ARAMCO to go public in Japan as reports suggest?

A: When the Arabs want to get out of the oil business (USO), (XLE), you want to also. That’s what the sale of ARAMCO is all about. They’re going to get a $1 trillion or more valuation, raising $100 billion in cash. And guess who the biggest investors in alternative energy in California are? It’s Saudi Arabia. They see no future in oil, nor should you. This is why we’ve been negative on the sector all year. By the way, bankruptcies by frackers in the U.S. are at an all-time high, another indicator that low oil prices can’t be tolerated by the US industry for long.

Q: Is it time to buy the ProShares Ultra Short 20 year Plus Treasury Bond Fund (TBT)?

A: No, not yet; I think we’re going to break 1.33% — the all-time low yield for the (TLT) will probably be somewhere just below 1.00%. We probably won’t go to absolute zero because we still have a growing economy. The countries that already have negative interest rates have shrinking economies or are already in recession, like Germany or Great Britain can justify zero rates.

Q: Are you going to run all your existing positions into expiration?

A: I’m going to try to—it’s only 12 days to expiration, and we get to keep the full profit if we do. As long as the market is dead in the middle here, there are no other positions to put on, no extreme low to buy into or extreme high to sell into. It’s a question of letting this sort of nowhere-trend play out, but also there's nothing else to buy, so there is no need to raise cash. So, we’re 60% invested now and we’re going to try running as many of those into expiration as we can. Looks like all the long technology positions are safe (FB), (AMZN), (MSFT), (DIS). The only thing we’re pressing here are the shorts in Walmart (WMT) and Russell 2000 (IWM).

Q: Do you think it’s a good idea for Tesla (TSLA) to build another Gigafactory in Shanghai, China during a trade war? Will this blow up in Elon’s face?

A: I don’t think so because the Chinese are desperate for the Tesla technology and they just gave Tesla an exemption on import duties on all parts that need to go there to build the cars. So, that’s a very positive development for Tesla and I believe the stock is up about $10 since that news came out.

Q: Will Roku (ROKU) ever pull back? Would you buy it up here?

A: No, we recommended this thing last year at $40; it’s now up to $165, and up here it’s just wildly overbought, in chase territory. Of course, the reason that’s happening is that the big concern last year was Amazon wiping out Roku, yet they ultimately ended up partnering with Roku, and that’s worth about a 400% gain in the stock. You know the second you get into this, it’s over. There are just too many better fish to fry in the technology area.

Q: What happens if our existing Russell 2000 (IWM) September 2019 $153-$156 in-the-money vertical BEAR PUT spread Russell 2000 position closes between $156 and $153?

A: You lose money. You will get the Russell 2000 shares put to you, or sold to you at $153.00, which means you now own them, and you’ll get a big margin call from your broker for owning the extra shares. If ever it looks like we’re getting close to the strike price going into expiration, I come out precisely because of that risk. You don’t want random chance dictating whether you’re going to make money in your position or not going into expiration. If you’re worried about that, I would get out now and you can still come out with a nice profit. Or, you can always wait for another down day tomorrow.

Q: Is it time to get super aggressive shorting Lyft (LYFT) or Uber (UBER) when they openly admit that they won’t make a profit anytime in the near future?

A: The time to short Uber (UBER) and Lyft was at the IPO when the shares became available to sell. Down here I don’t really want to do very much. It’s late in the game and Uber’s down about one third from its IPO price. We begged people to stay away from this. It’s another example where they waited for the company to go ex-growth before it went public, but it didn’t leave anything for the public. It was a very badly mishandled IPO—it’s now at $31 against a $45 IPO price and was at a new all-time low just 2 days ago. You knew when they offered the drivers shares, the thing was in trouble. Sometime this will be a buy, but not yet. Go take a long nap first.

Q: Is the fact that rich people are hoarding cash a good indicator that a recession is approaching?

A: Yes, absolutely. Bonds yielding 1.45% is also an indication that the wealthy are hoarding cash from other investment and parking it in US treasury bonds. I went to the Pebble Beach Concourse d’ Elegance vintage car show a few weeks ago and all of the $10 million plus cars didn’t sell, only those priced below $100,000. That is always a good indicator that the wealthy are bailing ahead of a recession. If you can’t get a premium price for your vintage Ferrari, trouble is coming.

Q: Argentina just implemented currency controls; is this the start of a rolling currency crisis among emerging nations?

A: No, I believe the problems are unique to Argentina. They’ve adopted what is known as Modern Momentary Theory—i.e. borrowing and printing money like crazy. Unfortunately, this is unsustainable and results in a devalued currency, general instability, and the eventual hanging of their leaders from the nearest lamppost. This is exactly the same monetary policy that the Trump administration has been pursuing since he came into office. Eventually, it will lead to tears, ours, not his.

Q: Is the new all-electric Porsche Taycan a threat to Tesla?

A: No, it’s not. Their cheapest car is $150,000 and it gets one third less range than Tesla does. It’s really aimed at Porsche fanatics, and I doubt they will get outside their core market. In the meantime, Tesla has taken over the middle part of the electric market with the Model 3 at $37,000 a car. That’s where the money is, and Porsche will never get there.

Q: How will the US pull out of recession if the interest rates are at or below zero?

A: It won’t—that’s what a lot of economists are concerned about these days. With interest rates below zero, the Fed has lost its primary means to stimulate the economy. The only thing left to do is use creative means like feeding the economy with currency, which Europe has been doing for 10 years, and Japan for 30, with no results. That’s another reason to not allow rates to get back to zero—so we have tools to use when we go into a recession 12-24 months from now.

Q: What’s the best way to buy silver?

A: The ETF iShares Silver Trust (SLV) and, if you want to be aggressive, the silver miners with the Global X Silver Miners ETF (SIL).

Q: Have global central banks ruined the western economic system as we know it for future generations?

A: They may have—mostly by printing too much money in the last 10 years in order to get us out of recession. This hasn’t really worked for Europe or Japan, mind you, though who knows how much worse off they would be if they hadn’t. What it did do here is head off a Great Depression. If we go back to money printing in a big way, however, and it doesn’t work, we will not have prevented a Great Depression so much as pushed it back 10 or 15 years. That’s the great debate ongoing among economists, and it will eventually be settled by the marketplace.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/08/JT-with-snorkel-story-1-image-6-e1535059927176.jpg267350Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-09-06 04:02:202019-10-14 09:46:34September 4 Biweekly Strategy Webinar Q&A

I have a pretty good view from my home on a mountaintop in San Francisco.

To the west, I can see through the Golden Gate Bridge all the way out to the Farallon Islands 20 miles off the coast. To the south, there is Stanford’s Hoover Tower and all of Silicon Valley. In the winter I can look east and see the snow-covered High Sierras 200 miles away.

However, during last year’s wildfires, I couldn’t see a thing. Visibility ended at 100 yards, the cars parked outside were covered in ash, and I could barely breathe. We were all confined indoors.

I kind of feel that’s the way the stock market is right now. You can’t see a thing, so it’s better to stay indoors.

Not only are market gyrations subject to unpredictable and random, out-of-the-blue influences. The old playbook about cross market correlations and how asset classes respond at different points of the economic cycle doesn’t work either.

The good news is that August is over, the second worth trading month of the year. The bad news? September is the WORST trading month of the year!

So, what does a trader do on the first day of the worst investment month of the year?

Research.

That's what I’ll be doing, waiting for the next cataclysmic collapse to buy or the next euphoric bubble to sell short. Until then, I’ll be sitting tight. Just running my existing long/short trading book, I’ll be up 3.4% by the September 20 option expiration date in 15 trading days.

There is one BIG positive for the economy that no one is talking about. The home ATM is open for business, and open like it’s never been open before.

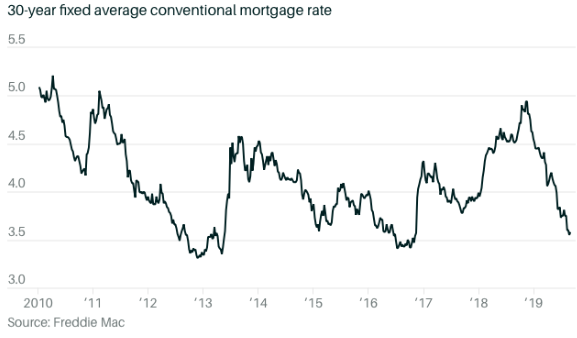

The thirty-year fixed rate mortgage rate is now at 3.56%, 10 basis points over a decade low and 20 basis points above an all-time low (see the chart below). There are currently $9.4 trillion of outstanding home mortgages in the US. Some $5 trillion is in Fannie Mae and Freddie Mac conforming loans, some 90% of which have interest rates higher than the current market.

If just ten million of these mortgages refinance obtaining an average of $4,560 in annual savings each, that will amount to a de facto tax cut of $456 billion per year, not an inconsequential amount. And Goldman Sachs thinks we could be in for as much as 37 million refis. It could be enough to offset the negative impact of the trade war.

As for the past week, it seemed like a disaster a day.

Trump ordered all US companies out of China. Like you can reverse 40 years’ worth of trillions of dollars of investment with a Tweet. If they did, an iPhone would cost $10,000 and your low-end laptop $15,000. An escalation of the trade war is the last thing your 401k wanted to hear. Kiss that early retirement goodbye.

Oilcrashed (USO) on trade war escalation, with the industry now seeing a recession as a sure thing. Russian cheating on quotas is pouring the fat on the fire creating a massive supply glut in the face of shrinking demand. Take a long nap before considering any energy investment (XLE). The long-term charts show they are all going to zero.

Prime Minister Boris Johnson suspended Parliament, prompting a free fall in the pound. It’s to keep Parliament from blocking his hard Brexit, where it would certainly loose by a landslide. It’s all up to the Queen now, the monarch, not the rock group.

The yield inversion is deepening, with the US Treasury selling two-year notes today at a 1.56% yield, with ten-year yield closing at 1.45%. And that’s with the Treasury selling a total of a gob smacking $113 billion worth of bonds last week, which should have driven rates UP! US ten-year TIPS now showing negative interest rates.

Company stock buybacks are fading. That's a big deal as corporations retiring their own shares have been the biggest buyers in the market for the past two years. As if you needed another reason for downside risk.

US 15% tariffs hit on Sunday, and the Chinese paused in retaliation. Christmas is about to get more expensive. Many large retailers won’t make it until the new year. Keep selling short Macy’s (M) on rallies.

Bond yields hit new lows, at 1.44% for ten-year US Treasury bonds. The next stop is zero. Fixed income markets are saying that a recession is imminent. “Inversion” will be the world of the year for 2019. Go refi that home if you can get a banker on the phone!

There is no way out of the next recession, says hedge fund titan Ray Dalio. With global rates below zero, you can’t cut to stimulate business. You can’t do any more quantitative easing either, as the world is already glutted with paper. This is the trap Japan has been caught in for the last 30 years. It is all sobering food for thought.

US growth slowed with the second reading of the Q2 GDP marked down from 2.1% to 2.0%. The downturn has continued since the economy peaked 18 months ago. Q3 will be much worse when the trade war and earnings downgrades hit big time. And then there’s the soaring deficit. Sow the wind, reap the whirlwind.

US Consumer Sentiment took a dive from 98.4 to 89.8 in August. Has the spending boom just peaked? If so, we’re all toast. The "tariff cliff" is already taking its toll.

The Mad Hedge Trader Alert Service has posted its best month in two years. Some 22 or the last 23 round trips, or 95.6%, have been profitable, generating one of the biggest performance jumps in our 12-year history.

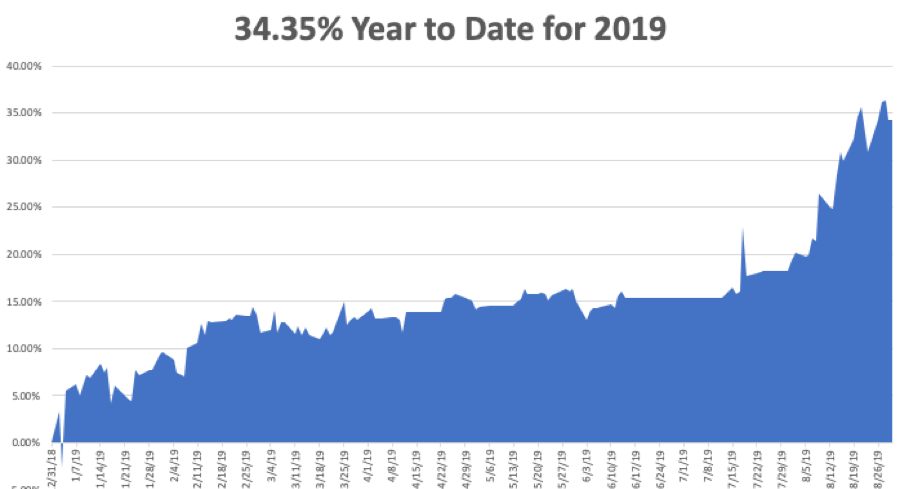

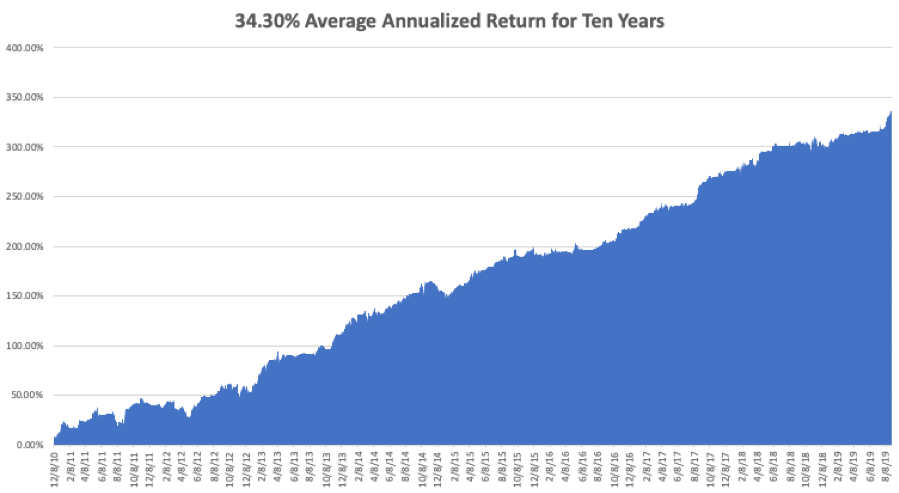

My Global Trading Dispatch has hit a new all-time high of 334.48% and my year-to-date shot up to +34.35%. My ten-year average annualized profit bobbed up to +34.30%.

I raked in an envious 16.01% in August. All of you people who just subscribed in June and July are looking like geniuses. My staff and I have been working to the point of exhaustion, but it’s worth it if I can print these kinds of numbers.

As long as the Volatility Index (VIX) stays above $20, deep in-the-money options spreads are offering free money. I am now 60% invested, 40% long big tech and 20% short Walmart (WMT) and the Russell 2000, with 20% in cash. It rarely gets this easy.

The coming week will be all about jobs, jobs, jobs.

Monday, September 2, markets were closed for the US Labor Day.

Today, Tuesday, September 3 at 10:00 AM, the August ISM Purchasing Manager’s Index is out.

On Wednesday, September 4, at 2:00 PM, the Fed Beige Book for July is published.

On Thursday, September 5 at 8:30 AM EST, the Weekly Jobless Claims are printed. At 10:30, we learn the ADP Report for private hiring.

On Friday, September 6 at 8:30 AM, the August Nonfarm Payroll Report is printed.

The Baker Hughes Rig Count follows at 2:00 PM.

As for me, I’ll be filling out the paperwork for my own home refi. JP Morgan Chase Bank (JPM) is offering the best deals, in my case a 30-year fixed rate no-cash-out jumbo loan for only 3.4%. Now where did I put that tax return?

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2019/06/john-thomas-camping.png431322Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-09-03 02:02:172019-10-14 09:45:45The Market Outlook for the Week Ahead, or Visibility is Poor

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.