Economists around the world have been scanning the horizon with their high powered Zeiss binoculars in search of the cause of the next global recession.

It has been a conundrum of the first order because a recession has NEVER taken place in the face of LOW interest rates and LOW oil prices.

However, we may have just found the trigger.

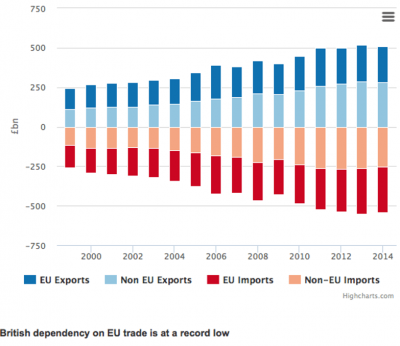

The possible impending departure of the United Kingdom from the European community has cataclysmic implications for economies everywhere.

We?ll know for sure when the referendum is held on June 23.

Yikes! I?ll be in England then!

The move is being driven by the same factors present in the American Republican Party presidential nomination race.

Working class Brits have lost jobs to a tidal wave of immigrants from the rest of the EC, whose common passports allow unfettered access to Old Blighty.

Take a weekend trip to London, and chances are that the desk clerk is from Poland, the porter is from Croatia, the waitress is from Italy, and the cleaning ladies are from Spain and Greece.

Actual Englishmen are to be found only in distant suburbs, or in unemployment offices.

The recent influx of immigrants from the Middle East has also placed a massive strain on the country?s social services resources.

Visit your local neighborhood National Health GP, and you will share the waiting room with foreign refugees missing arms or legs, or bearing near fatal combat injuries. It?s almost like visiting a wartime MASH unit.

Net net, the view is that EC membership is costing England jobs and money, probably in the billions of pounds per year.

As with the US, the populist view is at odds with the economic reality.

While the UK is a net contributor to the Brussels budget, that misses the point. It is greatly outweighed by the additional economic growth generated by EC membership.

Goods flow freely, duty free between all 23 member countries.

A manufacturer in Birmingham, Leeds, or Manchester doesn?t think twice about jumping on the Channel train to call on customers in Paris, Munich, or Copenhagen.

I often sit next to them during my summer continental travels and also get an update on whatever business they may be in.

A British departure would take nearly 20 years of business integration and dump it into the dustbin of history.

That would be a crushing loss for the British economy, which would lose much of the nearly ?200 billion pounds worth of exports it sent to the EC in 2015. These exports have grown at an impressive 3.6% a year for the past 15 years.

It would also deliver a fatal blow to the City of London, the financial center for all of Europe and one of its largest employers.

I can see the dominoes fall from here.

Europe would lose a similar amount of trade with the UK, taking a chunk out of GDP growth there.

A weak Europe brings a stumbling China, which relies on the continent as its largest customer (yes, even bigger than the US). And a wobbling China will certainly torpedo US exports, increasing volatility in our own financial markets.

In fact, the EC is the world?s largest economic entity. It is hard to see trouble there not spreading everywhere.

The turmoil is already easily visible in the foreign exchange markets. The British pound (FXB) has suffered a gut churning 10.5% nosedive over the past four months to a new ten year low. It has also smothered in the crib the recent rally in the Euro (FXE).

A newly resurgent dollar (UUP) is starting to once again cast a shadow over US multinational earnings.

It seems like the UK is determined to shrink to a smaller country, either by hook or crook.? Only last year, Scotland mounted a campaign to split off from the UK, an effort that eventually failed.

However, it is another one of those cases of being careful what you wish for.

How do you spell ?GLOBAL RECESSION??

Caveat Emptor

I Don't See Anything Yet

https://www.madhedgefundtrader.com/wp-content/uploads/2016/03/Man-with-Binoculars-e1456964153541.png186400DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2016-03-03 01:07:482016-03-03 01:07:48Will ?Brexit? Cause the Next Recession?

You wanted clarity in understanding the current state of play in the global financial markets? Here?s your #$%&*#!! clarity.

You should expect nothing less for this ridiculously expensive service of mine.

But maybe that is the cabin fever talking, now that I have been cooped up in my Tahoe lakefront estate for a week, engaging in deep research and grinding out the Trade Alerts, devoid of any human contact whatsoever.

Or, maybe it?s the high altitude.

I did have one visitor.

A black bear broke into my trash cans last light and spread garbage all over the back yard. He then left his calling card, a giant poop, in my parking space.

Judging by the size of the turds, I would say he was at least 600 pounds. This is why you never take out the trash at night in the High Sierras.

Ah, the delights of Mother Nature!

We certainly live in a confusing, topsy-turvy, tear your hair out world this year. Good news is bad news, bad news worse, and no news the worst of all.

The biggest under performing week of the year for stocks is then followed by the best. Net net, we are absolutely at a zero movement, and lots of clients complaining about poor returns on their investment.

I tallied the year-on-year performance of every major assets class and this is what I found.

+16% - Hedged Japanese Stocks (DXJ)

+15% - Hedged European stocks (HEDJ)

+13% - US dollar basket (UUP)

+10% - My house

0% - Stocks (SPY)

0% -? bonds (TLT)

-5% - Japanese Yen (FXY)

-11% - Euro (FXE)

-12% - Gold (GLD)

-18% -? Oil (USO)

-27% -? Commodities (CU)

-27% - Natural Gas (UNG)

There are some sobering conclusions to be drawn from these numbers.

There were very few opportunities to make money this year. If you were short energy, commodities, and foreign currencies, you did very well.

Followers of the Mad hedge Fund Trader can?t help but know and love these ticker symbols. They?ll notice that our long plays were found among the asset classes with the best performance, while our short bets populated the losers.

The problem with that is most financial advisors are not permitted to place client funds in the sort of inverse or leveraged ETF?s that most benefit from these kinds of moves (like the (YCS), (EUO), and (DUG)).

That left them reading about the success of others in the newspapers, even when they knew these trends were unfolding (through reading this letter).

How frustrating is that?

What was one of my best investments of 2015?

My San Francisco home, which has the additional benefit in that I get to live in it, have a place to stash all my junk, and claim big tax deductions (depreciated home office space, business use of phone, blah, blah, blah).

Of course, I do have the advantage of living in the middle of one of the greatest technology and IPO booms of all time. Every time one of these ?sharing? companies goes public, the value of my home rises by a few hundred grand.

The real problem here is that investing since the end of the Federal Reserve?s quantitative easing program ended a year ago has become a real uphill battle.

While the government was adding $3.9 trillion in funds to the economy we traders enjoyed one of the greatest free lunches of all time. It made us all look like freakin? geniuses!

Just maintaining their present $3.9 trillion balance sheet, not adding to it, has left almost every asset class dead in the water.

Heaven help us if they ever try to unwind some of that debt!

Janet has promised me that she isn?t going to engage in such monetary suicide.

The Fed is continuing with Ben Bernanke?s plan to run all of their Treasury bond holdings into expiration, even if it takes a decade to achieve this. And with deflation accelerating (see charts below), the need for such a desperate action is remote.

Still, one has to ponder the potential implications.

It all kind of makes my own 43% Trade Alert gain in 2015 look pretty good. But I don?t want to boast too much. That tends to invite bad luck and losses, which I would much rather avoid.

What! No QE?

https://www.madhedgefundtrader.com/wp-content/uploads/2015/11/Ship-Torpedoed-e1448310356189.jpg265400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-11-24 01:08:272015-11-24 01:08:27Bring Back QE!

Long-term observers of financial markets are befuddled, confused, and amazed at their complete lack of interest in the rapidly unfolding events in the Middle East.

It seems that the more horrific the atrocities, the higher stock prices want to climb.

Go figure.

ISIS is in fact accelerating the most important geopolitical event so far in this century, the rapprochement of relations between the U.S. and Iran, which have been in a deep freeze for 40 years.

A serious dialogue has not been held between these two countries since 52 hostages were seized at the American embassy in Tehran in 1979 and held for 444 days.

The Mullahs in Iran can?t help but notice last week?s U.S. air strikes to protect Shiite cities from a Sunni slaughter at the hands of ISIS. Suddenly, our natural enemy in the region has become our natural ally.

The Iranians have even offered to back up our air power with their ground forces, an offer the Obama administration has so far wisely turned down.

Don?t worry about ISIS. Their threat is being wildly overrated by the media.

There is a reason why terrorist groups have never held territory before. That makes them a big fat target for drones, smart bombs, and all the other types of fire that we rain down upon our enemies from above. This may be the first war in history entirely fought by drones on our side. That means it will be cheap, without casualties, and over quickly.

So what will the new treaty and peace between the U.S. and Iran bring us?

So far, Iran has agreed to a freeze on its nuclear enrichment program in exchange for international inspections and the unfreezing of $100 billion of their assets. Secret negotiations are being held intermittently in Geneva, Switzerland (I stopped by to say hello a few weeks ago).

This is unbelievably positive for all asset classes, except energy. This is the cause of the recent collapse of oil prices, which are now 65% off their 2014 high.

The US is now in a tremendously powerful negotiating position. If Iran dumps their nuclear program to our satisfaction, Iran then gets the carrot.

It will rejoin the world economy, unfreeze the rest of its assets and recover $100 billion a year in trade. The country?s banks will be allowed to rejoin U.S. dollar clearing, the $1 trillion a day CHIPS and SWIFT systems, their absence from which has been a deathblow to their international trade.

Its oil exports (USO) can recover from 750,000 barrels a day back to the pre crisis level of 3 million barrels. If it doesn?t then it gets the stick again in six months, resuming their economic freefall.

The geopolitical implications for the U.S. are enormous.? Iran is the last major rogue state hostile to the US in the Middle East, and it is teetering. The final domino of the Arab spring falls squarely at the gates of Tehran.

A friendly, or at least a non-hostile Iran, means we really don?t care what happens in Syria.

Remember that the first real revolution in the region was Iran?s Green Revolution in 2009. That revolt was successfully suppressed with an iron fist by fanatical and pitiless Revolutionary Guards.

The true death toll will never be known, but is thought to be well into the thousands. The antigovernment sentiments that provided the spark never went away and they continue to percolate just under the surface.

At the end of the day, the majority of the Persian population wants to join the relentless tide of globalization. They want to buy iPods and blue jeans, communicate freely through their Facebook pages and Twitter accounts, and have the jobs to pay for it all.

Since 1979, when the Shah was deposed, a succession of extremist, ultraconservative governments ruled by a religious minority, have abjectly failed to cater to these desires

If Iran doesn?t do a deal on nukes soon, it?s economy with sink deeper into the morass in which they currently find themselves. The Iranian ?street? will figure out that if they spill enough of their own blood that regime change is possible and the revolution there will reignite.

The Obama administration is now pulling out all the stops to accelerate the process.

The oil embargo former Secretary of State, Hillary Clinton, organized is steadily tightening the noose, with heating oil and gasoline becoming hard to obtain.

Yes, Russia and China are doing what they can to slow the process. This is what the Ukraine crisis is really all about, an attempt to keep oil prices high, Russia?s biggest earner.

But conducting international trade through the back door is expensive, and prices are rocketing. The unemployment rate is 40%.? The Iranian Rial has collapsed by 50%.

Let?s see how docile these people remain when the air conditioning quits running because of power shortages. Iran is a rotten piece of fruit ready to fall off on its own accord and go splat. The US is doing everything she can to shake the tree.

No military action of any kind is required on America?s part. No shot has been fired. That?s a big deal when the shots cost $10,000 apiece.

The geopolitical payoff of such an event for the U.S. would be almost incalculable. A successful revolution will almost certainly produce a secular, pro-Western regime whose first priority will be to rejoin the international community and use its oil wealth to rebuild an economy now in tatters.

Oil will has completely lost its risk premium, once believed by the oil industry to be $30 a barrel. A looming supply could cause prices to drop to as low as $20 a barrel.

This price drop seen so far amount to a gigantic $2.18 trillion trillion tax cut for not just the US, but the entire global economy as well (92 million barrels a day X 365 days a year X $65).

Almost all funding of terrorist organizations will immediately dry up. I might point out here that this has always been the oil industry?s worst nightmare.

ISIS is a short.

At that point, the US will be without enemies, save for North Korea, and even the Hermit Kingdom could change with a new leader in place. A long Pax Americana will settle over the planet.

The implications for the financial markets will be enormous. The US will reap a peace dividend as large, or larger, than the one we enjoyed after the fall of the Soviet Union in 1992.

As you may recall, that black swan caused the Dow Average to soar from 2,000 to 10,000 in less than eight years, also partly fueled by the technology boom.

A collapse in oil imports will cause the U.S. dollar (UUP) to rocket.? An immediate halving of our defense spending to $400 billion or less and burgeoning new tax revenues would cause the budget deficit to collapse.

With the US government gone as a major new borrower, interest rates across the yield curve will fall further. The national debt completely disappears by the 2030?s (as it almost did during the late 1990?s).

A peace dividend will also cause US GDP growth to reaccelerate from 2% to 4%. Risk assets of every description will soar to multiples of their current levels, including stocks, junk bonds, commodities, precious metals, and food.

The Dow will soar to 30,000 and the S&P 500 (SPY) to 3,500, the Euro collapses to parity, gold rockets to $2,300 an ounce, silver flies to $100 an ounce, copper leaps to $6 a pound, and corn recovers $8 a bushel.

Some 2 million of the armed forces will get dumped on the job market as our manpower requirements shrink to peacetime levels. But a strong economy should be able to soak these well-trained and motivated people right up.

We will enter a new Golden Age, not just at home, but for civilization as a whole.

Wait, you ask, what if Iran develops an atomic bomb and holds the US at bay?

Don?t worry. There is no Iranian nuclear device. There is no real Iranian nuclear program large enough to threaten the United States. The entire concept is an invention of Israeli and American intelligence agencies as a means to put pressure on the regime.

According to them, Iran has been within a month of producing a tactical nuclear weapon for the last 30 years. I'm still waiting.

The head of the miniscule effort they have was assassinated by Israeli intelligence two years ago (a magnetic bomb, placed on a moving car, by a team on a motorcycle, nice!).

If Iran had anything substantial in the works, the Israeli planes would have taken off a long time ago.

Even if Iran had one nuclear weapon, would they really want to attack a country with 6,700, the US?

There is no plan to close the Straits of Hormuz, either. The training exercises in small rubber boats we have seen are done for CNN?s benefit, and comprise no credible threat.

I am a firm believer in the wisdom of markets, and that the marketplace becomes aware of major history changing events well before we mere individual mortals do.

The Dow began a 25-year bull market the day after American forces defeated the Japanese in the Battle of Midway in May of 1942, even though the true outcome of that confrontation was kept top secret for years.

If the advent of a new, docile Iran were going to lead to a global multi-decade economic boom and the end of history, how would the stock markets behave now?

They would remain in a long-term bull market, much like we have seen for the past six years. That?s why 10% corrections have been few and far between.

The Problem is That it?s a Hollow Threat

Aim This One at the Bears

https://www.madhedgefundtrader.com/wp-content/uploads/2014/09/Missile-e1409784440285.jpg235400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-08-26 01:06:452015-08-26 01:06:45What?s Really Happening in the Middle East

Investors around the world have been confused, befuddled and surprised by the persistent, ultra low level of long term interest rates in the United States.

At today?s close, the 30 year Treasury bond yielded a parsimonious 2.01%, the ten year, 2.62%, and the five year only 1.51%. The ten-year was threatening its all time low yield of 1.37% only two weeks ago, a return as rare as a dodo bird, last seen in August, 2012.

What?s more, yields across the entire fixed income spectrum have been plumbing new lows. Corporate bonds (LQD) have been fetching only 3.29%, tax-free municipal bonds (MUB) 2.89%, and junk (JNK) a pittance at 5.96%.

Spreads over Treasuries are approaching new all time lows. The spread for junk over of ten year Treasuries is now below an amazing 3.00%, a heady number not seen since the 2007 bubble top. ?Covenant light? in borrower terms is making a big comeback.

Are investors being rewarded for taking on the debt of companies that are on the edge of bankruptcy, a tiny 3.3% premium? I think not.

It is a global trend.

German bunds are now paying holders 0.35%, and JGB?s are at an eye popping 0.30%. The worst quality southern European paper has delivered the biggest rallies this year. Portuguese government paper is paying only 2.40%, and is rapidly closing in on US government yields.

Yikes!

These numbers indicate that there is a massive global capital glut. There is too much money chasing too few low risk investments everywhere. Has the world suddenly become risk averse? Is inflation gone forever? Will deflation become a permanent aspect of our investing lives? Does the reach for yield know no bounds?

It wasn?t supposed to be like this.

Almost to a man, hedge fund managers everywhere were unloading debt instruments in January. They were looking for a year of rising interest rates (TLT), accelerating stock prices (QQQ), falling commodities (DBA), and dying emerging markets (EEM). Surging capital inflows were supposed to prompt the dollar (UUP) to take off like a rocket.

It all ended up being almost a perfect mirror image portfolio of what actually transpired since then. As a result, almost all mutual funds are down so far in 2014. Many hedge fund managers are tearing their hair out, suffering their worst year in recent memory.

What is wrong with this picture?

Interest rates like these are hinting that the global economy is about to endure a serious nose dive, possibly even re-entering recession territory?or it isn?t.

To understand why not, we have to delve into deep structural issues, which are changing the nature of the debt markets beyond all recognition. This is not your father?s bond market.

I?ll start with what I call the ?1% effect.?

Rich people are different than you and I. Once they finally make their billions, they quickly evolve from being risk takers into wealth preservers. They don?t invest in start-ups, take fliers on stock tips, invest in the flavor of the day, or create jobs. In fact, many abandon shares completely, retreating to the safety of coupon clipping.

The problem for the rest of us is that this capital stagnates. It goes into the bond market where it stays forever. These people never sell, thus avoiding capital gains taxes and capturing a future step up in the cost basis whenever a spouse dies. Only the interest payments are taxable and that at a lowly 20% rate.

This is the lesson I learned from servicing generations of Rothschild?s, Du Ponts, Rockefellers, and Getty. Extremely wealthy families stay that way by becoming extremely conservative investors. Those that don?t, you?ve never heard of, because they all eventually went broke.

This didn?t used to mean much before 1980, back when the wealthy only owned 10% of the bond market, except to financial historians and private wealth specialists, of which I am one. Now they own a whopping 23%, and their behavior affects everyone.

Who has bee the largest buyer of Treasury bonds for the last 30 years? Foreign central banks and other governmental entities, which count them among their country?s foreign exchange reserves. They own 36% of our national debt, with China in the lead at 8% (the Bush tax cut that was borrowed), and Japan close behind with 7% (the Reagan tax cut that was borrowed). These days they purchase about 50% of every Treasury auction.

They never sell either, unless there is some kind of foreign exchange or balance of payments crisis, which is rare. If anything, these holdings are still growing.

Who else has been soaking up bonds, deaf to repeated cries that prices are about to plunge? The Federal Reserve, which thanks to QE1, 2, and 3, now owns 22% of our $17 trillion debt. Both the former Federal Reserve governor Ben Bernanke, and the present one, Janet Yellen, have made clear they have no plans to sell these bonds. They will run them to maturity instead, minimizing the market impact.

An assortment of other government entities possess a further 29% of US government bonds, first and foremost the Social Security Administration, with a 16% holding. And they ain?t selling either, baby.

So what you have here is the overwhelming majority of Treasury bond owners with no intention to sell. Only hedge funds have been selling this year, and they have already done so, in spades.

Which sets up a frightening possibility for them, now that we are at the very bottom of the past year?s range in yields. What happens if bond yields fall further? It will set off the mother of all short covering squeezes and could take ten-year yield down to match the 2012, 2.38% low.

Fasten your seat belts, batten the hatches, and down the Dramamine!

There are a few other reasons why rates will stay at subterranean levels for some time. If hyper accelerating technology keeps cutting costs for the rest of the century, deflation basically never goes away (click here?for ?Peeking into the Future with Ray Kurzweil?).

Hyper accelerating corporate profits will also create a global cash glut, further levitating bond prices. Companies are becoming so profitable they are throwing off more cash then they can reasonably use or pay out.

This is why these gigantic corporate cash hoards are piling up in Europe in tax free jurisdictions, now over $2 trillion. Is the US heading for Japanese style yields, or 0.39% for 10 year Treasuries?

If so, bonds are a steal here at 2.55%. If we really do enter a period of long term -2% a year deflation, that means the purchasing power of a dollar increases by 35% every decade in real terms.

The threat of a second Cold War is keeping the flight to safety bid alive, and keeping the bull market for bonds percolating. This could put a floor under bond prices for another decade, and Vladimir Putin?s current presidential run could last all the way under 2014.

All of this is why I?m out of the bond market for now, and will remain so for a while.

Why Are They So Low?

https://www.madhedgefundtrader.com/wp-content/uploads/2014/05/Orangutan.jpg346382Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-16 01:05:282015-02-16 01:05:28Why Are Bond Yields So Low?

Foreign exchange traders are an odd lot. They tend to maintain a laser like focus on specific numbers that are utterly meaningless to us mere mortals, but which have momentous importance to themselves.

Right now, one is hearing the battle cry over the 120/120 targets. Specifically, traders want to take the yen down to Y120 to the US dollar, and the Euro down to $1.20 by the last trading day of 2014.

They may well get their wishes.

Powering the moves is the biggest policy divergence between central banks in a decade. The US Federal is threatening to take interest rates up every other day.

In the meantime, lower interest rates beckon in Europe and Japan as their economies lurch from one disaster to the next, dragging their own currencies down.

Accelerating the move is the gasoline that has been thrown on the economic fires caused by? You guessed it, plunging gasoline prices in the US, which is quickly turning into a massive stimulus program.

Wonder why Wal-Mart (WMT) has suddenly taken off to the races? It?s because their impoverished, gap toothed customers have suddenly received big cash bonuses, thanks to the war for market share among the members of OPEC.

Even a penny drop in the price of petrol adds $1 billion a year in consumer spending. Gas is so cheap that we might even break the $3 level here in high tax California.

Higher interest rates are great for the greenback because they prompt foreign investors to send more money here faster to chase higher returns than available at home.

The sharpest bond market move in history, taking ten year Treasury yields from 1.86% all the way up to 2.38% in four weeks, makes this view even more convincing.

Followers of this letter already know that the currencies have been in deep doo doo all year. That?s why I have been aggressively pushing out Trade Alerts to buy the dollar (UUP) and sell short the Euro (FXE), (EUO) and the Japanese yen (FXY), (YCS) for the past six months.

Readers have been laughing all the way to the bank.

The really thrilling part here is that this is only the beginning of a decade long move. My final target for the yen is Y150 and $1.00 for the Euro. This could be the trade that keeps on giving.

There are also important spillover implications for the stock market. It means more money for stocks at higher prices. The S&P 500 at 2,100 by yearend now looks like a chip shot, and we may probe even higher.

So why am I currently lacking any current positions in the currencies in my model trading portfolio? We are now at the end of extreme moves in all asset classes over the past month.

So, while everything looks hunky dory (a street in Yokohama where the cheap geishas used to hang out) in the markets, risk is, in fact, rising.

I have to admit that, being up 42.5% year to date, I have gotten spoiled. I am holding back for the low risk, high return type of entry points for new trades that my readers have become addicted to.

When I see one, you?ll be the first to know. Watch this space.

Gosh, I love this job.

See the Connection?

The Best Stimulus Program Ever

Wal-Mart Customer

https://www.madhedgefundtrader.com/wp-content/uploads/2014/11/Wacky-Guy.jpg288387Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-11-14 01:04:342014-11-14 01:04:34The 120/120 Battle

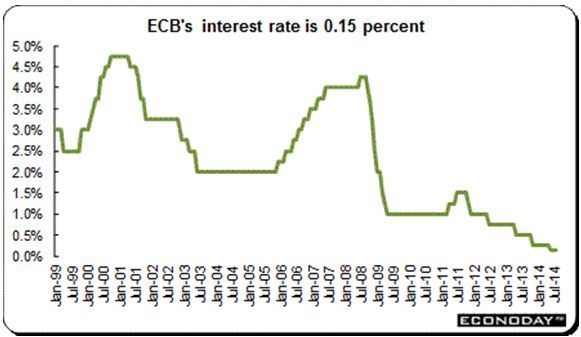

European Central Bank president Mario Draghi pulled the rug out from under the Euro (FXE), (EUO) this morning, announcing a surprise cut in interest rate and substantially adding to its program of quantitative easing.

The action caused the beleaguered currency to immediately gap down two full cents against the dollar, the ETF hitting a 15 month low of $127.40.

Surprise, that is, to everyone except a handful of strategists, including myself. Apparently, I was one of 4 out of 47 economists polled who saw the move coming, beating on my drum out of the coming collapse of the euro for the past six months.

I put my money where my mouth was, slamming out Trade Alerts to sell the Euro short, and sometimes even running a double position.

Of course, it helps that I just spent two months on the continent splurging at 90% off sales, and afterwards feasting on $10 Big Macs and $20 ice cream cones. Europe was practically begging for a weaker currency. Shorting the Euro against the greenback appeared to be a no-brainer.

A number of key economic indicators conspired to force Draghi?s hand this time around. August Eurozone inflation fell to a feeble 0.3%. France cut its 2014 GDP estimate at the knees, from 1.0% to 0.5%. Unemployment hovers at a gut wrenching 11.5%. To the continent?s leaders it all looked like a deflationary lost decade was unfolding, much like we saw in Japan.

Call the move an hour late, and a dollar short. Or more like 43,800 hours late and $4 trillion short. The US Federal Reserve started its own aggressive quantitative easing five years ago. The fruits of Ben Bernanke?s bold move are only just now being felt.

A major reason for the delay is that having a new currency, Europe lacks the breadth and depth of financial instruments in which it can maneuver. The Euro will soon be approaching its 15th birthday. Uncle Buck has been around since 1782.

The ECB?s move is bold when compared to its recent half hearted efforts to stimulate its economy. Its overnight lending rate has been cut from 0.15% to 0.05%, the lowest in history. Deposit rates have been pushed further into negative territory, from -0.10% to -0.20%. Yes, you have to pay banks to take your money! A QE program will lead to the purchase of 400 billion Euros worth of securities.

Am I selling more Euros here?

Nope.

I covered the last of my shorts last week, after catching the move in the (FXE) from $136 down to $130. That?s a major reason why my model trading portfolio is up a blistering 30% so far this year.

At $127, we are bang on my intermediate downside target. But get me a nice two or three cent short covering rally, and I?ll be back in there in a heartbeat. My next downside targets are $120, $117, and eventually $100. My European vacations are getting cheaper by the day.

https://www.madhedgefundtrader.com/wp-content/uploads/2014/09/Dollar-Certificate-e1409868770980.jpg400305Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-09-05 01:04:162014-09-05 01:04:16A Euro Collapse At Last!

I was amazed to see the Dow Average open up only 60 points this morning, and oil to fall a mere $1.50, given the enormous long term implications of a real nuclear deal with Iran. Over the decades, I have noticed that Wall Street isn?t very good at analyzing international political matters and the implications for their own markets. This appears to be one of those cases.

The news over the weekend about a freeze on Iran?s nuclear enrichment program in exchange for international inspections and the unfreezing of $4 billion of their assets is unbelievably positive for all asset classes, except energy. It came much sooner than expected. It proves that the administration?s preference for economic sanctions over military action has been wildly successful.

The US is now in a tremendously powerful negotiating position. If Iran dumps their nuclear program to our satisfaction it can get the carrot. It will rejoin the world economy, unfreeze the rest of its assets, and recover $100 billion a year in trade. Its oil exports (USO) can recover from 750,000 barrels a day back to the pre crisis level of 3 million barrels. If it doesn?t then it gets the stick again in six months, resuming their economic freefall.

The geopolitical implications for the U.S. are enormous.? Iran is the last major rogue state hostile to the U.S. in the Middle East, and it is teetering. The final domino of the Arab spring falls squarely at the gates of Tehran. A friendly, or at least a non-hostile Iran, means we really don?t care what happens in Syria.

Remember that the first real revolution in the region was Iran?s Green Revolution in 2009. That revolt was successfully suppressed with an iron fist by fanatical and pitiless Revolutionary Guards. The true death toll will never be known, but is thought to be in the thousands. The antigovernment sentiments that provided the spark never went away and they continue to percolate just under the surface.

At the end of the day, the majority of the Persian population wants to join the tide of globalization. They want to buy iPods and blue jeans, communicate freely through their Facebook pages and Twitter accounts, and have the jobs to pay for it all. Since 1979, when the Shah was deposed, a succession of extremist, ultraconservative governments ruled by a religious minority, have abjectly failed to cater to these desires

If Iran doesn?t do a deal on nukes soon, it?s economy with sink deeper into the morass in which they currently find themselves. The Iranian ?street? will figure out that if they spill enough of their own blood that regime change is possible and the revolution there will reignite. The Obama administration is now pulling out all the stops to accelerate the process.

The oil embargo former Secretary of State, Hillary Clinton, organized is steadily tightening the noose, with heating oil and gasoline becoming hard to obtain. Yes, Russia and China are doing what they can to slow the process, but conducting international trade through the back door is expensive, and prices are rocketing. The unemployment rate is 40%.? The Iranian Rial has collapsed by 50%. Iranian banks were kicked out of the SWIFT international settlements system, a deathblow to their trade.

Let?s see how docile these people remain when the air conditioning quits running this summer because of power shortages. Iran is a rotten piece of fruit ready to fall of its own accord and go splat. The US is doing everything she can to shake the tree. No military action of any kind is required on America?s part. No shot has been fired. That?s a big deal when the shots cost $10,000 apiece.

The geopolitical payoff of such an event for the U.S. would be almost incalculable. A successful revolution will almost certainly produce a secular, pro-Western regime whose first priority will be to rejoin the international community and use its oil wealth to rebuild an economy now in tatters.

Oil will lose its risk premium, now believed by the oil industry to be $30 a barrel. A looming supply could cause prices to drop to as low as $30 a barrel. This would amount to a gigantic $1.66 trillion tax cut for not just the U.S., but the entire global economy as well (87 million barrels a day X 365 days a year X $100 dollars a barrel X 50%). Almost all funding of terrorist organizations will immediately dry up. I might point out here that this has always been the oil industry?s worst nightmare. Hezbollah is a short.

At that point, the US will be without enemies, save for North Korea, and even the Hermit Kingdom could change with a new leader in place. A long Pax Americana will settle over the planet.

The implications for the financial markets will be enormous. The U.S. will reap a peace dividend as large, or larger, than the one we enjoyed after the fall of the Soviet Union in 1992. As you may recall, that black swan caused the Dow Average to soar from 2,000 to 10,000 in less than eight years, also partly fueled by the technology boom.

A collapse in oil imports will cause the U.S. dollar (UUP) to rocket.? An immediate halving of our defense spending to $400 billion or less and burgeoning new tax revenues would cause the budget deficit to collapse. With the U.S. government gone as a major new borrower, interest rates across the yield curve will fall further.

A peace dividend will also cause U.S. GDP growth to reaccelerate from 2% to 4%. Risk assets of every description will soar to multiples of their current levels, including stocks, junk bonds, commodities, precious metals, and food. The Dow will soar to 30,000 and the S&P 500 (SPY) to 3,500, the Euro collapses to parity, gold rockets to $2,300 an ounce, silver flies to $100 an ounce, copper leaps to $6 a pound, and corn recovers $8 a bushel. The 60-year bull market in bonds ends.

Some 1 million of the armed forces will get dumped on the job market as our manpower requirements shrink to peacetime levels. But a strong economy should be able to soak these well-trained and motivated people right up. We will enter a new Golden Age, not just at home, but for civilization as a whole.

Wait, you ask, what if Iran develops an atomic bomb and holds the U.S. at bay? Don?t worry. There is no Iranian nuclear device. There is no real Iranian nuclear program. The entire concept is an invention of Israeli and American intelligence agencies as a means to put pressure on the regime. According to them, Iran has been within a month or producing a tactical nuclear weapon for the last 30 years.

The head of the miniscule effort they have was assassinated by Israeli intelligence two years ago (a magnetic bomb, placed on a moving car, by a team on a motorcycle, nice!).

If Iran had anything substantial in the works, the Israeli planes would have taken off a long time ago. There is no plan to close the Straits of Hormuz, either. The training exercises in small rubber boats we have seen are done for CNN?s benefit, and comprise no credible threat.

I am a firm believer in the wisdom of markets, and that the marketplace becomes aware of major history changing events well before we mere individual mortals do. The Dow began a 25-year bull market the day after American forces defeated the Japanese in the Battle of Midway in May of 1942, even though the true outcome of that confrontation was kept top secret for years.

If the advent of a new, docile Iran were going to lead to a global multi-decade economic boom and the end of history, how would the stock markets behave now? They would rise virtually every day, led by the technology sector (XLK), industrials (XLI), and the banks (XLF) (C), offering no substantial pullbacks for latecomers to get in.

That is exactly what they have been doing since August. The markets are telling us that a treaty of real substance is a done deal.

Aim This One at the Bears

https://www.madhedgefundtrader.com/wp-content/uploads/2013/11/Iran-Nuclear-Missile.jpg310517Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-11-26 01:04:162013-11-26 01:04:16Here Comes the Next Peace Dividend

I think that oil peaked last week with the Egyptian Army?s ferocious and bloody attack on the Muslim Brotherhood. I hate to sound cynical here, but count the daily bodies in the street, which has been trending down sharply since Thursday?s, 1,000 plus tally. Fewer bodies mean lower oil prices.

This has most likely broken the back of the fundamentalist opposition movement for at least the time being, which has accounted for the $20 spike in oil prices over the last two months.

This returns us to the longer term fundamental trend for oil, which is sideways at best, and down at worst. The US is flooding the world?s oil markets with energy in all its many forms. The driver here is American fracking technology, which will continue to upend the traditional energy markets for decades to come. It?s just a matter of time before fracking goes mainstream in Europe, especially in the big coal countries of Germany, Poland, and England. Then they can thumb their noses at Russia, a major gas supplier over the last thirty years. China will follow.

In a crucial news item that wasn?t reported nationally, the California legislature voted down a measure to ban hydraulic fracturing in their state. It was defeated in a democratically controlled body. As the Golden State is the most anti energy state in the country, this gives the state a flashing green light to move forward against environmentalist opposition. There is a ton more of new supply coming. This is what the weakness in the price of natural gas is telling you (UNG).

We also received a new negative for oil this month, the collapse of the emerging market currencies, stock markets, and bonds, especially the Indian rupee. This reduces their international purchasing power in US dollar terms, thus raising the cost of oil in local currency terms. You see, oil is priced in dollars. As the emerging markets have seen the largest growth in demand for oil in recent years, this can only be bad for prices.

In terms of my own trading portfolio, I want to have a ?RISK OFF? position, like an oil short, to hedge my two existing ?RISK ON? positions in the Euro (FXE) and the yen (FXY) shorts. US stock markets could be weak into September, and they will take oil down with them.

The energy inventory figures released on Wednesday were another tell. Oil came in line with a 1.5 million barrel weekly draw down. But gasoline showed a precipitous 4 million barrel drop in supplies, meaning that more people are driving to their summer vacations than expected. Texas tea should have rallied at least $1 on the news. Instead it fell $1.50. It is an old trading nostrum that if a contract can?t rally on surprisingly positive developments, you sell the daylights out of it. Below, you will find another chart that you should wake up and take notice of, the Powershares DB US Dollar Bullish Index Fund (UUP).Commodities traditionally are weak when the dollar is strong. Both the chart and the fundamentals suggest that we are close to a multiyear low for the greenback and are about to enter a prolonged period of dollar strength.This is also grim tidings for oil.

Finally, there is that last resort, the charts. Check out those for the (USO) and oil and it very much looks like we have a triple top in place. That is the straw that breaks the camel?s back. Time to sell.

The only way I am wrong on my oil call is if the Chinese economy is about to take off like a rocket. They are the marginal big swing player in this market. But there is absolutely no sign of that happening in the economic data. If anything, the collapse in emerging markets suggest that conditions in the Middle Kingdom are about to get worse before they get better.

Ouch! That Hurt!

https://www.madhedgefundtrader.com/wp-content/uploads/2013/08/Camel.jpg406333Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-08-22 12:50:482013-08-22 12:50:48Why I Sold Oil

When I staggered downstairs at 11:00 PM to check the close for the Tokyo stock market, my eyes just about popped out of my head. Yikes! Down 6.3%! The yen was up another 2% to ?94 against the US dollar as well!! It looked like the world was in for another round of ?RISK OFF? with a turbocharger. Fasten your seatbelts, and pack an extra pair of shorts.

So I called an old friend in Japan who always seems to know what is going on whenever the wheels fall off there. Ed Merner is the CEO of the Atlantis Japan Growth Fund (LSE-AJG), who has long been rated the number one stock picker in the Land of the Rising Sun. Ed?s fund, which trades on the London Stock Exchange, was, at one point, up a gob smacking 53% this year without a stitch of leverage.

When the ink was barely dry on the US Japan peace treaty in 1950, Ed?s father uprooted his family from the rural High Sierra hamlet of Truckee, California, and moved them to Tokyo. That gave him a front row seat to the economic miracle that followed in the fifties and sixties.

Ed started managing money just a few years before me, in 1970. He toiled away as a portfolio manager at Schroeder?s & Co. in Tokyo for 25 years and then launched his own firm in 1995. Ed, who is a fascinating individual and a genuine nice guy, is the man I always turn to for my long-term view on Japan. Suffice it to say, Ed knows which end of a piece of sushi to hold upward, and is said to be able to snatch a fly midair with a pair of chopsticks. His Japanese is flawless, and he is now regarded as a local celebrity.

Ed says that the ?Rebirth of Japan? story is anything but over, and in fact, is just getting started. He thinks that the Nikkei index could soar from the current ?12,445 to above the 1989 all time high of ?39,000 in years to come. What we are seeing now is a long overdue rest for the world?s best performing major stock market. Bank of Japan mouthing?s of empty platitudes, rather than concrete action is what triggered the current rout.

Much of the money that went into Japan this year was of the hot, algorithm driven variety. You saw this in the dominance of the index names in trading, like Sony (SNE), Toyota (TM), and Honda Motors (HMC). Individual stock picking almost ceased to exist as an investment strategy. When the same hedge funds all tried to unwind their Japanese stock longs and yen shorts at the same time, you got the predictable flash fire in the movie theater. Margin calls became the order of the day.

As the index money leaves in this correction, it will be replaced by more traditional mutual fund and individual investors, who have a more stable orientation. Stock selection will become more fundamentally driven. That?s when Japan transitions from the flavor of the day to a serious core investment.

Now is about the time you should expect that to happen. Japan?s upper House of Councilors election will take place on July 21, and Prime Minister Abe?s ruling Liberal Democratic Party will win by a landslide. After that, you can expand Abe?s plans for an overdue major restructuring of the economy to mature from idle speculation to specific proposals. That is what the market wants to hear. Until then, he is loath to ruffle political feathers. He is going to have to break a lot of eggs to make this omelet.

On the table in his ?Third Arrow? plan are deregulation of virtually all financial markets, modernization of the health care system, immigration reform to open the way for more foreign workers, and rationalization of a bloated government bureaucracy. International trade will get streamlined and capital investment incentivized. More infrastructure spending will be aimed at maintenance and repair, so there will be no more ?bridges to nowhere.?

Oh, and he wants to enable the national pension fund system to step up its purchases of Japanese stocks. Abe wants to compress all of the deregulation that the US has enacted in the past 30 years into the next three.

The truly encouraging thing here is that Abe?s early actions are already bearing fruit. ?Arrows? 1 and 2 put the country on track to double its money supply in two years and paved the way for a staggering $150 billion in new public works spending. The crash in the yen this prompted is causing corporate earnings to go through the roof. Those results will be reported in the fall.

Then, the best company performance in two decades and a national reorganization plan on the scale of Roosevelt?s New Deal will be the impetus for the next leg up in the Great Japanese Bull Market of the 2010?s. That is why I banged out Trade Alerts on Wednesday to buy Japanese stocks through the Wisdom Tree Japan Hedge Equity ETF (DXJ) and sell short the yen through the Currency Shares Japan Yen Trust ETF (FXY) and the Proshares Ultra Short Yen ETF (YCS).

Atlantis Japan Growth Fund

Use the Dip to Buy Japan

https://www.madhedgefundtrader.com/wp-content/uploads/2013/06/Asian-Maids1.jpg180479Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-06-14 07:51:522013-06-14 07:51:52The Yen Carry Trade Blow Up

The big surprise today was not that the Federal Reserve launched QE3, but the extent of it. ?For a start, they moved the ?low interest rate? target out to mid-2015. ?They left the commitment to bond-buying open-ended. ?The first-year commitment came in at $480 billion, in-line with previous efforts.

Reading the statement from the Open Market Committee, you can?t imagine a more aggressive posture to stimulate the economy. ?You have to wonder how bad the data that we haven?t seen yet is, not just here, but in Europe and Asia as well. The big question now is: ?Will it make any difference??

Asset markets certainly bought the ?RISK ON? story hook, line, and sinker in the wake of the Fed action. ?Gold leapt $30, the Dow soared 200 points, the dollar (UUP) was crushed, the Australian dollar (FXA) rocketed a full penny (ouch!), and junk bonds (HYG) caught a new bid at all-time highs. ?The real puzzler was the Treasury bond market, which saw the (TLT) fall 2 ? points. ?I guess this is because the new Fed buying will be focused on mortgage-backed securities at the expense of Treasuries.

I knew that if they were to do anything, it would be aimed at the residential real estate market, which has been a thorn in their side for the last five years. ?The reason we have 1.5% growth instead of 3% is real estate. Real estate is the missing 1.5%.

But what will be the impact? ?Some $480 billion of buying of mortgage-backed securities over the next 12 months will lower the 30 year conventional mortgage from the current 3.70%. ?But all that will do is enable those who refinanced for the last two years in a row to do so a third time. Those who are underwater on their mortgages and have only negative equity to offer banks as collateral will remain shut out. ?This will generate a big payday for mortgage brokers, but won?t trigger any net new home-buying which the economy desperately needs.

The harsh reality for the housing market is that the demographic headwind of downsizing baby boomers is so ferocious that the Fed is unable to piss against it. Here is the problem:

*80 million baby boomers are trying to sell houses to 65 million Gen Xer?s who earn half as much

*6 million homes are late or in default on payments

*An additional shadow inventory of 15 million units overhangs the market owned by frustrated sellers

*Fannie Mae and Freddie Mac are in receivership, which account for? 95% of US home mortgages.? Each needs $100 billion in new capital. Good luck getting that out of a deadlocked congress

*The home mortgage deduction a big target in any tax revamp. The government would gain $250 billion in revenues in such a move

*The best case scenario for real estate is that we bump along a bottom for 5 years. The worst case is that we go down another 20% when a recession hits in 2013.

It could be that 95% of the new QE3 is already in the market, and that the markets will roll over once the initial headlines and ?feel good? factor wears off. ?With the markets discounting this action for nearly four months, this could be one of the greatest ?buy the rumor, sell the news? opportunities of all time.

Whatever the case, I am not inclined to chase risk assets up here. Anyway, I am now so far ahead of my performance benchmarks for the year that I can?t even see them on a clear day.

Is That My Benchmark Out There?

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-09-13 23:03:282012-09-13 23:03:28QE3 Blows Out Bears.

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.