Global Market Comments

April 19, 2022

Fiat Lux

Featured Trade:

(WHERE THE ECONOMIST “BIG MAC” INDEX FINDS CURRENCY VALUE TODAY),

(UUP), (FXE), (FXY), (CYB)

Global Market Comments

April 19, 2022

Fiat Lux

Featured Trade:

(WHERE THE ECONOMIST “BIG MAC” INDEX FINDS CURRENCY VALUE TODAY),

(UUP), (FXE), (FXY), (CYB)

Global Market Comments

February 17, 2022

Fiat Lux

Featured Trades:

(HOW TO HEDGE YOUR CURRENCY RISK),

(FXA), (UUP)

(TESTIMONIAL)

Mad Hedge Bitcoin Letter

November 23, 2021

Fiat Lux

Featured Trade:

(THE STRONG BREADTH OF CRYPTO)

(BTC), (ETH), (ADA), (SOL), (UUP)

Global Market Comments

September 20, 2021

Fiat Lux

Featured Trade:

(INTRODUCING THE MAD HEDGE BITCOIN PLATINUM SERVICE),

(MARKET OUTLOOK FOR THE WEEK AHEAD, or THE BATTLE OF THE 50-DAY),

(SPY), (TLT), (DIS), (BLOK), (MSTR), (QQQ), (EEM), (UUP)

The next long-term driver of financial markets will be rising interest rates.

It’s not a matter of if, but when. Is it this month, or next month? One way or the other it’s coming.

Which means you should be rearranging your portfolio right now big time.

In a rising interest rate regime seven big things will happen:

1) Bonds (TLT) will collapse.

2) Domestic recovery and commodity stocks (FCX) will soar.

3) Technology stocks (QQQ) will move sideways to down 10%

4) The US dollar (UUP) craters

5) Foreign stock markets (EEM) do better than American ones.

6) Bitcoin (BLOK), (MSTR) and other cryptocurrencies go through the roof.

7) Residential real estate keeps appreciate, but at a slower rate.

These trends will continue for six months, or until long-term interest rates hit an interim peak, such as at 2.00%.

The delta variant gave us a secondary recession. Its demise will give us a secondary recovery, and the same sectors will prosper as with the first. According to the Johns Hopkins University of Medicine, this is happening right now.

The only caution here is that long-term investors should probably keep their technology stocks. Once rates hit the next interest rate peak again, it will be off to the races for tech once again. In the long term, tech always comes back, and tech always wins.

Of course, the major event of the coming week will be the Federal Reserve’s Open Market Committee meeting where interest rates are decided and the press conference with Jay Powell that follows.

Interest rates won’t move. It’s the press conference that is crucial, where we gain insights into the taper. What’s different this time is that the European Central Bank has already begun their taper with an economy far weaker than ours. Will Jay take the cue?

Far and away, the most reliable indicator for “BUY” timing since the presidential election has been the 50-day moving average for the S&P 500. Increasing stock weightings there and you were golden.

The problem now is that we have not seen the index close below the 50-day for two consecutive days for a record 221 days. This has not happened for 31 years.

We all know the reasons: Record low-interest rates making cash trash, seven years of quantitative easing, and a global liquidity glut. Exploding equity in homes and stock portfolios helps too. Still, 31 years is a long time to be this bullish.

I saw all this coming a mile off.

Since the election, I have relentlessly pursued this market with a super aggressive 100% weighting. Then I started paring back risk in June. In July and August, I cut back further to the bone, running minuscule 20% long weightings against a few shorts.

And this is how you manage your risk control.

When markets are rigged in your favor and the lunch is free, you bet the ranch. When they aren’t, you cower on the sidelines and watch others take insane risks.

But who am I to know? I’ve only been doing this for 51 years, and 58 years if you count the (IBM) shares I bought with my paperboy earnings.

Antitrust Comes Home to Roost at Apple, sending the stock down $9 in two days. A judge ruled that Apple will no longer be allowed to prohibit developers from providing links or other communications that direct users away from Apple in-app purchasing. Apple typically takes a 15% to 30% cut of gross sales. It’s a slap on the wrist, as Apple’s main revenue stream is still from iPhones. The judge ruled in favor of Apple on nine of ten other issues. It creates massive new opportunities for hundreds of other Silicon Valley start-ups. Still, if you were looking for an excuse to take profits, this is it. Buy (AAPL) on dips.

Tesla to get EV Tax Credit Restored in a new overhaul of alternative energy subsidies. Both Tesla (TSLA) and General Motors (GM) lost their $7,500 per car subsidies when sales topped 200,000. GM will get an extra $5,000 discount for union-made cars. Tesla is ferociously non-union. Maybe this explains the 36% rally since May. It should help (TSLA) get reach its million-vehicle target for 2021 if it can get enough chips. Buy (TSLA) on dips.

China Inflation Hits 13 Year High, up 9.5% YOY. Soaring commodity and coal prices are the issue. Coal is up 57% YOY, reflecting an energy shortage during the covid economic rebound. It predicts a hot CPI for the US on Tuesday.

The Consumer Price Index rose by 5.3% YOY and up 0.3% in August. It was a seven-month low, with delta clearly a drag. Food and energy came in lighter than expected. Prices for used cars, air tickets, and insurance fell. Stocks loved it, rising triple digits, and bond prices halved losses. St next week’s FOMC we’ll see how Jay really feels.

House Looking at a Top 26.5% Corporate Tax Rate, well up from the current 21% but not as high as the 28% that was feared. Capital gains would rise from 20% to 25%. The goal is to raise $2.5 trillion to get the $3.5 trillion spending package into law. It’s all a trial balloon for what might be possible. Stocks loved it.

Amazon to Hire 125,000 and boost wages to $18 an hour. They are also paying $3,000 signing bonuses and taking pay up to $22.50 in prime areas like New York and California. It’s all part of a strategy to make (AMZN) the “best employer in the world”. Buy (AMZN) on dips as its dominance on online commerce grows.

China Destroys Casino Stocks, threatening to increase oversight of their Macao operations. The concern is that China will pull the gaming licenses of foreign companies when they come up for renewal in June. Buy (WYNN) and (LVS) on the dip.

Weekly Jobless Claims Come in at 332,000, a new post-pandemic low. The previous week was revised down even lower, to 312,000. The end of pandemic unemployment benefits is no doubt a factor, driving people off of their couches and back to the salt mines. Is this the light at the end of the tunnel?

Bitcoin Charts are Showing a Golden Cross, which usually presages upside breakouts in the cryptocurrency. A golden cross is where the 50-day moving average pierces the 200-day to the upside. This is crucial because technicals are more important in crypto than in any other financial instrument. In the meantime, (AMC) has started accepting Bitcoin for online movie ticket purchases. Buy (MSTR) on dips.

My Ten-Year View

When we come out the other side of the pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

My Mad Hedge Global Trading Dispatch saw a modest +1.10% loss so far in September following a blockbuster 9.36% profit in August. My 2021 year-to-date performance soared to 77.47%. The Dow Average is up 13.02% so far in 2021.

That leaves me 70% in cash, 10% short in the (TLT), and 20% long in the (SPY) and (DIS). Both of our September option positions expired at max profits.

I’m keeping positions small as long as we are at extreme overbought conditions. However, a Volatility Index (VIX) above $20 shows there may be a light at the end of the tunnel.

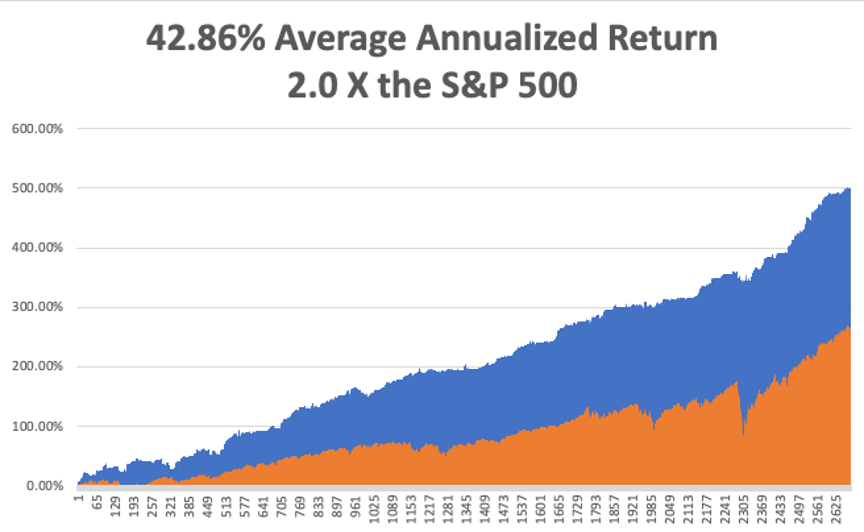

That brings my 12-year total return to 500.02%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 42.86%, easily the highest in the industry.

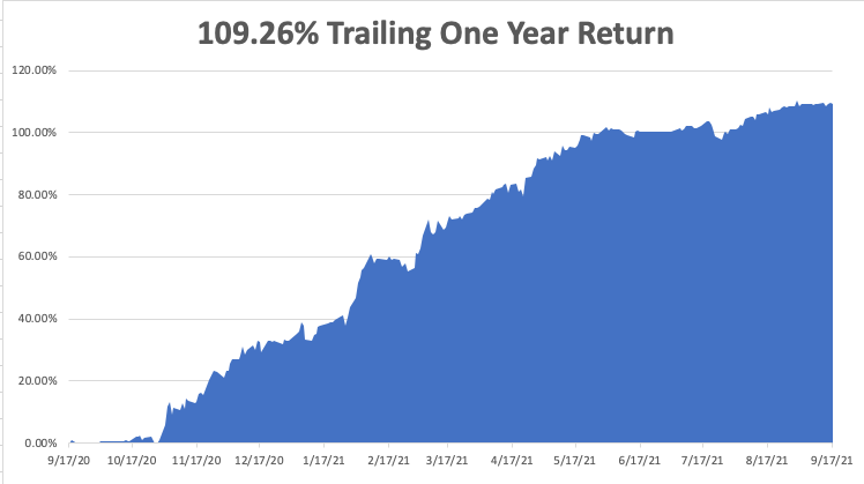

My trailing one-year return popped back to positively eye-popping 109.26%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 42 million and rising quickly and deaths topping 673,000, which you can find here.

The coming week will be all about the Fed meeting on Wednesday.

On Monday, September 20, at 11:00 AM, the NAHB National Housing Market Index for September is out.

On Tuesday, September 21 at 9:30 AM, Housing Starts for August are printed.

On Wednesday, September 22 at 11:00 AM, Existing Home Sales for August are announced. At 2:00 PM, the Fed interest rate decision is released and an important press conference about taper issues follows.

On Thursday, September 23 at 8:30 AM, Weekly Jobless Claims are announced.

On Friday, September 24 at 8:30 AM, we learn US Durable Goods for August. At 2:00 PM, the Baker Hughes Oil Rig Count is disclosed.

As for me, with the shocking re-emergence of Nazis on America's political scene, memories are flooding back to me of some of the most amazing experiences in my life.

I have been warning my long-term readers for years now that this story was coming. The right time is now here to write it.

I know the Nazis well.

During the civil rights movement of the 1960s, I frequently hitchhiked through the Deep South to learn what was actually happening.

It was not usual for me to catch a nighttime ride with a neo-Nazi on his way to a cross burning at a nearby Ku Klux Klan meeting, always with an uneducated blue-collar worker who needed a haircut.

In fact, being a card-carrying white kid, I was often invited to come along.

I had a stock answer: "No thanks, I'm going to another Klan meeting further down the road."

That opened my driver up to expound at length on his movement's bizarre philosophy.

What I heard was chilling.

During 1968 and 1969, I worked in West Berlin at the Sarotti Chocolate factory in order to perfect my German. On the first day at work, they let you eat all you want for free.

After that, you get so sick that you never wanted to touch the stuff again. Some 50 years later and I still can’t eat their chocolate with sweetened alcohol on the inside.

My co-worker there was named Jendro, who had been captured by the Russians at Stalingrad and was one of the 5% of prisoners who made it home alive in 1955. His stories were incredible and my problems pale in comparison.

Answering an ad on a local bulletin board, I found myself living with a Nazi family near the company's Tempelhof factory.

There was one thing about Nazis you needed to know during the 1960s: They loved Americans.

After all, it was we who saved them from certain annihilation by the teeming Bolshevik hoards from the east.

The American postwar occupation, while unpopular, was gentle by comparison. It turned out that everyone loved Hershey bars.

As a result, I got free room and board for two summers at the expense of having to listen to some very politically incorrect theories about race. I remember the hot homemade apple strudel like it was yesterday.

Let me tell you another thing about Nazis. Once a Nazi, always a Nazi. Just because they lost the war didn't mean they dropped their extreme beliefs.

Fast-forward 30 years, and I was a wealthy hedge fund manager with money to burn, looking for adventure with a history bent during the 1990s.

I was mountain climbing in the Bavarian Alps with a friend, not far from Garmisch-Partenkirchen, when I learned that Leni Riefenstahl lived nearby, then in her 90s.

Attending the USC film school with a young kid named Steven Spielberg decades earlier, I knew that Riefenstahl was a legend in the filmmaking community.

She produced such icons as Olympia, about the 1932 Berlin Olympics, and The Triumph of the Will, about the Nuremberg Nazi rallies. It is said that Donald Trump borrowed many of these techniques during his successful 2016 presidential run.

It was rumored that Riefenstahl was also the onetime girlfriend of Adolph Hitler.

I needed a ruse to meet her since surviving members of the Third Reich tend to be very private people, so I tracked down one of her black and white photos of Nubian warriors, which she took during her rehabilitation period in the 1960s.

It was my goal to get her to sign it.

Some well-placed intermediaries managed to pull off a meeting with the notoriously reclusive Riefenstahl, and I managed to score a half-hour tea.

I presented the African photograph and she seemed grateful that I was interested in her work. She signed it quickly with a flourish.

I then gently grilled her on what it was like to live in Germany in the 1930s. What I learned was fascinating.

But when I asked about her relationship with The Fuhrer, she flashed, "That is nothing but Zionist propaganda."

Spoken like a true Nazi.

The interview ended abruptly.

I took my signed photograph home, framed it, hung it on my office wall for a few years. Then I donated it to a silent auction at my kids' high school.

Nobody bid on it.

The photo ended up in storage at my home, and when it was time to make space, it went to Goodwill.

I obtained a nice high appraisal for the work of art and then took a generous tax deduction for the donation, of course.

It is now more than a half-century since my first contact with the Nazis, and all of the WWII veterans are gone. Talking about it to kids today, you might as well be discussing the Revolutionary war.

By the way, the torchlight parade we saw in Charlottesville, VA in 2017 was obviously lifted from The Triumph of the Will, except that they didn't use tiki poolside torches in Germany in the 1930s.

Leni Riefenstahl

Olympia

Former Paperboy

Global Market Comments

August 4, 2021

Fiat Lux

Featured Trade:

(WHERE THE ECONOMIST “BIG MAC” INDEX FINDS CURRENCY VALUE TODAY),

(UUP), (FXE), (FXY), (CYB)

Global Market Comments

May 24, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or IT'S ALL ABOUT THE NUMBERS),

(TLT), (SPY), (FCX), (QQQ), (VIX), (UUP), (AMAT), (CRM), (GOOG), (AMZN), (AAPL), (FB)

I know that not all of you are mathematicians, nor blessed with math degrees from UCLA, as I am. However, the future of your retirement funds relies on a few simple numbers. So, I will try to be gentle.

S&P tech stocks are trading at a 27 price earnings multiple. The S&P 500 Index, as a whole, trades at a 21 multiple. S&P value stocks, financials, and old-line recovery stocks like industrials and materials are trading at a 17 multiple.

Historically, companies with double the earnings power of the index trade at a 5-point premium to the main market. As long as this disparity exists, tech stocks will go down and value with go up.

However, we are getting close to a reversal. Allowing for market noise, I don’t see tech dropping more than 10% from here over the coming months. Then we will see the mother of all Q4 rallies taking it to new highs.

That explains why investors have been nibbling on tech lately, especially the best ones like NVIDIA (NVDA), Applied Materials (AMAT), and Salesforce (CRM). You also want to pick up big cap money machines like Alphabet (GOOG), Amazon (AMZN), Apple (AAPL), and Facebook (FB). Their LEAPS are begging for attention.

That means the downside from here is limited. Sorry Cassandras, no crashes here.

I am more convinced of this outcome than ever, given the substantial number of crashes and disasters, markets have weathered this year. These are truly Teflon markets. Last week, Bitcoin collapsed an amazing 55% in six weeks, wiping $1 trillion off the value of that market.

The fear had been that a crypto crash of this size would ignite a system contagion that would take everything down. A few years ago, it would have. But with massive Fed liquidity and unprecedented deficit spending, all we got was down 600 points one day and 600 up the next.

No crash here.

We’ve also had smaller crashes in sectors that were the most egregiously overpriced in February, like SPACS, meme stocks, and shares trading at 100 times sales with no earnings. Again, no harm no foul. It was a comeuppance that was well earned.

The big tell that I am right came screaming loud and clear last week from the US dollar, which hit a new 2021 low. A cheaper greenback means cheaper US stocks for foreign investors, which means they buy more of them. A weak buck also means that interest rates will stay lower for longer, which is great news for stocks, especially tech.

So, take it easy for the next few months. Keep positions small and rejoin the human race.

It seems odd going out into civilization and seeing live people walking around without masks. All the batteries on my watches are dead, as they have not been used for nearly two years, so they are getting replaced. I walked into my closet, and it was like adventuring into an archeological dig, with dozens of Turnbull & Asser shirts untouched by human hands. I’ve been living in Marine Corps sweats since 2019.

Bitcoin Crashes, down 33% on the day at the lows to $30,000, and off a heart-palpitating 55% from the April high. You wanted volatility, you got volatility! The problem for the rest of us is whether this will cause a real systemic financial crisis, with the Dow already down 560 at today’s low. Was Elon Musk the shoeshine boy giving tips at the market top?

Chip Shortage causes $110 Billion in US Car Industry Sales, in 2021 and will take years to address. Supply chains will need to be rebuilt. My neighbor just had to wait 11 months to take delivery of his Ford F-150.

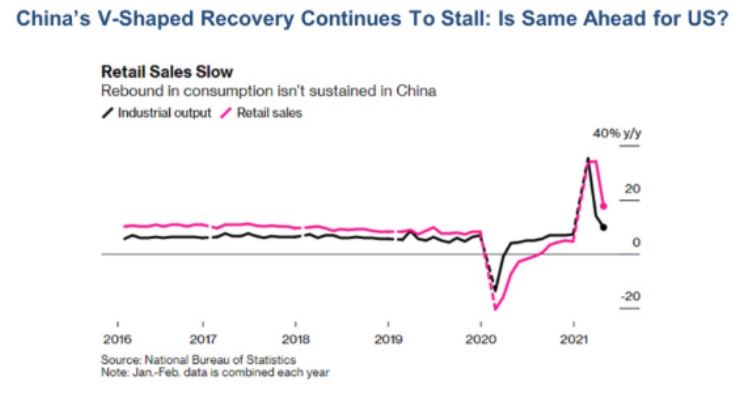

China’s Industrial Production Slows, from 14.1% in March to only 9.8% in April. That gives us a hint to our own future, as the Middle Kingdom emerged from the pandemic a year before we did. Retail sales also disappointed. After rocketing in 2020, the Chinese economy started slowing at the beginning of this year. The dead cat bounce in the economy is over. If this continues, it's bad news for copper prices of which the Middle Kingdom is the largest producer. If (FCX) closes under $40, stop out of all short-term longs immediately.

Housing Starts Dive, as builders run out of materials at reasonable prices. It gave the Dow Average a punch in the nose worth $220. Single family homes took the big hit, down 13.4% to 1.08 million. Permits are still up 70% YOY from when Covid completely shut the industry down. This is the most inflationary sector of the economy right now but barely registers in the CPI numbers. Prices must go even higher for frustrated buyers which are accelerating their rate of increase. Builders are including contingency clauses that allow price rises after the sale, a first. The South has dominated in starts where the population is moving and took the biggest hit. Buy (LEN), (KBH), and (PHM) on dips.

Existing Home Sales Drop 2.7%, in April to 5.85 million units. Inventories are down 20% YOY to only an unimaginable two-month supply. There’s nothing for sale. With the strongest YOY price gains in history, there is nothing for sale. It’s all about high prices, high prices, high prices. Homes over $1 million are up an incredible 214% YOY. The 70-year migration from North to South continues, costing democrats 5 seats in the House. Millennials are entering their peak home-buying years and that $150,000 four-bedroom home in Savannah, GA doesn’t look so bad.

Bitcoin is the Most Crowded State in the World, according to a survey of investment managers. That may explain the 35% plunge in cryptocurrency since April. Is this the end of the Ponzi scheme? Technology and ESG stocks are the second and third most over-owned, which may explain their recent flaccid performance.

Why is the Gold Hedge Working this Time? The Barbarous relic is finally giving investors the insurance and the downside hedge they need, after failing to do so during the last correction in February. That’s because interest rates were spiking in the winter but aren’t now. Interest rates are the enemy of all no-yielding assets, like precious metals.

Fed Hints of Early Rate Rise, trashing both stocks and bonds. The big one could be here, a complete collapse of the US Treasury bond market. I’m already running the biggest (TLT) shorts ever. We should fall from the current $135 to $120 by yearend. Sell all (TLT) rallies.

Lumber Futures Collapse by 40%. There goes your inflation. Now if only Biden will end the Trump-era import duty on Canadian lumber. It gives a big boost to the “transitory” camp, arguing that this is just a one or two-month spike spawned by the cover recovery. Soaring lumber prices had been a key factor igniting new home prices.

Applied Materials Knocks the Cover off the Ball, reporting blowout earnings. The semiconductors equipment maker has been the best performing chip-related stock of 2021, up 72%. (AMAT) sees a structural chip shortage lasting for years. DRAMs are speeding up, while NAN is slowing down. Customers are placing orders years in advance for the first time ever. A new $7.5 billion stock buyback plan and 9% dividend increase were announced. Buy (AMAT) on the dips.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch profit reached 7.48% gain so far in May on the heels of a spectacular 15.67% profit in April. That leaves me 50% invested and 50% cash. We actually have a shot at reaching a double-digit performance for the seventh month in a row.

My 2021 year-to-date performance soared to 67.24%. The Dow Average is up 11.79% so far in 2021.

We got another major meltdown last week followed by an immediate recovery. I used the dip to reinitiate new positions in the (TLT), Goldman Sachs (GS), and Berkshire Hathaway (BRKB) to replace ones that expired on the Friday options expiration.

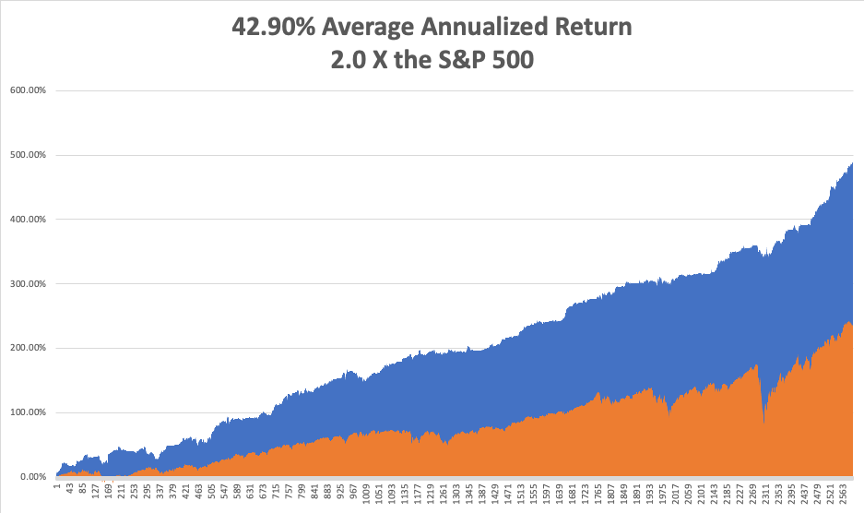

That brings my 11-year total return to 489.79%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 42.90%, easily the highest in the industry.

My trailing one-year return exploded to positively eye-popping 124.92%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 33.1 million and deaths topping 590,000, which you can find here. Some 33.1 million Americans have contracted Covid-19.

The coming week will be a weak one on the data front.

On Monday, May 24, at 8:30 AM, the Chicago Fed National Activity Index is released.

On Tuesday, May 25, at 10:00 AM, the S&P Case Shiller National Home Price Index for March is announced.

On Wednesday, May 26 at 8:30 PM, MBA Mortgage Applications are revealed.

On Thursday, May 27 at 8:30 AM, the Weekly Jobless Claims are Published. We also get a second estimate for the red hot Q2 GDP.

On Friday, May 28 at 8:30 AM, the even hotter Personal Spending for April is disclosed. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, as this pandemic winds down, I am reminded of a previous one in which I played a role in ending.

After a 30-year effort, the World Health organization was on the verge of wiping out smallpox, a scourge that had been ravaging the human race since its beginning. I have seen Egyptian mummies at the Museum of Cairo that showed the scarring that is the telltale evidence of smallpox, which is fatal in 50% of cases.

By the early 1970s, the dread disease was almost gone but still remained in some of the most remote parts of the world. So, they offered a reward to anyone who could find live cases.

To join the American Bicentennial Mt. Everest Expedition in 1976, I took a bus to the eastern edge of Katmandu and started walking. That was the furthest roads went in those days. It was only 150 miles to basecamp and a climb of 14,000 feet.

Some 100 miles in, I was hiking through a remote village, which was a page out of the 14th century, back when families threw buckets of sewage into the street. The trail was lined with mud brick two-story homes with wood shingle roofs, with the second story overhanging the first.

As I entered the town, every child ran to their windows to wave, as visitors were so rare. Every smiling face was covered with healing but still bleeding smallpox sores. I was immune, since I received my childhood vaccination, but I kept walking.

Two months later, I returned to Katmandu and wrote to the WHO headquarters in Geneva about the location of the outbreak. A year later, I received a letter of thanks at my California address and a check for $100 telling me they had sent in a team to my valley in Nepal and vaccinated the entire population.

Some 15 years later, while on customer calls in Geneva for Morgan Stanley, I stopped by the WHO to visit a scientist I went to school with. It turned out I had become quite famous, as my smallpox cases in Nepal were the last ever discovered.

The WHO certified the world free of smallpox in 1980. The US stopped vaccinating children for smallpox in 1972, as the risks outweighed the reward.

Today, smallpox samples only exist at the CDC in Atlanta frozen in liquid nitrogen at minus 346 degrees Fahrenheit in a high-security level 5 biohazard storage facility. China and Russia probably have the same.

That’s because scientists fear that terrorists might dig up the bodies of some British sailors who were known to have died of smallpox in the 19th century and were buried on the north coast of Greenland remaining frozen ever since. If you need a new smallpox vaccine, you have to start from somewhere.

As for me, I am now part of the 34% of Americans who remain immune to the disease. I’m glad I could play my own small part in ending it.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

On Mt. Everest, Smallpox-Free in 1976

Bitcoin

Global Market Comments

May 17, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or WHY HISTORY RHYMES),

(TLT), (SPY), (FCX), (MSFT), (DAL), (QQQ), (VIX), (DAL), (UUP)

The 19th century humorist and writer, Mark Twain, said, “History never repeats itself, but it rhymes.” This is certainly one of those rhyming times.

Remember back in 2011 when the Dow hit a short-term peak at $12,300 in May of 2011? The Cassandras had a heyday. The bull market was over, stocks were imminently going to crash, and the next stop for the Dow was $3,000. Gold and bonds were the only safe places.

Those who drank the Kool-Aid missed the greatest investment opportunity of the century and are now driving for Uber cars to earn their crust of bread. Those who drank the Kool-Aid twice sold their homes as well ahead of the greatest real estate boom of all time.

Not that a correction wasn’t sorely needed, we needed to scare money out of what I call the “super liquidity” investments like Bitcoin, SPACS, and tech companies selling at 100 times sales with failing business models.

We also needed to put the fear of god into newbie day traders by teaching them that stocks go down as well as up. We’ve already made good progress on this front. With many of the “meme” stocks down by half or more since February, we are already making good progress on that front.

What will power the Dow to my now very prescient looking $40,000 target by yearend? The unwind of the 40-year-old bull market in bonds has barely just begun. Ten-year US Treasury bond yields ($TNX) have only appreciated from 0.32% to 1.68%, compared to 5.6% at the last 2007 peak. That means there are still many tens of trillions of dollars to shift out of bonds (TLT) and INTO STOCKS!

Once the current correction ends, money will pour back into the recent leaders, the economic cyclicals, including financials, commodities, industrials, and commodities.

Technology will stay in the penalty box for the foreseeable future until they become under-owned and cheap again. The good news here is that tech earnings are growing at such a prolific rate that the sector is losing two price earnings multiple points a month and will return to the bargain basement in the not-too-distant future.

The long term view here is that you want to rent growth, but own tech, which still has double the growth rate of everything else.

It all makes my 2021 $40,000 Dow Average target look like a piece of cake, and my 2030 goal of $120,000 positively conservative, cautious, and circumspect.

Notice that our 2,000 point-swan dive in the Dow last week lasted only three days, and then delivered the sharpest fall in the Volatility Index (VIX) in history, from $29 to $19 in only 24 hours. The writing is still on the wall. People want to BUY.

Inflation explodes, with the Consumer Price Index posting a ballistic 4.2% YOY rate, the fastest gain since 2009. The Fed believes this is a temporary surge, the markets not so much. Bonds take it on the nose. Keep selling rallies in the (TLT). We’re making a fortune here.

Volatility Index (VIX) soars to $29, almost doubling in a week. Call me when it tops $30. That’s the usual signal for a short-term stock market bottom. I’m relaxed because I’m going into this with 80% cash and have just made a huge fortune on bond shorts.

Value and cyclicals are still the Big Play. That was the message of the stock market on Friday’s wild day which saw an 11-basis point trading range in the ten-year US treasury bond. If you think the next big move in rates is up, then Cyclicals will roar, and techs will fade.

It’s all about buying what people are underweight and selling what they are overweight. I’m looking for cyclicals that have recently corrected. Stay tuned to this station.

US Inventories see solid gains as retailers load the boat for the biggest economic recovery of all time. March was up 1.3%. One of an endless series of data points pointing to the best business conditions in a century.

The Home Buying Frenzy continues, with the median price for a single-family home soaring by 16.2% to $319,200 in Q1, according to the National Association of Realtors. Record high prices are hitting all markets. The perfect upside storm continues.

Weekly Jobless Claims come in at 473,000, a new post-Covid low. Continuing claims fall to 3,655,000. The greatest economic recovery of all time continues.

Producer Prices leap in April, up 0.6% following a 1% gain in March. It is a natural follow-on from the hot CPI. The PPI tracks changes in production costs, and supply bottlenecks and shortages tied to the pandemic recovery have caused commodity prices to soar. Temporary or continuing, that is the big debate. Watch the bond market for clues.

Stanley Druckenmiller says Bonds are Toast, and The Dollar is Worse. I couldn’t agree more with my old friend and trading counterparty. Current Fed policies are now the most extreme in history and threaten the reserve status of the US dollar. Sell all rallies in the (TLT) and the (UUP).

My Ten Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch profit reached 3.83% gain so far in May on the heels of a spectacular 15.67% profit in April. That leaves me 30% invested and 70% cash.

My 2021 year-to-date performance soared to 63.59%. The Dow Average is up 13.47% so far in 2021.

During the stock market meltdown, my hedges with shorts in the S&P 500 (SPY), NASDAQ (QQQ), and the United States Treasury Bond Fund (TLT) performed spectacularly well, leaving me up on the week. I managed to limit myself to only two stop losses, in Microsoft (MSFT) and Delta Airlines (DAL).

While everyone else was running around like chickens with their heads cut off, I was as relaxed as ever. Our worst case for May is that we will be only up single digits, instead of the double-digit gains of the past six months. That is not a bad “worst case” to have.

That brings my 11-year total return to 486.14%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 42.45%, easily the highest in the industry.

My trailing one-year return exploded to positively eye-popping 127.09%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 33 million and deaths topping 586,000, which you can find here.

The coming week will be a weak one on the data front.

On Monday, May 17, at 9:45 AM, the New York Empire State Manufacturing Index for May will be out

On Tuesday, May 18, at 10:00 AM, the Housing Starts for April are announced.

On Wednesday, May 19 at 2:00 PM, Minutes from the last Federal Reserve FOMC Meeting are published.

On Thursday, May 20 at 8:30 AM, the Weekly Jobless Claims are published.

On Friday, May 21 at 10:00 AM, Existing Homes Sales for April are announced. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, we had a big 4.7 earthquake at Lake Tahoe last week. The healthy live trees vibrated and swayed. But all of the brittle dead trees killed by pine beetles during the draught snapped at the base and fell over.

Those blocked all the fire roads, so every emergency and public service organization on the lake was called up and sent up into the mountains with chain saws. That included me, a member of Lake Tahoe Search and Rescue.

I hiked up to 9,000 feet with a 50-pound load and went to work. We cut these enormous 100-foot conifers into one-foot rounds and then rolled them off the road. Everyone else on the job was under 40.

After a day of heavy lifting, I hiked down the mountain and collapsed into bed. I slept for 12 hours, which is why the Monday letter was late. They say 70 is the new 40. I am the proof of that.

So can 100 be the new 60? One can only hope.

How was your weekend?

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

20 Year Chart of Ten Year US Treasury Yields