Mad Hedge Technology Letter

June 17, 2020

Fiat Lux

Featured Trade:

(WHY VEEVA HAS MORE TO RUN),

(VEEV), (CRM)

Mad Hedge Technology Letter

June 17, 2020

Fiat Lux

Featured Trade:

(WHY VEEVA HAS MORE TO RUN),

(VEEV), (CRM)

I am going to revisit a call I made last October 2019 on a tech stock that has outperformed mightily this year, and for good reasons.

There isn’t a tech stock more relevant today than Veeva Systems (VEEVA) because of the wave of health spending transcending the world.

Find me a country that is spending less on healthcare today!

I recommended this stock last October and the shares keep climbing over itself to reach all-time highs over and over again.

The one-sentence answer to why buy this stock is that Veeva’s latest earnings showed quarterly total revenue growing 37.7% year-over-year and EPS surging 32% year-over-year.

If I stopped here, that would most likely be enough to convince readers about this spectacular company.

Read on to understand more about this health cloud upstart positioned at the intersection of healthcare and cloud technology.

Veeva provides cloud-based CRM, data storage, and analytics services for life science and pharmaceutical companies.

It was co-founded by the former senior VP of technology at Salesforce, and its services are seamlessly integrated into Salesforce's platforms.

Veeva's tools help companies keep track of customer relationships, clinical trials, government regulations, prescribing habits, and other data in real-time.

I guess you could call it the Salesforce of cloud healthcare.

It enjoys a first-mover's advantage in the space and services an all-star lineup of top pharmaceutical companies like GSK and Novartis.

The first-mover advantage is critical because Microsoft announced a copycat version of Veeva’s services just a month ago.

To read about Microsoft heading into the health cloud business, click here.

Demand for Veeva's services has surged over the past few years, thanks to vicious competition between drugmakers and the need for real-time data.

The health crisis will also generate tailwinds for Veeva as leading drugmakers scramble to develop treatments and vaccines.

The company hasn’t been quiet, rolling out new products this year.

In May 2020, the company announced MyVeeva for clinical trials.

It is software built to enable clinical research sites to interact remotely with their patients easing the burden on in-clinic visits.

In March 2020, the company commercially launched Veeva Data Cloud, a robust technology platform constructed for the development and delivery of large-scale patient data and analytics.

The coronavirus is the catalyst that is forcing our healthcare industry to digitize rapidly and modernize.

The data backs up this trend.

The healthcare IT Market is forecasted to be valued at $511.06 Billion by 2027, growing at a CAGR of 13.8%.

To read more about this trend, click here.

Veeva analytics showed us that monthly doctor visits were halved in February compared to April before the widespread lockdown.

Teleconference doctor calls have skyrocketed increasing 30% year-over-year in April, compared with less than 1% in February.

Remote meetings between pharmaceutical companies and doctors increased more than 30 times and email communications doubled from February to April.

Veeva's management wholeheartedly believes it will reach its goal of generating $3 billion in revenue by 2025.

Their goals are impressive with an expectation of year-over-year growth rate of 26% at the midpoint.

Veeva loves to overdeliver, and if one thing is clear from the Q1 scorecard, health cloud computing services are more critical than ever to the life sciences and healthcare industries.

The company also has a pristine balance sheet with $1.38 billion in cash and short-term investments (nearly three years of cash operating expenses at the Q1 run rate) and zero debt.

Moving forward, I firmly believe that Veeva Systems will fetch a growing premium to the overall market.

The stock has zoomed from the March lows of $133 and is now trading at a robust $223 and the path of least resistance is up.

Mad Hedge Technology Letter

March 6, 2020

Fiat Lux

Featured Trade:

(HERE’S A BIG TECH CORONA PLAY)

(NUAN), (VEEV)

I love the cloud, and the health cloud is the ultimate coronavirus equalizer.

I am also on record saying that the 2 cloud sub-sectors that will be lights out in 2020 are the health cloud and network security cloud.

I believe Veeva Systems (VEEV) is one example of a cloud play that many long-term investors need to add before it gets too expensive.

I have another health cloud play for you up my sleeve as well.

While many investors were lamenting the coronavirus meltdown in tech shares, the same cannot be said for Nuance Communications, Inc. (NUAN), who seek to transform patient care with AI‑powered solutions for physicians, radiologists, and hospitals.

This company has famed scientist Ray Kurzweil's fingerprints all over it.

In 1974, Raymond Kurzweil founded Kurzweil Computer Products, Inc. to develop the first omni-font optical character-recognition system – a computer program capable of recognizing text written in any normal font.

In 1980, Kurzweil sold this company to Xerox, later becoming known as Xerox Imaging Systems (XIS), and later ScanSoft which merged with Nuance in 2005.

Healthcare is a focus for the company who on their webpage describes their mission as a company that “empowers organizations to unlock value and meaning in the millions of interactions that happen every day.”

They also provide their A.I. services to other industries such as financial, transportation, telecommunications, and government.

Their crown jewel is the Nuance Dragon Medical One cloud-based platform and it just expanded its access to France, Belgium, and the Netherlands.

Integrated within the electronic health record (EHR), Dragon Medical One offers physicians the ability to capture a patient’s complete snapshot at the point of care in their own local language – reducing administrative workloads while improving documentation quality and care.

Nuance delivers intelligent systems that aid a more natural and insightful approach to clinical documentation, freeing clinicians to spend more time caring for patients.

Nuance healthcare solutions enhance and communicate more than 300 million patient stories each year, helping more than 500,000 clinicians in 10,000 global healthcare organizations to drive meaningful clinical and financial outcomes.

Nuance’s award-winning clinical speech recognition, medical transcription, CDI, coding, quality, and medical imaging solutions offer a unique end-product to medical professionals and patients.

Its intelligent voice technology helps physicians produce clinical documentation up to 45% and capture up to 20% more relevant data using personalized A.I. tools.

Clinicians simply open the application, select the section of documentation, and start speaking to update the EHR.

Doctors recognized a dramatic improvement in clinic letter turnaround times since integrating with the Dragon Medical One platform describing the process as efficient and improving overall patient experience.

Nuance has accelerated the adoption of the electronic paper records system maximizing resources by forcing medical records to go entirely digital.

The demand for AI-powered documentation solutions worldwide is agnostic to location - physicians face the same headaches of administrative workloads and have the same dire need for tools that help them focus on providing the best possible care to their patients.

This unique platform addresses care quality while maximizing patient satisfaction and minimizing workload and burnout pressures on providers worldwide.

As an integral healthcare cloud play for the short- and long-term future, the coronavirus should have benign impact on its business.

We could ever say that the outbreak could galvanize healthier long-term demand trends for Nuance.

The pandemic acts as almost a non-stop commercial to the next generation technology needs in healthcare in which Nuance plays into with its top-level health cloud tools.

Investors have agreed with my idea that this is the year of the health cloud and Nuance shares are up 20% since the introduction of the coronavirus.

If readers want to be part of the future, pick up a few shares of Nuance Communications.

Mad Hedge Technology Letter

November 20, 2019

Fiat Lux

Featured Trade:

(MY CURRENT TECHNOLOGY TRADING STRATEGY),

(GOOGL), (MSFT), (APPL), (ADBE), (AKAM), (VEEV), (FTNT), (WKDAY), (TTD)

Some might say that we were due for a revaluation of growth tech stocks.

They have contributed greatly in this nine-year bull market.

Profit-generating software stocks are the order of the day.

Tech has led the overall market higher after projected quarterly earnings growth of -9% came in better than expected at -5%.

We have ebbed and flowed from pricing in a full-out recession in mid-2020 to now believing a recession is further off than first thought.

The pendulum swing ruptured many growth stocks from Workday (WKDAY) to The Trade Desk, Inc. (TTD) plummeting 30%.

We have retraced some of those losses but momentum in share appreciation has shifted to the perceived safer variation of tech stocks.

Investors have cut volatility and headed into bulletproof companies of Apple (AAPL), Google (GOOGL), and Microsoft (MSFT).

These companies have significant competitive advantages, Teflon balance sheets, and print money.

The tech markets just about priced in the U.S - China trade war in the fall as broad-based volatility plummeted because of optimism around making a deal.

This, in turn, has boosted chips stocks along with investors front running the 5G revolution and the administration granting Huawei a reprieve was a cherry on top.

The Mad Hedge Technology Letter has taken every dip to initiate new longs in safe trades like software companies Adobe (ADBE) and Veeva Systems (VEEV).

Tech is at the point that all loss-making companies are out of the running for tech alerts because the moment there is a recession scare, these shares drop 10% and often don’t stop until they lose 30%.

Now there is a deeply embedded set of narrow tech leadership by a few dominant tech companies buttressed by a select set of second-tier software stocks.

I would put PayPal (PYPL) and Twitter (TWTR), which I currently have open trades on, in the ranks of the second tier and they should do well as long as economic growth does better than expected.

Their share prices dipped on weak guidance and the bad news appears to have been shaken out of these names.

Professional investors could also be hanging on to meet end-of-year performance targets.

I do expect unique entry points on software stocks that drop after bad future guidance.

Profitability has moved to the fore as the biggest factor in holding a name or not.

Newly minted IPOs have fared even worse showing the markets' waning appetite for loss makers like Uber (UBER) and Lyft (LYFT).

Loss-making companies often tout their ability to change the world and disrupt industry, but that has been discovered as nothing more than a ruse.

They aren’t disrupting the way we change the world. For example, Uber is a dressed-up taxi service and the new CEO has failed to create any new momentum in the unit economics that spectacularly fail by any type of metric.

Even worse for these growth stocks, as the economy starts to falter, there will be even less appetite for them, and even more appetite for safer tech stocks.

A worst-case scenario would see Uber drop to $10 and Lyft to $20.

New all-time highs have crystalized with Google (GOOGL) under the gauntlet of regulation hysteria displaying the domination of these big tech machines.

The ongoing, consistent rotation out of growth and into value hasn’t run its course yet and fortunately, by identifying this important trend, our readers will be well placed to advantageously position themselves going into 2020.

Growth stocks won’t make a comeback anytime soon and deteriorating conditions could trigger renewed synchronized global monetary policy easing and central bank stimulus.

And yes, more negative rates.

I believe Oracle (ORCL), Fortinet (FTNT), Akamai Technologies, Inc. (AKAM) could weather the storm next year.

Tech growth is slowing and trade uncertainty is high, and readers must have a sense of urgency to avoid the losers in this scenario.

U.S. economic growth could slow to 1.3% next year, avoiding a recession, and the lack of enterprise spend will reduce software sales and combine that with peak smartphone growth and it won’t be smooth sailing.

The Mad Hedge Technology Letter has the pulse of the tech market and will show you how to navigate this minefield.

Mad Hedge Technology Letter

August 30, 2019

Fiat Lux

Featured Trade:

(DIVING BACK INTO VEEVA SYSTEMS)

(VEEVA)

A tech company that I won’t hesitate to pull the trigger on new trade alerts is Veeva Systems (VEEVA).

The most recent results illustrate how investors can never discount strong cloud companies even if the elevated levels of risk scare many people out of making committed investments.

Q2 was another strong quarter with total revenue of $267 million, up 27% year-over-year.

Subscription revenue grew 28% year-over-year, and non-GAAP operating margin was 39%.

Veeva has now passed the $1 billion revenue run rate.

This is 1.5 years ahead of the target first laid out in 2015, an influential contributor to this success has been customer satisfaction.

Strong momentum in Commercial Cloud contributed to outperformance in Q2.

In core customer relationship management (CRM), Veeva continues to extend its leadership position with new small and medium business (SMB) customers and additional enterprise expansions.

Customers continue to adopt more CRM add-ons. This happens on a product-by-product and region-by-region basis.

I’ll offer a few pertinent examples.

Veeva CRM Engage had one of its strongest quarters as 4 top 20 pharmas expanded their use of Engage to new field teams.

Customers are attracted by the deep functionality and multi-platform support of Engage and the tight integration with CRM.

Veeva notched some important design wins at the top 20 pharma for Events Management.

A current customer has been using core CRM globally for many years and recently decided to expand their Veeva relationship to include Events Management in more than 90 countries over time.

They chose Veeva because of the deep functionality and professional services capabilities needed for global events management rollout.

They will replace multiple custom systems and spreadsheets leading to a more efficient and compliant global process.

This type of commitment to Veeva’s products is a positive sign as it tries to retain a more long-standing customer.

Who else does Veeva Systems work with?

They recently signed their 10th top 20 Pharma for Vault QualityDocs. Following their success with Vault PromoMats, eTMF and Submissions.

The pharma customers selected QualityDocs as part of their move away from the legacy content management platform.

What is Veeva QualityDocs?

It is software that provides superior ease-of-use and seamless collaboration, Vault QualityDocs reduces compliance risk and improves quality processes.

It accelerates review and approval workflows and facilitates sharing of GxP documents among employees and partners.

The dire need for modernization is driving the move to Veeva in this area as is the benefit of having QMS integrated with QualityDocs and Training on the Vault platform.

This is another great example of the innovation Veeva captures from an underserved market.

There has also been meaningful progress in 3 targeted industries: consumer packaged goods (CPG), chemicals, and cosmetics.

Since announcing the new Vault Claims product last quarter, Veeva now has projects in place at 3 top CPG companies.

Veeva is also making similar inroads in chemicals and cosmetics industries.

In total, Veeva now has major business at a top 20 CPG, a top 20 cosmetics company and 2 major chemical companies.

And this is just the beginning.

I’ll continue to bet on this stock going up.

It’s the best health tech cloud play out there, no reason not to love the direction of the company.

Mad Hedge Technology Letter

February 19, 2019

Fiat Lux

Featured Trade:

(THE SAFE PLACE TO HIDE IN TECH),

(CSCO), (ORCL), (WDAY), (ZEN), (HUBS), (NOW), (PYPL), (VEEV), (TWLO)

Great quarter by Cisco (CSCO).

That was the first thought in my head when perusing their quarterly earnings.

It’s been hit or miss for tech companies lately and at the end of 2018, I stood up and told readers to double down on software companies and specifically enterprise software companies.

Well, Cisco has skin in this software game because corporations cultivating software need the best type of network infrastructure money can buy.

Cisco is the foundational hardware on what current high-end software is built on.

It is all rosy to have a spectacular roof design, but without a solid foundation, we have nothing more than a house of cards.

The great part about Cisco is that they are immune to the software battle taking place inside of industries because they do not build the enterprise software that is built on top of the Cisco infrastructure.

We have seen our fair share of software companies go sideways such as Oracle (ORCL) who have presided over a stale patchwork of database system software created last gen.

However, on the other side of the coin, my prediction of enterprise software companies leading tech has been spot on.

Zendesk (ZEN), HubSpot (HUBS), ServiceNow (NOW), Workday (WDAY), PayPal (PYPL), Salesforce (CRM), Veeva Systems (VEEV), and Twilio (TWLO) are software companies that I was incredibly bullish on as we turned the calendar year and they have not disappointed with nearly all of these names flirting with all-time highs.

All these software companies need Cisco.

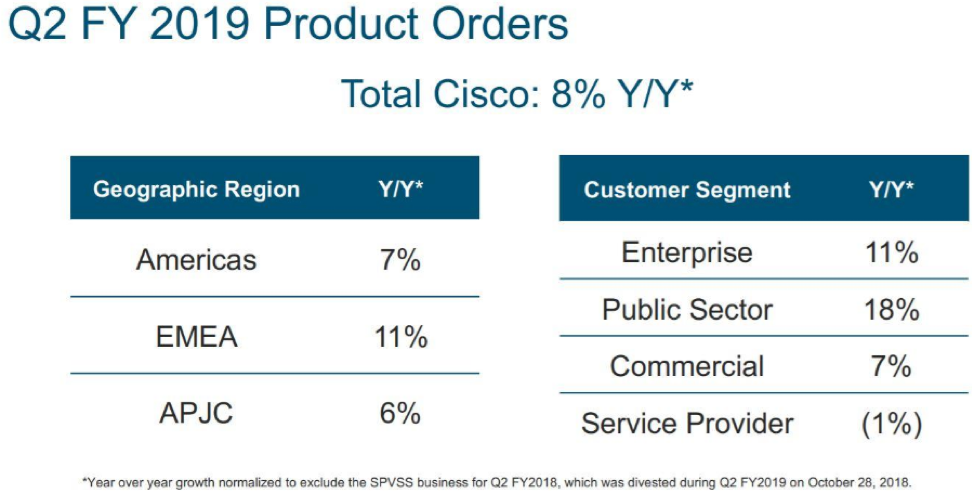

What stood out for me was that public sector orders grew 18% last quarter signaling that not only are the private corporations snapping up Cisco products, but governments are embedding their offices with Cisco’s Internet Protocol-based networking and other products related to the communications and information technology industry.

And if you wanted a general tech stock to capture the migration from analog commerce to digital and stay out of the high stakes online media segment, this would be the stable name that would check all the boxes.

And if you thought this was just a domestic story, once again, the scope is wider with Europe, the Middle East and Africa (EMEA) sales expanding by 11% which eclipsed America sales by 4%.

The only blip on the radar was service revenue slipping by 1% to $3.17 billion, but I do not view that as a pattern of sequential deceleration and pricing mechanisms can be altered to relaunch growth.

If you thought that Cisco doesn’t sell any software – you are wrong.

The software they do sell applies to operating the proprietary hardware that they produce.

Cisco’s wide competitive advantage stems from the industries toweringly high barriers of entry and that they make great products relative to other players.

The infrastructure software that liaises brilliantly with its hardware is succinctly named Cisco ONE Software.

This software suite is molded to face the most relevant use cases in the data center, WAN, and access edge.

CEO of Cisco Chuck Robbins characterized the current geopolitical and overall economic landscape as “complex” but experienced “zero difference” in Chinese revenue giving the company a quarterly victory in the Middle Kingdom.

China’s economy is decelerating faster than we can understand. The latest details of ride-hailing leader Didi sacking 2,000 employees is a warning flare to the rest that open wounds are appearing in the economy and are becoming harder to conceal.

And for Cisco to do a quarter with no significant Chinese downdraft is a good sign that the company can handle the upcoming recession in 2020.

As a sign of further strength, Cisco raised its dividend and boosted stock buybacks which are all the trappings of what great companies do.

Cisco already made $5 billion of repurchases last quarter which was on top of the $6 billion they bought in October 2018.

This method of financial engineering helps put a solid floor under the stock delighting investors and ignites the share price.

And the capital allocation encore means that Cisco will pile $15 billion into its buyback program with this fresh authorization, and the company is forecasted to produce at least $15 billion in free cash flow over the next year.

Cisco’s balance sheet is glistening and even has options to adventure into meaningful M&A if they see something that catches their eye without any real hit to the balance sheet.

These multiple tailwinds in a precarious economic point in the cycle have investors aware that there are worse options out there to invest capital than tech thoroughbred Cisco.

And if you thought the one variable that could turn this earnings report from good to bad was expenses and margins, well, Cisco covered their bases on that one too.

Margins came within the forecasted guidance with gross margins slightly trending down by 1% to 64.1%.

Expenses were reigned in and management saw a small nudge up of 3% causing investors to take a deep sigh of relief.

Cisco is in a superior strategic spot to most tech companies and is a staunch participant of the migration to digital.

Buy shares on the dip.