Mad Hedge Biotech & Healthcare Letter

April 13, 2021

Fiat Lux

FEATURED TRADE:

(MEGA CAP PHARMA UP FOR GRABS)

(MRK), (ABMD), (ILMN), (ALGN), (JNJ), (GILD), (PAND), (ALKS), (IMV)

Mad Hedge Biotech & Healthcare Letter

April 13, 2021

Fiat Lux

FEATURED TRADE:

(MEGA CAP PHARMA UP FOR GRABS)

(MRK), (ABMD), (ILMN), (ALGN), (JNJ), (GILD), (PAND), (ALKS), (IMV)

Since the great 2007 financial crisis, many companies have been coping to recapture their former glory. The healthcare industry is not spared of this struggle.

This makes the continuous growth of Merck (MRK) all the more impressive, with the company reaching $195 billion in market capitalization and sustaining its rise for over 130 years.

Curiously, Merck’s share price is still in the mid-$70s.

Meanwhile, other large-cap biopharmaceutical companies that offer similar products and services are trading higher.

For instance, the share price for Abiomed (ABMD) is over $330 while Illumina (ILMN) is nearly $400, and Align Technology (ALGN) is at a whopping $600.

Like Merck, investors gravitate towards Abiomed, Illumina, and Align because of their capacity to generate long-term sustainable revenues and boost earnings.

Notably, though, none of them hold the same depth or even breadth of products and services that Merck offers.

Recently, Merck disclosed some of its initiatives to boost the company’s earnings in the near- and long term.

One of the most visible efforts is its collaboration with Johnson & Johnson (JNJ) to help with the manufacturing of JNJ-78436735, in which Merck received federal funding.

While JNJ is one of the biggest healthcare companies across the globe, with a market capitalization of roughly $425 billion, joining forces with Merck will substantially boost its vaccine manufacturing capacity.

For context, JNJ’s goal prior to Merck’s help is to deliver 100 million doses by the end of the second quarter of 2021.

With Merck’s assistance, JNJ can now realistically manufacture up to 3 billion doses in 2022 alone.

This means that JNJ can implement a massive vaccination drive in the next two years since its manufacturing capacity ensures that it can deliver shots to over one-third of the population.

This is obviously good news for everyone as it means that the virus will be contained, but the enhanced manufacturing capacity also means profit accretion for both JNJ and Merck.

This partnership with JNJ is possibly a key factor in Merck’s move to invest heavily in the vaccine business.

Merck recently announced its plans to allocate $20 billion to expand its global vaccine manufacturing network from 2021 to 2024. This would mean an annual investment of $5 billion.

Part of this global vaccine plan is Merck’s acquisition of Pandion Therapeutics (PAND) in 2020.

Another recent initiative of the company is its joint effort with Gilead Sciences (GILD) to develop long-lasting HIV treatments.

Gilead will be in charge of the US market, while Merck will handle the EU and the rest of the international markets.

For starters, the companies will focus on a combination of Merck’s Islatravir and Gilead’s Lenacapavir to create a long-lasting and well-tolerate HIV treatment.

Outside these partnerships, Merck has been working on strengthening its oncology segment.

In fact, its top-selling drug, Keytruda, can be used to medicate an extensive range of indications, which include colorectal, esophageal, and even lung cancers.

At this point, Keytruda is generating north of $16 billion in sales every year and exhibiting roughly 30% growth annually.

Since the drug continues to gain approvals for additional indications, it looks like its growth runway is definitely far from over.

Keytruda is poised to reach $24 billion in annual sales in a few years’ time, which puts it on track to become the best-selling drug in the world by 2023.

Although Keytruda will be under patent protection until 2028, Merck remains active in expanding its oncology pipeline.

By then, Merck is projected to have multiple immunotherapy staples in its portfolio not only derived from its own R&D but also via partnerships like its 2020 collaboration with Alkermes (ALKS) to work on an ovarian cancer study and Immunovaccine (IMV) to cooperate on a blood cancer study.

The total oncology market is estimated to be $200 billion annually, with over 30 million cases projected to be added by 2040.

Overall, Merck is a well-oiled company that continues to deliver good results thanks to strategic acquisitions and partnerships neatly tied up together in a particular domain.

While its rival biotechnology and pharmaceutical companies become hot properties in the market and pose higher price tags, Merck silently moves forward in the shadows of sustainability and familiarity.

Mad Hedge Biotech & Healthcare Letter

April 8, 2021

Fiat Lux

FEATURED TRADE:

(A LOW-KEY POST-COVID-19 RECOVERY STOCK)

(REGN), (MRNA), (NVAX), (BNTX) (PFE), (VIR), (LLY), (RHHBY), (NVS)

If you still remember the news about the flash recovery from COVID-19 of then-President Trump during the campaign period last year, then you know that the express cure was not delivered by any of the vaccine makers that were all the rage at the time like Moderna (MRNA), Novavax (NVAX), BioNTech (BNTX), or even Pfizer (PFE).

Instead, the cure was credited to a lesser-known cocktail of antibodies, called REGEN-COV, developed by Regeneron (REGN).

Recently, the same treatment was used in Germany in response to the shortage of COVID-19 vaccines and the demand for alternatives.

Despite the promising results and the highly publicized effects of Regeneron’s treatment, the company’s share price still hasn’t shown any meaningful upside.

Nonetheless, Regeneron still secured some agreements for REGEN-COV.

Based on the June 2020 agreement of Regeneron with the US government, the company expects to sell $260 million worth of REGEN-COV in the first quarter of 2021 for a fixed number of orders.

For the second quarter of 2021, though, the two parties set different terms for their deal.

Under these new terms, the US government will pay per dose regardless of REGEN-COV’s dose size.

Given the latest numbers from Regeneron’s trials, this could mean lower costs for the company.

Data from the clinical trials showed that REGEN-COV had the same effectiveness at the lower 1,200 mg dosage compared to the currently approved amount by the US FDA, which is 2,400 mg.

In fact, Regeneron’s treatment is reported to be as effective as the COVID-19 antibody therapies developed by Vir Biotechnology (VIR) and even Eli Lilly’s (LLY) candidate.

Looking at the positive results from Regeneron’s Phase 3 trials for REGEN-COV, it’s reasonable to expect higher sales than previously estimated.

Now, Regeneron shared that it aims to supply 1.25 million doses of the COVID-19 antibody therapy at the lower but equally effective 1,200 mg dose level.

If the FDA agrees to this emergency use authorization request, then Regeneron will be able to supply twice the number of COVID-19 doses.

If it delivers these doses by June 30, the US government will buy them for $2.6 billion regardless of the dosage used.

On average, Regeneron is expected to generate roughly $2.9 billion in sales for its COVID-19 antibody treatment.

Meanwhile, if REGEN-COV gains full FDA approval and gets marketed commercially, then the treatment can rake in at least $3.5 billion and peak at $5 billion this year alone.

Outside its COVID-19 program, Regeneron actually recorded better-than-expected results last year despite the pandemic ravishing the economy.

For example, there was a rebound in demand for its top-selling Eylea, with sales of the wet age-related macular degeneration (AMD) drug rising by 10% in the fourth quarter of 2020 to reach a total of $1.34 billion.

Bolstering the dominance of Eylea in the AMD market and to combat emerging competitors like Roche (RHHBY) with Faricimab and Novartis (NVS) with Beovu, Regeneron is looking to expand the drug’s application to cover more age groups.

Meanwhile, another bestseller, Dupixent, reached $1.17 billion in sales last year.

This is an impressive climb for the atopic dermatitis medication, which was developed with Sanofi (SNY), since it only recorded $751.5 million in the same period in 2019.

That indicates roughly 75% growth, with over a million prescriptions written for Dupixent in the US alone.

However, only 6% of those eligible patients have been treated with Regeneron’s product thus far.

This means that Dupixent has a lot of room to grow, with this drug estimated to reach peak sales at $12.5 billion.

Needless to say, Dupixent is quickly transforming into a blockbuster treatment.

Since its approval for eczema in 2017, this drug has expanded its indication to cover moderate-to-severe atopic dermatitis not only among teens but also children. Notably, Dupixent holds a monopoly for this application to children.

Another revenue stream for Regeneron is its oncology sector led by Libtayo.

In 2020, net sales of this skin cancer treatment reached $348 million, showing an impressive 80% growth.

To date, Regeneron has at least 12 oncology treatments under clinical development.

In terms of the bottom line, Regeneron exceeded the expectations of $8.38 and reported adjusted earnings per share of $9.53 instead.

As vaccine rollouts continue to be a priority, it’s safe to say that the worst of the COVID-19 is just about in sight.

Consequently, investors are now looking into recovery and stocks that appear to be good buys when the coronavirus eventually becomes a thing of the past.

Regeneron is one of the attractive buys so far. While it has been underperforming in the past weeks, its business actually looks to be in great shape even if the pandemic goes on for longer.

Mad Hedge Biotech & Healthcare Letter

May 12, 2020

Fiat Lux

Featured Trade:

(GLAXOSMITHKLINE’S ENTRY INTO THE COVID-19 VACCINE RACE)

(GSK), (VIR), (AZN)

It’s all-hands-on-deck for the biotech sector as the world battles the deadly coronavirus disease COVID-19.

As the US coronavirus-related deaths mount to over 80,000 and reported cases hitting over 1.3 million, the need to find a cure and vaccines increases in urgency every passing minute.

Joining the biotech companies throwing their hats into the ring is GlaxoSmithKline (GSK), which recently announced its decision to work hand in hand with Vir Biotechnology (VIR) in the search for a coronavirus cure.

On top of the collaboration efforts, the partnership will also involve GSK investing $250 million in Vir. According to these terms, each Vir share will be worth $37.73.

The collaboration announcement also pushed Vir shares to rise by as much as 34% and trading more than doubled. Meanwhile, (GSK) went up by roughly 2%.

The partnership will explore several platforms to come up with a treatment for COVID-19.

So far, the most promising candidates involve two antibodies presently dubbed as VIR-7831 and VIR-7832. Both were developed by Vir as treatments for SARS, which is also caused by a coronavirus.

Actually, these antibodies were developed using samples from a patient who recovered from SARS. However, these could also be produced artificially.

(GSK) and Vir estimate that Phase 2 clinical trials will commence in three to five months.

Apart from these antibody treatments, the two companies are also looking into utilizing CRISPR screening technology to figure out which proteins are used by the coronavirus to infect the healthy cells.

Once they identify these, (GSK) and Vir could come up with drugs that block viral infection. That is, they can use the information to create a vaccine to be used not only for COVID-19 but also for other types of coronaviruses.

According to (GSK), the Vir proteins had been identified as “highly potent” when targeted at the coronavirus in the laboratory.

If all goes well, a coronavirus vaccine could be on its way in 12 to 18 months.

Aside from (GSK), Vir also has an ongoing collaboration with another bigwig biotech, Biogen (BIIB).

This isn’t the first venture of (GSK) in looking for a COVID-19 cure though.

The British biotech giant is also working with China’s Xiamen Innovex on another potential coronavirus vaccine.

In addition, (GSK) is looking into forming a joint laboratory with AstraZeneca (AZN) to assist the UK government in stretching and expanding its supplies for COVID-19 diagnostic tests.

Although diagnostics are not part of their primary efforts, the goal is for the two big biotechs to determine the best ways to help in detecting the spread of COVID-19.

While these efforts to help find a solution to the pandemic are at the forefront of the biotech world today, GSK has a lot more to offer.

(GSK) manufactures products that people need to take on a regular basis.

The need is so great that the company actually allocates 80% of its research efforts focused on drug development for various issues like oncology, immuno-inflammation, and HIV. These treatments are vital to the daily existence of so many patients across the globe.

Meanwhile, (GSK) also aims to streamline its business and focus on the research and development of products and services. Hence, it decided to split its businesses into two.

One will be geared towards pharmaceutical efforts. The second will be focused on consumer health.

This is an excellent move in ensuring that (GSK) maximizes its potential to dominate its chosen markets.

Throughout the years, (GSK) has demonstrated its capacity to grow while delivering a strong bottom line. From 2015 until 2019, the biotech giant’s sales increased by over 40% with its operating margin rising as well.

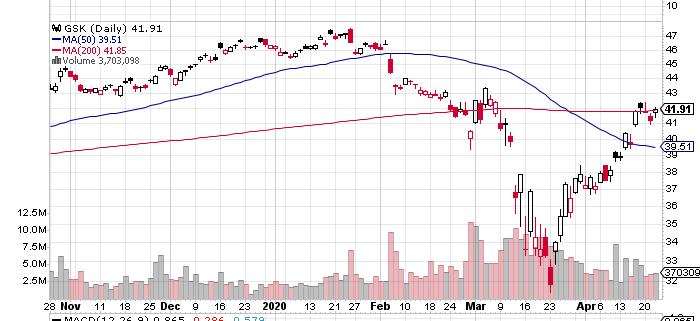

While it’s undeniable that this global biotech stock has gotten itself caught up in the COVID-19 whirlwind that managed to hurt virtually every sector, its downside alternative makes absolutely no sense.

No one has the ability to predict and control when they get sick or what type of illness they get afflicted with, which makes the biotech sector and specifically drug developers particularly safe bet whatever the financial climate is.

So, investors looking for a stable stock can now afford to buy (GSK) shares at approximately 10 times worth of next year’s per-share profit potential. As if that’s not enough, the company also offers a mouthwatering 7.5% dividend yield.

Keep in mind that a wise way to insulate your portfolio amid the fears of a market crash is through investing in stable businesses that offer products and services needed on a daily basis.

If the companies provide essential items in both good and bad times, it’s a good sign the stocks will be able to survive any market crash.

(GSK), which is currently at an 11-year low due to the pandemic and economic crisis, is worth considering.

![]()

Mad Hedge Biotech & Healthcare Letter

April 28, 2020

Fiat Lux

Featured Trade:

(THE FIVE FRONTRUNNERS IN THE RACE FOR A COVID-19 VACCINE)

(GSK), (SNY), (REGN), (TBIO), (VIR)

We’re finally pulling out the big guns.

Almost five months into this debilitating global pandemic, GlaxoSmithKline (GSK) and Sanofi (SNY) announced a collaboration to come up with a coronavirus disease (COVID-19) vaccine.

These vaccine heavy-hitters not only assured that the product would be ready by the second half of 2021 but also that they would be able to manufacture hundreds of millions of doses every year.

This is actually pretty impressive considering that the typical timeline for a vaccine takes at least a decade.

What we know so far is that Sanofi will conduct tests on its experimental vaccine using GSK’s adjuvants.

Adjuvants are added to improve the efficacy of some vaccines. These can also lower the amount of vaccine protein needed for every dose, boosting the likelihood of creating a shot that can be manufactured in large quantities.

According to GSK and Sanofi, human trials will begin in the second half of 2020.

GSK’s coronavirus adjuvant already demonstrated its value during the H1N1 influenza pandemic back in 2009 when this technology played a major role in the success of the Shingrix shingles vaccine.

As for Sanofi, the giant biotech company will be using a previously approved influenza vaccine for this joint effort.

GSK shares rose by 2% following the announcement while Sanofi got a 4.1% increase.

While both companies shared that they don’t really expect much profit from this COVID-19 vaccine, they plan to reinvest any short-term earnings in preparatory measures to better handle future pandemics.

Aside from this joint effort, GSK and Sanofi are also taking multiple shots in the hopes of solving this COVID-19 health crisis.

Sanofi is testing its malaria drug which contains hydroxychloroquine.

If you recall, this is the same drug that Donald Trump hailed as a “miracle” coronavirus cure earlier this year. Days following the president’s announcement, Sanofi offered to donate 100 million doses of hydroxychloroquine to 50 countries.

On top of that, Sanofi is also working with Regeneron (REGN) to assess whether its existing arthritis treatment Kevzara can work as a coronavirus medication.

It also has an ongoing collaboration with Translate Bio (TBIO) to come up with another COVID-19 vaccine using messenger RNA.

Outside its coronavirus efforts, Sanofi has been looking into streamlining the company’s focus to improve margins and shift into more lucrative growth areas. So far, so good.

One of the more drastic measures is eliminating diabetes and cardiovascular research sector of the company.

Funding for these was reallocated, with the acquisition of cancer and auto-immune biotechnology company Synthorx serving as a strong indication of the direction the company plans to take.

Apart from growing its immuno-oncology department, Sanofi is also betting on eczema treatment Dupixent -- a move that saw them rewarded almost immediately.

The company’s recent earnings report showed that Dupixent sales jumped 135% in the fourth quarter of 2019, with annual sales soaring to an impressive $2.3 billion. This indicates a 152% increase from the year prior.

Riding this momentum, Sanofi received FDA approval to expand the use of multiple myeloma drug Sarclisa in April.

This marks another significant win for the company.

Multiple myeloma ranks second in the list of most common blood cancer types, with the disease affecting roughly 32,000 Americans annually. It cannot be cured as well, which means that treatments are needed throughout the patients’ lives.

Needless to say, Sanofi has several platforms to contribute to finding the cure and even a vaccine for COVID-19. More importantly, the company has managed to transform itself into a more streamlined and innovative business.

Sanofi would be a wise choice for investors interested in a stock to hold for the long term. This company doesn’t only hold a starring role in the search for a coronavirus vaccine but also offers more opportunities beyond the current pandemic.

Meanwhile, GSK is also not limiting its adjuvant technology to Sanofi but to other companies developing COVID-19 vaccines as well. The list includes Vir Biotechnology (VIR) and even Chinese biotech company Clover Biopharmaceuticals.

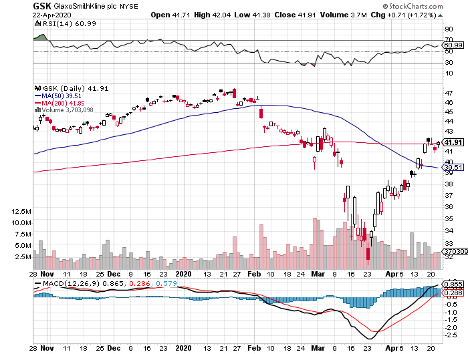

Despite its active participation in the coronavirus vaccine race, GSK tumbled down to over its 10-year low in March.

Although the pandemic’s negative impact looks discouraging, I think the overreaction is good news for value and dividend traders as the stock now trades at bargain-bin valuations.

Hence, investors could enjoy GSK’s lucrative 5.8% dividend at relatively cheap costs.

It also doesn’t hurt that GSK offers a diversified portfolio that all but guarantees minimal losses for its investors.

Its biggest revenue driver is the pharmaceutical arm of the business, which raked in total revenue of roughly $21.68 billion in 2019.

GSK’s vaccine segment contributed 8.87 billion while the consumer healthcare sector brought in over 11 billion.

Although smaller than its pharmaceutical arm, both segments are quickly catching up to GSK’s biggest moneymaker. In fact, its vaccine segment recorded revenue growth of 21% while its consumer healthcare arm jumped by 17%.

Overall, GSK is a compelling addition to any investor’s portfolio. Its impressive dividend combined with its diversified business makes this biotechnology company a wise choice as well.

The collaboration of GSK and Sanofi is considered as the most significant and promising COVID-19 vaccine effort to date.

This partnership not only maximizes the expertise of the two leading vaccine makers in the world but take advantage of their manufacturing capacity as well, which is a critical concern given that a COVID-19 vaccine would have to be distributed to millions, if not billions, of individuals across the globe.

Mad Hedge Biotech & Healthcare Letter

April 28, 2020

Fiat Lux

Featured Trade:

(THE FIVE FRONTRUNNERS IN THE RACE FOR A COVID-19 VACCINE)

(GSK), (SNY), (REGN), (TBIO), (VIR)

We’re finally pulling out the big guns.

Almost five months into this debilitating global pandemic, GlaxoSmithKline (GSK) and Sanofi (SNY) announced a collaboration to come up with a coronavirus disease (COVID-19) vaccine.

These vaccine heavy-hitters not only assured that the product would be ready by the second half of 2021 but also that they would be able to manufacture hundreds of millions of doses every year.

This is actually pretty impressive considering that the typical timeline for a vaccine takes at least a decade.

What we know so far is that Sanofi will conduct tests on its experimental vaccine using GSK’s adjuvants.

Adjuvants are added to improve the efficacy of some vaccines. These can also lower the amount of vaccine protein needed for every dose, boosting the likelihood of creating a shot that can be manufactured in large quantities.

According to GSK and Sanofi, human trials will begin in the second half of 2020.

GSK’s coronavirus adjuvant already demonstrated its value during the H1N1 influenza pandemic back in 2009 when this technology played a major role in the success of the Shingrix shingles vaccine.

As for Sanofi, the giant biotech company will be using a previously approved influenza vaccine for this joint effort.

GSK shares rose by 2% following the announcement while Sanofi got a 4.1% increase.

While both companies shared that they don’t really expect much profit from this COVID-19 vaccine, they plan to reinvest any short-term earnings in preparatory measures to better handle future pandemics.

Aside from this joint effort, GSK and Sanofi are also taking multiple shots in the hopes of solving this COVID-19 health crisis.

Sanofi is testing its malaria drug which contains hydroxychloroquine.

If you recall, this is the same drug that Donald Trump hailed as a “miracle” coronavirus cure earlier this year. Days following the president’s announcement, Sanofi offered to donate 100 million doses of hydroxychloroquine to 50 countries.

On top of that, Sanofi is also working with Regeneron (REGN) to assess whether its existing arthritis treatment Kevzara can work as a coronavirus medication.

It also has an ongoing collaboration with Translate Bio (TBIO) to come up with another COVID-19 vaccine using messenger RNA.

Outside its coronavirus efforts, Sanofi has been looking into streamlining the company’s focus to improve margins and shift into more lucrative growth areas. So far, so good.

One of the more drastic measures is eliminating diabetes and cardiovascular research sector of the company.

Funding for these was reallocated, with the acquisition of cancer and auto-immune biotechnology company Synthorx serving as a strong indication of the direction the company plans to take.

Apart from growing its immuno-oncology department, Sanofi is also betting on eczema treatment Dupixent -- a move that saw them rewarded almost immediately.

The company’s recent earnings report showed that Dupixent sales jumped 135% in the fourth quarter of 2019, with annual sales soaring to an impressive $2.3 billion. This indicates a 152% increase from the year prior.

Riding this momentum, Sanofi received FDA approval to expand the use of multiple myeloma drug Sarclisa in April.

This marks another significant win for the company.

Multiple myeloma ranks second in the list of most common blood cancer types, with the disease affecting roughly 32,000 Americans annually. It cannot be cured as well, which means that treatments are needed throughout the patients’ lives.

Needless to say, Sanofi has several platforms to contribute to finding the cure and even a vaccine for COVID-19. More importantly, the company has managed to transform itself into a more streamlined and innovative business.

Sanofi would be a wise choice for investors interested in a stock to hold for the long term. This company doesn’t only hold a starring role in the search for a coronavirus vaccine but also offers more opportunities beyond the current pandemic.

Meanwhile, GSK is also not limiting its adjuvant technology to Sanofi but to other companies developing COVID-19 vaccines as well. The list includes Vir Biotechnology (VIR) and even Chinese biotech company Clover Biopharmaceuticals.

Despite its active participation in the coronavirus vaccine race, GSK tumbled down to over its 10-year low in March.

Although the pandemic’s negative impact looks discouraging, I think the overreaction is good news for value and dividend traders as the stock now trades at bargain-bin valuations.

Hence, investors could enjoy GSK’s lucrative 5.8% dividend at relatively cheap costs.

It also doesn’t hurt that GSK offers a diversified portfolio that all but guarantees minimal losses for its investors.

Its biggest revenue driver is the pharmaceutical arm of the business, which raked in total revenue of roughly $21.68 billion in 2019.

GSK’s vaccine segment contributed 8.87 billion while the consumer healthcare sector brought in over 11 billion.

Although smaller than its pharmaceutical arm, both segments are quickly catching up to GSK’s biggest moneymaker. In fact, its vaccine segment recorded revenue growth of 21% while its consumer healthcare arm jumped by 17%.

Overall, GSK is a compelling addition to any investor’s portfolio. Its impressive dividend combined with its diversified business makes this biotechnology company a wise choice as well.

The collaboration of GSK and Sanofi is considered as the most significant and promising COVID-19 vaccine effort to date.

This partnership not only maximizes the expertise of the two leading vaccine makers in the world but takes advantage of their manufacturing capacity as well, which is a critical concern given that a COVID-19 vaccine would have to be distributed to millions, if not billions, of individuals across the globe.

Mad Hedge Biotech & Healthcare Letter

April 3, 2020

Fiat Lux

Featured Trade:

(THE BIOGEN PARTNERSHIP THAT MAY SAVE YOUR LIFE)

(BIIB, (VIR)