We have now rocketed all the back from -37% to a feeble 0% return for the Dow Average for 2018. By comparison, the Mad Hedge Fund Trader is up a nosebleed 8.5% during the same period.

If you had taken Cunard’s round-the-world cruise four months ago, as I recommended, you would be landing in New York about now, wondering what the big deal was. Indexes are nearly unchanged since you departed, with the Dow only 5.50% short of an all-time high.

This truly has been the Teflon market. Nothing will stick to it. Not, plague, not depression, not mass bankruptcies, not the worst economic data in history.

Go figure.

It makes you want to throw your hands up in despair and your empty beer can at the TV set. All this work and I’m delivered the perfectly wrong conclusions?

Let me point out a few harsh lessons learned from this most recent meltdown and the rip-your-face-off rally that followed.

Remember all those market gurus claiming stocks would rise every day for the rest of the year? They were wrong.

This is why almost every Trade Alert I shot out for the past two months has been from the “RISK ON” side, but only after cataclysmic market selloffs.

We have just moved from a “Buy in November” to a “Sell in May” posture.

The next six months are ones of historical seasonal market weakness. For the misty origins of this trend, read “If You Sell in May, What to Do in April?” On top of that, we have the uncertainty of the presidential election to deal with.

We go into this with big tech leaders, including Facebook (FB), Apple (AAPL), Amazon (AMZN), Google (GOOG), and Microsoft (MSFT), all at or close to all-time highs.

The other lesson learned this year was the utter uselessness of technical analyses. Usually, these guys are right only 50% of the time. This year, they missed the boat entirely. After perfectly buying the last top, they begged you to dump shares at the bottom.

When the S&P 500 (SPY) was meandering in a narrow nine-point range, and the Volatility Index (VIX) hugged the $11-$15 neighborhood, they said this would continue for the rest of the year.

It didn’t.

When the market finally broke down in February, cutting through imaginary support levels like a hot knife through butter ($26,000? $25,000? $24,500?), they said the market would plunge to $24,000, and possibly as low as $22,000.

It didn’t do that either.

If you believed their hogwash, you lost your shirt. The market just kept going, and going, and going down to $18,000.

This is why technical analysis is utterly useless as an investment strategy. How many hedge funds use a pure technical strategy? Absolutely none, as it doesn’t make any money on a stand-alone basis.

At best, it is just one of 100 tools you need to trade the market effectively. The shorter the time frame, the more accurate it becomes.

On an intraday basis, technical analysis is actually quite useful. But I doubt a few of you engage in this hopeless persuasion.

This is why I advise portfolio managers and financial advisors to use technical analysis as a means of timing order executions, and nothing more.

Most professionals agree with me.

Technical analysis derives from humans’ preference for looking at pictures instead of engaging in abstract mental processes. A picture is worth 1,000 words, and probably a lot more.

This is why technical analysis appeals to so many young people entering the market for the first time. Buy a book for $5 on Amazon and you can become a Master of the Universe.

Who can resist that?

The problem is that high-frequency traders also bought that same book from Amazon a long time ago and have designed algorithms to frustrate every move of the technical analyst.

Sorry to be the buzzkill, but that is my take on technical analysis.

Hope you enjoyed your cruise.

https://www.madhedgefundtrader.com/wp-content/uploads/2016/05/John-in-Owners-Suite.jpg404398DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2020-06-11 09:04:172020-06-11 09:13:25Why Technical Analysis Doesn't Work

We are getting some tantalizing tastes of the new America that will soon arise from the wreckage of the pandemic.

Companies are evolving their business models at an astonishing rate, digitizing what’s left and abandoning the rest, and taking a meat cleaver to costs.

The corporate America that makes it through to the other side of the Great Depression will earn far more money on far fewer sales. That has been the pattern of every recession for the past 100 years.

While the pandemic may take earnings down from $162 per S&P 500 share in 2019 to only $50 in 2020, it sets up a run at a staggering $500 a share during the coming Roaring Twenties and Golden Age. All surprises will be to the upside and anything you touch will make you look like a genius.

For example, Target’s online sales have exploded 153%, allowing customers to order their groceries online and pick them up at curbside. (TGT) pulled this off in a mere three weeks. Without a pandemic, it would have taken three years to implement such a radical idea, if ever.

Survival is a great motivator.

The (SPY) has been greatly exaggerating the public’s understanding of the stock market. Five FANGs and Tesla (TSLA) with 50%-200% moves off the bottom have made the index look irrationally strong.

The fact is that the majority who have shares have not even made a 50% retracement of this year’s losses. A lot of stocks, especially the reopening ones, are still crawling back of subterranean bottoms.

Investors now have the choice of chasing wildly expensive stocks that have already had spectacular runs, or cheap ones that will go bankrupt by the end of the year. It is a Hobson’s choice for the ages. I expect 10% of the S&P 500 to go under by the end of 2020.

I am spending a lot of time on the ground talking to businesses in California and Nevada and have come to two conclusions. They cannot fathom the true depth of the Depression we are now in and are greatly underestimating the length of time it may take to recover. We may not see the headline unemployment rate under 10% for years unless the government redefines the statistics, which they always do.

The S&P 500 is not the economy. It only employs 25% of America’s private sector labor force accounting for 20% of its total costs. Real estate accounts for another 15%. That leaves 35% of costs that can be completely eliminated or reengineered. This creates enormous share price upside possibilities.

The concentration of the market is the most extreme I have ever seen, with five stocks getting most of the action, (FB), (AAPL), (NFLX), (GOOGL), and (MSFT).

There is a staggering $3.6 trillion in equity allocations sitting on the sidelines in cash. All those who got out at the March bottom are now desperately trying to get back in at the May top. Algorithms are making sure you get out cheap and get back expensive.

It will all end in tears.

One of the stunning developments of the crash has been the near doubling of retail stock trading. Options trading has increased even more. Millions of stimulus check recipients have poured their newfound wealth into the stock market instead of spending it on consumer goods, like they were supposed to.

This explains the over-concentration on the five FANG stocks, (FB), (AAPL), (NFLX), (GOOGL), and (MSFT), the greatest momentum stocks are out age, but in high speculative ones like Tesla (TSLA). The lowest cost online platforms like Robin Hood (click here).

All of this is completely irrevocably changing the character of the stock market, perhaps permanently. This may also explain why the Volatility Index remains stuck above$26.

Fed Governor Jerome Powell said no recovery without vaccine, and that’s without a second wave. It could be a long wait. In the meantime, the Atlanta Fed said Q2 US GDP will be down -42%, the weakest quarter in American history. We find out mid-July.

Housing Starts collapsed by 30.2% in April, in the sharpest drop on record. But prices aren’t falling. There is still a massive bid under the market from still-employed millennials. Your home could be you best performing asset this year. The 30-year fixed rate mortgage at 3.0% is a big help.

Weekly Jobless Claims topped 2.4 million, taking the two-month total to a breathtaking 39 million. One out of four Americans is now unemployed, matching the Great Depression peak. US deaths just topped 98,000, 21 times China’s fatality rate where the disease originated and with four times our population. People will keep losing jobs until the death rate peaks, which could be many months, or years.

Leading Economic Indicators crashed by 4.4% for April, showing the economy is still in free fall. So, how much more stock do you want to buy here?

Up to 60% of mall tenants aren’t paying rent, with $7.4 billion skipped in April alone. See my earlier “Death of the Mall” piece. It’s another harsh example of the epidemic accelerating all existing trends.

The market is not reflecting the long-term damage to the economy, says my old buddy and Morgan Stanley colleague David Gerstenhaber. When the bailouts run out, the economy could go into free fall. It could take years to get below 10% unemployment rate again, as many of the layoffs and furloughs are permanent. Keep positions small. Anything could happen. I spent the 1987 crash with David.

Existing Home Sales cratered an incredible 17.8% in April to an annualized 4.88 million units, the largest one-month drop since 2010. Inventory dropped to an all-time low of only 1.7 million, down 19.7%, presenting a 4.1-month supply. Sellers failed to list and those who had a home took them off. Unbelievably, this pushed median home prices to a new all-time high of 286,000, up 7.4% YOY. The biggest sales fall in the west, where the US epidemic started.

China took over Hong Kong, suspending most civil liberties in response to Trump’s multiple attacks. And you know what? There is nothing we can do about it that hasn’t already been done. Talk about going into battle with no dry powder. I’m sure the US 7th Fleet will be out there soon to provoke an attack. Anything to distract attention from the 100,000 Americans who died from Covid-19 on Trump’s watch. As if markets didn’t already have enough to worry about.

When we come out on the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates at zero, oil at $0 a barrel, and many stocks down by three quarters, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade.

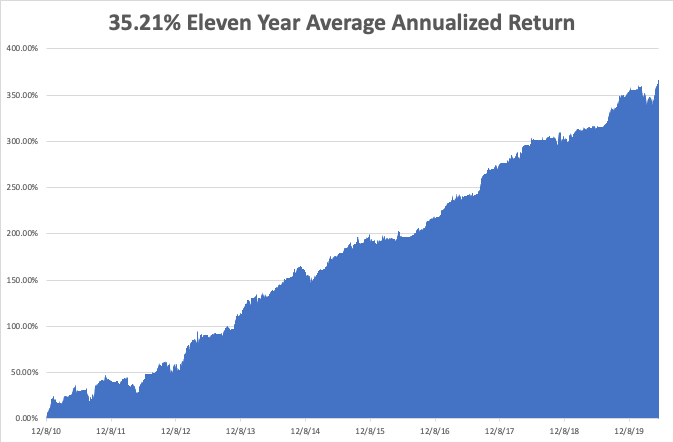

My Global Trading Dispatch performance had another fabulous week, up an awesome +4.97%, and blasting us up to a new eleven-year all-time high of 77%. It has been one of the most heroic performance comebacks of all time.

My aggressive short bond positions really delivered some nice profits, despite the fact the bond market went almost nowhere. That’s because time decay for the June 19 expiration is really starting to kick in. I also got away with a small long in the bond market for the second time in two weeks.

That takes my 2020 YTD return up to +10.86%. That compares to a loss for the Dow Average of -12.6%. My trailing one-year return exploded to 50.85%, nearly an all-time high. My eleven-year average annualized profit exploded to +35.21%.

The only numbers that count for the market are the number of US Coronavirus cases and deaths, which you can find here at https://coronavirus.jhu.edu.

On Monday, May 25, I’ll be leading the neighborhood veterans parade for Memorial Day. Markets are closed.

On Tuesday, May 26 at 9:00 AM, the S&P Case Shiller National Home Price Index is released.

On Wednesday, May 27, at 4:30 PM, weekly EIA Crude Oil Stocks are published.

On Thursday, May 28 at 8:30 AM, Weekly Jobless Claims are announced. We also get the second estimate for the Q1 GDP is printed. At 10:00 AM, April Pending Home Sales are announced.

On Friday, May 29, at 2:00 PM, the Baker Hughes Rig Count follows at 2:00 PM.

As for me, I will be hitting the town beaches at Lake Tahoe for the first time this spring, mask in hand, where waitresses serve you mixed drinks on order. Outdoors will be the only safe place this year.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2020/05/john-thomas-beach.png419315Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-05-26 09:02:102025-05-15 11:41:31Market Outlook for the Week Ahead, or Looking for the New America

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader May 20Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Do you believe chairman Powell when he says no negative rates?

A: I do believe that he does not want negative rates—that would be hugely detrimental to the economy. Europe and Japan have been trying them for the last ten years and they absolutely do not work. When it costs something to deposit money in the bank, people take it out of the financial system and hide it under their mattresses or buy gold (GLD). Although Powell doesn’t want negative rates, he may not have a choice; the market’s already taking them there in the futures market one year out. If we do get a big second wave of corona in the fall, and we do go to new lows in the stock market, and unemployment goes to new highs, negative rates will happen on their own whether Powell wants them or not.

Q: What is your best metric for determining when this bounce is over?

A: We passed those metrics on when a normal bounce is over weeks and weeks ago, and it just keeps going up. If you’ll notice, I have no stocks right now. I have some balanced long and short stock indexes but that’s it. My big trade is short bonds. When an asset class is no longer attractive, avoid it like Covid-19.

Q: What range should I wait for to buy the Proshares Ultra Short S&P 500 ETF (SDS)?

A: I’m really only using (SDS) as a hedge to limit the risk on much bigger long positions that I may have. (SDS) doesn’t lend itself to normal technical analysis because it is an artificial construct.

Q: What price to get into Tesla (TSLA)?

A: If you look at the Tesla chart, it's almost exactly the same as all of the other FANGS, as it’s essentially becoming the next FANG. So, they will trade with the FANGS for that reason, at least in the short term. Don’t buy it here, wait for the next major selloff to $600 or so. We actually had a bunch of concierge customers to buy long term leaps under $500 dollars in March, and they got 500% returns in 3 weeks.

Q: Why didn’t we just buy the ProShares Ultra Technology ETF (ROM) and go to sleep for five years?

A: If you recall, I was actually recommending just that in March when (ROM) was trading in the $80s, and we actually had a (ROM) position that we got stopped out of. The (ROM) is the 2x long technology ETF that's gone from $80 to $160 since the market bottomed almost 2 months ago.

Q: Why do you keep using deep in the money put spreads and call spreads?

A: You use them when volatility is very high like it is now—right now the Volatility Index (VIX) is at $28. The normal price is at $14 or $15, and we’ve just come down from $80. Even in the high $20s, you still get huge payoffs (like 10% a month) per call and put spread. As long as (VIX) is that high, we’ll keep doing them. They are also the perfect trade to have in range trading markets like we’ve had for the past month. They give you a nice extra kicker on your P&L.

Q: What is the worst-case scenario?

A: We get a second wave of the virus, another couple hundred thousand Americans die, the stock market goes to new lows, and we have a presidential election. How’s that for a worst-case scenario? Other than that, how is your day going?

Q: Do you trade pre and post market?

A: No; I used to when I ran my hedge fund, but I don’t do anything now if it’s beyond the capability of most individuals. I only want to put out trade alerts that people can get done. So, I'm only trading US hours. The reason you trade overseas is that you always get the highest highs and lowest lows in the Asian markets. During the late 1990s, I was the number one or two volume trader in the Singapore futures market.

Q: Do you think the 200-day moving average will be substantial resistance to the market?

A: I think absolutely yes, and I also believe that the only downside trigger for a major breakdown in the market is a second corona wave.

Q: If we get negative interest rates, would (SDS) fall?

A: No, (SDS) is a 2X bear (SPY) ETF that would go through the roof because negative rates would only happen if the stock market was collapsing. You might get a double on (SDS) on a second corona wave and negative interest rates. That’s why I’m keeping my position.

Q: Could the market just keep going up with no major pullbacks if the Fed keeps stimulating the economy?

A: Yes, and that’s what has been happening. Jerome Powell has said that the Fed’s ability to borrow is unlimited, therefore the amount of stimulus they can keep throwing is also unlimited, and if that’s what happens, all of that money will go into financial assets, even if the real economy is in utter freefall (which it has been). You can’t rule out anything these days. You always have to trade with the belief that anything can happen at any time.

Q: I need help setting up Long term Equity Participation Securities (LEAPS). Is there a video on that?

A: You can take all the educational videos we have on call spreads and put spreads, and everything applies exactly the same, except that instead of doing a one-month maturity, you do a two-year maturity. If you play around with the maturity tab on your platform, you can find the longest dated maturity on each option series. Sometimes, it’s only a year, sometimes all the way up to 2.5 years.

Q: Are there any other options besides the United States Treasury Bond Fund (TLT) to short the bond market?

A: Yes, there’s the ProShares Ultra Short 20 Year Treasury ETF (TBT); that’s a 2x short bond market ETF. But you don’t get anywhere near the leverage that we have in the (TLT) put options spreads.

Q: Do you expect a return in inflation with all the stimulus going on?

A: Absolutely yes; food prices have already increased 20%—that will be a big inflationary push. Another $14 trillion in government QE and spending hitting the economy is also highly inflationary. And a lot of the price cuts which fueled deflation are ending as global supply chains are cut and the US food distribution system breaks down.

Q: Is the Great Depression on the table?

A: We are in a Great Depression now that is already far worse than the last one, except that this one will be shorter than the decade seen in the 1930s.

Q: How long will it take for unemployment to recover to the December 2019 3.5% unemployment lows?

A: We will never get back to those lows. A lot of that was over employment (artificial employment), with a lot of temporary marginal workers being picked up. And the net effect of the epidemic will be to make businesses forcibly more efficient; that means getting a lot more done with a lot fewer workers. So, I don't think we’ll ever see that 3.5% rate again. Economists are predicting that the next new low in unemployment may be 5% or 6%, and even that could take 2 or 3 years to get there.

Q: Will the market soar on vaccine news?

A: Well probably not; I would bet that two-thirds of any real vaccines are already in the price. We are getting vaccine announcements every day and the market is immediately discounting it, so when we actually do get the real thing, we may get a rally of only a few days and that’s it. We also won’t know for many months if it is real and is moved to mass production.

Q: If you would buy one restaurant, what would it be?

A: None; I would not touch the restaurants here with a 10-foot pole. None of the restaurant chains have any prospect of making a profit, except for maybe the ones that already had takeout models like Subway or Chipotle Mexican Grill (CMG). Some hedge funds are buying Darden (DRI), but with their money, not mine.

Q: Should I double my short position in volatility (VIX)?

A: No, not down here, especially after a huge run in the stock market like we had—a 40% rise off the bottom. If we do get above $50 though, I will be shorting volatility then.

Q: I bought the (BOTZ) AI and robotics ETF, on your recommendation—it’s now almost double off the lows. What should I do with it now?

A: Short term, take profits, long term keep it. I think the (BOTZ) doubles again from these levels, and I know some of you out there bought LEAPS on the (BOTZ) at the lows and you’re up 1,000% on those. If you have a 1,000% profit take it, you probably won’t get another one in your lifetime.

Q: Time to refi the house?

A: No, I think refi rates are artificially high now (and totally out of line with the bond market) because the default rate is so high—8%. Once that default rate starts to drop, the interest rate on mortgages should also fall, and I think you could see 2.5% on the 30-year fixed rate mortgage. Europe has had 0% rates for almost 10 years, and their home mortgages are at 2%, so that’s ultimately how low we could go.

Q: Are you worried about the debt related to Crown Castle International (CCI)?

A: No because they’re putting all the debt to good use and they can always refi at lower rates. There is no question that the demand for cell phone towers is going to be enormous—epidemic or not, because of the roll-out of 5G phones.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2014/06/John-Thomas.jpg454350Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-05-21 13:04:522020-06-22 11:46:14May 20 Biweekly Strategy Webinar Q&A

We are all living the Bill Murray movie “Groundhog Day” over and over again. Every day seems to blend seamlessly into the next, ad infinitum.

I think it’s Monday, but I’m not sure. The stock market is open so that must mean it’s Monday to Friday. The trash goes out tomorrow, so it might be Tuesday. No, wait! CBS 60 Minutes was on last night, so it has to be Monday. Maybe.

When a Marine Corp 60mm mortar team zeros in on a target, it is said to be “bracketed.” No matter which way the enemy goes, he gets blown up.

The S&P 500 is now “bracketed”.

If it falls, the support of the free Fed put option kicks in to limit the damage via QE infinity. If the market tries to rally, it is capped by the worst economic data in history, last week joined by a new trade war with China.

Who is the enemy that gets destroyed in this military metaphor? Anyone betting on an imminent upside or downside breakout, especially those who are long the Volatility Index (VIX).

That means the thousands who follow the Mad Hedge Fund Trader have just been given a money-printing machine, a new rich uncle.

For every time the market rallies, you simply buy a vertical bear put option spread in the front month with strikes prices well outside the bracketed area as I did last week with (DIS). When it dives, you strap on vertical bull call spreads, as I did last week with the (DIS) and the (SPY). Then you laugh all the way to the bank.

We could be bracketed a long time. The early data from opening-up states is that consumers returning to stores only amounts to a ruinous 7% of pre-pandemic levels. That suggests the Unemployment Rate will soar to 30% or more before it peaks, exceeding the Great Depression apex. There are easily another 10 million that haven’t been counted yet because the state benefit processors are so slow.

However, as long as we are bracketed, I reckon I can make 10% a month, as I already have done from the Middle of April and in May.

It is not a riskless strategy.

The day an actual vaccine is announced, the market Dow Average could soar by 3,000 points in a day, wiping out the shorts. The White House has been declaring this on a daily basis. But until we get a vaccine the market believes, we will remain bracketed. That could take years, if ever.

Dr. Fauci triggered a 1,000-point market dive with his sobering analysis of the course of the pandemic in the coming months. Don’t count on going back to school in the fall.

No “V” for the economy, said the Fed. The job losses are a complete economic disaster that will take years to recover from. That’s the opinion of Minneapolis Federal Reserve Bank President Neel Kashkari. The president just said Corona deaths will reach 100,000. Buzzkill. Do you think the stock market will notice?

Fed funds futures are discounting negative interest rates in a year. They say they don’t want negative rates but may not have a choice. The markets may go there without them. The disruptions to the financial service will be enormous. Do you really want to pay the bank to deposit your hard-earned money?

Fed Governor Powell warns the worst is yet to come, and the need for more stimulus is paramount. However, negative interest rates which failed in Europe and Japan won’t work here either. The problem is rampant fear, not the overnight cost of funds.

Weekly Jobless Claims are still soaring, up 3 million on the week to 36.5 million. It’s going to get worse before it gets better. The Fed is targeting a peak of 36.5 million. Connecticut is the worst-performing state, California the best. Stan Druckenmiller says stocks are the most overvalued in his career, says my former client, one of the best traders in the market. My friend David Tepper says they’re the most expensive since 1999. It may be splitting hairs, but how much do you want to own here? Keep those shorts!

Another death knell for US Treasury bonds (TLT) as the April budget deficit soars to $738 billion. That is an $8.85 trillion annual rate. Overissuance is about to destroy deflation big time.

Retail Sales collapse by 16.4%, the worst on record in another Great Depressionary data release. The stock market is starting to lean towards a view that the economy will take years to recover, not months. I’m somewhere in the middle.

A new trade war with China heats up, with the president banning more export items, especially chips for telecom giant Huawei. I guess our economy isn’t bad enough. Knock another few thousand off the Dow.

When we come out on the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates at zero, oil at $0 a barrel, and many stocks down by three quarters, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade.

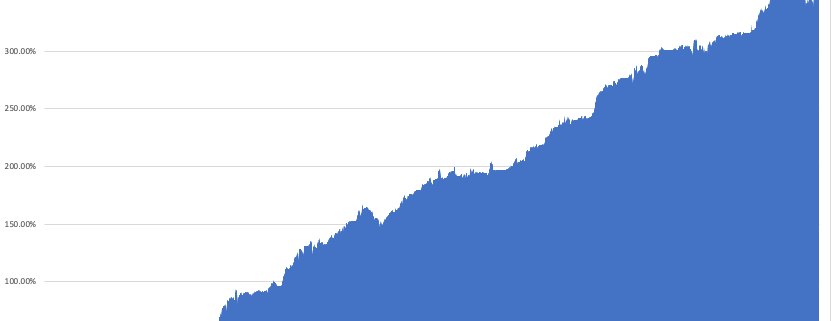

My Global Trading Dispatch performance had another fabulous week, up an awesome +11.26%, and blasting us up to a new eleven-year all-time high of 20%. It has been one of the most heroic performance comebacks of all time.

My aggressive short bond positions gave back some money on the ‘RISK OFF” posture for the week. However, we offset those losses and a lot more on longs in bonds and shorts in the (SPY) and Walt Disney (DIS).

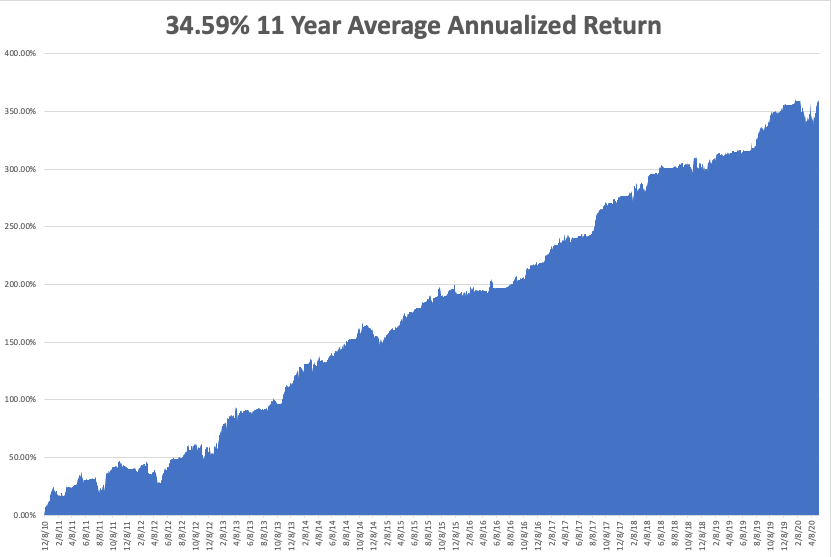

That takes my 2020 YTD return up to +7.29%. That compares to a loss for the Dow Average of -16.89%. My trailing one-year return exploded to 48.47%. My eleven-year average annualized profit returned to +34.59%.

The only numbers that count for the market are the number of US Coronavirus cases and deaths, which you can find here.

On Monday, May 18 at 10:00 AM, the NAHB Housing Market Index for May is released.

On Tuesday, May 19 at 8:30 AM, US Housing Starts for April are printed. Home Depot (HD) and Walmart (WMT) report.

On Wednesday, May 20, at 10:30 AM, weekly EIA Crude Oil Stocks are published. Target (TGT) and Lowes (LOW) report.

On Thursday, May 21 at 8:30 AM, Weekly Jobless Claims are announced. NVIDIA (NVDA) reports.

On Friday, May 22, the Baker Hughes Rig Count follows at 2:00 PM. Alibaba (BABA) reports.

As for me, I am headed back up to Incline Village, NV, a town completely free of Covid-19. The village is thinking of barring entry to all non-residents. Maybe it’s the fresh air.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2020/05/11yr-may18.png557831Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-05-18 10:02:192020-06-22 11:47:37The Market Outlook for the Week Ahead, or The Market is Bracketed

I always get my best ideas when hiking up a steep mountain carrying a heavy backpack.

Yesterday, I was just passing through the 9,000-foot level on the Tahoe Rim Trail when suddenly, the fog lifted and the skies cleared. I was hit with an epiphany.

It was my “AHA” moment.

The next American Golden Age, the next Roaring Twenties, started on March 23.

However, you have to dive deep into investor psychology to reach that astonishing conclusion.

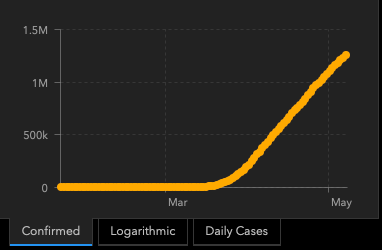

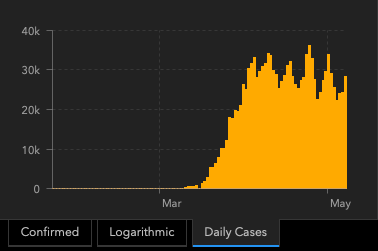

The conundrum of the day is why stocks are trading at a plus 30X multiple two months into a Great Depression. The economic data has been so horrific that the mainstream news has been reporting them.

Some 30 million unemployed on the way to 51 million? Those are Fed numbers, not mine (click here for the link ). Over 52% of small businesses going bankrupt in the next six months? A GDP that is shrinking at an amazing -40% annualized rate?

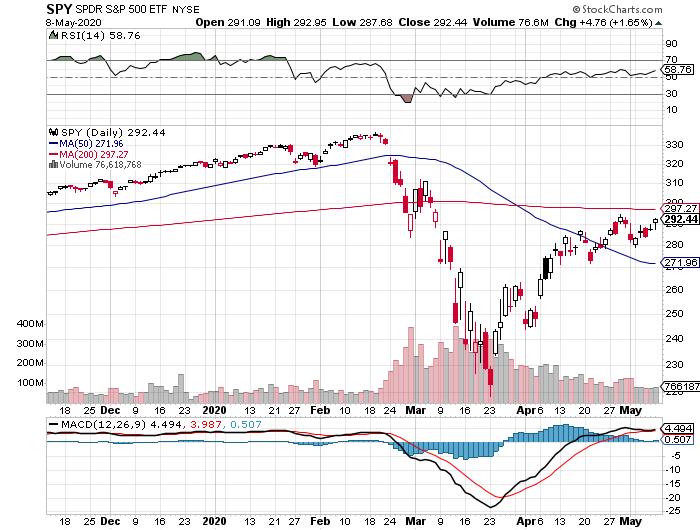

Yet, we have a Dow Average that has risen a breathtaking 38% in six weeks. The market has essentially dropped 38% and risen 38% over three months, with the Volatility Index (VIX) making a brief visit to the $80 handle.

To understand these massive contradictions, you have to understand what investors think they are buying. They are not hoovering up stocks that are cheap, offer value, or at the bottom of an economic cycle.

Instead, they are investing in a hope, a vision, an expectation that the coming decade will bring a major economic boom. Yes, they are buying my coming American Golden Age.

Only 10% of the value of a stock is reflected in current year earnings, according to Dr. Jeremy Siegal at the Wharton School of Economics (click here to go to the site). The other 90% is in the following nine years. Investors have written off this year’s earnings and are paying up for the following nine.

Long term followers of this newsletter are well aware of my approaching forecast of the next Roaring Twenties (click here for the link).

Except that this time we have a catapult, the pump-priming effects of the pandemic. The government has stepped in with $14 trillion worth of fiscal and monetary stimulus. Creative destruction is taking place at an exponential rate. Companies have to become hyper-efficient overnight or die.

It’s not rocket science. More than 85 million millennials are aging into their peak spending years, buying homes, cars, and all the luxuries of life. Every time this has happened for the past century, US economic growth leaped to 4%.

It happened in the 1920s, the 1960s, the 1990s, and is about to take place in the 2020s. And with each pop in growth, the stock market rises about 400%. Look at your long-term charts and you’ll see I’m dead right.

That takes us from the March 23 Dow Average low at 18,000 up to 72,000 by 2030, except that it’s a low number. Throw in the hyper-acceleration of innovation by the technology and biotech sectors, a Dow 120,000 is within reach.

You may recall that number from my marketing pitches, except that this time it’s happening. In a decade you are going to look like an absolute genius by following the recommendation of the Mad Hedge Fund Trader.

It also means that we may not see market corrections of any more than 10% this year. That would take us down to a Dow Average of 22,500, and an (SPX) of 2,600 in the coming months. That’s where you should jump in and buy with both hands. The only way I would be wrong is if the US epidemic explodes to unimaginable levels, which is not impossible.

Last week, U-6 unemployment rates exploding to a stratospheric 22.8%. The rate was far higher among high school graduates, but only 8% for college grads. Some 20.2 million lost jobs, ten times the previous record, and more than seen during the Great Depression. The BLS (click here) said the true figure was probably 5% higher due to counting anomalies and a huge backlog of data. And this is just the beginning. The good news is that next month, only 10 million jobs will be lost.

NASDAQ (QQQ) turned positive for 2020, and the followers who piled into tech LEAPS at the March bottom are eternally grateful. Tech and biotech are the only places to be. Everywhere else is a waste of time and money. The entire country is turning into a tech economy or going out of business. Buy tech on dips.

Warren Buffet sold all his airline shares, taking a major loss, including Delta (DAL), Southwest (LUV), American (AA) and United (UAL). The Fed’s $50 billion airline bailout blocked him from making a real killing. His Berkshire Hathaway (BRK/A) (click here) owned close to 10% of all of them. The complete collapse of tourism and business travel are the issues. He sees no recovery in the foreseeable future. They don’t call him the “Oracle of Omaha” for nothing.

US Auto Sales are down a mind-blowing -48% in April, the worst on record. Only 8.6 million cars were sold in the US against last year’s annual rate of 17 million. Toyota and Honda saw the biggest falls as their ships can’t unload due to lack of storage space.

The US Treasury will borrow $3 Trillion this Quarter to fund the massive bailout programs. Announced programs amount to 20 times the $789 billion 2009 rescue package, which Republicans opposed. I’m increasing my bond shorts. Sell short (TLT) again, even if we don’t get a decent rally. Oh, and Trump is threatening a default too. He doesn’t see the connection.

Bonds crashed on massive issuance, with the Treasury announcing a record 20-year bond floatation. Yields hit a one-month high. With the (TLT) down $18 from its recent high, I am taking profits on my bond shorts. I’ll be selling the next rally….again. This could be my core trade for the next decade.

Consumer Debt soared to $14.3 trillion in Q1, a new all-time high. A lot of people are living on their credit cards right now.

Trump threatens to cancel China trade deal, blaming them for Covid-19, sending stocks into a 400-point dive. The last time he did this, shares plunged 20%. It’s all part of an effort to divert attention from the administration’s disastrous handling of the pandemic. America’s Corona deaths are now 20 times China’s, and they are still an emerging nation. Just what we needed, a renewed trade war on top of a pandemic-caused Great Depression, as if the market needed more uncertainty. Sell rallies in the (SPY)

When we come out on the other side of this, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates at zero, oil at $0 a barrel, and many stocks down by three quarters, there will be no reason not to. The Dow Average will rise by 400% or more in the coming decade.

My Global Trading Dispatch performance had one of the best weeks in years again, up a gob-smacking +6.46%. We are now only 0.65% short of a new all-time high.

My aggressive short bond positions came in big time on the back of theannounced $3 trillion in new debt issuance in Q2. Short bonds are far and away the better quality trade of buying stocks at these elevated levels.

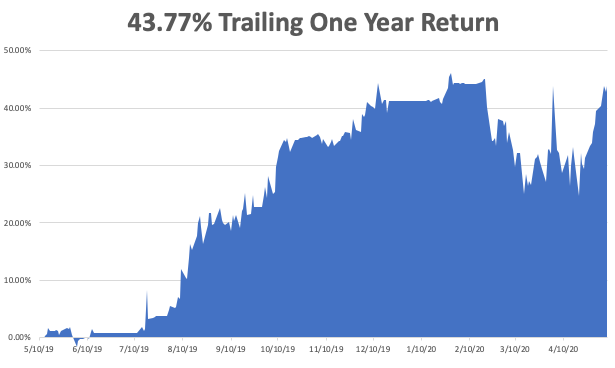

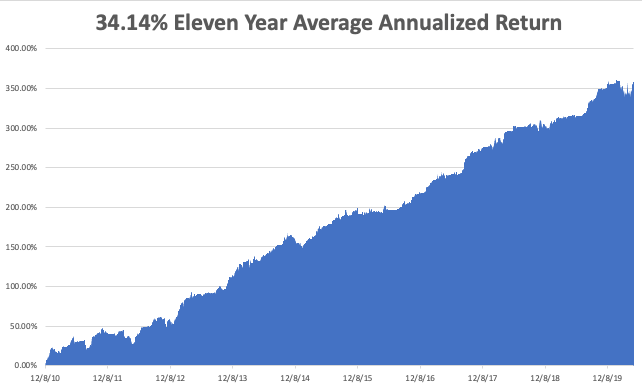

May is up +6.46%, taking my 2020 YTD return up to 2.59%. That compares to a loss for the Dow Average of -13.43% from the February top. My trailing one-year return exploded to 43.77%. My ten-year average annualized profit returned to +34.14%.

This week, Q1 earnings reports continue, and so far, they are coming in much worse than the most dire forecasts. We also get the monthly payroll data, which should be heart-stopping to say the list.

The only numbers that count for the market are the number of US Coronavirus cases and deaths, which you can find here.

On Monday, May 11 at 10:00 AM, the April US Inflation Expectations are out. Caesar’s Entertainment (CZR) and Marriot International (MAR) report earnings.

On Tuesday, May 12 at 5:00 PM, the NFIB Small Business Optimism Index for April is released. Toyota Motors (TM) reports earnings.

On Wednesday, May 13 at 9:30 AM, the ever fascinating weekly Cushing Crude Oil Stocks is announced. Cisco Systems (CSCO) reports earnings.

On Thursday, May 14 at 8:30 AM, we get another blockbuster Weekly Jobless Claims. Advanced Micro Devices (AMD) reports earnings.

On Friday, May 15 at 7:30, AM the Empire State Manufacturing Index is published. The Baker Hughes Rig Count follows at 2:00 PM.

As for me, I’ll continue my solo circumlocution of the 160 mile Tahoe Rim Trail every afternoon in ten-mile segments. Why solo? Do you know anyone else who wants to hike 160 miles at 10,000 feet in two weeks?

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

We Had a 3 Month Warning of the Pandemic and Did Nothing

https://www.madhedgefundtrader.com/wp-content/uploads/2020/05/john-hiking.png523432Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2020-05-11 09:02:132020-06-15 12:08:54The Market Outlook for the Week Ahead, or The Next Golden Age Has Already Started

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.