Mad Hedge Biotech and Healthcare Letter

March 14, 2024

Fiat Lux

Featured Trade:

(TIPPING THE SCALE)

(NVO), (LLY), (VKTX), (PFE), (TSLA)

Mad Hedge Biotech and Healthcare Letter

March 14, 2024

Fiat Lux

Featured Trade:

(TIPPING THE SCALE)

(NVO), (LLY), (VKTX), (PFE), (TSLA)

Imagine, if you will, me sitting down for my morning coffee, flipping through the latest in the biotechnology and healthcare world, when I stumble upon a story that's about as juicy as they come in the world of pharmaceuticals.

The headline? Novo Nordisk's (NVO) stock is on a joyride to the moon, courtesy of their latest heavyweight champ in the weight-loss drug arena, Amycretin.

And let me tell you, this isn’t some minor upgrade. This new candidate is like Wegovy's bigger, bolder cousin.

Now, for those of you who've been tracking the pulse of the market with me, you know I've got a soft spot for stories like these. It's not every day you see a drug come out swinging, making Wegovy look like it's been skipping gym sessions.

As for Novo, the stock didn't just jump following the reports about Amycretin’s performance. It practically did a backflip, soaring over 7% in Copenhagen. And Stateside? We're talking an 8.4% leap to a whopping $135.28. Yes, my friends, that's record-breaking territory.

Let me put this into perspective. Novo Nordisk, with this surge, practically eyeballed Tesla's (TSLA) market value and said, "Hold my beer."

We're talking about a market cap north of $560 billion. Makes you wonder if Elon's feeling the heat, doesn't it?

But this isn’t the last time we’ll hear about Wegovy. Novo’s former golden child of weight loss hasn't been kicked to the curb yet. Far from it.

In fact, the US Food and Drug Administration (FDA) recently stamped it with a seal of approval for reducing heart attack and stroke risks.

This is huge. Why? Because it cracks the door wide open for Medicare coverage. And considering more than 40% of American adults are wrestling with obesity, that's no small target market.

Now, I hear you asking, "But isn't Wegovy's price tag a bit... steep?" Sure, at over $16,000 annually, it's not chump change.

Still, this approval could shift the entire healthcare chessboard. Imagine, medications that once were shrugged off by insurers now potentially becoming mainstays in treatment plans. More importantly, this decision could lead to a surge in demand like never before.

Let me explain why. Prior to this FDA approval, insurers were practically turning their noses up at coughing up the cash for these types of meds. Despite that, folks were clamoring for Wegovy like it was the last slice of pizza at a party.

What do you suppose happens now that Wegovy's got the golden ticket for conditions that insurance can't help but cover? I mean, we're about to see demand go from "Please, sir, I want some more" to a full-blown Oliver Twist riot.

Given this demand, it’s no longer surprising that the scene is getting crowded with competitors itching for a piece of the pie.

Eli Lilly's (LLY) not sitting this dance out, with Zepbound and Mounjaro drawing eyes and opening wallets. Actually, analysts are already placing bets, with some forecasts shooting as high as $60 billion by 2030 across various applications.

Aside from the established names in this niche, there are also up-and-comers like Viking Therapeutics (VKTX) with its impressive trial results for VK2735. Then there's Pfizer (PFE), fumbling a bit with orforglipron but not out of the game yet.

For all of us watching all these unfold, this is the kind of narrative we live for. Novo Nordisk's Amycretin and the bustling competition in the obesity drug market are not just stories of medical innovation; they're tales of market intrigue, investment opportunities, and, yes, a bit of drama.

Before getting in the fray, I suggest you wait for the dip. For now, just grab your popcorn (low-cal, of course) and stay tuned. This biotech thriller is just getting started, and something tells me the plot twists are going to be worth the price of admission.

Mad Hedge Biotech and Healthcare Letter

March 7, 2024

Fiat Lux

Featured Trade:

(RALLY CAPS ON)

(VKTX), (LLY), (NVO), (AKRO), (GILD), (BMY), (AMGN), (PFE)

The biotech sector just flipped its rally cap inside out. After a brutal losing streak, it's clawing its way back. The SPDR S&P Biotech (XBI) exchange-traded fund, a barometer for the sector, started to show signs of life when it soared by 5.7% last month, cresting over $100 a share for the first time in two whole years.

While champagne might be premature, this comeback is heating up, and whispers of a full-fledged rally are echoing through Wall Street.

After a rough patch that kicked off in early 2021, seeing the fund take a nosedive of over 60% by late October 2023, the tide began to turn last fall. Initially, whispers of lower interest rates in 2024 sparked interest across small-cap indexes, including our biotech heroes.

Yet, lately, the buzz is all about biotech's own merits — think breakthrough medical trials and the juicy prospect of big pharma playing Pac-Man with smaller but promising biotech firms to beef up their drug pipelines.

And let me tell you, if the current rally's got legs, we might just be witnessing the most thrilling biotech comeback in over half a decade. Especially if the merger and acquisition scene stays hot, we could see biotech stocks climbing even higher.

Take everything that happened in the sector in February as an example. Viking Therapeutics (VKTX) threw down the gauntlet with promising data on its weight loss drug, VK2735, making investors sit up and take notice.

Actually, this candidate is shaping up to be a formidable rival to obesity treatments from Eli Lilly (LLY) and Novo Nordisk (NVO), sending Viking's shares skyward by a jaw-dropping 121% in a single day.

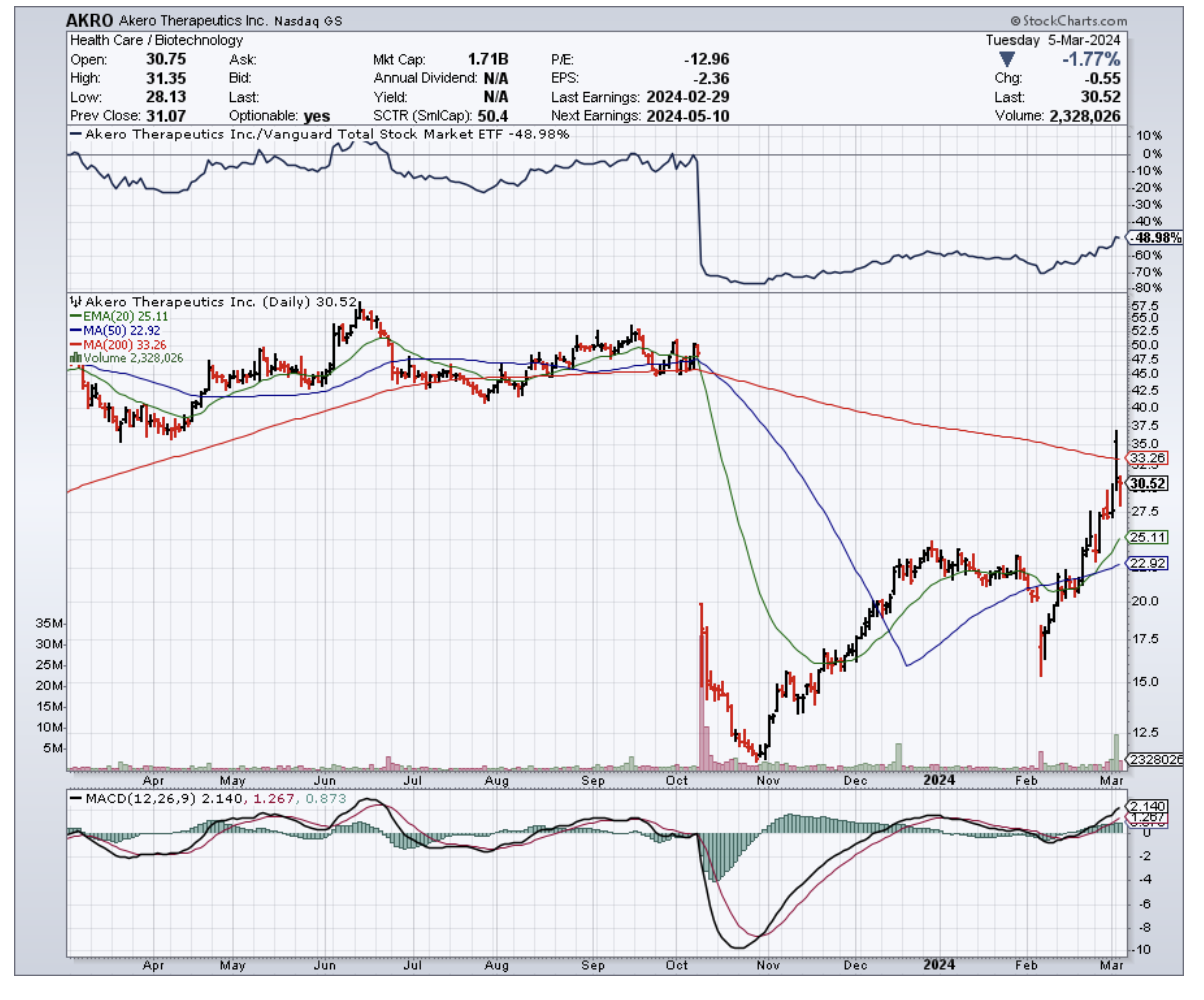

And it's not just Viking stealing the spotlight. Another biotech named Akero Therapeutics (AKRO) also bounced back with some impressive data of its own, challenging the doom and gloom that settled over biotech firms following Eli Lilly's bombshell MASH trial results.

Akero's mid-stage study showed that their drug, efruxifermin, could significantly roll back liver fibrosis in MASH patients — putting a whopping 75% of high-dose recipients on the mend, a stark contrast to the 24% placebo group.

This revelation was a game-changer, especially after Lilly's tirzepatide threw the sector for a loop, hinting at a potential endgame for MASH-specific treatments. But while Lilly's announcement left many details to the imagination, Akero's clear-cut results have reignited excitement over what might be the best MASH treatment yet seen.

As expected, in the midst of this resurgence, the likes of Viking and Akero are catching eyes not just for their groundbreaking treatments but also as tantalizing acquisition targets. Heavyweights like Gilead Sciences (GILD), Bristol Myers Squibb (BMY), Amgen (AMGN), and Pfizer (PFE) are said to be circling, each eyeing a slice of the biotech pie.

As for the biotech investment landscape in general, it's buzzing with renewed vigor. The early months of 2024 have welcomed a smattering of biotech IPOs, a refreshing change after a long drought. CG Oncology's late January debut practically set the market ablaze, doubling in value on its first trading day.

Moreover, public biotechs have found a lifeline in PIPE deals, sidestepping the regulatory hoops of secondary offerings. For instance, Denali Therapeutics' (DNLI) recent PIPE deal, expected to rake in $500 million, is proof of the sector's warming investment climate.

So, dust off those rally caps because the biotech sector isn't just back in the game – it's swinging for the fences.

Breakthrough treatments, a sizzling M&A market, and investors throwing their support behind innovation — this rally has all the ingredients to paint a bright future for the industry. While there will be bumps along the road, one thing's for sure: the biotech sector is poised for a season no one wants to miss.

Mad Hedge Biotech and Healthcare Letter

January 16, 2024

Fiat Lux

Featured Trade:

(PHARMA GIANTS HUNTING FOR THE NEXT BIG THING)

(IMCR), (SNDX), (BPMC), (MRK), (JNJ), (HARP), (AMAM), (MDGL), (VKTX)

Alright, let's dive back into the biotech pool – and no, it's not the kind where you just dip your toes. We're talking about a full-blown belly flop into the deep end of the stock market.

Since October 2023, biotech stocks have been playing a game of limbo, asking themselves, "How low can you go?" But just when they hit two-thirds below their Covid pandemic peak, Big Pharma came to the rescue like knights in shining armor (or should I say, lab coats?).

In an earlier letter, I talked about J.P. Morgan’s annual healthcare conference, essentially the Super Bowl for healthcare geeks. The buzz? Merck (MRK) grabs Harpoon Therapeutics (HARP) for $680 million – a move as sharp as, well, a harpoon.

Not to be outdone, Johnson & Johnson (JNJ) scoops up Ambrx Biopharma (AMAM) for a cool $2 billion. Talk about shopping sprees!

But wait, there’s more. Looking into the rest of the biotech companies in the market today, I can spot a few potential biotech Cinderellas, waiting for their Big Pharma prince. And no, I don't have a crystal ball, but I do have some educated guesses.

First up, let’s chat about Immunocore Holdings (IMCR). These British wizards have been turning heads since Kimmtrak, their first drug for a rare eye cancer, got the green light in 2022.

This biotech is a $1.9 billion David amidst the Goliaths, with a therapy that’s like whispering secret orders to the patient's immune system – "Psst, go beat up that tumor, will you?" And guess what? It listens. This approach isn’t just for show; it’s bumping up survival rates, and that’s a big deal.

Impressively, Immunocore isn't just a one-hit wonder. Kimmtrak, their star player, is not your average Joe of the T-cell receptor (TCR) immunotherapy world. It's more like the valedictorian – first of its kind to get the thumbs up in a who’s who of countries, including the United States, Canada, the E.U., the U.K., and Australia.

For a small-cap player, that’s like winning the World Cup in its rookie year. And with no rivals for Kimmtrak’s indication, it’s like they’ve got the whole playground to themselves.

Next, let’s take a trip to Boston’s backyard – Syndax Pharmaceuticals (SNDX). They’re nearly doubling their value faster than you can say “biotech boom,” thanks to some promising drugs for leukemia and transplant complications.

With a market cap near $1.7 billion and potential FDA nods on the horizon, they're like the biotech version of a sleeper hit.

Checking out the long-term plans of Syndax, they've got a lineup of compounds that are like a biotech fan's dream team, eyeing not one, but two FDA green lights in 2024. They're buddying up with Incyte (INCY) on these compounds, and let me tell you, the scientific world is giving them the thumbs up. And to keep the lights on and the science humming, they've tucked away a cool $200 million from a recent capital raise.

But that’s not all. Since the market hit rock bottom in late October, Syndax's stock has been shooting up like a rocket, a whopping 75% jump. It’s like they've been hitting the gym hard. Bank of America's bullish call on the stock? That was the protein shake.

Now, I'm all for a good success story, but let’s not get ahead of ourselves. I'm keeping an eagle eye on this one, waiting for the perfect moment when the shares might take a little breather, maybe dip into the mid-teens. That's when I’ll swoop in, snagging a slice of SNDX, especially with those FDA approvals on the horizon. After all, these deals are all about timing.

And who could ignore Blueprint Medicines (BPMC)? Straight out of Cambridge, Massachusetts, these folks have a drug targeting certain white blood cell cancers.

These folks aren't your average biopharma company; they're more like the MIT of medicine, crafting precision treatments that home in on the genetic bad guys causing cancer and blood disorders. Their lineup? A dynamic duo of Ayvakit for systemic mastocytosis and Gavreto for those tricky RET-cancers, plus four more contenders in clinical trials, all ready to rumble in the biotech arena.

Blueprint's story started in 2011. They then hit the public scene in 2015, where they raised a whopping $154.8 million at their IPO - talk about making an entrance.

Fast forward to today, and their stock is hovering around $85.00 a pop, boasting a market cap of $5.4 billion – that's billion with a “B.”

What’s their secret sauce, you ask? These geniuses have a discovery platform that's like a GPS for kinases, the sneaky culprits behind many diseases. Their method? Create compounds that are like guided missiles, targeting these kinases with precision. The result? Two FDA approvals, and probably a few high fives in the lab.

But hey, it’s not all about cancer. The weight-loss drug arena is heating up, too. Madrigal Pharmaceuticals (MDGL) and Viking Therapeutics (VKTX) are the names to drop here. Madrigal’s eyeing FDA approval for a liver treatment, while Viking’s showing some early promise in the weight-loss game.

So, there you have it – the biotech scene is sizzling, and these companies are the ones turning up the heat. My two cents? Keep these companies under your watchful eye. You never know, one of them might just be the golden ticket in this dazzling biotech arena.

Mad Hedge Biotech and Healthcare Letter

December 28, 2023

Fiat Lux

Featured Trade:

(CLOSING THE YEAR WITH A BANG)

(XBI), (ABBV), (IMGN), (RHHBY), (PFE), (MRK), (AMGN), (VKTX), (TERN)

The biotechnology sector, pretty much like a phoenix rising from the ashes of its recent lackluster performance, is experiencing a renaissance as 2023 draws to a close. The recent spree of high-stakes deals has set the stage for what could be a significant rebound, a situation that savvy investors should watch closely.

In a remarkable display of strategic maneuvering, AbbVie (ABBV) has been on an acquisition tear.

Earlier in December, they've recently snapped up Cerevel Therapeutics for an eye-popping $8.7 billion, only a week after announcing their intent to acquire ImmunoGen (IMGN) for a formidable $10.1 billion.

And in this high-stakes game, Roche Holding (RHHBY) isn't playing second fiddle, having declared their acquisition of Carmot Therapeutics for $2.7 billion.

This flurry of activity isn't just a few isolated incidents. It's actually a trend. Of the 18 biotech acquisitions exceeding $1 billion announced this year, a significant one-third have emerged since October. This surge is like a shot in the arm for the sector, suggesting a much-anticipated uptick.

But let's take a step back and consider the broader picture.

The SPDR S&P Biotech ETF (XBI) has shown some muscle in November and December. However, it's still trailing behind this year, down by 3%, while the S&P 500 has surged by 19.5%.

Now, focusing on the XBI, a temperature check for the sector: trading around $80, it's a steep drop from its heyday in the $140 range during late 2020 and early 2021. It's down nearly 50% from its peak in February 2021.

This isn't just a dip; it's a nosedive.

Looking at the turn of events, it’s possible that the AbbVie-ImmunoGen deal is perhaps the precursor to a more consistent pattern of mergers and acquisitions in 2024. It seems that we've hit the floor and the only way now is up, with M&A activities poised to inject some much-needed vitality into the sector.

In previous years, the biotech valuations took a hit, and understandably, companies were hesitant to settle for offers that undervalued them compared to their pandemic-era zeniths. But this year, the tide has turned.

Notably, the cumulative value of biopharma deals at a whopping $128 billion this year, shooting up from $61 billion in 2022.

Key transactions fueling this jump include Pfizer's (PFE) massive $43 billion deal for Seagen and Merck’s (MRK) $10.8 billion acquisition of Prometheus Biosciences.

The shift in the regulatory landscape is also worth noting.

Antitrust regulators, who initially seemed poised to block deals like Amgen's (AMGN) $27.8 billion acquisition of Horizon Therapeutics, have shown more flexibility. This change in stance is likely emboldening companies to pursue larger deals.

Now, let's talk about the financial clout.

Large-cap biopharma companies are projected to have about $199 billion in cash by year-end. There's a noticeable dip in dividends and stock buybacks, hinting at a strategic pivot towards mergers and acquisitions. It could indicate that we can expect Pharma to maintain an aggressive stance on the M&A front.

So, what's in store for the XBI and investors alike?

This uptick in M&A activity is like untying the strings of a tightly held purse, releasing cash back into the sector. It's a magnet for both specialist and generalist investor interest, a potential boon for the XBI.

Predicting the next wave of M&A is basically like reading tea leaves. Yet, this year has shown a marked preference for biotechs specializing in obesity, immunology, and cancer.

A notable example is the speculation around Pfizer eyeing a deal with a biotech firm developing an anti-obesity pill.

The ripple effect? Shares of Viking Therapeutics (VKTX) and Terns Pharmaceuticals (TERN), both in the obesity pill race, have seen their stocks jump 47% and 62.5%, respectively, in December.

Evidently, the biotech sector, once in the doldrums, is now witnessing a renaissance. This resurgence is marked by major deals reshaping the industry landscape, holding significant implications for 2024 and beyond.

For investors, this sector represents a fertile ground for growth and opportunity. Staying informed and nimble is key to capitalizing on these dynamic developments. The biotech sector, it seems, is back in the game, and how!

Mad Hedge Biotech and Healthcare Letter

December 12, 2023

Fiat Lux

Featured Trade:

(A REBOUNDING BLUE CHIP)

(PFE), (LLY), (NVO), (RHHBY), (AZN), (SGEN), (VKTX), (TERN), (GPCR), (ALT)

In the maelstrom of 2023, Pfizer (PFE) found itself navigating through a tempest, much to the dismay of shareholders. The aftermath? A harrowing -40% total return loss, leaving shareholders reeling.

This downturn followed Pfizer's COVID-19 vaccine triumph, a success story that lost its sheen as global government demand for the vaccine and Paxlovid antiviral dwindled.

Looking back, Pfizer's narrative in 2023 could rival a Shakespearean tragedy. The demand dip for its COVID arsenal was just the beginning; a cascade of other factors compounded the company's misfortunes.

Take, for instance, the controversial $43 billion acquisition of Seagen (SGEN) in March. While this move aimed for cancer treatment breakthroughs, it was widely seen as a Hail Mary, signaling gaps in Pfizer's drug pipeline.

I estimate this strategy might have slashed shareholder value by at least 10%, given the immediate financial aftermath of the merger.

Then, adding to the woes, Pfizer's Nash County production facility in North Carolina faced devastation by a tornado in July.

It seemed as though, for Pfizer in 2023, trouble came not just in droves but in torrents.

The final blow? The discontinuation of the twice-daily dose development for Danuglipron, Pfizer's weight-loss drug candidate.

This decision casts a shadow over the prospects of its once-a-day dosage, still in trials, and simultaneously cracks open the door for other biotech players in the oral weight-loss drug arena.

Meanwhile, the company also aimed to join the race for obesity treatment innovation. In this arena, injectable weight-loss drugs from Eli Lilly (LLY) and Novo Nordisk (NVO) have set the stage, and now, the demand for oral solutions is burgeoning.

Pfizer once pegged this market's potential at an eye-watering $90 billion a year — a target that has not gone unnoticed by keen biotechs.

Yet, with Pfizer stepping back from its Danuglipron project due to adverse side effects, it finds itself trailing in this race. In comparison, Lilly and Novo are forging ahead with their products, turning Pfizer's stumble into a potential windfall for other biotech firms.

Notably, the biotech sector is witnessing a flurry of activity in response to Pfizer’s failed attempt.

Firms like Viking Therapeutics (VKTX), Terns Pharmaceuticals (TERN), Structure Therapeutics (GPCR), and Altimmune (ALT) have seen their share prices soar following their own positive trial results or strategic announcements.

The diverse approaches these biotechs are employing in their anti-obesity drug development have piqued investors’ interest.

In effect, speculation is rife about which one might emerge as a desirable acquisition target for Pfizer — and this speculation isn't without basis.

I previously shared that Roche Holding (RHHBY) recently acquired Carmot Therapeutics for $2.7 billion, and AstraZeneca (AZN) entered a licensing agreement with Eccogene.

With a history of significant acquisitions, Pfizer might well consider a similar path to address its challenges in the weight-loss pill sector.

Pfizer's journey through 2023 was a series of unfortunate events, to say the least. As we look to the future, questions about potential challenges in 2024 loom.

While major acquisitions seem unlikely in the wake of the Seagen deal, shareholder sentiment is fragile. The immediate risks for Pfizer include the possibility of a 2024 recession impacting sales and a generally bearish stock market, potentially keeping share prices around the $30 mark.

Historically, however, Pfizer has stood as a bastion of strength during recessions and bear markets.

Looking longer term, the specter of Medicare drug price negotiations looms large, threatening to dampen growth investor sentiment.

This challenge isn't unique to Pfizer; it's a cloud hovering over all of Big Pharma.

Yet, despite these formidable challenges, there's a sense that Pfizer's tumultuous 2023 journey might be approaching a pivotal turning point. Investor sentiment is at a nadir, marred by negative press and shareholder dissatisfaction, painting Pfizer as a stock currently out of favor.

As we look ahead into 2024, a cautious optimism emerges. Should Pfizer return to operational normalcy and continue to reduce its reliance on COVID-related sales — now a smaller part of its business — the company could reassert itself as a prime value and dividend player in the Big Pharma space.

For the resilient investor willing to delve into a bruised yet potentially rebounding blue-chip, Pfizer merits a closer examination. After a year where Murphy's Law seemed the only law, Pfizer stands as a beacon of resilience and a potential phoenix in the biotech and healthcare sector.