Global Market Comments

June 21, 2023

Fiat Lux

Featured Trades:

(WEDNESDAY, JULY 19, 2023 LONDON GLOBAL STRATEGY LUNCHEON)

(THE BUY AND FORGET PORTFOLIO),

(SPY), (IXUS), (EEM), (VNQ), (TLT), (TIP)

CLICK HERE to download today's position sheet.

Global Market Comments

June 21, 2023

Fiat Lux

Featured Trades:

(WEDNESDAY, JULY 19, 2023 LONDON GLOBAL STRATEGY LUNCHEON)

(THE BUY AND FORGET PORTFOLIO),

(SPY), (IXUS), (EEM), (VNQ), (TLT), (TIP)

CLICK HERE to download today's position sheet.

All traders and portfolio managers with experience approaching a half-century, like myself and a handful of close friends, agree on one thing.

Someday, you will be wrong.

I don’t mean just a little bit wrong, I mean disastrously wrong. A real humdinger, even a life-threatening experience. Even wrong up the wazoo.

In fact, most old salts, even the best performing ones, suffer at least a couple of 50% losses of their total assets, and at least one 75% hit, at least once in their lives.

We’ve all been there.

The 1973 oil crisis. The 1987 stock market crash, when the Dow Average gave up a withering 22% in a single day (I tried to place an order to buy stock at the close and the clerk burst into tears and dissolved into a puddle on the floor).

The Dotcom crash. And of course, the granddaddy of them all, the Great Crash of 2008, which you all remember with the greatest discomfort.

Even my mentor, Warren Buffet, has admitted to taking three 50% hits in his lifetime and lived to tell about it.

The trick is to keep these misfortunes from wiping you out so completely that you can never make a comeback.

Better yet, don’t get into trouble in the first place. And I’ll tell you exactly how to do that right now.

One of the great pleasures of running the Mad Hedge Fund Trader is that I get to speak to thousands of interesting people every year. Believe me, there are all kinds.

I have found kids straight out of school who take to trading like a fish to water. Their instincts are incredible. They figure out the harsh realities of the market decades before I ever did.

When they ask me questions, I think, “Damn! Why didn’t I think of that?”

I have seen several of these gifted, natural born traders use the Mad Hedge Fund Trader turn pennies into millions over unbelievably short times.

You see, they have the trader gene.

Sadly, I also run into the opposite extreme. With some people you could have George Soros sitting on their left, Paul Tudor Jones on their right, both guiding their hands on the mouse to execute trades, and they are still going to still lose money.

These are not stupid people.

I have met many with Harvard MBAs, advanced degrees from MIT, and even Phi Beta Kappa’s, and it doesn’t do them a whit of good on the trading front. They just don’t have trading in them.

In other words, they lack the trading gene.

When I stumble across these people, I tell them to quit trading, end the self-abuse, and preserve whatever wealth they have left. I then order them to buy what I call my “Buy and Forget Portfolio.”

This is a collection of only six investments, which I have assembled over the decades that will be profitable in almost all circumstances. In good years it will grow generously. In bad years it will be down marginally. Over the long term, it will do extremely well.

Here it is:

The Mad Hedge Buy and Forget Portfolio

20% domestic US stocks (SPY)

20% international stocks (IXUS)

10% emerging stock markets (EEM)

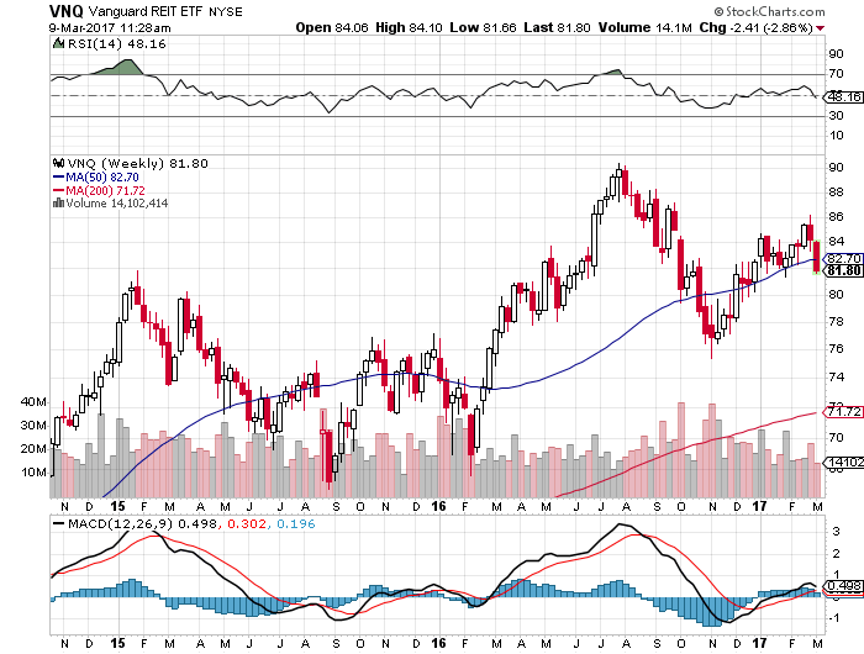

20% Real Estate Investment Trusts (VNQ)

15% long term US Treasury Bonds (TLT)

15% Treasury Inflation Protected Securities (TIP)

Notice that half the money is in equities and the remainder in fixed income securities.

If you initiated this portfolio in 1997, the year that TIPS first became available to the public, you would have earned an average annualized compounded return of 7.86% through the end of 2014, assuming reinvestment of dividends and interest.

During the bear market of 2000-2002, when the S&P 500 dropped 50%, this portfolio never suffered a loss of more than -4.7%. During the Great Crash of 2008, it fell -31%, versus -37% for the (SPY), and then very quickly bounced back.

Most long-only investors would have killed for returns like these.

So the bottom line is this. Expect a 4% drawdown every decade, a 31% hickey twice a century, and one of those twice-a-century events is only eight years behind us. That is not a bad proposition.

The heavy stock weighting can be easily explained by the fact that historically, stocks have outperformed bonds by a large margin.

For long periods of time, such as much of the 19th century, the Great Depression, and now, chronic structural deflation meant that bonds paid very little in interest.

Stocks also have the advantage in that during periods of inflation they can pass rising costs on to consumers via price hikes.

Guess what? We are just going into an inflationary period.

For the past 200 years, stocks have therefore delivered a compounded average annualized return of 8.3%.

Just to give you an example of how valuable the stock advantage can be, $1 invested in 1802 would be worth $8.8 million today.

This is why Oracle of Omaha Warren Buffet constantly sings the praises of compounding and dividend reinvestment and is why he rarely sells anything. In fact, his authorized biography is entitled Snowball (a great read, by the way).

The beauty of the Buy and Forget Portfolio is that the six elements counterbalance each other in all market circumstances. When stocks go up, bonds usually go down, and vice versa.

They both go the wrong way only for very short periods, such as in 2008 and always snap back.

And remember inflation, that long-forgotten thing where prices actually go up? It will make a return someday. And there is no better time to buy TIPS than during the deflationary surge that we are enduring now. TIPS prices are cheap.

Such is the beauty of diversification.

The great thing about the Buy and Forget Portfolio is that you can literally buy and forget about it. You won’t lose sleep at night, you could care less about what they say on CNBC, and don’t have to hide those embarrassing brokerage statements from your spouse.

The only thing you have to do is to rebalance it once a year to restore each component to its original weighting. More often than that and you run up big commission and tax bills.

Remember, you are trying to buy your own yacht, not your broker’s.

This will free you up to focus on the more important things in life.

Will Daenerys Targaryen gain her rightful place on the throne of the Seven Kingdoms in The Game of Thrones? Will Don Draper get his well-deserved comeuppance in the final season of Mad Men? Can the widow, Lady Mary, ever find true love again in the next season of Downton Abbey?

Of course, knowing all of this, some bad traders will continue to trade. For some, it is like an addition. They just have to win, whatever the cost. For others, it's like buying lottery tickets. Some just love the adrenaline and the thrill of the chase, even if it costs them money.

Whatever the reason, they continue trading until they run out of money. Then they will try to borrow your money to trade.

Could this be you?

All I can do is wish them the best.

Leave the trading to the masochists, like me.

Leave the Trading to the Masochists

Mad Hedge Technology Letter

October 16, 2020

Fiat Lux

Featured Trade:

(CELL TOWER INDUSTRY IS PRINTING MONEY)

(CCI), (SBAC), (UNIT), (VNQ), (LMRK), (VMI)

Investors who want to green light capital into this sector should consider American Tower (AMT), Crown Castle (CCI), SBA Communications (SBAC), and Uniti Group (UNIT). Cell towers are the largest property sector by market capitalization making up 18% of the broad-based Vanguard Real Estate ETF (VNQ).

Three disruptive developments started before the pandemic will remain influential from the chronic housing shortage to retail apocalypse, and the migration to digital.

The 2020s will supercharge these three trends and tech investors need to scurry into the intersection of seminal trends to profit from the appreciation taking place in the U.S. economy.

As a 10% pullback in cell tower REITs over the last quarter reared its ugly head, offering a rare entry point into this segment of the U.S. tech ecosystem.

Usage of the cell towers has mushroomed throughout the pandemic. Cellular network capacity has been pushed to the limits as businesses, schools, and individuals take their in-person life and migrate it online.

5G is circling in the skies looking for a soft landing. Phone makers are frantically upgrading their device iterations to accommodate an internet speed that is 100X faster than what we have now.

Any company that flubs the 5G smartphone will be left in the dust.

Cell tower REITs will eventually be the focal point of 5G networks, supported by a network of higher-density small cells. High-power macro towers provide the most economical mix of wide coverage and capacity.

Super-fast Wi-Fi speeds will usher in a new era of super apps that will fundamentally disrupt the telecommunications space and deliver cheaper and more efficient apps to the consumer marketplace.

These super apps will make the apps we use now on our phones seem like a waste of time.

Cell tower REITs continue to benefit from favorable competitive positioning within the telecommunication sector. Scant supply and high demand should translate into continued pricing power for cell tower REITs.

Cell tower REITs are the “landlords” to the United States' four nationwide cellular network operators: AT&T (T), Verizon (VZ), T-Mobile (TMUS), and DISH Network (DISH). These three cell tower REITs own roughly 50-80% of the 100-150k investment-grade macro cell towers in the United States. This favorable competitive positioning has given these REITs substantial pricing power over the last decade amid the roll-out of 3G and 4G networks.

5G is the fifth-generation mobile network that powers mobile broadband, promising far-faster speeds and lower latency than the prior iteration.

5G networks require up to 10 times more physical antennas per tower, and cell tower REITs typically negotiate higher revenue per tower after each incremental equipment upgrade.

Cell tower REITs continue to be one of the few remaining growth engines of the REIT sector, and the health crisis has validated the need for additional network investments.

The dearth of cell tower supply - combined with the absolute necessity of these towers for networks - has given REITs substantial pricing power even as the number of potential tenants has dwindled down to just four national carriers over the last two decades.

High barriers to entry through the local permitting process and due to the economics of mass scaling make competition irrelevant.

This is a high-margin business with significant operating leverage driven by adding additional multiple tenants to existing towers.

Cell towers aren’t going away anytime soon and there is nothing to replace it on the horizon.

Another viable infrastructure play would be Landmark Infrastructure Partners (LMRK), an MLP that owns real property interests that underlie cellular towers, rooftop wireless sites, billboards, and wind turbines.

I would throw Valmont Industries, Inc. (VMI), who manufactures communication infrastructure, into the mix as well.

Global Market Comments

November 1, 2019

Fiat Lux

Featured Trade:

(OCTOBER 30 BIWEEKLY STRATEGY WEBINAR Q&A),

(SQ), (CCI), (SPG), (PGE), (BA), (MSFT), (GOOGL), (FB), (AAPL), (IBB), (XLV), (USO), (GM), (VNQ)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader October 30 Global Strategy Webinar broadcast from Silicon Valley, CA with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Would you buy Square (SQ) around here?

A: I don’t want to buy anything around here—that’s why I’m 90% cash. Would I buy Square on a market selloff? Absolutely, it's one of our favorite fintech stocks for the long term. The fintech stocks are eating the lunch of the legacy banks at an accelerating rate.

Q: What's the best yield play currently, now that bonds have gone so high?

A: High-quality REITs—especially cell tower REITs. We’re going to get a significant increase in the number of cell towers, thanks to 5G, and there are REITs specifically dedicated to cell phone towers. An example is Crown Castle (CCI), which has a generous 3.45% dividend yield. The worst REITs are the mall-based like Simon Property Group (SPG).

Q: PG&E (PGE) has just had a huge selloff of 50%. Should I buy it now or is it a potential zero?

A: I wouldn’t touch PG&E at all—They’re already in bankruptcy, and they are now accepting responsibility for starting another eight fires this week, including the big Kincaid fires. You could have the state government take over the company and wipe out all the shareholders— the liabilities are just growing by the second, so I would turn my attention elsewhere. Don’t reach for new ways to get in trouble.

Q: Regarding Boeing (BA), it looks like you caught the bottom on the last dip—should I buy it here or wait for another dip?

A: Wait for another dip. The company seems to have an endless supply of bad news. That said, if we visit $325 a share one more time, I would buy it again. We caught about a $10 dollar move in Boeing to the upside. Keep buying the dips. The bad news story on this is almost over.

Q: Do you think the earnings season will be better than expected? If so, which sectors do you think will outperform?

A: It’s always better than expected because they always downgrade right before earnings, so everything is a surprise to the upside. Some 80% of all stocks surprise to the upside every quarter. And what would I be buying on dips? Big Tech. Especially things like Apple (AAPL), Facebook (FB), Alphabet (GOOGL), and Microsoft (MSFT) —that is where the only reliable longer-term growth is in the economy. If you want to buy cheap companies on dips, go for Biotech (IBB) and Health Care (XLV), which have gone up almost every day since we launched the Biotech letter a month ago. To subscribe to the Mad Hedge Biotech and Healthcare Letter, please click here.

Q: What does it mean that the Chile APEC summit is cancelled? What is Trump going to do now for signing on the trade deal?

A: There may not be a trade deal. It's another postponement and could be another trigger for a long-overdue selloff in the market. We've basically been going up nonstop now for 2½ months, and almost everyone's market timing indicators are saying extreme overbought territory here, including ours.

Q: Will there be a replay of this webinar posted?

A: Yes, we always post these on the website a couple of hours after it airs. Some 95% of our viewers watch the recordings, especially those overseas in weird time zones like Australia and India. You need to be logged in to access it. Just go to www.madhedgefundtrader.com, log in, go to My Account, then Global Trading Dispatch, then click on the Webinars button. It’s there in all its glory.

Q: Does Invesco DB US Dollar Index Bullish Fund ETF (UUP) make sense (the dollar basket)?

A: No, I'm staying out of the currency market because there are no clear trends right now and there are much clearer trends in other asset classes, like stock and bonds.

Q: How do you see General Electric (GE)?

A: There are a lot of people shouting accounting fraud like Harry Markopolos, the whistleblower on Bernie Madoff. Sure, they had a good today, up a buck, but their problems are going to take a long time to fix. So, don't think of this as a trading vehicle, but rather a long-term investment vehicle.

Q: Could the Saudi Aramco IPO push the price of oil up?

A: You can bet they're going to do everything humanly possible to get the price of oil (USO) up and to get this IPO off their hands—that's why you shouldn't buy the IPO. The Saudis are desperate to get out of the oil business before prices go to zero and are pouring money into alternative energy and technology through Masayoshi Son’s Vision Fund. When you have the chief supplier of oil rigging the price, you don’t want to be anywhere near the distributor and that’s Saudi Aramco.

Q: What about selling the (SPG) (Simon Property) REIT?

A: It’s kind of too late to sell, but what you might think of doing is selling short just one deep out-of-the-money put, just to bring in a small amount of income. These things don’t crash, they grind down; so, it could be a good naked put shorting situation, but only on a very small scale. If you want to play REITs on the long side, look at the Vanguard Real Estate ETF (VNQ), which pays a handy 3.12% dividend. Guess what its largest holdings are? 5G cell tower REITs.

Q: Is General Motors (GM) a buy on the union detent?

A: Only for a trade, but not much; the auto industry is the last thing you want to buy into going into a recession, even just a growth recession.

Q: Have we topped out on Apple (AAPL) for the year at $250?

A: If we did, it’s probably just short term. Remember their 5G phone is coming out next September and I expect the stock to go to $300 dollars just off of that. Any dips in Apple won’t last more than a month or two.

Q: Could we get another leg up for the end of the year?

A: Yes, not much, maybe another 5% from here, and I wouldn't do that until we get another 5% drop in the market first which should happen sometime in November. If that happens, then you’ll have a shot at making another 10% by the end of the year, which is exactly what I plan on doing for myself. That would take our 2019 performance from 50% to 60%.

Q: Is the Fed’s printing infinite money going to lead to runaway inflation crashing the value of the dollar?

A: Yes, but it may take us a couple of years to get to that point. So far, no sign of inflation, except inflation of things you want to buy, like healthcare, a college education, and so on. For anything you want to sell, like your labor or service, the prices are collapsing. That’s the new inflation, the type that screws you the most.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Let?s face it, the carnage in the bond markets in May outdid the sack of Rome.

Not only did the Treasury bonds (TLT) get hit. The entire high yield space was slaughtered, including corporates (LQD), junk bonds (JNK), REITS (VNQ), master limited partnerships (KMP), municipal bonds (MUB), and high dividend equities. Anything that looked and smelled like a bond got dumped.

As American bonds get their clocks cleaned, so did virtually the entire fixed income space worldwide. Yields on ten-year Japanese government bonds nearly tripled from 0.37% to 0.95%. German bond yields skyrocketed, from 1.20% to 1.55%. Suddenly, a global capital shortage broke out all over like a bad rash.

So has the Great Reallocation out of bonds into stocks begun? Has the Great Bond Crash of 2013 only started? Or is there something more complex going on here?

Don?t worry, the bond market is not about to crash. All we are seeing is a move to a new trading range for the ten year, from 1.50%-2-10% to 1.90%-2.50%. This has been my forecast for the Treasury bond markets all year. High yielding instruments, like those in junk bonds and REITS, will see more dramatic price declines. There are several reasons why this is the case.

For a start, the economy is just too weak to support any further back up in rates. Much of corporate American has grown so used to free money that even a modest rise in rates would be cataclysmic. It was also drop the residential real estate recovery dead in its tracks. Watch the US government?s budget deficit soar, once again, if interest rates continue their assent.

A 2% GDP growth will never be a springboard for 4%, 5%, or 6% yields. In fact, the risk is that we slow down from here, forcing the Fed to come to the rescue with more accommodative swaths of quantitative easing.

Look at the inflation, that great destroyer of bonds. The last reported unadjusted YOY CPI by the Bureau of Labor Statistics came in at a gob smackingly low 1.1% in April (click here for the website).? Real deflation is anything but a major threat, and will not provide the rocket fuel for further bond selling. When you here of friends getting surprise 20% pay hikes, then you can expect a return in inflation. That has been happening in China for several years now. But so far, I have not heard the good news at home.

Check out who has been buying bonds for the last five years? More than half of the Treasury auctions have gone to foreign governments. First it was China, and more recently to European central banks. These people don?t sell. They just redirect new cash flows. You can count on them keeping the bonds they already have until maturity, even if it is 30 years out. They will never be the source of large scale selling.

Examine who has the highest fixed income weightings in the US. It is the fabled ?1%.? When I serviced some of the wealthiest old money families on behalf of Morgan Stanley during the 1980?s, I was struck by one thing. These were the most conservative people in the world. Protection of principal was their primary consideration. Interest income was almost an afterthought.

This is because the majority of wealthy investors inherited their money, and lived in constant fear they would lose what they have. This is because, as trust fund kids, they had no idea how to earn their own money and create new wealth. Once capital disappeared, it was gone for good. Get a job? Heaven forbid! This investor class also has no desire to get hit with the long-term capital gains such sales would generate. So don?t expect selling from them either.

So, at worst case, you might see another 20-25 basis point rise in Treasury yields to the top end of the new range. At that point, they will be a buy for a rally that might correspond to a stock market selloff and flight to safety bid for bonds which I expect this summer. This takes the ten-year back to a 1.90% yield.

This will be particularly crucial for those who have been trading leveraged short fixed income instruments like the (TBT). They saw a dramatic 12-point, 20% rally in May from bottom to top. Any further gains from here will be of the high risk, low return variety. Maybe, it?s time to sit down and smell the roses? Or take a long summer vacation, as I plan to.