Mad Hedge Technology Letter

December 7, 2022

Fiat Lux

Featured Trade:

(MEDIOCRE TECH FURNITURE)

(W)

Mad Hedge Technology Letter

December 7, 2022

Fiat Lux

Featured Trade:

(MEDIOCRE TECH FURNITURE)

(W)

As we gather up to steam to the December 13th CPI report, it is important to keep mindful of avoiding the tech traps out there.

Many tech companies are still worth their weight in gold but some aren’t.

The ones to ignore are specifically the zombie companies.

Low rates almost gave them a great excuse not to profit because back then, with low rates, they could just roll over debt and kick the can down the road.

Suddenly, in 2022, the unthinkable happened, and now profitability matters.

Zombie firms tapping debt markets can be a good thing, but doing so at elevated rates could topple their business model.

One company to stay vigilant about is digital furniture dealer Wayfair (W) whose business model and share price have been disproportionately damaged over the past year and a half.

Just take a look at W’s share price if you don’t believe me.

Shares of W were trading at $315 per share around June 2021 and fast forward to today and the same stock is $36.

I personally believe that it will be a tough slog moving forward for W and it is highly unlikely the easy conditions of 2021 will ever come back to anything similar.

W will inherently struggle to produce real cash flows which means that they are at risk of filing for bankruptcy.

Getting third parties to sell furniture for you and offering a website for that isn’t the greatest business model and they have been exposed.

In the current environment, investors are searching for real cash flows, strong balance sheets, shareholder returns, and sustainable profits.

W doesn’t check one box.

After the arbitrary lockdowns ceased, W’s business resumed burning cash.

W has burned through $4.1 billion in Free Cash Flow, excluding acquisitions, since 2013.

The burn rate is getting worse by the day because of the poor unit economics.

W burned through $1.3 billion in FCF excluding acquisitions over the trailing-twelve-months through the third quarter of 2022, compared to $214 million in the trailing 12 months through the third quarter of 2021.

In August, Wayfair announced plans to lay off about 870 employees, or about 5% of its global workforce.

However, the cost saving is more of a one-time boost to cash flow than anything long-term.

In general, since the last quarter of 2021, earnings per share losses have accelerated to the point where last quarter they delivered -$2.15 of earnings growth.

That was the worst profitability in the last 4 quarters.

Then there is the issue of inflation tearing apart American budgets.

When the cost of furniture was in demand during the government-mandated lockdowns, there was outsized demand for bespoke furniture because Americans spent all day at home.

Now, the cost of food and shelter has become so exorbitant that they are exerting maximum strain on middle class American budgets.

Amid this backdrop, there will be a longer lag until the beginning of a new furniture upgrade cycle.

Consumers were furniture-splurging during the arbitrary lockdowns and now they are splurging on food.

Food now trumps furniture.

I don’t believe this problem has a solution in the near term and any bounce in W shares will be a dead cat bounce.

If the cost of living crisis goes from bad to worse in 2023, then expect even less furniture bought from W.

Global Market Comments

June 6, 2022

Fiat Lux

Featured Trade:

(THE MAD HEDGE TRADERS & INVESTORS SUMMIT IS ON FOR JUNE 14-16)

(MARKET OUTLOOK FOR THE WEEK AHEAD, or PUTIN’S DEAD END),

(VIX), (HYG), (JNK), (PTON), (W), (MSTR), (RDFN), (BYND), (F), (TSLA), (NVDA)

The current consensus for market strategists is that volatility will remain high.

Please pinch me because I think I died and went to heaven. For every time the Volatility Index (VIX) tops $30, I make another 10%-15% for my followers.

The bulk of market players are now obsessing whether we are entering a recession or not, as if their investment faith depended on it.

Recession, resmession.

As long as I can keep making a 65.40% trailing one-year return, while the Dow Average is off -4.2% during the same time period, I could care less what the economy is actually going to do.

After an impressive 380-point, 10% rally in the S&P 500, it now looks like the stock market is failing once again. Best case, we revisit this year’s low at 3,800. Worst case, we break to new lows at 3,600. The very worst case, we break below 3,500 and wish you had never heard of the stock market.

If you are a trader, there is a fantastic opportunity here to buy low, sell high, and retire early. If you are disciplined, you still have a ton of cash left over from the end of 2021 (I was 100% cash) and will be cherry-picking on the big down days.

It's really very simple. The longer you have been doing this, the easier it gets and the more money you will make. After 52 years of practice, I can do this in my sleep.

As the bear market worsens, we are seeing old asset classes return from the dead like the revived dinosaurs of Jurassic Park. Call convertible bonds are the velociraptors of the bunch.

Take the main junk bond ETF like the iShares iBoxx High Yield Corporate Bond Fund (HYG) and the SPDR Barclays High Yield Bond Fund (JNK), which have seen yields double from 3% to over 6% in only six months.

If you are willing to take on more risk, individual busted convertible bonds yield infinitely more. You know all the names. Peloton (PTON) converts are paying a 10.4% yield to maturity, Wayfair (W) 11.0%, MicroStrategy (MSTR) 13.1%, Redfin (RDFN) 14.5%, and Beyond Meat (BYND) 19.5%. Buy ten of these and even if one goes under, you still earn a decent double-digit return.

Having run a convertible bond trading desk for ten years, I can tell you that the risk/reward balance for many individuals with this investment class is just right.

As my summer military duty approaches, information about the Ukraine War is pouring into me. I will share with you what I can, what has been declassified for the war is still a major factor in your investment outcomes. I have been able to use my “top secret” status for 50 years,= to your benefit.

The amazing thing is that in this modern age, information goes from “top secret” to declassified in only a day. It is a new strategy used by the current administration that is working incredibly well. Information is more valuable shared than locked up.

I have been getting a lot of questions from readers as to why Vladimir Putin committed such a disastrous error by invading Ukraine as he is considered a smart guy. My initial response was that he surrounded himself with “yes” men who only told him what he wanted to hear, leading to terrible outcomes, which I have seen happen many times.

The costs of the war for Putin have so far been enormous; 50,000 casualties, 1,000 tanks, 1,300 armored vehicles, banishment from the western economy, the loss of $1 trillion in foreign held assets, and the decline of the national GDP from $1.5 trillion to $1 trillion.

The costs are about to substantially rise. The US is now sending over its most advanced artillery systems, the MRLS, or Multiple Rocket Launch System, which can hit any target within 300 miles with an accuracy of one meter. All you have to do is dial in the latitude and longitude of the target and it never misses. This one weapon will certainly bring the war to a stalemate and consign it to page three of the newspapers.

But after doing a ton more research, my view has evolved. Putin has in fact launched a Resource War against the entire rest of the world. The result has been to boost the price of practically everything Russia produces, including oil ($123 billion), refined petroleum products ($63 billion), iron & steel ($28 billion), coal ($17 billion), fertilizer ($13 billion), wood ($12 billion), wheat ($9 billion), aluminium ($8 billion), platinum, palladium, uranium.

There is also the inflation angle. While the US benefits from many of these high prices as well, they have raised the US inflation rate from 5% to 8.3%. That damages the election prospects of Biden and the Democrats. High inflation improves the election of prospects of a former president who Putin seems to vastly prefer for whatever reason.

After covering Russia for 50 years, flying their front-line fighters, springing a wife out of jail in Moscow, I can tell you that everything there is a chess game, and they play a very long game.

Nonfarm Payroll Report comes in at 390,000, better than expected. Leisure & Hospitality led the gains with 84,000, and Professional & Business Services by 75,000. Manufacturing fell to only 18,000, largely because of a shortage of workers. The Headline Unemployment Rate remained the same at 3.6%. Average hourly earnings rose by an inflationary 5.2% YOY. The U6 “discouraged worker” rate rose back to 7.1%.

Weekly Jobless Claims jump 19,000 to 200,000, a two-month high, according to the Department of Labor. Compensation for American workers has hit a 30-year high. New York showed the largest increase followed by Illinois.

OPEC+ raises oil output to meet surging energy demand caused by the Ukraine War. Up 648,000 barrels a month for July and August. They could easily do a lot more. The cartel is aiming for the pre-pandemic 10 million barrels a day. No dent in prices at the pump yet.

Hedge Funds were slaughtered in May, with the flagship Tiger Global Fund down a massive 14%. Gee, Mad Hedge Fund Trader was UP 11% in May and am up 44% on the year. Maybe there’s something in the water here at Lake Tahoe. Or, maybe it’s the “Mad” that is giving me my edge?

S&P Case Shiller National Home Price Index tops 20.6%, a new all-time high. Tampa (34.8%), Miami (32.4%), and Phoenix (32.0%) lead the gains. Incredible as it may seem, price rises are accelerating. But expect that to cool off once current prices start feeding into the index.

Home Listings soar, with homes for sale up 9% YOY as homeowners fear missing getting out at the top. New listings have doubled in a year, according to Redfin. Outrageous over-market bids have definitely ended in California. So far, no hint of price drops….yet.

A Ford (F) Electric Pickup can power your house for ten days, but only if you live in a tiny house. Ford is the first company to introduce bidirectional charging that lets your home run off the vehicle’s 1,300-pound lithium-ion battery. All you need is a $3,895 hardware upgrade from Sunrun. The range is 320 miles, not as much as the latest Tesla Model X (TSLA). Good luck getting one. Ford isn’t taking any new orders until it fills the 200,000 it already has. Expect Tesla to copy the move.

The Fed may overshoot on raising interest rates if Fed governor Christopher Waller has his way. That’s because going too tight may be necessary to break the back of inflation. That’s what happened in 1980, when Fed Funds hit 17%, and ten-year bond yields hit 15.84%. My first home mortgage interest rate for a coop in Manhattan back then was 17%.

China Covid Cases fade, prompting a big Bitcoin rally. This could be the impetus for a sudden global economic recovery that will deliver a big US stock market rally. Good thing I loaded the boat with tech stocks two weeks ago.

The Fed Minutes were not so horrible, downplaying the risk of a full 1% rate rise, triggering a 1,000-point rally in the Dow. With five up days in a row this is starting to look like THE bottom. Is this the light at the end of the tunnel?

NVIDIA (NVDA) rips, surprising to the upside on almost every front, sending the stock up $30, or 18.75%. Mad Hedge followers bought (NVDA) last week. This is one of the best run companies in the world. I expect the shares to rise from the current $178.51 to $1,000 in five years. Buy (NVDA) on dips.

Q1 GDP dives 1.5%, in its final read. It’s the worst quarter since the pandemic began during Q2 2022. Weekly Jobless Claims dropped 8,000 to 210,000.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still historically cheap, oil peaking out soon, and technology hyperaccelerating, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

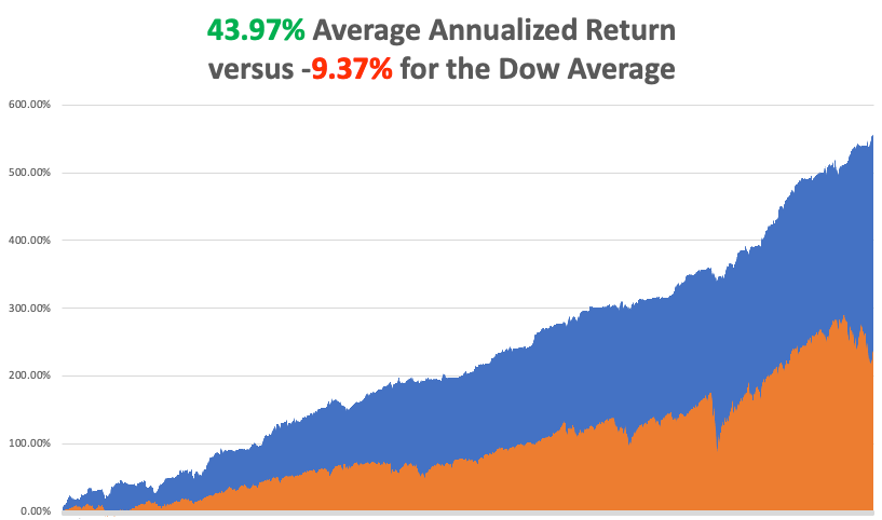

With some of the greatest market volatility seen since 1987, my June month-to-date performance recovered to +2.49%.

My 2022 year-to-date performance exploded to 44.36%, a new all-time high. The Dow Average is down -9.37% so far in 2022. It is the greatest outperformance on an index since Mad Hedge Fund Trader started 14 years ago. My trailing one-year return maintains a sky high 65.40%.

That brings my 14-year total return to 556.92%, some 2.37 times the S&P 500 (SPX) over the same period and a new all-time high. My average annualized return has ratcheted up to 43.97%, easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 84.7 million, up 300,000 in a week and deaths topping 1,000,000 and have only increased by 2,000 in the past week. You can find the data here.

On Monday, June 6 is the 78th anniversary of the D-Day invasion of Normandy. All of the veterans I knew have long since passed. I’ll miss the memorial this year.

On Tuesday, June 7 at 8:30 AM, the US Balance of Trade for April is released.

On Wednesday, June 8 at 10:30 AM, US Crude Inventories are published.

On Thursday, June 9 at 8:30 AM, Weekly Jobless Claims are out.

On Friday, June 10 at 8:30 AM, the blockbuster US Core Inflation Rate is announced. More importantly, the new dinosaur movie, Jurassic World: Dominion, is released. At 2:00 the Baker Hughes Oil Rig Count are out.

As for me, this is not my first Russian invasion.

Early in the morning of August 20, 1968, I was dead asleep at my budget hotel off of Prague’s Wenceslas Square when I was suddenly awoken by a burst of machine gun fire. I looked out the window and found the square filled with T-54 Russian tanks, trucks, and troops.

The Soviet Union was not happy with the liberal, pro-western leaning of the Alexander Dubcek government so they invaded Czechoslovakia with 500,000 troops and overthrew the government.

I ran downstairs and joined a protest demonstration that was rapidly forming in front of Radio Prague trying to prevent the Russians from seizing the national broadcast radio station. At one point, I was interviewed by a reporter from the BBC carrying this hulking great tape recorder over his shoulder, as I was the only one who spoke English.

It seemed wise to hightail it out of the country, post haste, as it was just a matter of time before I would be arrested. The US ambassador to Czechoslovakia, Shirley Temple Black (yes, THE Shirley Temple), organized a train to get all of the Americans out of the country.

I heard about it too late and missed the train.

All borders with the west were closed and domestic trains shut down, so the only way to get out of the country was to hitch hike to Hungary where the border was still open.

This proved amazingly easy as I placed a small American flag on my backpack. I was in Bratislava just across the Danube from Austria in no time. I figured worst case, I could always swim it, as I had earned both, the Boy Scout Swimming, and Lifesaving merit badges.

Then I was picked up by a guy driving a 1949 Plymouth who loved Americans because he had a brother living in New York City. He insisted on taking me out to dinner. As we dined, he introduced me to an old Czech custom, drinking an entire bottle of vodka before an important event, like crossing an international border.

Being 16 years old, I was not used to this amount of high-octane 40 proof rocket fuel and I was shortly drunk out of my mind. After that, my memory is somewhat hazy.

My driver, also wildly drunk, raced up to the border and screeched to a halt. I staggered through Czech passport control which duly stamped my passport. I then lurched another 50 yards to Hungary, which amazingly let me in. Apparently, there is no restriction on entering the country drunk out of your mind. Such is Eastern Europe.

I walked another 100 yards into Hungary and started to feel woozy. So, I stumbled into a wheat field and passed out.

Sometime in the middle of the night, I felt someone kicking me. Two Hungarian border guards had discovered me. They demanded my documents. I said I had no idea what they were talking about. Finally, after their third demand, they loaded their machine guns, pointed them at my forehead, and demanded my documents for the third time.

I said, “Oh, you want my documents!”

I produced my passport, When they got to the page that showed my age they both started laughing.

They picked me and my backpack up and dragged me back to the road. While crossing some railroad tracks, they dropped me, and my knee hit a rail. But since I was numb, I didn’t feel a thing.

When we got to the road, I saw an endless stream of Russian army trucks pouring into Czechoslovakia. They flagged down one of them. I was grabbed by two Russian soldiers and hauled into the truck with my pack thrown on top of me. The truck made a U-turn and drove back into Hungary.

I contemplated my surroundings. There were 16 Russian Army soldiers in full battle dress holding AK-47s between their legs and two German Shepherds all looking at me quizzically. Then I suddenly felt the urge to throw up. As I assessed that this was a life and death situation, I made every effort to restrain myself.

We drove five miles into the country and then stopped at a small church. They carried me out of the truck and dumped me and my pack behind the building. Then they drove off.

The next morning, I woke up with the worst headache of my life. My knee bled throughout the night and hurt like hell. I still have the scar. Even so, in my enfeebled condition, I realized that I had just had one close call.

I hitch-hiked on to Budapest, then to Romania, where I heard that the beaches were filled with beautiful women. My Italian let me get by passably in the local language.

It all turned out to be true.

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

One More Off to College

![]()

If You Don’t Like the Price, Don’t Use it

Mad Hedge Technology Letter

November 30, 2020

Fiat Lux

Featured Trade:

(THE GREEN LIGHT FOR E-COMMERCE)

(AMZN), (W), (OSTK), (WMT), (TGT), (MELI), (EBAY), (CRM), (ADBE)

Data from Adobe Analytics is in and it suggests that e-commerce is delivering on its expected domination over retail.

I can’t ignore the helping hand of the pandemic which has deemed pedestrian shopping malls too dangerous to set foot in and for analog businesses that survive, it is essentially coming down to whether a digital footprint has been developed or not.

There is only so much a PPP loan can do to paper over the cracks of a non-digital business.

At some point, CEOs will need to wake up and understand that survival means a migration to digital.

Forecasts show that Black Friday online sales will register between $8.9 billion and $10.6 billion, which represents growth of up to 42% year over year.

The data firm expects Black Friday and Cyber Monday to become the two largest online sales days in history as consumers shift more spending toward e-commerce amid the public health crisis.

By last Friday morning, Salesforce projected online sales in the U.S. for Black Friday to spike 15% to $11.9 billion.

The truth is that many shoppers got their shopping done even before Thursday and Friday with digital sales in the U.S. spiking 72% year over year on Tuesday and were up 48% on Wednesday.

E-commerce companies front-ran the actual holidays to eke out more profit in the anticipation of competitors offering earlier sales.

According to Adobe, Thanksgiving sales hit a record $5.1 billion, up 21.5% over 2019 and this aggressive growth rate can be considered the new normal.

Smartphones continued to account for an increasing segment of online sales, with this year’s $3.6 billion up 25.3%, while alternative deliveries — a sign of the e-commerce space maturing — also continued to grow, with in-store and curbside pickup up 52% on 2019.

Shopify said that over 70% of its sales are being made using smartphones.

What are the hot gift items?

Electronics, tech, toys, and sports goods being the most popular categories — at the right price will help retailers continue to experience elevated sales volume.

Adobe said a survey of consumers found that 41% said they would start shopping earlier this year than previous years due to much earlier discounts.

This season is headed for record-breaking levels as consumers power online sales for both holiday gifts and necessities.

Not all big-box retailers were open over the holidays and getting that extra surge from the likes of daily needs such as paper towels, cleaning products, and garbage bags has boosted the top-line growth as well.

We have seen the perfect storm of elements fuse together to help the bottom line records of the likes we have never observed.

Comps will be difficult to beat next year if the vaccine solution starts coming online by next winter and considering that the worst economic damage is behind us.

Next year, the U.S. consumer will have more to spend setting up a tough but possible beat to next year’s numbers along with the high likelihood that tech stocks will experience another leg up.

There will be a lot happening in between, such as a new U.S. administration that is primed for a different economic polic; but it’s impossible not to love the narrative of certain e-commerce companies such as Shopify (SHOP), MercadoLibre (MELI), Target (TGT), Walmart (WMT), Etsy (ETSY), Wayfair (W), eBay (EBAY), Overstock.com (OSTK), Amazon (AMZN) and the companies that measure their data like Salesforce (CRM) and Adobe (ADBE).

If we ever could anoint when a year became the year of technology, then this would be it in 2020.

The base case for next year is that the borders and states will still grapple with the virus and the knock-on effects to society, economy, and politics as the capacity to produce the virus won’t meet demand for at least a year.

Tech stocks are primed to outperform non-tech next year and even though multiples are high, the momentum suggests that this group of stocks will be the gift that keeps giving as the Fed has offered generous liquidity conditions to tech investors.

Mad Hedge Technology Letter

November 23, 2020

Fiat Lux

Featured Trade:

(COMMUNICATIONS HAS NEVER BEEN MORE IMPORTANT)

(TWLO), (TWTR), (CRM), (SQ), (AMZN), (OSTK), (W)

Growth is not dead as last week’s tech rally shows that tech stocks still have their allure.

One tech growth stock that I am absolutely in-love with is communications-as-a-platform cloud stock Twilio who services Airbnb and Uber as the software that connects the users to their staff.

The ability to communicate with customers in real time has never been more urgent in a fast-paced world, especially in the software-centric economy.

From food delivery to booking hotels, from customer service to password resets, literally anything revolves around the ability to connect reliably and rapidly.

Many people in 2020 still do not even know what Twilio (TWLO) does!

They are the dark horse cloud company that nobody has heard of.

The company provides the software building blocks that lets developers embed Twilio's communication technology in their apps, messaging systems, emails, and more. It also streamlines the process so it can be accomplished in a matter of hours, rather than weeks or months.

Here’s an insanely applicable example: The update you received from Lyft regarding your ride, the text messages and reservation confirmation you got from Airbnb, the customer service interactions with Disney's Hulu, and the booking confirmation from your restaurant via Yelp? These were delivered by Twilio's technology.

In pandemic third quarter, Twilio's revenue climbed 52% year over year, while also avoiding a loss, swinging from a loss in the prior-year quarter.

The company reported 208,000 active customers, up 24% year over year.

There is no mistake that these types of cloud stocks are in the vein of Twitter (TWTR), Salesforce (CRM), Square (SQ), and so on and at the vanguard of the hullabaloo of growth stocks.

Why are growth stocks so popular?

Growth stocks are companies that increase their revenue and earnings faster than average.

A growth company relentlessly develops an innovative product or service or at the top of the pack of fastest-growing industries and unsurprisingly that is technology, and that fact won’t change for generations.

Firms growing faster than average for long periods tend to be rewarded by the market, and this is why there has been a massive migration to growth stocks that has enriched shareholders of Apple (APPL), Facebook (FB), Netflix (NFLX), and so on.

Growth also begets additional growth and the faster they grow, the bigger the returns can be.

They are also more expensive than the average stock in terms of metrics like price-to-earnings, price-to-sales, and price-to-free-cash-flow ratios, but investors look past this in an age of expanding liquidity which is the catalyst that breathes even more momentum into these stocks.

US growth stocks secure a premium just for the possibility they will fulfill their parabolic growth potential.

Capitalizing on powerful long-term trends can grow their sales and profits for many years, and the following are a list of seminal trends that all involve technology data points as the secret sauce.

These powerful trends will last decades giving you plenty of time to claim your share of the profits they create.

Rank growth companies with strong competitive advantages. Otherwise, their business might fail.

Some competitive advantages are:

Pinpointing large addressable markets means a larger opportunity to secure higher revenue and Twilio is occupying a spot at the intersection of generational, long-term trends and almost unfair competitive advantages.

The underlying shares have rocketed this year as communications has never been more important. This is a great buy and hold stock for the long term because trading short term is difficult with its elevated volatility.

Mad Hedge Technology Letter

July 8, 2020

Fiat Lux

Featured Trade:

(THE ONLY RETAIL PLAY YOU WANT TO KNOW)

(OSTK), (W)

As U.S. virus cases explode, the shelter-in-home trade is back in full force, meaning investors need to look at Overstock.com, Inc. (OSTK).

We are talking about parabolic action in a stock price with shares up 16% yesterday alone and even doubling in the last 40 days.

The U.S. is now hugging that 50,000 cases per day mark and it is only a matter of time until the health crisis spirals so far out of control that everybody will be back inside online shopping again on their touchpads.

And if it doesn’t get that bad, it certainly will trend in that direction which is why Overstock.com will be back in vogue.

The short-term performance validates my thesis that Overstock.com is going through a renaissance as it goes from the edge of the periphery to a tech darling.

Revenue in April and May were up 120% year-over-year as the company expects to see continued momentum in the near-term, Overstock CEO Jonathan Johnson remarked during a Fox Business interview.

Consumers "still aren't ready" to return to furnishing stores to test couches, beds, and other furniture due to the coronavirus pandemic, Johnson said. The online venue clearly remains "the place" to buy home furnishing items.

Overstock.com wholeheartedly believes they will experience "strong" double-digit growth rate through the summer.

The mother of all tailwinds has legs and you might think of Overstock as a smaller e-commerce store in the mold of Amazon.com, but they have really taken the business model up a notch.

Overstock started out as a pure play on online retail operations, based on a low-cost business model that involves the selling of excess inventory from factories and other retailers at discounted prices.

Overstock.com Inc. became a household name as an e-commerce pioneer, but in recent years, excitement in the investment community was focused more on the company’s blockchain efforts.

The pandemic changed the world and the company is dusting off its e-commerce playbook.

Mushrooming sales at Overstock’s retail business have helped transform a timid stock to one of the Covid-era’s best performers, an irony for a division that had long been considered for sale.

Overstock shares have gained nearly 11-fold since closing at a record low on March 16, and this is just the beginning as the administration hopes to convince the population that the virus doesn’t need any managing.

Sweeping the carnage of the virus under the carpet makes no sense, and with the internet disseminating information and disinformation, will Americans be inclined to believe the virus has no teeth?

It’s hard to wrap our heads around the US government’s response to a global health crisis and the bountiful harvest the tech sector is collecting.

They hardly needed it.

Tech was crushing it before the pandemic.

If you strip out the earnings of the Big 6 of Facebook, Amazon, Apple, Microsoft, Netflix, and Google, there is no earnings growth for the last five years in any sector.

Stocks went up purely based on excess liquidity and a monstrous corporate tax break.

Then the administration’s disregard of the health crisis gifted accelerating revenue to the tech sector while every other sector was cruelly pillaged.

Granted, the U.S. administration had no intention to hammer non-tech businesses, but that is exactly what is playing out.

So now this is what you get – a once sluggish tech stock like Overstock.com turning into an e-commerce pandemic play on steroids overnight.

The stock is frantically gapping up almost every day and it was just a few years ago when the company was really grasping at straws by jumping on the cryptocurrency bandwagon.

The U-turn by CEO Jonathan Johnson says it all as he has “no interest” in selling the e-commerce business which he was desperate to sell last month.

And just based on the news that Johnson didn’t sell the e-commerce unit last month, the stock doubled.

It’s unfathomable times in the tech sector.

The decor and home improvement market could end up benefiting from a total of $200 billion in an annual tailwind because of the pandemic’s effect on consumers.

If consumers are looking for a similar e-commerce play, then Wayfair (W) should fit the bill.

It’s getting to the point where if the late first wave or early second wave hits harder than the initial wave in March, there might be nowhere else to buy home furnishings and décor but at e-commerce stores.

I am bullish Overstock.com