Below, please find subscribers’ Q&A for the December 11 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Lake Tahoe, Nevada.

Q: I was assigned options—called away on both my short-call positions in BlackRock (BLK) and Bank of America (BAC).

A: What you do there is call your broker and exercise your long to cover your short; that should get you 100% of the profit 10 days ahead of expiration, and that is the best way to get out of that position. If you get hit with the dividend, then you're at break-even on the total trade. The way to get around this is you have 10 positions, including several non-dividend paying positions, so you don't have a call-away risk. You really only have about a 1 in 100 chance to get called away, so it's worth doing. If the worst case is you break even, the best case is you make 15% or 20% on the position in a month. That is worth doing.

Q: What do you think of the situation in Syria?

A: We don't know. For us, it's a huge win because it eliminates the last Russian position in the Middle East. They have lost Egypt, Syria, Iraq, and at one point Algeria—so they have no more positions in the Middle East. They lose all their air bases, military bases, and naval bases in Syria, and they also lose their only warm water port in the Mediterranean. It happened because they couldn't afford to draw troops away from Ukraine to help support Syria. Given the choice between Syria and Ukraine, they'll pick Ukraine. It is another argument for the US to maintain support for Ukraine.

The trouble is in the Middle East, whenever you get a chance, you often end up getting somebody else that's worse. Did we just trade one terrorist for another one? We'll have to wait and see. Fortunately, this war didn't cost us any money. It cost Russia a lot. We had no troops in Syria and no weapons commitments, so we got off easily on this one. It’s probably the most important foreign policy achievement of the last four years.

In the meantime, we're destroying all their weapons stockpiles, just in case the new people coming in are bad guys. We'd rather not wait until after they identify themselves as bad guys—we might as well destroy all the weapons now while nobody is defending them. So, as I speak, we're destroying weapons stockpiles for its ships and rocket facilities. Also, this is a huge loss for Iran because they lose easy sea access to Gaza. They used to just truck weapons to the coast in Lebanon, put them on a boat, and send them to Gaza. Now, they have to go all the way around Africa to supply Gaza. So basically it's a huge win for us, and I'll write more about that in the Monday letter.

Q: Do the spread positions need to be actively closed out to achieve profits?

A: No, they don't. You don't have to touch them. That's the beauty of these positions. All ten I expect to expire in the money at maximum profit point, and on the following Monday morning opening, you will find that the margin is freed up, the cash profit is credited to your account, and you're in a 100% cash position. So don't do anything, even if your broker will tell you to individually buy and sell the individual legs and wipe out your profit. I sent out a research piece on this today about how to handle when calls are called away.

Q: I sold BlackRock (BLK) last week because Schwab called and warned me I could owe $6,000 due to the dividend. They did not suggest I close my long position.

A: Again, it goes back to how to handle option call-aways. The only reason they call you is to eliminate any liability for Charles Schwab because, in the past, people would get options called away, they'd say my broker never told me, and they sued the broker. So, the reason they emailed you and called you with warnings is to avoid liability for themselves. In actual fact, only 1 out of 100 different options actually get called away. It's done randomly by a computer, and you're far better off holding the position. And then, if you do get called away, use your long to exercise your short. It's a perfectly hedged position, so you have no actual outright risk. The only real risk is if you don't check your email every day and you don't know you've been called away, so you don't call your broker to exercise your long to cover your short.

Q: Do you envision other countries trending towards more tariffs? How would that affect global growth?

A: Any time we raise a tariff on another country, they're going to raise by an equal amount, and it becomes a perfect growth destruction machine. That's why every economic agency in the world is predicting lower growth for next year.

Q: Why are stocks so expensive? Can the high prices be an impediment for new investors to participate or not?

A: It's obviously not an impediment because we're at an all-time high, and we keep going to new all-time highs. Most investors, not just a few, are still underweight stocks, and they're chasing the market. I predicted this would happen all year basically, and now it's happening, and we're 100% invested in making a fortune. So that's what happens when you make big predictions far into the future, and they happen.

Q: What do you think about meme stocks like GameStop (GME)?

A: Don't bother with the meme stocks like GameStop when the good stuff like Tesla (TSLA), Meta (META), and Amazon (AMZN) are going up like a rocket. Why buy the garbage when the high-quality stuff is doing well? And, of course, most of the people buying that stuff, the meme stocks, are kids who don't know what the good stuff is, but they'll find out someday.

Q: If you like Japanese cars, what do you think of Korean cars and, therefore, those companies’ stocks?

A: I don't like them. When you take your Tesla in for a service, sometimes you get a KIA in return. Ouch. You can literally hear every bolt rattle as you drive down the freeway, and you leave behind a trail of parts; the quality difference is enormous.

Q: How do you determine the limit price on spread trades?

A: I don't like making less than a 5% profit in a month. It's just not worth the risk. So let's say if I do a trade alert at $9.00, I'll create a spread of, say, $9.00, $9.10, $9.20, $9.30, $9.40, and that's it. We tell people to not pay more than $9.40. Before we told people not to do that, they used to buy at market, and they would end up paying $10.00 for a $10.00 spread, and it is absolutely not worth it. That is the reason we do that.

Q: Ihave trouble getting your recommended price.

A: When we put out a trade alert, and 6,000 people are trying to do it at once, you'll never get the recommended price. You may get it at the close because a lot of the high-frequency traders that pile into these positions and pay the maximum price have to be out of that position by the end of the day, so they often dump their positions at the close. And if you just leave your limit order in there, it'll get filled. If it doesn't get filled at the close, it will get filled at the opening the next morning. So that's why I'm telling people on every alert now to put in a spread, put in good-until-cancelled orders, and most of the time, you'll get some or all of those orders done. That is a good way to make money; if you don't believe me, just go to our testimonials page (click here), where hundreds of people have sent in recommendations on their experience.

Q: What do you think about crypto here (BITO)?

A: I wouldn't touch it with a 10-foot pole. The time to get involved in crypto was when it was at $6,000 two years ago, not at $100,000 now. And when the quality is trading and rising up almost every day, why bother with crypto? You'd never know if your custodian is going to steal your position. And by the way, if anyone knows an attorney expert at recovering stolen crypto, please send me their name because I have a few clients who took someone else's advice, invested in crypto, and had their accounts completely wiped out.

Q: Should I bet big on oil stocks (USO) because of the possible deregulation starting in 2025?

A: Absolutely not. “Drill, baby, drill” means oil glut—lower oil prices, which is terrible for oil companies, so you shouldn't touch them. The only plus for oil under the new administration is they'll probably refill the Strategic Petroleum Reserve in Texas and Louisiana from the current 425 million barrels to 700 million barrels by buying on the open market and enriching the oil companies.

Q: Would you sell long-term holds in pharma stocks?

A: No. If it's a long-term hold, your holding will survive the new administration. They'll probably go back up starting from a year going into the next election unless they find ways to deal with the current administration. But if you're in the vaccine business and the head of Health and Human Services is a lifetime anti-vaxxer, that is not going to be good for business, no matter how you cut it, sorry.

Q: Why is Walgreens (WBA) doing so poorly?

A: Terrible management and too late getting into online commerce. The service there is terrible. Every time I go to Walgreens to get a prescription filled, there's a line a mile long. It seems to be a dying company. Someone actually is making a takeover offer for the company today, so I would stand aside on that.

Q: Is Tesla (TSLA) risky?

A: Any stock that's tripled in four months is risky. But the rule of thumb with Tesla is that it always goes up more than you expect and then down more than you expect. Here is where high risk means high reward. My $1,000 target is now looking pretty good.

Q: If you're receiving Global Trading Dispatch, do you get the stock option service?

A: Yes, every trade alert we send out gives you the choice of a stock, an ETF, or an option to buy to take advantage of that alert.

Q: The EV stock Lucid (LCID) just got an analyst upgrade, but the chart looks terrible. Should I buy this cheap stock?

A: Absolutely not. Never confuse “gone down a lot" with “cheap.” Lucid only exists because it's supported by the Saudi royal family. They own about 75% of the company. They have no chance of ever competing with Tesla. Period. End of story.

Q: I have LEAPS on Google (GOOG), Amazon (AMZN), and Microsoft (MSFT). They expire in January, February, and March.

A: I would keep all of those—those are all good stocks. I expect them to keep rising at least until January 20th. After that, the Trump administration may announce antitrust actions against all three of these companies, but you'll probably have most of your profit by then. So from here on, if I had longs in all of these companies, I would definitely run them over the holidays because you'll probably get another pop sometime in January.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, TECHNOLOGY LETTER, or JACQUIE'S POST, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

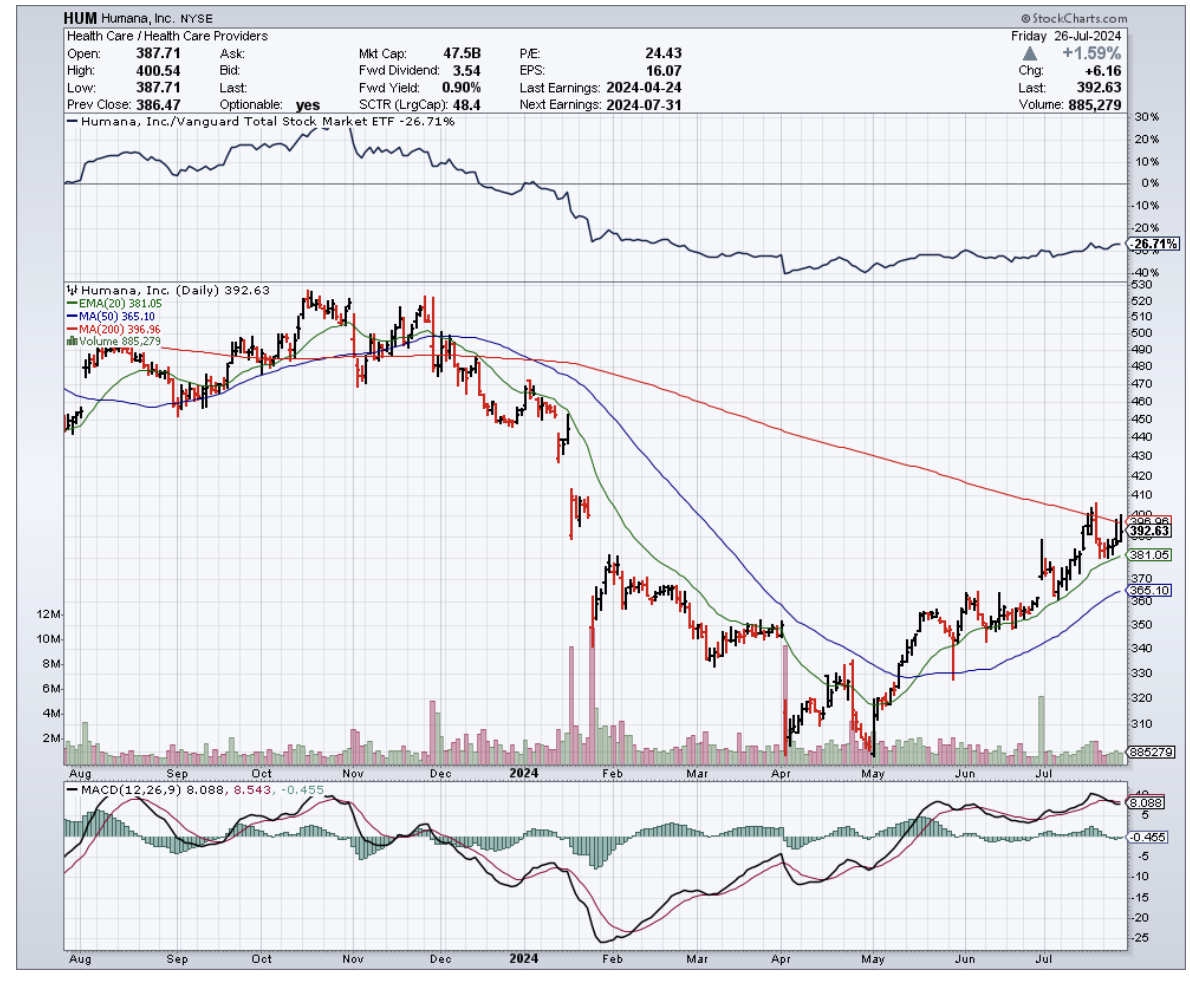

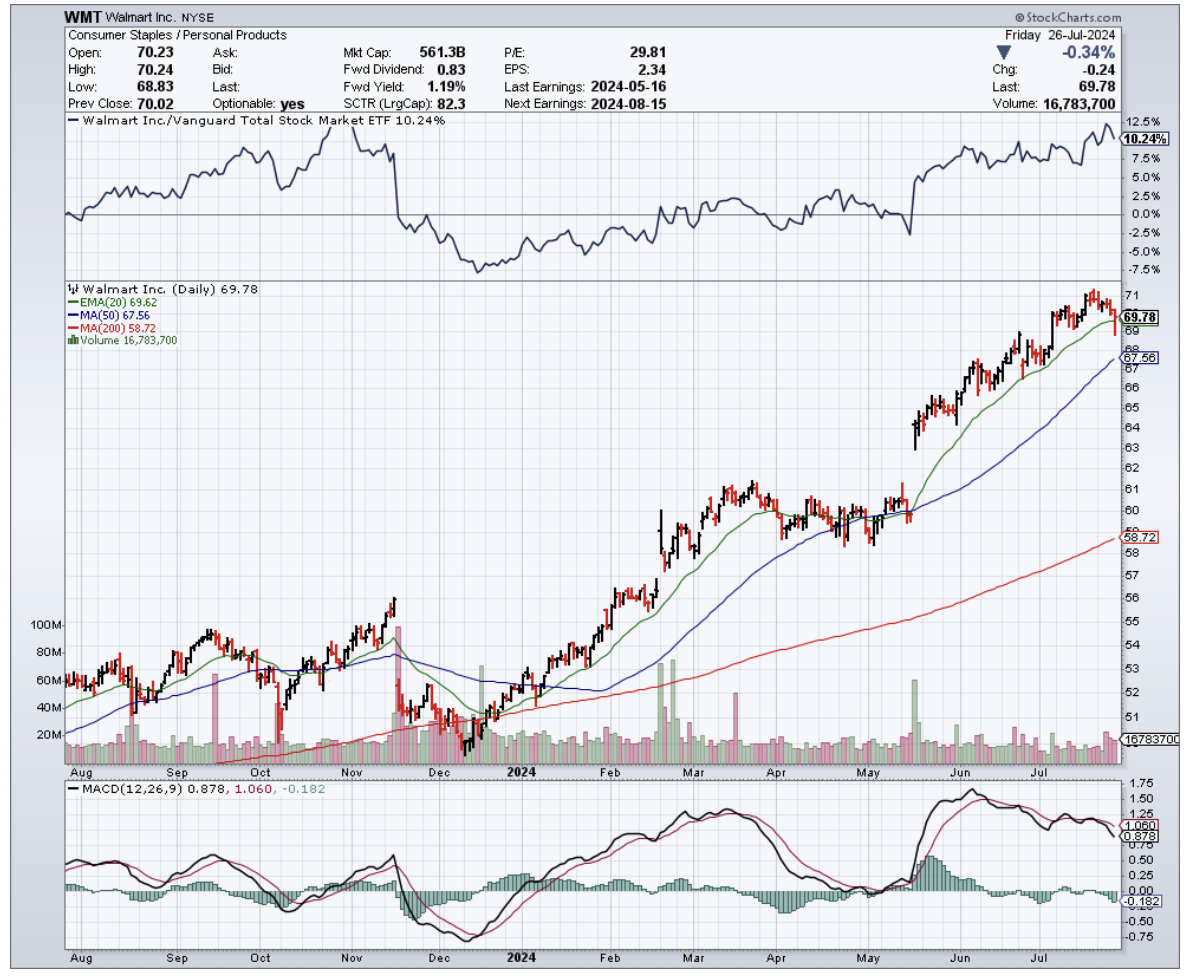

In my years of covering the markets, from the trading floors of Tokyo to the halls of power in Washington, I've seen my fair share of unexpected partnerships.

But the recent tie-up between Walmart (WMT) and Humana (HUM) has me sitting up and paying attention.

That’s right. Walmart, the king of rollbacks and home of the $1 hot dog, has found a new tenant for the vacant spaces that used to house its healthcare business: Humana's CenterWell health clinics.

Humana, as you know, is one of the biggest players in the Medicare Advantage game, and is setting up shop in 23 Walmart Supercenters across Florida, Georgia, Missouri, and Texas.

And they're not just dipping their toes in the water – they're diving in headfirst, with plans to have these clinics up and running by the first half of 2025.

Now, I know what you're thinking. "John, why should I care about some dusty old retail giant like Walmart getting into bed with a health insurance company?"

Let me tell you why.

Humana's Q1 2024 earnings were nothing to sneeze at, with revenues growing 11% year-over-year to a whopping $29.6 billion.

And while the company did revise its full-year EPS guidance downward, it maintained its outlook for adjusted EPS and even revised its membership growth in MA plans upward.

This is a big deal, folks. Medicare Advantage plans have been the bread and butter of Humana's business model, underpinning the company's phenomenal share price gains from $25 per share in 2010 to over $550 in late 2022.

With the population aging faster than fine wine, the demand for senior-focused healthcare services will only grow.

But Humana isn't the only one benefiting from this partnership.

For Walmart, renting out these spaces to CenterWell allows them to recoup some of the infrastructure investments they made in building out their 51 Walmart Health clinics, which they recently shut down due to profitability challenges.

It's like finding a roommate to help pay the rent after your startup goes belly up.

But the healthcare industry is like a giant game of Jenga, with players constantly pulling out blocks and hoping the whole thing doesn't come crashing down.

Just look at Walgreens Boots Alliance (WBA), another retail giant that recently announced the closure of 150 of its in-store clinics due to profitability challenges. It's a stark reminder of how difficult it can be to make a buck in this business.

That's why Walmart's pivot to a partnership model with Humana is so intriguing.

By leasing out pre-equipped facilities to CenterWell, Walmart is essentially letting Humana handle the nitty-gritty of patient care while still maintaining a presence in the rapidly growing primary care industry.

It's like having your cake and eating it too, without having to worry about the pesky details of actually baking the cake.

As expected, Walmart and Humana aren't the only ones making moves in the healthcare space.

CVS Health (CVS) and UnitedHealth Group (UNH) are also betting big on primary care, with CVS acquiring Oak Street Health for $10.6 billion and UnitedHealth's Optum division going on an acquisition spree to expand its network of physicians and healthcare providers.

Then, there’s the meteoric rise of telehealth during the pandemic. Companies like Teladoc Health (TDOC) saw their revenues skyrocket as patients turned to virtual care in droves.

While growth has slowed down since the height of the pandemic, telehealth is still a force to be reckoned with and could potentially disrupt traditional brick-and-mortar clinics.

So, what does all this mean for us?

Well, if you're an investor looking to get in on the action, you've got plenty of options. From established players like Humana and UnitedHealth to up-and-comers like Oak Street Health and Teladoc, there's no shortage of companies vying for a piece of the healthcare pie.

With an aging population, rising healthcare costs, and a growing focus on preventative care and chronic disease management, the demand for innovative healthcare solutions is only going to increase in the coming years.

And who knows, maybe one day we'll all be getting our annual check-ups at the local Walmart, with a side of low-priced toilet paper and a jumbo bag of Cheetos.

Stranger things have happened in the wild world of healthcare.

Once upon a time, in the not-so-distant 1980s, national pharmacy chains sprouted up across the American landscape like mushrooms after a rainstorm.

They nestled into every nook and cranny of our lives, from the bustling urban streets to the tranquil rural towns, becoming as ubiquitous as the local diner.

Fast forward to 2010, and their numbers had climbed from 18,600 to a staggering 22,500.

It was a golden era for these giants. Like a high school jock on prom night, Walgreens (WBA) and CVS Health (CVS) were on top of the world. Their share prices did the financial equivalent of bench pressing 300 pounds, ballooning to about 14 times their original size between 1995 and 2015, while the S&P 500 merely did a respectable fourfold increase.

Walgreens' wallet got a lot thicker, going from a total revenue of $42.2 billion in 2005 to a hefty $103.4 billion a decade later.

CVS wasn't far behind, with its treasure chest growing from $37 billion to an eye-watering $153.3 billion.

But as the saying goes, what goes up must come down. Today, the once invincible giants are feeling the squeeze, like a middle-aged man trying to fit into his high school jeans.

The tale of woe includes Rite Aid's (RADCQ) bankruptcy bow in October 2023, CVS's share price taking a more than 30% nosedive over two years, and pharmacists so fed up they're leaving their posts faster than rats from a sinking ship.

The crux of their dilemma? A dwindling stream of reimbursement rates from the pharmacy benefit managers, akin to trying to drink a milkshake through a cocktail straw.

Walgreens saw its adjusted operating income from its U.S. retail pharmacy division shrink by 31.1%, from $5.4 billion in 2016 to a more modest $3.7 billion in 2023.

In a similar bind, CVS saw its profits dip, leading to a drastic measure: closing up shop on hundreds of stores.

Despite these turbulent times, the enduring importance of chain pharmacies in the U.S. healthcare system cannot be overstated. They continue to play a crucial role, dispensing everything from life-saving medications to the latest in blood pressure tech.

The question now is, what's next for these once mighty titans? So far, we can see that both CVS and Walgreens are attempting a Hail Mary, broadening their healthcare horizons in hopes of justifying their sprawling presence across the nation.

Over the coming years, a significant transformation is expected to happen to Walgreens and CVS, with the brands likely to streamline their presence. With an extensive network of physical outlets, these companies are confronted with the inevitable: the need for a massive workforce and substantial resources, all of which escalate operational costs and complexities.

In an age where efficiency is king — think Starbucks (SBUX) with its pivot to drive-thru exclusives — it stands to reason that Walgreens and CVS might steer in a similar direction.

Actually, Walgreens has already dabbled in new solutions like drone delivery, a venture that aligns perfectly with the future of quick and efficient distribution of essentials, including medicines, to its customer base.

The next thing to consider is how dramatic this downsizing will be. Looking a decade ahead, we can anticipate a considerable shrinkage in their storefronts, possibly with a shift towards more compact, delivery- and pick-up-friendly formats.

As they move forward with these changes, one thing remains clear: the landscape of American healthcare and retail is evolving, and with it, these pharma giants need to adapt or risk being left behind in the annals of history, remembered as nothing more than relics of a bygone era.

The stories of these national pharmacy chains are far from over, but the next chapters promise to be as unpredictable as they are compelling. So grab your popcorn. This is one show you won't want to miss.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-02-13 12:00:402024-02-13 10:54:57Pill Pushers in Peril

Today, let’s talk about something that might make dividend enthusiasts a tad uncomfortable — when beloved companies take an axe to dividends. Yeah, it’s a bummer.

Imagine you’re on a steady course, relying on those dividends to keep flowing in, and suddenly, a storm hits. That's what happened when Walgreens Boots Alliance (WBA) rocked the boat by slashing its dividend by a whopping 48%. Ouch, right?

But, let's not dwell on the past. Instead, how about we scout for a stock that’s less likely to leave us in such a pickle?

Spoiler alert: no stock comes with a no-risk guarantee, but sticking with big names sporting robust businesses and hefty moats might just do the trick. And where better to look than the evergreen healthcare sector?

That’s where Johnson & Johnson (JNJ) comes in.

This old-timer isn’t just another name in the pharma game; it’s practically royalty, with a lineage stretching back nearly 140 years.

The year 2023 was a period of change for JNJ, as it waved goodbye to slow movers like Band-Aid and Tylenol by spinning off its consumer health division into Kenvue, netting a cool $13 billion from Kenvue’s (KVUE) market debut.

And yes, JNJ still keeps a watchful eye on Kenvue with a 9.5% stake.

Digging into the numbers, JNJ boasted a hefty $21 billion in sales in the third quarter of 2023 alone, marking a 7% jump from the previous year, with profits tallying up to a cool $4.3 billion.

The pharmaceutical division, with stars like Darzalex and Stelara, brought home the bacon, contributing $14 billion to the total revenue.

Not to be outdone, the medical device division strutted its stuff with a 10% sales hike, raking in $7.5 billion.

Here’s the deal with JNJ: it’s like that reliable old friend you can count on for the long haul. It’s not just resting on its laurels, though.

JNJ has been on the prowl, having acquired Abiomed, known for the world's smallest heart pump, and eyeing Ambrx Biopharma (AMAM) for future innovations.

Plus, with a 60-year streak of not just paying but boosting its dividend, JNJ is like that steady drummer in a rock band, keeping the beat alive and kicking, having increased its dividend by 80% over the last decade.

Still, nothing is perfect. So, let’s not sugarcoat it — JNJ has its share of headaches. The Inflation Reduction Act is looking to play hardball on drug prices, which could mean thinner pie slices for JNJ’s top sellers.

And then there’s the talc saga, a storm JNJ is still navigating with a $700 million settlement not putting a full stop to the legal drama, considering there are still thousands of personal injury lawsuits pending.

Yet, for all the turbulence, JNJ’s resilience is nothing short of legendary. With an AAA credit rating, it stands more solid than many sovereign states. It’s the kind of ship that keeps its course steady, no matter the weather.

So, what’s the takeaway for those hunting for dividends in the healthcare seas?

With its solid track record, including a Dividend King crown for 61 years of dividend increases, JNJ is a ship built for long voyages.

Founded in 1886, it has shown a remarkable ability to adapt and grow, charting a course for future success. It’s not promising a gold rush overnight, but as a steadfast companion on your investment journey, JNJ is as good as it comes.

Investing in JNJ is like joining a voyage with a seasoned captain at the helm. Sure, there might be choppy waters ahead, but with a history of navigating through just about any storm, JNJ is a ship you’d be wise to board.

And who knows? With its commitment to growth and a knack for bouncing back, JNJ could well be the treasure chest you’ve been searching for in the vast investment seas.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-02-01 12:00:012024-02-01 11:25:01Steady As She Goes

The battle for telemedicine dominance might have just ended before it even began.

Amazon (AMZN) just announced its all-cash plan to acquire One Medical (ONEM) for $3.9 billion, paying $18 per share.

To date, this will be Amazon’s biggest step toward the healthcare world.

With the entry of Amazon into this telehealth segment, companies like Teladoc (TDOC) and Amwell (AMWL) would need to work overtime to match the resources of the e-commerce giant.

However, Amazon’s move isn’t exactly novel considering that other FAANG companies like Google (GOOGL), Apple (AAPL), and Microsoft (MSFT) have already acquired healthcare companies.

What this move simply indicates is that Amazon has finally turned serious in its bid for a bigger piece of the healthcare market.

This isn’t even the first time Amazon decided to go beyond its retail business. It has a pretty diverse portfolio including Amazon Web Services, a cloud infrastructure service, and even Whole Foods.

However, the decision to aggressively pursue the $800 billion healthcare industry might just be what Amazon needs to really move the needle.

In 2018, Amazon shelled out roughly $1 billion to buy an online pharmacy called PillPack which led to the launch of virtual Amazon Care clinics.

On that same year, the e-commerce company also pursued a joint venture, dubbed Haven, with Berkshire Hathaway and JPMorgan Chase. Unfortunately, that plan didn’t pan out and was eventually shut down.

Buying One Medical at a premium of 77%, Amazon beat other interested bidders including CVS (CVS), Walgreens (WBA), and UnitedHealth (UNH).

It’s still unclear what Amazon plans with One Medical. The e-commerce giant might add it to its Amazon Care brand or let it operate independently.

One Medical is a membership-based platform, which is backed by the Carlyle Group (CG) and managed under 1Life Healthcare.

Like most telehealth companies, it offers virtual healthcare services like virtual visits. What makes it different is that it also provides in-person checkups in accredited medical offices within the US.

One Medical’s app enables clients to schedule appointments, talk with their healthcare provider, and ask for prescriptions.

A key selling point is that the company guarantees that all the appointments start on time. Another notable feature is that users can gift a yearlong subscription to someone for $199.

Like Teladoc and Amwell, the company isn’t profitable yet. This case isn’t shocking for a relatively new field.

However, One Medical’s strategy has led to impressive revenue and membership growth.

The company’s revenue has consistently increased since its 2020 IPO. In 2021, its membership count climbed by 34% to reach 736,000.

In the first quarter of 2022, One Medical’s membership grew again by 28% and revenue jumped 109% to record over $254 million. So far, more than 8,000 companies provide One Medical services to their staff.

For 2022, One Medical projects its revenue to be between $831 million and $853 million.

Admittedly, these figures seem inconsequential when you compare them to the other sectors of Amazon’s business. For example, Amazon Web Services raked in $18.4 billion in sales in the first quarter of 2022.

Actually, One Medical’s revenue and membership growth might even look small and unimpressive compared to Teladoc, which recorded $565 million in the first quarter and has more than 54 million members in the US alone.

Undoubtedly, the healthcare market offers a mouthwatering opportunity for the likes of Amazon. It’s a lucrative industry, one of the handful that can truly make a difference in an already thriving business. Moreover, it has been highly profitable over the years.

Nonetheless, the acquisition of One Medical isn’t a foolproof plan for Amazon’s dominance in healthcare. So far, the e-commerce giant’s track record has been mixed. That doesn’t mean that the deal is a bad move. In fact, it indicates Amazon’s seriousness in making a play for the healthcare market.

Either way, the clear winner would be One Medical. Since the announcement, the stock has risen 70%.

Moreover, even if Amazon falls victim to politicization or anti-trust issues involving the deal, One Medical still has a number of suitors lined up.

Basically, it’s a win-win for this emerging telehealth company.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-07-26 17:00:102022-08-03 10:53:59Another Tech and Healthcare Crossover

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.