Global Market Comments

June 4, 2024

Fiat Lux

Featured Trade:

(The Mad June traders & Investors Summit is ON!)

(THE BIGGEST “TELL” IN THE MARKET RIGHT NOW),

(GOOGL), (FRC), (PINS), (WORK), (UBER),

(ADSK), (WDAY), (SNE), (NVDA), (MSFT)

Global Market Comments

June 4, 2024

Fiat Lux

Featured Trade:

(The Mad June traders & Investors Summit is ON!)

(THE BIGGEST “TELL” IN THE MARKET RIGHT NOW),

(GOOGL), (FRC), (PINS), (WORK), (UBER),

(ADSK), (WDAY), (SNE), (NVDA), (MSFT)

I am constantly looking for “tells” in the market, little nuggets of information that no one else notices, but give me a huge trading advantage.

Well, there is a big one out there right now. The bottom feeders are pouring into San Francisco commercial real estate, taking advantage of valuations that sometimes reach negative numbers. Owners are walking away from buildings, mailing in the keys, and going into default rather than keeping up mortgage payments. What’s worse is refinancing at today’s lofty rates. That’s what you would expect with a 36% vacancy rate.

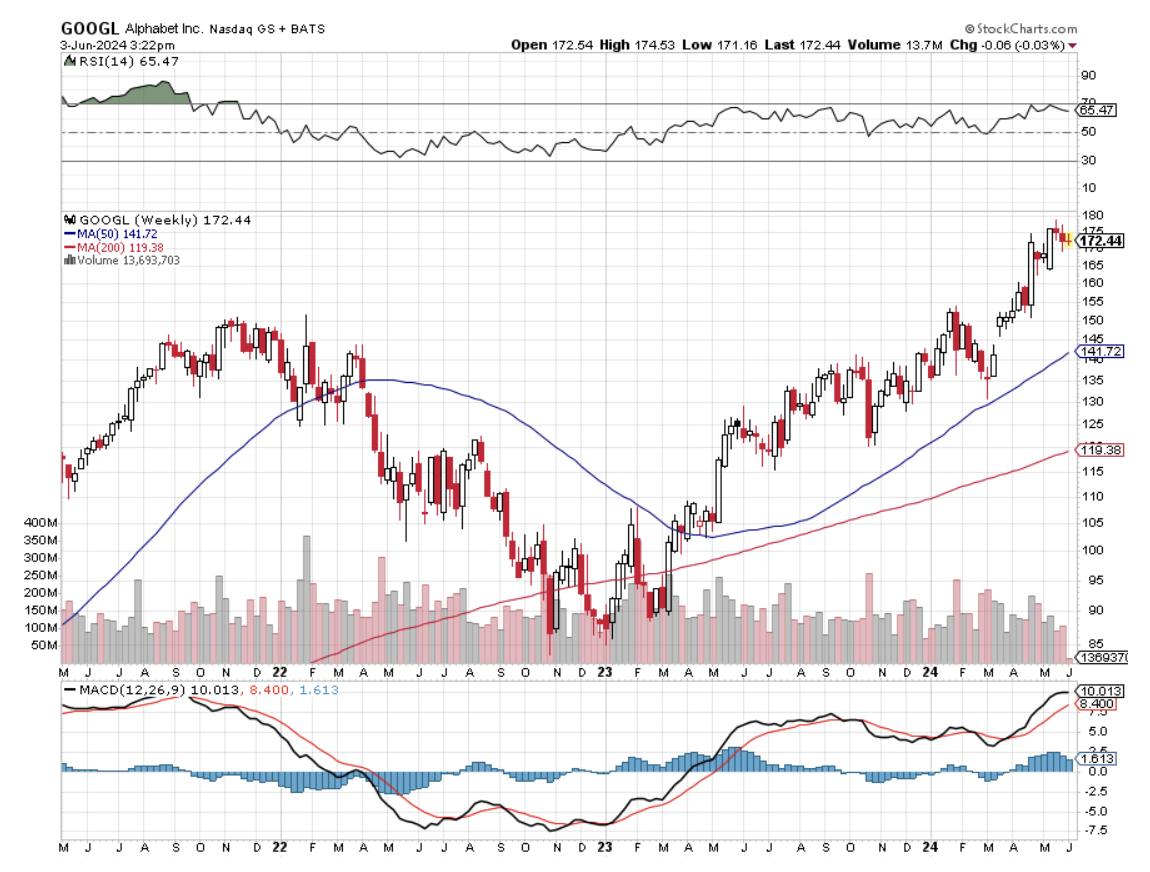

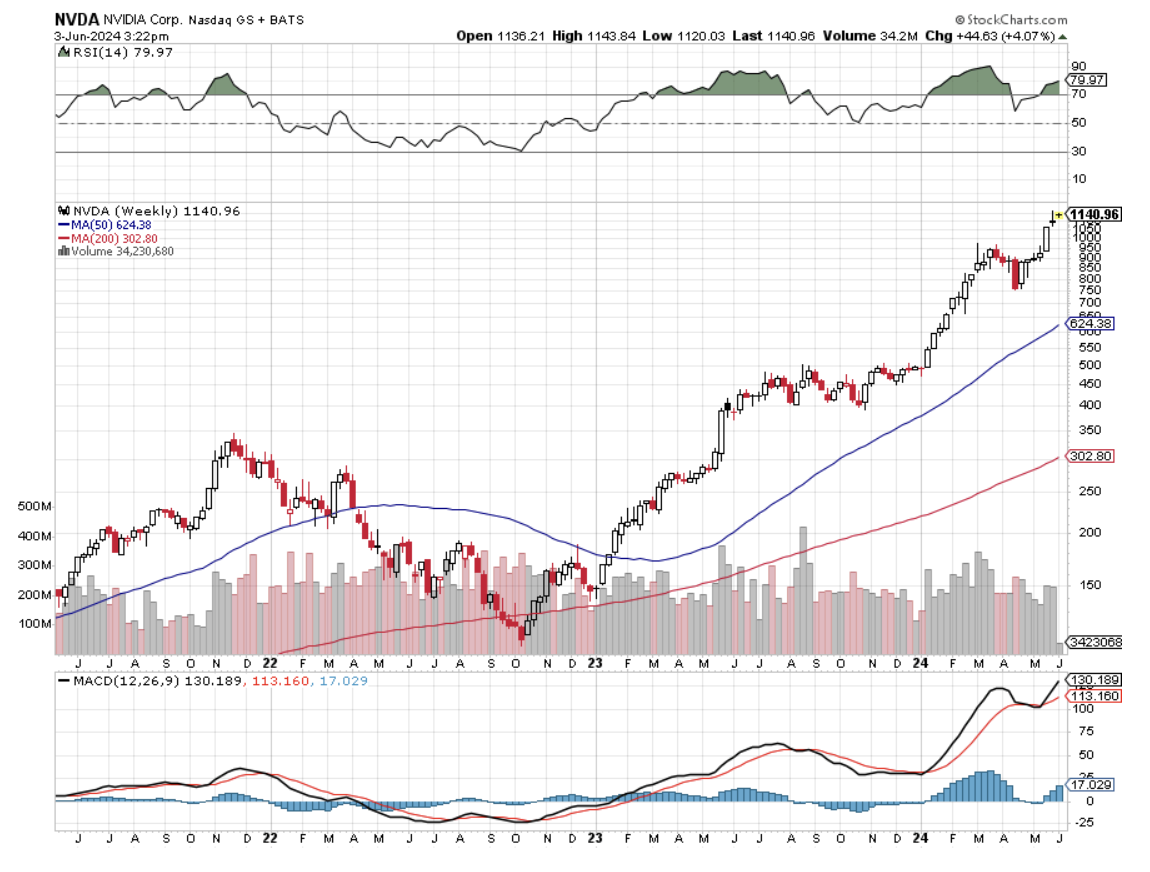

The message for you traders is loud and clear. You should be picking up the highest quality technology growth stocks on every substantial dip, such as Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOGL), Meta (META), and NVIDIA (NVDA). For they all know some things that you don’t. Their businesses are about to triple, if not quadruple over the coming decade thanks to AI. For every abandoned building out there are 200 new AI start-ups taking advantage of today’s bargain basement rates, and ALL of them use the services of the five companies above.

Technology stocks, which now account for an eye-popping 30% of stock market capitalization, will make up more than half of the market within ten years, much of that through stock price appreciation. And they are all racing to lock up the office space with which to do that….now.

San Francisco office rents reached a record pre-pandemic as the continued growth of tech — now turbocharged by nearly $100 billion in new capital raised in a series of initial public offerings — met a severe space crunch.

Asking rents rose to a staggering $84.16 per square foot annually for the newest and highest quality offices in the central business district, and citywide asking rents for such spaces, known as Class A, were up over 9% from the prior year. The citywide office vacancy rate was 5.5% in June, down from 7.4% a year ago.

In addition, local Bay Area home prices could get a turbocharger by the fall, when interest rates are expected to start falling.

San Francisco companies that have gone public continue to grow by leaps and bounds. Pinterest (PINS), Slack (WORK), and Uber (UBER) also signed office leases this year, with room for thousands of new employees.

Tech companies Autodesk (ADSK) and Glassdoor also signed deals at 50 Beale St. in the spring. In a sign of the city’s rapidly changing economy, old-line construction firm Bechtel and Blue Shield, the legacy health insurer, are both moving out of 50 Beale St. Sensor maker Samsara, software firm Workday (WDAY), and Sony’s (SNE) PlayStation video game division also expanded.

Globally, San Francisco has the seventh-highest rents in prime buildings. It’s still behind financial powerhouses Hong Kong, London, New York, Beijing, Tokyo, and New Delhi (San Francisco’s average office rents beat out New York.)

Only a handful of new office projects are being built, and future supply is further constrained by San Francisco’s Proposition M, which limits the amount of office space that can be approved each year. That is creating a steadily worsening structural shortage. Only two large office projects are under construction without tenant commitments.

Suddenly, it’s Not Crowded in San Francisco

Mad Hedge Technology Letter

May 8, 2023

Fiat Lux

Featured Trade:

(DON’T LET THESE 3 GET AWAY)

(SNOW), (WDAY), (NOW)

Even though the tech market isn’t in a renaissance, that doesn’t mean there aren’t any good choices to park capital.

I’d like to bring readers' attention to 3 cloud stocks that still have some upside.

It’s true that tech stocks no longer go up in a straight line, that auto-pilot mindset blew up spectacularly in 2022 when tech stocks finally stopped defying gravity.

The 16% the Nasdaq has gained this year is somewhat due to the expectations of a rebound and better-than-expected earnings.

With that in mind, software still has legs and it would be a shame to not go where the value is in tech.

After the big 7 behemoths, there are some tech plays that readers need to target because workloads will migrate to the cloud over the next decade.

There has been a significant shift to the cloud in recent years from legacy on-premise workloads and infrastructure. Cloud computing allows organizations to rent rather than buy IT and other functions.

Given the cost savings, scalability, flexibility, productivity gains, and improved security features, it’s obvious why this shift is happening.

These advantages mean more workloads will continue moving to the cloud. SaaS growth stocks are expanding despite the current macro uncertainty.

IT service management giant ServiceNow (NOW) is one to slide into your black leather wallet.

The company is a leader in the cloud-based IT service management and digital workflow solutions sphere. Its software helps businesses streamline operations, automate workflows and improve customer experience.

NOW recently grew revenues by 24% year-over-year last quarter.

It reported a healthy 35% free cash flow margin, which ranks in the top quartile among SaaS growth stocks.

Another one to keep an eye on is Snowflake (SNOW).

Data migration to the cloud is a secular trend that will support growth for years. Snowflake is a cloud-based data warehousing, processing, and analytics company.

Their data platform provides businesses with a scalable and flexible service for managing their data. It enables organizations to store, analyze and share large amounts of data in real-time, helping them to make better decisions and improve their operations.

Over the last five years, it has reported a net revenue retention rate above 150%.

Its platform capabilities are critical for any enterprise, and it has been winning customers in various industries.

On March 1, they reported quarterly revenues of $589 million, a 53% year-over-year growth rate.

Just as impressive, the company announced a plan to return cash to shareholders through a $2 billion buyback.

Lastly, Workday (WDAY) is a cloud-based software company that provides businesses with human capital management, financial management, and analytics solutions.

The company’s cloud software helps businesses improve workforce management, financial management, and decision-making processes.

It counts many Fortune 500 companies as customers. The company hit the 10,000 customers milestone lately with revenue increasing 19.6% year-over-year.

The runway is long for WDAY with a total addressable market for this subsector at $73 billion, respectively. Considering that organizations will continue to modernize HR and finance operations, Workday is one of the top SaaS stocks to buy to play this trend.

Global Market Comments

July 16, 2019

Fiat Lux

Featured Trade:

(THE BIGGEST TELL IN THE MARKET RIGHT NOW),

(GOOGL), (FRC), (PINS), (WORK), (UBER),

(ADSK), (WDAY), (SNE), (NVDA), (MSFT),

(POPULATION BOMB ECHOES),

(CORN), (WEAT), (SOYB), (DBA), (MOS)

Mad Hedge Technology Letter

February 19, 2019

Fiat Lux

Featured Trade:

(THE SAFE PLACE TO HIDE IN TECH),

(CSCO), (ORCL), (WDAY), (ZEN), (HUBS), (NOW), (PYPL), (VEEV), (TWLO)

Great quarter by Cisco (CSCO).

That was the first thought in my head when perusing their quarterly earnings.

It’s been hit or miss for tech companies lately and at the end of 2018, I stood up and told readers to double down on software companies and specifically enterprise software companies.

Well, Cisco has skin in this software game because corporations cultivating software need the best type of network infrastructure money can buy.

Cisco is the foundational hardware on what current high-end software is built on.

It is all rosy to have a spectacular roof design, but without a solid foundation, we have nothing more than a house of cards.

The great part about Cisco is that they are immune to the software battle taking place inside of industries because they do not build the enterprise software that is built on top of the Cisco infrastructure.

We have seen our fair share of software companies go sideways such as Oracle (ORCL) who have presided over a stale patchwork of database system software created last gen.

However, on the other side of the coin, my prediction of enterprise software companies leading tech has been spot on.

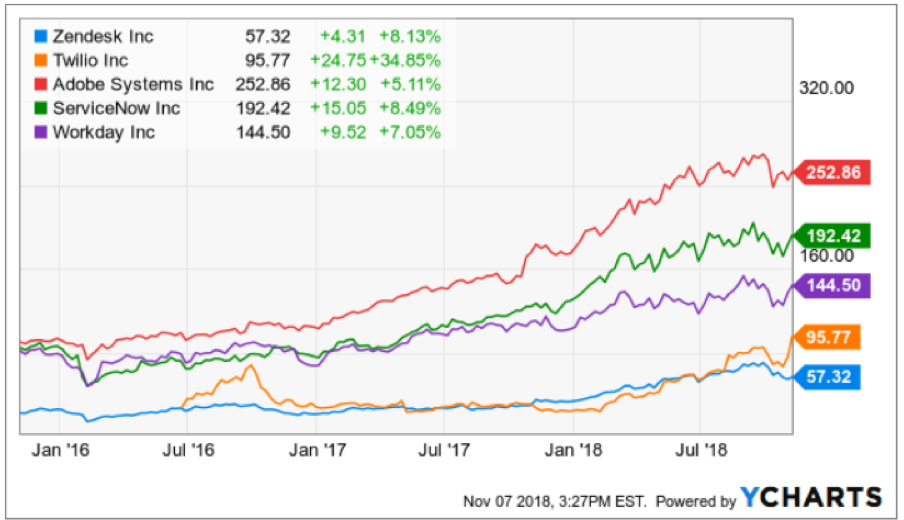

Zendesk (ZEN), HubSpot (HUBS), ServiceNow (NOW), Workday (WDAY), PayPal (PYPL), Salesforce (CRM), Veeva Systems (VEEV), and Twilio (TWLO) are software companies that I was incredibly bullish on as we turned the calendar year and they have not disappointed with nearly all of these names flirting with all-time highs.

All these software companies need Cisco.

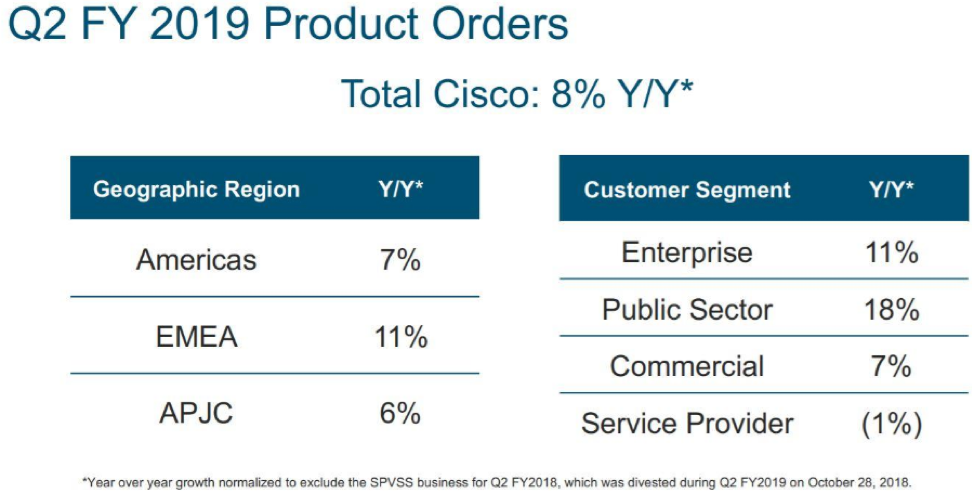

What stood out for me was that public sector orders grew 18% last quarter signaling that not only are the private corporations snapping up Cisco products, but governments are embedding their offices with Cisco’s Internet Protocol-based networking and other products related to the communications and information technology industry.

And if you wanted a general tech stock to capture the migration from analog commerce to digital and stay out of the high stakes online media segment, this would be the stable name that would check all the boxes.

And if you thought this was just a domestic story, once again, the scope is wider with Europe, the Middle East and Africa (EMEA) sales expanding by 11% which eclipsed America sales by 4%.

The only blip on the radar was service revenue slipping by 1% to $3.17 billion, but I do not view that as a pattern of sequential deceleration and pricing mechanisms can be altered to relaunch growth.

If you thought that Cisco doesn’t sell any software – you are wrong.

The software they do sell applies to operating the proprietary hardware that they produce.

Cisco’s wide competitive advantage stems from the industries toweringly high barriers of entry and that they make great products relative to other players.

The infrastructure software that liaises brilliantly with its hardware is succinctly named Cisco ONE Software.

This software suite is molded to face the most relevant use cases in the data center, WAN, and access edge.

CEO of Cisco Chuck Robbins characterized the current geopolitical and overall economic landscape as “complex” but experienced “zero difference” in Chinese revenue giving the company a quarterly victory in the Middle Kingdom.

China’s economy is decelerating faster than we can understand. The latest details of ride-hailing leader Didi sacking 2,000 employees is a warning flare to the rest that open wounds are appearing in the economy and are becoming harder to conceal.

And for Cisco to do a quarter with no significant Chinese downdraft is a good sign that the company can handle the upcoming recession in 2020.

As a sign of further strength, Cisco raised its dividend and boosted stock buybacks which are all the trappings of what great companies do.

Cisco already made $5 billion of repurchases last quarter which was on top of the $6 billion they bought in October 2018.

This method of financial engineering helps put a solid floor under the stock delighting investors and ignites the share price.

And the capital allocation encore means that Cisco will pile $15 billion into its buyback program with this fresh authorization, and the company is forecasted to produce at least $15 billion in free cash flow over the next year.

Cisco’s balance sheet is glistening and even has options to adventure into meaningful M&A if they see something that catches their eye without any real hit to the balance sheet.

These multiple tailwinds in a precarious economic point in the cycle have investors aware that there are worse options out there to invest capital than tech thoroughbred Cisco.

And if you thought the one variable that could turn this earnings report from good to bad was expenses and margins, well, Cisco covered their bases on that one too.

Margins came within the forecasted guidance with gross margins slightly trending down by 1% to 64.1%.

Expenses were reigned in and management saw a small nudge up of 3% causing investors to take a deep sigh of relief.

Cisco is in a superior strategic spot to most tech companies and is a staunch participant of the migration to digital.

Buy shares on the dip.

Mad Hedge Technology Letter

December 10, 2018

Fiat Lux

Featured Trade:

(IT’S ALL ABOUT THE CLOUD)

(OKTA), (ZS), (DOCU), (INTU)

If you thought software week at the Mad Hedge Technology Letter was over, you were absolutely wrong.

I have done my best to offer a barrage of cloud-based software stocks with monstrous upside potential that would put any other industry companies six feet under.

Silicon Valley software companies have access to quinine in a mosquito-infested market – digitally savvy talent.

This talent is the best and brightest the world has to offer, and they want to work for a dominant company that gets it.

Much of this involves companies with bright futures, career opportunities galore, solving deep-rooted problems, all applying a treasure trove of data and a mountain of capital your rich uncle would giggle at.

In the short term, I have been succinctly rewarded by my software picks with communication software Twilio (TWLO) rocketing upward 35% intraday at the time of this writing from when I recommended it just a few days ago.

Another Mad Hedge Technology Letter recommendation Zendesk (ZEN), a software company solving customer support tickets across various channels, is up a tame 10% after the election.

All in all, I would desire readers to access due caution as the volatility can bite you badly with crappy entry points, but the upside cannot be denied.

The turbocharged price action means the pivot to software with its new best friend, the software as a service (SaaS) pricing model, encapsulates the outsized profits this industry will rake in going forward.

Without further ado, I’d like to slip in two more companies rounding out a robust quintet of software companies – I bring to you Workday (WDAY) and Service Now (NOW).

Workday is a software company based on a critical component of every successful company – human resources.

Unsurprisingly, human resources are tardy to this wave of software modernization.

Sensibly, companies have chosen short-term software fixes that drive profits with instant success rather than to update its human resource department’s processes.

Big mistake.

I would argue that getting the right people in the doors is paramount and can save substantial time because of the wasted time rooting out toxic employees who weren’t suitable fits.

Ultimately, I have concluded the worst-case scenario entails the enterprise resource planning market stagnating driving minimal growth to the cloud, however, this minimal growth would be substantial enough for Workday to outperform.

The landscape as of now only involves several vendors with a competitive (SaaS) solution auguring well for Workday allowing them to capture a further chunk of market share.

Workday’s growth metrics back up my thesis with its businesses posting a 3-year EPS growth rate of 291% and a 3-year sales growth rate of 36%, painting a picture of a company that will turn profitable in the next few years.

They can even showboat their glittering array of heavy-hitting customers who purchase their software that include Walmart (WMT), Target (TGT), and Bank of America (BAC).

The one headwind tarnishing these types of software companies is the stock-based compensation awarded to employees.

SBC rose 21% YOY and is slightly worrying in an otherwise stellar company. This method of compensation only works when the stock is rising and is a major issue for new Facebook (FB) hires who will prefer cash over its burnt-out share price.

If Workday doesn’t whet your appetite, then how about sampling a main dish of ServiceNow.

This company completes technology service management tasks offering a centralized service catalog for workers to request technology services or information about applications and processes that are being used in the system.

Admirably, this software helps IT workers fix IT system problems which in this day and age is useful considering the bottleneck of chaos many tech and non-tech companies face.

And more often than not, the chaos inundates the in-house IT departments causing the whole business to go offline.

Putting out digital fires is a perpetual business that will never flame out.

As websites and enterprise systems become more complicated, a bombardment of errors are prone to crop up and instant remedies are crucial to carrying out businesses in a time sensitive manner.

Even ask the best tech company in the universe Amazon (AMZN), whose move off Oracle’s (ORCL) database software was the ultimate reason for a serious outage in one of its biggest warehouses on this past Amazon Prime Day, according to Amazon’s internal documents.

The faux paux underscores the hurdles Amazon and other companies could face as they seek to move completely off the Oracle legacy database software whose development has stayed relatively stagnant for a generation.

The slipup was minutes and snowballed into excruciating hours on Amazon Prime Day resulting in over 15,000 delayed packages and roughly $90,000 in wasted labor costs.

Crikey!

These numbers didn’t even consider the wasted man-hours spent by developers troubleshooting and solving the errors or any potential lost sales.

When these mammoth tech giants are running at an incredible scale, a small blip can result in job losses, lost revenue, lost time, a slew of IT engineer sackings, and for some smaller companies, an existential crisis.

The large-scale acts as a powerful multiplier to the lost resources and cost, and as you can see with the Amazon debacle, a few hours can make or break a developer’s career.

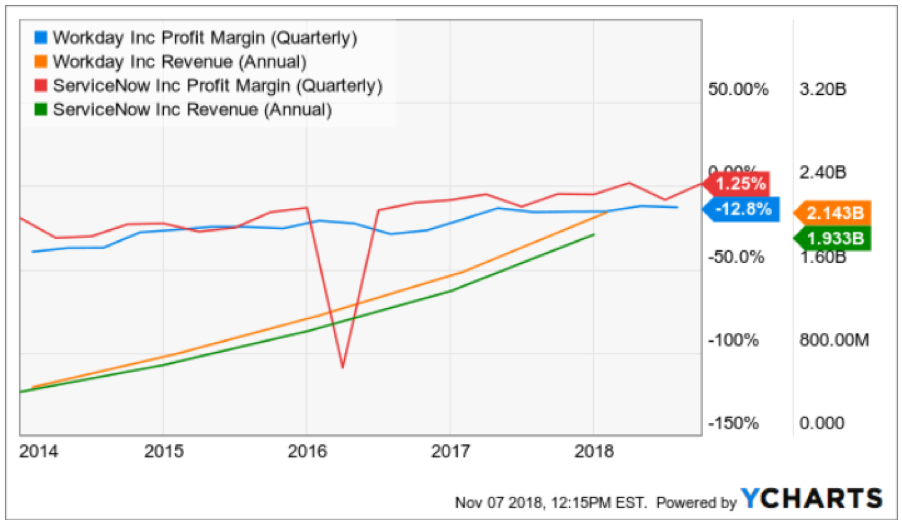

Fortunately, IT budgets are higher up the food chain than human resource budgets while more than inching up every year. This is the main reason why I believe ServiceNow will outperform Workday.

The proof is in the pudding and when I scrutinize various metrics, the truth is filtered out.

ServiceNow’s quarterly growth rate is 35% which is higher than Workday’s who slipped back to 28% last quarter even though the 3-year growth rate is in the mid-30%.

Put mildly, accelerating sales growth is better than decelerating sales growth.

Both companies have a market cap in the low $30 billion and almost identical annual sales in the $2 billion range.

However, ServiceNow presides over significantly higher quarterly profit margins than Workday and will achieve profitability sooner than Workday.

In short, Workday loses more money than ServiceNow.

I believe in the underlying thesis of HR modernization underpinning Workday’s rapidly growing revenue and this secular trend is here to stay.

But I much rather put my hard-earned money on a company tied to IT modernization which is imminent and harder to put on the backburner because of its strategic position at the forefront of the tech curve.

HR CAN be put on the backburner and kept analog longer, and as the economy inches closer to a recession, this expense will be shifted further away from greener pastures supported by the fact that companies decelerate hiring new talent in poor economic environments.

To wrap it up, I do believe ServiceNow is the Burmese python consuming a cow, but that doesn’t mean I am bearish on Workday.

Workday will flourish, just not as much on a relative basis as ServiceNow.

Effectively, these stocks are well placed to move higher even after the violent moves upward this year. As the economic cycle moves further into the late innings, the importance of cloud-based software companies will become magnified further.

As for the software week at the Mad Hedge Technology letter, these solid five picks will offer deep insight into one of the most compelling parts of the internet sector.

As many observers have found out, not all tech firms are created equal and that is made even trickier with the existence of the vaunted FANGs who are the real Burmese python in the current tech landscape.