Global Market Comments

April 14, 2022

Fiat Lux

Featured Trade:

(JULY 22 ZERMATT, SWITZERLAND STRATEGY SEMINAR)

(THE BULL CASE FOR BANKS),

(JPM), (BAC), (C), (WFC), (GS), (MS)

Global Market Comments

April 14, 2022

Fiat Lux

Featured Trade:

(JULY 22 ZERMATT, SWITZERLAND STRATEGY SEMINAR)

(THE BULL CASE FOR BANKS),

(JPM), (BAC), (C), (WFC), (GS), (MS)

Global Market Comments

January 24, 2022

Fiat Lux

Featured Trades:

(MARKET OUTLOOK FOR THE WEEK AHEAD,

or PARACHUTING WITHOUT A PARACHUTE),

(AAPL), (SPY), (MSFT), (TLT), (TBT), (TDOC), (NFLX), (DIS), (VALE), (FCX), (USO), (JPM), (WFC), (BAC), (TSLA), (AMZN), (NVDA)

It has been the worst New Year stock market opening in history.

After a two-day fake-out to the upside, stocks rolled over like the Bismarck and never looked up. NASDAQ did its best interpretation of flunking parachute school without a parachute, posting the worst month since 2008.

Markets can’t hold on to any rally longer than nanoseconds, and the last hour of the day has turned into one from hell.

What is even more confusing is that stocks are now trading like commodities, with massive one-way moves, while commodities, like oil (USO), copper( FCX), and iron ore (VALE) have resumed a steady grind up.

We had a lovefest going on here at Incline Village, Nevada for Technology and Bitcoin researcher Arthur Henry has been staying with me for the week to plot market strategy.

Once the market showed its hand, I sold short Microsoft (MSFT), which elicited torrents of complaints from readers. Then Arthur sold short Netflix (NFLX), inviting refund demands. Then I sold short Apple (AAPL), prompting accusations of high treason. Then Arthur sold short Teledoc (TDOC). There wasn’t a lot of talking, but frenetic writing and emailing instead.

Followers cried all the way to the bank.

In a mere two weeks, the price earnings multiple for the S&P 500 plunged from 22X to 20X. A lot of traders were only buying stock because they were going up. Take out the “up” and Houston we have a problem.

The entire streaming industry seems to have gone up in smoke and ex-growth practically overnight. Netflix (NFLX) delivered a gob smacking 29.5% swan dive in the wake of disappointing subscriber growth forecasts. Walt Disney (DIS), which ate the Netflix lunch, was dragged down 10% through guilt by association.

It is often said that the stock market has discounted 12 of the last six recessions. It is currently pricing in one of those non-recessions. What we are seeing is a sudden growth scare of the first order.

Despite last week’s carnage, stocks are still the most attractive asset class in the world, offering a potential 10% return in 2022. The problem is that they may make that 10% profit starting from 10% lower than here.

Despite all the red ink, big tech stocks are still on track to see a 30% earnings growth this year, and they account for a hefty 28% of the market.

Let’s look at Apple’s past declines for guidance on this meltdown.

Steve Jobs’ creation gave back 60% in the 2008 Great Recession, 34% during the 2015 growth scare, 48% during the great 2018 Christmas collapse, and 28% in the 2020 pandemic crash. So, the good news is that you won’t get killed by this selloff, you’ll just lose an arm and a leg. But they’ll grow back.

Remember, it’s always darkest just before it goes completely black. This correction is survivable, although it may not seem so at the moment.

It does vindicate my 2022 view that the first half will be about survival and that big money can be had in the second half.

So far, so good.

The Market is De-Grossing Big Time. That means cutting total market exposure and selling everything, regardless of stock or sector. The market is discounting a recession and bear market that isn’t going to happen, which occurs often. When it ends in a few weeks, interest rate sensitives, especially the banks, will bounce back hard, but tech won’t. Buy (JPM), (WFC), and (BAC) on bigger dips.

The Bond Collapse Goes Global, with German 10-year bunds going positive for the first time in three years, up 40 basis points in a month. Yes, inflation is finally hitting the Fatherland, home of post-WWI billion percent inflation. Eurozone inflation just topped 5%, well above its 2% target. British inflation hit a 30-year high. The move has lit a fire under all Euro currencies. Methinks the down move in (TLT) has more to go.

Fed to Raise Rates Eight Times, says Marathon Asset Management. That’s what will be needed to curb the current runaway inflation now at 7.0% and still rising. Personally, I think it will be 12 quarter-point increments to peak out at a 3 ¼% overnight rate. Any more and Powell might bring on a recession.

NASDAQ is Officially in Correction, down 10%, in the wake of poor performance this month. It’s the fourth one since the pandemic began two years ago. Tesla (TSLA), Amazon (AMZN), and NVIDIA (NVDA) have been leading the swan dive, all felled by rapidly rising interest rates. This could go on for months.

Weekly Jobless Claims Hit 286,000, a four-month high, as omicron sends workers fleeing home.

Goldman Sachs (GS) Gets Crushed, down 8%, on disappointing earnings. Tough market conditions are fading trading volumes while 2021 bonuses were through the roof. The move is particularly harsh in that buyers were flooding in right at support at the 200-day moving average.

China GDP (FXI) Grows 8.1% YOY but is rapidly slowing now, thanks to Omicron. China was first in and first out with the pandemic but is getting hit much harder in this round. That has prompted new mass lockdowns which will make out own supply chain problems worse for longer. In Chinese, “lockdown” means they weld your door shut, unlike here. Harsh, but it works.

Oil (USO) Hits Seven-Year High, as inventories hit a 21-year low. No new capital is entering the industry, crimping supplies as old fields play out. The threat of a Russian invasion of the Ukraine is prompting advance stockpiling. Russia is the world’s second-largest oil exporter.

Existing Homes Sales Hit a 15-Year High, at 6.12 million, the best since 2006. December fell 4.6%. Extreme inventory shortage is the issue, with only 910,000 homes for sale at the end of the year, an incredibly low 1.8-month supply. You can’t find anything on the market now, to buy or rent. The median price of a home sold in December was $358,000, a 15.8% gain YOY.

Bitcoin (BITO) Crashes, decisively breaking key support at $40,000. Non-yielding assets of every description are getting wiped. Bail on all crypto options plays asap.

My Ten-Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

With the pandemic-driven meltdown on Friday, my January month-to-date performance bounced back hard to 5.05%. My 2022 year-to-date performance also ended at 5.05%. The Dow Average is down -6.12% so far in 2022.

Once stocks went into free fall, I piled on the short positions as fast as I could write the trade alerts, including in Microsoft (MSFT), Apple (AAPL), and a double short in the S&P 500 (SPY). I also increased my shorts in the bond market (TLT) to a triple position. When prices became the most extreme, when the Volatility Index (VIX) hit $30, I bought both (SPY) and (TLT).

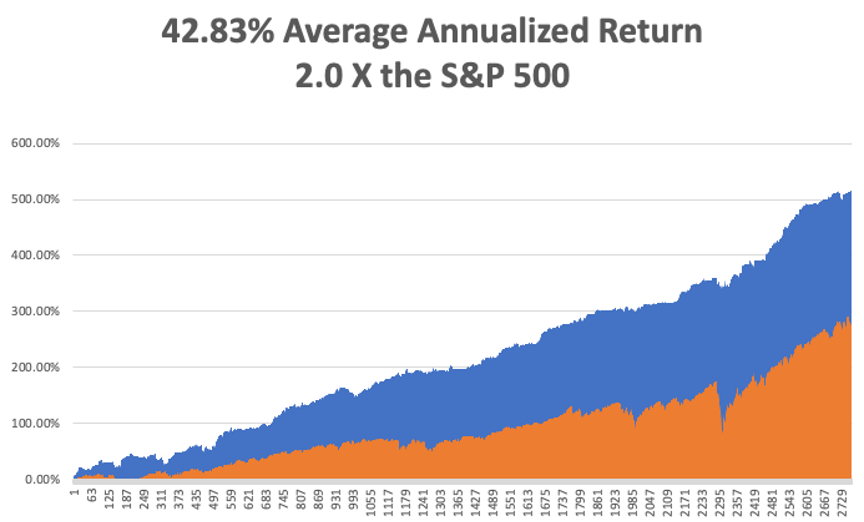

If everything goes our way, we should be up 14.26% by the February 18 options expiration.

That brings my 12-year total return to 517.61%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return has ratcheted up to 42.82% easily the highest in the industry.

We need to keep an eye on the number of US Coronavirus cases at 71 million and rising quickly and deaths topping 866,000, which you can find here.

On Monday, January 24 at 6:45 AM, The Market Composite Flash PMI for January is out. Haliburton (HAL) reports.

On Tuesday, January 25 at 6:00 AM, the S&P Case Shiller National Home Price Index for November is released. American Express (AXP) reports.

On Wednesday, January 26 at 7:00 AM, the New Home Sales for December are published. At 11:00 AM The Federal Reserve interest rate decision is announced. Tesla (TSLA), Boeing (BA), and Freeport McMoRan (FCX) report.

On Thursday, January 27 at 8:30 AM the Weekly Jobless Claims are disclosed. We also get the first look at US Q4 GDP. Alaska Air (ALK) and US Steel (X) report.

On Friday, January 28 at 5:30 AM EST US Personal Income & Spending is printed. Caterpillar (CAT) reports. At 2:00 PM, the Baker Hughes Oil Rig Count is out.

As for me, when I drove up to visit my pharmacist in Incline Village, Nevada, I warned him in advance that I had a question he never heard before: How good is 80-year-old morphine?

He stood back and eyed me suspiciously. Then I explained in detail.

Two years ago, I led an expedition to the South Pacific Solomon Island of Guadalcanal for the US Marine Corps Historical Division (click here for the link). My mission was to recover physical remains and dog tags from the missing-in-action there from the epic 1942 battle.

Between 1942 and 1944, nearly four hundred Marines vanished in the jungles, seas, and skies of Guadalcanal. They were the victims of enemy ambushes and friendly fire, hard fighting, malaria, dysentery, and poor planning.

They were buried in field graves, in cemeteries as unknowns, if not at all left out in the open where they fell. They were classified as “missing,” as “not recovered,” as “presumed dead.”

I managed to accomplish this by hiring an army of kids who knew where the most productive battlefields were, offering a reward of $10 a dog tag, a king's ransom in one of the poorest countries in the world. I recovered about 30 rusted, barely legible oval steel tags.

They also brought me unexploded Japanese hand grenades (please don’t drop), live mortar shells, lots of US 50 caliber and Japanese 7.7 mm Arisaka ammo, and the odd human jawbone, nationality undetermined.

I also chased down a lot of rumors.

There was said to be a fully intact Japanese zero fighter in flying condition hidden in a container at the port for sale to the highest bidder. No luck there.

There was also a just discovered intact B-17 Flying Fortress bomber that crash-landed on a mountain peak with a crew of 11. But that required a four-hour mosquito-infested jungle climb and I figured it wasn’t worth the malaria.

Then, one kid said he knows the location of a Japanese hospital. He led me down a steep, crumbling coral ravine, up a canyon and into a dark cave. And there it was, a Japanese field hospital untouched since the day it was abandoned in 1943.

The skeletons of Japanese soldiers in decayed but full uniform laid in cots where they died. There was a pile of skeletons in the back of the cave. Rusted bottles of Japanese drugs were strewn about, and yellowed glass sachets of morphine were scattered everywhere. I slowly backed out, fearing a cave-in.

It was creepy.

I sent my finds to the Marine Corps at Quantico, Virginia, who traced and returned them to the families. Often the survivors were the children or even grandchildren of the MIAs. What came back were stories of pain and loss that had finally reached closure after eight decades.

Wandering about the island, I often ran into Japanese groups with the same goals as mine. My Japanese is still fluent enough to carry on a decent friendly conversation with the grandchildren of their veterans. It turned out I knew far more about their loved ones than they. After all, it was our side that wrote the history. They were very grateful.

How many MIAs were they looking for? 30,000! Every year, they found hundreds of skeletons, cremated in a ceremony, one of which I was invited to. The ashes were returned to giant bronze urns at Yasakuni Ginja in Tokyo, the final resting place of hundreds of thousands of their own.

My pharmacist friend thought the morphine I discovered had lost half of its potency. Would he take it himself? No way!

As for me, I was a lucky one. My dad made it back from Guadalcanal, although the malaria and post-traumatic stress bothered him for years. And you never wanted to get in a fight with him….ever.

I can work here and make money in the stock market all day long. But my efforts on Guadalcanal were infinitely more rewarding. I’ll be going back as soon as the pandemic ends, now that I know where to look.

Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

True MIAs, the Ultimate Sacrifice

My Collection of Dog Tags and Morphine

My Army of Scavengers

Dad on Guadalcanal (lower right)

Global Market Comments

July 15, 2021

Fiat Lux

Featured Trade:

(THE BULL CASE FOR BANKS)

(JPM), (BAC), (C), (WFC), (GS), (MS)

Global Market Comments

June 23, 2021

Fiat Lux

Featured Trade:

(WHY YOU MISSED THE TECHNOLOGY BOOM AND WHAT TO DO ABOUT IT NOW),

(AAPL), (AMZN), (MSFT), (NVDA), (TSLA), (WFC), (FB)

I often review the portfolios of new concierge subscribers looking for fundamental flaws in their investment approach and it is not unusual for me to find some real disasters.

The Armageddon scenario was quite popular a decade ago. You know, the philosophy that said that the Dow ($INDU) was plunging to 3,000, the US government would default on its debt (TLT), and gold (GLD) was rocketing to $50,000 an ounce?

Those who stuck with the deeply flawed analysis that led to those flawed conclusions saw their retirement funds turn to ashes.

Traditional value investors also fell into a trap. By focusing only on stocks with bargain basement earnings multiples, low price to book values, and high visible cash flows, they shut themselves out of technology stocks, far and away the fastest-growing sector of the economy.

If they are lucky, they picked up shares in Apple a few years ago when the earnings multiple was still down at ten. But even the Giant of Cupertino hasn’t been that cheap for years.

And here is the problem. Tech stocks defy analysis because traditional valuation measures don’t apply to them.

Let’s start with the easiest metric of all, that of sales. How do you measure the value of sales when a company gives away most of its services for free?

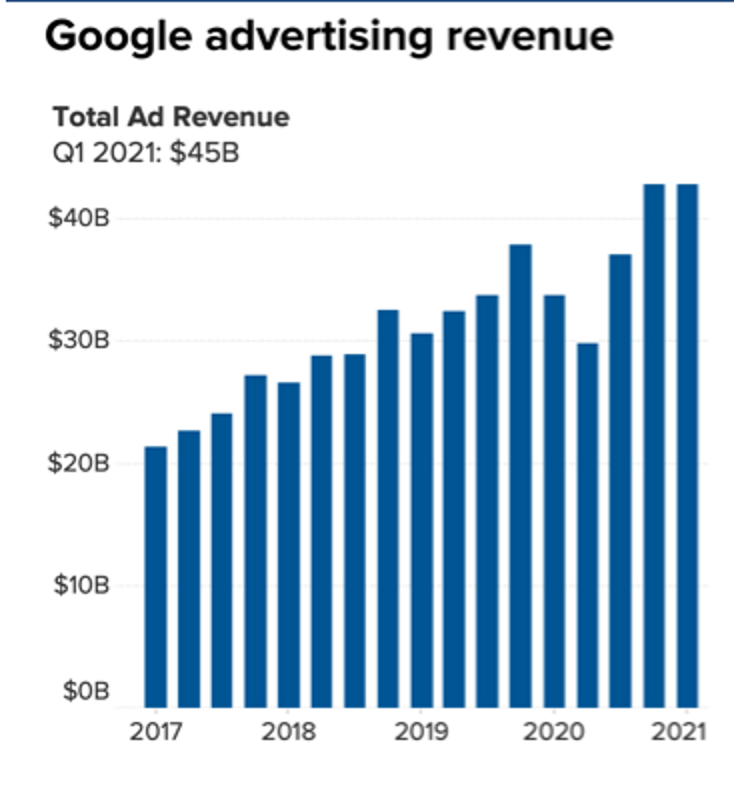

Take Google (GOOG) for example. I bet you all use it. How many of you have actually paid money to Google to use their search function? I would venture none.

What would you pay Google for search if you had to? What is it worth to you to have an instant global search function? Probably at least $100 a year. I would pay $10,000 as I use it all day long. With 92.05% of the global search market comprising 2 billion users, that means $200 billion a year of potential Google revenues are invisible.

Yes, the company makes a chunk of this back by charging advertisers access to these search users, generating some $55.31 Billion in revenues and $17.93 billion in net income in the most recent quarter.

But much of the increased value of this company is passed on to shareholders not through rising profits or dividend payments but through an ever-rising share price. If you’re looking for dividends, Google doesn’t exist. It is also very convenient that unrealized capital gains are tax-free until the shares are sold, which may be never.

I’ll tell you another valuation measure that investors have completely missed, that of community. The most successful companies don’t have just customers who buy stuff, they have a community of members who actively participate in a common vision, which is then monetized. There are countless communities out there now making fortunes, you just have to know how to spot them.

Facebook (FB) has created the largest community of people who are willing to share personal information. This permits the creation of affinity groups centered around specific interests, from your local kids’ school activities to municipality emergency alerts, to your preferred political party.

This creates a gigantic network effect that increases the value of Facebook. Each person who joins (FB) makes it worth more, raising the value of the shares, even though they haven’t paid it a penny. Again, it’s advertisers who are footing your tab.

Tesla (TSLA) has one million customers willing to lend it $400 billion for free in the form of deposits on future car purchases because they also share in the vision of a carbon-free economy. When you add together the costs of initial purchase, fuel, and maintenance savings, a new Tesla Model 3 is now cheaper than a conventional gasoline-powered car over its entire life.

REI, a privately held company, actively cultivates buyers of outdoor equipment, teaches them how to use it, then organizes trips. It will then pursue you to the ends of the earth with seasonal discount sales. Whole Foods (WFC), now owned by Amazon (AMZN), does the same in the healthy eating field.

If you spend a lot of your free time in these two stores, as I do, The United States is composed entirely of healthy, athletic, good-looking, and long-lived, intelligent people.

There is another company you know well that has grown mightily thanks to the community effect. That would be the Diary of a Mad Hedge Fund Trader, one of the fastest-growing online financial services firms of the past decade. What is the value of our community? To give you a hint, the price of my Global Trading Dispatch has soared from $29 a month to $3,000 a year.

We have succeeded not because we are good at selling newsletters, but because we have built a global community of like-minded investors with a common shared vision around the world, that of making money through astute trading and investment.

We produce daily research services covering global financial markets, like Global Trading Dispatch, the Mad Hedge Technology Letter, and the Mad Hedge Biotech & Healthcare Letter. We teach you how to monetize this information with our books like Stocks to Buy for the Coming Roaring Twenties and the Mad Hedge Options Training Course.

We then urge you to action with our Trade Alerts. If you want more hands-on support, you can upgrade to the Concierge Service. You can also meet me in person to discuss your personal portfolios and my Global Strategy Luncheons.

The luncheons are great because long-term Mad Hedge veterans trade notes on how best to use the service and inform me on where to make improvements. It’s a blast.

The letter is self-correcting. When we make a mistake, readers let us know in 60 seconds and we can shoot out a correction immediately. The services evolve on a daily basis.

It all comes together to enable customers to make up to 20% to 100% a year on their retirement funds. And guess what? The more money they make, the more products and services they buy from me. This is why I have so many followers who have been with me for a decade or more. And some of my best ideas come from my own subscribers.

So, if you missed technology now what should you do about it? Recognize what the new game is and get involved. Microsoft (MSFT) with the fastest-growing cloud business offers good value here. Amazon looks like it will eventually hit my $5,000 target. You want to be buying graphics card and AI company NVIDIA (NVDA) on every 10% dip. It’s going to $1,000.

You can buy the breakouts now to get involved or patiently wait until the 10% selloff that usually follows blowout quarterly earnings.

My guess is that tech stocks still have to double in value before their market capitalization of 26% matches their 50% share of US profits. And the technologies are ever hyper-accelerating. That leaves a lot of upside even for the new entrants.

Global Market Comments

January 11, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or A WEEK FOR THE HISTORY BOOKS),

($INDU), (TSLA), (TBT), (TLT), (JPM), (WFC)

A man came at me with a crowbar last week.

I drove into Reno to buy some used backpacks for my Boy Scout troop and parked my Tesla in a nice residential neighborhood. Out of nowhere, a man ran down the street at me screaming profanities, crowbar in hand.

He shouted that I was from Antifa and that I had hired people to invade the Capitol Building to make President Trump look bad.

I reached into my car for my own crowbar. Then the local residents interceded, separating us. The man turned around and walked away, fuming.

“Who the heck was that?” I asked.

“He has mental issues,” said a neighbor. “We’ve had many problems with him before.”

Another said “He’s a Trump supporter. He saw your Tesla and thought you were a liberal.”

Wow! Looks like the nation has a very long way to heal.

Last year, the US defense budget amounted to $622 billion. When the greatest threat to congress in the nation’s history presented itself, it was antique chairs piled against the door that provided the best defense. Maybe we should ditch some big-ticket nuclear missiles and buy more chairs.

Of course, once the insurrection started on Wednesday, I was inundated with international calls from investors asking if they should pull all their money out of the US. I answered “NO” and that it was in fact time to double down. Those who did made a killing.

Ask any professional money manager what his reaction to a coup d’état in Washington would be, their response definitely would NOT be to run out and buy a ton of Tesla (TSLA). Yet, that was exactly the perfect thing to do, the stock soaring an astonishing $135, or 18% in two days. I have many followers who did exactly that and they made millions.

All I can say is that if a market gets hit with an insurrection, and exploding pandemic, and a crashing economy and only goes down 400 points and then bounces back the next day, you want to buy the hell out of it.

I’m talking about going on margin and taking a second mortgage on your home and pouring it into stocks. You might even consider going to a loan shark and borrowing at 18% because you can easily make double that in the right stocks.

After the Biden win and the Georgia sweep, there is now more rocket fuel pouring into the stock market than ever. Call it the “Biden blank check”. Estimates of new spending and subsidies about to hit the market now go up to $10 trillion. Let me list some of them:

*$2 trillion in enforced savings by locked up American consumers.

*Credit card balances have collapsed to multi-year lows, making available hundreds of billions in spending power.

*Trillions of Money market balances sitting on the sidelines yielding zero

*$908 billion stimulus package passed in the closing days of 2020

*A further $2 trillion stimulus package to pass shortly, including $2,000 checks for all 150 million US taxpayers.

*Add another $2 trillion infrastructure budget

*$1 trillion in student loan forgiveness for 10 million borrowers at $10,000 each

*Enormous subsidies for any alternative energy companies and Tesla cars

*The return of the deductibility of $1 trillion worth of state and local real estate taxes (known as (SALT)).

MUCH OF THIS CASH MOUNTAIN IS GOING STRAIGHT INTO THE STOCK MARKET!

It all sets up a stock market that has the potential to have “extreme” moves to the upside, according to my friend, Fundstrat’s Tom Lee.

All you need to retire early is someone to point you in the right direction, into the right sectors and the right stocks. Actually, I happen to know just the right person who can do that and that would be me!

Storming of the Capital shut down markets. After the initial crash, markets flatlined as the entire country dropped what they were doing and glued themselves to a TV, their jaws hanging open. The Dow dove 400 points, bonds and the US dollar stabilized, Tesla and oil took big hits, and gold and silver took off. The electoral college vote has been suspended, gunfights broke out on the house floor, and several explosive devices placed. Trump incited his followers to attack the capitol and they did exactly that. Washington DC is now subject to a 6:00 PM curfew for two weeks. Is this the beginning of the 2024 presidential election? It’s the worst day in Washington since the British burned it in 1814.

Democrats took Georgia, giving them Senate control and a blank check on spending for at least two years. Trump clearly blew the election for his party. My 3X short in bonds soared as the market crashed. Banks rocketed on a 10-basis point leap in interest rates. Infrastructure plays went ballistic. The US dollar faded. Add another couple of percentage points of US GDP growth for 2021.

Tesla Shorts posted biggest loss in history, setting on fire a staggering $38 billion in short positions. Many of these were financed by big oil looking to put Tesla out of business. The short interest in the stock has plunged from 37% to 5%. Did I mention that Tesla was the biggest Mad Hedge long of 2020? I’ve been buying it since it was a split-adjusted $3.30 a share in 2010 against a Friday close of $880, a gain of 290X. Elon Musk is now the richest man in the world and he’s only just getting started!

Tesla met its 500,000-unit 2020 target, far in excess of analyst forecasts. Q4 came in at a surprise 180,570 units. The firm’s 2021 target is 1.1 million units. The market Cap is about to touch $1 trillion, more than all of the global car industry combined. The Model 3 is doing the heavy lifting. Model Y production in Shanghai is about to ramp up and Berlin is to follow. If Tesla can mass-produce their solid-state batteries, they’ll attain a global monopoly in the car industry with 25 million units a year and a share price of $10,000.

A Saudi surprise production cut, a million barrels a day, sent oil over $50. But with demand that weak, how long can the rally last? The market is entering short-selling territory. I bet you didn’t use much gas today commuting from your bedroom to your home office. Use the rally to unload what energy you have left. Sell the (XLE) on rallies.

Bitcoin topped $42,000, more than doubling in a month, and exceeded $1 trillion as an asset class. A Biden-run economy means more money creation which has to find a home. My friend’s pizza purchase for 8 Bitcoin a decade ago is now worth $320,000. I hope it was good!

The Nonfarm Payroll came in at a loss of 140,000, giving more credence to the Q1 double-dip scenario and far worse than expected. The headline Unemployment Rate came in unchanged at 6.7%, Leisure & Hospitality lost a mind-blowing 498,000 and an incredible 3.9 million since January. Private Education lost 63,000 and Government 45,000. Professional & Business Services gained 161,000. The real U-6 Unemployment Rate is a very high 11.6%.

The bond crash has only just begun, with the (TLT) down $8 on the week. The risk/reward is the worst of any financial asset anywhere. I am maintaining my triple short position. Massive government borrowing will be a death knell for fixed income investors.

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

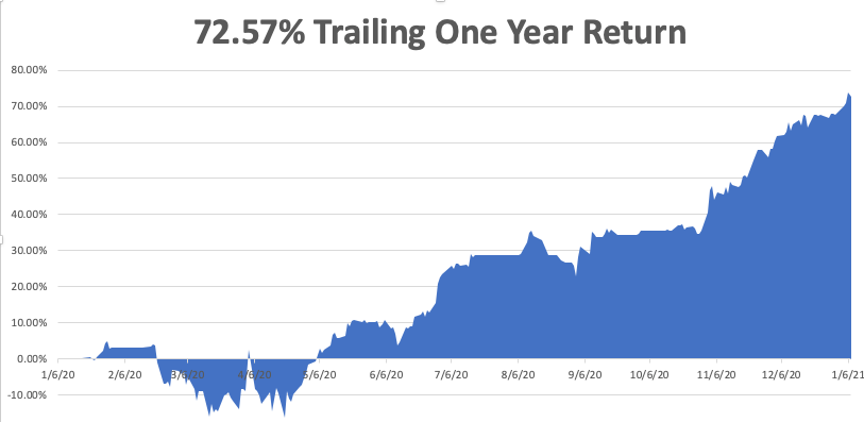

My Mad Hedge Global Trading Dispatch closed out a blockbuster 2020 with a blockbuster 10.20% in December, taking me up to an eye-popping 66.64% for the year. I’m up 81% since the March low. In 2021, I shot out of the gate with an immediate 5.93% profit for the first four trading days of the year.

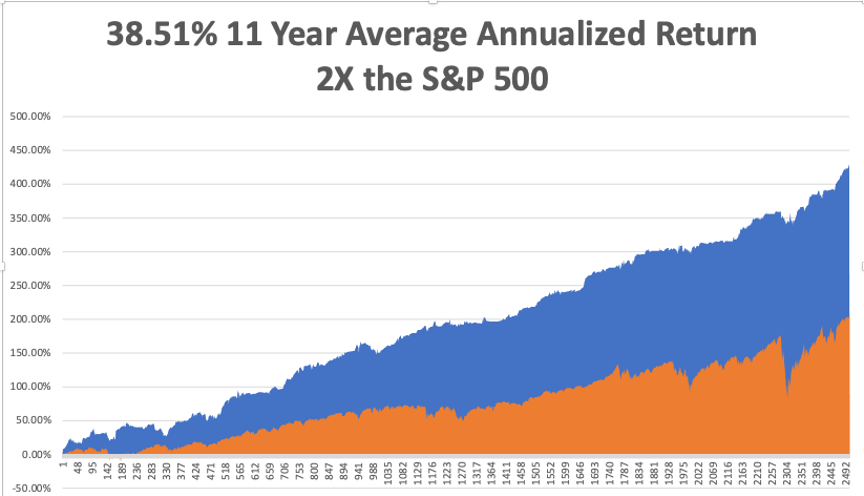

That brings my eleven-year total return to 428.48% double the S&P 500 over the same period. My 11-year average annualized return now stands at a nosebleed new high of 38.51%. My trailing one-year return exploded to 72.57%, the highest in the 13-year history of the Mad Hedge Fund Trader. We have earned 89% since the March low.

The coming week will be a slow one on the data front after last week's fireworks. We also need to keep an eye on the number of US Coronavirus cases at 22 million and deaths 370,000, which you can find here.

When the market starts to focus on this, we may have a problem.

On Monday, January 11 at 11:00 AM EST, US Inflation Expectations are released, which will increasingly become an area of interest.

On Tuesday, January 12 at 4:30 PM, API Crude Inventories are published.

On Wednesday, January 13 at 8:30 AM, the US Inflation Rate for December is announced.

On Thursday, January 14 at 8:30 AM, the Weekly Jobless Claims are published. We also get November Housing Starts.

On Friday, December 15 at 8:30 AM, December Retail Sales are printed. Q4 earnings seasons starts, with JP Morgan Chase (JPM) and Wells Fargo (WFC) reporting. At 2:00 PM we learn the Baker-Hughes Rig Count.

As for me, I’ll be taking my old Toyota Highlander down to the dealer in Reno. Squirrels moved into the engine and ate the wiring, knocking out the heater and the fan. All part of the cost of living in a mountain paradise. However, you have to share it with the critters.

I’ll also be investing in some pepper spray.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

September 16, 2020

Fiat Lux

Featured Trade:

(THE BULL CASE FOR BANKS),

(JPM), (BAC), (C), (WFC), (GS), (MS)

Banks have certainly been the red-headed stepchild of equity investment in 2020.

While technology shares have rocketed by two, three, and four-fold, banks have remained mire in the muck, down 35% on the year while the S&P 500 is up 6%.

However, all that is about to change.

Banks have become the call option on a US economic recovery. When the economic data runs hot, banks rally. When it’s cold, they sell-off. So, in recent months bank share prices have been flat-lining.

You have to now ask the question of when the data stay hot, how high will banks run?

There also is a huge sector rotation issue staring you in the face. Where would you rather put new money, stocks at all-time highs trading at ridiculous multiples, or a quality sector in the bargain basement? Big institutions have already decided what to do and are buying every dip.

Banks certainly took it on the nose with the onset of the pandemic. Interest rates went to zero and loan default rates soared, demanding a massive increase in loan loss provisions.

Much more stringent accounting rules also kicked in during January known as “Current Expected Credit Losses.” That requires banks to write off 100% of their losses immediately, rather than spread them out over a period of years.

Then in June, the Federal Reserve banned bank share buybacks and froze dividends to preserve capital in expectation of more loan defaults.

So what happens next?

For a start, fall down on your knees and thank Dodd-Frank, the Obama era financial regulation bill.

Banks carped for years that it unnecessarily and unfairly tied their hands by limiting leverage ratios to only 10:1. Morgan Stanley reached 40:1 going into the Great Recession and barely made it out alive, while ill-fated Lehman Brothers reached a suicidal 100:1 and didn’t.

That meant the banks went into the pandemic with the strongest balance sheets in decades. No financial crisis here.

Thanks to government efforts to bring the current Great Depression to a quick end, generous fees have been raining down on the banks from the numerous loan programs they are helping to implement.

And trading profits? You may have noticed that options trading volume is up a monster 95% so far in 2020 and increased by a positively meteoric 120% in August. That falls straight to the banks’ bottom lines. If you’re wondering why your online trading platform keeps crashing, that’s why.

I list below my favorite bank investments using the logic that during depressions, you want to buy Rolls Royces, Teslas, and Cadillacs at deep discounts, not Volkswagens, Fiats, or Trabants.

JP Morgan (JPM) – Is the crown jewel of the sector, with the best balance sheet and the strongest customers. It has over reserved for losses that are probably never going to happen, stowing away some $25 billion in the last quarter alone.

Morgan Stanley (MS) - Brokerage-oriented ones like Morgan Stanley (MS) and Goldman Sachs (GS) are benefiting the most from the explosion in stock and options trading. I’ll pick my former employer (MS), where I once accounted for 80% of equity division profits, as (GS) is still mired in the aftermath of the $5 billion Malaysia scandal.

Bank of America (BAC) - is another quality play with a fortress balance sheet.

Citigroup (C) – Is the leveraged play in the sector with a slightly weaker balance sheet and more aggressive marketing strategy. It seems like they’re always trying to catch up with (JPM). This week’s revelation of a surprise $900 million “operational loss” and the penalties to follow knocked 13% of the share price. This is the high volatility play in the sector.

And what about Wells Fargo (WFC), you may ask, the cheapest bank of all? Unfortunately, it still has to wear a hair suit because of its many regulatory transgressions, before, during, and after the financial crisis so I’ll give it a miss. Oh, and Warren Buffet is selling too.