Global Market Comments

August 23, 2019

Fiat Lux

Featured Trade:

(AUGUST 21 BIWEEKLY STRATEGY WEBINAR Q&A),

(FXB), (NVDA), (MU), (LRCX), (AMD),

(WFC), (JPM), (BIDU), (GE), (TLT), (BA)

Global Market Comments

August 23, 2019

Fiat Lux

Featured Trade:

(AUGUST 21 BIWEEKLY STRATEGY WEBINAR Q&A),

(FXB), (NVDA), (MU), (LRCX), (AMD),

(WFC), (JPM), (BIDU), (GE), (TLT), (BA)

Below please find subscribers’ Q&A for the Mad Hedge Fund Trader August 21 Global Strategy Webinar broadcast with my guest and co-host Bill Davis of the Mad Day Trader. Keep those questions coming!

Q: Hey Bill, how often have you heard the word “recession” in the last 24 hours?

A: Seems like every time I turn around. But then we’re also getting a pop in the market; we thought it bottomed a few days ago. The question was: how far were we going to get to bounce? This is going to be very telling as to what happens on this next rally.

Q: Can interest rates go lower?

A: Yes, they can go a lot lower. The general consensus in the US is that we bottom them out somewhere between zero and 1.0%. We’re already way below that in Europe, so we will see lower here in the US. It’s all happening because QE (quantitative easing) is ramping up on a global basis. Europe is about to announce a major QE program in the beginning of September, and the US ended their quantitative tightening way back in March. So, the global flooding of money from central banks, now at $17 trillion, is about to increase even more. That’s what’s causing these huge dislocations in the bond market.

Q: If we’re having trouble getting into trades, should we chase or not?

A: Never chase. Leave your limit in there at a price you’re happy with. Often times, you’ll get done at the end of the day when the high frequency traders cash out all their positions. They will artificially push up our trade alert prices during the day and take them right back down at the end of the day because they have to go 100% cash by the close of each day—they never carry overnight positions. That’s becoming a common way that people get filled on our Trade Alerts.

Q: Will Boris Johnson get kicked out before the hard Brexit occurs?

A: Probably, yes. I’m hoping for it, anyway. What may happen is Parliament forcing a vote on any hard Brexit. If that happens, it will lose, the prime minister will have to resign, and they’ll get a new prime minister. Labor is now campaigning on putting Brexit up to a vote one more time, and just demographic change alone over the last four years means that Brexit will lose in a landslide. That would pull England out of the last 4 years of indecision, torture, and economic funk. If that happens, expect British stock markets to soar and the pound (FXB) to go up, from $1.17 all the way back up to $1.65, where it was before the whole Brexit disaster took place.

Q: Is the US central bank turning into Japan?

A: Yes. If we go to zero rates and zero growth and recession happens, there’s no way to get out of it; and that is the exact situation Japan has been in. For 30 years they have had zero rates, and it’s done absolutely nothing to stimulate their economy or corporate profits. The question then—and one someone might ask Washington—is: why pursue a policy that’s already been proven unsuccessful in every country it’s been tried in?

Q: Will US household debt become a problem if there is a sharp recession?

A: Yes, that’s always a problem in recessions. It’s a major reason why financials have been in a freefall because default rates are about to rise substantially.

Q: Given the big spike in earnings in NVIDIA (NVDA), what now for the stock?

A: Wait for a 10% dip and buy it. This stock has triple in it over the next 3 years. You want to get into all the chip stocks like this, such as Micron Technology (MU), Lam Research (LRCX), and Advanced Micro Devices (AMD).

Q: Baidu (BIDU) has risen in earnings, with management saying the worst is over. Is this reality or is this a red herring?

A: I vote for A red herring. There’s no way the worst is over, unless the management of Baidu knows something we don’t about Chinese intentions.

Q: When will Wells Fargo (WFC) be out of the woods?

A: I hate the sector so I’m really not desperate to reach for marginal financials that I have to get into. If I do want to get into financials, it will be in JP Morgan (JPM), one of my favorites. The whole sector is getting slaughtered by low interest rates.

Q: Any idea when the trade war will end?

A: Yes, after the next presidential election. It’s not as if the Chinese are negotiating in bad faith here, they just have no idea how to deal with a United States that changes its position every day. It’s like negotiating with a piece of Jell-O, you can’t nail it down. At this point the Chinese have thrown their hands up and think they can get a better deal out of the next president.

Q: Would you short General Electric (GE) or wait for another bump up to short it?

A: I would wait for a bump. Obviously—with the latest accounting scandal, which compares (GE) with Enron and WorldCom—I don’t want to get involved with the stock. And we could get new lows once the facts of the case come out. There are too many better fish to fry, like in technology, so I would stay away from (GE).

Q: How do you put stop losses on your trade?

A: It’s a confluence of fundamentals and technicals. Obviously, we’re looking at key support levels on the charts; if those fail then we stop out of there. That doesn’t happen very often, maybe on 10% of our trades (and more recently even less than that). Our latest stop loss was on the (TLT) short. That was our biggest loss of the year but thank goodness we got out of that, because after we stopped out at $138 it went all the way to $146, so that’s why you do stop losses.

Q: How about putting on a (TLT) short now?

A: No, I think we’re going to new highs on (TLT) and new lows on interest rates. We’re just going through a temporary digestion period now. We’ll challenge the lows in rates and highs in prices once again, and you don’t want to be short when that happens. The liquidity is getting so bad in the bond market, you’re getting these gigantic gaps as a global buy panic in bonds continues.

Q: Do you have thoughts on what Fed Governor Powell may say in Jackson Hole, and any market reaction?

A: I have no idea what he might say, but he seems to be trying to walk a tightrope between presidential attacks and economic reality. With the stock market 3% short of an all-time high, I’m not sure how much of a hurry he will be in to lower interest rates. The Fed is usually behind the curve, lowering rates in response to a weak economy, and I’m not sure the actual data is weak enough yet for them to lower. The Fed never anticipates potential weakness (at least until the last raise) so we shall see. But we may have little volatility for the rest of the week and then a big move on Friday, depending on what he says.

Q: What is your take on the short term 6-18 months in residential real estate? Are Chinese tariffs and recession fears already priced in or will prices continue to drop?

A: Prices will continue to drop but not to the extent that we saw in ‘08 and ‘09 when prices dropped by 50, 60, 70% in the worst markets like Florida, Las Vegas, and Arizona. The reason for that is you have a chronic structural shortage in housing. All the home builders that went bankrupt in the last crash has resulted in a shortage, and you also have an immense generation of Millennials trying to buy homes now who’ve been shut out by higher interest rates and who may be coming back in. So, I’m not expecting anything remotely resembling a crash in real estate, just a slowdown. And new homes are actually not falling at all. That’s because the builders are deliberately restraining supply there.

Q: What is a good LEAP to put on now?

A: There aren’t any. We’re somewhat in the middle of a wider, longer-term range, and I want to wait until we get to the bottom of that; when people are jumping out of windows—that’s when you want to start putting on your long term LEAPS (long term equity anticipation securities), and when you get the biggest returns. We may get a shot at that sometime in the next month or two before a year in rally begins. If you held a gun to my head and told me I had to buy a leap, it would probably be in Boeing (BA), which is down 35% from its high.

Global Market Comments

August 21, 2019

Fiat Lux

Featured Trade:

(WHY YOU MIISED THE TECHNOLOGY BOOM AND WHAT TO DO ABOUT IT NOW),

(AAPL), (AMZN), (MSFT), (NVDA), (TSLA), (WFC), (FB)

Mad Hedge Technology Letter

May 7, 2019

Fiat Lux

Featured Trade:

(THE LURKING DANGERS BEHIND FACEBOOK)

(FB), (WFC), (NFLX)

The current business model of social media is dead, and the future model seems in doubt – that was the take away from world's largest social media platform at F8 that I attended, its annual developer conference.

Co-founder and CEO Facebook (FB) Mark Zuckerberg stated at the event that “in our digital lives, we also need both public and private spaces,” an impromptu call to action to migrate users into a new private digital world with Facebook dictating the terms.

The sushi must really be hitting the fan for Zuckerberg to announce his future vision of social media, and the writing is on the wall for his current social media experiment, that is, if he continues along at the same rate.

The projected $5 billion fine incurred by Facebook from the Federal Trade Commission over its privacy handling of personal data is peanuts for the social media company, but this could be the first of numerous fines doled out by regional and national regulatory bureaus that span from the Bay Area to Vietnam.

Facebook is a company that made over $55 billion in revenue last year and the $5 billion would amount to less than 10% of annual sales.

From that $55 billion, Facebook earned profits of over $22 billion, and this $22 billion is what the regulatory battles are about, along with the co-founder’s tenacious defense of deploying his users as free content.

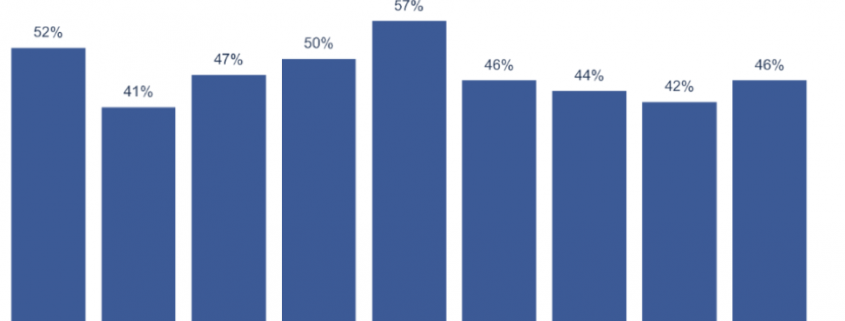

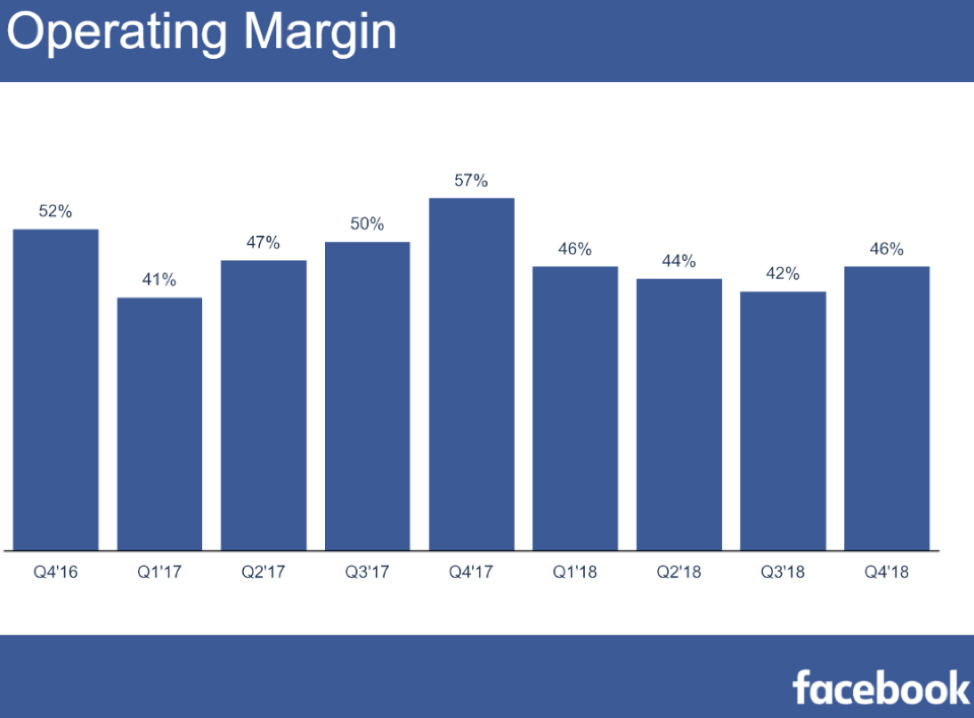

The firm has continued to post operating margins of over 40% and delivered margins of 46% last quarter, a sequential rise of 4% in Q4 2018.

The Oracle of Omaha better known as Warren Buffet cited necessitating accountability for CEOs that drive a company into a government bailout especially banks.

He advocated that these executives and their spouses should be stripped of their net worth if they damage shareholder value.

The comments were directed at the way Wells Fargo’s (WFC) former CEO Tim Sloan crippled Wells Fargo and has since been sidelined during the long bull market in equities.

At some point, Zuckerberg could confront similar ructions because of his efforts at perverting democracy that has caused innumerable damage to American democracy and global society, and I am certain his legion of lawyers are already hatching a plan to tackle this thorny predicament.

If you ponder about his announcement in a zero-sum environment, it makes no sense for Facebook to pivot to “private” messages.

This leads me to believe his words are smoke and mirrors so that Facebook can perpetuate its duopoly and force digital ad players to continue to drink from the same Kool-Aid.

As before, Zuckerberg still believes this game of cat and mouse is a half-baked marketing fix.

This is why many of his trusted disciples such as former executive Chris Cox left under a shroud of mystery citing “artistic differences” in terminating his tenure at Facebook.

It is clear to many that Facebook is barreling straight into an even more frightening future.

What does the announcement mean from a business perspective?

Zuckerberg will continue to purge anyone that disagrees with him, even trusted lieutenants, and continue to integrate the family of apps into one big platform that includes Facebook, Instagram, and WhatsApp messenger.

These three will become one and thus, Zuckerberg’s ad machine rolls on like the dystopian action film Mad Max.

Let me remind you, these drastic measures boil down to Facebook doing everything they can to keep content costs down.

If they, for example, have to go the same route as Netflix (NFLX) - overpaying for the best actors and directors to generate premium content, the stock would halve the next day.

And that is what Zuckerberg is desperately hoping to avoid after the 30% dip in shares in 2018 because of regulatory headwinds.

Combining the three apps would be impossible to regulate at a time that regulation is rearing its ugly head.

Zuckerberg is intentionally upping the ante and accruing more risk in the hope that Facebook can outmuscle its way through in one piece.

The ad industry is crying out for something new, but as long as Zuckerberg’s claws are firmly into the meat of the digital ad budgets for most companies, he gets to decide how the industry develops because he knows the ad dollars will stick.

In the future, your private chats won’t be private because Zuckerberg will be mining the data for ad dollar revenue.

No matter what he says, nothing will change unless Facebook goes in an entirely new direction which would inhibit sales.

Until the fines become material, let’s say 70% of annual revenue or something of that nature, a $5 billion hit to the bottom line will not persuade the management to transform their practices.

Expect less privacy, and WhatsApp and Instagram to be heavily monetized through ad promotion and data mining even though Zuckerberg pledging his company won’t hold user data “longer than necessary.”

As for Facebook itself, Zuckerberg can’t throw his baby out with the bathwater and will hope to minimize its deceleration by bundling it with the growth trajectory of WhatsApp and Instagram.

Instead of major structural changes, Zuckerberg continues to beat around the bush saying, “You should expect that we’re not going to store your data in countries where there's weak data protection.”

This is not the crux of the problem and shows Zuckerberg is still paying lip service and not ponying up to reality.

Attaching Facebook and its dying model is not an attractive strategy leading to a slew of executive resignations.

I believe this could all end in calamity for Zuckerberg as he figures piling on more risk onto the elevated risk levels is the right decision making Warren Buffet’s point for him about CEO’s accountability.

Should Zuckerberg refund shareholders if his flight turns into a suicide mission then claims to be an unwitting victim?

And how does he even refund democracy with his apps causing major unrest to society such as killings that occur because of the distribution of fake news on his platforms?

Making a hot potato hotter might work for the short term and if ad dollars stream into WhatsApp and Instagram, Zuckerberg will claim victory.

But at some point, the potato will scald his hands so bad that it will drop.

Your private chats will be the content at the fulcrum of his data broker empire since his “digital town square” approach isn’t working anymore.

The company is utterly incentivized to figure out how to continue this ad revenue carnival because 93% of total revenue last quarter came from digital ads which is up from the prior year when it constituted 89%.

It all sounds like a big brother apocalyptical novel, which we are in, scarily, in putting out this dialogue before the firestorm starts, Facebook wants to normalize, and front runs the craziness of selling your private chat data before it becomes a national issue.

Will regulators shut this down or will they be naïve and turn a blind eye?

Global Market Comments

March 5, 2019

Fiat Lux

Featured Trade:

(THE BIPOLAR ECONOMY),

(AAPL), (INTC), (ORCL), (CAT), (IBM),

(TESTIMONIAL)

Global Market Comments

March 4, 2019

Fiat Lux

Featured Trade:

(THE MARKET FOR THE WEEK AHEAD, or THE RECESSION HAS BEGUN),

(SPY), (TLT), (GLD), (AAPL)

Global Market Comments

March 1, 2019

Fiat Lux

Featured Trade:

(OH, HOW THE MIGHTY HAVE FALLEN),

(BRK/A), (AXP), (AAPL), (BAC), (KO), (WFC), (KHT),

(AMGEN’S BIG WIN), (AMGN), (SNY), (REGN)

Going through Warren Buffet’s letter to the shareholders of Berkshire Hathaway (BRK/A) you can’t help but notice that his performance nosedived from a breathtaking 21.9% in 2017 to a much more sedentary 2.8% last year. That is with an S&P 500 down -4.4%, including dividends.

That compares to my own 23.67% profit for 2018. But Warren has a much higher bar to reach. He does this with a staggering market capitalization that was pegged at $496 billion as of today. At best, the combined buying power of my Trade Alerts is only about a billion dollars.

And here is the stunning piece of information that should have been the headline. Warren has $112 billion in cash and equivalents, some 22.58% of the total, and an all-time high. That means buying stocks at these levels is the least attractive in the fund’s 57-year history.

Buffet would much rather buy back his own stock. He is willing to pay a premium to book value but only when it trades at a discount to intrinsic value, as he did in size during the fourth quarter of 2018.

Which raises one screaming great question. If Warren Buffet isn’t buying stocks, why should you?

Buffet isn’t even buying Apple, which he only started soaking up in 2017. It now is his second largest holding, with an average cost of $140. I’m amazed that the stock didn’t get crushed on this news, but then we live in a constantly amazing world these days.

The big change in Berkshire Hathaway over the years is that it is becoming more of an operating company and less of an investing one. That is because Buffet is increasingly buying entire companies, rather than exchange-traded stocks. One of the reasons for his cash hoard that an effort to buy a company for high double-digit billions of dollars fell through last year.

Still, Warren bought $43 billion worth of public stocks in 2018 and only sold $19 billion worth. These are his five largest public shareholdings and his percentage of outstanding shares:

American Express (AXP) – 17.9%

Apple (AAPL) – 5.4%

Bank of America (BAC) – 9.5%

Coca-Cola (KO) – 9.4%

Wells Fargo (WFC) – 9.8%

Warren likes to break up his entire holdings into five “groves”, as there are too many companies to follow individually.

1) Wholly owned companies where Berkshire has 80%-100% stakes, such as the BNSF railroad and Berkshire Hathaway Energy.

2) Publicly listed equities like those listed above

3) Companies controlled with third parties, like Kraft Heinz (KHT)

4) US Treasury bills

5) Property/Casualty Insurance operations like GEICO that generate an enormous free cash float

Buffet described the enormous tax benefits his company received from the 2017 tax bill. It amounted to the government’s indirect ownership of Berkshire shares falling, which he humorously calls “AA” shares, from 35% to 21% at no cost whatsoever. That greatly increased the value of the remaining shares.

Warren spent the rest of his letter talking about the Great American Tailwind. Since he started investing on March 11, 1942, one dollar invested in the S&P 500 has grown to an eye-popping $5,288! That works out to an average annualized compound return of 11.8% a year.

The end result has been the greatest creation of wealth and rise in standards of living in human history.

That is a tough record to beat.

Mad Hedge Technology Letter

January 17, 2019

Fiat Lux

Featured Trade:

(WHY FINTECH IS EATING THE BANKS’ LUNCH),

(WFC), (JPM), (BAC), (C), (GS), (XLF), (PYPL), (SQ), (SPOT), (FINX), (INTU)