I found myself gridlocked in Bay Area traffic a few days ago, inching past Gilead's (GILD) sprawling Foster City headquarters, when my phone lit up with a call from an old friend at Goldman.

“Alright, tell me—what’s the real story with biotech this year?” she asked, her tone hovering somewhere between curiosity and exasperation. “Half my portfolio feels like a masterstroke, the other half... well, let’s just say it’s testing my patience.”

As I watched a Tesla (TSLA) weave through traffic like it was auditioning for a Fast & Furious reboot, I smiled.

Biotech has always been a bit of a high-stakes chess game—brilliance in one corner, chaos in another, and always a few surprises lurking behind the next move.

“Let me break it down for you,” I said, steering the conversation as carefully as I did my car through the bumper-to-bumper maze.

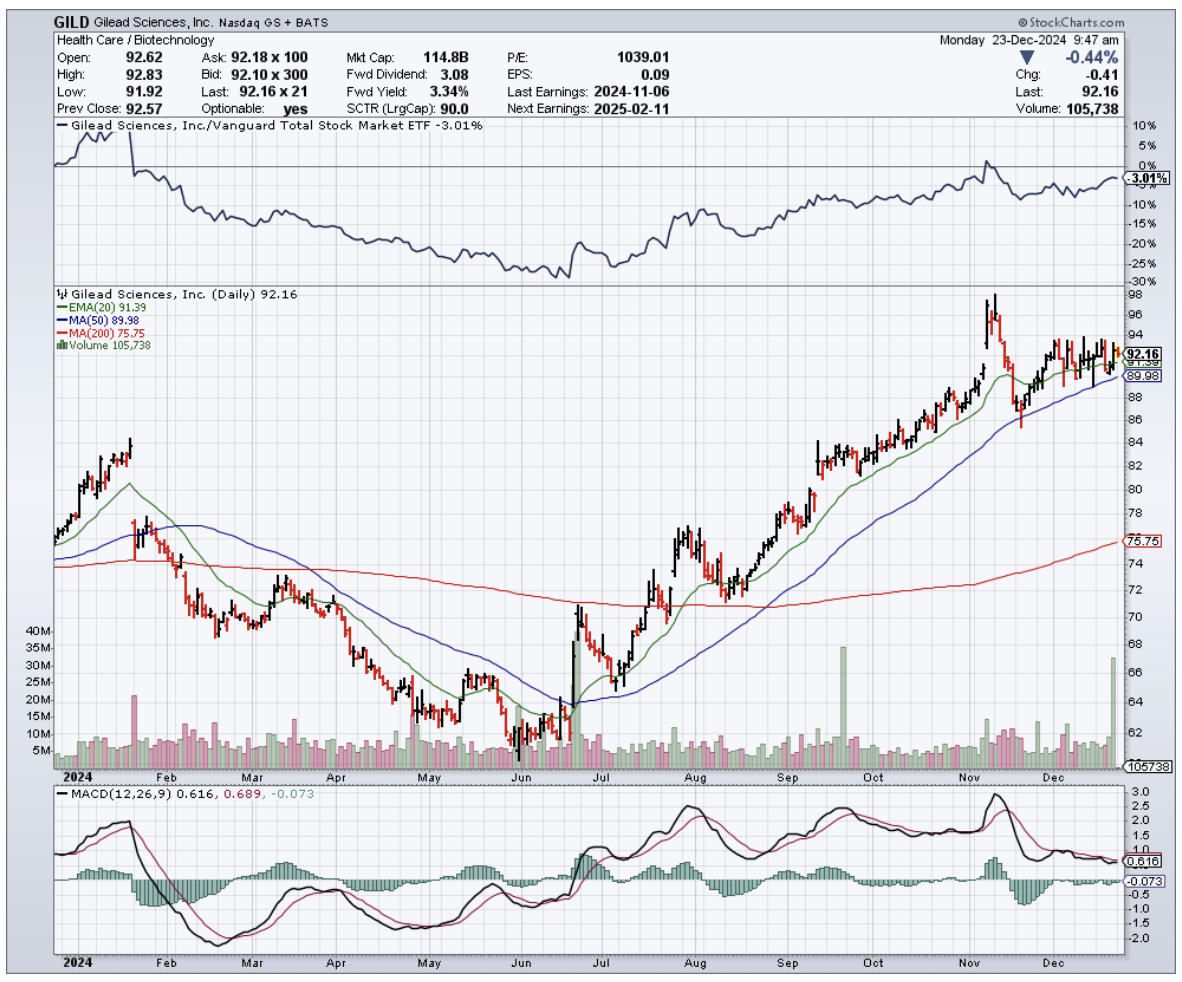

First, the winners are crushing it, and I mean crushing it. Gilead (GILD) finally cracked the code on HIV treatment, developing what's essentially a vaccine that doesn't require popping pills like they're Tic Tacs.

My contacts in clinical development tell me the Phase 3 data in cisgender women is nothing short of spectacular. With a $6 billion annual market potential by 2028, this isn't just another incremental advance - it's the kind of breakthrough that makes everyone in biotech salivate.

Then there's Wave Life Sciences (WVE) and their RNA editing technology. Remember when we thought CRISPR was the only game in town? Well, Wave just showed us there's more than one way to edit a gene.

Their liver-targeting therapy is the first successful RNA editing in humans - think of it as spell-check for your DNA, but reversible. The market's currently at $1.1 billion, but with 35% CAGR through 2030, this train is just leaving the station.

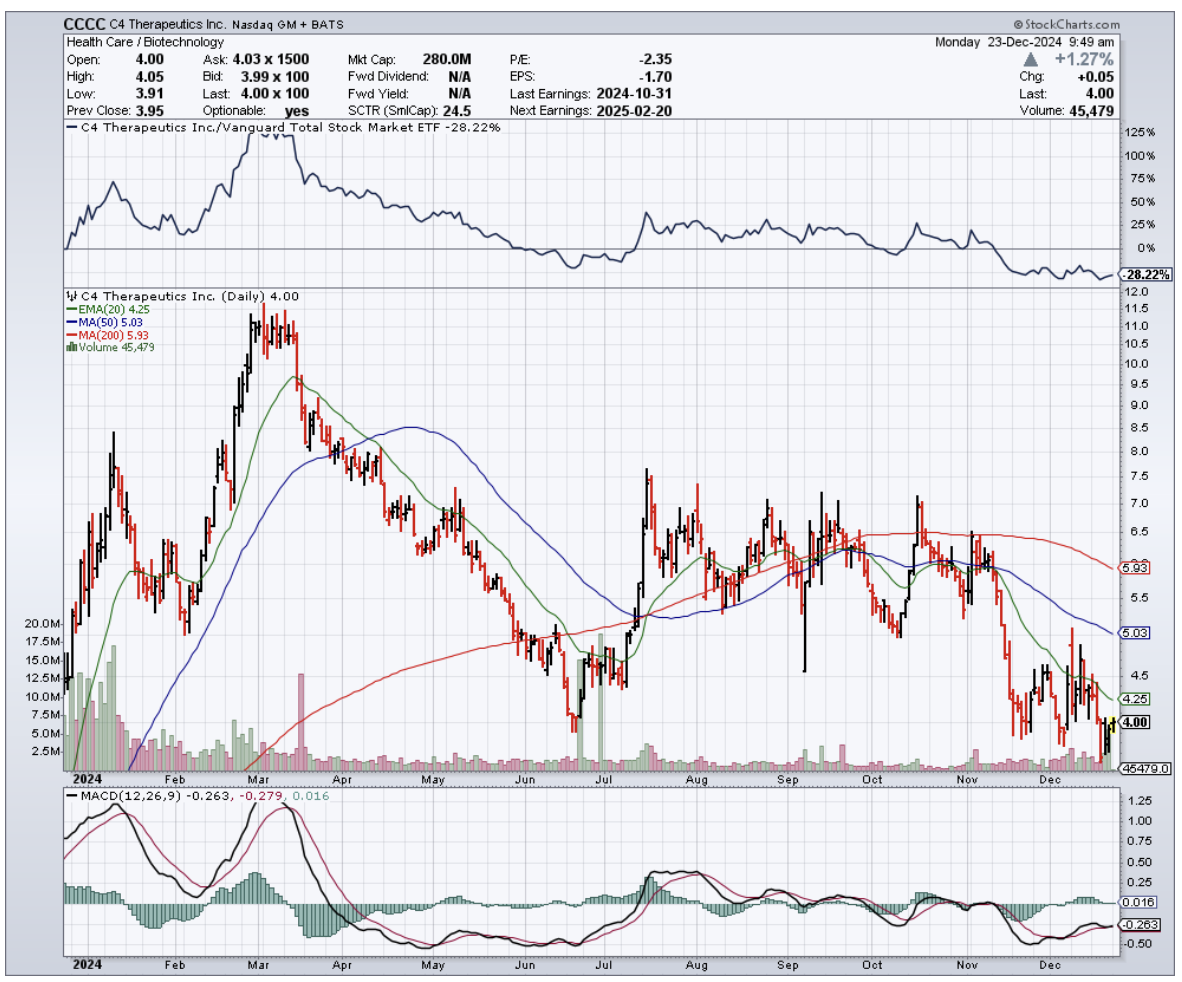

Speaking of trains leaving stations, molecular glue developers like C4 Therapeutics (CCCC) are watching Big Pharma back up the Brink's truck.

We're talking $8 billion in licensing deals this year alone. After all, when Roche (RHHBY) drops $300 million upfront - not milestone payments, mind you, but cold hard cash - you know they've seen something special in the data room.

But here's where it gets interesting, and I had to pull over at this point in the conversation because my friend wasn't going to like what came next.

CRISPR stocks? Down 20%. Editas (EDIT) and CRISPR Therapeutics (CRSP) are learning that revolutionary science doesn't always translate to revolutionary returns.

My friend Janet at the Fed might be talking about higher rates, but these companies are bleeding cash faster than a Silicon Valley startup's WeWork budget.

The obesity market? Unless your name is Eli Lilly (LLY) or Novo Nordisk (NVO), you're probably not having a great time.

Only three startups cleared $100 million in funding this year. In biotech terms, that's like trying to build a house with pocket change.

The global market's sitting at $4.1 billion, but it's more crowded than a San Francisco coffee shop during a tech conference.

And don't get me started on Walmart (WMT) and CVS (CVS) trying to play doctor. They thought they could disrupt traditional healthcare with their “get your physical next to the garden tools” model.

The result? A combined loss of $250 million and a wave of clinic closures.

The lesson here is clear: just because you can sell lightbulbs and Band-Aids in the same aisle doesn’t mean you should try to diagnose strep throat next to the automotive department.

A kid in a modded Subaru WRX cut me off as I wrapped up the call, but I left my friend with this: In biotech, timing is everything.

Gilead and Wave are showing us that patience pays off when the science is solid. Meanwhile, CRISPR stocks remind us that even the most promising technology needs good timing and deep pockets.

So, watch those clinical trial results like a hawk, and keep an eye on where the venture money's flowing.

But most importantly, remember what my old mentor used to say: "In biotech, you're not just betting on the science - you're betting on the scientist, the CFO, and sometimes, just sometimes, on whether people are ready to get their flu shot next to the garden center."

Now, where's that highway patrol when you need them?

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2024-12-24 12:00:482024-12-24 12:26:07The Lab Results Are In

Below please find subscribers’ Q&A for the September 25 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Lake Tahoe Nevada.

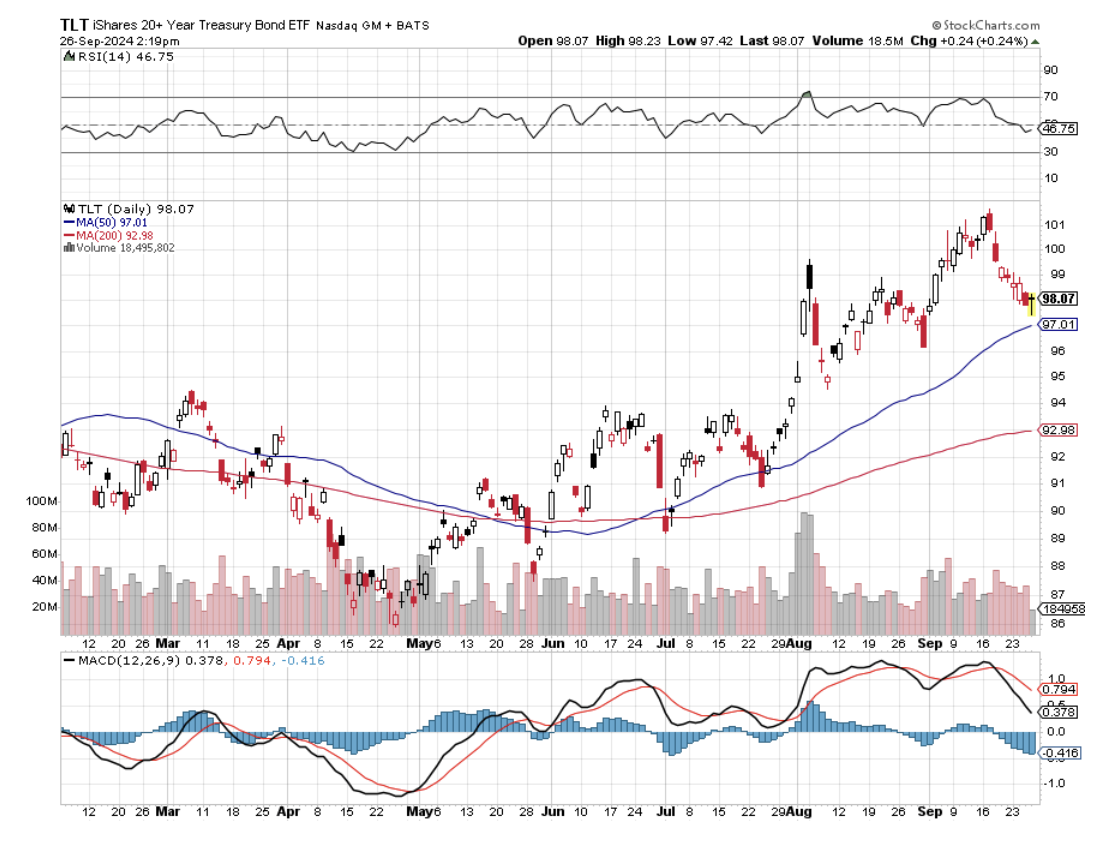

Q: The iShares 20+ Year Treasury Bond ETF (TLT) is not advancing like I had hoped. I’m not sure why the interest rate cuts have not impacted the 20-year maturity—is it too far out?

A: It’s not an issue of maturity; the fact is that the market has been discounting falling interest rates for six months, all the way back to March. It’s a classic “buy the rumor, sell the news” scenario. (TLT) rose $20 off the low this year, and once the rate cut actually happened, all the news was in. That is why I actually went short the TLT a couple of days ago, and that trade immediately started making money. Here’s the real problem: Fed futures are discounting 250 basis points in rate cuts by June of next year. If you don’t think we’re going to get 250 basis points in rate cuts, which is two 50 basis point rate cuts and five 25 basis point rate cuts, then the market is overbought for the short term and we’re selling short. That’s exactly what I did.

Q: Is it too late to buy Tesla (TSLA) and Nvidia (NVDA)?

A: No, it’s not, I think Tesla could hit $300 this year, and Nvidia could revisit $140. However, the more you wait, the more pain you have to take along the way. Nvidia did drop 40% off its high at one point this year, and Tesla dropped 80% off its high. The price of coming in late is pain, so be ready to take that pain or, even worse, to stop out.

Q: What is your take on Japan’s attempt to take over US Steel (X)?

A: Well, it’s entirely political. They definitely picked the wrong year to take a run at US steel because it’s headquartered in Pittsburgh, Pennsylvania, and neither political party can win their election without winning Pennsylvania. Nippon Steel is now 3x larger than US Steel (I covered the company for ten years when I lived in Japan.) It’s the steel factor Jimmy Doolittle bombed in the Pearl Harbor movie. US Steel is using 140-year-old technology—Open Hearth Technology—which hasn’t been updated since the Great Depression. Nippon Steel, meanwhile, is promising to scrap all of that and bring the Steel Industry into the 21st Century. All great ideas for Nippon Steel and their shareholders, but not so great for Unions; all of these takeovers always result in massive layoffs of Union workers. So, that is the issue. That’s where a large part of the added value comes from.

Q: What are the chances that interest rates drop to zero?

A: Zero. I don’t think we’ll ever see 0% interest rates again because people now understand the massive damage that causes to the economy and to savers. So, on the next interest rate cycle, we’ll go down maybe to 2% if we get a recession, but probably not much more than that.

Q: Is it a good time to buy FedEx Corp (FDX)?

A: Yes, it probably is. If there was one rule of trading this year, you buy everything on top of these monster selloffs that are caused by weak guidance. We did it on Palo Alto Networks (PANW) earlier this year—people made a fortune on that. FedEx just did the same thing, so yes, I’m looking very carefully at FedEx calls, call spreads, and LEAPS two years out.

Q: I recently saw a recommendation to buy California Utility Company PG&E (PGE) because of recent revenue gains. Should I take a look?

A: Absolutely, you should. PG&E has gone bankrupt twice in the last 25 years, and the current new management seems to know what they’re doing. They borrowed $20 billion to underground all the long-distance power lines in the state so they won’t be liable for any of these gigantic wildfires that caused the last bankruptcy. Also, you kind of want to own utilities when interest rates are falling because utilities are among the biggest borrowers in the country.

Q: Is Global X Uranium ETF (URA) a good proxy for Cameco Corp (CCJ)?

A: Yes, another one is Consolidation Energy Corp. (CEG), but they’ve all had absolutely astronomical moves ever since the announcement came out that Microsoft was reopening the Three Mile Island nuclear power plant. So, wait for a dip, but the thing is just going up every day right now.

Q: Is it time to buy iShares 20+ Year Treasury Bond ETF (TLT) LEAPS?

A: No, LEAPS territory was last year or the beginning of this year when we were in the $80s (and we issued a ton of (TLT) LEAPS last year.) LEAPS are what you do at market bottoms, not at new all-time highs or two-year highs. Remember, if LEAPS don’t work, they can go to zero, and you want to avoid the zero outcome as much as possible.

Q: Should I look at Visa Inc (V)?

A: Yes, this is another one of those poor guidance situations leading to 20% selloffs. In Visa’s case, they’re being sued by the US government for antitrust because they own 47% of the credit card market. So, I would maybe wait a little bit more, let the market fully digest that, and then Visa’s probably a really strong buy because they’re still growing at 15% a year and minting money like crazy.

Q: Do you see gold going to $3,000 next year?

A: Absolutely, yes, unless it goes to $3,000 this year, which raises a better question: what happens when gold hits $3,000? It goes to 4$,500, because Chinese savers have no other place to put their money except gold. The real estate has crashed and isn’t coming back, they don’t trust their own banks or currency—there really is nowhere else for them to put their own money. They don’t even buy gold miners, they just buy the gold metal and coins. So I think we could see much higher highs than gold, and I’m sticking to my longs.

Q: Will silver continue to lag?

A: No. In fact, in the last couple of weeks, silver has done a big catch-up that is happening because recession fears are going away. Even the soft-landing fears are starting to vaporize—we may have no landing at all. The economy may just keep going, and silver is far more sensitive to the economy than gold is; and that is all silver positive. When we get to the metals, you’ll see how much silver has actually caught up. Silver is probably the better buy here because it tends to outperform gold by two to one.

Q: Do you think the Japanese will cross 100 yen to the dollar in the near future?

A: No, but I think it may cross 100 to the dollar in two years. You’re looking at a permanently weak US dollar from now on. As long as we’re cutting interest rates faster than anyone else, our currency will be the weakest. Japan’s rates are at zero, so they’re not going to cut interest rates at all, which is why we've had this enormous move in the Japanese yen.

Q: Can you give me some good renewable energy stocks and reasons why they are good buys?

A: Well, my favorite renewables are the Canadian Uranium stock Cameco Corporation (CCJ), First Solar (FSLR), which has been the leading industrial-scale solar producer for a long time, and NextEra Energy (NEE), which is very heavily dependent on producing electric power from renewables and also have a 3% dividend.

Q: Why is the euro going up even though their economy is in such terrible shape?

A: Europe has much lower interest rates than the US, and therefore, much less ability to cut interest rates than the US; it is the interest rate cuts that are driving currencies down, and we are the world’s greatest interest rates cutter right now. So, that is why you’re getting outperformance of the euro (FXE).

Q: Financials have moved up over the last two weeks; what’s your take on year-end and beyond? Should I buy Goldman Sachs (GS), JP Morgan (JPM) and Morgan Stanley (MS)?

A: Yes on all three. They’re all big beneficiaries of falling interest rates, improving economies, declining default rates, and rising stock markets. So, you have a triple play on all three of those. I’d be buying the dips on all financials.

Q: When will the sell volatility come back?

A: When you get the Volatility Index ($VIX) over $30. That seems to be the sweet spot for selling volatility. We are now at $15.

Q: If the US sharply increases tariffs, what will be the impact on the economy?

A: It would basically amount to a 20% price increase on everything you buy—from clothes to electronic parts to everything else—and the stock market would crash. Probably 90% of the non-food items Walmart (WMT) sells is from China. That’s why they call it the Chinese embassy. Tariffs are a tremendous restraint of trade and never, ever work, except for targeted items like cars or solar panels. For instance, I am in favor of a 100% tariff on Chinese cars to keep them from demolishing our own car industry as they are currently doing in Europe.

Q: Do we expect commodities like copper (FCX) and foodstuffs to go up as rates are cut?

A: I do. They’re big beneficiaries of falling rates, but more importantly, they’re even bigger beneficiaries of a stimulated Chinese economy, and that’s why we see these monster moves over the last two days.

Q: If you had to invest in one rideshare company, would it be Lyft (LYFT) or Uber (UBER)?

A: Uber—they have far superior management, they’ll be the first into robo-taxis, and they are constantly evolving their model, with Lyft always struggling to catch up.

Q: How will antitrust regulation affect the Magnificent Seven?

A: The bottom line is it will double the value of the Magnificent Seven. If these companies are broken up, the individual parts are worth far more than the whole companies, and we saw this when we broke up AT&T (T) 50 years ago, and the resulting seven companies within a year had a combined market value that vastly exceeded the original AT&T. I actually participated in that deal when I was at Morgan Stanley (since I am 6’4” I was asked to carry the ballots from one floor to another). Expect the same to happen with the Magnificent Seven. They will be worth double or triple more.

Q: If China has a falling population, how will a stimulus program help?

A: Well, it will fill in for the 600 million consumers who were never born as a result of the one-child policy. Not many others are talking about this besides me, but the fact is that the current economic weakness comes entirely from the one-child policy, and there is no way out of that, so they are going to have to keep stimulating again and again, much like the US did through the pandemic.

Q: If you can buy gold and silver on the UK market in sterling, does that make more sense for a UK resident?

A: Yes, it does, since your home currency is in sterling. You will actually get a double play or a “hockey stick effect” because not only is gold going up against the US dollar, but sterling (FXB) is going up against the US dollar, so you’ll get a multiplied effect relative to the pound. We used to play this all day long in Europe in the 1970s and 1980s, back when you had individual currencies to trade and the euro hadn’t been invented yet.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com , go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.