Mad Hedge Technology Letter

February 28, 2019

Fiat Lux

Featured Trade:

(WHY ETSY KNOCKED IT OUT OF THE PARK),

(ETSY), (AMZN), (WMT), (TGT), (JCP), (M)

Mad Hedge Technology Letter

February 28, 2019

Fiat Lux

Featured Trade:

(WHY ETSY KNOCKED IT OUT OF THE PARK),

(ETSY), (AMZN), (WMT), (TGT), (JCP), (M)

I wrote to readers that I expected online commerce company Etsy to “smash all estimates” in my newsletter Online Commerce is Taking Over the World last holiday season, and that is exactly what they did as they just announced quarterly earnings.

To read that article, click here.

I saw the earnings beat a million miles away and I will duly take the credit for calling this one.

Shares of Etsy have skyrocketed since that newsletter when it was hovering at a cheap $48.

The massive earnings beat spawned a rip-roaring rally to over $71 - the highest level since the IPO in 2015.

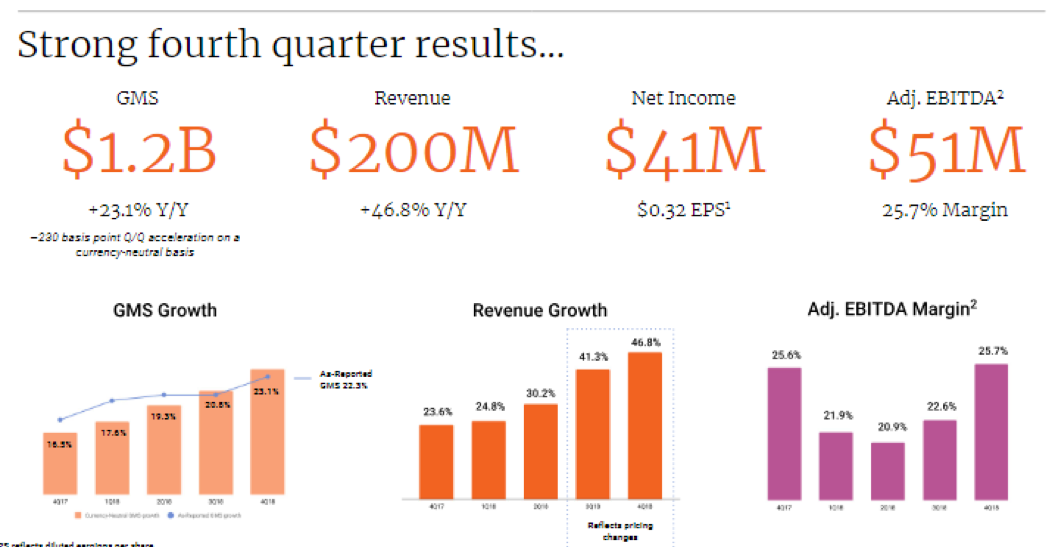

Three catalysts serving as Etsy’s engine are sales growth, strength in their core business, and high margin expansion.

Sales growth was nothing short of breathtaking elevating 46.8% YOY – the number sprints by the 3-year sales growth rate of 27% signaling a firm reacceleration of the business.

The company has proven they can handily deal with the Amazon (AMZN) threat by focusing on a line-up of personalized crafts.

Some examples of products are stickers or coffee mugs that have personalized stylized prints.

This navigates around the Amazon business model because Amazon is biased towards high volume, more likely commoditized goods.

Clearly, the personalized aspect of the business model makes the business a totally different animal and they have flourished because of it.

Active sellers have grown by 10% while active buying accounts have risen by 20% speaking volumes to the broad-based popularity of the platform.

On a sequential basis, EPS grew 113% QOQ demonstrating its overall profitability.

Estimates called for the company to post EPS of 21 cents and the 32 cents were a firm nod to the management team who have been working wonders.

Margins were healthy posting a robust 25.7%.

The holiday season of 2018 was one to reminisce with Amazon, Target (TGT), and Walmart (WMT) setting online records.

Pivoting to digital isn’t just a fad or catchy marketing ploy, online businesses harvested the benefits of being an online business in full-effect during this past winter season.

Etsy’s management has been laser-like focusing on key initiatives such as developing the overall product experience for both sellers and buyers, enhancing customer support and infrastructure, and tested new marketing channels.

Context-specific search ranking, signals and nudges, personalized recommendations, and a host of other product launches were built using machine learning technology that aided towards the improved customer experience.

New incremental buyers were led to the site and returning customers were happy enough to buy on Etsy’s platform multiple times voting with their wallet.

The net effect of the deep customization of products results in unique inventory you locate anywhere else, differentiating itself from other e-commerce platforms that scale too wide to include this level of personalization.

Backing up my theory of a hot holiday season giving online retailers a sharp tailwind were impressive Cyber Monday numbers with Etsy totaling nearly $19,000 in Gross Merchandise Sales (GMS) per minute marking it the best single-day performance in the company’s history.

Logistics played a helping hand with 33% of items on Etsy capable to ship for free domestically during the holidays which is a great success for a company its size.

This wrinkle drove meaningful improvements in conversion rate which is evidence that product initiatives, seller education, and incentives are paying dividends.

Overall, Etsy had a fantastic holiday season with sellers’ holiday GMS, the five days from Thanksgiving through Cyber Monday, up 30% YOY.

Forecasts for 2019 did not disappoint which calls for sustained growth and expanding margins with GMS growth in the range of 17% to 20% and revenue growth of 29% to 32%.

Execution is hitting on all cylinders and combined with the backdrop of a strong domestic economy, consumers are likely to gravitate towards this e-commerce platform.

Expanding its marketing initiatives is part of the business Josh Silverman explained during the conference call with Etsy dabbling in TV marketing for the first time in the back half of 2018, and finding it positively impacting the brand health metrics particularly around things like intending to purchase.

However, Etsy has a more predictable set of marketing investments through Google that offers higher conversion rates and the firm can optimize to see how they can shift the ROI curve up.

Etsy can invest more at the same return or get better returns at the existing spend from Google, it is absolutely the firm's bread and butter for marketing, particularly in Google Shopping, and some Google product listing ads.

With all the creativity and reinvestment, it’s easy to see why Etsy is doing so well.

Online commerce has effectively splintered off into the haves and have-nots.

Those pouring resources into innovating their e-commerce platform, customer experience, marketing, and social media are likely to be doing quite well.

Retailers such as JCPenney (JCP) and Macy’s (M) have borne the brunt of the e-commerce migration wrath and will go down without a fight.

Basing a retail model on mostly physical stores is a death knell and the models that lean feverishly on an online presence are thriving.

At the end of the day, the right management team with flawless execution skills must be in place too and that is what we have with Etsy CEO Josh Silverman and Etsy CFO Rachel Glaser.

Buy this great e-commerce story Etsy on the next pullback - shares are overbought.

Mad Hedge Technology Letter

February 26, 2019

Fiat Lux

Featured Trade:

(WHY THE BIG PLAY IS IN SOFTWARE),

(AMZN), (WMT), (ZEN), (FB), (TWLO)

Buy and hold domestic software companies for dear life because that is what the market is giving you.

Take them with both hands.

These revenue models should revolve around developing the lucrative North American digital consumer markets.

Tech is all about giving you pockets of dispersion and my job to herd you into these pockets of opportunity created by pockets of dispersion.

We have once again been delivered a few more poignant indicators allowing us to gauge the market appetite for certain tech barometers.

Incandescent as can be, recent news of hardware companies planning to bring exorbitant foldable phones to market has me profusely shaking my head.

Huawei announced plans to debut the Mate X foldable 5G smartphone with a price tag of a staggering $2,600.

This followed an announcement by Korean behemoth Samsung to roll out the Samsung's Galaxy Fold and the Koreans plan to sell this luxury product for $1,980.

Chinese Huawei Mate X is 5G-supported and can simply fold into a slimmer 6.6-inch smartphone or unfold into an 8-inch tablet.

This is another case of smart manufacturers overreaching for a market that doesn’t exist and shouldn’t exist.

I believe the demand for screen-related smart products at this price point is scant at best.

If you compare foldable phones to a $600 high-tier Samsung Android smartphone with a 6-inch screen, Samsung and Huawei would need to convince consumers the extra $1,500 or in Samsung’s case, $2,200 is worth the extra relative wad of cash.

My bet is that these foldable phones aren’t worth even $300 more of aggregated incremental value let alone $500 and for many consumers like me, it’s worth zilch.

In no way, aside from the gimmick of buying one of these novelties, does buying a foldable phone justify the price.

This is another example of the common-sense factor that has been completely absent from a product cycle.

Product viability and product desirability do not walk hand in hand.

The screen-related smart device market is saturated, evident by the elongated refresh cycle in smartphone usership.

Blame the expensive price tags of over $1,000 and the removal of carrier subsidies that have caused the upgrade cycle to skyrocket from 2.39 years in 2016 to 2.83 years in late 2018.

Then there is the touchy issue of cannibalizing other hardware product lines as many of the potential foldable phone customers might interchange the foldable phone with normal smartphones.

This all screams bad strategy with companies saddled in a glut of inventory.

It takes R&D years to follow through and develop the technology to bring it to market, and it is entirely conceivable this could become a big write-off.

If price cuts happen shortly after the debut, prospects look bleak.

In general, consumer sentiment has soured for more of this type of tech. Many people are just exhausted from screen time and the cycle of the newest hardware screens is failing to excite existing customers bases.

The only conclusion I can make is that tech today is about software, software, and particularly domestic software.

If you compare software to hardware head to head now, software functionality is still increasing 15% YOY juicing up efficiency and productivity.

What will foldable phones offer a digital nomad or working professional?

Not much.

It highlights the absence of a productivity or functionality boost that digital device users are scouring for now.

Stay away from hardware.

Why is domestic software preferred over international software that scales the earth five times around?

Regulation.

It has reared its ugly head again.

The avalanche of negative headlines applied to American big tech is finally becoming a self-fulfilling prophecy.

It was only a matter of time until someone took note, and in this case, various Asian governments have taken note.

In a bid to blunt American tech’s first mover advantage, the Indian government has written up a draft of regulatory measures in order to make the Indian tech landscape a fairer playground.

This will have the intended effect of creating a national powerhouse of tech firms employing local people.

India has effectively taken a page out of China’s playbook using home-field advantage to nurture homegrown talent.

Large American tech companies have made India a playground of binge investments lately with Amazon (AMZN) shelling out $5 billion and Walmart (WMT) brazenly pouring $15 billion into e-commerce heartthrob Flipkart.

This is awful news for them.

They will have to adjust to India’s new-found zeal for digital regulation and a heavy restructuring of the business model could be in the cards in 2019 along with higher costs of running these businesses.

India has followed China in its footsteps demanding data to be localized meaning data centers won’t be able to run and store Indian data abroad.

American participants will have no other choice but to pony up the extra costs.

Readers might forget that India is the current battleground of global tech growth and Amazon will not have unfettered market access like they did breaking into Europe and dominating e-commerce from the start.

Amazon and Walmart can thank Facebook (FB) which has been the main culprit in bringing wave after monstrous wave of heavy criticism on a whole industry.

Facebook has effectively brought forward the regulatory storm that otherwise would have happened a few years later down the road.

In any case, this makes life harder for data-oriented companies who wish to navigate hazardous foreign tech climates.

Domestic angst against local tech has given the rubber stamp for full-on data government mandates abroad from India to Vietnam.

What does this all mean?

In 2019, data regulation could shrink expected growth levers while hardware companies are becoming even more desperate as these Hail Marys could quickly turn into liabilities.

I nailed software picks Zendesk (ZEN) and Twilio (TWLO) amongst others from a strong group of enterprise software stocks.

Twilio’s performance could potentially become my best pick of 2019, it’s on a straight line up even with all this clutter and chaos around the world.

Mad Hedge Technology Letter

February 20, 2019

Fiat Lux

Featured Trade:

(WALMART’S DRAMATIC SAVE),

(WMT), (AMZN)

This is not your father’s Walmart (WMT).

Peel back a layer or two of that thin veneer and in Walmart, you have nothing closely resembling the Walmart you grew up with.

This would have been a coup de grâce for many companies facing the tsunami of tech strength crushing business models left and right.

Yet, Walmart has found a way to turn the tables and flourish when many industry experts thought this once legacy shopping business was careening towards extinction.

Walmart’s outstanding performance of growing e-commerce sales 43% YOY in the winter quarter of 2018 is a proclamation that they are here to stay through hell or high water and it’s the e-commerce segment leading the charge.

Betting the ranch on e-commerce has them inevitably on a collision course heading directly towards competitor Amazon (AMZN).

Instead of shriveling up and waving the white flag, Walmart’s President and CEO Doug McMillon is acutely aware that the overall pie is growing and there is room for more than just Amazon.

His company’s recent success echoes this trend of the overall marketing growing, and I believe passing the acid test of the 2018 winter shopping season is concrete evidence that Walmart has a prosperous future if they can navigate around four objectives.

First, triple-down on the e-commerce strategy which could translate into being a tad cavalier to operating margins.

This would take a machete to short-term profitability, but I believe Walmart investors are starting to believe in this tech pivot and further margin erosion can be stomached because they are currently conditioned for it.

To capture a larger footprint in the e-commerce market, data analytics specialists will need to be recruited in heavy numbers and convinced of the future vision of Walmart.

The turn of the calendar year means that end of the year bonuses are out and now is the time to capture the horde of tech talent sitting on the open market waiting to be put on Walmart’s books.

Walmart could potentially leap into position to nab some of these tech high flyers who specialize in Python and SQL programming languages. The demand for these wizards is insatiable and the key to any corporate digital migration strategy.

Second, being able to penetrate the target audience a notch above than what Walmart is traditionally accustomed to.

This would correlate into higher average spend per Walmart transaction which would become a feedback loop into Walmart carving out higher-grade product line-ups to compensate increasingly pressured margins.

Third, enhance the logistics and fulfillment strategy by automating more of the business process through robotics and a streamlined IT department.

Walmart has been in the process of scaling out this portion of the business process and they are probably the only one that can pull this off because of the gigantic addressable market and flowing access to capital.

Fourth, originate an educational program coaching up spendthrift customers on how to access its products digitally.

Investors must remember that a large swath of Walmart’s customers aren’t at the top of the socioeconomic ladder and seamlessly culling them into the digital orbit is a responsibility shouldered on upper management.

The goal is to gradually migrate every type of order variant online or through self-checkout means, and self-navigating through these payment and service barriers could be a hindrance as Walmart’s customer base is less tech-savvy than Amazon’s prime subscription customer base.

However, the smaller digital native customer base on a percentage basis is offset by the 4,700 physical stores allowing these partially digital-savvy customers to click and collect.

I view the click and collect distribution channel as a bridge towards becoming fully digital and if Walmart can provide superior customers service, this cohort will likely stick with Walmart’s full-service digital offerings in the future once they upgrade.

In the distant future, it’s almost guaranteed these physical stores end up as fulfillment centers with robotic automation or some type of mix of the two.

Walmart is starting to get serious looks as an e-commerce powerhouse, and I have consistently described Walmart as the next FANG. This latest earnings report reinforces this thesis.

I champion some of the moves to add to product lines such as online brands Art.com and female garment retailer Bare Necessities.

If Walmart could whip up an in-house brand similar to Amazon Basics, that would also be a gamechanger. That step is down the road and Walmart would need to accumulate higher expertise to convert certain products from the 3rd party variety.

Another growth inducer would be establishing a subscription-based service similar to Amazon Prime. Software as a subscription (SaaS) is all the rage in technology and for all the right reasons as this recurring revenue is a boon for the CFO and stabilizes finances.

The Arkansas-based firm forecasted e-commerce annual sales growth of 35% and indicated that huge sums of capital would be allocated into remodeling store units, reinforcing the e-commerce platform, and juicing up its supply chain operations.

Walmart is only scratching the surface and it would take a debacle of epic proportions or a massive recession crimping product demand to knock off Walmart from this high-speed train of positive momentum.

Yes, I agree this company isn’t even close to Amazon now, but the catch-up potential and that path to catch up is clear as daylight.

There is no need to chase shares at this price, but I can say that Walmart is on the verge of locking itself up at the $100 price point as an eternal support level moving forward.

If shares sell off to $90 because of the recent buying from oversold conditions, it could be one of the last times ever to secure a price that cheaply for a precious FANG company.

The company is also famous for continuously raising its dividend.

Walmart is an intriguing stock for the rest of 2019, particularly if the momentum snowballs from here.

Global Market Comments

February 15, 2019

Fiat Lux

Featured Trade:

(THE CONTINUING DEATH OF RETAIL),

(AMZN), (WMT), (M), (JWN),

(TESTIMONIAL)

Mad Hedge Technology Letter

January 9, 2019

Fiat Lux

Featured Trade:

(TOP 8 TECH TRENDS OF 2018),

(GOOGL), (FB), (WMT), (SQ), (AMZN), (ROKU), (KR), (FDX), (UPS), (CRM), (TWLO), (ADBE), (PYPL)

As 2019 christens us with new technological trends, building our portfolio and lives around these themes will give us a leg up in battling the algorithms that have upped the ante in our drive to get ahead.

Now it’s time to chronicle some of these trends that will permeate through the tech universe.

Some are obvious, and some might as well be hidden treasures.

American consumers will start to notice that locations they frequent and the proximities around them will integrate more smart-tech.

The hoards of data that big tech possesses and the profiles they subsequently create on the American consumer will advance allowing the possibilities of more precise and useful products.

These products won’t just accumulate in a person’s home but in public areas, and business will jump at the chance to improve services if it means more revenue.

Amazon and Google have piled money into the smart home through the voice assistant initiatives and adoption has been breathtaking.

The next generation will provide even more variety to integrate into daily lives.

The gains in technology have given the consumer broader control over their lives.

The ability to practically manage one’s life from a remote location has remarkably improved leaps and bounds.

The deflation of mobile phone data costs, the advancement of high-speed broadband internet services in developing countries, more cloud-based software accessible from any internet entry point, and the development of affordable professional grade hardware have made life easy for the small business owners.

What a difference a few years make!

This has truly given a headache for traditional companies who have failed to evolve with the times such as television staples who rely on analog advertising revenue.

Millennials are more interested in flicking on their favorite YouTuber channel who broadcast from anywhere and aren’t locally based.

Another example is the quality of cameras and audio equipment that have risen to the point that anybody can become the next Justin Bieber.

Music executives are even using Spotify to target new talent to invest in.

Blockchain technology has the makings of transforming the world we live in.

And the currency based on the blockchain technology had a field day in the press and backyard summer barbecues all over the country.

Well, 2019 will finally put this topic on the backburner even though Bitcoin won’t disappear into irrelevancy, the pendulum will swing the other direction and this digital currency will become underhyped.

The rise to $20,000 and the catastrophic selloff down to $4,000 was a bubble popping in front of us.

It made a lot of people rich like the Winklevoss brothers Cameron and Tyler who took the $65 million from Facebook CEO Mark Zuckerberg and spun it into bitcoin before the euphoria mesmerized the American public.

On the way down from $20,000, retail investors were tearing their hair out but that is the type of volatility investors must subscribe to with assets that are far out on the risk curve.

The volatility that FinTech leader Square (SQ) and OTT Box streamer Roku (ROKU) have are nothing compared to the extreme volatility that digital currency investors must endure.

Video games classified as a spectator sport will expand up to 40% in 2019.

This phenomenon has already captivated the Asian continent and is coming stateside.

This is a bit out of my realm as standard spectator sports don’t appeal to me much at all, and watching others play video games for fun is something I am even further removed from.

But that’s what the youth like and how they grew up, and this trend shows no signs of stopping.

Industry experts believe that the U.S. is at an inflection point and adoption will accelerate.

Remember that kids don’t play physical sports anymore because of the risk to head trauma, blown ligaments, and the sheer distances involved traveling to and from venues turn participants away.

Franchise rights, advertising, and streaming contracts will energize revenue as a ballooning audience gravitates towards popular leagues, tapping into the fanbase for successful video game series such as Overwatch.

The rise of eSports can be attributed to not only kids not playing physical sports but also younger people watching less television and spending more time online.

Soon, there will be no difference in terms of pay and stature of pro athletes and video gaming athletes.

The amount of money being thrown at the world’s best gamers makes your spine tingle.

The era of digital data regulation is upon us and whacked a few companies like Google and Facebook in 2018.

Well, this is just the beginning.

The vacuum that once allowed tech companies to run riot is no more, and the government has big tech in their cross-hairs.

The A word will start to reverberate in social circles around the tech ecosphere – Antitrust.

At some point towards the end of 2019, some of these mammoth technology companies could face the mother of all regulation in dismantling their business model through an antitrust suit.

Companies such as Amazon and Facebook are praying to the heavens that this never comes to fruition, but the rhetoric about it will slowly increase in 2019 because of the mischievous ways these tech companies have behaved.

The unintended consequences in 2018 were too widespread and damaging to ignore anymore.

Antitrust lawsuits will creep closer in 2019 and this has spawned an all-out grab for the best lobbyists tech money can buy.

Tech lobbyists now amount to the most in volume historically and they certainly will be wielded in the best interest of Silicon Valley.

Watch this space.

The demand for smart consumer devices will fall off a cliff because most of the people who can afford a device already are reading my newsletter from it.

The stunting of smart device innovation has made the upgrade cycle duration longer and consumers feel no need to incrementally upgrade when they aren’t getting more bang for their buck.

The late-cycle nature of the economy that is losing momentum because of a trade war and higher interest rates will see companies look to add to efficiencies by upgrading software systems and processes.

This bodes well for companies such as Microsoft (MSFT), Salesforce (CRM), Twilio (TWLO), PayPal (PYPL), and Adobe (ADBE) in 2019.

This is where Amazon has gotten so good at efficiently moving goods from point A to point B that it is threatening to blow a hole in the logistic stalwarts of UPS and FedEx.

Robots that help deploy packages in the Amazon warehouses won’t just be an Amazon phenomenon forever.

Smaller businesses will be able to take advantage of more robotics as robotics will benefit from the tailwind of deflation making them affordable to smaller business owners.

Amazon’s ramp-up in logistics was a focal point in their purchase of overpriced grocer Whole Foods.

This was more of a bet on their ability to physically deliver well relative to competition than it was its ability to stock above average quality groceries.

If Whole Foods ever did fail, Amazon would be able to spin the prime real estate into a warehouse located in wealthy areas serving the same wealthy clientele.

Therefore, there is no downside short or long-term by buying Whole Foods. Amazon will be able to fine-tune their logistics strategy which they are piling a ton of innovation into.

Possible new logistical innovations include Amazon attempting to deliver to garages to avoid rampant theft.

This is all happening while Amazon pushes onto FedEx’s (FDX) and UPS’s (UPS) turf by building out their own fleet.

Innovative logistics is forcing other grocers to improve fast giving customers better grocery service and prices.

Kroger (KR) has heavily invested in a new British-based logistics warehouse system and Walmart (WMT) is fast changing into a tech play.

Current Chair of the Federal Reserve Jerome Powell unleashed a dragon when he boxed himself into a corner last year and had to announce a rate hike to preserve the integrity of the institution.

Markets whipsawed like a bull at a rodeo and investors lost their pants.

Tech companies who have been leading the economy and trot out robust EPS growth out of a whole swath of industries will experience further volatility as geopolitics and interest rate rhetoric grips the world.

Apple’s revenue warning did not help either and just wait until semiconductors start announcing disastrous earnings.

The short volatility industry crashed last February, and the unwinding of the Fed’s balance sheet mixed with the Chinese avoiding treasury purchases due to the trade war will insert even more volatility into the mix.

Powell attempted to readjust his message by claiming that the Fed “will be patient” and tech shares have had a monstrous rally capped off with Roku exploding over 30% after news of positive subscriber numbers and news of streaming content platform Hulu blowing past the 25 million subscriber mark.

Volatility is good for traders as it offers prime entry points and call spreads can be executed deeper in the money because of the heightened implied volatility.

Mad Hedge Technology Letter

January 7, 2019

Fiat Lux

Featured Trade:

(NOT TOO GOOD TO BE TRUE),

(SCHW), (FB), (SQ), (WMT), (AMZN), (FFIDX), (BOX)