Global Market Comments

June 4, 2024

Fiat Lux

Featured Trade:

(The Mad June traders & Investors Summit is ON!)

(THE BIGGEST “TELL” IN THE MARKET RIGHT NOW),

(GOOGL), (FRC), (PINS), (WORK), (UBER),

(ADSK), (WDAY), (SNE), (NVDA), (MSFT)

Global Market Comments

June 4, 2024

Fiat Lux

Featured Trade:

(The Mad June traders & Investors Summit is ON!)

(THE BIGGEST “TELL” IN THE MARKET RIGHT NOW),

(GOOGL), (FRC), (PINS), (WORK), (UBER),

(ADSK), (WDAY), (SNE), (NVDA), (MSFT)

I am constantly looking for “tells” in the market, little nuggets of information that no one else notices, but give me a huge trading advantage.

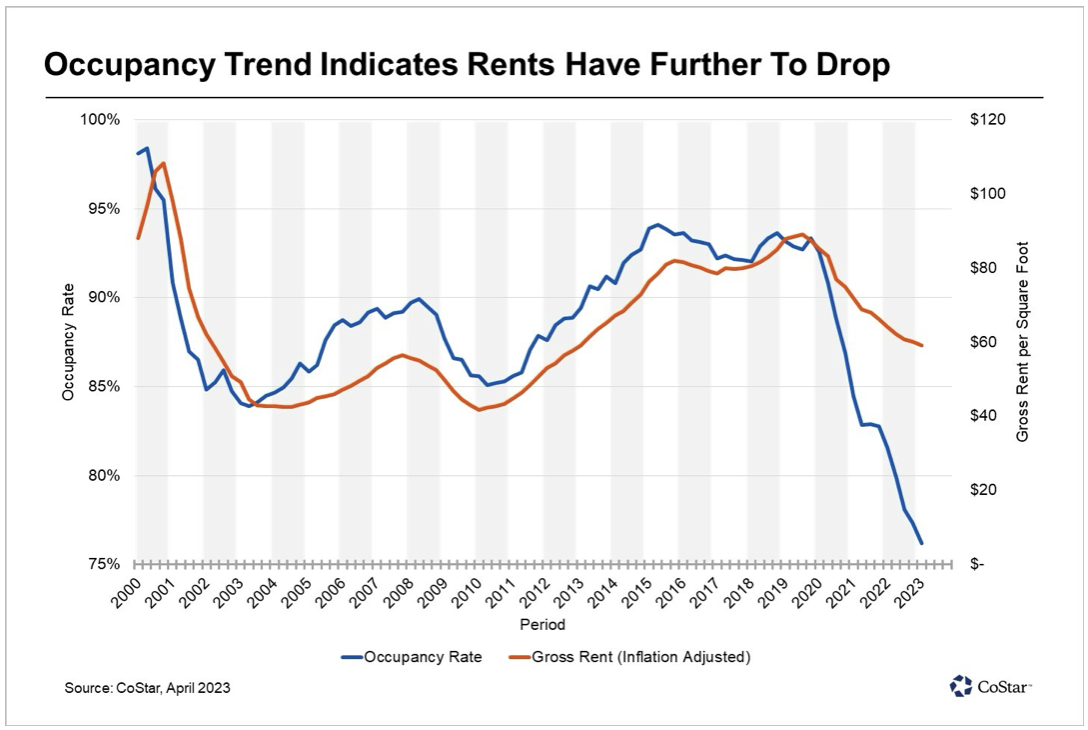

Well, there is a big one out there right now. The bottom feeders are pouring into San Francisco commercial real estate, taking advantage of valuations that sometimes reach negative numbers. Owners are walking away from buildings, mailing in the keys, and going into default rather than keeping up mortgage payments. What’s worse is refinancing at today’s lofty rates. That’s what you would expect with a 36% vacancy rate.

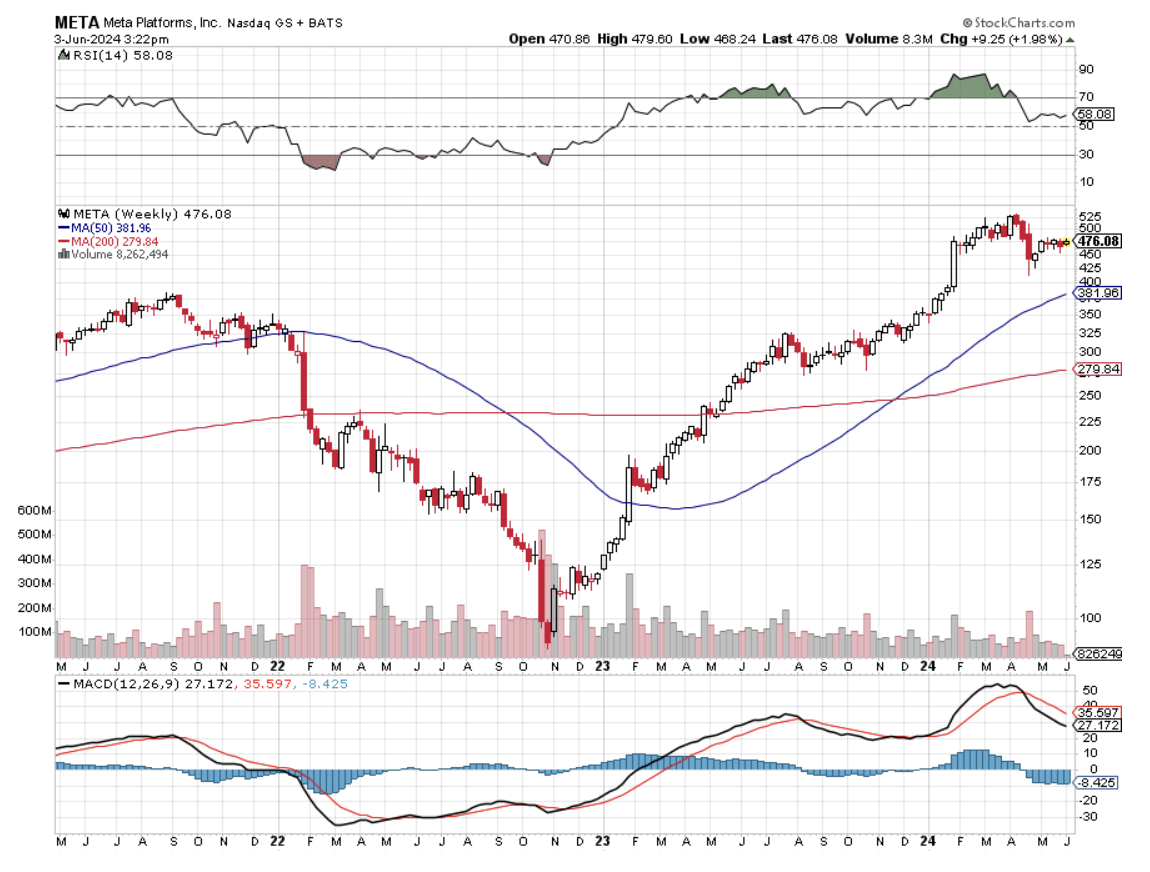

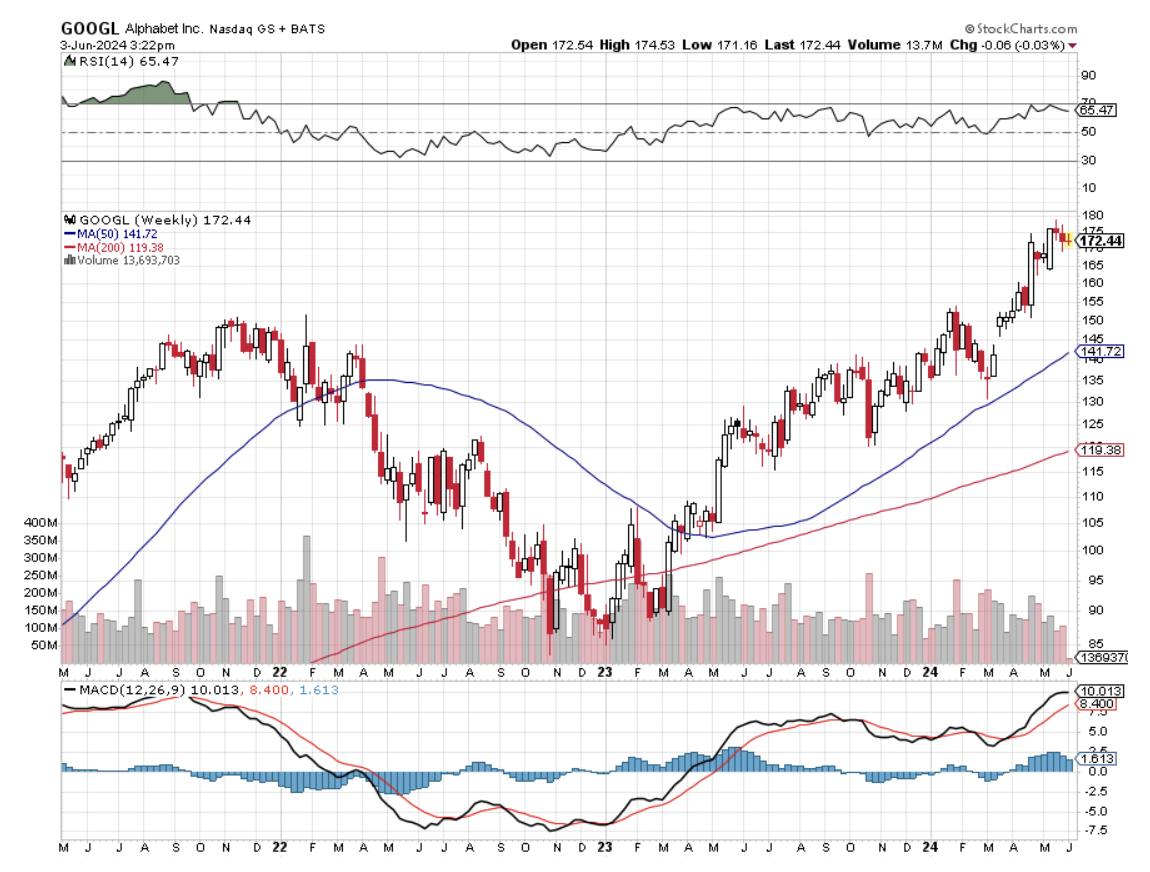

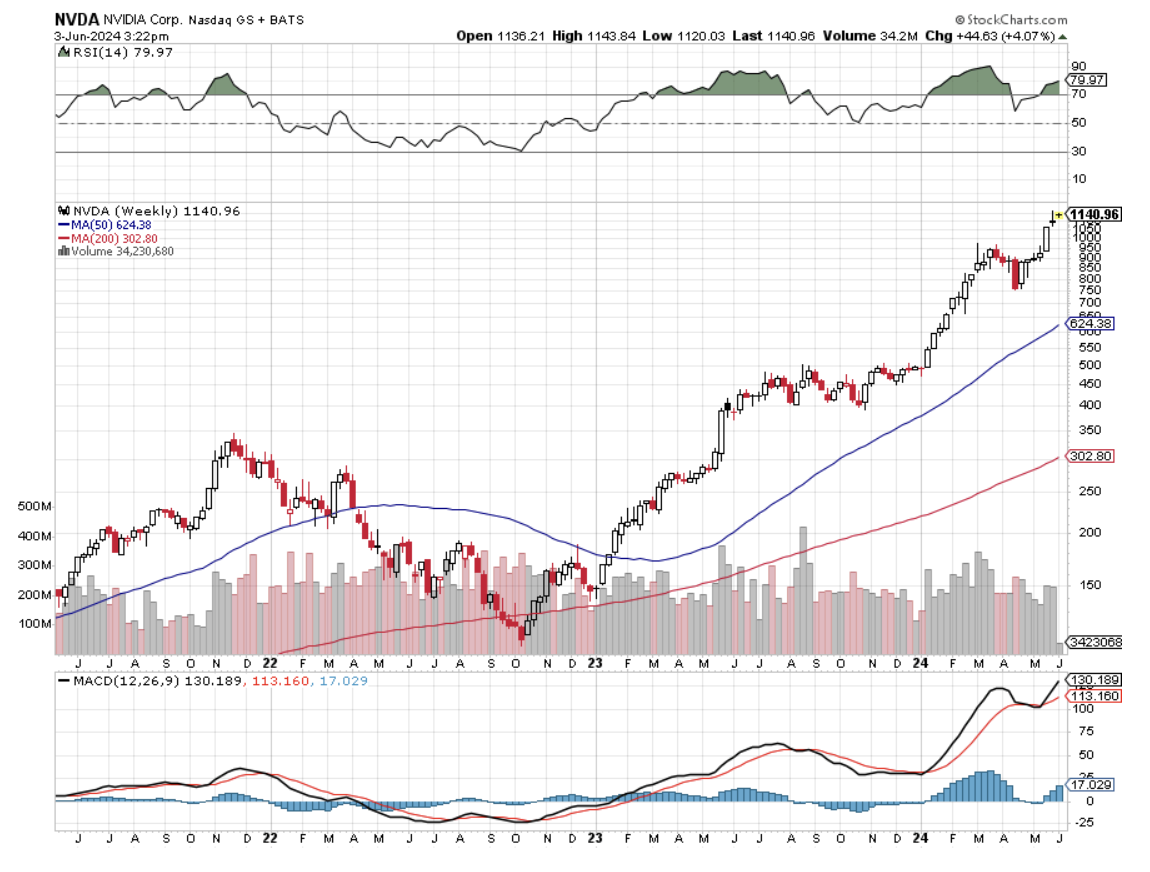

The message for you traders is loud and clear. You should be picking up the highest quality technology growth stocks on every substantial dip, such as Microsoft (MSFT), Amazon (AMZN), Alphabet (GOOGL), Meta (META), and NVIDIA (NVDA). For they all know some things that you don’t. Their businesses are about to triple, if not quadruple over the coming decade thanks to AI. For every abandoned building out there are 200 new AI start-ups taking advantage of today’s bargain basement rates, and ALL of them use the services of the five companies above.

Technology stocks, which now account for an eye-popping 30% of stock market capitalization, will make up more than half of the market within ten years, much of that through stock price appreciation. And they are all racing to lock up the office space with which to do that….now.

San Francisco office rents reached a record pre-pandemic as the continued growth of tech — now turbocharged by nearly $100 billion in new capital raised in a series of initial public offerings — met a severe space crunch.

Asking rents rose to a staggering $84.16 per square foot annually for the newest and highest quality offices in the central business district, and citywide asking rents for such spaces, known as Class A, were up over 9% from the prior year. The citywide office vacancy rate was 5.5% in June, down from 7.4% a year ago.

In addition, local Bay Area home prices could get a turbocharger by the fall, when interest rates are expected to start falling.

San Francisco companies that have gone public continue to grow by leaps and bounds. Pinterest (PINS), Slack (WORK), and Uber (UBER) also signed office leases this year, with room for thousands of new employees.

Tech companies Autodesk (ADSK) and Glassdoor also signed deals at 50 Beale St. in the spring. In a sign of the city’s rapidly changing economy, old-line construction firm Bechtel and Blue Shield, the legacy health insurer, are both moving out of 50 Beale St. Sensor maker Samsara, software firm Workday (WDAY), and Sony’s (SNE) PlayStation video game division also expanded.

Globally, San Francisco has the seventh-highest rents in prime buildings. It’s still behind financial powerhouses Hong Kong, London, New York, Beijing, Tokyo, and New Delhi (San Francisco’s average office rents beat out New York.)

Only a handful of new office projects are being built, and future supply is further constrained by San Francisco’s Proposition M, which limits the amount of office space that can be approved each year. That is creating a steadily worsening structural shortage. Only two large office projects are under construction without tenant commitments.

Suddenly, it’s Not Crowded in San Francisco

Mad Hedge Technology Letter

December 18, 2020

Fiat Lux

Featured Trade:

(TECH IN 2021)

(ZM), (WORK), (NVDA), (AMD), (QCOM), (SQ), (PYPL), (INTU), (PANW), (OKTA), (CRWD), (SHOP), (MELI), (ETSY), (NOW), (AKAM), (TWLO)

The tech sector has been through a whirlwind in 2020, and if investors didn’t lose their shirt in March and sell at the bottom, many of them should have ended the year in the green.

My prediction at the end of 2019 that cybersecurity and health cloud companies would outperform came true.

What I didn’t get right was that almost every other tech company would double as well.

Saying that video conferencing Zoom (ZM) is the Tech Company of 2020 is not a revelation at this point, but it shows how quickly a hot software tool can come to the forefront of the tech ecosystem.

M&A was as hot as can be as many cash-heavy cloud firms try to keep pace with the Apples and Googles of the tech world like Salesforce’s purchase of workforce collaboration app Slack (WORK).

Not only has the cloud felt the huge tailwinds from the pandemic, but hardware companies like HP and Dell have been helped by the massive demand for devices since the whole world moved online in March.

What can we expect in 2021?

Although I don’t foresee many tech firms making 100% returns like in 2020, they are still the star QB on the team and are carrying the rest of the market on their back.

That won’t change and in fact, tech will need smaller companies to do more heavy lifting come 2021.

The only other sector to get through completely unscathed from the pandemic is housing, and unsurprisingly, it goes hand in hand with converted remote offices that wield the software that I talk about.

The world has essentially become silos of remote offices and we plug into the central system to do business with each other with this thing called the internet.

In 2021, this concept accelerates, and cloud companies could easily check in with 20%-30% return by 2022. The true “growth” cloud firms will see 40% returns if external factors stay favorable.

This year was the beginning of the end for many non-tech businesses and just because vaccines are rolling out across the U.S. doesn’t mean that everyone will ditch the masks and congregate in tight, indoor places.

There is nothing stopping tech from snatching more turf from the other sectors and the coast couldn’t be clearer minus the few dealing with anti-trust issues.

I can tell you with conviction that Facebook, Google, Apple, and Amazon have run out of time and meaningful regulation will rear its ugly head in 2021.

We are already seeing the EU try to ratchet up the tax coffers and lawsuits up the wazoo on Facebook are starting to mount.

Eventually, they will all be broken up which will spawn even more shareholder value.

Even Fed Chair Jerome Powell told us that he thinks stocks aren’t expensive based on how low rates have become.

That is the green light to throw new money at growth stocks unless the Fed signal otherwise.

As we head into the 5G world, I would not bet against the semiconductor trade and the likes of Nvidia (NVDA), AMD (AMD), Qualcomm (QCOM) should overperform in 2021.

Communication is the glue of society and communications-as-a-platform app Twilio (TWLO) will improve on its 2020 form along with cloud apps that make the internet more efficient and robust like Akamai (AKAM).

Workflow cloud app ServiceNow (NOW) is another one that will continue its success.

The uninterrupted shift to the cloud will not stop in 2021 and will be a strong growth driver for numerous tech companies next year.

I will not say this is a digital revolution, but as corporate executives realize they haven’t spent enough on the cloud in the lead-up to the pandemic and must now play catch-up in order to satisfy new demands in the business.

The most recent CIO survey was the thesis that cloud and digital adoption at 10% of enterprise and 15% of consumer spend entering 2020 would continue to accelerate post-pandemic and into 2021-2022.

A key dynamic playing out in the tech world over the next 12 to 18 months is the secular growth areas around cloud and cybersecurity that are seeing eye-popping demand trends.

Consumers will still be stuck at home, meaning e-commerce will still be big winners in 2021 such as Shopify (SHOP), Etsy (ETSY), and MercadoLibre (MELI).

The reliance on e-commerce will open the door for more tech companies to participate in the digital flow of transactions and the U.S. will finally catch up to the Chinese idea of paying through contactless instruments and not cards.

This highly benefits U.S. fintech companies like Square (SQ) and PayPal (PYPL). Intuit (INTU) and its accounting software is another niche player that will dominate.

Intuit most recently bought Credit Karma for $8.1 billion signaling deeper penetration into fintech.

Since we are all splurging online, we need cybersecurity to protect us and the likes of Palo Alto Networks (PANW), Okta (OKTA), and CrowdStrike Holdings, Inc. (CRWD).

The side effect of the accelerating shift to digital and cloud are troves of data that need to be stored, thus anything related to big data will also outperform.

Most of the information created (97%) has historically been stored, processed, or archived.

As new mountains of digital gold are created, we expect AI will have an increasingly critical role.

I believe that 2021 will finally see the integration of 5G technology ushering in another wave of digital migration and data generation that the world has never seen before and above are some of the tech companies that will make out well.

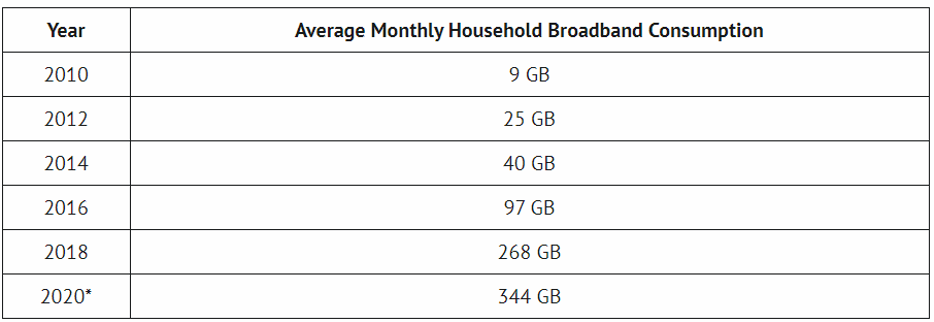

The average household is using 38x the amount of internet data they were using ten years ago and this is just the beginning.

Mad Hedge Technology Letter

December 2, 2020

Fiat Lux

Featured Trade:

(SALESFORCE TRIES TO STAY RELEVANT IN THE CLOUD)

(CRM), (WORK), (MSFT), (GOOGL)

This was basically a deal they had to do even though I believe Salesforce (CRM) massively overpaid for Slack (WORK).

The other option would be to fall even further behind Microsoft (MSFT) who has hit a home run with their own in-house iteration of Slack-ish software called Microsoft Teams.

In fact, this is the biggest acquisition in Salesforce’s software history and purchasing the software developer Slack for over $27 billion marks a new chapter in their history.

Through a combination of cash and stock, Salesforce is purchasing Slack for $26.79 a share and .0776 shares of Salesforce.

Other big software deals such as IBM’s $34 billion purchase of Red Hat in 2018, the largest in its history, followed by Microsoft’s $27 billion acquisition of LinkedIn in 2016 are also noteworthy.

Last year, the London Stock Exchange agreed to buy data provider Refinitiv for $27 billion, though the deal has yet to be cleared by European regulators.

Salesforce has decided to grow via M&A as CEO Marc Benioff hopes to stave off a growth downturn by pre-emptively addressing these potential problems.

His goal is to get more investors on board for the long haul.

In the short term, the jury is out on whether Salesforce can “grow into” the high valuation which they agreed to pay for Slack.

Other deals made by Salesforce are when the company spent $15.3 billion on data visualization company Tableau in 2019 and, a year earlier, they captured MuleSoft for $6.5 billion whose back-end software connects data stored in disparate places.

The future of enterprise software is transforming the way everyone works in the all-digital, work-from-anywhere world and Salesforce will be one of the leading voices in how this plays out.

Don’t forget that Salesforce started the enterprise cloud revolution, and two decades later, they are still tapping into all the possibilities it offers to transform the way we work.

For Slack, this is a major victory because they had begun to see the writing on the wall with two uninspiring earnings reports which signaled that Microsoft was having their cake and eating it too.

For Salesforce to pay a 30%-40% premium for Slack reveals the sense of desperation permeating into the ranks of Salesforce management.

Another takeaway is that enterprise software is putting their money where their mouth is convinced that the shelter-in-home economy will last long after the brutal public health crisis is over.

I tend to agree with this diagnosis, but I don’t agree with overpaying for Slack at the degree in which they did.

However, the climate of cheap rates and high liquidity feeds into the normalcy of overpaying for quality assets.

What’s so bad about Slack?

Slack has blamed the downturn in fortunes on some of its small business customers being hurt by the pandemic.

The company has loosened contract structures and extended credits to help them out which is a major red flag.

The slowdown has only fueled nervousness that Microsoft (MSFT) Teams’ ascent is weighing on Slack’s growth potential.

Teams now has more than 115 million users while Slack has a fraction of that, despite having the edge in the minds of most in terms of user interface.

Slack’s slowing growth, in turn, hurt its sentiment and ultimately its stock price.

Salesforce could have acquired Slack for a discount in a year or two, but by that time, Salesforce would be left in the dust.

Salesforce had to act with urgency even if Slack still expects to post a net loss this fiscal year. It’s unclear when Slack will turn a profit-making company even less attractive.

Salesforce will need to subsidize Slack’s losses for the time being.

What’s in it for Salesforce?

Salesforce could help easily scale up Slack to more high-paying corporate customers in a major challenge to Microsoft Teams which would vastly help Slack’s margins.

There are also numerous synergies in being under the Salesforce umbrella which would only strengthen the profit potential of the communications platform.

By acquiring Slack, a business chat service with over 130,000 paid customers, Salesforce is bolstering its portfolio of enterprise applications and filling out its broader software roster as it seeks additional growth engines.

Salesforce obviously believes that the sum of the parts will be greater than each individual segment and I agree.

Salesforce’s annualized revenue topped $20 billion in the fiscal second quarter, with growth of 29%. But the forecast for the full year of 21% to 22% growth would represent the company’s slowest rate of expansion since 2010.

Microsoft and Salesforce are direct rivals at this point and Salesforce is the dominant player in customer relationship management software, where Microsoft is a distant challenger. Both companies tried to buy LinkedIn, the professional networking site, but Microsoft was the ultimate winner.

The company’s core Sales Cloud product for keeping track of current and potential customers delivered $1.3 billion in revenue, up 12% year over year and that’s simply not good enough to be considered a “growth asset.”

Many investors won’t bite at the bid unless a burgeoning tech company is north of 20% and preferably plus 30%.

Salesforce will now embark on a narrative of engineering growth to fit its investors’ preferences, but I do hesitate to think that this will most likely mean continuing to overpay for software companies.

Salesforce does have the resources to absorb this pricey endeavor but is it sustainable when the likes of Microsoft, Google, and so on are competing for the same assets?

Does this mean that Twitter would be $60 billion in today’s climate?

That’s a scary thought.

M&A could disappear soon from tech because the valuations might reach some sort of peak that even cash-rich Silicon Valley firms might balk at.

Yes, we are getting to that stage of tech. Tech is becoming a luxury.

In the short term, buy Salesforce’s dip as some investors will sell as a way to signal to Salesforce that they aren’t happy with their capital allocation strategy and ultimately this isn’t a guarantee of adding growth and could possibly backfire in Benioff’s face.

Mad Hedge Technology Letter

April 27, 2020

Fiat Lux

Featured Trade:

(FRONT RUNNING THE MICROSOFT EARNINGS)

(MSFT), (AMZN), (WORK)

It’s hard to imagine that Microsoft’s earnings report on Wednesday will be anything other than remarkable as their growth drivers plow ahead in a digital-first economy.

The only risk that could soften shares following the report is the forward guidance.

Bill Gates asserted that the U.S. economy will come back to “semi-normal” in the next 2 months, and I wouldn’t bet against management putting a positive spin on the path going forward tying the company’s short-term prospects with the comeback of the wider economy. By semi-normal, he means still falling economic growth, just at a slower rate.

There is a high probability that this “semi-normal” state of the economy will last for longer than we think, but even in that scenario, Microsoft will outperform competition widening the gap between the haves and have nots.

Another theme picking up traction is the massive volume of business that will migrate digitally and will want to work with a quality cloud provider who is not their direct competitor Amazon.

What is there to like about Microsoft?

Almost all of it is the short answer.

Momentum in Microsoft’s cloud computing platform is strong and has experienced a surge in usage becoming a lifeline to many companies that have been forced to go all digital.

Even in the cutthroat COVID-19 environment, I still believe Microsoft’s Azure cloud expanded 50% year over year in the past quarter.

Even more successful, Microsoft’s workspace communication product, Teams, has seen a dramatic surge in popularity as co-workers try to solve company problems remotely.

Teams broke a daily record of 2.7 billion meeting minutes, up 200% from 900 million minutes on March 16.

In late March, Teams has 44 million daily active users (DAU), and 93 firms have implemented Microsoft Teams in the Fortune 100.

Another strong data point is Microsoft 365 and Dynamics 365 suite of solutions.

Every company needs these platforms as a utility to boost enterprise productivity.

The subscriber base has benefited from the avalanche of remote workers with their array of tools.

Microsoft’s professional network LinkedIn platform is likely to show outperformance adding to the top line in the quarter to be reported.

Another outstanding segment that can’t be overlooked is gaming, and specifically a meaningful increase in the Xbox Live monthly active users and a boost in the adoption of Game Pass subscriptions.

The only negative segment that is probable will most likely be the hardware segment as a deteriorating trend in PC shipments in the first quarter rears its ugly head because of coronavirus crisis-induced supply constraints.

A demand shock doesn’t help as well.

Consumers just don’t have the cash to upgrade their Microsoft Surface computer-tablet hybrid device.

Total PC shipments in first-quarter 2020 declined 12.3% year over year to 51.6 million units.

Another damper on profitability could come in the form of higher investments in cloud and AI engineering, amid stiff competition from Amazon (AMZN) in the cloud computing vertical and Slack (WORK) in enterprise communication domain.

Even with the global economy coming to a standstill, growing cloud sales by 50% would represent a massive relative victory in the broader scheme of things.

As the economy opens back up, Microsoft is well-positioned to capture much more of the rapid transformation into digital the has been a dramatic side-effect form this pandemic.

The company is already worth over $1.3 trillion and in a new economic world where big tech gets bigger, I see nothing in their path that will slow them down.

The anticipation of the new reality that Microsoft will become more influential post-COVID gives way to a rapid recovery in shares that will only gain steam as the 5G revolution approaches.

Microsoft will easily become a $200 stock and if the U.S. economy opens up sooner than people expect, then nail down this stock for a price of $230 a share by year-end.

I am strongly bullish Microsoft for the rest of 2020.

Mad Hedge Technology Letter

March 30, 2020

Fiat Lux

Featured Trade:

(THE NEW CROWN JEWELS OF SOCIAL DISTANCING)

(DOCU), (SIRI), (ZNGA), (NOK), (AMZN), (WORK), (MSFT), (ZM)

The second tier of social distancing tech stocks will do well in this brave new world in which digital lives have superseded physical ones.

Sure, most of you already know that Amazon (AMZN), Slack (WORK), Microsoft (MSFT), Zoom Communications (ZM), and Teladoc Health (TDOC) are the crown jewels of current social distancing tech stocks, but there is another group that should also outperform.

Here are 4 that you should take a look at with DocuSign being the best of the bunch:

DocuSign (DOCU)

Teleconferencing and other niches have come front and center and consummating deals have migrated to one place since people cannot physically sign their name from pen to paper.

Electronic signatures were basically a cottage industry when it came out, but it is here to stay and this company has investors buzzing. Although the volume of business agreements being signed globally may temporarily slip, those that are continuing to work are enabled by DocuSign to close agreements without meeting eye to eye.

I expect resiliency in the type of products DocuSign provides and the remote implementation options.

DocuSign is well-positioned within the defensive category of digital transformation spend. Their recent acquisition of Seal Software will help boost DocuSign’s ability to leverage the power of artificial intelligence in the domain of contract analytics.

The opportunity to mitigate time spent on manual workflows through the addition of Seal to the portfolio can bolster the value proposition and drive ROI (return on investment) for customers.

The trajectory of the company was validated by DocuSign’s strong fourth-quarter earnings results with adjusted earnings increasing 12 cents per share which is a 100% increase year over year.

Just as impressive, DocuSign posted quarterly revenue of $274.9 million, an increase of 38%. As the data suggests, the signals all point to this company continuing its outperformance.

The e-document market has been monopolized by DocuSign with competition shut out, and as business goes 100% virtual in the current environment, this should have a positive network effect that will resonate when the world opens back up.

The next 3 stocks aren’t growth companies like DocuSign but are cheap stocks under $10 that might be worth a look.

Sirius XM Holdings (SIRI)

With all the extra time at home, satellite radio has hit the jackpot, making their services much more appealing.

Since Sirius and XM Radio merged in 2008, the combined Sirius XM Holdings has enjoyed a near-monopoly on satellite radio.

Sirius built on that with the 2018 acquisition of Pandora, the music streaming product, helping to fill the sails again with rapid revenue growth; its audio products now reach more than 100 million people.

Sirius' situation is appearing healthy and added a further 1.1 million subscribers in 2019 alone, bringing its total paying subscribers to roughly 30 million. The company's audacious strategy of partnering with auto manufacturers to pre-install SiriusXM in new models should help steadily grow the business.

Zynga (ZNGA)

This video game stock is cheap and could be a beneficiary of the stay at home revolution.

Zynga's portfolio of popular games, combined with hyper-charged growth, makes it one of the best cheap stocks to buy under $10.

Last quarter, the social gaming developer behind franchises like Words With Friends, Zynga Poker, CSR Racing, and FarmVille set new company revenue records up 48%.

While growth is likely to decelerate quickly from such temporary coronavirus catalysts, I expect double-digit revenue growth in 2020.

Still, Zynga is holding up remarkably well, especially in the COVID-19 era, as people increasingly turn to mobile devices for entertainment.

Nokia Corp. (NOK)

Nokia's expected earnings growth is impressive with Wall Street looking for an 8% bump in 2020 and roughly 30% profit growth in 2021.

Cheap stocks to invest in under $10 don't often come in the form of well-oiled global corporations valued at $15 billion.

The Finnish communication equipment telecom is one of the rare exceptions against the rule.

Sales have grown 14% annually for the last five years. Nokia may end up one of the 5G stocks to watch in the coming years because of the stigma of Huawei forcing many Europeans to go with brands closer to home.

Nokia pays a hefty 8% dividend as well and will never need a last-second bailout.