I have always considered the US military to have one of the world?s greatest research organizations. The frustrating thing is that their ?clients? only consist of the President and a handful of three and four star generals.

So I thought that I would review my notes from a dinner I had with General James E. Cartwright, the former Vice Chairman of the Joint Chiefs of Staff, who is known as ?Hoss? to his close subordinates.

Meeting the tip of the spear in person was fascinating. The four star Marine pilot was the second highest ranking officer in the US armed forces and showed up in his drab green alpha suit, his naval aviator wings matching my own, and spit and polished shoes.

As he spoke, I was ticking off the stock, ETF and futures plays that would best capitalize on the long term trends he was outlining.

The cycle of warfare is now driven by Moore?s Law more than anything else (XLK), (CSCO) and (PANW). Peer nation states, like Russia, are no longer the main concern.

Historically, inertia has limited changes in defense budgets to 5%-10% a year, but in 2010 defense secretary Robert Gates pulled off a 30% realignment, thanks to a major management shakeup. We can only afford to spend on winning current conflicts, not potential future wars. No more exercises in the Fulda Gap.

The war on terrorism will continue for at least 4-8 more years. Afghanistan is a long haul that will depend more on cooperation from neighboring Iran and Pakistan. ?We?re not going to be able to kill our way or buy our way to success in Afghanistan,? said the general.? However, the 30,000-man surge there brought a dramatic improvement on the ground situation.

Iran is a big concern and the strategy there is to interfere with outside suppliers of nuclear technology in order to stretch out their weapons development until a regime change cancels the whole program.

Water (PHO), (CGW) is going to become a big defense issue, as the countries running out the fastest, like Pakistan and the Sahel, happen to be the least politically stable.

Cyber warfare is another weak point, as excellent protection of .mil sites cannot legally be extended to .gov and .com sites.?

We may have to lose a few private institutions in an attack to get congress to change the law and accept the legal concept of ?voluntarism.? General Cartwright said ?Anyone in business will tell you that they?re losing intellectual capital on a daily basis.??

The START negotiations have become complicated by the fact that for demographic reasons, Russia (RSX) will never be able to field a million man army again, so they need more tactical nukes to defend against the Chinese (FXI).? The Russians are trying to cut the cost of defending against the US, so they can spend more on defense against a far larger force from China.

I left the dinner with dozens of ideas percolating through my mind, which I will write about in future letters.

https://www.madhedgefundtrader.com/wp-content/uploads/2013/07/General-James-Cartwright.jpg388313Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-07-01 01:07:432016-07-01 01:07:43My Briefing from the Joint Chiefs of Staff

Long-term observers of financial markets are befuddled, confused, and amazed at their complete lack of interest in the rapidly unfolding events in the Middle East.

It seems that the more horrific the atrocities, the higher stock prices want to climb.

Go figure.

ISIS is in fact accelerating the most important geopolitical event so far in this century, the rapprochement of relations between the U.S. and Iran, which have been in a deep freeze for 40 years.

A serious dialogue has not been held between these two countries since 52 hostages were seized at the American embassy in Tehran in 1979 and held for 444 days.

The Mullahs in Iran can?t help but notice last week?s U.S. air strikes to protect Shiite cities from a Sunni slaughter at the hands of ISIS. Suddenly, our natural enemy in the region has become our natural ally.

The Iranians have even offered to back up our air power with their ground forces, an offer the Obama administration has so far wisely turned down.

Don?t worry about ISIS. Their threat is being wildly overrated by the media.

There is a reason why terrorist groups have never held territory before. That makes them a big fat target for drones, smart bombs, and all the other types of fire that we rain down upon our enemies from above. This may be the first war in history entirely fought by drones on our side. That means it will be cheap, without casualties, and over quickly.

So what will the new treaty and peace between the U.S. and Iran bring us?

So far, Iran has agreed to a freeze on its nuclear enrichment program in exchange for international inspections and the unfreezing of $100 billion of their assets. Secret negotiations are being held intermittently in Geneva, Switzerland (I stopped by to say hello a few weeks ago).

This is unbelievably positive for all asset classes, except energy. This is the cause of the recent collapse of oil prices, which are now 65% off their 2014 high.

The US is now in a tremendously powerful negotiating position. If Iran dumps their nuclear program to our satisfaction, Iran then gets the carrot.

It will rejoin the world economy, unfreeze the rest of its assets and recover $100 billion a year in trade. The country?s banks will be allowed to rejoin U.S. dollar clearing, the $1 trillion a day CHIPS and SWIFT systems, their absence from which has been a deathblow to their international trade.

Its oil exports (USO) can recover from 750,000 barrels a day back to the pre crisis level of 3 million barrels. If it doesn?t then it gets the stick again in six months, resuming their economic freefall.

The geopolitical implications for the U.S. are enormous.? Iran is the last major rogue state hostile to the US in the Middle East, and it is teetering. The final domino of the Arab spring falls squarely at the gates of Tehran.

A friendly, or at least a non-hostile Iran, means we really don?t care what happens in Syria.

Remember that the first real revolution in the region was Iran?s Green Revolution in 2009. That revolt was successfully suppressed with an iron fist by fanatical and pitiless Revolutionary Guards.

The true death toll will never be known, but is thought to be well into the thousands. The antigovernment sentiments that provided the spark never went away and they continue to percolate just under the surface.

At the end of the day, the majority of the Persian population wants to join the relentless tide of globalization. They want to buy iPods and blue jeans, communicate freely through their Facebook pages and Twitter accounts, and have the jobs to pay for it all.

Since 1979, when the Shah was deposed, a succession of extremist, ultraconservative governments ruled by a religious minority, have abjectly failed to cater to these desires

If Iran doesn?t do a deal on nukes soon, it?s economy with sink deeper into the morass in which they currently find themselves. The Iranian ?street? will figure out that if they spill enough of their own blood that regime change is possible and the revolution there will reignite.

The Obama administration is now pulling out all the stops to accelerate the process.

The oil embargo former Secretary of State, Hillary Clinton, organized is steadily tightening the noose, with heating oil and gasoline becoming hard to obtain.

Yes, Russia and China are doing what they can to slow the process. This is what the Ukraine crisis is really all about, an attempt to keep oil prices high, Russia?s biggest earner.

But conducting international trade through the back door is expensive, and prices are rocketing. The unemployment rate is 40%.? The Iranian Rial has collapsed by 50%.

Let?s see how docile these people remain when the air conditioning quits running because of power shortages. Iran is a rotten piece of fruit ready to fall off on its own accord and go splat. The US is doing everything she can to shake the tree.

No military action of any kind is required on America?s part. No shot has been fired. That?s a big deal when the shots cost $10,000 apiece.

The geopolitical payoff of such an event for the U.S. would be almost incalculable. A successful revolution will almost certainly produce a secular, pro-Western regime whose first priority will be to rejoin the international community and use its oil wealth to rebuild an economy now in tatters.

Oil will has completely lost its risk premium, once believed by the oil industry to be $30 a barrel. A looming supply could cause prices to drop to as low as $20 a barrel.

This price drop seen so far amount to a gigantic $2.18 trillion trillion tax cut for not just the US, but the entire global economy as well (92 million barrels a day X 365 days a year X $65).

Almost all funding of terrorist organizations will immediately dry up. I might point out here that this has always been the oil industry?s worst nightmare.

ISIS is a short.

At that point, the US will be without enemies, save for North Korea, and even the Hermit Kingdom could change with a new leader in place. A long Pax Americana will settle over the planet.

The implications for the financial markets will be enormous. The US will reap a peace dividend as large, or larger, than the one we enjoyed after the fall of the Soviet Union in 1992.

As you may recall, that black swan caused the Dow Average to soar from 2,000 to 10,000 in less than eight years, also partly fueled by the technology boom.

A collapse in oil imports will cause the U.S. dollar (UUP) to rocket.? An immediate halving of our defense spending to $400 billion or less and burgeoning new tax revenues would cause the budget deficit to collapse.

With the US government gone as a major new borrower, interest rates across the yield curve will fall further. The national debt completely disappears by the 2030?s (as it almost did during the late 1990?s).

A peace dividend will also cause US GDP growth to reaccelerate from 2% to 4%. Risk assets of every description will soar to multiples of their current levels, including stocks, junk bonds, commodities, precious metals, and food.

The Dow will soar to 30,000 and the S&P 500 (SPY) to 3,500, the Euro collapses to parity, gold rockets to $2,300 an ounce, silver flies to $100 an ounce, copper leaps to $6 a pound, and corn recovers $8 a bushel.

Some 2 million of the armed forces will get dumped on the job market as our manpower requirements shrink to peacetime levels. But a strong economy should be able to soak these well-trained and motivated people right up.

We will enter a new Golden Age, not just at home, but for civilization as a whole.

Wait, you ask, what if Iran develops an atomic bomb and holds the US at bay?

Don?t worry. There is no Iranian nuclear device. There is no real Iranian nuclear program large enough to threaten the United States. The entire concept is an invention of Israeli and American intelligence agencies as a means to put pressure on the regime.

According to them, Iran has been within a month of producing a tactical nuclear weapon for the last 30 years. I'm still waiting.

The head of the miniscule effort they have was assassinated by Israeli intelligence two years ago (a magnetic bomb, placed on a moving car, by a team on a motorcycle, nice!).

If Iran had anything substantial in the works, the Israeli planes would have taken off a long time ago.

Even if Iran had one nuclear weapon, would they really want to attack a country with 6,700, the US?

There is no plan to close the Straits of Hormuz, either. The training exercises in small rubber boats we have seen are done for CNN?s benefit, and comprise no credible threat.

I am a firm believer in the wisdom of markets, and that the marketplace becomes aware of major history changing events well before we mere individual mortals do.

The Dow began a 25-year bull market the day after American forces defeated the Japanese in the Battle of Midway in May of 1942, even though the true outcome of that confrontation was kept top secret for years.

If the advent of a new, docile Iran were going to lead to a global multi-decade economic boom and the end of history, how would the stock markets behave now?

They would remain in a long-term bull market, much like we have seen for the past six years. That?s why 10% corrections have been few and far between.

The Problem is That it?s a Hollow Threat

Aim This One at the Bears

https://www.madhedgefundtrader.com/wp-content/uploads/2014/09/Missile-e1409784440285.jpg235400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-08-26 01:06:452015-08-26 01:06:45What?s Really Happening in the Middle East

Mad Day Trader Jim Parker is expecting the first quarter of 2015 to offer plenty of volatility and loads of great trading opportunities. He thinks the scariest moves may already be behind us.

After a ferocious week of decidedly ?RISK OFF? markets, the sweet spots going forward will be of the ?RISK ON? variety. Sector leadership could change daily, with a brutal rotation, depending on whether the price of oil is up, down, or sideways.

The market is paying the price of having pulled forward too much performance from 2015 back into the final month of 2014, when we all watched the December melt up slack jawed.

Jim is a 40-year veteran of the financial markets and has long made a living as an independent trader in the pits at the Chicago Mercantile Exchange. He worked his way up from a junior floor runner to advisor to some of the world?s largest hedge funds. We are lucky to have him on our team and gain access to his experience, knowledge and expertise.

Jim uses a dozen proprietary short-term technical and momentum indicators to generate buy and sell signals. Below are his specific views for the new quarter according to each asset class.

Stocks

The S&P 500 (SPY) and NASDAQ have met all of Jim?s short-term downside targets, and a sustainable move up from here is in the cards. But if NASDAQ breaks 4,100 to the downside, all bets are off.

His favorite sector is health care (XLV), which seems immune to all troubles, and may have already seen its low for the year. Jim is also enamored with technology stocks (XLK).

The coming year will be a great one for single stock pickers. Priceline (PCLN) is a great short, dragged down by the weak Euro, where they get much of their business. Ford Motors (F) probably bottomed yesterday, and is a good offsetting long.

Bonds

Jim is not inclined to stand in front of a moving train, so he likes the Treasury bond market (TLT), (TBT). He thinks the 30-year yield could reach an eye popping 2.25%. A break there is worth another 10 basis points. Bonds are getting a strong push from a flight to safety, huge US capital inflows, and an endlessly strong dollar.

Foreign Currencies

A short position in the Euro (FXE), (EUO) is the no brainer here. The problem is one of good new entry points. Real traders always have trouble selling into a free fall. But you might see profit taking as we approach $1.16 in the cash market.

The Aussie (FXA) is being dragged down by the commodity collapse and an indifferent government. The British pound (FXB) is has yet to recover from the erosion of confidence ignited by the Scotland independence vote and has further mud splattered upon it by the weak Euro.

Precious Metals

GOLD (GLD) could be in a good range pivoting off of the recent $1,140 bottom. The gold miners (GDX) present the best opportunity at catching some volatility. The barbarous relic is pulling up the price of silver (SLV) as well. Buy the hard breaks, and then take quick profits. In a deflationary world, there is no long-term trade here. It is a real field of broken dreams.

Energy

Jim is not willing to catch a falling knife in the oil space (USO). He has too few fingers as it is. It has become too difficult to trade, as the algorithms are now in charge, and a lot of gap moves take place in the overnight markets. Don?t bother with fundamentals as they are irrelevant. No one really knows where the bottom in oil is.

Agriculturals

Jim is friendly to the ags (CORN), (SOYB), (DBA), but only on sudden pullbacks. However, there are no new immediate signals here. So he is just going to wait. The next directional guidance will come with the big USDA report at the end of January. The ags are further clouded by a murky international picture, with the collapse of the Russian ruble allowing the rogue nation to undercut prices on the international market.

Volatility

Volatility (VIX), (VXX) is probably going to peak out her soon in the $23-$25 range. The next week or so will tell for sure. A lot hangs on Friday?s December nonfarm payroll report. Every trader out there remembers that the last three visits to this level were all great shorts. However, the next bottom will be higher, probably around the $16 handle.

If you are not already getting Jim?s dynamite Mad Day Trader service, please get yourself the unfair advantage you deserve. Just email Nancy in customer support at support@madhedgefundtrader.com and ask for the $1,500 a year upgrade to your existing Global Trading Dispatch service.

Volatility Weekly

Volatility Monthly

Euro to the Dollar

https://www.madhedgefundtrader.com/wp-content/uploads/2015/01/Volatility-Weekly.jpg325579Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-01-08 09:44:082015-01-08 09:44:08Mad Day Trader Jim Parker?s Q1, 2015 Views

Since I am in a major patting myself on the back mood, I thought I would rerun a piece I ran last October entitled ?Apple is Ready to Explode?. This is back when the shares were trading at a lowly $490 a share.

Since then I have been urging readers to get in on the long side at every opportunity. They are now up a mind boggling 43% from that timely recommendation. They are laughing all the way to the bank.

?You have to be impressed how Apple shares have been trading during the Washington shutdown and the debt ceiling crisis. While other highflying technology stocks have crashed and burned, Apple has held like the Rock of Gibraltar.

Is this presaging much better things to come?

After the bar was set extremely low in the run up to the iPhone 5s launch, there has been an onslaught of good news. The first weekend sales came in at a staggering 9 million units, nearly double analyst forecasts. That?s a lot of units to be wrong by.

This has led to a series of broker upgrades by Cantor Fitzgerald, Cowen & Co., Piper Jaffray, Sanford Bernstein, and most recently by Jeffries. Entrenched bears are slowly an inexorably turning into bulls. Targets range up to $780.

During the summer, when the shares were trading in the low $400?s, Apple emerged as the largest buyer of its own stock. Still, it only made a dent in the $60 billion the company has dedicated to the program.

Of course, corporate raider and green mailer Carl Icahn (he lived in my building in Manhattan and was always a bit of a jerk) wants Apple to buy $160 billion of its stock, about $36% of the total market capitalization. But with a position of only $2 billion, Carl doesn?t have enough skin in the game to get anything more than a free dinner from CEO Tim Cook.

Still, the more Icahn bangs the drum about the value of Apple, the more money he sucks in. His blustering has probably added about $50 to the stock price. That works for me.

Like the Origin of the Universe and the 105-year long losing streak suffered by the Chicago Cubs baseball team, the cheapness of Apple shares is one of those mysteries that baffles investors. Sure, you?d expect some natural profit taking after the meteoric 15 year run in the shares, from $4 to $707. But a 46% drawdown is a lot, and many would say too much.

The company has eye popping net profits of $3.5 million per business hour (click here for the most recently quarterly announcement). Some one third of it capitalization, or $150 billion, sits in cash in European bank accounts.

That works out to $165 of the current $490 share price. This brings the ex cash trailing price earnings multiple down to a subterranean 11.8 times, or a 25% discount to the 16X market multiple. The dividend yield of 2.5% still exceeds that of the ten year Treasury bond. This is absurdly cheap.

Anyone who makes their living looking at the numbers has been loading up on the stock for the past eight months. Even permabear and short seller, Jim Chanos, has been buying on the theory that both Apple, and competitor Samsumg, together have been demolishing the Wintel architecture.

I think there is something important going on here. Apple is bringing out the next generation iPad in two weeks. Product refreshes for the iMac, Macbook, and Airbook in coming months are already well known. Every time an announcement of an announcement is made, the stock spikes $10.

But the 800-pound gorilla in Apples earnings stream is the iPhone, which accounts for more than 70% of its profits. The wildly successful 5s and 5c launches will take total smart phone sales from around 36 million in Q3 to at least 56 million units in Q4. The analyst community is nowhere near these numbers, so they are substantially underestimated the profitability of the company.

Apple has already cracked the China market for cash buyers with the latest upgrade of its wireless operating system. The whale here is a deal with China Mobile (CHL) with its 740 million customers, which has been to subject to on again and off again negations for years. Still, Apple has already told its manufacturers to add china Mobile to its approved carrier list.

I think the stock is beginning to discount the launch of the iPhone 6, which is still a distant 11 months away. That will take the company another generation ahead, with an expansive six-inch screen and a blazing fast A8 processor, leaving competitors in the dust.

The business is so big that my favorite airline, Virgin America, has initiated nonstop service from San Francisco to Austin. I?m told the plane is always full. That?s where they make processors for the new phones.

All of this leads me to believe that Apple will be a major mover in 2014. The chip shot is $600, and we get a real head of steam into the iPhone 6 rollout, we could match the old high at $707.

You can buy the stock here with some comfort. If you are hyper aggressive, try playing the weekly call options on the next breakout. The more cautious can settle for the Technology Select Sector SPDR ETF (XLK), or the ProShares Ultra Technology 2X leveraged ETF (ROM). Apple has major weightings in both of these ETF?s.?

For the link to the original story, please click here.

So Where is the Power Button on this Thing?

https://www.madhedgefundtrader.com/wp-content/uploads/2013/10/Gibraltar.jpg331496Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-08-20 08:46:282014-08-20 08:46:28Apple Breaks $100

You have to be impressed how Apple shares have been trading during the Washington shutdown and the debt ceiling crisis. While other highflying technology stocks have crashed and burned, Apple has held like the Rock of Gibraltar. Is this presaging much better things to come?

After the bar was set extremely low in the run up to the iPhone 5s launch, there has been an onslaught of good news. The first weekend sales came in at a staggering 9 million units, nearly double analyst forecasts. That?s a lot of units to be wrong by.

This has led to a series of broker upgrades by Cantor Fitzgerald, Cowen & Co., Piper Jaffray, Sanford Bernstein, and most recently by Jeffries. Entrenched bears are slowly an inexorably turning into bulls. Targets range up to $780.

During the summer, when the shares were trading in the low $400?s, Apple emerged as the largest buyer of its own stock. Still, it only made a dent in the $60 billion the company has dedicated to the program.

Of course, corporate raider and green mailer Carl Icahn (he lived in my building in Manhattan and was always a bit of a jerk) wants Apple to buy $160 billion of its stock, about $36% of the total market capitalization. But with a position of only $2 billion, Carl doesn?t have enough skin in the game to get anything more than a free dinner from CEO Tim Cook. Still, the more Icahn bangs the drum about the value of Apple, the more money he sucks in. His blustering has probably added about $50 to the stock price. That works for me.

Like the Origin of the Universe and the 105-year long losing streak suffered by the Chicago Cubs baseball team, the cheapness of Apple shares is one of those mysteries that baffle investors. Sure, you?d expect some natural profit taking after the meteoric 15 year run in the shares, from $4 to $707. But 46% is a lot, and many would say too much.

The company earns an eye popping net profits of $3.5 million per business hour (click here for the most recent quarterly announcement). Some one-third of it capitalization, or $150 billion, sits in cash in European bank accounts. That works out to $165 of the current $490 share price. This brings the ex cash trailing price earnings multiple down to a subterranean 11.8 times, or a 25% discount to the 16X market multiple. The dividend yield of 2.5% still exceeds that of the ten year Treasury bond. This is absurdly cheap.

Anyone who makes their living looking at the numbers has been loading up on the stock for the past eight months. Even permabear and short seller, Jim Chanos, has been buying on the theory that both Apple and competitor Samsumg together have been demolishing the Wintel architecture.

I think there is something important going on here. Apple is bringing out the next generation iPad in two weeks. Product refreshes for the iMac, Macbook, and Airbook in coming months are already well known. Every time an announcement of an announcement is made, the stock spikes $10.

But the 800-pound gorilla in Apples earnings stream is the iPhone, which accounts for more than 70% of its profits. The wildly successful 5s and 5c launches will take total smart phone sales from around 36 million in Q3 to at least 56 million units in Q4. The analyst community is nowhere near these numbers, so they are substantially underestimating the profitability of the company.

Apple has already cracked the China market for cash buyers with the latest upgrade of its wireless operating system. The whale here is a deal with China Mobile (CHL) with its 740 million customers, which has been to subject to on again and off again negations for years. Still, Apple has already told its manufacturers to add China Mobile to its approved carrier list.

I think the stock is beginning to discount pending the launch of the iPhone 6, which is still a distant 11 months away. That will take the company another generation ahead, with an expansive six-inch screen and a blazing fast A8 processor, leaving competitors in the dust. The business is so big that my favorite airline, Virgin America, has initiated nonstop service from San Francisco to Austin. I?m told the plane is always full.

All of this leads me to believe that Apple will be a major mover in 2014. The chip shot is $600, and we get a real head of steam into the iPhone 6 rollout, we could match the old high at $707. You can buy the stock here with some conform. If you are hyper aggressive, try playing the weekly call options on the next breakout. The more cautious can settle for the Technology Select Sector SPDR ETF (XLK), or the ProShares Ultra Technology 2X leveraged ETF (ROM). Apple has major weightings in both of these ETF?s.

So Where is the Power Button On This Thing?

https://www.madhedgefundtrader.com/wp-content/uploads/2013/10/Gibraltar.jpg331496Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-10-11 01:03:242013-10-11 01:03:24Apple is Ready to Explode

If it hasn?t happened by today, then it is no more than a week away. The deep discount suffered by American stocks is about to go away. Thanks to the manufactured uncertainty emanating from the nation?s capital created by the government shutdown, stocks have been selling at a 10% or more discount to where they should be.

As things stand, the shutdown is chopping about 1/8% a week from America?s GDP growth. If it runs for another week, it will add up to a 0.25%. What economists haven?t considered in these figures is the additional 0.25% loss that will come from a restart of the government. People are so afraid of the shocking cessation of many government services that they are cleaning out ATM?s, forcing the banks to maintain higher than normal cash levels.

The 2013 Federal budget provides for $3.8 trillion in government spending out of a $16.5 trillion GDP, some 23%. I tried to get more precise figures by clicking the link for the Department of Commerce Bureau of Economic Analysis website (http://www.bea.gov/index.htm ), and was greeted by the closest thing you can imagine for a middle fingered salute. You just don?t snap your fingers and expect a quarter of the economy to sprint out of the blocks.

There is another cost to consider. All government statistics have been rendered meaningless for the rest of the year. Even if the government restarts tomorrow, aberrations in the data will plague us well into next year, making economic forecasts more difficult and less meaningful than usual. This is when the moving averages for data series will really earn their pay.

My political theory for the past three years has been that the Tea Party wing of the Republican Party will act unimaginably stupid, dragging governance to new lows, wreaking the maximum amount of damage possible. They feel that if they can?t own the government, they must break it.

Gerrymandering means they can?t be dislodged by elections. These people are being cheered by supporters for their appalling behavior back home in the heartland of America. This will ultimately lead to the destruction of the Republican Party, and is why President Obama is quite happy to sit on his hands and do nothing. Why interfere when your opponent is committing suicide?

So far I have been right on the money. An accurate political read has been a major element in delivering my 100% gain since the end of 2010, no matter how unpopular it may be.

This analysis has the government shutdown lasting until October 17, little more than a week from today, and vastly longer than expected. That?s the day the government shutdown rolls into the debt ceiling crisis. With far more cataclysmic consequences at stake, this crisis has a greater likelihood of getting solved.

This is all spectacular news for investors, who have recently been boning up on their history. The 17 government shutdowns since 1975 have averaged six days. After each one, stock rose by an average 7.8% in the following six months, and by 13.2% over the following year. We could be in for similar returns in this round. ?It looks like its going to be off to the races once again, and my yearend target of 1,780 for the (SPY) is looking good.

The 0.5% in growth we are losing this quarter will get rolled into the next. Q1, 2014 was already setting up to be hot, thanks to a global synchronized recovery in the US, Europe, Japan, China, and even Australia. Some 60% of world GDP is now enjoying unprecedented easy money. This concentration of more growth into the next quarter could take the US GDP figure as high as an annualized 3.5%.

Portfolio managers have already figured this out, which is why they are relentlessly buying every dip, and explains the modest 3.5% drop in the S&P 500 we have seen since the shutdown began. Providing additional rocket fuel is the fact that many firms are under the gun to get new money into the market by the end of the year.

There is one certainty here. The shutdown firmly takes a taper by the Federal Reserve off the table for 2013. It turns out that Ben Bernanke correctly read that the Tea Party would drive the economy off a cliff, and that the safety net of continued monetary stimulus was needed. Nice call, Ben! This will give the bulls the fodder they need to take stock prices up all the way until next spring, when we may finally get a real taper.

I would be using the down days from here on to scale into the hottest sectors of the market, especially the 2X leveraged ETF?s. You can do this with consumer discretionary stocks with the (XLY), (UCC), industrials with (XLI), (UXI), technology with (XLK), (ROM), and with health care through the (XLV), (RXL).

This is what I really want to know. Last Sunday, the hit TV drug show, Breaking Bad, saw its series finale. The cult terrorism drama, Homeland, delivered its third season opener at the same time. The next day, the government closed.

Do you think there is a connection?

Is There a Connection?

https://www.madhedgefundtrader.com/wp-content/uploads/2013/10/National-Parks-Closed.jpg357541Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-10-07 01:04:392013-10-07 01:04:39Say Goodbye to the Washington Discount

Apple blew away the bears today with the issuance of $17 billion in bonds, the largest such corporate debt issue in history. Spread over two, five, ten, and 30 years, the deal was oversubscribed by more than 3:1, with $40 billion in demand left unfilled.

Foreign investors took down a major part of the deal, which explains Deutsche Bank?s senior role in the syndicate. The yield on the ten-year bonds came in at 2.40%, a mere 70 basis points over equivalent US Treasury paper.

The mega deal, dubbed ?iBonds? by traders, underlies the tremendous shortage of high-grade fixed income securities worldwide. Since 2007, the amount of double ?A? or better rated paper has declined by 60%, thanks to widespread downgrades inspired by the newfound religion of the ratings agencies.

As I never tire of pointing out at my strategy luncheons and lectures, the principal sin of governments is not that they are borrowing too much money, but not enough. This has given us a global bond shortage that has taken returns to insanely low levels. Look no further than the ten-year yield of 1.68% in the US, 1.20 % in Germany, and a pitiful 0.60% in Japan.

The issue also highlights the sudden fascination of all things Apple since its better than expected calendar Q1 earnings report last week, with $43 billion in revenues spinning off $9.5 billion in profits. Since then, we learned that the richest man in Russia, Alisher Usmanov, soaked up some $100 million of stock close to the $392 bottom. This is a man who?s proven track record of market timing is uncanny.

It doesn?t require a lot of imagination to figure out what this deal is all about. With $145 billion in cash on the balance sheet, why borrow another $17 billion? The reality is that this is a way of repatriating, through the back door and tax-free, some of the estimated $100 billion in cash the company has parked in offshore bank accounts.

What will it do with the money? How about buying back $17 billion worth of stock? Buy borrowing at 2.4% and retiring 3.2% dividend stock, the yield pick up on the transaction comes to $136 million a year. That goes straight to the bottom line. The deal reminds me of the kind of financial engineering that dominated Japanese finance during the late 1980?s. When I was a director of Morgan Stanley, I signed many of these multi billion dollar deals as a co-manager.

It wasn?t just Apple that has returned from the grave, which saw its stock rise by 14% since last week?s two year low. Look at many of the old tech warhorses, like Microsoft (MSFT), Applied Materials (AMAT), Hewlett Packard (HPQ), and Intel (INTC), which have blasted forth from long moribund levels in recent weeks.

Which raises an interesting possibility. What if the long predicted selloff in May does a no show? What if, instead of the usual 10%-25% swan dive, we only get the 2.5% that has been the pattern for 2013? The possibilities boggle the mind.

In that case where will the money flood into next? Stocks that have been going up like a rocket for the past eight months, or shares that have either fallen like a stone during this time, or barely budged? Stocks that are trading at double the market multiple, or at half the market multiple? Hmmmm. Let me think about this one.

There are two major categories of the latter, commodity related shares and technology ones. China is still slowing, placing a monkey on the back of most commodities related companies. So I vote for technology, which by the way, is the cheapest it has ever been on an earnings multiple basis.

In that case, the strength in old tech will develop into far more than a one-week wonder. It could provide the rocket fuel that will power the major indexes for the rest of the year. That would take the S&P 500 up to 1,700 where it can flaunt a glitzy earnings multiple of 17.

Don?t get too giddy. This is definitely a best-case scenario. But then lately, the best-case scenarios have been happening, thanks to the reflationary efforts of our friend, Ben Bernanke.

That would be fantastic news for Apple?s long-suffering shareholders. Now that its stock has clearly broken through the 50-day moving average on the upside, the eventual target of this leg could be as high as the 200-day moving average at $541. One can only hope.

Old Tech is Rising From the Dead

https://www.madhedgefundtrader.com/wp-content/uploads/2013/05/Dracula.jpg268337Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-05-01 09:26:212013-05-01 09:26:21Old Tech?s Big Comeback

When Japanese central bank governor, Haruhiko Kuroda, announced the most aggressive monetary stimulus program in history last week, he no doubt expected Tokyo share prices to head for the moon. In that, he has succeeded admirably, the yen hedged Japanese equity ETF (DXJ) soaring by 13.4% in the five trading days since he lobbed his bombshell.

What the bespectacled bureaucrat did not anticipate was that his action would send American shares through the roof as well. Both the Dow average and the S&P 500 surged to new all time highs today, much of the move powered by new Japanese cash. Just when American traders were wringing their hands over the potential loss of quantitative easing, they instead were handed a second campaign of ultra monetary easing.

Until last week, the Fed was pumping $85 billion a month into the financial system. From this week, the Fed plus the BOJ monthly total doubles to $170 billion. I don?t have to draw pictures for you to explain what this means for stock prices.

Indeed, the BOJ?s fingerprints could be found daily on securities of almost every imaginable description. What they have been buying is size exchange traded funds of equities (ETF?s) and bonds of every maturity. Imagine the Fed coming in one morning, calling all the major brokers, and placing orders for a billion dollars each of the (SPX) and the (IWM). That is what?s happening in Japan now.

The problem is that domestic investors in Japan have been unloading positions they have been lugging for years to the central bank, and then reinvesting the cash into better quality, higher yielding US stocks. Notice how well the big cap dividend yielders have been trading, favorite targets of foreign investors. Notice, also, that technology appears to be staging a turnaround on the back of the international money, with recent pariah, Apple (AAPL) actually showing signs of life.

It?s easy to see why this is happening. If you were a Japanese investor, would you want to buy a low growth, low yielding stock in a depreciating currency? Or buy a share in a faster growing company with a much higher dividend an appreciating currency. I rest my case. God bless America!

Needless to say, beyond the sunset made a complete hash of my few remaining short positions in the S&P 500, which only had seven days left to run into expiration. Thank you, Mr. Market for my biggest loss of the year.

Fortunately, that hickey was more than generously offset by profits on shorts I harvested last week, in addition to remaining longs in Bank of America (BAC), Apple (AAPL), and hefty shorts in the yen. As of this writing, I am up a breathtaking 37% so far in 2013.

Where does this party end? Now that we have two QE?s, instead of just one, I think it is safe to say that risk assets everywhere are going much higher. How high is anyone?s guess. It also means that the ?RISK OFF? assets of gold (GLD), silver (SLV), and Treasury bonds (TLT) are headed lower. That?s why I added a long in the leverage short Treasury bond ETF (TBT) this week for the first time in years. The punch bowl just got topped up again, and I don?t have to be asked twice to refill my glass.

The Punch Bowl Has Just Been Refilled

https://www.madhedgefundtrader.com/wp-content/uploads/2013/04/Punch-Bowl.jpg288353Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-04-11 09:30:212013-04-11 09:30:21Japanese Cash Tsunami Hits US

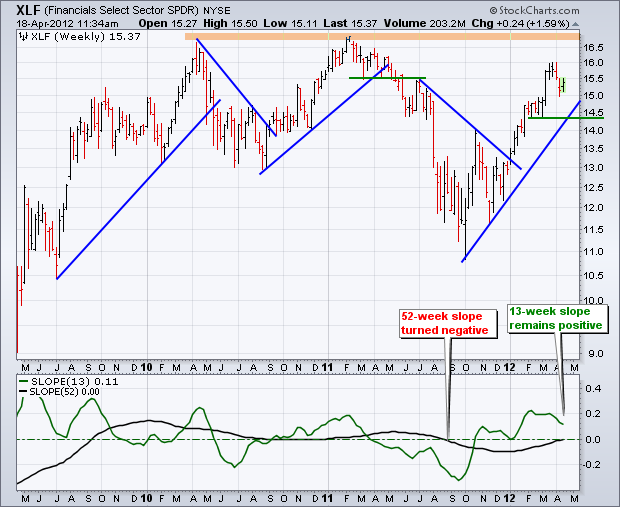

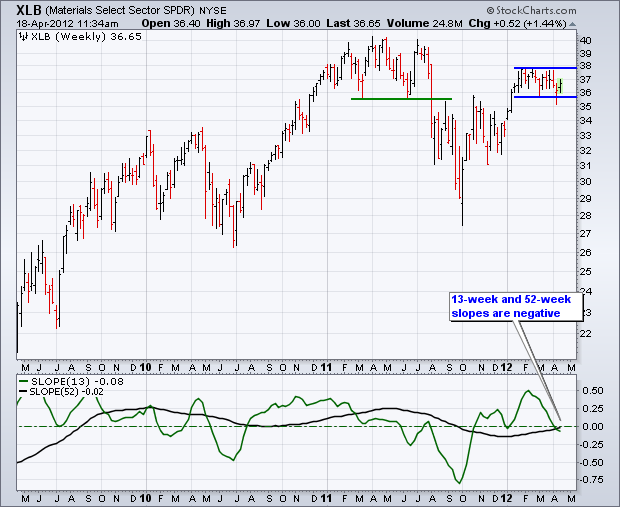

I ran through a number of charts provided by my friends at Stockcharts.com, and as a person who has been piling on the shorts for the past two weeks I was greatly encouraged. Almost every single one was pregnant with gloomy implications. This is all happening a mere 12 days before the Great Escape in May commences. Virtually every technical indicator I follow is now flashing warning signs and ringing alarm bells.

Here is my own personal interpretation. The Russell 2000 (IWM) could potentially be setting up a head own shoulder top targeting $75 on the downside. My short here is one of my biggest positions. The Consumer Discretionary Select SPDR (XLY) is pulling away from the absolute top end of its upward channel and is ripe for a 10% pullback. Ditto for the Technology Select Sector SPDR (XLK), which could give back 15%. The Financials Select Sector SPDR (XLF), one of the hottest areas this year, could actually be setting up a new downtrend. The same is true for the Materials Select Sector SPDR (XLB). And tell me that is not a double top in the Industrials Select Sector SPDR (XLI).

This all suggests that 1,325 for the S&P 500 is a chip shot on the downside, and maybe more. I have a feeling that killings are about to me made on the short side.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-04-18 23:02:122012-04-18 23:02:12Check Out These Interesting Charts

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.