Mad Hedge Technology Letter

May 21, 2021

Fiat Lux

Featured Trade:

(THE STRENGTH OF AMD)

(AMD), (INTC), (TSM), (XLNX), (SMH)

Mad Hedge Technology Letter

May 21, 2021

Fiat Lux

Featured Trade:

(THE STRENGTH OF AMD)

(AMD), (INTC), (TSM), (XLNX), (SMH)

Advanced Micro Devices Inc. (AMD) is a chip stock that needs some serious attention, even more so because of their new share repurchase program that has no end date.

They are led by one of the best tech CEOs in Silicon Valley Lisa Su, who has been in charge since 2014.

She transformed the company into a profitable one, secured incremental market share from Intel Corp. (INTC) and diminished concerns that AMD has a weak balance sheet.

Strength begets strength as AMD introduced a $4 billion stock buyback plan, its first repurchase authorization since 2001, signaling the chipmaker’s robust momentum in their own business.

The buyback will be distributed through cash from operations and will total about 4% of AMD’s market value.

AMD's stock in the high $70s right here looks like a screaming buy.

Share buyback is not only something Apple and Microsoft do, but other smaller players are getting in on the action displaying the great breadth and depth of the tech market.

We don’t see this anywhere else in any other industry because profitable companies simply return money back to shareholders and tech has the luxury of accelerated future earnings and revenue growth to buttress this.

Cut it up however you want, the tech sector is responsible for the bulk of earnings as it relates to the total market and that won’t change.

AMD delivered $832 million in free cash flow in Q1 2021.

The company has now pivoted from a net debt position to a balance sheet that will harness over $3 billion in net cash by the end of the current quarter.

This strength of the balance sheets is even pertinent if you strip out the Xilinx deal which will bring in their own array of financial pluses to add on to the might of AMD's current cash flow situation.

An accumulating share count is something to be wary of in any stock and given that AMD had the opportunity to reduce share count, it was a no-brainer.

Years ago, AMD had 766 million shares outstanding, and it would have climbed to over 1.6 billion considering the Xilinix shares by the end of this year.

This obviously makes EPS metrics appear rosier in future earnings reports and inching them up is a nod to AMD CFO Devinder Kumar who usually has a big say in these decisions.

Under Su’s helmsmanship, the company’s market value has toppled the $90 billion mark from only $2 billion just seven years ago.

That was the year she was named CEO and she hasn’t looked back.

Su’s key to returning AMD to profitability was to rely on the quality of product delivered — these new products snatched market share from Intel.

As what a savvy CEO usually does, she has played down success in order to tamper down high expectations in the stock price and business by saying, “without a doubt it does not get easier.”

I don’t think it was ever easy to begin with but that’s beside the point.

Su’s AMD has gone from an inferior chipmaker building cheaper knockoffs to Intel products to a premium provider of computer processors that win orders solely based on superior performance.

AMD has already repurchased $77 million of stock in its prior buyback plan two decades ago.

Su has rejuvenated AMD’s reputation and performance at a critical juncture and as chip shortages become the norm in this boom-and-bust industry.

The public health problem triggered a crazy demand for remote work and the devices that facilitate a work from home economy.

During this sensitive period, the world’s largest chipmaker, Intel, had struggled to develop its manufacturing technology, one of the foundations of its decades-long dominance of the computer industry.

The chip shortage is an example of the periodic mismatch between supply and demand in the semiconductor market whose companies avoid dipping into capital expenditure until capacity is stretched to the extreme limit.

This is an expensive business to get into, constructing high-performance chips is time-consuming and an engineering headache, thus barriers of entry are incredibly insurmountable.

Most new chip foundries and designers don’t happen unless sovereign nations make it a national security issue which is the case lately.

Ancillary industries started to hoard chips 6-8 months ago and I believe that these pressures will begin to subside soon as supply chains start to normalize.

These longer-term contracts to secure inputs we are seeing now will eventually be reduced easing the supply crunch as demand begins to slow and capacity begins to rise.

Even Su predicts supply of AMD chips, which are built by Taiwan Semiconductor Manufacturing (TSM), will catch up throughout 2021.

As the tech consolidation rips through chip stocks, I see this as an unequivocal buying opportunity for the strongest of names.

If AMD continues to build on their strong financial position — continue to offer more share repurchases and even a sweet dividend — it clearly means they are building premium products buyers want and that satisfaction not only filters down to the end-user of their chips but the owners of the stock.

I first recommended this stock at $18 at the advent of the Mad Hedge tech letter in 2018, and I am still bullish AMD long term period.

It was a great company in 2018 — it’s gotten even better in 2021 — don’t miss out.

Mad Hedge Technology Letter

October 30, 2020

Fiat Lux

Featured Trade:

(THE TWO CAN'T-MISS CHIP COMPANIES)

(NVDA), (AMD), (XLNX), (ARM)

I want to talk about two companies that are the “no-brainers” of the semiconductor space that would give you a call option on the data center space.

Let’s take a quick look back at some of their latest moves and what it would mean for your tech portfolio.

A few months ago, Nvidia said it would buy British chip company Arm from SoftBank for $40 billion in a stock and cash deal.

CEO Jensen Huang admitted that while the company's acquisition of the rival British chipmaker was a little on the expensive side, it would make sense in the long-term.

“I had to pay you an arm and a leg for it,” the Nvidia CEO said, and “I told you I was going to be the last and highest bidder.”

Overpaying for high quality companies is something that is only possible from a position of strength.

Huang justified Arm’s price tag saying that the chipmaker’s network of customers made it worthwhile and that he wants to expose those customers to Nvidia’s artificial intelligence technology.

Cross-selling the products and services is where the synergies between the companies can be exploited.

AMD is the other player that is really crushing it along with Nvidia and they recently made a deal to acquire Xilinx.

The deal is a direct response to Nvidia’s attempts to become the leader in high performance computing.

Obviously, the acquisitions are made possible because of years of refining their balance sheets and buying into more growth is a time-honored strategy that tech companies focus on.

AMD will give Nvidia a run for their company with a combined additional 13,000 talented engineers and over $2.7 billion in annual R&D investments.

This is very much a talent grab as well as a revenue grab.

Xilinx offers AMD access to adaptive platforms in critical areas such as 5G and automotive.

The tie-up is a transformational opportunity to tap into a total addressable market of $110 billion, up from previous AMD standalone estimates of $79 billion for 2022.

Xilinx adds about $31 billion to the total addressable market and on the operational side, AMD will see gross margins spike from 45% to 51%.

Even more impressive, operating income margins will surge to 21%, up from 16%.

It’s not like AMD needed much help, as they smashed expectations by growing 55.6% and beating estimates by $240 million in the latest earnings report.

EPS beat analyst estimates by $0.06 providing the highest level of earnings in years at $0.41 per share.

The Computing and Graphics division beats estimates with revenues of $1.67 billion.

The ramp-up of new consoles and data center sales led to a mindboggling 101% sequential revenue increase.

The company’s server processor revenue almost doubled compared with the year earlier, and AMD is on track to begin shipping its next-generation server processors later this year.

The current and future status of gaming is very much tied to the fortunes of Nvidia and AMD and the pandemic has fueled massive migration to time spent playing video games.

Who would have thought if people can’t go outside, more video games would be played?

The new generation of consoles is set to launch in November from Microsoft (MSFT) and Sony (SNE) which has helped boost AMD’s gaming chip business.

Typically, this gaming chip segment drops in the fourth quarter, but this year it will mushroom because of the new console launches and ramp-up in production and sales.

Ultimately, in terms of the Xilinx (XNLX) deal, it is complimentary to AMD’s business – an appetizer to the main dish.

It will help improve the company’s ability to support data center customers and adds exposure to sectors such as automotive, aerospace, defense, and industrials.

Through Xilinx’s field-programmable gate array (FPGA) chips—or semiconductors that can be reprogrammed after production, unlike most semiconductors—AMD could benefit from the tail end of the 5G upgrade cycle, too.

That’s because with many emerging technologies, it’s too expensive to experiment with chips with instructions that are set in stone, and build emerging infrastructure such as 5G.

Xilinx’s businesses also tend to retain customers for longer because its strong designs can lead to longer product cycles.

Together, Xilinx and AMD will also operate at a significantly larger scale, which should improve margins and cash flow.

These deals will create a leading supplier of chips for edge-network base stations.

Unlike in the data center market where general-purpose chips win, edge networks require chips that are good at specific things: low-latency, custom-built, specific units.

Those are all things AMD and Xilinx are good at making. Edge computing is a concept that refers to moving processing power and data storage closer to where it’s needed, thus improving performance on local machines.

In short, Nvidia and AMD are the leading lights of the semi-chip industry involved in all the growth industries from artificial intelligence, data centers, video gaming, and self-driving technologies.

I am highly bullish both.

Mad Hedge Technology Letter

May 18, 2020

Fiat Lux

Featured Trade:

(CHINA’S BIG SEMICONDUCTOR PLAY),

(SMH), (SOXX), (DOCU), (AKAM), (NVDA), (AMD), (XLNX)

We received a convincing data point as to why we trade cloud companies and not the semiconductor chips.

The rift between blacklisted telecom equipment giant Huawei Technologies and the U.S. administration has had a dramatic side-effect on the business models of U.S. chip companies.

The U.S. commerce department now will require licenses for sales to Huawei of semiconductors made abroad with U.S. technology signaling more turbulent times ahead.

Huawei is the Chinese smartphone maker and telecom provider who has stolen intellectual property from the West and used mammoth subsidies funded by the Chinese communist party to build itself into one of the premier telecom equipment sellers and number two maker of smartphones in the world.

I seldom issue trade alerts on semiconductor chip companies because I'd rather not compete with the Chinese communist party and their capital funding capacity.

China is hellbent on subsidizing its own chip capacity as many Western chip companies are blocked from doing deals with them.

A recent example is the Chinese communist party injecting $2.25 billion into a Semiconductor Manufacturing International Corp. wafer plant to ramp up development in the sector.

To read about this, click here.

Exploiting the economic freedom and laws of the West has worked out perfectly for Chinese tech enabling them to develop juggernauts like Tencent and Baidu.

In fact, state-sponsored hacking of Western intellectual property is not considered a malicious activity in China.

There is the Chinese notion that everything is fair game in business and war and protecting company secrets falls on the shoulders of the cybersecurity sector.

To read more about the fallout in the West from China’s aggressive trade strategy, click here.

The concept that you should only blame yourself if you allow your secrets to get stolen prevails in China.

The consequences are impactful with U.S. chip companies suffering large drops in revenue without notice.

Leading up to the coronavirus, chip companies experienced a revenue slide of 12% in 2019 to $412 billion largely due to the trade war.

An example is Xilinx Inc. (XLNX) who will fire 7% of its workforce citing lower revenue from Huawei and delayed adoption of superfast 5G networks.

Along with the West getting smacked by the trade war, the ripple effect of increased uncertainty and guide-downs across the semiconductor supply stems from China’s economy being hit even worse than the U.S. economy.

There are no winners here and it will be a hard slog back from the nadir.

Either way, the sabre-rattling doesn’t stop here and each tweet and counterpunch will cause heightened volatility in chip shares.

Then consider that the existence of supply chains will most likely uproot, and we got indication of that type of activity with Taiwan Semiconductor’s (TSM) announcement to build a new chip factory in Phoenix.

To read more about this impactful deal then click here.

This would have never happened during prior administrations where all manufacturing was offshored to China.

As it stands, China has been circumventing existing U.S. law to clampdown chip sales by buying U.S. chips from 3rd party channels.

Once many of the supply chains come back, it will be almost impossible for Chinese to procure those same chips.

The Taiwan semiconductor manufacturing facility in Arizona will ultimately employ 1,600 high-tech workers.

Building is slated for 2021 with production targeted to begin in 2024.

Moving forward, the U.S. administration will make it implausible for many U.S. chip companies to offshore using the reasons of national security and domestic job demand to ensure that many factories are rerouted back to U.S. shores.

The boom and bust nature of chip companies make for treacherous spikes and drops in share prices.

The insane volatility is why I stay away from them as the Mad Hedge Technology Letter mainly opts for short-term options trades.

Nvidia (NVDA) and AMD (AMD) are great individual chip stocks that I would encourage readers to buy and hold.

Another option is to just park your money in the semi ETF VanEck Vectors Semiconductor ETF (SMH) or iShares PHLX Semiconductor ETF (SOXX).

On the flip side, cloud stock’s backbone of recurring monthly revenue is just too savory.

The constant cash flow with minimal international risk along with pristine balance sheets is what makes U.S. cloud companies top on the list of trade alert candidates.

That won’t stop anytime soon as the pandemic has offered us more conviction into the moat between cloud stocks and the rest of technology.

I apologize if I sound like a broken record, but I love my Akamai’s (AKAM) and DocuSign’s (DOCU), they have the growth portfolio that backs up my thesis.

Buy cloud stocks on the dip.

Mad Hedge Technology Letter

March 23, 2020

Fiat Lux

Featured Trade: (THE CORONA DRAG ON 5G)

(VZ), (T), (AAPL), (NFLX), (NVDA), (XLNX), (QRVO), (QCOM)

It will be inevitable – the 5G shift in 2020 will be delayed.

Last year, 5G was available on only about 1% of phones sold in 2019 and demand has cratered this year because of exogenous variables.

Up to just recently, Apple (AAPL) was the bellwether of the success of tech with wildly appreciating shares due to the expected ramp-up to a new 5G phone later this year.

Well, things are more complicated now.

I will be the first one to say it - the new Apple 5G iPhone will be delayed until 2021 – the project has been thrown into doubt because of a demand drop off and headaches with the supply chain in China.

The phenomenon of 5G cannot blossom until consumers can upgrade to 5G devices.

Concerning all the media print of China Inc. going back to work, don’t believe a word of it.

People of the Middle Kingdom are sitting at home just like you and me by navigating around top-down government edicts.

Instead of the perilous commute in a country of 1.4 billion people, Chinese workers are fabricating attendance figures per my sources.

Overall data is grim - global smartphone shipments dropped 38% year-over-year during February from 99.2 million devices to 61.8 million - the largest fall ever in the history of the smartphone market and that is just the tip of the iceberg.

The new data point underscores the magnitude of how the coronavirus is sucking the vitality out of the tech ecosystem in China and thus the end market for global consumer electronics.

The statistic also foreshadows imminent trouble in the smartphone market as other regions have now shut down not only in China but the manufacturing hubs of South East Asia.

The outbreak squeezes both supply and demand.

Factories in Asia are unable to manufacture phones as usual because of obligatory government shutdowns and complexities securing critical components from the supply chain.

5G has been hyped up as the great leap forward for wireless technology that will usher in unprecedented new use cases supercharging global GDP — from driverless transport to robotic automation to smart football stadiums.

And coronavirus is just that Godzilla destroying 5G momentum down.

Mass quarantines, social distancing, remote work, and schooling have been instituted in American cities, meaning that the current network carriers are swamped and overloaded with a surge in data usage.

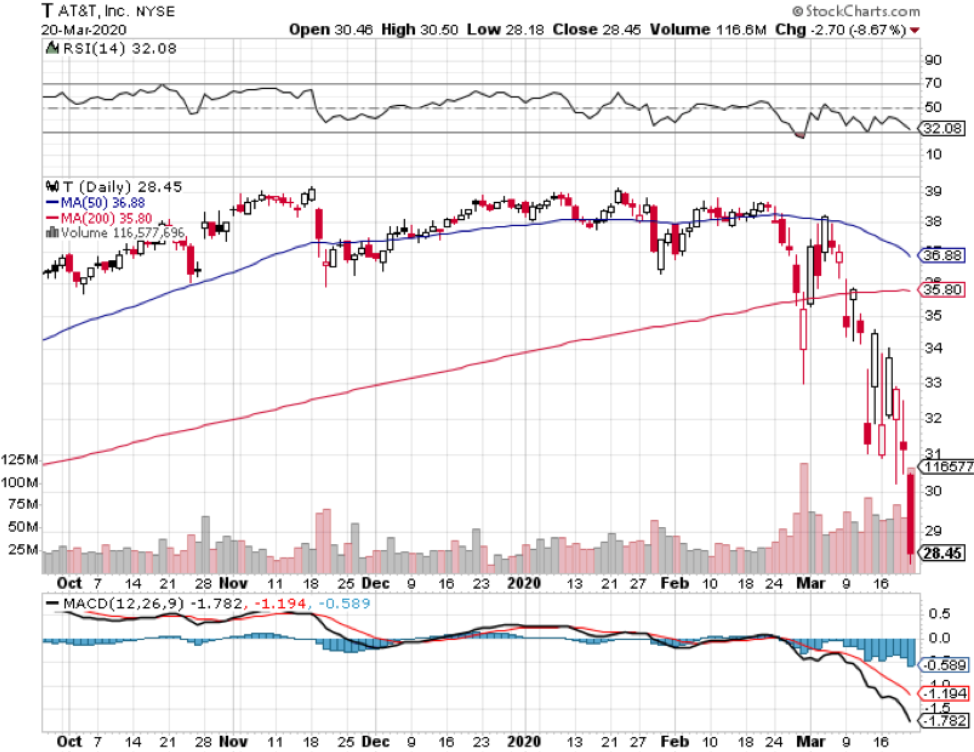

The Verizon’s (VZ) and the AT&T (T) Broadbands of America are currently focused on maintaining their current core customers, adding extra broadband to handle the increased load, and making sure the health of the network stays intact.

This is a poor climate to upsell products to beleaguered Americans who have just lost income and possibly their house because they cannot pay mortgages.

Services such as YouTube and Netflix (NFLX) have even decreased the quality of streaming on their platforms to handle the dramatic spike in extra usage in Europe with the whole continent locked down.

The Chinese consumer was the Darkhorse catalyst to ramp up the global economic expansion during the last economic crisis, picking up world spending in 2009.

On the contrary, this group of super spenders is less inclined to save the global economy this time around because they are saddled with domestic debt.

Just as unhelpful to Silicon Valley revenues, the technology relationship at the top of the governments are poised to worsen because of the health scare.

The U.S. administration has already banned the use of Chinese components in the U.S. 5G network amid suspicions the devices would be used for espionage.

Back stateside, I believe the U.S. telecoms will explicitly detail a sudden slowdown in the 5G network rollout during their next earnings report.

The telecom companies have been able to successfully handle the extra incremental load, but it has had to allocate resources to service the extra volume.

In the meantime, companies will shift to doing infrastructure and site preparation in anticipation of the re-build up to 5G, but that could be next to be put on ice if crisis management moves to the forefront.

Considering every 5G base station is being manufactured in Asia, one must be naïve in believing all is well and they will probably need to do what the 2020 Tokyo Olympics will shortly do – postpone it.

It’s not business as usual anymore.

This time it’s different.

The world just isn’t ready to digest such a shift in global business as 5G until the fallout of the coronavirus is in the rear-view mirror.

The 5G phenomenon underlying effect is to supercharge globalization into smaller networks of interconnectivity and that is not possible during a black swan event like the coronavirus which is the antithesis of globalization and interconnected business.

Just take the situation across the Atlantic Ocean in Europe, UBS Group AG, and Credit Suisse Group AG required clients to post additional collateral, and money managers in New York are preparing term sheets for ultra-rich Americans to urgently meet margin calls.

Many people are scurrying back to their doomsday’s shelter and that does not scream global business.

If you thought gold was the safe haven – wrong again – it experienced back-to-back weekly losses as margin pressures force fire sales of gold to raise cash.

Another glaring example are the assets of Eldorado Resorts Inc., controlled by the founding Carano family, which burned $28.7 million of stock in the casino entity to meet a margin call to satisfy a bank loan.

Things are that bad now!

Sure, telecom players might argue that a sudden influx of workers from home necessitates more investment in 5G, but if they have no income, all bets are off.

The capacity of 4G home broadband has proved it is good enough for today’s demands and it means the last stage of 4G will be a high data consumption longer phase before business lethargically pivots to 5G in 2021.

Verizon’s CEO Hans Vestberg said last year that half the U.S. will have access to 5G by the end of 2020, and I will say that is now impossible.

This sets up a generational buy in the Silicon Valley chip names involved in 5G after coronavirus troubles peak such as Nvdia (NVDA), Xilinx (XLNX), Qorvo (QRVO), and QUALCOMM Incorporated (QCOM).

Mad Hedge Technology Letter

July 3, 2019

Fiat Lux

Featured Trade:

(CHIPS ARE BACK FROM THE DEAD)

(XLNX), (HUAWEI), (AAPL), (AMD), (TXN), (QCOM), (ADI), (NVDA), (INTC)

The overwhelming victors of the G20 were the semiconductor companies who have been lumped into the middle of the U.S. and China trade war.

Nothing substantial was agreed at the Osaka event except a small wrinkle allowing American companies to sell certain chips to Huawei on a limited basis for the time being.

As expected, these few words set off an avalanche of risk on sentiment in the broader market along with allowing chip companies to get rid of built-up inventory as the red sea parted.

Tech companies that apply chip stocks to products involved with value added China sales were also rewarded handsomely.

Apple (AAPL) rose almost 4% on this news and many investors believe the market cannot sustain this rally unless Apple isn’t taken along for the ride.

Stepping back and looking at the bigger picture is needed to digest this one-off event.

On one hand, Huawei sales comprise a massive portion of sales, even up to 50% in Nvidia’s case, but on the other hand, it is the heart and soul of China Inc. hellbent on developing One Belt One Road (OBOR) which is its political and economic vehicle to dominate foreign technology using Huawei, infrastructure markets, and foreign sales of its manufactured products.

Ironically enough, Huawei was created because of exactly that – national security.

China anointed it part of the national security apparatus critical to the health and economy of the Chinese communist party and showered it with generous loans starting from the 1980s.

China still needs about 10 years to figure out how to make better chips than the Americans and if this happens, American chip sales will dry up like a puddle in the Saharan desert.

Considering the background of this complicated issue, American chip companies risk being nationalized because they are following the Chinese communist route of applying the national security tag on this vital sector.

Huawei is effectively dumping products on other markets because private companies cannot compete on any price points against entire states.

This was how Huawei scored their first major tech infrastructure contract in Sweden in 2009 even though Sweden has Ericsson in their backyard.

We were all naïve then, to say the least.

Huawei can afford to take the long view with an Amazon-like market share grab strategy because of possessing the largest population in the world, the biggest market, and backed by the state.

Even more tactically critical is this new development crushes the effectiveness of passive investing.

Before the trade war commenced, the low-hanging fruit were the FANGs.

Buying Google, Amazon, Apple, Netflix, and Facebook were great trades until they weren’t.

Things are different now.

Riding on the coattails of an economic recovery from the 2008 housing crisis, this group of companies could do no wrong with our own economy flooded with cheap money from the Fed.

Well, not anymore.

We are entering into a phase where active investors have tremendous opportunities to exploit market inefficiencies.

Get this correct and the world is your oyster.

Get this wrong, like celebrity investors such as John Paulson, who called the 2008 housing crisis, then your hedge fund will convert to a family office and squeeze out the extra profit through safe fixed income bets.

This is another way to say being put out to pasture in the financial world.

My point being, big cap tech isn’t going up in a straight line anymore.

Investors will need to be more tactically cautious shifting between names that are bullish in the period of time they can be bullish while escaping dreadful selloffs that are pertinent in this stage of the late cycle.

In short, as the trade winds blow each way, strategies must pivot on a dime.

Geopolitical events prompted market participants to buy semis on the dips until something materially changes.

This is the trade today but might be gone with one Tweet.

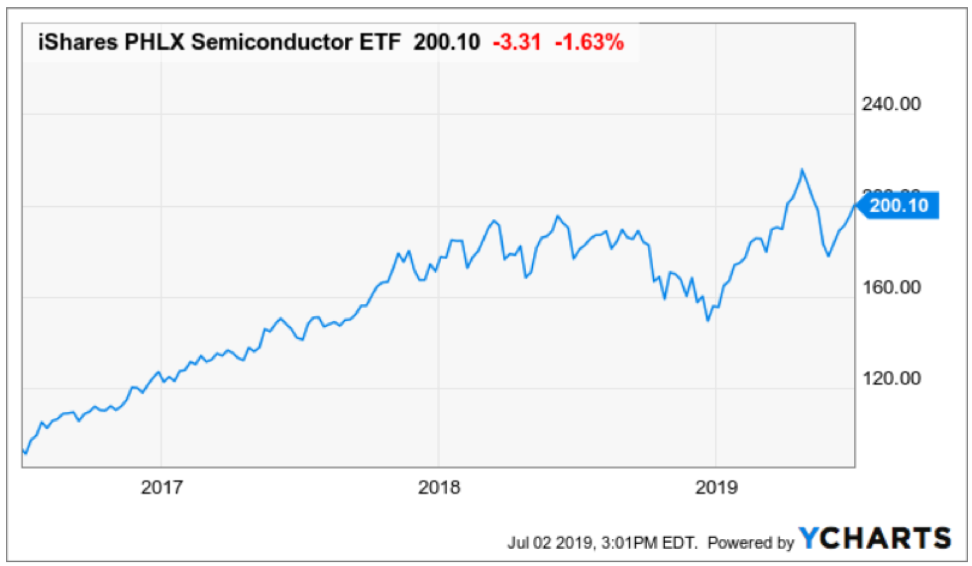

If you want to reduce your beta, then buy the semiconductor chip iShares PHLX Semiconductor ETF (SOXX).

I will double down in saying that no American chip company will ever commit one more incremental cent of capital in mainland China.

That ship has sailed, and the transition will whipsaw markets because of the uncertainty in earnings.

The rerouting of capital expenditure to lesser-known Asian countries will deliver control of business models back to the corporation’s management and that is how free market capitalism likes it.

Furthermore, the lifting of the ban does not include all components, and this could be a maneuver to deliver more face-saving window-dressing for Chairman Xi.

In reality, there is still an effective ban because technically all chip components could be regarded as connected to the national security interests of the U.S.

Bullish traders are chomping at the bit to see how these narrow exemptions on non-sensitive technologies will lead to a greater rapprochement that could include the removal of all new tariffs imposed since last summer.

The risk that more tariffs are levied is also high as well.

I put the odds of removing tariffs at 30% and I wouldn’t be surprised if the administration doubles down on China to claim a foreign policy victory leading up to the 2020 election which could be the catalyst to more tariffs.

It’s difficult to decode if U.S. President Trump’s statements carry any real weight in real time.

The bottom line is the American government now controls the mechanism to when, how, and the volume of chip sales to Huawei and that is a dangerous game for investors to play if you plan on owning chip stocks that sell to Huawei.

Artificial intelligence or 5G applications chips are the most waterlogged and aren’t and will never be on the table for export.

This means that a variety of companies pulled into the dragnet zone are Intel (INTC), Nvidia (NVDA), and Analog Devices (ADI) as companies that will be deemed vital to national security.

These companies all performed admirably in the market following the news, but that could be short lived.

Other major logjams include Broadcom’s future revenue which is in jeopardy because of a heavy reliance on Huawei as a dominant customer for its networking and storage products.

Rounding out the chip sector, other names with short-term bullish price action are Qualcomm (QCOM) up 2.3%, Texas Instruments (TXN) up 2.6%, and Advanced Micro Devices (AMD) up 3.9%.

(AMD) is a stock I told attendees at the Mad Hedge Lake Tahoe conference to buy at $18 and is now above $31.

Xilinix (XLNX) is another integral 5G company in the mix that has their fortunes tied to this Huawei mess.

Investors must take advantage of this short-term détente with a risk on, buy the dip trade in the semi space and be ready to rip the cord on the first scent of blood.

That is the market we have right now.

If you can’t handle this environment when there is blood in the streets, then stay on the sidelines until there is another market sweet spot.