Mad Hedge Technology Letter

March 13, 2019

Fiat Lux

Featured Trade:

(NVIDIA STEPS UP ITS GAME),

(NVDA), (INTC), (MSFT), (ANET), (CSCO), (MCHP), (XLNX)

Mad Hedge Technology Letter

March 13, 2019

Fiat Lux

Featured Trade:

(NVIDIA STEPS UP ITS GAME),

(NVDA), (INTC), (MSFT), (ANET), (CSCO), (MCHP), (XLNX)

Nvidia (NVDA) was right to pull the trigger – that was my first reaction when I first learned that they had aggressively acquired Israeli chip company Mellanox for $6.9 billion.

The fight to seize these assets were fierce triggering a bidding war -American heavyweights Intel and Microsoft were also in the mix but lost out.

CEO of Nvidia Jensen Huang touted the importance of the deal by explaining that “the emergence of AI and data science as well as billions of simultaneous computer users, is fueling skyrocketing demand on the world's data centers."

Therefore, satisfying this demand will require holistic architectures that connect massive numbers of fast computing nodes over intelligent networking fabrics to form a giant datacenter-scale compute engine.

Mellanox and its capabilities cover all the bases for Nvidia and will nicely slot into its portfolio offering, an added bonus of cross-selling and upselling opportunities to existing clients.

The strategic motives behind the deal are plentiful with increased importance of connectivity and bandwidth enhancing Nvidia's ability to provide datacenter-scale computing across the full stack for next-generation high-performance computing and AI workloads.

The agreement is the result of the company's shift toward next-gen technology as adoption of cloud, AI, and robotics ramps up and Nvidia will be at the forefront of this massive migration.

As the fourth industrial revolution advances, Nvidia is best of breed of semiconductor companies and the imminent adoption of 5G will aid the likes of Microchip Technology (MCHP) and Xilinx (XLNX).

Technology is rapidly changing, and the data center is the segment that is accelerating at a faster clip than in previous years translating into de-emphasizing current revenues of gaming and autonomous on a relative growth basis.

These segments will be secondary to the addressable opportunity in data center and signing up Mellanox is a key strategic initiative to exploit this growth opportunity.

Missing the boat on this compelling opportunity could have dragged Nvidia into an existential crisis down the road as the missed opportunity costs of lucrative data center revenues would begin to bite, and with no quick fix on the horizon, Nvidia’s growth drivers would be potentially disarmed.

Investors need to remember that Nvidia derives half of its revenue from China and up until this point, gaming had been a huge tailwind to its total revenue, however, the Chinese communist party has identified gaming addiction in young adults as a national crisis and have been refusing to deliver new gaming licenses to gaming creators.

As the data center via the cloud begins its next ramp-up of insatiable demand, Nvidia was acutely aware they could not miss the boat and to grab a foot hole against larger player Intel.

Almost overpaying to have more skin in the game does not do justice to what the ramifications would have been if Intel or even Microsoft were able to hijack this deal.

The two-fold victory will in turn boost sales of Nvidia's data center products long term while depriving Intel of extending the lead in data center.

And after the lack of recent underperformance in the prior quarter, Nvidia needed a gamechanger to cauterize the blood flow.

Nvidia's total revenue plunged more than 24% YOY in Q4 of 2018, and shareholders have been looking for remedies, especially after the once mythical cryptocurrency business blew up and the company was stuck with a glut of inventory.

The purchase of Mellanox will help Nvidia start competing with other dominant players like Cisco Systems (CSCO) and Arista Networks (ANET).

Mellanox is one of a handful of firms selling hardware that connects devices in the data center through network cards, switches, and cables.

The deal still needs regulatory approval and could be a stumbling block if Chinese authorities drag this into the orbit of the trade war and make it a bullet point in negotiations.

The net result is positive to the overall business model, and this move will breathe oxygen into Nvidia’s long-term narrative with a flow of revenue set to come online once the 5,000 Mellanox employees are integrated into Nvidia’s levers of operation.

Shares should be the recipient of short-term strength and after getting smushed by a poor last quarter, there is substantial room to the upside.

A dip back to $150 would serve as a good entry point to strap on a short-term bullish trade in Nvidia shares.

Mad Hedge Technology Letter

January 28, 2019

Fiat Lux

Featured Trade:

(BUY DIPS IN SEMIS, NOT TOPS),

(XLNX), (LRCX), (AMD), (TXN), (NVDA), (INTC), (SOXX), (SMH), (MU), (QQQ)

Global Market Comments

January 28, 2019

Fiat Lux

Featured Trade:

(THE MARKET FOR THE WEEK AHEAD, or IT’S FINALLY OVER)

(SPY), (TLT), (FXE), (MSFT), (AAPL),

(PG), (F), (LRCX), (AMD), (XLNX)

Last week, I was too busy to cook dinner for my brood, so I ordered a pizza delivery. When an older man showed up with our dinner, I told the kids to tip him double. After all, he might be an unpaid federal air traffic controller.

It is a good thing I work late on Friday afternoon because that's when the government shutdown ended after 35 days. The bad news? The government stops getting paid again in only 18 more days. If you have to travel, you better do it quick as the open window may be short.

The most valuable thing we learned from all of this is that the weak point in America is the airline transportation system which relies on 4,000 flights to get the country’s business done.

Having once owned a European air charter company, I could have told you as much was coming. Every nut, bolt, and screw that goes into a US registered aircraft has to be inspected by the federal government. They are painted yellow when viewed which is called “yellow tagging”. No inspection, no screw. No screw, no airplane. No airplane, no flight. No flight, no economy. I can’t tell you how many times I have seen a $30 million aircraft grounded by a failed 50-cent part.

And here’s what most investors don’t get. We lost 75 basis points in GDP growth from the shutdown. We may lose another 75 basis points restarting. And if you lose 1.50% from a post-Christmas period that is normally weak anyway, Q1 GDP may well come in negative. Hello recession!

We won’t know for sure until the first advanced estimate of Q1 GDP from the US Department of Commerce’s Bureau of Economic Analysis is published on April 26. That’s when the sushi will hit the fan. That, by the way, is perilously close for the May 10 prediction of the end of the entire ten-year bull market.

How did investors fare during the shutdown? We clocked the best January in 32 years with the Dow Average up 7.55%. Maybe the government should stay closed all the time!

It is not like the government shutdown, the fading Chinese trade talks, and the arrest of the president’s pal were the only things happening last week.

A slowing China is freaking out investors everywhere. Even if a trade deal is cut tomorrow, it may not be enough to pull the economy out of a downward death spiral. Look out below! A 6.6% growth rate for 2018 is the slowest in 30 years.

Existing Home Sales were down a disastrous 6.4%, in December and 10% YOY, the worst read since 2012. The government shutdown is made closings nearly impossible.

The EC’s Mario Draghi said there would be no euro rate rises until 2020 and the US bond market took off like a rocket. Another point or two and we’ll be in short selling territory again. Don’t count on Europe to pull us out of the next recession. Whoever came up with the idea of putting an Italian in charge of Europe’s finances anyway? Like that was such a great idea.

Procter & Gamble (PG) beat with an upside earnings surprise. It must be all those people buying soap to wash their hands of our political system. But Ford (F) disappointed, dragged down by weak foreign earnings. The weakest big car company to get into electric cars is really starting to suffer. The last of the buggy whip makers is taking a swan dive

The semis have bottomed in the wake of spectacular earnings reports from (LRCX), (AMD), and (XLNX). The great artificial intelligence play is back in action after a severe spanking. I never had any doubt they would come back. Now for an entry point.

Farmers are leaving crops to rot in the field as the trade war with China destroys prices and the Mexicans needed to harvest them are trapped at the border. There’s got to be an easier way to earn a living. Avoid the ags and all ag plays. Short tofu stocks!

Investors are now sitting on pins and needles wondering if we get a repeat of the horrific February of 2018, or whether so far great earnings reports will drive us to higher highs. Earnings tail off right when the next government shutdown is supposed to start so our lives will be interesting, to say the least.

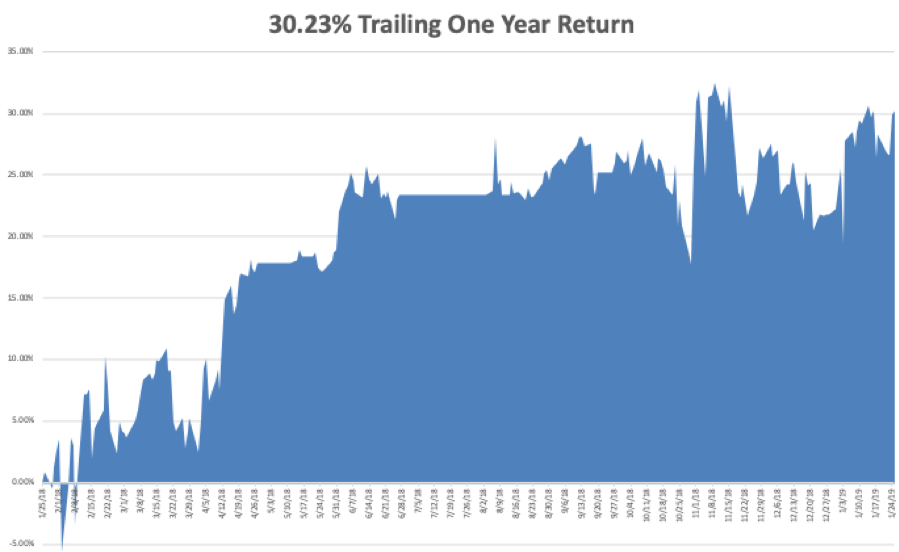

My January and 2019 year to date return soared to +7.24%, boosting my trailing one-year return back up to +30.23%.

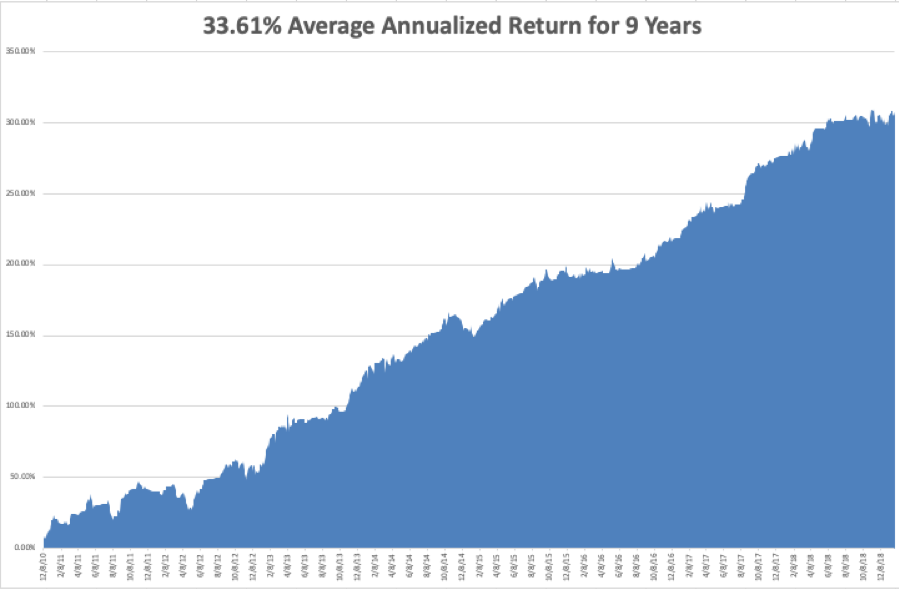

My nine-year return climbed up to +308.14%, a mere 1.72% short of a new all time high. The average annualized return revived to +33.61%.

I have been dancing in between the raindrops using rallies to take profits on longs and big dips to cover shorts.

I started out the week using the 4 1/2 point plunge in the bond market (TLT) to cover the last of my shorts there, bring in a whopper of a $1,680 profit in only 13 trading days. To quote the Terminator (whose girlfriend I once dated, the Terminatrix), I’ll be back.”

I used the big 500-point swoon in the Dow on Monday to come out of my (SPY) short at cost. An unfortunate comment on interest rates by the European Central Bank forced me to stop out of my long in the Euro (FXE), also at cost.

That has whittled my portfolio down to only two positions, a long in Microsoft (MSFT) and a short in Apple (AAPL). As a pairs trade you could probably run this position for years. I am now 80% in cash.

The goal is to go 100% into cash into the February option expiration in 14 trading days, wait for a big breakout, and then fade it. Essentially, I am waiting for the market to tell me what to do. That will enable me to bank double-digit profits for the start of 2019, the best in a decade.

The upcoming week is very iffy on the data front because of the government shutdown. Some government data may be delayed and other completely missing. Private sources will continue reporting on schedule. All of the data will be completely skewed for at least the next three months. You can count on the shutdown to dominate all media until it is over.

Jobs data will be the big events over the coming five days along with some important housing numbers. We also have several heavies reporting earnings.

On Monday, January 28 at 8:30 AM EST, we get the Chicago Fed National Activity Index.

On Tuesday, January 29, 9:00 AM EST, the Case Shiller National Home Price Index for November is released. The ever important Apple (AAPL) earnings are out after the close, along with Juniper Networks (JNPR).

On Wednesday, January 30 at 8:15 AM EST, the ADP Private Employment Report is announced. Pending Home Sales for December follows. Boeing Aircraft (BA) and Facebook (FB), and PayPal (PYPL) announce.

Thursday, January 31 at 8:30 AM EST, we get Weekly Jobless Claims. We also get the all-important Consumer Spending Index for December. Amazon (AMZN) and General Electric (GE) announce.

On Friday, February 1 at 8:30 AM EST, the January NonFarm Payroll Report hits the tape.

The Baker-Hughes Rig Count follows at 1:00 PM. Schlumberger (SLB) announces earnings. Home Sales is released. AbbVie Inc (ABBV) and DR Horton (DHI) report.

As for me, I will be celebrating my birthday. Believe me, lighting 67 candles creates a real bonfire. I received the best birthday card ever from my daughter which I have copied below

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Don’t buy the dead cat bounce – that was the takeaway from a recent trading day that saw chips come alive with vigor.

Semiconductor stocks had their best day since March 2009.

The price action was nothing short of spectacular with names such as chip equipment manufacturer Lam Research (LRCX) gaining 15.7% and Texas Instruments (TXN) turning heads, up 6.91%.

The sector was washed out as the Mad Hedge Technology Letter has determined this part of tech as a no-fly zone since last summer.

When stocks get bombed out at these levels - sometimes even 60% like in Lam Research’s case, investors start to triage them into a value play and are susceptible to strong reversal days or weeks in this case.

The semi-conductor space has been that bad and tech growth has had a putrid last six months of trading.

In the short-term, broad-based tech market sentiment has turned positive with the lynchpins being an extremely oversold market because of the December meltdown and the Fed putting the kibosh on the rate-tightening plan.

Fueled by this relatively positive backdrop, tech stocks have rallied hard off their December lows, but that doesn’t mean investors should take out a bridge loan to bet the ranch on chip stocks.

Another premium example of the chip turnaround was the fortune of Xilinx (XLNX) who rocketed 18.44% in one day then followed that brilliant performance with another 4.06% jump.

A two-day performance of 22.50% stems from the underlying strength of the communication segment in the third quarter, driven by the wireless market producing growth from production of 5G and pre-5G deployments as well as some LTE upgrades.

Give credit to the company’s performance in Advanced Products which grew 51% YOY and universal growth across its end markets.

With respect to the transformation to a platform company, the 28-nanometer and 16-nanometer Zynq SoC products expanded robustly with Zynq sales growing 80% YOY led by the 16-nanometer multiprocessor systems-on-chip (MPSoC) products.

Core drivers were apparent in the application in communications, automotive, particularly Advanced Driver Assistance Systems (ADAS) as well as industrial end markets.

Zynq MPSoC revenues grew over 300% YOY.

These positive signals were just too positive to ignore.

Long term, the trade war complications threaten to corrode a substantial chunk of chip revenues at mainstay players like Intel (INTC) and Nvidia (NVDA).

Not only has the execution risk ratcheted up, but the regulatory risk of operating in China is rising higher than the nosebleed section because of the Huawei extradition case and paying costly tariffs to import back to America is a punch in the gut.

This fragility was highlighted by Intel (INTC) who brought the semiconductor story back down to earth with a mild earnings beat but laid an egg with a horrid annual 2019 forecast.

Intel telegraphed that they are slashing projections for cloud revenue and server sales.

Micron (MU) acquiesced in a similar forecast calling for a cloud hardware slowdown and bloated inventory would need to be further digested creating a lack of demand in new orders.

Then the ultimate stab through the heart - the 2019 guide was $1 billion less than initially forecasted amounting to the same level of revenue in 2018 - $73 billion in revenue and zero growth to the top line.

Making matters worse, the downdraft in guidance factored in that the backend of the year has the likelihood of outperforming to meet that flat projection of the same revenue from last year offering the bear camp fodder to dump Intel shares.

How can firms convincingly promise the back half is going to buttress its year-end performance under the drudgery of a fractious geopolitical set-up?

This screams uncertainty.

Love them or crucify them, the specific makeup of the semiconductor chip cycle entails a vulnerable boom-bust cycle that is the hallmark of the chip industry.

We are trending towards the latter stage of the bust portion of the cycle with management issuing code words such as “inventory adjustment.”

Firms will need to quickly work off this excess blubber to stoke the growth cycle again and that is what this strength in chip stocks is partly about.

Investors are front-running the shaving off of the blubber and getting in at rock bottom prices.

Amalgamate the revelation that demand is relatively healthy due to the next leg up in the technology race requiring companies to hem in adequate orders of next-gen chips for 5G, data servers, IoT products, video game consoles, autonomous vehicle technology, just to name a few.

But this demand is expected to come online in the late half of 2019 if management’s wishes come true.

To minimize unpredictable volatility in this part of tech and if you want to squeeze out the extra juice in this area, then traders can play it by going long the iShares PHLX Semiconductor ETF (SOXX) or VanEck Vectors Semiconductor ETF (SMH).

In many cases, hedge funds have made their entire annual performance in the first month of January because of this v-shaped move in chip shares.

Then there is the other long-term issue of elevated execution risks to chip companies because of an overly reliant manufacturing process in China.

If this trade war turns into a several decades affair which it is appearing more likely by the day, American chip companies will require relocating to a non-adversarial country preferably a democratic stronghold that can act as the fulcrum of a global supply chain channel moving forward.

The relocation will not occur overnight but will have to take place in tranches, and the same chip companies will be on the hook for the relocation fees and resulting capex that is tied with this commitment.

That is all benign in the short term and chip stocks have a little more to run, but on a risk reward proposition, it doesn’t make sense right now to pick up pennies in front of the steamroller.

If the Nasdaq (QQQ) retests December lows because of global growth falls off a cliff, then this mini run in chips will freeze and thawing out won’t happen in a blink of an eye either.

But if you are a long-term investor, I would recommend my favorite chip stock AMD who is actively draining CPU market share from Intel and whose innovation pipeline rivals only Nvidia.

Mad Hedge Technology Letter

July 26, 2018

Fiat Lux

Featured Trade:

(THE TRADE WAR'S COLLATERAL DAMAGE),

(SWKS), (ACIA), (CRUS), (XLNX), (ROKU), (SQ)

As the trade ruckus rumbles on for the foreseeable future, there are some places to deploy cash and some places to avoid like the zika virus.

The one area of tech to avoid that is clearer than daylight is the small cap chips companies.

Like a fish out of water, you should not feel comfortable holding shares in this type of equity amid the backdrop of an unresolved trade skirmish.

Although the Mandarins ironically need our chips, the uncertainty permeating around small chip firms means it's not time to hold let alone initiate new positions.

Investors still don't know how this standoff with shake out.

Until, there is more clarity going forward, give way to the next guy who can take the heavy loss.

Keep the powder dry for better times.

The long-term demand picture is healthy with IoT, cloud, and software companies never being thirstier for chips.

Short term is a different story with many of these smaller chip companies subscribing to grotesque charts that will make your jaw drop.

Take Skyworks Solutions, Inc. (SWKS) whose shares have spent the majority of 2018 trending lower and are stuck in purgatory.

(SWKS) produces semiconductors deployed in radio frequency (RF) and mobile systems.

This stock has been tainted by the horrid reality that it generates 25% to 30% of revenue from China.

If you have been living in a cave for the past eight months, technology is the battleground for global supremacy pitting two of the leading technological heavyweights in the world against each other in a fiercely contested, drawn-out conflict.

Any American listed chip company doing at least 20% of revenue in China has the same chart trajectory and that is not up.

Adding insult to injury, (SWKS) generates 35% to 40% of its total revenue from Apple.

As we approach every earnings season, the story rewinds and plays again to loud applause.

A slew of analysts appears on air condemning Apple promulgating lower iPhone sales due to surveys taken across various key suppliers giving them a snapshot into production numbers.

Each time, the analysts are proved wrong. However, the avalanche of downgrades that ensues knocks the stuffing out of the small chip companies dipping viciously, at times more than 10% or more on the headline.

One of the larger Chinese contracts that was signed by (SWKS) was with ZTE. Yes, that ZTE, the one the U.S. administration temporarily put out of business for selling telecommunication equipment to North Korea and Iran.

That was the nail in the coffin.

According to the (SKWS) official website, it has an ongoing, expanding relationship with ZTE and its chips would be "powering data cards and USB modems" in ZTE-manufactured next-generation tablets.

Luckily, the American government reversed its initial decision restoring operations to ZTE.

That does not mean it is out of the woods yet as lingering risks still overhang over this company.

This revelation underscores the massive contract risk for companies that unlike behemoths such as Micron, are desperately reliant on just a handful of contracts to propagate short-term revenue.

Effectively, the U.S. administration views American chip companies as collateral damage to the bigger picture.

The only reason the ZTE ban was lifted was because it was a prerequisite to restart talks between both sides.

If the ban was upheld, 75,000 Chinese workers would have needed to polish the dust off their resumes to start a fresh job search.

The inability to sell components to service the Chinese consumer will strike where it hurts most: the bottom line.

Chip producers did $1.5 billion in sales with ZTE in 2017. That business is in a precarious situation when a tweet can just wipe out those contracts in one fell swoop.

Acacia Communications, Inc. (ACIA) churns out high-speed coherent interconnect products.

The stock was beaten down then beaten some more in 2018.

(ACIA) revealed 30% of its $385.2 million revenue derived from one contract with guess who...ZTE.

On word of ZTE ban, (ACIA) plummeted from $40 to $27.50 in one trading day.

The disappearance of a contract this vital to survival is tough for a small business to handle even if temporary.

Layoffs and a squeezed financial situation apply unrelenting pressure on management to find an elixir.

Cirrus Logic Inc. (CRUS) pumping out a mix of analog, mixed-signal, and audio DSP integrated circuits (ICs) was trading more than $62 just a year ago.

Fast forward to today and its shares are at a measly $39.

To say Cirrus Logic's eggs are in one basket is an understatement.

(CRUS) procures 80% of revenue from Apple.

It's all hunky-dory to develop a close relationship with Apple, but in light of this unpredictable economic climate, shares have been hit hard and there is no end in sight.

(CRUS) even won a contract to help produce Apple's noise canceling and water-resistant AirPods, but that does not do anything to change the narrative.

The vultures are circling around this name and it was time to abort a long time ago.

Xilinx, Inc. (XLNX) is another small chip company and the first to create the first fabless manufacturing model headquartered in San Jose, California.

This company, founded in 1984, procures around 35% of revenue from China

The trade headwinds have set this stock in the crosshairs, being the victim of frequent 5% drops and two 10% slides in 2018.

It is a miracle this stock is slightly in the green this year, and (XLNX) is one of the lucky ones.

Skim through the rest of small cap chips stocks and the charts look the same. Dreadful with massive rally busting sell-offs.

The extreme volatility in and of itself is a sensible reason to steer clear of these names.

The headline risks that splash across the morning news spreads are a daily reminder that chip stocks, big and small, aren't out of the woods yet.

The Johnny-come-latelies must expose themselves to higher quality, unique assets which possess little or no China exposure.

For the experts, trade the volatility at your peril. But if volatility is what you want with scarcity of value, leg into Roku (ROKU) or Square (SQ) on moderate sell-off days.

________________________________________________________________________________________________

Quote of the Day

"Technological progress is like an ax in the hands of a pathological criminal," said German-born theoretical physicist Albert Einstein.