All of those years spent living in rabbit hutch sized apartments, getting hand packed by white gloved railway men into rush hour train cars, and learning an impossible language, are finally paying off.

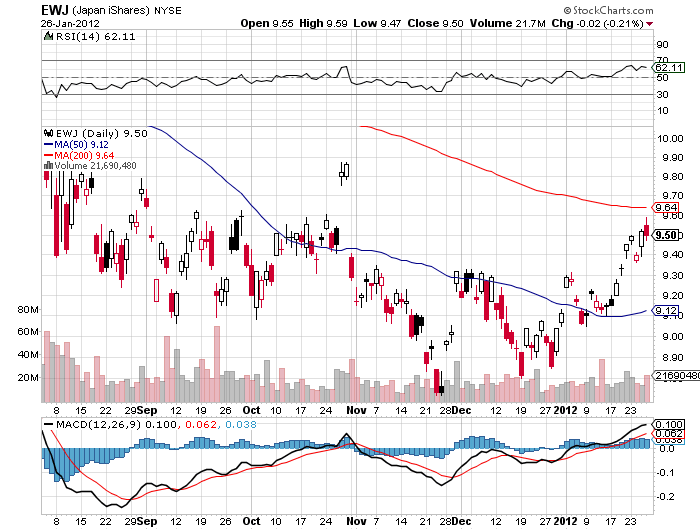

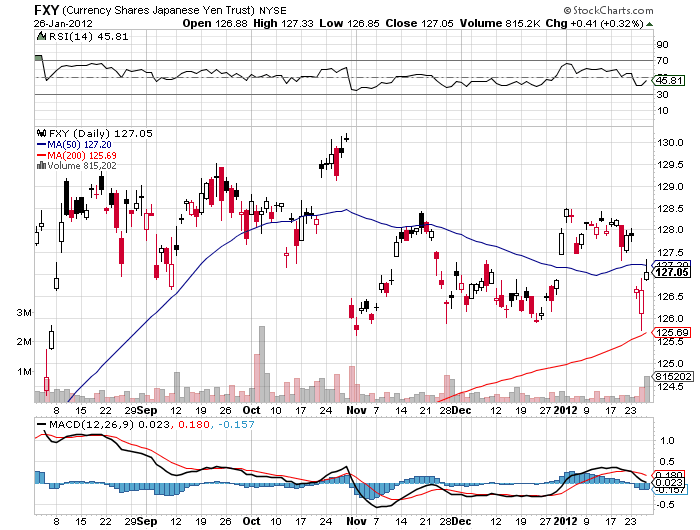

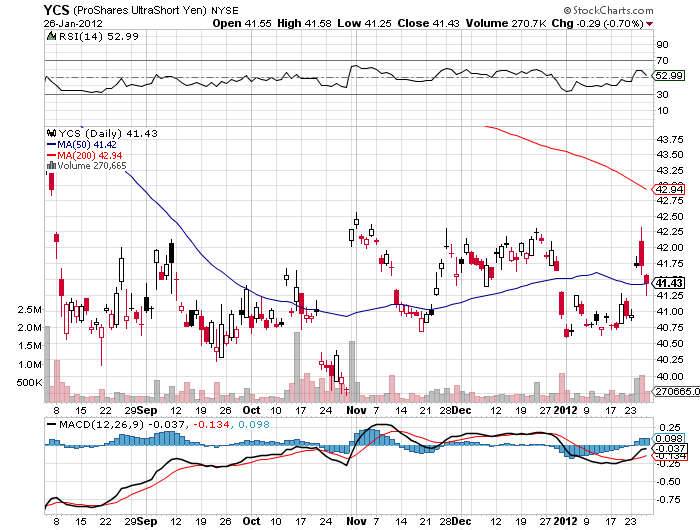

I have to tell you, I really have to think hard to recall a plunge in a major currency that has been as dramatic as the yen?s over the past two months. Since the Mid-November route began in earnest, the cash market has collapsed from ?76.80 to ?92.60 to the dollar. That has taken the ETF (FXY) down from $126.30 to an eye popping $105.50. The double leveraged short ETF (YCS) soared from $42 to $57.93. It?s a good thing that I was short the entire time.

In fact, I have devoted 20% of my entire capital to short yen plays since the beginning of the year. Newly elected Prime Minister, Shinzo Abe, was my willing coconspirator this week, announcing one of the most ambitious, expansionary budgets in history. The vice governor of the Bank of Japan chipped in, suggesting that the yen had more room to fall. Another senior government official suggested that ?100 to the dollar might be a reasonable target. It seems that any time someone in Tokyo says ?boo?, another round of yen selling by traders ensues.

But like all good things, this trade is getting rather long in the tooth. I?ll tell you how this is going to end. When the cash market declines to ?96 to the dollar, the grumblings about unfair import competition by the US car industry will escalate to an uproar. At ?100 to the dollar it will balloon into a full blown trade dispute. So get ready to start hearing a lot about Japan?s unfair manipulation of their currency to undervalued levels, especially from congressmen from Midwest states with large car plants.

The yen will probably fall short of that. The last time this happened, in the early 1990?s, the US was afraid that Japan was taking over the world. Our country was recoiling from a Japanese share of the American car market that had ratcheted up from 1% to 43% in just 20 years. Remember the tome ?Japan is Number One?? You have to laugh now.

Those fears abated long ago. A Japanese collapse on the scale of an IMF bailout is now much more likely than Japanese dominance. It?s tough to smack down an international competitor that is trying to claw its way up after 20 years on the mat. One complicating factor this time is that the principal lobbyist against a stronger yen is now US government owned, General Motors (GM).

I get emails every day from readers asking if they should initiate, double up, or triple up their short positions in the yen. As of today, I am saying no more. My best-case scenario had Japan?s beleaguered currency plunging to ?92 over the course of the next several months. Here we are over that figure in just ten weeks. So at best, a short yen position is a ?HOLD? here. Don?t chase it any more. Remember, hogs get fed, but pigs get slaughtered.

Japan is not an entirely bad place. Certainly the world would be a duller, more boring place without sushi, sake, hot tubs, and karaoke. And I never heard anyone complain about those coed public baths. Too bad I could never find a pair of sandals that fit.

Six Month Chart

Five Year Chart

https://www.madhedgefundtrader.com/wp-content/uploads/2013/02/Harakiri-Femail.jpg340230Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-02-04 09:28:382013-02-04 09:28:38Look at That Yen!

If anyone is expecting the Japanese yen to take back the losses it has suffered over the last two months, you can forget about it happening anytime soon, eventually, or in your lifetime.

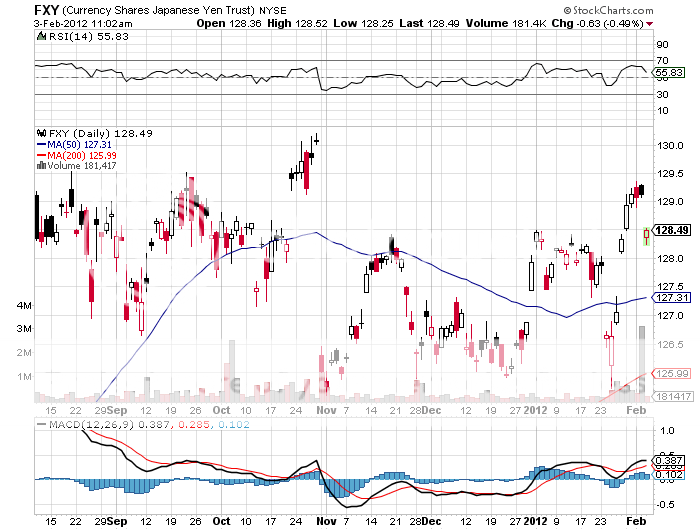

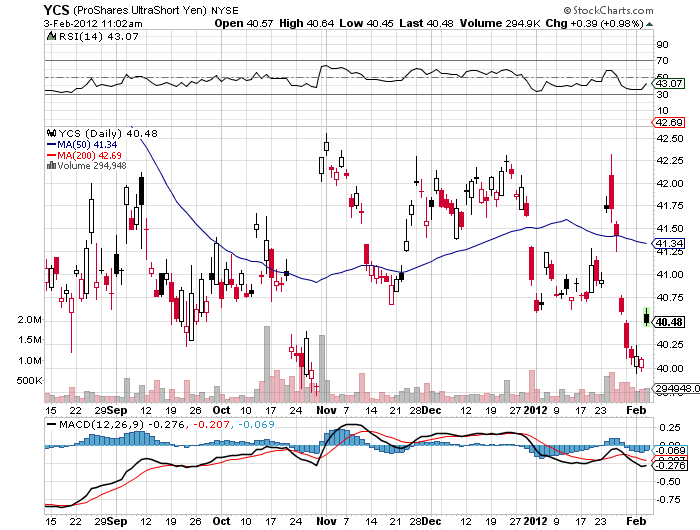

Naysayers have been pointing to this week?s policy meeting at the Bank of Japan as proof that the yen has stumbled in the international race to the bottom, and that it is running up the white flag of surrender in the currency wars. They point to the rise in the beleaguered currency from a ?90.16 to the dollar Friday low, back to ?88.4 in the cash market, and a gain in the (FXY) from $108.20 to $110.70. The inverse ETF (YCS) has backed off from $55 to $52.60.

There were several reasons for the pause. BOJ governor, Masaaki Shirakawa, said he would delay any substantial monetary easing until 2014. Hold the presses! Prime Minister Shinzo Abe indicated that if the yen fall became too severe, it might have to be slowed. The US government started carping that the weak yen was giving Japan?s car exports an unfair advantage.

That all-electric Nissan Leaf that cost $38,000 in November can now be sold for $31,000, once the recent currency depreciation is factored in. That is a big difference, and was a cause of frequent trade wars in decades past. How do you think we ended up with a Corolla factory in Fremont, California?

There is something much more fundamental afoot. Japan has been far and away the world?s largest international direct investor for the last 20 years. Trillions of dollars have poured out of the country, snapping up energy resources, commodities, manufacturing facilities, commercial real estate, and yes, lots of golf courses.

When the interest and dividends thrown off by these holdings were brought back to Japan, dollars were sold and yen bought, some $100 billion worth a year. On top of this, you can add $40 billion in interest payments earned on $800 billion in US Treasury bonds held by the Japanese government. Total it all up, and it is not only enough to support the yen, but to send it to new highs continuously for the past two decades, no matter how dire the worsening fundamentals of the domestic Japanese economy.

So what happens next? Think of the Nissan Leaf trade in reverse. That American factory that cost $1 billion in 2012 will now set a Japanese investor back $1.2 billion. Ditto for the government?s purchase of US Treasuries. The Japanese won?t stop their foreign investment completely, but they are now being priced out of the market in many transactions, and it will slow appreciably. So does that repatriated interest and dividends. This will feed into a weaker yen over the long term.

Given more time, Japan?s other awful fundamentals will start to kick in as well. Those include a deplorable demographic outlook, a debt/GDP ratio of 240%, the hollowing out of Japanese industry as it decamped for China, and the new cold war with the Middle Kingdom.

I?ll tell you how recent developments will end. Prime Minister Abe will fire the BOJ governor Shirakawa or he will wait a couple of months for him to retire. That will be consistent with his pedal to the metal strategy for reviving the Japanese economy. Then, the aggressive monetary easing he campaigned and won the election on, will get moved from 2014 back up to 2013--early 2013. Like, tomorrow. Then it will be back to free-fall for the yen.

Use this temporary and long overdue weakness to add short positions in the Japanese yen. You can also pick up more of the short yen ETF here, the (YCS).

Take Away the Meatball and What Are You Left With?

https://www.madhedgefundtrader.com/wp-content/uploads/2013/01/Shinzo-Abe.jpg277360Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-01-24 09:23:152013-01-24 09:23:15Why the Yen Will Never Recover

You know how I love second helpings, especially when the sushi bar is involved. I especially like unagi, or cooked eel, which is said to be an oriental aphrodisiac.

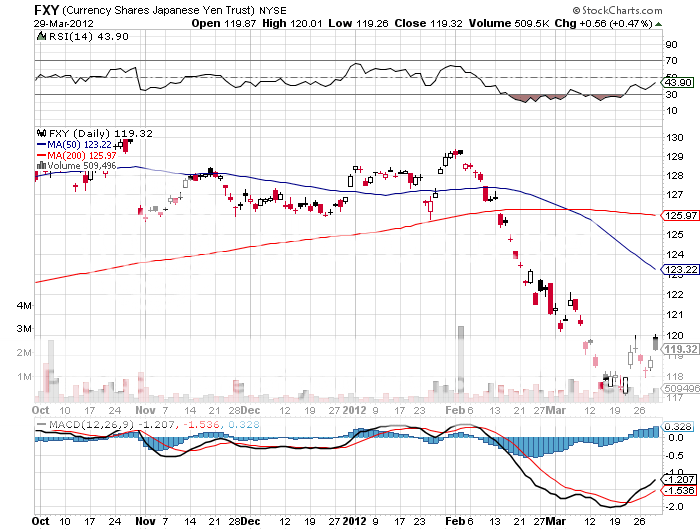

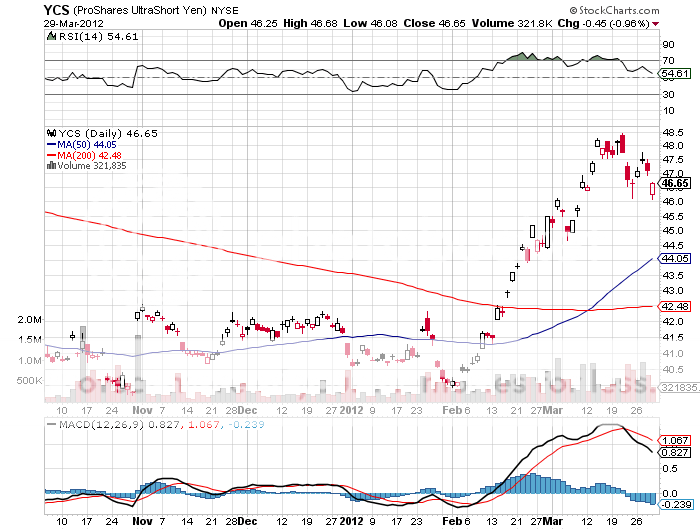

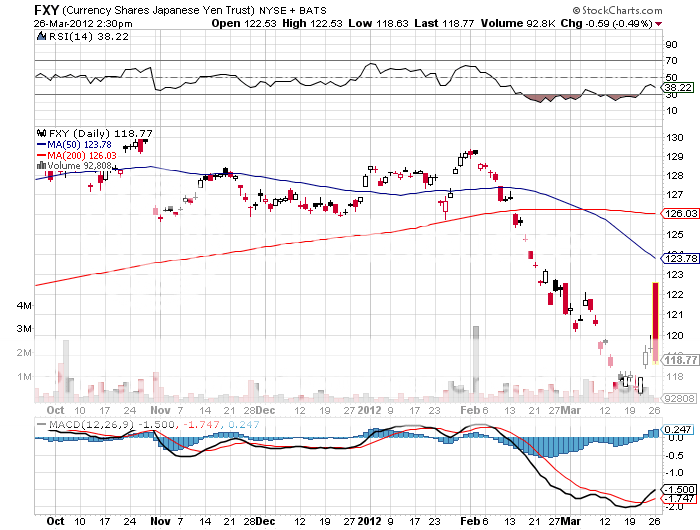

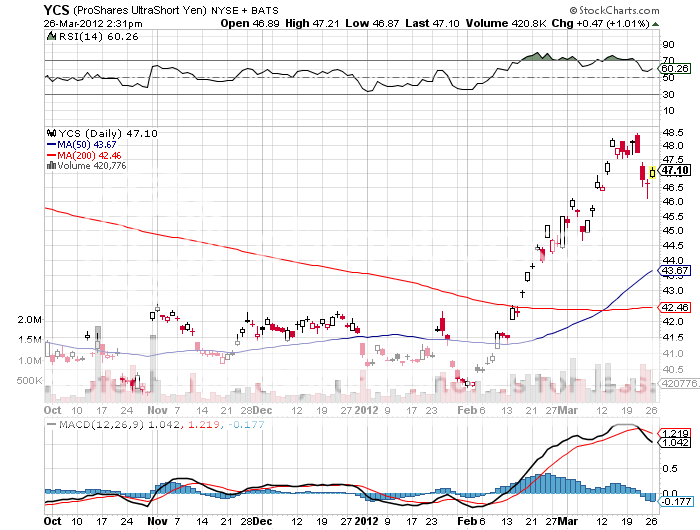

I am going to take advantage of Japan?s fiscal year end book closing on March 30 to reenter my short position of the Japanese yen. This is the one time a year when Japanese corporations suddenly repatriate yen back to Japan to beef up the cash on their books for their annual reports. Every year, this creates a quick boost to the yen against the US dollar which fades away in the following weeks like so much smoke.

Like everything else this year, the yen has had a straight line move since I put out my last call to sell the yen at the end of January. So while I made a nice profit on the first trade, I was never given another chance to reenter on the way down. Now I have that opportunity.

Since the yen bottomed on March 21, it has given back 25% of the move. Sure, I would prefer to get back in on the traditional one third pull back. But there are so few attractive trading opportunities out there right now that I am happy to jump the gun. If the yen strengthens more from here I will simply double up the position. This is a trade that I?ll be happy to live with for a while.

I have hammered away at the structural weakness of the Japanese economy ad nauseum for the past year. The one liner is that buyers of the country?s 1% yielding ten year bonds are dying off in droves, it has the world?s worst debt to GDP ratio, and labors under an Armageddon like demographic burden. It doesn?t help that they haven?t invested anything new since Godzilla ate the big screen. Sony (SNE) should have become Apple (AAPL). For those who wish to undertake a refresher course, please read the research pieces listed below:

* ?Momentum is Building for the Yen Shorts? on March 26 at http://madhedgefundradio.com/momentum-is-building-for-the-yen-shorts/

*? ?Nikkei Shows the Yen Move is Real? on February 20 at http://madhedgefundradio.com/nikkei-shows-the-yen-move-is-real/

*? ?Global Trading Dispatch Hits 64%, 11 Day Home Run on Yen Short? on February 13 at

http://madhedgefundradio.com/global-trading-dispatch-hits-64-11-day-home-run-on-yen-short/

*? ?Rumblings in Tokyo? on February 5 at http://madhedgefundradio.com/rumblings-in-tokyo/

*? ?Is This the Chink in Japan?s Armor?? on January 29 at http://madhedgefundradio.com/is-this-the-chink-in-japans-armor/

My preferred instrument here is the Currency Shares Japanese Yen Trust ETF (FXY) , where I will be buying the June, 2012 puts. At the very least, the (FXY) should make it back down to $117 in the near future, a price we visited just a week ago, which should give you a quickie 70%? return on the June $120 puts.

For those who are unwilling or unable to play in the options space, you can invest in the ProShares Ultra Yen Short ETF (YCS), a 2X leveraged bet that the yen falls against the dollar.

Do I hear Any Bids?

Japan?s Last Good Invention

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-04-01 23:04:022012-04-01 23:04:02Double Dipping on the Yen

I?m hearing from my buddies in Japan that while things are already quite bad in that enchanting country, they are about to get a whole lot worse, and that it is time to start scaling into a major short in the yen. Australia and China have already raised interest rates, to be followed by the US, and eventually Europe.

With its economy enfeebled, the prospects of Japan raising rates substantially are close to nil, meaning the yield spread between the yen and other currencies is about to widen big time. In the case of the Australian dollar, that works out to 4% per annum. Leverage up ten to one, and pile on anticipated capital gains brought in by a weakening yen, and you have a real carry trade on your hands. This will generate hundreds of billions of dollars? worth of cascading yen selling as hedge funds dog pile in. It?s macro investing at its finest.

Until now, the government has been able to finance ballooning budget deficits caused by two lost decades, but those days are coming to an end. Japan is quite literally running out of savers. The savings rate has dropped from 20% during my time there, to a spendthrift 3%, because real falling standards of living leave a lot less money for the piggy bank.

The national debt has rocketed to over 200% of GDP, and 100% when you net out government agencies buying each other?s securities. Japan has the world?s worst demographic outlook. Unfunded pension liabilities are exploding. Other than once great cars and video games, what does Japan really have to offer the world these days, but a carry currency?

Until now, the government has been able to cover up these problems with tatami mats, because almost all of the debt it issued has been sold to domestic institutions. Now that this pool is drying up, there is nowhere else to go but foreign investors. With Greece and the rest of the PIIGS at the forefront, and awareness of sovereign risks heightening, this is going to be a much more discerning lot to deal with.

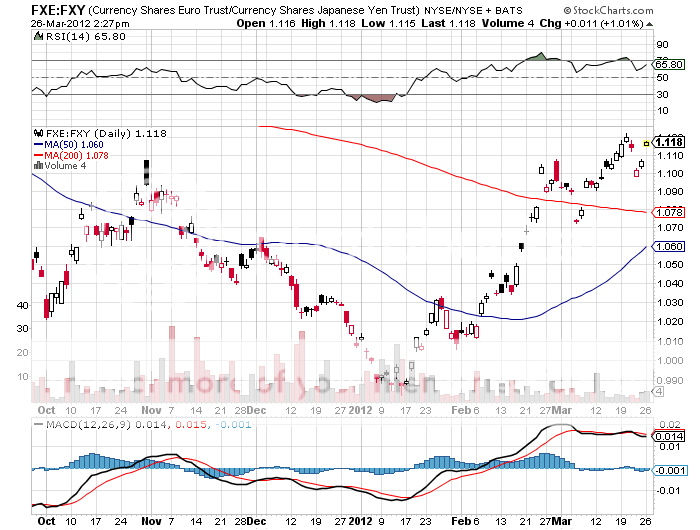

That great bell weather of global risk taking, the Euro/Yen cross is telling us that the mother of all carry trades has already started. You also see this in the Ausie/Yen cross, and outright yen markets. I have scored one round trip in the yen this year and hope to do several more.

You could dip your toe in the water here around ?82.40. In a perfect world you could sell it at the next stop at the ?85 level. My initial downside target is ?90, and after that ?100. If you?re not set up to trade in the futures or the interbank market like the big hedge funds, then take a look at the leveraged short yen ETF, the (YCS) or buying puts on the (FXY). This is a home run if you can get in at the right price.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-03-26 23:02:092012-03-26 23:02:09Momentum is Building for the Yen Shorts.

I spent ten years of my life tramping in and out of Japan?s Ministry of Finance headquarters in Tokyo?s Kasumigaseki district. It was a dreadful reinforced steel and concrete affair with a dull grey tile siding that was so solidly built that it was one of the few structures in the city to survive WWII. But the building offered spacious prewar dimensions, and I never tired of walking its worn hardwood floors. I was there so often that some government officials thought I worked there, and they did eventually give me an office, the first ever granted to a foreign correspondent.

So to get an update on the Land of the Rising Sun, I called a senior official whose father I knew well as a Deputy Minister of Finance for International Affairs during the 1970?s. I was a regular at his apartment in Shinjuku on Saturday nights, where we spent endless hours alternately playing chess and Scrabble over a bottle of Johnny Walker Red and smoking Mild Sevens. We did everything we could to expand each other?s? Japanese and English vocabularies with the words not found in dictionaries. When the bottle was almost finished and his face was beet red, the Elvis impersonations would start.

My friend told me that the ongoing strength of the yen is rapidly becoming a major political issue in Japan. The spot market is now threatening an all-time high, and on a trade weighted basis it was already at a new peak. Exporters were getting destroyed by the strong yen, which was making their goods increasingly expensive in a cost cutting competitive world.

This was forcing them to accelerate a 20 year effort by corporations to offshore production to China, which was ?hollowing out? Japan and causing economic growth to bleed away, and unemployment to rocket. The situation was getting so bad that American companies that offshored jobs to Japan years ago, like Caterpillar (CAT), were taking them back home because labor costs are so high. He expected Japan?s GDP to shrink at a 1.4% annualized rate during Q4, compared to a healthy 2.9% rate in the US.

His boss, Japanese finance minister, Juri Azumi, made comments in the Diet this week about his concern over yen strength. More specifically, he is seeking approval for a much more aggressive stance to pursue Bernanke style quantitative easing to knock the stuffing out of the yen and stimulate the economy.

The last time he did this, on October 31 last year, the Bank of Japan followed up with a massive $120 billion intervention in the foreign exchange market a few weeks later. One of the largest such interventions in history, it instantly knocked the yen down from ?75.90 to ?79.20. We may be about to see a replay. In fact, if they can just break resistance at ?80, then they might be able to knock it down to the 2011 low of ?85.30.

This time, Azumi has much more ammunition to work with. Japan reported its first trade deficit in 30 years just a few weeks ago. This may not be an anomaly. In response to the tsunami induced melt down at the Fukushima plant, Japan is permanently shutting down a large part of its nuclear power generating capacity. At its peak, nuclear accounted for 25% of the country?s electric power supply. That is forcing a huge surge in oil imports from the Middle East that has greatly tipped Japan?s balance of trade against it. Crude?s surge from $75/barrel to as high as $103 has only made matters worse.

He then told me that he too was now learning to play Scrabble and asked me for my list of words where the letter ?Q? is not followed by a ?U?. I said that I was not inclined to disclose America?s most valuable trade secrets to a foreign competitor. However, in deference to his late father, he couldn?t go wrong starting with ?Qi?, ?Qabala?, ?Qadi?, ?Qaid?, ?Qat? and ?Qanat?. I hung up the phone and immediately sold more yen against the dollar.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-02-05 23:03:382012-02-05 23:03:38Rumblings in Tokyo

?Oh, how I despise the yen, let me count the ways.? I?m sure Shakespeare would have come up with a line of iambic pentameter similar to this if he were a foreign exchange trader. I firmly believe that a short position in the yen should be at the core of any hedged portfolio for the next decade, but so far every time I have dipped my toe in the water, it has been chopped off by a samurai sword.

I was heartened once again this week when Japan?s Ministry of Finance released data showing that the country suffered its first annual trade deficit since 1980. Specifically, the value of imports exceeded exports by $39 billion. Japan still ran healthy surpluses with the US and Europe. But it ran a gigantic deficit with the Middle East, its primary supplier of energy.

You can blame the March tsunami and the Fukushima nuclear meltdown that followed for much of this. Japan depended on nuclear power for 25% of its electric power generation, and since then the number of operating plants has been cut from 54 to just 5. Conventional plants powered by oil and LNG have had to make up the difference, causing a surge in imports. Crude?s leap from $75/barrel in the fall to $100 made matters worse.

It also hasn?t helped that Japan has offshored much of its low end manufacturing to China over the last 30 years, as America has done. Exacerbating the problem were the Thai floods, which caused immense supply chain problems, further eroding exports.

To remind you why you hate all investments Japanese, I?ll refresh your memory with this short list of the other problems bedeviling the country:

* With the world?s weakest major economy, Japan is certain to be the last country to raise interest rates.

* This is inciting big hedge funds to borrow yen and sell it to finance longs in every other corner of the financial markets.

* Japan has the world?s worst demographic outlook that assures its problems will only get worse. They?re not making Japanese any more.

* The sovereign debt crisis in Europe is prompting investors to scan the horizon for the next troubled country. With gross debt exceeding 200% of GDP, or 100% when you net out inter-agency crossholdings, Japan is at the top of the hit list.

* The Japanese long bond market, with a yield of 0.98%, is a disaster waiting to happen.

* You have two willing co-conspirators in this trade, the Ministry of Finance and the Bank of Japan, who will move Mount Fuji, if they must, to get the yen down and bail out the country?s beleaguered exporters.

When the big turn inevitably comes, we?re going to ?100, then ?120, then ?150. That could take the price of the leveraged short yen ETF (YCS), which last traded at $41.43, to over $100.? But it might take a few years to get there. The fact that the Japanese government has come on my side with this trade is not any great comfort. Many intervention attempts have so FAR been able to weaken the Japanese currency only for a few nanoseconds.

If you think this is extreme, let me remind you that when I first went to Japan in the early seventies, the yen was trading at ?305, and had just been revalued from the Peace Treaty Dodge line rate of ?360. To me the ?78 I see on my screen today is unbelievable.

Noted hedge fund manager Kyle Bass says he is already in this trade in size. All he needs for it to work is for Japan to run out of domestic savers essential to buy the government?s domestic yen bond issues, who have pitifully had sub 1% yields forced upon them for the past 17 years. Then the yen, the bond market, and the stock market all collapse like a house of cards. Kyle says that could happen as early as the spring.

It?s All Over For the Yen

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-01-29 23:04:342012-01-29 23:04:34Is This the Chink in Japan?s Armor?

I am writing this report from a first class cabin on Amtrak?s California Zephyr en route from Chicago to San Francisco. The majestic snow covered Rocky Mountains are behind me. There is now a paucity of scenery, with the endless ocean of sage brush and salt flats of Northern Nevada outside my window, so there is nothing else to do but to write. My apologies to readers in Wells, Elko, Battle Mountain, and Winnemucca. It is a route long traversed by roving banks of Indians, itinerant fur traders, the Pony Express, my immigrant forebears in wagon trains, the transcontinental railroad, the Lincoln Highway, and finally US Interstate 80.

After making the rounds with strategists, portfolio managers, and hedge fund traders, I can confirm that 2011 was the most hellacious in careers lasting 30, 40, or 50 years. With the S&P 500 up 0.4% 2011, following a roaring 0.04% decline in 2010, the average hedge fund was up a pitiful 1%, and thousands lost money.

It is said that those who ignore history are doomed to repeat it. I am sorry to tell you that we are about to endure 2011 all over again. You can count on another 12 months of high volatility, gap moves at the opening, tape bombs, a lot of buying of rumors and selling of news, promises and disappointments from governments, and American markets being held hostage to developments overseas.

If you lost money in 2011, you will probably do so again in 2012, and should consider changing your line of work. It takes a special kind of person to make money in markets like these; someone who thrives on raw data and ignores the hype and the spin, who invests based on facts and not beliefs, and who thinks all things can happen at all times.? In other words, you need somebody like me, as my 40% return last year will attest. Those who don?t think they are up to it might consider pursuing that long delayed ambition to open a trendy restaurant, the thoughtful antique store, or finally get their golf score down to 80.

If you think I spend too much time absorbing conspiracy theories from the Internet, let me give you a list of the challenges I see financial markets facing in the coming year:

*Long term structural issues will overwhelm short term positives.

*Corporate profits continue to grow, but at a much slower rate, reaching diminishing returns.

*2009 stimulus spending is a distant memory, and there will be no replays.

*Bush tax cuts expire, creating a 1% drag on GDP.

*An epochal downsizing continues by state and local governments, chopping another 2-3% off of GDP.

*A recession in Europe further reduces American growth by 1%.

*Expect an actual default out of the continent in 2012, certainly from Greece, possibly also from Portugal and Ireland.

*There will be no QE3, since QE2 never filtered down to the real economy. There is little the Fed can do to help us.

*Huge demographic headwinds bring another leg down in the residential real estate market.

*The first baby boomer hit 65 last year and it is now time to pay the piper on entitlements.

*The new hot button social issue will become ?senior homelessness,? as millions retire without a cent in the bank and are unable to find jobs.

*Falling home prices bring secondary banking crisis, but this time there will be no TARP and no bail outs

*Gridlock in Washington prevents any real government solution, and there is nothing they can do anyway.

*Candidates from both parties will attempt to convince us that their opponents are crooks, thieves, idiots, or ideologues, and largely succeed. That will leave the rest of us confused and puzzled, and less likely to invest or hire.

*Unemployment remains stuck at an 8-9% level, then ratchets up to 15%. The real, U-6 rate soars to 25%.

Now let me give you a list of possible surprise positives, which may mitigate the list of negatives above.

*American multinationals continue to squeeze more blood out of a turnip and post stellar earnings increases yet again.

*China successfully slams the breaks on the real estate market without cutting the rest of the economy off at the knees and engineers a soft landing with 7%-8% GDP growth.

*Europe somehow pulls a new treaty out of its hat that addresses its structural financial and monetary shortfalls a decade ahead of schedule.

*Through some miracle, the American consumer keeps spending at the expense of a declining savings rate. There is evidence that this has been going on since October.

The Election Will Not Be Good for Risk Assets

So, let me summarize what your 2012 will look like. The ?RISK ON? trade that started on October 4 will spill into the new year, driven by value players loading up on cheap multinationals, chased by frantically short covering hedge funds, hitting a peak sometime in Q1. The S&P 500 could reach 1,350. In Q2 and Q3 traders will have to deal with flocks of black swans, giving 4-7 months of the ?RISK OFF? trade. We should rally into Q4 as markets discount the end of the election cycle. It really makes no difference who wins. The mere disappearance of electioneering will be positive for risk takers.

I Said ?Black Swans,? Not Crows!

The Thumbnail Portfolio

Equities-A ?V? shaped year, up, down, then up again Bonds-Treasuries grind towards new 60 year peaks, then an eventual collapse Currencies-dollar up and Euro and Australian, Canadian and New Zealand dollars down Commodities-Look to buy for a long term hold mid-year Precious Metals-take a longer rest, then up again Real estate-multifamily up, single family down, commercial sideways

1) The Economy-The Second Lost Decade Continues

I am sticking with a 2% growth forecast for 2012. I see the huge list of negatives above that add up to at least a 5% drag on the economy. There is only one positive that we can really count on. Corporate earnings will probably come in at $105 a share for the S&P 500 this year, a gain of 15% over the previous year, and a double off the 2008 lows. During the last three years we have seen the most dramatic increase in earnings in history, taking them to all-time highs, no matter how much management complains about over regulation.

Can the magic continue? I think not. Slowing economies in China and Europe will fail to deliver the stellar gains seen in 2011, which account for half the profits of many large multinationals.? A global economy that grew at 4.1% in 2010 and 2.5% in 2011 will probably eke out only a subdued 1.5% in 2012. A strong dollar will further eat into foreign revenues.

Cost cutting through layoffs is reaching an end as there is no one left to fire. Growing companies can?t delay new hires forever. That leaves technology as the sole remaining source of margin increases, which will continue its inexorable improvements. So corporate earnings will rise again in 2012, but possibly only by 5%-10%? to $105-$110 for the $S&P 500. Hint: technology will be the top performing sector in the market in 2012, with Apple (AAPL) taking the lead.

Deleveraging will remain a dominant factor affecting the economy for another 5-8 years. Much of the hyper growth we witnessed over the past 30 years, possibly half, was borrowed from the future through excessive credit, and it is now time to pay the piper. We are still at the beginning of a second lost decade. Don?t expect a robust GDP while governments, corporations, and individuals are sucking money out of the economy. This lines up nicely with my 2% target.

Forget about employment. The news will always be bad. I believe that the US has entered a period of long term structural unemployment similar to what Germany saw in the 1990?s. Yes, we may grind down to 8% before the election. But the next big move in this closely watched indicator is up, possible as high as 15%. Keep close tabs on the weekly jobless claims that come out at 8:30 AM Eastern every Thursday for a good read of the financial markets to head in a ?RISK ON? or ?RISK OFF? direction.

With a GDP growing at a feeble 2% in 2012, and corporate earnings topping out at $105-$110 a share, those with a traditional buy and old approach to the stock market will fare better taking this year off. While earnings are growing, multiples will shrink from 13 to 12, multiple? for the indexes unchanged. It is also possible that the economy will never meet the textbook definition of a recession, that of two back to back quarters of negative GDP numbers.? But the market will think the economy is going into recession and behave accordingly. ?Double dip? will get dusted off one again. Remember how ?Sell in May and Go Away? has worked so well for the past three years? This year you may want to sell in January.

I am looking for some new liquidity from value players and additional short covering to spill over into the New Year, possibly taking us up to 1,325-$1,350. If we get that high, take it as a gift, as the big hedge funds will be very happy to pile on the leveraged shorts at the top of a multiyear range.

A continuing stream of positive economic data will also help. Since we don?t have the ?oomph? offered by the tax compromise and QE2 a year ago, look for equities to peak much earlier than the April 29 apex we saw in 2011. The trigger for this deluge could be a sudden spike in jobless claims as the temporary Christmas hires are fired combined with economic data that cools coming off a hot Q4.

Let me tell you why the value players up here don?t get it. A 2% growth rate doesn?t justify the 10-22 price earnings multiple range that we have enjoyed during the last 30 years. At best it can support an 8-16 range, or maybe even the 6-15 range that prevailed when I first started on Wall Street 40 years ago. That makes the current 13 multiple look cheap according to old models, but expensive in the new paradigm.

When the guys in the white coats show up to drag away the value managers, they will be screaming that ?They were cheap,? all the way to the insane asylum. What these hapless souls didn?t grasp was that we are only four years into a secular, decade long downtrend in PE multiples, the bottom for which is anyone?s guess.

After that, the way should be clear for a 25% swoon down to 1,000, which will happen sometime in Q2 or Q3. That will be caused by a ton of new short selling triggered by the break of the 2011 low at 1,070, which then get stopped out on the upside. The heating up of trouble with Iran is another unpredictable variable, which is really just a pretext for attacking Syria, their only ally. How will the market decline in the face of growing earnings? That is exactly what markets did in 2011, once the fear trade was posted on the mast for all to see?

Crash, we won?t, and this is what my Armageddon friends don?t get. To break to new lows, you need sellers, and lots of them. Those were in abundance in 2008, when the bear market caught many completely by surprise, everyone was leveraged to the hilt, and risk controls provided all the security of wet tissue paper.

This time around it?s different. Prime brokers now require a pound of flesh as collateral, especially in the wake of the MF Global Bankruptcy, and leverage as almost an extinct species. In the meantime, individuals have been decamping from stocks en masse, with equity mutual fund sales over the past three year hitting $400 billion, compared to $800 billion in bond fund purchases. That will leave hedge funds the only players at an (SPX) of 1,000, who will be loath to run big shorts at multiyear bottoms. You can?t have a crash if there is no one left to sell.

That gives us the juice to rally into Q4, just as the presidential election is coming to an end. It really makes no difference who wins, as long as one doesn?t get control all three branches of government. My money is on Obama, who has the highest approval rate in history with unemployment at 8.6%. The mere fact that the election is over will lift a cloud of uncertainty overhanging risk assets. It will be a real stretch to hope that stock markets will close unchanged in 2012, as we did in 2011. My expectation is for a single digit loss for 2012.

This Could? be the Big Trade of 2012

Equities will be no place for old men

3) Bonds?? (TBT), (JNK), (PHB), (HYG), (PCY)

The single worst call by myself and the hedge fund industry at large this year was that massive borrowing by the Federal government would cause the Treasury bond market to collapse. Not only did it fail to do so, it blasted through to new 60 year highs, sending ten year yields to 1.80%, which adjusted for inflation is a real negative yield of -1.5% a year.

Investors today will get back 80 cents worth of purchasing power at maturity for every dollar they invest. But institutions and individuals will grudgingly lock in these appalling returns because they believe that the losses in any other asset class will be much greater.

What I underestimated was the absolute perniciousness of today?s deflation. The price for everything you want to sell is continuing a relentless fall, including your home and your labor.? The cost of the things you need to buy, like food, energy, health care, and education, is rocketing. Globalization is the fat on the fire. I call this ?The New Inflation?. This goes a long way in explaining the causes behind a 30 year decline in the middle class standard of living.

The other thing I miscalculated on was how rapid contagion fears spread from Europe. When the world gets into trouble, everyone picks up their marbles and goes home. For the financial markets, that translates into massive buying of the core ?flight to safety? assets of the US dollar and Treasury bonds.

While much of the current political debate centers around excessive government borrowing, the markets are telling us the exact opposite. A 1.80%, ten year yield is proof to me that there is a Treasury bond shortage, and that the government is not borrowing too much money, but not enough. Given the choice between what a politician wants me to believe and the harsh judgment of the marketplace, I will take the latter every time.

So what will 2012 bring us? More of the same. For a start, we have seen a substantial ?RISK ON? rally for the past three months where equities tacked on a virile 20% gain. Bond yields have ticked up barely 30 basis points from the lows, not believing in the longevity of this rally for one nanosecond. That tells me that the next equity sell off could see Treasury yields punch through to new lows, possibly down to 1.60%. Given even a modest recession, bond yields could touch 1%.

Surveying the rocky landscape that lies ahead of me, I expect to get five months of ?RISK ON? conditions and a turbulent and volatile seven months of ?RISK OFF?. This augers very well for a continuation of the bull market in Treasuries at least until August.

This scenario does not presage a good year for the riskiest corner of the fixed income asset class - junk bonds, whose default rates are not coming in anywhere near where they were predicted just a few months ago. Don?t get enticed by the siren song of high yields by the junk ETF?s, like (JNK), (PHB), and the (HYG). There will be better buying opportunities down the road.

As for municipal bonds, we are seeing only the opening act of a decade of fiscal woes by local government. Still, there is a good case for sticking with munis. No matter what anyone says, taxes are going up, and when they do, this will increase muni values. The continued bull market in Treasuries will do the same.

So if you hate paying taxes, go ahead and buy this exempt paper, but only with the expectation of holding it to maturity. Liquidity could get pretty thin along the way. Be sure to consult with a local financial advisor to max out the state, county, and city tax benefits. And thank Meredith Whitney for creating the greatest buying opportunity in history for muni bonds a year ago.

Perhaps the best place to live in bond world is in emerging market debt, where you can participate via the (PCY). At least there, you have the tailwinds of strong economies, little outstanding debt, appreciating currencies, and already high interest rates. But don?t buy here. This is something you want to pick up at the nadir of a ?RISK OFF? cycle, when the dollar and Treasury markets are peaking.

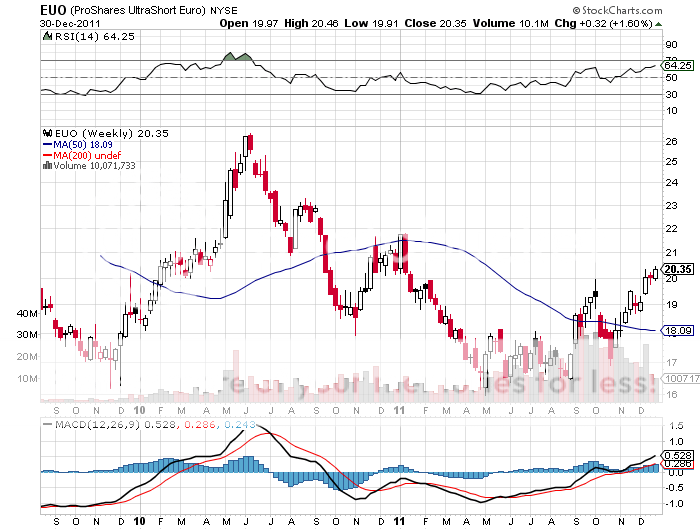

(FXC)

The Fat Lady Will Have to Wait to Sing for the Treasury Market

Any trader will tell you to never bet against the trend, and the overwhelming direction for the US dollar for the last 220 years has been down. The only question is how far, how fast. Going short the currency of the world?s largest borrower, running the greatest trade and current account deficits in history, with a diminishing long term growth rate is a no brainer.

But once it became every hedge fund trader?s free lunch, and positions became so lopsided against the buck, a reversal was inevitable. We seem to be solidly in one of those periodic bear market corrections, which began in March and could continue for several more months, or even years.

The big driver of the currency markets is interest rate differentials. With US interest rates safely at zero, and the rest of the world chopping theirs as fast as they can, this will provide a very strong tailwind for the greenback for much of 2012. Use rallies to sell short the Euro (FXE), (EUO), the Canadian dollar (FXC), the high beta Australian dollar (FXA), and the lagging New Zealand dollar (BNZ). Australians could see a print of 85 cents before the bloodletting is over, and should pay for their upcoming imports and foreign vacations now, while their currency is still dear.

The Euro presents a particular quandary for foreign exchange traders, with a never ending sovereign debt crisis causing its death through a thousand cuts. Just look at Greece, with a budget deficit of 13% of GDP against the 3% it promised on admission to the once exclusive club. But this is not exactly new news, and traders have already built shorts to all-time records. Still, the next crisis in confidence could easily take the Euro to $1.25, and new momentum driven shorts could take us to the $1.17?s.

As far as the Japanese yen is concerned, I am going to stay away. How the world?s worst economy has managed to maintain the planet?s strongest currency is beyond me. The problems in the Land of the Rising Sun are almost too numerous to count: the world?s highest debt to GDP ratio, a horrific demographic problem, flagging export competitiveness against neighboring China and South Korea, and the world?s lowest developed country economic growth rate. But until someone provides me with a convincing explanation, or until the yen decisively reverses, I?ll pass. Let hedge fund manager, Kyle Bass, figure this one out.

For a sleeper, use the next plunge in emerging markets to buy the Chinese Yuan ETF (CYB) for your back book, but don?t expect more than single digit returns. The Middle Kingdom will move heaven and earth to in order to keep its appreciation modest to maintain their crucial export competitiveness.

This is my favorite asset class for the next decade, as investors increasingly catch on to the secular move out of paper assets into hard ones. Don?t buy anything that can be manufactured with a printing press. Focus instead on assets that are in short supply, are enjoying an exponential growth in demand, and take five years to bring new supply online. The Malthusian argument on population growth also applies to commodities; hyperbolic demand inevitably overwhelms linear supply growth.

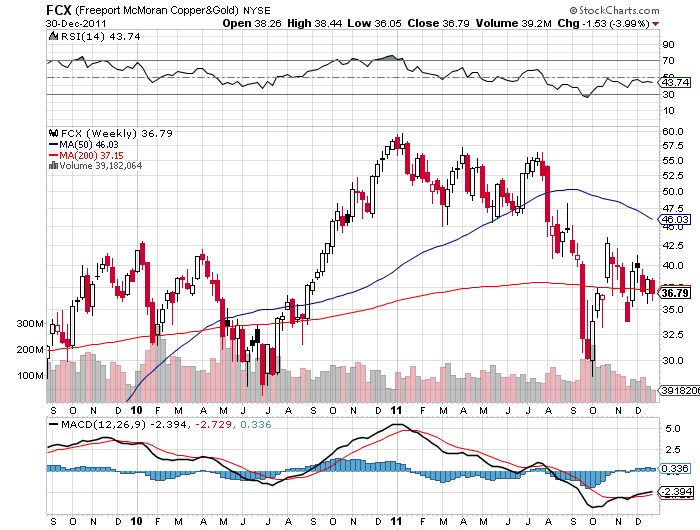

Of course, we?re already nine years into what is probably a 30 year secular bull market for commodities and these things are no longer as cheap as they once were. You?ll never buy copper again at 85 cents a pound, versus today?s $3.40. You are going to have to allow these things to breathe. Ultimately, this is a demographic play that cashes in on rising standards of living in the biggest and highest growth emerging markets. You can start with the traditional base commodities of copper and iron ore.

The derivative equity plays here are Freeport McMoRan (FCX) and Companhia Vale do Rio Doce (VALE). Add the energies of oil (DIG), coal (KOL), uranium (NLR), and the equities Transocean (RIG), Joy Global (JOY), and Cameco (CCJ).

As much as I love the long term case for hard commodities, I am not expecting any action in the immediate future. Commodities will remain a no go area until it is clear whether China?s economy will suffer a soft or a hard landing, or continues to remain airborne. Use this year?s big ?RISK OFF? trade to acquire serious positions. If markets rally into year end, you might catch a quick 50% gain in the more volatile securities.

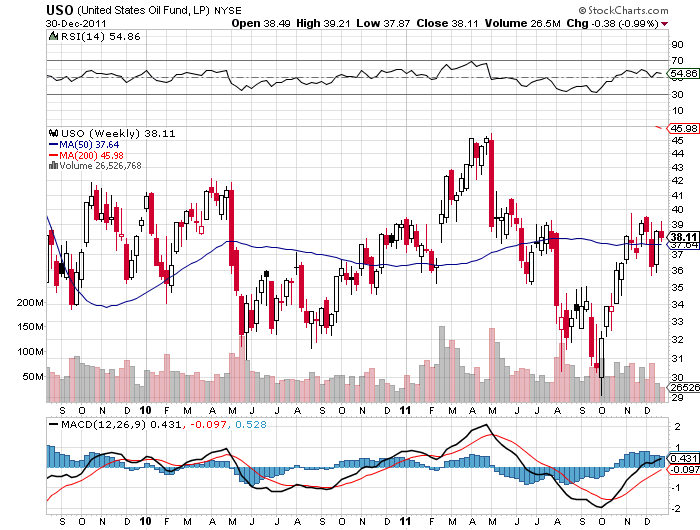

Oil has in fact become the new global de facto currency, and probably $30 of the current $100 price reflects monetary demand, and another $30 representing a Middle Eastern risk premium. Strip out these factors, and oil should be trading at $40.? That will help it grind to $100 sometime in early 2012, and we could spike as high as $120. After that, the ?RISK OFF? trade could take it back down to the $75 we saw in September.

Skip natural gas (UNG), because the discovery of a new 100 year supply from ?fracking? and horizontal drilling in shale formations is going to overhang this subsector for a very long time. Major reforms are required in Washington before use of this molecule goes mainstream.

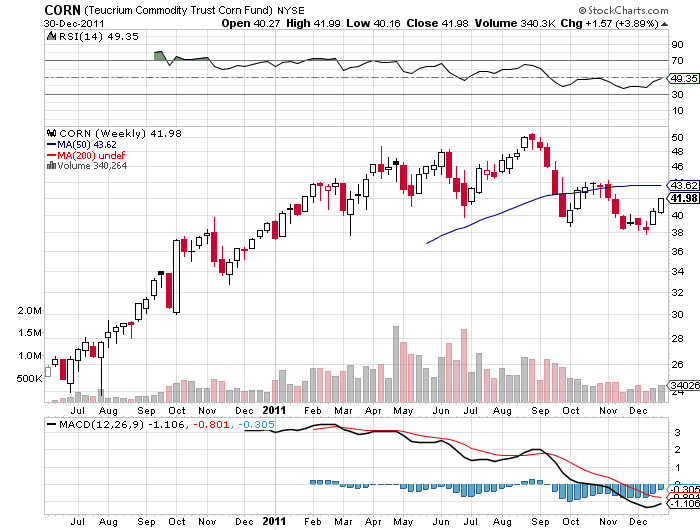

The food commodities are also a great long term Malthusian play, with corn (CORN), wheat (WEAT), and soybeans (SOYB) coming off the back of great returns in 2010. These can be played through the futures or the ETF?s (MOO) and (DBA), and the stocks Mosaic (MOS), Monsanto (MON), Potash (POT), and Agrium (AGU). The grain ETF (JJG) is another handy play. Though an unconventional commodity play, the impending shortage of water will make the energy crisis look like a cake walk. You can participate in this most liquid of asset with the ETF?s (PHO) and (FIW).

Let?s face it, gold is not a hard asset anymore, it?s a paper one. Since hedge funds and high frequency traders moved into this space, the barbarous relic has been tracking one for one with the S&P 500 and other risk assets.

The chip shot here is $1,500 on the downside, once the remaining hedge fund redemptions and other hot money are cleared out. If we have a real recession this year, $1,050 might be doable. Remember, the speculative frenzy is as great as it was in 1979, which saw the beginning of a 75% plunge in the yellow metal.

But the long term bull case is still there. Obama has not suddenly become a paragon of fiscal restraint. Bernanke has not morphed into a tightwad. When I pull a dollar bill out of my wallet, it?s as limp as ever.

If you forgot to buy gold at $35, $300, or $800, another entry point is setting up for those who, so far, have missed the gravy train. The precious metals have to work off a severely overbought condition before we make substantial new highs. Remember, this is the asset class that takes the escalator up and the elevator down, and sometimes the window.

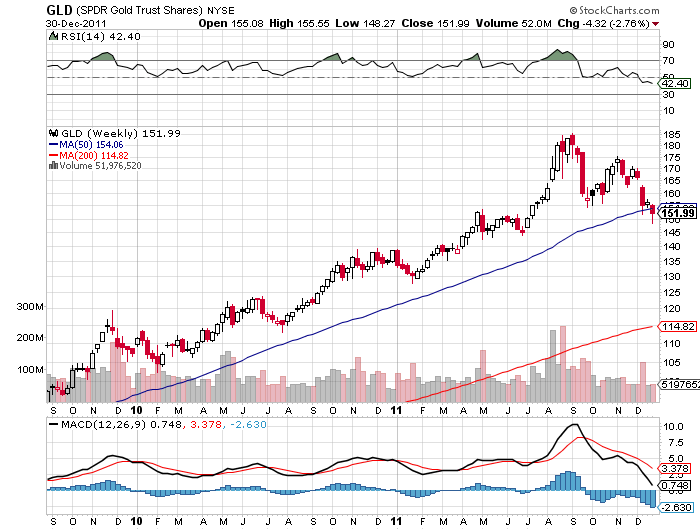

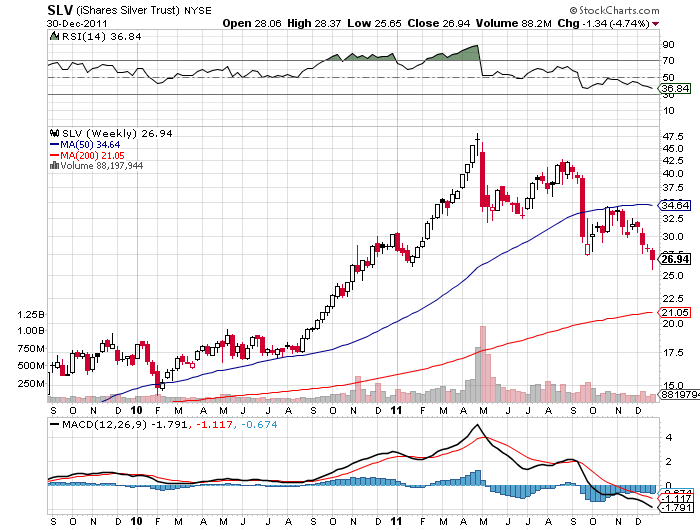

If the institutional world devotes just 5% of their assets to a weighting in gold, and an emerging market central bank bidding war for gold reserves continues, it has to fly to at least $2,300, the inflation adjusted all-time high, or more. ETF players can look at the 1X (GLD) or the 2X leveraged gold (DGP). But you should only go into these as part of a broader ?RISK ON? move.

I would also be using the next bout of weakness to pick up the high beta, more volatile precious metal,+ silver (SLV), which I think could hit $50 once more. Palladium (PALL) and platinum (PPLT), which have their own auto related long term fundamentals working on their behalf would also be something to consider on a dip.

Here?s a Nice Busted Bubble

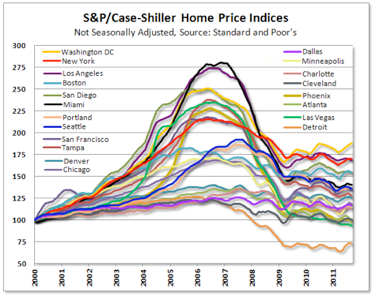

6) Real Estate

There is no point in spending much time on this most unloved of asset classes, so I?ll keep it brief. There are only three numbers you need to know in the housing market: there are 80 million baby boomers, 65 million Generation Xer?s who follow them, and 85 million in the generation after that, the Millennials.

The boomers have been desperately trying to unload dwellings to the Gen Xer?s since prices peaked in 2007. But there are not enough of them, and three decades of falling real incomes mean that they only earn a fraction of what their parents made. If they have prospered, banks won?t lend to them.

Now consider the coming changes that will affect this market. The home mortgage deduction is unlikely to survive any attempt to balance the budget. And why should renters be subsidizing homeowners anyway? Nor is the government likely to spend billions keeping Fannie Mae and Freddie Mac alive, which now account for 95% of home mortgages.

That means the home loan market will be privatized, leading to mortgages rates 200 basis points higher than today. If this sounds extreme, look no further than the jumbo market for proof. It is already bereft of government subsidy, and loans here are now priced at premiums of this size. This also means that the fixed rate 30 year loan will disappear, as banks seek to offload duration risk to consumers. This happened long ago in the rest of the developed world.

There is a happy ending to this story. By 2025 the Millennials will start to kick in as the dominant buyers in the market. Some 85 million Millennials will be chasing the homes of only 65 Gen Xer?s, causing housing shortages and rising prices. This will happen in the context of a labor shortfall and rising standards of living. In fact, the mid 2020?s could bring a repeat of our last golden age, the 1950?s.

The best case scenario for residential real estate is that it bounces along a bottom for another decade. The worst case is that it falls another 25% from here. Only buy a home if your wife is nagging you about living in that cardboard box under the freeway overpass. But expect to put up your first born child as collateral, and bring in your entire extended family in as cosigners if you want to get a bank loan. Then pray that the price starts to go up in 15 years. Rent, don?t buy.

Rent, Don?t Buy

Well, that?s all for now. We?ve just passed the Pacific mothball fleet and we?re crossing the Benicia Bridge, where the Sacramento River pours into San Francisco Bay. The pressure drop caused by an 8,000 foot descent from Donner Pass has crushed my water bottle. The Golden Gate and the soaring spire of the Transamerica building are just around the next bend. So it is time for me to unglug my laptop and pack up.

I?ll shoot you a trade alert whenever I see a window open on any of the trades above. Good trading in 2012!

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00DougDhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngDougD2012-01-02 21:00:542012-01-02 21:00:542012 Annual Asset Class Review

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.

Six Month Chart

Six Month Chart Five Year Chart

Five Year Chart

(FXC)

(FXC)