Mad Hedge Technology Letter

April 22, 2022

Fiat Lux

Featured Trade:

(THE FALLOUT FROM IBUYING)

(Z)

Mad Hedge Technology Letter

April 22, 2022

Fiat Lux

Featured Trade:

(THE FALLOUT FROM IBUYING)

(Z)

The real estate platform Zillow (Z) continues to underperform.

Readers should not buy the stock and I will tell you why.

Many of us, including me, want to overperform in business and we concoct all sorts of extreme strategies as the vehicle to take us to riches.

Zillow was not different.

They thought their business was too vanilla and wanted to snort that pixie dust to supercharge their business model.

That is why in 2018, Z launched a new initiative coined Zillow Offers, where it began purchasing homes of its own.

Fast forward about three years and a couple of billion dollars worth of home purchases later, and the company is now in the process of completely shutting down Zillow Offers.

The debacle wasn’t as bad as Bill Ackman’s 3 months pump and dump of Netflix, but it was of the same vein.

Exiting iBuying

The value of the homes Zillow acquired deviated big time. This hurt Zillow's profitability and increased the riskiness of its balance sheet, as the value of the homes could swing wildly.

Zillow Offers, however, was starting to weigh on their normal business of selling ads to people who look at real estate on their platform. Also, 90% of Zillow's offers on homes were rejected by sellers, suggesting that Zillow was hurting its reputation with many homeowners.

Next is where one might believe Zillow can wash its hands of past failures and move on.

Incorrect.

As the 30-year fixed mortgage rate has climbed to 5.20% at the time of this writing, that has turned off many potential buyers and visitors to the website by pricing them out of the market.

Potential buyers are the most ravenous consumers of Zillow’s platform because they hope to jump on a new listing after its listed and convert this info into a new house.

As the fixed mortgage becomes exorbitant, prices have not come down because of a dearth of inventory as builders stick to only building luxury dwellings.

These new record highs in American real estate prices have been achieved on scant volume which is bad news for Zillow’s platform.

As the overarching economy exhibits more stagflation, potential buyers will allocate finite budgets to essentials like food and gas.

Downsizing or upsizing isn’t in the cards for many.

Especially families with children who will essentially need to leave their city if they sold their house and their 2.5% mortgage rate. The move to the sun belt from coastal areas has largely run its course.

The net net of everything is that everybody is staying in place, renters are extending leases even contacting their landlords 4.5 months before the end to lock another year in. People aren’t migrating to other cities as well.

Homeowners are stuck in their houses avoiding a scenario where they can’t find a rental or a new purchase if they sell their current house.

No traffic means no eyeballs for Zillow (Z) and their ad business will suffer.

This is why they were so desperate to supercharge the business model by grasping at straws that glamorously backfired.

Unfortunately, Zillow is still confined by the market we are in amid a backdrop of spiking rates and souring consumer sentiment.

Like the very consumers it services, Zillow, too, cannot upsize and upgrade its situation.

It’s not like they have $43 billion in secured funding to buy a social media company or anything like that.

Now is a time to pull back and sell any tech rallies because innovation at many levels in tech has become stale.

There are many mature models out there that need reinvention or risk becoming zombie companies.

Readers shouldn’t touch Zillow until mortgage rates become more reasonable for the median buyer.

Global Market Comments

November 19, 2021

Fiat Lux

Featured Trade:

(NOVEMBER 17 BIWEEKLY STRATEGY WEBINAR Q&A),

(RIVN), (WMT), (BAC), (MS), (GS), (GLD), (SLV), (CRSP), (NVDA),

(BAC), (CAT), (DE), (PTON), (FXI), (TSLA), (CPER), (Z)

Below please find subscribers’ Q&A for the November 17 Mad Hedge Fund Trader Global Strategy Webinar broadcast from the safety of Silicon Valley.

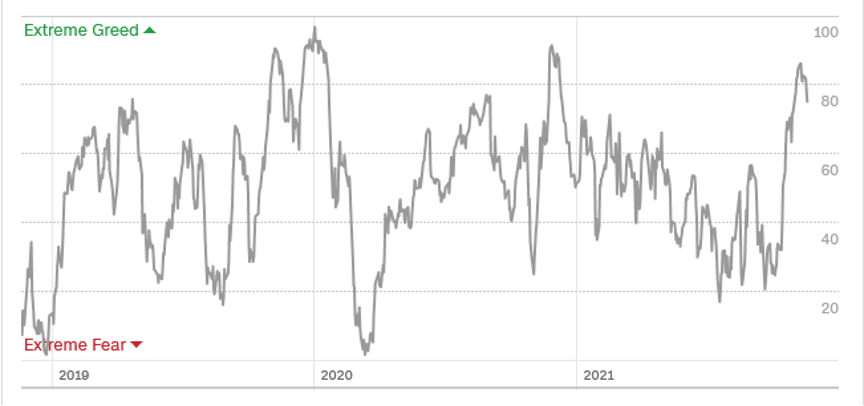

Q: Even though your trading indicator is over 80, do you think that investors should be 100% long stocks using the barbell names?

A: Yes, in a hyper-liquidity type market like we have now, we can spend months in sell territory before the indexes finally rollover. That happened last year and it’s happening now. So, we can chop in this sort of 50-85 range probably well into next year before we get any sell signals. Selling apparently is something you just do anymore; if things go down, you just buy more. It’s basically the Bitcoin strategy these days.

Q: What do you think about Rivian's (RIVN) future?

A: Well, with Amazon behind them, it was guaranteed to be a success. However, we mere mortals won't be able to buy any cars until 2024, and they have yet to prove themselves on mass production. Moreover, the stock is ridiculously expensive—even more than Tesla was in its most expensive days. And it’s not offering any great value, just momentum so I don’t want to chase it right here. I knew it was going to blow up to the upside when the IPO hit because the EV sector is just so hot and EVs are taking over the global economy. I will watch from a distance unless we get a sudden 40% drawdown which used to happen with Tesla all the time in the early days.

Q: Are you worried about another COVID wave?

A: No, because any new virus that appears on the scene is now attacking a population that is 80-90% immune. Most people got immunity through shots, and the last 10% got immunity by getting the disease. So, it’s a much more difficult population for a new virus to infect, which means no more stock market problems resulting from the pandemic.

Q: Is investing in retail or Walmart (WMT) the best way to protect myself from inflation?

A: It’s actually quite a good way because Walmart has unlimited ability to raise prices, which goes straight through to the share price and increases profit margins. Their core blue-collar customers are now getting the biggest wage hikes in their lives, so disposable income is rocketing. And really, overall, the best way to protect yourself from inflation is to own your own home, which 62% of you do, and to own stocks, which 100% of the people in this webinar do. So, you are inflation-protected up the wazoo coming to Mad Hedge Fund Trader. Not to mention we buy inflation plays like banks here.

Q: Why are financials great, like Bank of America (BAC)?

A: Because the more their assets increase in value, the greater the management fees they get to collect. So, it’s a perfect double hockey stick increase in profits.

*Interest rates are rising

*Rising interest rates increase bank profit margins

*A recovering economy means default rates are collapsing

*Thanks to Dodd-Frank, banks are overcapitalized

*Banks shares are cheap relative to other stocks

*The bank sector has underperformed for a decade

*With rates rising value stocks like banks make the perfect rotation play out of technology stocks.

*Cryptocurrencies will create opportunities for the best-run banks.

Q: Do you think the market is in a state of irrational exuberance?

A: Yes. Warning: irrational exuberance could last for 5 years. That’s what happened when Alan Greenspan, the Fed governor in 1996, coined that phrase and tech stocks went straight up all the way up until 2000. We made fortunes off of it because what happens with irrational exuberance is that it becomes more irrational, and we’re seeing that today with a lot of these overdone stock prices.

Q: Should I hold cash or bonds if you had to choose one?

A: Cash. Bonds have a terrible risk/reward right now. You’re getting like a 1% coupon in the face of inflation that's at 6.2%. It’s like the worst mismatch in history. In fact, we made $8 points on our bond shorts just in the last week. So just keep selling those rallies, never own any bonds at all—I don’t care what your financial advisor tells you, these are worthless pieces of paper that are about to become certificates of confiscation like they did back in the 80s when we had high inflation.

Q: What’s your yearend target for Nvidia (NVDA)?

A: Up. It’s one of the best companies in the world. It’s the next trillion dollar company, but as for the exact day and time of when it hits these upside targets, I have no idea. We’ve been recommending Nvidia since it was $50, and it’s now approaching $400. So that’s another mad hedge 20 bagger setting up.

Q: What about CRISPR Therapeutics (CRSP)?

A: The call spread is looking like a complete write-off; we missed the chance to sell it at $170, it’s now at $88. So, I’m just going to write that one-off. Next time a biotech of mine has a giant one-day spike, I am selling. What you might do though with Crisper is convert your call spread to straight outright calls; that increases your delta on the position from 10% to 40% so that way you only need to get a $20 move up in the stock price and you’ll get a break-even point on your long position. So, convert the spreads to longs—that’s a good way of getting out of failed spreads. You do not need a downside hedge anymore, and you’ll find those deep out of the money calls for pennies on the dollar. That is the smart thing to do, however, you have to put money into the position if you’re going to do that.

Q: Would you buy a LEAP in Tesla (TSLA) at this time?

A: No, it’s starting a multi-month topping out process, then it goes to sleep for 5 months. After it’s been asleep for 5 months then I go back and look at LEAPS. Remember, we had a 45% drawdown last year. I bet we get that again next year.

Q: Will inflation subside?

A: Probably in a year or so. A lot depends on how quickly we can break up the log jam at the ports, and how this infrastructure spending plays out. But if we do end the pandemic, a lot of people who were afraid of working because of the virus (that’s 5 or 10 million people) will come back and that will end at least wage inflation.

Q: When is the next Mad Hedge Fund Trader Summit?

A: December 7, 8, and 9; and we have 27 speakers lined up for you. We’ll start emailing probably next week about that.

Q: Are gold (GLD) and silver (SLV) getting close to a buy?

A: Maybe, unless Bitcoin comes and steals their thunder again. It has been the worst-performing asset this year. The only gold I have now is in my teeth.

Q: Morgan Stanley (MS) is tanking today, should I dump the call spread?

A: I’m going to see if we hold here and can close above our maximum strike price of $98 on Friday. But all of the financials are weak today, it’s nothing specific to Morgan Stanley. Let’s see if we get another bounce back to expiration.

Q: Where can I view all the current positions?

A: We have all of our positions in the trade alert service in your account file, and you should find a spreadsheet with all the current positions marked to market every day.

Q: What is the barbell strategy?

A: Half your money is in big tech and the other half is in financials and other domestic recovery plays. That way you always have something that’s going up.

Q: Is Elon Musk selling everything to avoid taxes from Nancy Pelosi?

A: Actually, he’s selling everything to avoid taxes from California governor Gavin Newsom—it’s the California taxes that he has to pay the bill on, and that’s why he has moved to Texas. As far as I know, you have to pay taxes no matter who is president.

Q: Will the price of oil hit $100?

A: I doubt it. How high can it go before it returns to zero?

Q: Is it time to buy a Caterpillar (CAT) LEAP?

A: We’re getting very close because guess what? We just got another $1.2 billion to spend on infrastructure. Not a single job happens here without a Caterpillar tractor or a tractor from Komatsu for John Deere (DE).

Q: Will small caps do well in 2022?

A: Yes, this is the point in the economic cycle where small caps start to outperform big caps. So, I'd be buying the iShares Russell 2000 ETF (IWM) on dips. That's because smaller, more leveraged companies do better in healthy economies than large ones.

Q: Is it too late to buy coal?

A: Yes, it’s up 10 times. The next big move for coal is going to be down.

Q: Peloton (PTON) is down 300%; should I buy here?

A: Turns out it’s just a clothes rack, after all, it isn't a software company. I didn’t like the Peloton story from the start—of course, I go outside and hike on real mountains rather than on machines, so I’m biased—but it has “busted story” written all over it, so don’t touch Peloton.

Q: Will spiking gasoline prices cause US local governments to finally invest in Subways and Trams like European cities, or is this something that will never happen?

A: This will never happen, except in green states like New York and California. A lot of the big transit systems were built when labor was 10 cents a day by poor Irish and Italian immigrants—those could never be built again, these massive 100-mile subway systems through solid rock. So if you want to ride decent public transportation, go to Europe. Unfortunately, that’s the path the United States never took, and to change that now would be incredibly expensive and time-consuming. They’re talking about building a second BART tunnel under the bay bridge; that’s a $20 billion, 20-year job, these are huge projects. And for the last five years, we’ve had no infrastructure spending at all, just lots of talk.

Q: Would Tesla (TSLA) remains stable if something happened to Elon Musk?

A: Probably not; that would be a nice opportunity for another 45% correction. But if that happened, it would also be a great opportunity for another Tesla LEAPS. My long-term target for the stock is $10,000. Elon actually spends almost no time with Tesla now, it’s basically on autopilot. All his time is going into SpaceX now, which he has a lot more fun with, and which is actually still a private company, so he isn’t restricted with comments about space like he is with comments about Tesla. When you're the richest man in the world you pretty much get to do anything you want as long as you're not subject to regulation by the SEC.

Q: How realistic is it that holiday gatherings will trigger a huge wave of COVID in the United States forcing another lockdown and the Fed to delay a rise in interest rates?

A: I would say there’s a 0% chance of that happening. As I explained earlier, with 90% immunity in much of the country, viruses have a much harder time attacking the population with a new variant. The pandemic is in the process of leaving the stock market, and all I can say is good riddance.

Q: What about the Biden meeting with President Xi and Chinese stocks (FXI)?

A: It’s actually a very positive development; this could be the beginning of the end of the cold war with China and China’s war on capitalism. If that’s true, Chinese stocks are the bargain of the century. However, we’ve had several false green lights already this year, and with stuff like Microsoft (MSFT) rocketing the way it is, I’d rather go for the low-risk high-return trades over the high-risk, high return trades.

Q: What’s your opinion of Zillow (Z)?

A: I actually kind of like it long term, despite their recent disaster and exit from the home-flipping business.

Q: Do you like copper (CPER) for the long term?

A: Yes, because every electric car needs 200 lbs. of copper, and if you’re going from a million units a year to 25 million units a year, that’s a heck of a lot of copper—like three times the total world production right now.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last ten years are there in all their glory.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

An Old Fashioned Peloton (a Mountain)

Mad Hedge Technology Letter

November 3, 2021

Fiat Lux

Featured Trade:

(AVOID THIS TECH STOCK)

(Z)

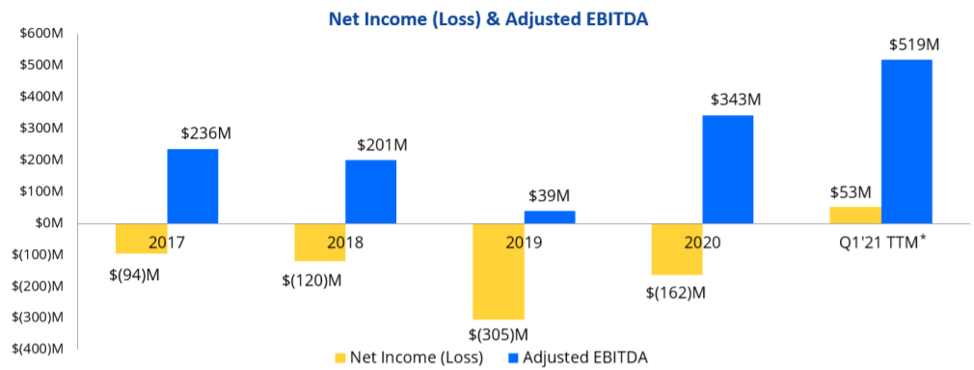

Zillow iBuying division, Zillow Offers, registered a meager average gross loss per home sold of $80,771.

This division did so bad that they are closing it down translating into a culling of 25% of the workforce.

Zillow's co-founder and CEO Rich Barton is to blame for this disastrous attempt at going from a digital ad company on a real estate platform to a full-blown house flipping company.

This idea probably looked good on paper at first (though I'm not sure how) but executing it was hell.

It seemed that nobody even considered the carrying costs, such as HOA fees, local property taxes, utilities, home insurance, appraisal costs that added up to most of the gross loss per house.

And the fact that competition to buy housing lately has resulted in buyers offering well above the listed price should have sent a warning signal to stay out of this.

It is hard to understand how they would ever make a profit while employing 2,000 full-time iBuying employees to carry this out.

Even if profit could be possible, it would be minimal at best.

Zillow partially blamed the algorithms for the lack of success, but I would lean towards saying this was a hopeless endeavor from the start.

The failure has led to a total write-down of more than $540 million and the company said it was halting new purchases of homes, so at least they got that right.

In the earnings report, Zillow Offers purchased homes during the last quarter for prices higher than it believes it can sell them.

It also could be a sign for a short-term post-pandemic market top in housing.

Flipping houses doesn’t work when buying at the market peak and Zillow, who possesses the most real estate data out of anyone, should have known that.

Yes, housing prices are unpredictable, but this is not a type of business that can scale.

Flipping houses also has to do with finding anomalies, bargains, or renovating fixer-uppers which are hard to do now because supply chain disruptions and the labor shortage are causing a backlog in home repairment services.

Instead of going so far off the path from their core business, they should have just bought Bitcoin in 2018 or even big tech and sat on the couch and watched it appreciate.

We all try to minimize our cost of doing business and Zillow chose to shoulder outsized risk in an unscalable business.

Zillow Offers tried to offer homeowners a fair market cash offer; or at least that was the plan.

The idea was to grow that service and offer it to a wider audience. But because of the price forecasting volatility, the company had to reconsider and management probably realized they needed a lot more capital which would create massive problems in the quarter-to-quarter balance sheet.

Remember selling ads is a remarkably predictable revenue stream for these platforms.

Much of their revenue are annuity-like.

The competition in the market amid other iBuyers meant that most proposals Zillow Offers made to homeowners were rejected.

Only 10% of offers from Zillow were accepted because the housing market has largely been irrational the past 18 months.

I commend Zillow for cutting their losses, and they still need to work through their backlog of already purchased homes which will surely result in a higher than $80,000 per unit loss.

Zillow ended the quarter with 9,790 homes in inventory and 8,172 homes under contract that it will still purchase, which it will sell over the next six months or at least try to.

The company should do what it does best — sell ads.

Consequently, Zillow’s stock has been battered peaking at $200 this February and now at $70.

I personally wouldn’t touch Zillow stock with a 10-foot pole, and would be suspicious of management if they announce some grand plan to regain momentum.

Management needs wholesale changes to get back to its core competencies.

It’s a crime that it took 3 years for Zillow to figure out this was a cruddy direction.

Mad Hedge Technology Letter

May 10, 2021

Fiat Lux

Featured Trade:

(WILL INVESTORS PAY THE HIGH PREMIUM FOR ZILLOW?)

(Z)

In a typical year, spring begins the traditional home-buying season. But we know that this past year was anything but ordinary.

An internal Zillow (Z) report indicated that the pandemic has indeed caused people to rethink where they live and concludes that approximately 8 million existing homeowner households that have been on the sidelines may enter a real estate market already beset by unrelenting demand.

Also, 8.9% of consumers plan to purchase a home in the next six months near a 20-year high per the conference board's April consumer confidence survey.

The housing market is underpinned by demographic and economic tailwinds that will persist for the foreseeable future.

Millennials are moving up.

Baby Boomers are downsizing and in between, people of all generations are rethinking their lives.

Zillow (Z) is the most popular real estate portal in the country with hundreds of millions of consumers visiting the platform.

It’s easy to put up an advertisement on Zillow, while other competitors need to spend tens of millions of dollars to generate those leads.

It’s a sustainable competitive advantage which is one of the main factors for the stock going from $20 to $200 last year.

This effectively makes Zillow’s customer acquisition cost zero!

And because of that, it’s disappointing that they aren’t more profitable.

The PE ratio is currently 517 and as we look forward, we need to ask ourselves, will investors continue to bid up this high growth real estate tech stock?

This past quarter’s revenue growth was strong with Zillow reporting Q1 revenue of $1.2 billion, exceeding the high end of the forecast.

Q1 Internet, media, and technology (IMT) segment revenue was $446 million, grew 35% year-over-year, as this company continues to see accelerated growth in Premier Agent and strong growth in rentals.

This is Zillow’s bread and butter and represented over 37% of their total revenue.

Premier Agent revenue that connects realtors to consumers grew 38% year-over-year in Q1, the accelerated growth was primarily driven by connections growing faster than traffic, as well as focus on providing outstanding service and optimizing to connect high intent customers with high performing partner agents.

The inherent strength of the company lies in being the Uber of real estate and matching up ad-paying agents to customers.

However, I do believe we are hitting the high-water mark in the short-term as housing inventory levels hit generational lows and sellers stop putting their homes up for sale.

Therefore, it’s easy to argue that Zillow and its revenue growth will have a hard time pushing incremental growth now, and like many other tech firms, are facing tough metrics to beat year-over-year in for next earnings’ season.

Cratering interest rates of 2020 was the catalyst that drove the incremental buyer into the market, and I believe that harvest has mostly been collected.

Prospective buyers simply are at the extreme upper limit of affordability, now that the median house for sale in the U.S. is around $400,000.

Growth in Zillow Offers which is direct purchase and sale of homes continued to reaccelerate in Q1.

Zillow reported home segment revenue of $704 million, which exceeded the high-end outlook with 1,965 home sales.

Purchases increased to 1,856 homes in the quarter from 1,789 homes purchased in Q4, but not quite at the rapid pace planned as Zillow continued to work on retooling algorithm models to catch up with the rapid acceleration in home price appreciation.

The flipping game is just becoming too expensive, even for a subsidized tech corporation like Zillow and the algorithms are having a hard time competing with properties selling for $50,000 over the asking price!

Zillow is now competing with Qatar Sheikhs, sovereign wealth funds, and family offices of the elite who are piling into U.S. residential real estate at the same time.

Management has said they “buy homes at the median”, but wait, I thought technology would find the market inefficiencies in the pricing and Zillow would be able to find discounts.

Apparently not and that goes out of the window in an era of ultra-liquidity.

Management also claims they avoid buying houses in “really wealthy or really unique neighborhoods because they’re harder to resell and harder to price.”

The problem I have with Zillow Offers is that this division would be sucker-punched by a devastating blow from a property market pullback and be stuck with the carrying costs of thousands of mortgages and homeowner association fees per month.

That’s most likely the real reason for avoiding pricey areas.

Also, there is the conundrum that in market downdrafts, pricing power in the neighborhoods that Zillow targets fall fastest in terms of velocity of price and quality of buyer.

Even more worrying, Zillow charges the seller a fee of about 7.5% on average, which is notably higher than the traditional 6% commission a seller pays to realtors.

I thought technology was supposed to incite a deflationary effect?

Apparently not.

Mortgages segment revenue increased 169% year-over-year in Q1 to $68 million and was primarily driven by mortgage loan origination volume, which was up more than 8x year-over-year.

Sure, the 8x growth looks great on paper, but this division is still only 5% of total revenue and is a recipient of the law of small numbers looking better than they are.

In Q1, refinance loan origination volume comprised 90% of total origination volume.

There will be no refi boom in 2021.

Zillow really missed a gold mine in the mortgage division last year when they couldn’t even turn a profit in this division.

For the IMT segment, Zillow is forecasting 66% year-over-year revenue growth in Q2.

This is Zillow’s strength and you can expect Premier Agent revenue to be between $342 million to $350 million up 80% year-over-year.

On a sour note, they expect mortgage segment revenue to be down from Q1 and with respect to margins, Zillow’s Q2 IMT margin is expected to be 41% down sequentially from the 47% in Q1.

It’s clear that on the horizon, margins will shrink and nascent businesses will stall, and that’s a poor recipe for short-term price action in shares.

I don’t think investors will pay the current high premium for Zillow at these inflated levels, and yes, it’s a great buy and hold long term company, with a superior ad business that connects agents, but I do not see the case for the next leg up in the next few months.

This year will be remembered as a consolidation year as a few years of revenue were brought forward because of a once-in-a-lifetime interest rate collapse and pandemic tailwind.

Unfortunately, this year might just be too boring to 10X Zillow’s stock.

Mad Hedge Technology Letter

March 1, 2021

Fiat Lux

Featured Trade:

(HOUSING GOES DIGITAL)

(Z), (RDFN)

One of the more bizarre knock-on effects of the health crisis is the swaths of people doing at-home reconnaissance work on where and how to relocate via the online real estate platform Zillow (Z).

When a polar vortex hits the South of the United States causing electricity bills to spike north of $6,000 per month and folks to boil snow to flush toilets because water treatment facilities are down, you bet that internet search for relocation would explode in a heartbeat.

Well, Zillow makes this a reality and facilitates the better understanding of what type of houses are where and for what listing prices giving users access to an interactive map of properties for sale.

Not only are homes for sale listed, but Zillow has a thriving rental market function where many landlords post units for rent with contact information and details.

The pandemic has been a godsend for Zillow who was floundering before the virus.

Stuck between migrating to selling properties directly from the platform and a slow-to-move advertising business, they couldn’t get their act together.

Fast forward to today, clicks and eyeballs on Zillow have skyrocketed with some looking for larger homes.

Looking for a house during climate change is the new thing to do.

And then there are those who don't even know why they are endlessly looking at listings on the real estate site and most likely because they are bored.

Whatever the reason, the result is clear: Zillow's website traffic numbers are surging.

Some regions have felt some serious follow-through with the newfound attention like the state of Florida.

With its moderate temperature and suppression of state taxes, it's no surprise to see Miami, Tampa Bay, Palm Beach, and Fort Myers, Florida in the top 20 in terms of traffic. Broader demographic and structural shifts also lifted Pennsylvania cities like Scranton and Allentown.

The top three were Las Vegas, Stamford, Connecticut, and Austin, Texas.

Of the 100 largest metros in the country, every one of them saw an increase in traffic.

Millennials are the largest generational group in the country and they're barreling towards home-buying years. They're hitting their mid-30s. They want stability.

Zillow describes it as “the great reshuffling,” and it's leading to a lot more than just a spike in Zillow traffic.

In all four corners of the country, the property market is scolding hot and the median time that a home goes on the market and then goes to pending is 17 days as of December.

That's 25 days faster than a year ago.

How do the numbers look under the hood?

Gangbusters.

Zillow had 9.6 billion page visits to its website and to its app in 2020.

That was up 1.5 billion from 2019.

Zillow shares have been the ultimate benefactor with shares surging up around 500% since the March 2020 bottom.

The ongoing growth acceleration in the real estate macro environment, a sustainable shift in real estate activity online, and the longer-term opportunity for these companies to capture share of industry economics all bode well for the stock price.

Given the pandemic driven outperformance across the internet sector, with housing activity and buyer demand continuing to accelerate, new listings growth and velocity offsetting challenges to supply and lower mortgage rates drive a more affordable buyer environment despite meaningful home price appreciation.

I expect that the macro impact alone will lead to upward forward earnings revisions in the category as companies report results.

I believe that a tectonic shift of real-estate activity online continues.

Lastly, Zillow’s investments in technology and business model evolution which improves conversion of site visitors to home buyers and sellers, increase purchase and sale options, and enhance the experience for agents and consumers.

In the end, this will increase the number of property purchasers.

It’s hard not to see financial outperformance in the near-term future for Zillow.

The growth in the existing home sales market and home price appreciation will continue to benefit Zillow and I expect views of between 13-14 billion in 2021 which sets up the opportunity for Zillow to beat in revenue and profitability. I would also take a look at Redfin Corporation (RDFN) who has a similar business model.