Mad Hedge Technology Letter

August 19, 2019

Fiat Lux

Featured Trade:

(ZILLOW’S BAD MOVE)

(Z),

Mad Hedge Technology Letter

August 19, 2019

Fiat Lux

Featured Trade:

(ZILLOW’S BAD MOVE)

(Z),

If you think Zillow posting lower guidance for the third quarter was a one-off event then open your eyes a little bigger – real estate conditions for selling homes will most likely worsen even though interest rates have dropped in a rapid fashion of late.

In fact, the velocity of the recent interest rate drop is a harbinger for an upcoming recession or the best we can hope for is a mild slowdown even if not recessionary.

Who is that company that leveraged up to make big bets at the top of the economic cycle?

Zillow.

There are smart times to do risky business and times to sit on your hands and wait.

Timing couldn’t have been more abysmal.

Zillow also confided to investors that their business that facilitates agents to connect with potential home buyers for a fee will burn $80 million in the third quarter before EBITDA.

But Zillow didn’t stop there.

They have mobilized a good chunk of their chips betting that house flipping is a good idea when the global economy is decelerating at warp speed and price appreciation in property value is slowing meaningfully.

They even broke off around 41.5% of its revenue from selling homes in the three months ending June 30 which could be the high watermark.

Precisely $248.9 million of $599.6 million in revenue came from Homes segment which is described as buying up property and selling them on for a profit.

Investors must calculate whether Zillow will get stuck with thousands of properties and the cost of carry.

Zillow could enter a situation where nobody will buy their properties and must sell them for deep discounts.

That is the end game and Zillow and its audacious management is barreling right ahead.

This worse case scenario would put heavy pressure on their ability to service debt.

Other signs have gone unnoticed like the recent canary in the coal mine of recessionary data from manufacturing in the U.S.

The slowdown in the volume of housing sales has been pronounced too.

In the current market, many buyers and particularly homebuyers are priced out of the market supported by the lack of buyers even with historically lower rates.

Refinancers took advantage of these rates to cut their debt load but there has been a lukewarm response and no flurry of new homebuying that economist had predicted.

As the global slowdown veers closer and closer to the American economy, Zillow could be in for a hard landing and whoever is caught out with too many properties in the wrong markets is doomed too.

Then there are other risks such as climate change and a wildfire season that is about to grow fiercer by the year.

Can Zillow absorb another hurricane in Houston or New Orleans?

Zillow has not only levered up on the type of business but as well as dipping into the M&A sphere by gobbling up StreetEasy for $50 million in 2013 and Trulia for $3.5 billion the following year.

The company has been caught asleep at the wheel by a stagnating digital ads business which was once the bread and butter.

Management’s response of electing to go for a riskier business instead of the lower hanging fruit of ramping up the digital ad business is a head-scratcher.

Digital ads can be scaled easier than buying physical homes, and 2020 could be a year to forget for Zillow and it is too late to sell on these assets without a deep discount.

Any tech company scaling their tech know-how has been an outsized winner.

Everybody and their mother are preparing for a global slowdown and American recession except Zillow.

I am bearish Zillow for the rest of the year and 2020.

Stocks that negatively correlate with higher trending interest rates are on a suicide mission as the Fed gradually raises interest rates because of the robust domestic economy hitting on all cylinders.

That is why I am unequivocally bearish on online real estate database companies Zillow (Z) and Redfin (RDFN).

Invest in these stocks at your peril because the short-term path to accelerated EPS growth and higher revenue growth looks treacherous at best.

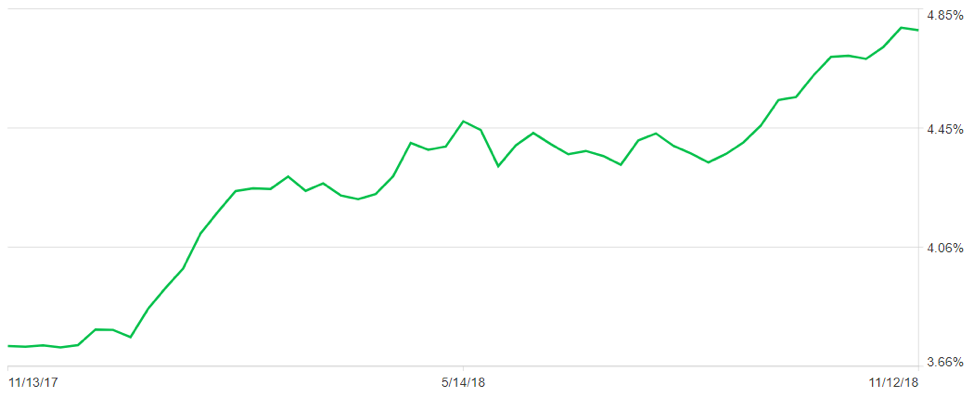

The last few months has brought forth a massive contraction in mortgage applications as a lack of affordability cripples home buyers around the country.

Buyers are simply waiving the white flag and giving up home searches unable to digest the potential monthly mortgage payments.

As recent as last week, mortgage applications dropped 4% from the previous week and this is only the tip of the iceberg.

Buyers are holding off pulling the trigger and have concluded that housing is about to peak, or the peak is in view.

Why splurge on a big investment when you can buy a house cheap on the next dip?

The supposed silver lining is that inventory is slightly up but that is largely irrelevant because the inching up stems from a dire shortage of inventory that incited vicious bidding wars in the most sought-after metropolitan areas mainly around the east and west coasts.

This is all bad news for Zillow and Redfin who are the main real estate database firms buyers use to do research on the properties and sellers use to advertise housing-related products.

The more buyers drop out of the market altogether, the fewer eyeballs gravitate towards these platforms creating less traffic volume.

Aptly aware of the pitfalls around this business model, both Redfin and Zillow desperately attempted to evolve and fortify their business model.

They decided to get into the business of selling houses and originating mortgage loans when real estate specialists view short-term housing prices in a precarious situation at best.

Zillow preceded this up by purchasing online mortgage lender, Mortgage Lenders of America, which is a dangerous short-term bet as the loan book could sour if the real estate market is crushed by rising rates.

Buy low and sell high, it seems Zillow understood this the other way around.

One bright note was that Zillow shouldn’t face liquidity problems because the purchase was made in cash for $65 million.

Attempts to corner the real estate advertising market was Zillow’s cash cow, and careening into a high-risk part of the real estate market at the wrong time could turn into a painful write-off.

Both of these companies are chronic loss-markers and if the recession graces our shores earlier than expected, it could stick Zillow and Redfin with a hefty inventory of housing units in a downtrodden market.

Pouring fuel on the flames, turning into a mortgage lender could cannibalize 3rd party agent business who could decide to pull the plug on their listings and ads from the database completely.

This could be dreadful for Zillow because the main source of revenue is the advertising revenue they rely on from its platform.

In one fell swoop, Zillow effectively damaged both businesses failing to recognize the disconnection of the synergies between them.

I would argue that this could have been a sublime idea if there was no competition and a monopolistic moat would force customers to search on a single platform.

However, these two companies have minimal product differentiation and the risk of starting a pricing war to zero could be in the fold as shoppers will cherry-pick for the best deal depending on the platform since the products are the same.

Fast food outlets have faced this problem in the last few years as their products have been commoditized.

Prematurely rolling out this new strategy could emasculate these companies.

The time is ripe for an outsider with access to cheap capital to easily roll into town and play nice with the independent broker industry promising to protect future broker’s commission and not step onto their turf.

3rd party brokers would migrate towards this peaceful platform in an instant if they sensed cooperating with Redfin and Zillow hampered business, and it would be game over for Zillow and Redfin in a jiffy.

It would make sense for outliers like Homesnap, Neighborhood Scout, and Realtor.com to summon a batch of capital and surgically target the weakness left gaping open by Zillow and Redfin.

Naturally, investors voted with their wallets and each of these “transformational” moves was met by a cascade of torrential selling in the shares.

As interest rates trend higher, it will automatically ratchet up pressure on these marginal business models.

The coming potential lack of mortgage originations from fewer buying candidates and a slide in internet traffic disrupting ad revenue will quickly erode sales revenue growth.

Zillow is already buying houses from sellers in Denver, Atlanta, Las Vegas and Phoenix with their own capital.

If buyers dry up, Zillow will be on the hook for these houses saddled with a growing inventory of units with a return rate of zero while dealing with a high cost of carry.

All of this shouts lower growth and decelerating revenue.

Management has effectively offered shareholders a difficult path to profits beset by landmines that could potentially blow up a limb or two along the way.

If management stuck with the ad business, they could revisit this risky business at the start of the new cycle with the tailwind of low-interest rates and lower house prices.

Patience is a virtue, and nobody told Zillow’s and Redfin’s management.

That is exactly the type of tech company not to invest in even though Zillow’s 22% sales revenue growth is not bad.

I commend management for seeking fresh levers to stoke growth, but this was a badly calibrated commitment that will cast a pall over its operations for the next few years.

As predicted, these companies blew up its future guidance which is a sign of things to come.

Redfin reduced guidance for profits on the home selling unit by 80%.

Not only did they pull back guidance for the new division, but the core advertising unit was hit with a mild reset in guidance.

Elevated execution risk effectively moving forward to this back end of the economic cycle could turn out to be a genius move. But until management can prove this move could gain traction, investors need to abstain from taking risks with this potential catastrophe.

My bet is that this will end in tears.

Zillow is a far stronger company than Redfin with stronger revenue accumulation while boasting higher revenue growth. But when the industry fundamentals are dictating the weak price action, it’s a great time to sit on the sidelines.

Avoid Zillow and Redfin, the boat is sinking and unfortunately this time, the tide won’t raise all boats and say hello to margin capitulation while you’re at it.

Mad Hedge Technology Letter

June 19, 2018

Fiat Lux

Featured Trade:

(TRAVIS IS BACK!),

(UBER), (RDFN), (Z), (LEN), (CRM), (MSFT), (AAPL)

Travis Kalanick is back in full force after his Uber fiasco.

His creation kicked him to the curb preferring a more rigid approach to corporate governance as the 2019 IPO draws closer.

It didn't take much time for him to take stock of his piggy bank.

Yes, the $1.4 billion payout he received means he has nothing to do with Uber anymore.

Some piggy bank.

Travis intends to wield this wad aggressively using his new fund "10100" as his finance vehicle to pounce on hot, new tech names.

Travis doesn't know any other way, and investors should be alert to where he turns to find his new Uber and his new baby.

Future foes should understand Kalanick is one of the most feared disruptors on the face of the earth.

He co-founded Uber in 2009 growing it into the premier transportation platform.

The whirlwind few years launched him from a nobody to one of the premier tech names in Silicon Valley.

So, what's the deal?

What I can tell you is that house prices are about to get a whole lot pricier and there is nothing you can do about it.

Travis Kalanick's investment into house flipping app Opendoor will be the first stage of a torrential stampede of tech capital flowing into this sector.

More importantly, it's a sign of intent by Kalanick.

The real estate industry is the unequivocal prehistoric dinosaur that hasn't changed for decades.

It's almost a matter of time before the process of buying a house becomes digitized, either partially or fully.

Remember, Uber functions as a broker app matching drivers and passengers through a platform built on algorithmic software.

It would make logical sense for tech companies to attack the low-hanging fruit - meaning every industry that places brokers at the heart of business.

The broker app software is tried and tested with a gold stamp of approval. It works, and tech executives understand how to monetize the data.

Traditional brokers would get pummeled in this scenario, as the data applied to a new real estate broker app would eclipse anything a real human would be able to accomplish removing human error.

Real estate is next on disruption pecking order, and tech is coming for its bacon because of the huge sums of money associated with American real estate.

The real estate industry is not a scooter sharing business and requires boat loads of money to get ahead.

Tech has the cash but needs to figure out execution and its future road map.

The bulk of tech capital has been funneled into M&A that has seen tech companies pay multiples above what were guessed as fair value.

Share buybacks have been another hot source of investment.

Opendoor is a house-flipping firm intent on changing the status quo.

The business model entails snapping up distress properties, fixing them up, and selling them for a profit.

Opendoor receives a 6% commission for facilitating this whole process.

Opendoor has already served 20,000 customers saving more than 400,000 of prep time.

It is already on the hook for $1.5 billion in loans. SoftBank's vision fund is knocking on the door eager to become the next investor.

In 2016, this company was valued at $1 billion and after the latest round of financing giving Opendoor another $325 million, that number has crept up to $2 billion.

I have heard from solid sources that the SoftBank capital could be delivered in the next few months, likely paying another solid premium boosting tech valuations across the board.

Paying up has been a universal theme in 2018.

Microsoft's (MSFT) purchase of GitHub and Salesforce's (CRM) purchase of MuleSoft seem like overpaying but appear cheap in hindsight.

With the new cash ready to deploy, Opendoor seeks to expand to 50 cities by 2020, a swift upward jolt from its current 10 cities.

Not only will tier 1 cities feel the brunt of this new development, Opendoor plans to go into the lesser known cities and plans to double its staff from 650 to 1,300 in the upcoming year.

Kalanick caught onto this investment opportunity after one of his former Uber minions, Gautam Gupta, made the jump to Opendoor as COO and liaised CEO Eric Wu with Kalanick to hash out a deal.

It's nice to have friends in high places as Kalanick knows very well.

Even traditional home builders are getting in on the venture capitalist act.

Lennar was one of the investors in the latest round of Opendoor investment, underscoring the existential threat these traditional companies face.

It makes more sense to partner now and form a budding relationship than get utterly wiped out down the road.

Uber hopes to deploy this strategy with Waymo as Kalanick's former company knows it will never possess superior self-driving technology over Waymo.

The Lennar investment also gave Jon Jaffe, the COO of home builder Lennar, a seat on Opendoor's board.

Opendoor is the first serious tech foray into the housing business. It is initiating business on the periphery by focusing on fixer uppers.

This will allow Opendoor to cut its teeth and learn more about the industry before it migrates into higher margin business such as downtown condos that Millennials love.

A swift migration of other tech names will briskly follow into this undisrupted industry if Opendoor can pry open its floodgates.

Fixing up distressed houses is the gateway into brokering and the holy grail of constructing.

Tech could eventually wipe out everyone and control the whole process just like what investors have seen in the transportation industry.

I can imagine a future where tech companies will be the best firms to construct smart houses, which all houses will eventually become.

One massive aftereffect is that the average quality of housing will rise dramatically in all metropolitan areas.

Once the data amasses, Opendoor will be able to identify every property from where it can extract value allowing America to transform into a nation of pristine, smart houses.

Renovating a house and selling it will boost the prices of current houses.

Effectively, tech with gentrify housing creating higher quality but higher priced properties.

Millennials, who have had an awful time jumping on the property ladder, will have an even more difficult task finding a starter home if every starter house turns into a beautiful Tuscan-styled villa from a shabby shed.

Vice-versa, beautiful Tuscan-styled villas that cannot be "flipped" will become smart homes creating even more demand for IoT smart products and higher prices per square foot.

Andreessen Horowitz, a venture capitalist firm based in Menlo Park, California, has been one of the avant-garde tech investors seizing stakes in Twitter, Facebook, Skype, Coinbase, and Lyft.

And these were just some of its investments before 2014!

An industry where Travis Kalanick, SoftBank, and Andreesen Horowitz are piling in must have real estate agents shivering in their wake.

If the general trend keeps up, the Oracle of Omaha Warren Buffett could be next on this powerful list.

He usually likes to buy things he understands with healthy cash flow. I am sure he understands real estate more than Apple (AAPL), in which he had no problem investing.

Traditional home builders and real estate agents aren't the only players that could be left in the dust.

Zillow (Z), the online real estate database company, reacting from the Opendoor threat launched its new business to buy and sell homes.

It was only three years ago that Zillow CEO Spencer Rascoff determinedly hunkered down telling investors "we sell ads, not houses."

Innovation, tech disruption, and competition changes everything.

The stock sold off hard due to the exorbitant costs related to buying homes on the announcement of buying and selling houses.

Margins will get massacred in this scenario, but I applaud the decision to move up higher on the value chain diminishing the existential threat.

This whole industry is about to be flipped on its head, and the winners will be the most innovative companies that incorporate data best.

Rascoff further expanded saying, "I can say without exaggeration, that no company understands the American homebuyer and home seller better than Zillow Group."

Zillow is 12 years old and the12-year treasury trove of data will give it an optimal chance to pivot from selling ads to buying and selling houses.

Seattle-based Redfin (RDFN), Zillow's arch nemesis competitor founded in 2004, has an even larger treasure trove of data dating back 14-plus years and has moved in the same direction.

Redfin was anointed the top tech company to work for in Seattle in 2017 by Hired.com.

There is enormous potential to add another monstrous business to Redfin and Zillow's top line.

The real estate industry is next in line to be digitized, and the Mad Hedge Technology Letter will be the first to know when it's time to dip your toe in.

_________________________________________________________________________________________________

Quote of the Day

"As a tech entrepreneur, I try to push the limits. Pedal to the metal," - said former cofounder of Uber Travis Kalanick.