Mad Hedge Technology Letter

June 27, 2022

Fiat Lux

Featured Trade:

(NOTHING ZEN ABOUT ZENDESK)

(ZEN)

Mad Hedge Technology Letter

June 27, 2022

Fiat Lux

Featured Trade:

(NOTHING ZEN ABOUT ZENDESK)

(ZEN)

Zendesk (ZEN) bought out for $10.2 billion is good business.

This is after ZEN declined a $17 billion offer just 4 months ago which in hindsight looks highly illogical.

This event crystallizes the souring mood in growth technology that has seen a colossal re-rating of its assets during a cringe-worthy stock market sell-off.

These micro-events bode poorly for growth tech and expect desperation from the illiquid.

Remember that the quickest way to go out of business is to not have any money.

Interest rates skyrocketing has really harmed the ability of growth tech to pay interest on their corporate bonds or to even issue reasonable debt.

The attack on balance sheets is what everybody is scared of and rightly so.

The investor consortium buying the company includes Hellman & Friedman, Permira, a subsidiary of the Abu Dhabi Investment Authority, and Singapore’s GIC sovereign wealth fund. Subject to shareholder approval, the deal is likely to close in Q4 this year, after which time ZEN will operate as a private company.

ZEN isn’t all that bad of a company based on pre-pandemic metrics.

However, fast forward to today and the goalposts have switched

, and investors will look at the last 4 years of unprofitable growth as a liability even if gross revenue has been gaining at a nice clip.

Investors need standalone businesses now, not later, and the zombie company of old are receiving the cold shoulder.

Mikkel Svane, Founder and CEO of Zendesk, had hoped to persuade shareholders to buy into a planned $4.1 billion takeover of Momentive Global Inc, owners of the SurveyMonkey platform.

But this was rejected by shareholders following lobbying by a number of activist investors. Around the same time, the firm rejected an unsolicited takeover bid from an unnamed private equity firm, reportedly offering $17 billion.

Svane clearly needs to be offloaded for such a rookie move.

The reading of the tea leaves in the short term is positive for ZEN as a business model with 30% growth rates year-over-year still in play.

My synopsis is that the next solution will be what private equity usually does, gut the company of high costs including expensive workers and spin it out into a profitable enterprise.

Outsource to poor countries like Moldova, and cancel all in-person office facilities.

Then go back to the public markets to fetch a premium before it goes ex-growth and collects a nice profit.

ZEN’s customers with more than $250,000 Annual Recurring Revenue (ARR) make up 39% of the total, up from 34% last year, while customers with more than $1 million ARR were up 65% year-on-year.

The management and shareholder kerfuffle highlights the sensitive times we are in for unprotected tech companies which are essentially the non-Apple, Microsoft, and Google tech firms.

It’s been a whole economic cycle since public tech companies really had any type of stress, and the stress in 2022 is disguised from all directions.

Just look at Founder of Tesla Elon Musk whose Tesla shares are down almost by half from its 2021 peak and most people will understand that it will be harder to buy Twitter when Tesla shares are crashing.

Existing on public tech markets is just harder when the Nasdaq is in a bear market.

Unfortunately for some, the bear market doesn’t treat everybody the same, and now the goal is survival.

Sure, management wants to fight workers on working remotely too much, but in a tight labor market, they understand it’s a battle to fight another day or just outsource abroad.

Egos must be put aside and when a firm fails to accept an offer $7 billion higher than what they settle on, it’s embarrassing.

This must be characterized and recorded as an unmitigated failure.

For a tech firm that only has revenue of $350 million per year, $17 billion is a ridiculous sum to pay.

I value this software company at half of that - $8.5 billion and paying $10 billion for it in this climate is plausible.

The financing for the deal will be provided by Blackstone, almost guaranteeing this will be a thorough gut job and spin back to the public arena.

Gone is the day of overpaying for mediocre tech.

Mad Hedge Technology Letter

February 26, 2019

Fiat Lux

Featured Trade:

(WHY THE BIG PLAY IS IN SOFTWARE),

(AMZN), (WMT), (ZEN), (FB), (TWLO)

Buy and hold domestic software companies for dear life because that is what the market is giving you.

Take them with both hands.

These revenue models should revolve around developing the lucrative North American digital consumer markets.

Tech is all about giving you pockets of dispersion and my job to herd you into these pockets of opportunity created by pockets of dispersion.

We have once again been delivered a few more poignant indicators allowing us to gauge the market appetite for certain tech barometers.

Incandescent as can be, recent news of hardware companies planning to bring exorbitant foldable phones to market has me profusely shaking my head.

Huawei announced plans to debut the Mate X foldable 5G smartphone with a price tag of a staggering $2,600.

This followed an announcement by Korean behemoth Samsung to roll out the Samsung's Galaxy Fold and the Koreans plan to sell this luxury product for $1,980.

Chinese Huawei Mate X is 5G-supported and can simply fold into a slimmer 6.6-inch smartphone or unfold into an 8-inch tablet.

This is another case of smart manufacturers overreaching for a market that doesn’t exist and shouldn’t exist.

I believe the demand for screen-related smart products at this price point is scant at best.

If you compare foldable phones to a $600 high-tier Samsung Android smartphone with a 6-inch screen, Samsung and Huawei would need to convince consumers the extra $1,500 or in Samsung’s case, $2,200 is worth the extra relative wad of cash.

My bet is that these foldable phones aren’t worth even $300 more of aggregated incremental value let alone $500 and for many consumers like me, it’s worth zilch.

In no way, aside from the gimmick of buying one of these novelties, does buying a foldable phone justify the price.

This is another example of the common-sense factor that has been completely absent from a product cycle.

Product viability and product desirability do not walk hand in hand.

The screen-related smart device market is saturated, evident by the elongated refresh cycle in smartphone usership.

Blame the expensive price tags of over $1,000 and the removal of carrier subsidies that have caused the upgrade cycle to skyrocket from 2.39 years in 2016 to 2.83 years in late 2018.

Then there is the touchy issue of cannibalizing other hardware product lines as many of the potential foldable phone customers might interchange the foldable phone with normal smartphones.

This all screams bad strategy with companies saddled in a glut of inventory.

It takes R&D years to follow through and develop the technology to bring it to market, and it is entirely conceivable this could become a big write-off.

If price cuts happen shortly after the debut, prospects look bleak.

In general, consumer sentiment has soured for more of this type of tech. Many people are just exhausted from screen time and the cycle of the newest hardware screens is failing to excite existing customers bases.

The only conclusion I can make is that tech today is about software, software, and particularly domestic software.

If you compare software to hardware head to head now, software functionality is still increasing 15% YOY juicing up efficiency and productivity.

What will foldable phones offer a digital nomad or working professional?

Not much.

It highlights the absence of a productivity or functionality boost that digital device users are scouring for now.

Stay away from hardware.

Why is domestic software preferred over international software that scales the earth five times around?

Regulation.

It has reared its ugly head again.

The avalanche of negative headlines applied to American big tech is finally becoming a self-fulfilling prophecy.

It was only a matter of time until someone took note, and in this case, various Asian governments have taken note.

In a bid to blunt American tech’s first mover advantage, the Indian government has written up a draft of regulatory measures in order to make the Indian tech landscape a fairer playground.

This will have the intended effect of creating a national powerhouse of tech firms employing local people.

India has effectively taken a page out of China’s playbook using home-field advantage to nurture homegrown talent.

Large American tech companies have made India a playground of binge investments lately with Amazon (AMZN) shelling out $5 billion and Walmart (WMT) brazenly pouring $15 billion into e-commerce heartthrob Flipkart.

This is awful news for them.

They will have to adjust to India’s new-found zeal for digital regulation and a heavy restructuring of the business model could be in the cards in 2019 along with higher costs of running these businesses.

India has followed China in its footsteps demanding data to be localized meaning data centers won’t be able to run and store Indian data abroad.

American participants will have no other choice but to pony up the extra costs.

Readers might forget that India is the current battleground of global tech growth and Amazon will not have unfettered market access like they did breaking into Europe and dominating e-commerce from the start.

Amazon and Walmart can thank Facebook (FB) which has been the main culprit in bringing wave after monstrous wave of heavy criticism on a whole industry.

Facebook has effectively brought forward the regulatory storm that otherwise would have happened a few years later down the road.

In any case, this makes life harder for data-oriented companies who wish to navigate hazardous foreign tech climates.

Domestic angst against local tech has given the rubber stamp for full-on data government mandates abroad from India to Vietnam.

What does this all mean?

In 2019, data regulation could shrink expected growth levers while hardware companies are becoming even more desperate as these Hail Marys could quickly turn into liabilities.

I nailed software picks Zendesk (ZEN) and Twilio (TWLO) amongst others from a strong group of enterprise software stocks.

Twilio’s performance could potentially become my best pick of 2019, it’s on a straight line up even with all this clutter and chaos around the world.

Mad Hedge Technology Letter

February 19, 2019

Fiat Lux

Featured Trade:

(THE SAFE PLACE TO HIDE IN TECH),

(CSCO), (ORCL), (WDAY), (ZEN), (HUBS), (NOW), (PYPL), (VEEV), (TWLO)

Great quarter by Cisco (CSCO).

That was the first thought in my head when perusing their quarterly earnings.

It’s been hit or miss for tech companies lately and at the end of 2018, I stood up and told readers to double down on software companies and specifically enterprise software companies.

Well, Cisco has skin in this software game because corporations cultivating software need the best type of network infrastructure money can buy.

Cisco is the foundational hardware on what current high-end software is built on.

It is all rosy to have a spectacular roof design, but without a solid foundation, we have nothing more than a house of cards.

The great part about Cisco is that they are immune to the software battle taking place inside of industries because they do not build the enterprise software that is built on top of the Cisco infrastructure.

We have seen our fair share of software companies go sideways such as Oracle (ORCL) who have presided over a stale patchwork of database system software created last gen.

However, on the other side of the coin, my prediction of enterprise software companies leading tech has been spot on.

Zendesk (ZEN), HubSpot (HUBS), ServiceNow (NOW), Workday (WDAY), PayPal (PYPL), Salesforce (CRM), Veeva Systems (VEEV), and Twilio (TWLO) are software companies that I was incredibly bullish on as we turned the calendar year and they have not disappointed with nearly all of these names flirting with all-time highs.

All these software companies need Cisco.

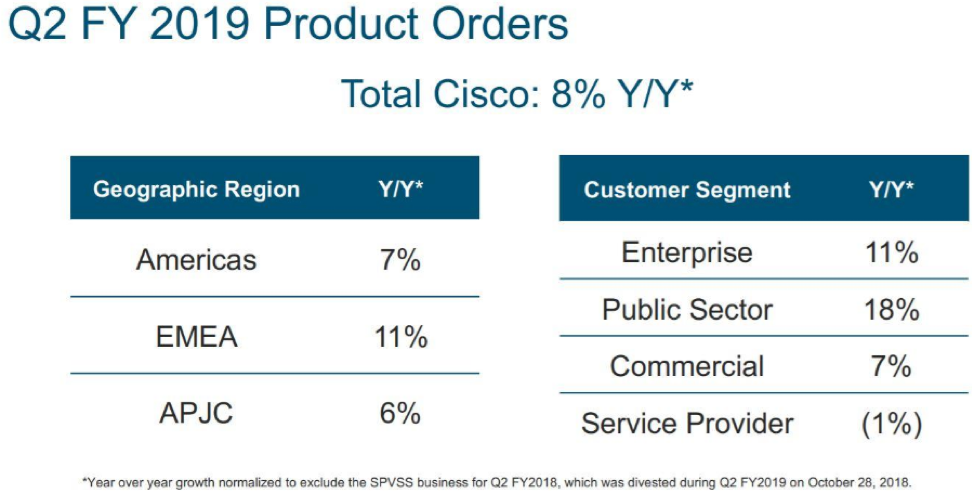

What stood out for me was that public sector orders grew 18% last quarter signaling that not only are the private corporations snapping up Cisco products, but governments are embedding their offices with Cisco’s Internet Protocol-based networking and other products related to the communications and information technology industry.

And if you wanted a general tech stock to capture the migration from analog commerce to digital and stay out of the high stakes online media segment, this would be the stable name that would check all the boxes.

And if you thought this was just a domestic story, once again, the scope is wider with Europe, the Middle East and Africa (EMEA) sales expanding by 11% which eclipsed America sales by 4%.

The only blip on the radar was service revenue slipping by 1% to $3.17 billion, but I do not view that as a pattern of sequential deceleration and pricing mechanisms can be altered to relaunch growth.

If you thought that Cisco doesn’t sell any software – you are wrong.

The software they do sell applies to operating the proprietary hardware that they produce.

Cisco’s wide competitive advantage stems from the industries toweringly high barriers of entry and that they make great products relative to other players.

The infrastructure software that liaises brilliantly with its hardware is succinctly named Cisco ONE Software.

This software suite is molded to face the most relevant use cases in the data center, WAN, and access edge.

CEO of Cisco Chuck Robbins characterized the current geopolitical and overall economic landscape as “complex” but experienced “zero difference” in Chinese revenue giving the company a quarterly victory in the Middle Kingdom.

China’s economy is decelerating faster than we can understand. The latest details of ride-hailing leader Didi sacking 2,000 employees is a warning flare to the rest that open wounds are appearing in the economy and are becoming harder to conceal.

And for Cisco to do a quarter with no significant Chinese downdraft is a good sign that the company can handle the upcoming recession in 2020.

As a sign of further strength, Cisco raised its dividend and boosted stock buybacks which are all the trappings of what great companies do.

Cisco already made $5 billion of repurchases last quarter which was on top of the $6 billion they bought in October 2018.

This method of financial engineering helps put a solid floor under the stock delighting investors and ignites the share price.

And the capital allocation encore means that Cisco will pile $15 billion into its buyback program with this fresh authorization, and the company is forecasted to produce at least $15 billion in free cash flow over the next year.

Cisco’s balance sheet is glistening and even has options to adventure into meaningful M&A if they see something that catches their eye without any real hit to the balance sheet.

These multiple tailwinds in a precarious economic point in the cycle have investors aware that there are worse options out there to invest capital than tech thoroughbred Cisco.

And if you thought the one variable that could turn this earnings report from good to bad was expenses and margins, well, Cisco covered their bases on that one too.

Margins came within the forecasted guidance with gross margins slightly trending down by 1% to 64.1%.

Expenses were reigned in and management saw a small nudge up of 3% causing investors to take a deep sigh of relief.

Cisco is in a superior strategic spot to most tech companies and is a staunch participant of the migration to digital.

Buy shares on the dip.

Mad Hedge Technology Letter

December 10, 2018

Fiat Lux

Featured Trade:

(IT’S ALL ABOUT THE CLOUD)

(OKTA), (ZS), (DOCU), (INTU)

If you thought software week at the Mad Hedge Technology Letter was over, you were absolutely wrong.

I have done my best to offer a barrage of cloud-based software stocks with monstrous upside potential that would put any other industry companies six feet under.

Silicon Valley software companies have access to quinine in a mosquito-infested market – digitally savvy talent.

This talent is the best and brightest the world has to offer, and they want to work for a dominant company that gets it.

Much of this involves companies with bright futures, career opportunities galore, solving deep-rooted problems, all applying a treasure trove of data and a mountain of capital your rich uncle would giggle at.

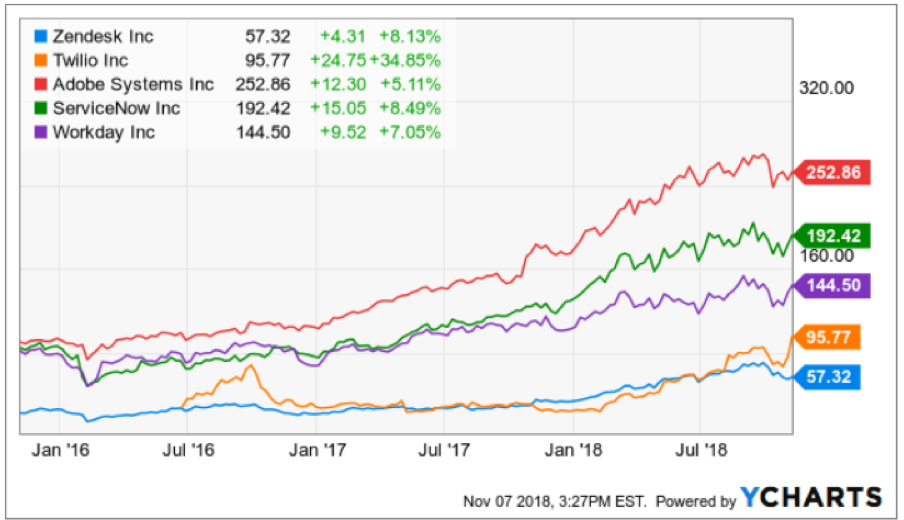

In the short term, I have been succinctly rewarded by my software picks with communication software Twilio (TWLO) rocketing upward 35% intraday at the time of this writing from when I recommended it just a few days ago.

Another Mad Hedge Technology Letter recommendation Zendesk (ZEN), a software company solving customer support tickets across various channels, is up a tame 10% after the election.

All in all, I would desire readers to access due caution as the volatility can bite you badly with crappy entry points, but the upside cannot be denied.

The turbocharged price action means the pivot to software with its new best friend, the software as a service (SaaS) pricing model, encapsulates the outsized profits this industry will rake in going forward.

Without further ado, I’d like to slip in two more companies rounding out a robust quintet of software companies – I bring to you Workday (WDAY) and Service Now (NOW).

Workday is a software company based on a critical component of every successful company – human resources.

Unsurprisingly, human resources are tardy to this wave of software modernization.

Sensibly, companies have chosen short-term software fixes that drive profits with instant success rather than to update its human resource department’s processes.

Big mistake.

I would argue that getting the right people in the doors is paramount and can save substantial time because of the wasted time rooting out toxic employees who weren’t suitable fits.

Ultimately, I have concluded the worst-case scenario entails the enterprise resource planning market stagnating driving minimal growth to the cloud, however, this minimal growth would be substantial enough for Workday to outperform.

The landscape as of now only involves several vendors with a competitive (SaaS) solution auguring well for Workday allowing them to capture a further chunk of market share.

Workday’s growth metrics back up my thesis with its businesses posting a 3-year EPS growth rate of 291% and a 3-year sales growth rate of 36%, painting a picture of a company that will turn profitable in the next few years.

They can even showboat their glittering array of heavy-hitting customers who purchase their software that include Walmart (WMT), Target (TGT), and Bank of America (BAC).

The one headwind tarnishing these types of software companies is the stock-based compensation awarded to employees.

SBC rose 21% YOY and is slightly worrying in an otherwise stellar company. This method of compensation only works when the stock is rising and is a major issue for new Facebook (FB) hires who will prefer cash over its burnt-out share price.

If Workday doesn’t whet your appetite, then how about sampling a main dish of ServiceNow.

This company completes technology service management tasks offering a centralized service catalog for workers to request technology services or information about applications and processes that are being used in the system.

Admirably, this software helps IT workers fix IT system problems which in this day and age is useful considering the bottleneck of chaos many tech and non-tech companies face.

And more often than not, the chaos inundates the in-house IT departments causing the whole business to go offline.

Putting out digital fires is a perpetual business that will never flame out.

As websites and enterprise systems become more complicated, a bombardment of errors are prone to crop up and instant remedies are crucial to carrying out businesses in a time sensitive manner.

Even ask the best tech company in the universe Amazon (AMZN), whose move off Oracle’s (ORCL) database software was the ultimate reason for a serious outage in one of its biggest warehouses on this past Amazon Prime Day, according to Amazon’s internal documents.

The faux paux underscores the hurdles Amazon and other companies could face as they seek to move completely off the Oracle legacy database software whose development has stayed relatively stagnant for a generation.

The slipup was minutes and snowballed into excruciating hours on Amazon Prime Day resulting in over 15,000 delayed packages and roughly $90,000 in wasted labor costs.

Crikey!

These numbers didn’t even consider the wasted man-hours spent by developers troubleshooting and solving the errors or any potential lost sales.

When these mammoth tech giants are running at an incredible scale, a small blip can result in job losses, lost revenue, lost time, a slew of IT engineer sackings, and for some smaller companies, an existential crisis.

The large-scale acts as a powerful multiplier to the lost resources and cost, and as you can see with the Amazon debacle, a few hours can make or break a developer’s career.

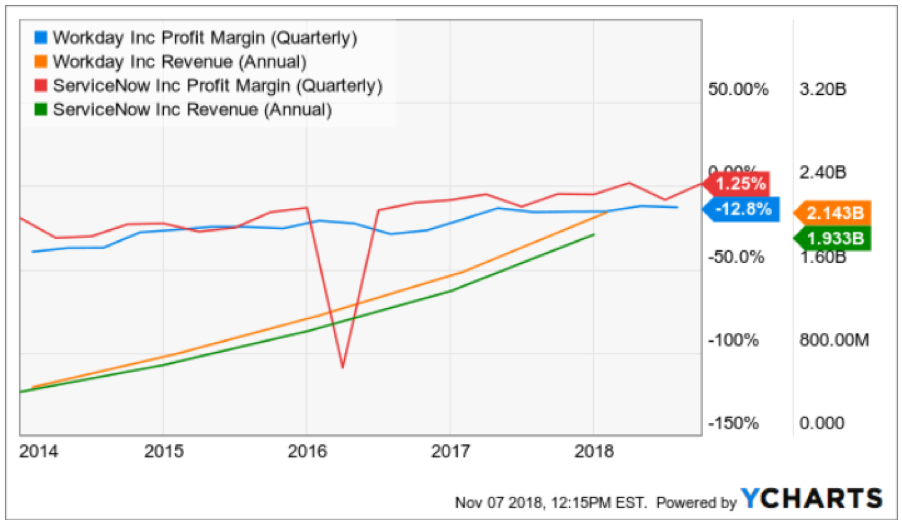

Fortunately, IT budgets are higher up the food chain than human resource budgets while more than inching up every year. This is the main reason why I believe ServiceNow will outperform Workday.

The proof is in the pudding and when I scrutinize various metrics, the truth is filtered out.

ServiceNow’s quarterly growth rate is 35% which is higher than Workday’s who slipped back to 28% last quarter even though the 3-year growth rate is in the mid-30%.

Put mildly, accelerating sales growth is better than decelerating sales growth.

Both companies have a market cap in the low $30 billion and almost identical annual sales in the $2 billion range.

However, ServiceNow presides over significantly higher quarterly profit margins than Workday and will achieve profitability sooner than Workday.

In short, Workday loses more money than ServiceNow.

I believe in the underlying thesis of HR modernization underpinning Workday’s rapidly growing revenue and this secular trend is here to stay.

But I much rather put my hard-earned money on a company tied to IT modernization which is imminent and harder to put on the backburner because of its strategic position at the forefront of the tech curve.

HR CAN be put on the backburner and kept analog longer, and as the economy inches closer to a recession, this expense will be shifted further away from greener pastures supported by the fact that companies decelerate hiring new talent in poor economic environments.

To wrap it up, I do believe ServiceNow is the Burmese python consuming a cow, but that doesn’t mean I am bearish on Workday.

Workday will flourish, just not as much on a relative basis as ServiceNow.

Effectively, these stocks are well placed to move higher even after the violent moves upward this year. As the economic cycle moves further into the late innings, the importance of cloud-based software companies will become magnified further.

As for the software week at the Mad Hedge Technology letter, these solid five picks will offer deep insight into one of the most compelling parts of the internet sector.

As many observers have found out, not all tech firms are created equal and that is made even trickier with the existence of the vaunted FANGs who are the real Burmese python in the current tech landscape.

Mad Hedge Technology Letter

November 7, 2018

Fiat Lux

Featured Trade:

(THE RELIABILITY OF ADOBE)

(ADBE), (GOOGL), (ZEN), (TWLO), (SQ)

Tech companies have a habit of suddenly coming and going because of the nature of the relentless environment that spits out losers and celebrates winners.

It’s hard-pressed to find software companies that pass the test of time but there is one that is healthily chugging along that most people know quite well.

Adobe (ADBE) was established 35 years ago in co-founder John Warnock's garage.

This legacy software company’s name, Adobe, was named after the Adobe Creek in Los Altos, California, which ran behind Warnock's house.

Adobe cut its teeth in an era when tech CEOs were not larger-than-life cult figures, and all Adobe has done is quietly infiltrating its way into everybody’s devices by way of Adobe Flash Player and its smorgasbord of useful software applications.

Adobe acquired Macromedia in 2005 which was responsible for building Adobe Flash Player.

This Macromedia software has been developed and distributed by Adobe Systems ever since the purchase and its functions involve viewing multimedia contents, executing rich internet applications, and streaming audio and video. Flash Player can run from a web browser as a browser plug-in or on supported mobile devices.

Flash player was its second hit success software program after its Adobe Acrobat and Reader software introduced PDF, the Portable Document Format, which is still ubiquitously used today even after all these years.

Most software companies are relatively new to the scene and like companies I have recently written about such as Zendesk (ZEN) and Twilio (TWLO), they can brag about growing sales of 30% or 40% plus per year.

Adobe isn’t too shabby itself growing sales at over 24% annually – remarkably high for such an ancient tech company.

The company’s strengths are similar to that of Apple (AAPL) – high-quality products and high profitability.

There will be no back-to-back doubling of the stock like some hyper-growth tech stocks because Adobe doesn’t subscribe to the type of growth trail that Square (SQ) has blazed.

What you can expect from Adobe is a slow grind up in share price stoked by its outperforming EPS expansion and acceptable sales growth of mid-20%.

Its annual operating margins have essentially tripled since the beginning of 2015 from around 10% and now boasts an Apple-like 30%.

There are no bones about it – Adobe has high-quality software across its diversified portfolio.

Other Adobe software products universally soaked up are its stable array of graphic design software such as Adobe Photoshop and Adobe Dreamweaver.

Adobe has also ventured into video editing, animation, and visual effects with Adobe Premiere Pro.

Not only that, Adobe has forayed into more conventional types of software such as digital marketing management software and server software.

Simply put, Adobe’s assortment of digital media software products has a religious-like following especially for iOS users.

As you might have guessed correctly, the lion’s share of Adobe’s revenue stream stems from its software as a service (SaaS) segment contributing 80% to the top line.

More narrowly, the digital media segment makes up almost 70% of the subscription-based revenue. This division will expand at least 20% each year boding well for Adobe to maintain its 20% plus sales growth that any legacy software company would sacrifice a right leg to achieve.

It’s digital marketing software products rub up against stifling competition in Alphabet (GOOGL) amongst others and contribute a less robust 30% to overall sales.

I am less bullish on this part of the business because they have it rough competing against one of the Fangs, the path of less resistance clearly sides with its bread and butter of the digital media offerings.

Its subscription-based pricing model was the catalyst for boosting profitability causing the stock to experience massive price gains. The stock has doubled in the past two years which is unheard of for most legacy software companies.

No longer does Adobe need to manufacture the ancient CD of yore physically delivering it to customers, users can briskly download these products directly from the official website, receive constant upgrades over broadband internet, and pay Adobe monthly for their humble services.

In fact, any investors looking for some hot software stocks only need to find companies that recently shifted to a subscription-based pricing model. It’s pretty much a license to print money if the software quality can backup the monthly costs for the user.

I can tell you that Adobe’s software has remained world class, embedded at the heart of most digital devices at home and in the office, and who would have thought that just a little shift to the pricing model would have doubled the stock price?

Well, instead of one-off sales, Adobe can book revenue month after month, and year after year demonstrating the supercharged effect of shifting to a recurring revenue stream model.

Highlighting the pivot to profitability is Adobe’s three-year EPS growth rate of 48% turning this company into a mammoth software company with a $117 billion market cap.

Another positive for Adobe’s future sales are its fertile addressable markets in Europe and Asia.

There is ample room to expand in these geographical regions with Europe already chipping in with almost $2 billion of revenue per year and Asia with another $1 billion.

Future harvests look even more bountiful.

These two regions make up almost 40% of sales and as the Asian middle class is poised to elevate a giant swath of its people to middle class, Adobe will be a handsome beneficiary of this trend as middle-class families tend to pump out more university graduates who migrate to software-based occupations.

Even though Adobe isn’t the sexiest name out there, it certainly is in the category of “safe.”

In no way do I see an eradication of its embedded software spread widely throughout the tech universe.

Its digital media software tools are best-in-show and loyally followed with a long-lasting revenue stream that has room to grow abroad.

Do not expect Adobe to debut any earth-shattering products, but I fully anticipate Adobe to become even more profitable to the point that they might offer a dividend or reallocate capital to shareholders through stock buybacks.

Apple has similar strengths in its business model, albeit on a much grander scale.

I feel that Adobe doesn’t get the credit it deserves because of its steady as it goes drivers that keep motoring higher in an industry that adores groundbreaking products that revolutionize the world.

I would wait for a major sell-off because a double in two years has bid up the stock to expensive levels represented in its premium forward PE multiple of 35.

However, as the conclusion of the mid-term elections offers some certainty to the market, tech stocks could get swept up in a positive rush to round out the year.

Luckily for Mad Hedge Tech readers, this is the golden age for software companies and we are just scratching the surface of the capability software efficiencies can deliver to small and large companies across every bit of the economy.

Another Apple-like similarity is that Adobe is annually voted one of the best places to work according to Fortune, stacked up against companies represented across the full economic spectrum and not just tech.

If you have a kid, tell him to find a job in San Jose, he or she could find worse places to cut a paycheck.