It’s official: Absolutely no one is confident in their long-term economic forecasts right now. I heard it from none other than the chairman of the Federal Reserve himself. The investment rule book has been run through the shredder.

It has in fact been deleted.

That explains a lot about how markets have been trading this year. It looks like it is going to be a reversion to the mean year. Forecasters, strategists, and gurus alike are rapidly paring down their stock performance targets for 2025 to zero.

When someone calls the fire department, it’s safe to assume that there is a fire out there somewhere. That’s what Fed governor Jay Powell did last week. It raises the question of what Jay Powell really knows that we don’t. Given the opportunity, markets will always assume the worst, that there’s not only a fire, but a major conflagration about to engulf us all. Jay Powell’s judicious comments last week certainly had the flavor of a president breathing down the back of his neck.

It's interesting that a government that ran on deficit reduction pressured the Fed to end quantitative tightening. That’s easing the money supply through the back door.

For those unfamiliar with the ins and outs of monetary policy, let me explain to you how this works.

Since the 2008 financial crisis, the Fed bought $9.1 trillion worth of debt securities from the US Treasury, a policy known as “quantitative easing”. This lowers interest rates and helps stimulate the economy when it needs it the most. “Quantitative easing” continued for 15 years through the 2020 pandemic, reaching a peak of $9.1 trillion by 2022. For beginners who want to know more about “quantitative easing” in simple terms,please watch this very funny video.

The problem is that an astronomically high Fed balance sheet like the one we have now is bad for the economy in the long term. They create bubbles in financial assets, inflation, and malinvestment in risky things like cryptocurrencies. That’s why the Fed has been trying to whittle down its enormous balance sheet since 2022.

By letting ten-year Treasury bonds it holds expire instead of rolling them over with new issues, the Fed is effectively shrinking the money supply. This is how the Fed has managed to reduce its balance sheet from $9.1 trillion three years ago to $6.7 trillion today and to near zero eventually. This is known as “quantitative tightening.” At its peak a year ago, the Fed was executing $120 billion a month quantitative tightening.

By cutting quantitative tightening, from $25 billion a month to only $5 billion a month, or effectively zero, the Fed has suddenly started supporting asset prices like stocks and increasing inflation. At least that is how the markets took it to mean by rallying last week.

Why did the Fed do this?

To head off a coming recession. Oops, there’s that politically incorrect “R” word again! This isn’t me smoking California’s largest export. Powell later provided the forecasts that back up this analysis. The Fed expects GDP growth to drop from 2.8% to 1.7% and inflation to rise from 2.5% to 2.8% by the end of this year. That’s called deflation. Private sector forecasts are much worse.

Just to be ultra clear here, the Fed is currently engaging in neither “quantitative easing nor “quantitative tightening,” it is only giving press conferences.

Bottom line: Keep selling stock rallies and buying bonds and gold on dips.

Another discussion you will hear a lot about is the debate over hard data versus soft data.

I’ll skip all the jokes about senior citizens and cut to the chase. Soft data are opinion polls, which are notoriously unreliable, fickle, and can flip back and forth between positive and negative. A good example is the University of Michigan Consumer Confidence, which last week posted its sharpest drop in its history. Consumers are panicking. The problem is that this is the first data series we get and is the only thing we forecasters can hang our hats on.

Hard data are actual reported numbers after the fact, like GDP growth, Unemployment Rates, and Consumer Price Indexes. The problem with hard data is that they can lag one to three months, and sometimes a whole year. This is why by the time a recession is confirmed by the hard data, it is usually over. Hard data often follows soft data, but not always, which is why both investors and politicians in Washington DC are freaking out now.

Bottom line: Keep selling stock rallies and buying bonds and gold (GLD) on dips.

A question I am getting a lot these days is what to buy at the next market bottom, whether that takes place in 2025 or 2026. It’s very simple. You dance with the guy who brought you to the dance. Those are:

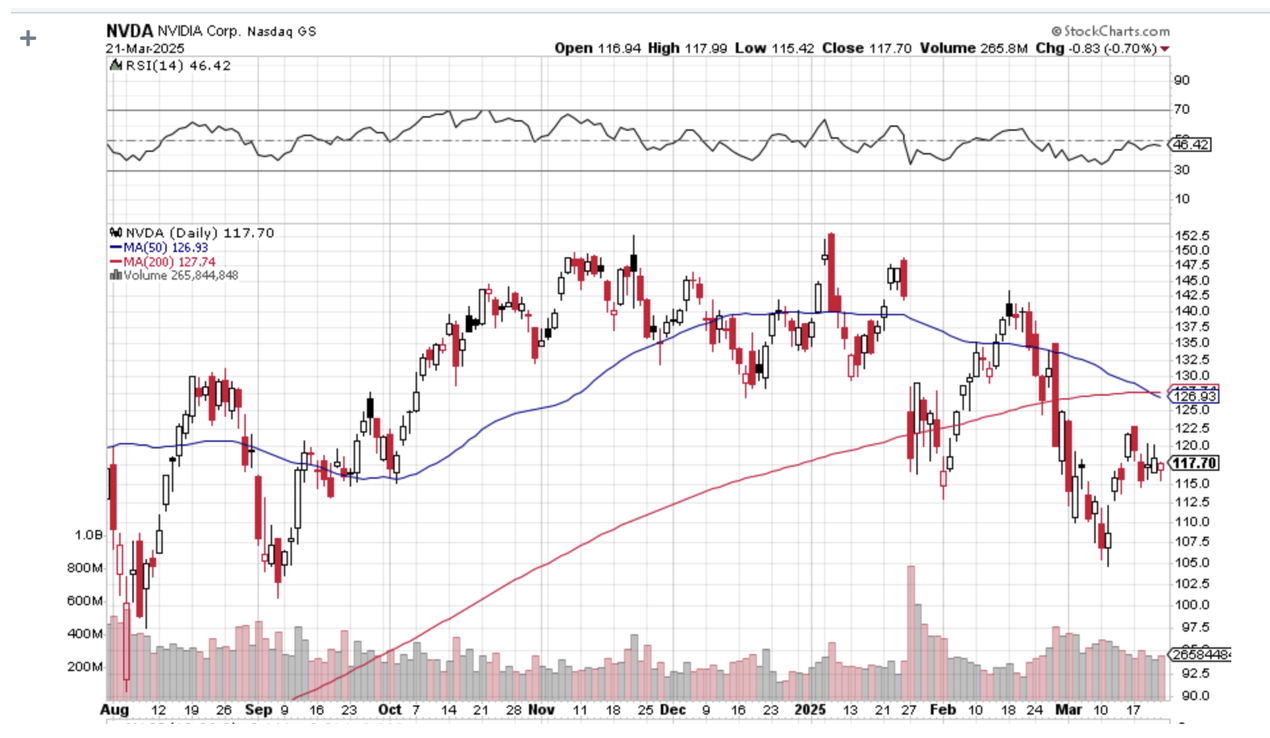

Best Quality Big Tech: (NVDA), (GOOGL), (AAPL), (META), (AMZN)

Big tech is justified by Nvidia CEO Jensen Huang’s comment last week that there will be $1 trillion in Artificial Intelligence capital spending by the end of 2028. While we argue over trade wars, AI technology and earnings are accelerating.

Cybersecurity: (PANW), (ZS), (CYBR), (FTNT)

Never goes out of style, never sees customers cut spending, and is growing as fast as AI.

Best Retailer: (COST)

Costco is a permanent earnings compounder. You should have at least one of those.

Best Big Pharma: (AMGN), (ABBV), (BMY)

Big pharma acts as a safety play, is cheap, and acts as a hedge for the three sectors above.

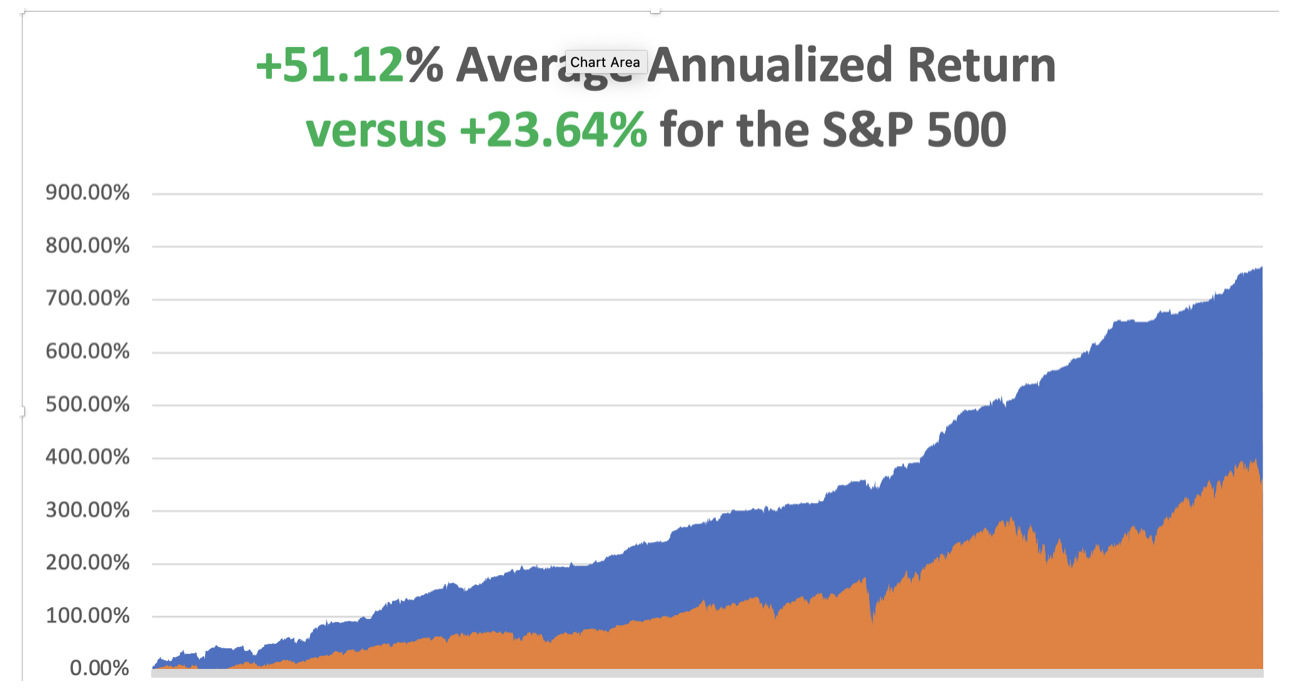

March is now up +2.92% so far. That takes us to a year-to-date profit of +12.29% in 2025. That means Mad Hedge has been operating as a perfect -1X short S&P 500 ETF since the February top. My trailing one-year return stands at a spectacular +82.50%. That takes my average annualized return to +51.12%and my performance since inception to +764.28%.

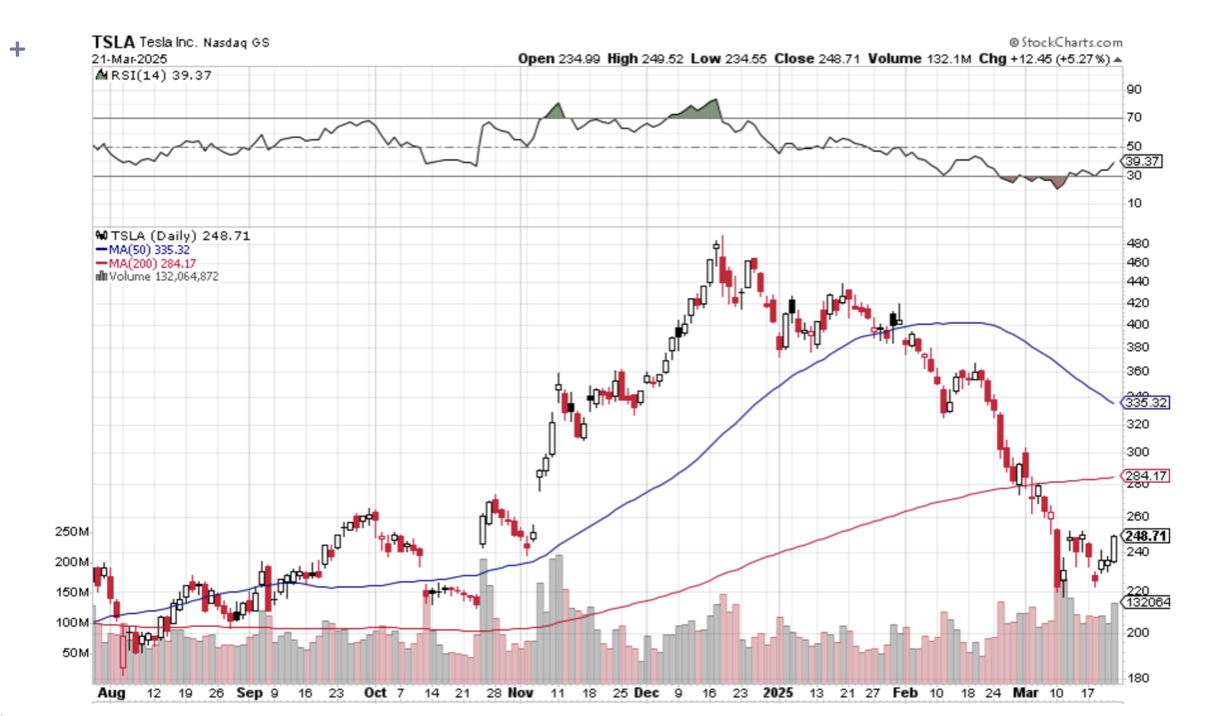

It has been another busy week for trading. I had four March positions expire at their maximum profit points on the Friday options expiration, shorts in (GM), and longs in (GLD), (SH), and (NVDA). I added new longs in (TSLA) and (NVDA). This is in addition to my existing longs in the (TLT) and shorts in (TSLA), (NVDA), and (GM).

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 74 of 94 trades have been profitable in 2024, and several of those losses were really break-even. That is a success rate of +78.72%.

UCLA Andersen School of Business announced a “Recession Watch,” the first ever issued. UCLA, which has been issuing forecasts since 1952, said the administration’s tariff and immigration policies and plans to reduce the federal workforce could combine to cause the economy to contract. Recessions occur when multiple sectors of the economy contract at the same time.

Retail Sales Fade, with consumers battening down the hatches for the approaching economic storm. Retail sales rose by less than forecast in February and the prior month was revised down to mark the biggest drop since July 2021.

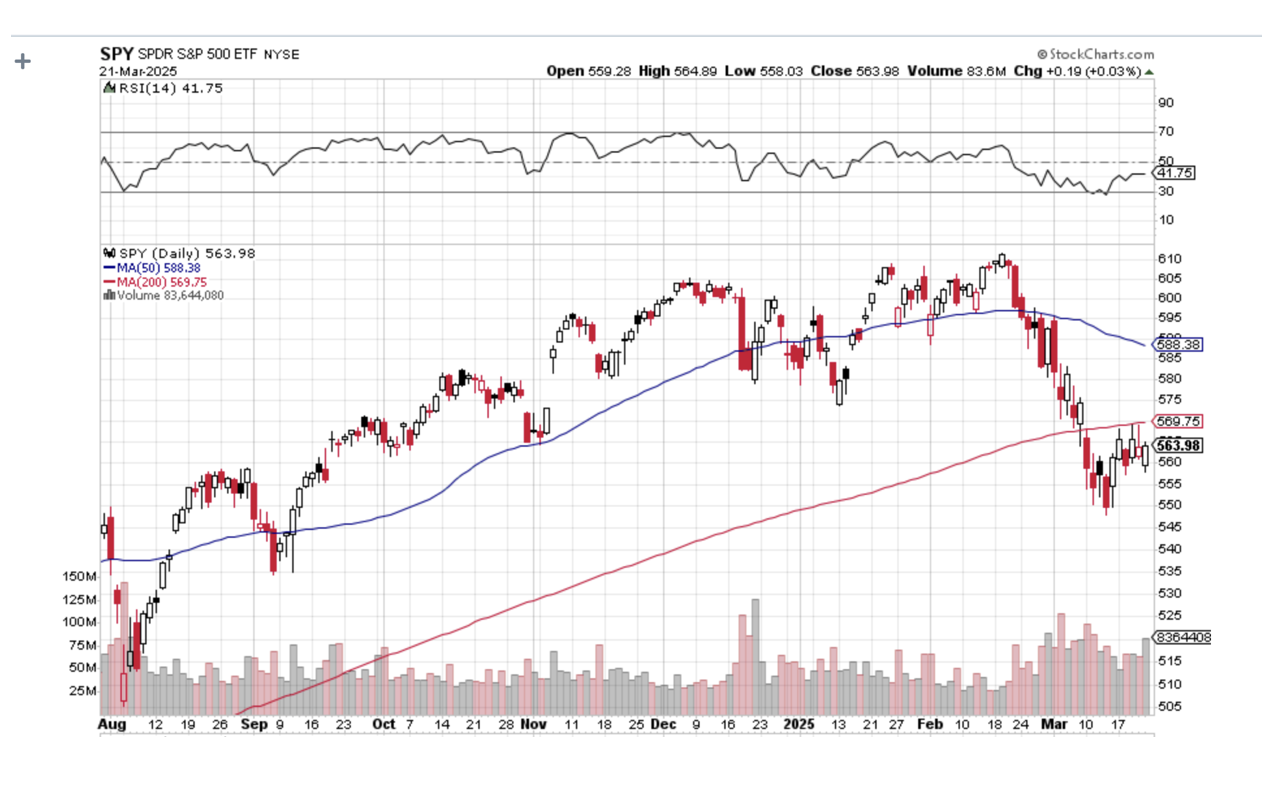

This Has Been One of the Most Rapid Corrections in History, leaving no time to readjust portfolios and put on short positions.

The rapid descent in the S&P 500 is unusual, given that it was accomplished in just 22 calendar days, far shorter than the average of 80 days in 38 other examples of declines of 10% or more going back to World War II.

Home Builder Sentiment Craters to a seven-month low in March as tariffs on imported materials raised construction costs, a survey showed on Monday. The National Association of Home Builders/Wells Fargo Housing Market Index dropped three points to 39 this month, the lowest level since August 2024. Economists polled by Reuters had forecast the index at 42, well below the boom/bust level of 50.

BYD Motors (BYDDF) Shares Rocket, up 72% this year, on news of technology that it claims can charge electric vehicles almost as quickly as it takes to fill a gasoline car. BYD on Monday unveiled a new “Super e-Platform” technology, which it says will be capable of peak charging speeds of 1,000 kilowatts/hr. The EV giant and Tesla rival say this will allow cars that use the technology to achieve 400 kilometers (roughly 249 miles) of range with just 5 minutes of charging. Buy BYD on dips. It’s going up faster than Tesla is going down.

Weekly Jobless Claims Rise 2,000, to 223,000. The number of Americans filing new applications for unemployment benefits increased slightly last week, suggesting the labor market remained stable in March, though the outlook is darkening amid rising trade tensions and deep cuts in government spending.

Copper Hits New All-Time High, at $5.02 a pound. The red metal has outperformed gold by 25% to 15% YTD. It’s now a global economic recovery that is doing this, but flight to safety. Chinese savers are stockpiling copper ingots and storing them at home distrusting their own banks, currency, and government. I have been a long-term copper bull for years as you well know. New copper tariffs are also pushing prices up. Buy (FCX) on dips, the world’s largest producer of element 29 on the Periodic Table.

Boeing (BA) Beats Lockheed for Next Gen Fighter Contract for the F-47, beating out rival Lockheed Martin (LMT) for the multibillion-dollar program. Unusually, Trump announced the decision Friday morning at the White House alongside Defense Secretary Pete Hegseth. Boeing shares rose 5.7% while Lockheed erased earlier gains to fall 6.8%. The deal raises more questions than answers, in the wake of (BA) stranding astronauts in space, their 737 MAX crashes, and a new Air Force One that is years late. Was politics involved? You have to ask this question about every deal from now on.

Carnival Cruise Lines (CCL) Raises Forecasts, on burgeoning demand from vacationers, including me. The company’s published cruises are now 80% booked. Cruise lines continue to hammer away at the value travel proposition they are offering. However, the threat of heavy port taxes from the administration looms over the sector.

My Ten-Year View – A Reassessment

We have to substantially downsize our expectations of equity returns in view of the election outcome. My new American Golden Age, or the next Roaring Twenties is now looking at multiple gale-force headwinds. The economy will completely stop decarbonizing. Technology innovation will slow. Trade wars will exact a high price. Inflation will return. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old. My Dow 240,000 target has been pushed back to 2035.

On Monday, March 24, at 8:30 AM EST, the S&P Global Flash PMI is announced.

On Tuesday, March 25, at 8:30 AM, the S&P Case Shiller National Home Price Index isreleased.

On Wednesday, March 26, at 1:00 PM, the Durable Goods are published.

On Thursday, March 27, at 8:30 AM, the Weekly Jobless Claims are disclosed. We also get the final report for Q1 GDP.

On Friday, March 28, the Core PCE is released, and important inflation indicator. At 2:00 PM, the Baker Hughes Rig Count is printed.

As for me, I received calls from six readers last week saying I remind them of Ernest Hemingway. This, no doubt, was the result of Ken Burns’ excellent documentary about the Nobel Prize-winning writer on PBS last week.

It is no accident.

My grandfather drove for the Italian Red Cross on the Alpine front during WWI, where Hemingway got his start, so we had a connection right there.

Since I read Hemingway’s books in my mid-teens I decided I wanted to be him and became a war correspondent. In those days, you traveled by ship a lot, leaving ample time to finish off his complete work.

I visited his homes in Key West, Cuba, and Ketchum Idaho.

I used to stay in the Hemingway Suite at the Ritz Hotel on Place Vendome in Paris where he lived during WWII. I had drinks at the Hemingway Bar downstairs where war correspondent Ernest shot a German colonel in the face at point-blank range. I still have the ashtrays.

Harry’s Bar in Venice, a Hemingway favorite, was a regular stopping-off point for me. I have those ashtrays too.

I even dated his granddaughter from his first wife, Hadley, the movie star Mariel Hemingway, before she got married, and when she was also being pursued by Robert de Niro and Woody Allen. Some genes skip generations and she was a dead ringer for her grandfather. She was the only Playboy centerfold I ever went out with. We still keep in touch.

So, I’ll spend the weekend watching Farewell to Arms….again, after I finish my writing.

Oh, and if you visit the Ritz Hotel today, you’ll find the ashtrays are now glued to the tables.

As for last summer, I stayed in the Hemingway Suite at the Hotel Post in Cortina d’Ampezzo Italy where he stayed in the late 1940’s to finish a book. Maybe some inspiration will run off on me.

Hemingway’s Living Room in Cuba, Untouched Since 1960

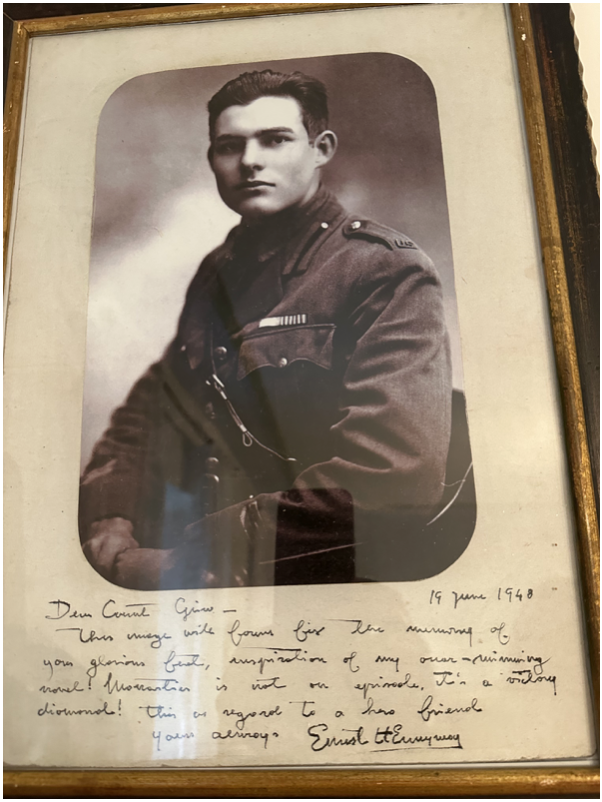

Earnest in 1918

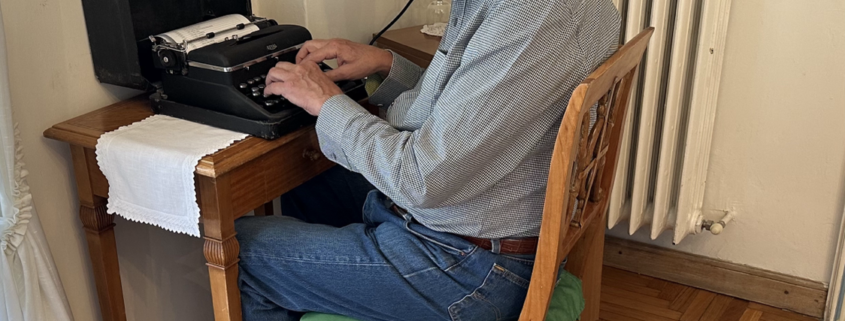

Typing at Hemingway’s Typewriter in Italy from the 1940’s

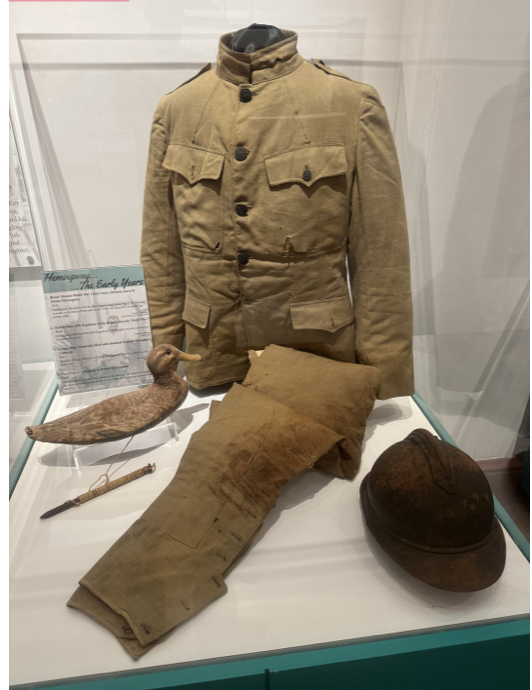

The Red Cross Uniform Hemingway Wore when He was Blown Up in 1917

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2024/01/John-thomas-typewriter.png11861124april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2025-03-24 09:02:532025-03-24 13:19:15The Market Outlook for the Week Ahead, or The Special No Confidence Issue

Below please find subscribers’ Q&A for the March 19 Mad Hedge Fund Trader Global Strategy Webinar, broadcast from Incline Village, NV.

Q: I tried to get into ProShares Short S&P500 (SH), it seems pretty illiquid. How did you get in?

A: Well, before I actually sent out the trade alert, I tested the liquidity of the SH seeing if you could get anything done. This is an easy thing to buy on up days in the market when others are taking profits. It is a really difficult thing to get into on down days in the market because you have so many long-only mutual funds trying to hedge their exposure through buying the (SH). We literally had just one up day at the beginning of the month, and I was able to increase my position tenfold and had no trouble getting my price on the LEAPS at $0.50. If you waited one day, you would have had to pay $0.60 for the same position, and that’s because the volatility explodes on this thing. If you look at the charts, the 1x short play has actually delivered enormous returns, as well as the 2x. It’s outperforming 2 to 1. So you have to buy when other people are selling, that’s the only way to get in and out of the (SH). Of course, I’m buying these things with the intention of running these to expiration.

Q: Is it time to sell US stocks?

A: Yes but only on the up days like today. Don’t sell into a pit, don’t sell into bottoms—wait for rally days like today. That's a good place to reduce risk and add some short positions like the ProShares Short S&P500 (SH) and the ProShares UltraShort S&P500 (SDS).

Q: How did you miss the rotation to Europe and China in emerging markets?

A: Very simple—if you ignore something for 15 years, it’s easy to miss a turn. I also missed the turn in Japan, which I ignored for 35 years. The real reason though is that I underestimated the extremity of this government, its economic policies, and the chaos it would create. I think almost everyone underestimated what the new government would actually do and how it would affect the stock market. If I knew ahead of time that the government would adopt recessionary policies, I would have done everything to get my money out of the US and into Europe and China, but this kind of unfolded with a shock a day, sometimes a shock an hour, and markets don’t like shocks and surprises, so they sold off. The more a stock had gone up in the last six months, the more it went down when the new government came into office.

Q: What are your downside targets for the market?

A: Now that we are in recession, I think any 5% rally off the recent low at 5500, you want to sell. The market could rally 3-5% off the bottom—that would be half of the recent loss. Then you’d want to get rid of more longs, cut your portfolio down to a few very high-quality positions, and add downside protection by buying the ProShares Short S&P500 (SH), the ProShares UltraShort S&P500 (SDS), doing buy rights on the calls and buying outright puts. That would be my recommendation. Eventually I see the S&P 500 falling to 5,000 by the summer, and if I’m wrong, it’s going down 30% to 4,500. That is a deep recession scenario, which we are on the track for unless the government suddenly reverses its draconian policies. This is the most extreme government in American history.

Q: Are you going to use the selloff to get into Costco (COST) after a 20% selloff?

A: Absolutely. I’ve been trying to get into Costco for years and it’s just always been too expensive. They keep increasing earnings every year —investors are willing to pay very high multiples for that. This time around, I am going to get into Costco because they are an absolutely outstanding company. By the way, my mentor at Morgan Stanley was a guy named Barton Biggs, who created the asset management division some 40 years ago. He was close friends with Sam Walton, the founder of Walmart, and Sam Walton was a huge admirer of Costco, which was just starting up then. I’m surprised they never took over the company, which is too big to take over now.

Q: What to buy at the bottom?

A: You want to buy what was leading right before we went into this collapse. Those are financials, and the highest quality profit making of the Mag7 which include Nvidia (NVDA), Amazon (AMZN), Alphabet (GOOGL), Meta (META), as well as cybersecurity stocks like Palo Alto Networks (PANW), Fortinet (FTNT), Zscaler (ZS) and so on.

Q: Why are you making your recession call when we have no evidence of that fact?

A: If you wait for proof of recession, that often is the market bottom. And that could be August of this year. You know, I talk to hundreds of businessmen around the world, and everyone is saying business is slowing. Companies stop making decisions. Customers stop buying. Everyone's afraid of the tariffs. Nobody knows what's going to happen next. Business confidence is terrible. That adds up to a recession, but data tends to move very slowly, so we won't see it in the data for months. If you're a stock trader, you don't have the luxury of waiting for confirmation of the data. By the time you get it, the move is over. But if you cut half of government spending or 12% of GDP, the recession outcome is guaranteed. It's not a speculation. That is the government's goal: to cause a recession, so they can have a recovery going into the next election to take credit for.

Q: If Alphabet (GOOGL) is broken up, what will happen to the company?

A: With all of these big tech breakups, the parts will be worth a lot more than the whole. The individual pieces can be sold off at much bigger premiums creating new companies with more stock liquidity. This is what happened with AT&T (T) in 1982. I participated in that, and the parts were worth more than the original AT&T was within two years. I expect that to happen to Alphabet, and I expect that to happen if Amazon (AMZN) is broken up— eventually, these companies become so big, they become too big to manage. And if the management sees they can get 100% premium on a spinoff, they'll take it so fast it makes your head spin.

Q: None of the 90% gain in stock prices during the Biden administration was a result of his policies.

A: That's absolutely correct. He stayed out of the way, which is the best thing that governments can do—get the hell out of the way. American capitalism on its own will innovate and create profits far faster than any other economic system in history. Biden did quite a good job of staying away.

Q: Why are credit spreads still okay to do in this environment?

A: Because the implied volatility on the options are so high, you can get insane amounts of money—in the money like 30% or 40% —and get trades done and have a 0% chance of taking a loss on that. Suddenly you're being paid double to take risks on these option trades. The classic example is the $88-$90 call spread in Nvidia (NVDA), which we have expiring on Friday, March 21. We never even got close to $90, but the implied volatility on the day we added that trade was a ridiculous 75%. So, it's almost impossible to lose money when you put on trades with implied volatility in the options of 75%.

Q: What's your long-term target on gold now that your last long-term target of 3,000 finally got hit?

A: Yes, we've been recommending gold (GLD) for seven years now. In that time, it's doubled: $1,500 to $3,000. I'm now looking for $5,000 in gold by 2030, in five years. I got a feeling that flight-to-safety plays are going to be very popular in the world going forward. And by the way, people who did look for Bitcoin to protect them in any downturns: Bitcoin actually went down three times faster than the S&P 500 in the last month.

Q: Will stocks rise if the Fed cuts interest rates?

A: No, they won't, because the only reason the Fed will cut interest rates is if inflation falls, and right now, inflation is about to see a big upturn as those import duties of 25% or 50% work their way through the system. A lot of companies are front-running price increases before they even pay the tariffs and try to carve out some extra margin for themselves in advance. On Wednesday, Jay Powell said he expects inflation to rise from 2.5% to 2.8% by yearend and this will prove to be a low number. That is his “president breathing down the back of his next” forecast.

Q: What are your favorite Chinese stocks?

A: Well, a lot of these leading stocks have already gone up 50% or more since the beginning of the year as capital flees the United States and goes abroad. But if you held a gun to my head and said you had to buy two, I would buy Baidu (BIDU), and I would buy Alibaba (BABA). Those would be my Chinese picks. Alibaba is the closest thing you get to an Amazon in China.

Q: Has the dollar hit its lows this year?

A: No. Risk of the next Fed rate move is an interest rate cut. That is going to hang over the dollar and the currency markets for the entire year. And I don't see any recovery in the dollar this year. In fact, it's easy to see much lower lows, and higher highs in the foreign currencies. Buy (FXA), (FXE), (FXC), and (FXB) on dips.

Q: How do you feel about natural gas?

A: I would not be a buyer here. I think we've had a terrific run off of extreme cold weather—believe me, we got some of that in Nevada too—and that is starting to fade now. This is historically when that gas starts to fade for the year. Long term, my view on gas is bullish because of increased exports to China. We have a very pro-energy administration here; that means taking off the export restraints on natural gas, which can only be good for the gas companies and the gas price. China has basically told us they'll take all the natural gas they can get from us because every shipload of gas they buy (LNG) means less coal they have to burn.

To watch a replay of this webinar with all the charts, bells, whistles, and classic rock music, just log in to www.madhedgefundtrader.com, go to MY ACCOUNT, click on GLOBAL TRADING DISPATCH, then WEBINARS, and all the webinars from the last 12 years are there in all their glory.

Good Luck and Good Trading

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Dealing with the Cloud works, and for every relevant tech company, this division serves as the pipeline to the CEO position.

If this isn’t the case for a tech company, then there’s something egregiously wrong with them!

Take Andy Jassy, the mastermind behind Amazon’s (AMZN) lucrative cloud computing division and the man who succeeded company founder Jeff Bezos.

He was rewarded with this important position based on his performance in the cloud and faced the daunting proposition of following Bezos as CEO.

Bezos incorporated Amazon almost 30 years ago.

Jassy developed a highly profitable and market-leading business, Amazon Web Services, that runs data centers serving a wide range of corporate computing needs.

Cloud 101

If you've been living under a rock for the past few years, the cloud phenomenon hasn't passed you by and you still have time to cash in.

You want to hitch your wagon to cloud-based investments in any way, shape, or form.

Amazon leads the cloud industry it created.

It still maintains more than 30% of the cloud market. Microsoft would need to gain a lot of ground to even come close to this jewel of a business.

Amazon relies on AWS to underpin the rest of its businesses and that is why AWS contributes most of Amazon's total operating income.

Total revenue for just the AWS division would operate as a healthy stand-alone tech company if need be.

The future is about the cloud.

These days, the average investor probably hears about the cloud a dozen times a day.

If you work in Silicon Valley, you can quadruple that figure.

So, before we get deep into the weeds with this letter on cloud services, cloud fundamentals, cloud plays, and cloud Trade Alerts, let's get into the basics of what the cloud actually is.

Think of this as a cloud primer.

It's important to understand the cloud, both its strengths and limitations.

Giant companies that have it figured out, such as Salesforce (CRM) and Zscaler (ZS), are some of the fastest-growing companies in the world.

Understand the cloud and you will readily identify its bottlenecks and bulges that can lead to extreme investment opportunities. And that is where I come in.

Cloud storage refers to the online space where you can store data. It resides across multiple remote servers housed inside massive data centers all over the country, some as large as football fields, often in rural areas where land, labor, and electricity are cheap.

They are built using virtualization technology, which means that storage space spans many different servers and multiple locations. If this sounds crazy, remember that the original Department of Defense packet-switching design was intended to make the system atomic bomb-proof.

As a user, you can access any single server at any one time anywhere in the world. These servers are owned, maintained, and operated by giant third-party companies such as Amazon, Microsoft, and Alphabet (GOOGL), which may or may not charge a fee for using them.

The most important features of cloud storage are:

1) It is a service provided by an external provider.

2) All data is stored outside your computer residing inside an in-house network.

3) A simple Internet connection will allow you to access your data at any time from anywhere.

4) Because of all these features, sharing data with others is vastly easier, and you can even work with multiple people online at the same time, making it the perfect, collaborative vehicle for our globalized world.

Once you start using the cloud to store a company's data, the benefits are many.

No Maintenance

Many companies, regardless of their size, prefer to store data inside in-house servers and data centers.

However, these require constant 24-hour-a-day maintenance, so the company has to employ a large in-house IT staff to manage them - a costly proposition.

Thanks to cloud storage, businesses can save costs on maintenance since their servers are now the headache of third-party providers.

Instead, they can focus resources on the core aspects of their business where they can add the most value, without worrying about managing the IT staff of prima donnas.

Greater Flexibility

Today's employees want to have a better work/life balance and this goal can be best achieved by letting them work remotely which effectively happened because of the public health situation. Increasingly, workers are bending their jobs to fit their lifestyles, and that is certainly the case here at Mad Hedge Fund Trader.

How else can I send off a Trade Alert while hanging from the face of a Swiss Alp?

Cloud storage services, such as Google Drive, offer exactly this kind of flexibility for employees.

With data stored online, it's easy for employees to log into a cloud portal, work on the data they need to, and then log off when they're done. This way a single project can be worked on by a global team, the work handed off from time zone to time zone until it's done.

It also makes them work more efficiently, saving money for penny-pinching entrepreneurs.

Better Collaboration and Communication

In today's business environment, it's common practice for employees to collaborate and communicate with co-workers located around the world.

For example, they may have to work on the same client proposal together or provide feedback on training documents. Cloud-based tools from DocuSign, Dropbox, and Google Drive make collaboration and document management a piece of cake.

These products, which all offer free entry-level versions, allow users to access the latest versions of any document so they can stay on top of real-time changes which can help businesses to better manage workflow, regardless of geographical location.

Data Protection

Another important reason to move to the cloud is for better protection of your data, especially in the event of a natural disaster. Hurricane Sandy wreaked havoc on local data centers in New York City, forcing many websites to shut down their operations for days.

And we haven’t talked about the ransomware attacks by Eastern Europeans on energy company Colonial Pipeline and meat producer JBS Foods.

The cloud simply routes traffic around problem areas as if, yes, they have just been destroyed by a nuclear attack.

It's best to move data to the cloud, to avoid such disruptions because there your data will be stored in multiple locations.

This redundancy makes it so that even if one area is affected, your operations don't have to capitulate, and data remains accessible no matter what happens. It's a system called deduplication.

Lower Overhead

The cloud can save businesses a lot of money.

By outsourcing data storage to cloud providers, businesses save on capital and maintenance costs, money that in turn can be used to expand the business. Setting up an in-house data center requires tens of thousands of dollars in investment, and that's not to mention the maintenance costs it carries.

Plus, considering the security, reduced lag, up-time, and controlled environments that providers such as Amazon's AWS have, creating an in-house data center seems about as contemporary as a buggy whip, a corset, or a Model T.

The cloud is where you want to be.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2023-12-01 14:02:292023-12-01 11:13:43The Place To Be

Dealing with the Cloud works and for every relevant tech company, this division serves as the pipeline to the CEO position.

If this isn’t the case for a tech company, then there’s something egregiously wrong with them!

Take Andy Jassy, the mastermind behind Amazon’s (AMZN) lucrative cloud computing division and was the man who succeeded company founder Jeff Bezos.

He was rewarded this important position based on his performance in the cloud and faces a daunting proposition of following Bezos as CEO.

Bezos incorporated Amazon almost 30 years ago.

Jassy developed a highly profitable and market-leading business, Amazon Web Services, that runs data centers serving a wide range of corporate computing needs.

Cloud 101

If you've been living under a rock the past few years, the cloud phenomenon hasn't passed you by and you still have time to cash in.

You want to hitch your wagon to cloud-based investments in any way, shape, or form.

Amazon leads the cloud industry it created.

It still maintains more than 30% of the cloud market. Microsoft would need to gain a lot of ground to even come close to this jewel of a business.

Amazon relies on AWS to underpin the rest of its businesses and that is why AWS contributes most of Amazon's total operating income.

Total revenue for just the AWS division would operate as a healthy stand-alone tech company if need be.

The future is about the cloud.

These days, the average investor probably hears about the cloud a dozen times a day.

If you work in Silicon Valley, you can quadruple that figure.

So, before we get deep into the weeds with this letter on cloud services, cloud fundamentals, cloud plays, and cloud Trade Alerts, let's get into the basics of what the cloud actually is.

Think of this as a cloud primer.

It's important to understand the cloud, both its strengths and limitations.

Giant companies that have it figured out, such as Salesforce (CRM) and Zscaler (ZS), are some of the fastest-growing companies in the world.

Understand the cloud and you will readily identify its bottlenecks and bulges that can lead to extreme investment opportunities. And that is where I come in.

Cloud storage refers to the online space where you can store data. It resides across multiple remote servers housed inside massive data centers all over the country, some as large as football fields, often in rural areas where land, labor, and electricity are cheap.

They are built using virtualization technology, which means that storage space spans across many different servers and multiple locations. If this sounds crazy, remember that the original Department of Defense packet-switching design was intended to make the system atomic bomb-proof.

As a user, you can access any single server at any one time anywhere in the world. These servers are owned, maintained, and operated by giant third-party companies such as Amazon, Microsoft, and Alphabet (GOOGL), which may or may not charge a fee for using them.

The most important features of cloud storage are:

1) It is a service provided by an external provider.

2) All data is stored outside your computer residing inside an in-house network.

3) A simple Internet connection will allow you to access your data at anytime from anywhere.

4) Because of all these features, sharing data with others is vastly easier, and you can even work with multiple people online at the same time, making it the perfect, collaborative vehicle for our globalized world.

Once you start using the cloud to store a company's data, the benefits are many.

No Maintenance

Many companies, regardless of their size, prefer to store data inside in-house servers and data centers.

However, these require constant 24-hour-a-day maintenance, so the company has to employ a large in-house IT staff to manage them - a costly proposition.

Thanks to cloud storage, businesses can save costs on maintenance since their servers are now the headache of third-party providers.

Instead, they can focus resources on the core aspects of their business where they can add the most value, without worrying about managing IT staff of prima donnas.

Greater Flexibility

Today's employees want to have a better work/life balance and this goal can be best achieved by letting them working remotely which effectively happened because of the public health situation. Increasingly, workers are bending their jobs to fit their lifestyles, and that is certainly the case here at Mad Hedge Fund Trader.

How else can I send off a Trade Alert while hanging from the face of a Swiss Alp?

Cloud storage services, such as Google Drive, offer exactly this kind of flexibility for employees.

With data stored online, it's easy for employees to log into a cloud portal, work on the data they need to, and then log off when they're done. This way a single project can be worked on by a global team, the work handed off from time zone to time zone until it's done.

It also makes them work more efficiently, saving money for penny-pinching entrepreneurs.

Better Collaboration and Communication

In today's business environment, it's common practice for employees to collaborate and communicate with co-workers located around the world.

For example, they may have to work on the same client proposal together or provide feedback on training documents. Cloud-based tools from DocuSign, Dropbox, and Google Drive make collaboration and document management a piece of cake.

These products, which all offer free entry-level versions, allow users to access the latest versions of any document so they can stay on top of real-time changes which can help businesses to better manage workflow, regardless of geographical location.

Data Protection

Another important reason to move to the cloud is for better protection of your data, especially in the event of a natural disaster. Hurricane Sandy wreaked havoc on local data centers in New York City, forcing many websites to shut down their operations for days.

And we haven’t talked about the ransomware attacks by Eastern Europeans on energy company Colonial Pipeline and meat producer JBS Foods.

The cloud simply routes traffic around problem areas as if, yes, they have just been destroyed by a nuclear attack.

It's best to move data to the cloud, to avoid such disruptions because there your data will be stored in multiple locations.

This redundancy makes it so that even if one area is affected, your operations don't have to capitulate, and data remains accessible no matter what happens. It's a system called deduplication.

Lower Overhead

The cloud can save businesses a lot of money.

By outsourcing data storage to cloud providers, businesses save on capital and maintenance costs, money that in turn can be used to expand the business. Setting up an in-house data center requires tens of thousands of dollars in investment, and that's not to mention the maintenance costs it carries.

Plus, considering the security, reduced lag, up-time and controlled environments that providers such as Amazon's AWS have, creating an in-house data center seems about as contemporary as a buggy whip, a corset, or a Model T.

The cloud is where you want to be.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00april@madhedgefundtrader.comhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngapril@madhedgefundtrader.com2023-10-16 20:02:232023-10-16 16:41:40Go Straight To The Top With The Cloud

Automation is taking place at warp speed displacing employees from all walks of life.

Next could be you!

According to a recent report, the U.S. financial industry will depose of 200,000 workers in the next decade because of automating efficiencies.

Yes, humans are going the way of the dodo bird and banking will effectively become algorithms working for a handful of executives and engineers.

The x-factor in this equation is the $250 billion annually that banks spend on technological development in-house which is second highest after the traditional tech giants.

Welcome to the world of lower cost, shedding wage bills, and boosting performance rates.

We forget to realize that employee compensation eats up around 50% of bank expenses.

The 200,000 job trimmings would result in 10% of the U.S. banking sector getting axed.

The hyped-up “golden age of banking” should deliver extraordinary savings and premium services to the customer at no extra cost.

This iteration of mobile and online banking has delivered functionality that no generation of customers has ever seen.

Gutting bank jobs will naturally occur in the call centers first, because they are the low-hanging fruit for the automated chatbots.

A few years ago, chatbots were suboptimal, even spewing out arbitrary profanity, but they have slowly crawled up in performance metrics to the point where some customers are unaware they are communicating with an artificially engineered algorithm.

The wholesale integration of automating the back-office staff isn’t contained to the rudimentary part of the staff.

The front office will experience a 30% drop in numbers sullying the predated ideology that front office staff are irreplaceable heavy hitters.

The front-office staff has already felt the brunt of downsizing with purges carried out from 2022 representing a twelfth year of continuous decline.

Front-office traders and brokers are being rapidly replaced by software engineers as banks follow the wider trend of every company transitioning into a tech company.

The infusion of artificial intelligence will lower mortgage processing costs by 30% and the accumulation of hordes of data will advance the marketing effort into a potent, multi-pronged, hybrid cloud-based, and hyper-targeted strategy.

The last two human bank hiring waves are a distant memory.

The most recent spike came in the 7 years after the dot com crash of 2001 until the sub-prime crisis of 2008 adding around half a million jobs on top of the 1.5 million that existed then.

After the subsidies wear off from the pandemic, I do believe that the banking sector will quietly put in the call to trim even more.

The longest and most dramatic rise in human bankers was from 1935 to 1985, a 50-year boom that delivered over 1.2 million bankers to the U.S. workforce.

This type of human hiring will likely never be seen again in the U.S. financial industry.

And if you thought that this phenomenon was limited to the U.S., think again, Europe is by far the biggest culprit by already laying off 100,000 employees in 2022.

Even Europe’s banking jewel Credit Suisse is on the brink of collapsing and in need of a bailout.

Don’t tell your kid to get into banking, because they will most likely be feeding on scraps at that point.

An interesting tech stock that integrates financial payments is Square (SQ) which has given back its entire pandemic performance.

As US interest rates are expected to peak and go down in 2023, I recommend dollar cost average into this stock at bargain basement prices.

THE LAST STAGE OF HUMAN-FACING BANK SERVICES IS NOW!

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2022-12-21 14:02:452023-01-02 20:08:33Fin-Tech Automation and Banking

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.