Mad Hedge Biotech and Healthcare Letter

March 21, 2024

Fiat Lux

Featured Trade:

(THE TOP DOG IN ANIMAL HEALTHCARE)

(ZTS), (AMGN), (PFE), (JNJ), (ELAN)

Mad Hedge Biotech and Healthcare Letter

March 21, 2024

Fiat Lux

Featured Trade:

(THE TOP DOG IN ANIMAL HEALTHCARE)

(ZTS), (AMGN), (PFE), (JNJ), (ELAN)

You've likely witnessed a scene like this: You're at the park, and you see a young couple playing fetch with their golden retriever.

The dog is absolutely loving life, jumping and bounding after the ball, tail wagging furiously. It's a heartwarming scene, and it's one that's becoming more and more common these days.

In fact, just the other day, over coffee, a veterinarian buddy of mine spilled the beans.

"You wouldn't believe how people are pampering their pets these days," she said, shaking her head in amusement. "It's no longer just about the basics—food and health. Nope, we're talking top-tier, VIP treatment. They're ready to drop serious cash to ensure their furry friends are living their best lives."

It's a whole new world for pets, and their owners are leading the charge, wallets wide open.

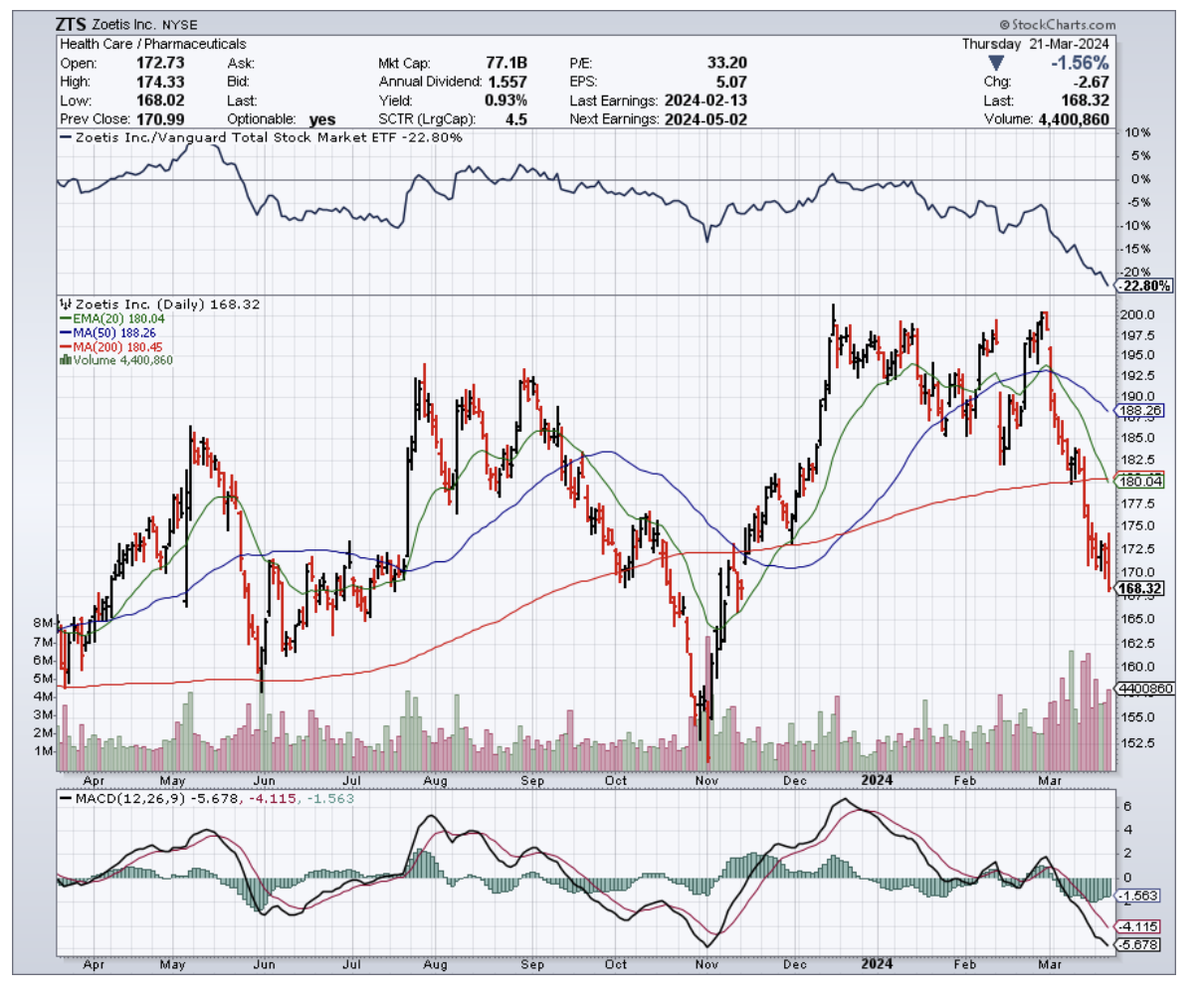

And that is where Zoetis (ZTS) comes in. This company is the top dog (pun intended) in the animal healthcare space, and it's been making some serious waves in the market lately.

Now, I know what you're thinking - "What about those big-shot human healthcare stocks like Amgen (AMGN), Johnson & Johnson (JNJ), and Pfizer (PFE)?"

Well, let me tell you, Zoetis has been giving them a run for their money since spinning off from Pfizer back in 2013. This company has been posting positive annual EPS growth every single year, with an average annual EPS growth rate of a whopping 15.9%.

But that's not all — Zoetis has also been dishing out some seriously impressive dividend growth, with a CAGR of nearly 25% since it was spun off. That's right, this stock is checking all the boxes for dividend growth investors.

And if you think this is just an income play, think again.

Zoetis has been absolutely crushing the S&P 500, posting price returns of 492% compared to the market's measly 176% gains over the last decade.

So, what's the secret behind Zoetis' success?

Well, it all comes down to our furry (and sometimes scaly) friends. You see, people are lonelier than ever these days, and they're turning to pets for that much-needed companionship.

The US Surgeon General even called loneliness an epidemic, sounding the alarm on its dire impacts on health, likening its risks to smoking up to 15 cigarettes a day.

From the gripping claws of loneliness among young adults to the isolation felt by mothers with young children, the pandemic has only deepened this crisis, affecting a staggering 36% of Americans.

More than that, this loneliness trend isn't just about having a buddy to binge-watch Netflix (NFLX) with. It's actually impacting our species' survival. Studies show that sexual activity is on the decline, and technology is distorting the way we interact with each other.

It's a bit of a downer, I know, but here's where Zoetis shines through. As people turn to pets for love and affection, they're also shelling out some serious cash to keep their furry friends healthy and happy.

The American Pet Products Association says that nearly 87 million U.S. households own pets (roughly 66%), and it's not just the younger generations who are getting in on the action. Baby Boomers and Gen Xers are also big-time pet owners.

What does all this pet love mean for the industry? Well, the pet industry is expected to be a $150 billion behemoth in 2024.

Now, what really sets Zoetis apart from the pack? It all comes down to pricing power and growth potential.

In the animal health market, drug prices aren't determined by pesky regulations, government buyers, or PBMs. That means Zoetis can charge premium prices for their trusted, name-brand drugs without having to jump through hoops.

Plus, with less competition in the animal health space, Zoetis' products have longer growth runways and aren't constantly battling generic copycats.

For context, Elanco (ELAN), Zoetis' pure-play competitor, only managed to bring in $4.4 billion in sales.

So, what's the bottom line here?

Zoetis is a best-in-breed play on the booming animal healthcare market, with a safe and growing dividend to boot. As this sell-off continues, Zoetis keeps climbing higher on my personal watch list. I'm ready to back up the truck and load up on shares come April when I put my March dividends to work.

If you're looking for a unique way to play the healthcare space with a company that's got plenty of bark and bite, Zoetis might just be the stock for you.

Mad Hedge Biotech and Healthcare Letter

October 12, 2023

Fiat Lux

Featured Trade:

(BARKING UP THE RIGHT STOCK)

(ZTS), (MRK)

When I search for investment opportunities, it's rare for an old article to capture my attention. Yet, an article from The Wall Street Journal in January titled "Americans Can't Stop Pampering Their Pets - Companies Want In" has lingered in my thoughts. While the sentiment of treating pets as family isn't new, the financial implications of this trend are profound.

The global animal healthcare market, a sector once overlooked, has now burgeoned into a significant investment avenue. Recent data reveals the global animal healthcare market size was worth $40.21 billion in 2022.

Astoundingly, it's projected to soar to $84.98 billion by 2030, growing at a CAGR of 9.81%. This growth isn't just a fluke; it's propelled by rising animal health expenditure, increasing prevalence of diseases in animals, concerns over zoonoses, and strategic initiatives by industry giants.

A case in point: In January 2023, Merck (MRK) inaugurated a state-of-the-art manufacturing facility in Boxmeer, Netherlands, specifically for companion animal vaccines, responding to surging global demand.

But what's driving this demand? The answer lies in our plates and our living rooms.

On one hand, there's a rising global appetite for animal protein. While plant-based diets are gaining traction, the majority still lean towards animal-derived sources like eggs, meat, and milk. On the other hand, the human-animal bond has never been stronger, especially with pets. This bond translates to a willingness to spend on their well-being, ensuring they receive the best care possible.

Enter companies like Zoetis Inc. (ZTS). As the world's premier provider of animal medicines, vaccines, and diagnostic products, Zoetis stands at the forefront of this booming market.

With an impressive portfolio boasting over 300 product lines, including 15 blockbuster drugs, Zoetis has strategically positioned itself in two pivotal markets: companion animals (our beloved cats and dogs) and livestock (primarily cattle). Their dominance isn't just regional; they lead in North America, Latin America, and Asia.

To provide a snapshot of their market prowess, Zoetis recently highlighted that pet expenditure remains unaffected even in economic downturns, where household budgets shrink by 20%.

This resilience proves the anti-cyclical nature of the animal health sector, especially the companion animal segment. Concurrently, the livestock market is set to flourish, driven by a global population surge.

By 2050, with 2 billion more mouths to feed, the demand for healthcare products for livestock will inevitably skyrocket.

Notably, Zoetis isn't just riding the wave; they're steering it. Their growth strategy is clear: sustain a 3-point premium over market growth in the long term. This ambition is backed by a robust product portfolio, continuous innovation, and a keen understanding of market dynamics. Their focus isn't just on current market leaders like parasiticides but also on potential future heavyweights in areas like atopic dermatitis, cardiovascular diseases, chronic kidney diseases, and oncology.

So, what does this mean for investors?

Zoetis' financial trajectory is promising. Their revenue forecast for this year stands between $8.575 billion and $8.725 billion, marking a 6% to 8% rise.

Their earnings per share is also set to climb, with projections between $5.03 and $5.14, up from $4.49 in 2022.

Moreover, their consistent dividend hikes, with a recent 15% increase to $0.38, signal a company that's not only growing but also rewarding its shareholders.

Overall, with its blend of resilience and growth, the animal healthcare market presents a compelling investment opportunity. Zoetis, with their strategic vision, robust product portfolio, and financial strength, is poised to lead this sector. For investors eyeing long-term growth coupled with stability, adding this company to your portfolio is undoubtedly a prudent move. I recommend you buy the dip.

Mad Hedge Biotech and Healthcare Letter

March 30, 2023

Fiat Lux

Featured Trade:

(ANOTHER MONOPOLY ON THE RISE)

(ZTS), (PFE)

Whether you’re a devoted dog mom or a tough-as-nails cattle rancher, you’ll most likely agree that animals should have healthcare, pretty much like humans. This is where Zoetis (ZTS) comes in, a company that focuses exclusively on developing treatments and other healthcare needs for livestock and, of course, pets.

Zoetis is the only pure-play animal health company in the world. It sells everything related to animal healthcare, from painkillers for your beloved pets to diagnostic equipment needed in veterinary clinics. Spun off from Pfizer (PFE) roughly a decade ago, Zoetis’ profits have consistently climbed thanks to the steady rise in spending on domestic animals.

Admittedly, macroeconomic issues and a pause in earnings growth recently affected the stock negatively, which saw its price fall by almost 13% since 2022. However, short- and long-term catalysts are anticipated to boost the stock this year, with the company expected to report at least a 33% increase in price in the following months.

Pet ownership across the globe has been exhibiting an increase in demand even before the pandemic, with pets gaining more importance and getting treated as part of the family. This indicates lower chances of skimping when it comes to their health, paving the way for more innovative treatments and possibly more expensive trips to the vet.

The increasing demand for animal protein has also called for higher livestock production worldwide, which translates to more sales in the animal healthcare sector. In fact, over half of the antibiotics sold in 2022 were used for the improvement of farm yields.

Incredibly, even concerns over recession have not hampered these trends. If anything, the demands continue to rise.

This is one of the most compelling reasons to consider Zoetis stock. It is already the biggest name in the global markets, particularly for companion animals, cattle, swine, and even fish. Since it is virtually a monopoly in the animal healthcare industry, it is strategically positioned to sustain its momentum and penetrate the market quicker than the up-and-coming competition.

Its total addressable market is estimated to be approximately $45 billion. For context, this market recorded an annual growth of 5.8% over the past 20 years.

Surprisingly, Zoetis only spent $529 million out of its $8 billion revenue for research and development, which means it won’t cost the company too much money to continue churning out new drugs, vaccines, software packages, treatments, and other animal healthcare needs for the foreseeable future.

The company is also expanding faster compared to the broader market, with Zoetis’ earnings forecast to rise at an average of 13% each year over the following five years.

Another underappreciated factor that makes Zoetis attractive is its pipeline of innovation. Unlike competitors that depend on price hikes for their growth, Zoetis leverages its cutting-edge innovations.

An excellent example is its game-changing drug, Simparica Trio, a triple combo product for parasite prevention launched in 2020. By 2022, sales of this drug jumped by an impressive 57% to hit $744 million. Another example is Librela, an osteoarthritis treatment for dogs, which achieved the blockbuster status of $100 million in sales outside the United States and is slated for release in the country sometime this 2023. Meanwhile, a feline counterpart of the drug, Solensia, received FDA approval last year and raked in $30 million in revenue.

These types of innovations provide Zoetis with a competitive edge in the form of a unique organic volume growth trajectory that’s not found in other companies.

Notably, a mere $100 million qualifies an animal health drug as a blockbuster. This is one reason that discourages potential Big Pharma rivals from entering the space and challenging Zoetis. After all, they are used for human drugs worth $1 billion or more.

However, it’s essential to remember that many animal treatments are paid out of pocket. That means there are no insurance companies pressuring the patients to get or switch to cheaper drugs or generics even when Zoetis’ products lose their patent exclusivity. Actually, in 2019, about 75% of the company’s revenue was generated from its products that had already lost patent protection.

Overall, Zoetis is a solid investment thanks to its growth potential and highly competitive moat. It has a strong track record and an impressively diverse revenue stream, making this animal health company well-equipped to sustain its momentum in the years to come at a fast pace. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

November 17, 2022

Fiat Lux

Featured Trade:

(A QUALITY BEATEN-DOWN STOCK)

(ZTS), (ELAN)

Always focus on the bright side. Not only does that perspective get you in a better mood, but it can also work as good advice when it comes to making money. This becomes especially effective with the downturn of the stock market.

It’s pretty easy to discover beaten-down stocks in today’s environment. However, finding businesses that are worth your money at current levels and holding on to them for a long time is an entirely different story. Long-term stocks are not your run-of-the-mill companies, especially since many businesses with declining shares are better left alone.

While it didn’t suffer as much as the other sectors, the biotech and healthcare industry still has some beaten-down stocks that are worth buying. One of them is Zoetis (ZTS).

It has been a particularly rough year for Zoetis, with shares of this animal health company falling by over 40%. Things didn’t get better when it disclosed its third-quarter earnings report for 2022.

Going direct to the point, neither Zoetis’ earnings nor updated guidance. Zoetis dialed down its full-year guidance for 2022, estimating its initial expected revenue, which was between $8.225 billion and $8.325 billion, to fall to $8.08 billion instead.

As expected, the market reacted negatively to these figures, with the stock declining by 11%.

Although this might not appear to be a substantial drop in comparison to how other companies are performing this earnings season, it’s still a significant one-day drop for Zoetis. For context, this latest drop was the company’s second-biggest one-day decline in the past 10 years—only second to the one they recorded when COVID struck.

Reviewing the “numbers” section of Zoetis’ earnings report, one of the major causes of the lower-than-anticipated growth was supply constraints. This issue affected both US and international markets, albeit involving the former more.

Actually, “supply” was the most important issue discussed during the earnings call—so much so that the term “supply” was uttered a whopping 62 times.

It wasn’t just Zoetis that suffered from supply-related issues. These concerns affected practically the entire animal health sector this year, including another major competitor, Elanco (ELAN).

Knowing the root of the issue behind Zoetis’ recent decline is key to determining whether this remains a good stock. It always helps if we can understand the factors in play that led to the earnings report and add some context around the figures presented.

After all, the figures at times portray one thing and miss out on what is under the surface—the things that we need to understand and know about to interpret the results better.

At this point, Zoetis can still be considered an excellent company that needs to deal with some supply issues. When these are resolved, it will do just fine as a long-term investment.

Moreover, the animal health market has an incredibly bright future ahead.

This industry is projected to record a compound annual growth rate of 10% through 2030.

Pet ownership has climbed notably during the pandemic and is projected to sustain its upward trajectory in the years to come.

In addition, population growth will result in an increased demand for protein-rich food sources like livestock. That would translate to an expanded revenue stream for animal health companies, which offer products geared towards these demands.

With a market capitalization of $69.11 billion and a broad reach both in the US and across the globe, Zoetis is well-positioned to profit from this projected growth.

Moreover, this company is currently recognized as the market leader in animal health for cattle, swine, companion animals, and fish, while it ranks #5 in the global poultry market.

Overall, Zoetis is worth adding to your portfolio. While it’s facing some short-term challenges, this animal healthcare business is a pretty solid buy.

Mad Hedge Biotech & Healthcare Letter

June 24, 2021

Fiat Lux

FEATURED TRADE:

(AN ANIMAL HEALTH CARE STOCK WORTH A LOOK)

(ZTS), (PFE), (ELAN), (LLY), (IDXX), (CHWY), (FRPT)

The animal health industry has been expanding rapidly over the past years, particularly on the pet side.

If you’re treating your pets more like people, then you’re part of the growing number of customers doing the same thing.

While the “humanization” of animals has actually been going on for years, house pets have made an inexorable transition from the backyard to the couch as more and more people treat their pets as family, especially during the pandemic.

Sales for pet supplies continue to surge as pet owners splurge on everything for their furry friends, from kibble to supplements.

In fact, animal health product sales went up 7% in 2020, generating roughly $11 billion despite the pandemic—a trend that’s expected to gain even more momentum as retail sales start to shift from vet clinics to stores and online platforms.

Pfizer’s (PFE) spinoff company, Zoetis (ZTS), is the undisputed leader in the animal healthcare industry with a proven track record and a rich history spanning 65 years.

The way the company handled the challenges in 2020 showcased its ability to not only rise to the occasion but also turn red-hot despite the setbacks.

Meanwhile, Zoetis stock experienced continuing growth in 2021.

Revenues from its Simparica franchise, which fights off heartworms and other parasites in dogs and cats, grew by 133% year-on-year in the first quarter of 2021 thanks to its expansion in the US, Europe, Australia, and Canada markets.

Next to the US, Zoetis’ biggest market is China. In the first quarter of this year, the company saw a 75% climb in its revenues in the region, raking in $123 million for the period.

Simparica Trio, which generated $90 million in the first quarter alone, also received approvals in new markets, such as Japan and Mexico.

Its predecessor, Simparica, also continues to rake in good numbers, with $74 million in sales during the same period.

However, another player appears to be making big moves to dethrone the company.

Elanco Animal Health (ELAN), which is a spinoff of Eli Lilly (LLY), struck an impressive $440 million deal to acquire Kindred Biosciences (KIN) in an effort to bolster its drug pipeline.

This deal, which is expected to close in the third quarter of this year, will focus primarily on Elanco’s pet dermatology segment.

The move to invest in dermatology is a great decision for Elanco. Dermatology has become one of the fastest growing divisions of pet care.

For context, Zoetis’ 2020 revenues for this segment reached $925 million, recording a $170 million boost from its 2019 earnings.

The dermatology segment grew 24% year on year in the first quarter of 2021 as well, recording $245 million in revenues for this period.

Looking at the performance of the products in this segment, Zoetis is on track to exceed the $1 billion revenue estimate for 2021.

Outside its dermatology segment, Zoetis also enjoyed a 47% year-on-year growth in its diagnostics sector in the first quarter—a trend that’s anticipated to improve in the long run due to the company’s continuous expansion globally.

Zoetis stock is projected to continue its momentum throughout 2021 and well beyond 2022.

For this year, the company estimates revenue growth by 9% to 11%, which would be driven by the pet care segment, additional product launches, and rising demand for their existing drugs. The reopening of the economy also plays a key role in this growth.

Other than Elanco and Zoetis, some companies working on dominating the booming animal health care sector include Idexx Laboratories (IDXX), Chewy (CHWY), and FreshPet (FRPT).

Overall, Zoetis stock has offered excellent returns for its investors. Looking at its pipeline programs and future plans, the company shows great potential for growth in the coming years.

Investors on the lookout for a stock in the animal health industry would be wise to take Zoetis into serious consideration.