Global Market Comments

January 16, 2019

Fiat Lux

Featured Trade:

(WHAT THE HECK IS ESG INVESTING?),

(TSLA), (MO)

(WILL UNICORNS KILL THE BULL MARKET?),

(TSLA), (NFLX), (DB), (DOCU), (EB), (SVMK), (ZUO), (SQ),

Global Market Comments

January 16, 2019

Fiat Lux

Featured Trade:

(WHAT THE HECK IS ESG INVESTING?),

(TSLA), (MO)

(WILL UNICORNS KILL THE BULL MARKET?),

(TSLA), (NFLX), (DB), (DOCU), (EB), (SVMK), (ZUO), (SQ),

I am always watching for market-topping indicators and I have found a whopper. The number of new IPOs from technology mega unicorns is about to explode. And not by a little bit but a large multiple, possibly tenfold.

Some 220 San Francisco Bay Area private tech companies valued by investors at more than $700 billion are likely to thunder into the public market next year, raising buckets of cash for themselves and minting new wealth for their investors, executives, and employees on a once-unimaginable scale.

Will it kill the goose that laid the golden egg?

Newly minted hoody-wearing millionaires are about to stampede through my neighborhood once again, buying up everything in sight.

That will make 2020 the biggest year for tech debuts since Facebook’s gargantuan $104 billion initial public offering in 2012. The difference this time: It’s not just one company but hundreds that are based in San Francisco, which could see a concentrated injection of wealth as the nouveaux riches buy homes, cars and other big-ticket items.

If this is not ringing a bell with you, remember back to 2000. This is exactly the sort of new issuance tidal wave that popped the notorious Dotcom Bubble.

And here is the big problem for you. If too much money gets sucked up into the new issue market, there is nothing left for the secondary market, and the major indexes can fall by a lot. Granted, probably only $100 billion worth of stock will be actually sold, but that is still a big nut to cover.

The onslaught of IPOs includes home-sharing company Airbnb at $31 billion, data analytics firm Palantir at $20 billion, and FinTech company Stripe at $20 billion.

The fear of an imminent recession starting sometime in 2020 or 2021 is the principal factor causing the unicorn stampede. Once the economy slows and the markets fall, the new issue market slams shut, sometimes for years as they did after 2000. That starves rapidly growing companies of capital and can drive them under.

For many of these companies, it is now or never. They have to go public and raise new money or go under. The initial venture capital firms that have had their money tied up here for a decade or more want to cash out now and roll the proceeds into the “next big thing,” such as blockchain, healthcare, or artificial intelligence. The founders may also want to raise some pocket money to buy that mansion or mega yacht.

Or, perhaps they just want to start another company after a well-earned rest. Serial entrepreneurs like Tesla’s Elon Musk (TSLA) and Netflix’s Reed Hastings (NFLX) are already on their second, third, or fourth startups.

And while a sudden increase in new issues is often terrible for the market, getting multiple IPOs from within the same industry, as is the case with ride-sharing Uber and Lyft, is even worse. Remember the five pet companies that went public in 1999? None survived.

Some 80% of all IPOs lost money last year. This was definitely NOT the year to be a golfing partner or fraternity brother with a broker.

What is so unusual in this cycle is that so many firms have left going public to the last possible minute. The desire has been to milk the firms for all they are worth during their high growth phase and then unload them just as they go ex-growth.

Also holding back some firms from launching IPOs is the fear that public markets will assign a lower valuation than the last private valuation. That’s an unwelcome circumstance that can trigger protective clauses that reward early investors and punish employees and founders. That happened to Square (SQ) in its 2015 IPO.

That’s happening less and less frequently: In 2019, one-third of IPOs cut companies’ valuations as they went from private to public. In 2019, that ratio has dropped to one in six.

Also unusual this time around is an effort to bring in more of the “little people” in the IPO. Gig economy companies like Uber and Lyft have lobbied the SEC for changes in new issue rules that enabled their drivers to participate even though they may be financially unqualified. They were all hit with losses of a third once the companies went public.

As a result, when the end comes, this could come as the cruelest bubble top of all.

Mad Hedge Technology Letter

June 13, 2019

Fiat Lux

Featured Trade:

(THE TRADE WAR MOVES DOWN MARKET)

(DOCU), (PSTG), (ZUO), (MSFT), (PYPL), (ADBE)

To understand the consequences of the global trade war, just take a look at the second-tier software companies.

There has been softness in the latest earnings reports and guidance signaling a lukewarm upcoming summer.

The best-case scenario is the likes of DocuSign (DOCU) and Zuora (ZUO) rallying into the end of the year.

That is hardly a given considering the global turmoil has shifted supply chains in every which way as well as denting overall demand.

Cloud-based companies have seen meaningful weakness this earnings season, even some of them absorbing heavy losses in the wake of their quarterly results, but analysts aren’t ready to write off this industry yet.

Referencing the latest industry survey, 20 software companies reported results in the last month, and of those, only six saw a positive response in their stock prices.

DocuSign and Pure Storage (PSTG) were among names that got clobbered, along with cloud-computing plays like Cloudera Inc., Nutanix Inc., Box Inc., and Pivotal Software Inc.

The current malaise in software is due to higher valuations and macroeconomic issues which subsequently elevates uncertainty.

There is no reason to go hysterical over this, and in no way, shape, or form, does this signal an imminent implosion of cloud companies, any incremental caution may be reversible if macro indicators and sentiment rebound.

And this rebound can be swift once all the stars align together.

Adding to the comfort is that some of the sharp drawdowns were company-specific reasons.

MongoDB Inc. or Zscaler Inc., were coming off strong year-to-date advances in their shares and it was time to take profits before the next upward explosion.

Cybersecurity company Zscaler, is appropriately accounting for outperformance and have already been crushing higher than normal expectations.

DocuSign eclipsed expectations on some metrics but disappointed on others, such as billings growth.

This disappointing miss punished the company with a drop of 15% in the pre-market session, as DocuSign grew sales by 27%, a lower rate than in previous quarters.

Management blamed the poor performance to an elongated sales cycle.

Bulls were hoping for a beat-and-raise quarter and instead got in-line numbers with some soft spots around the periphery.

Investors aren’t in a charitable mood and the sensitive mood around geopolitics has made investors more agitated with a shorter leash.

There was a tone of a broader deceleration in software demand prompting stronger names to get comingled together, but the bulk of this negative price action has been overdone.

Even further down the pecking order, results from smaller cloud firms have pointed to more fundamental issues, and these stocks have emerged as a particularly weak sub-sector.

A number of these companies reigned in their forecasts, a trend that has buttressed analyst caution over the group.

Considering that many companies have labored and there exist clear narrative similarities, it’s hard not to surmise that some real systemic pains in infrastructure exist.

Many in the industry are acutely aware of the growing chorus of companies blaming competition or poor sales execution.

Lower growth rates are effectively the predominant reason for lower stock prices in this group of cloud companies.

On the flipside of this weaker cloud growth are the heavy hitters who are throwing around their weight getting through largely unscathed.

If any of these bigger cloud companies can fuse together a business model with no China exposure, then shares are likely stable to upward trending.

A company like Adobe (ADBE) is a perfect company to look at with an unpretentious yet steady growth rate and wildly successful products.

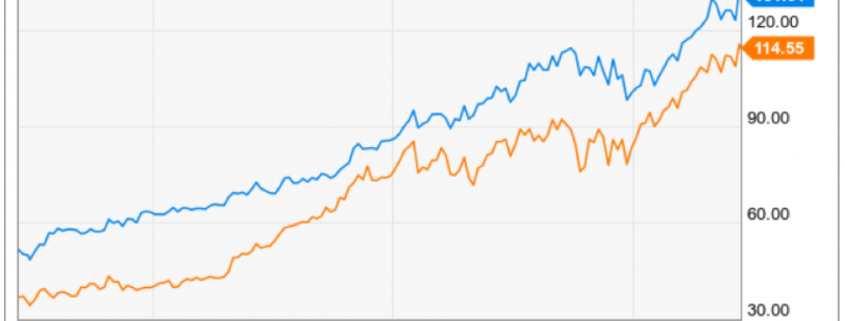

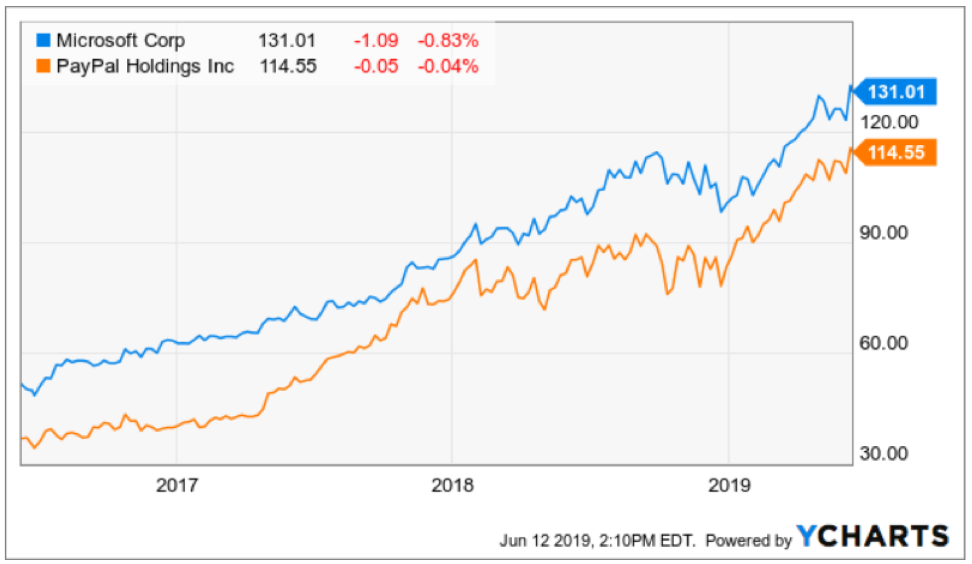

If we were to look at more growth-based companies with larger scale, then PayPal (PYPL) and Microsoft (MSFT) epitomize the type of cloud companies that are thriving in this environment and if geopolitics subsides, take on another 10% in sales.

Not only is the weather hot in the summer, but the anti-trust regulators are turning up the heat on certain tech companies on anti-trust concerns.

This could be a time to wait out those stocks and there could be another move to the upside if regulation is weaker than expected.

Global Market Comments

March 6, 2018

Fiat Lux

Featured Trade:

(WILL UNICORNS KILL THE BULL MARKET?),

(TSLA), (NFLX), (DB), (DOCU), (EB), (SVMK), (ZUO), (SQ),

(A NOTE ON OPTIONS CALLED AWAY), (TLT)

Global Market Comments

October 23, 2018

Fiat Lux

Featured Trade:

(WATCH OUT FOR THE UNICORN STAMPEDE IN 2019),

(TSLA), (NFLX), (DB), (DOCU), (EB), (SVMK), (ZUO), (SQ),

(A NOTE ON OPTIONS CALLED AWAY), (MSFT)

I am always watching for market topping indicators and I have found a whopper. The number of new IPOs from technology mega unicorns is about to explode. And not by a little bit but a large multiple, possibly tenfold.

Six San Francisco Bay Area private tech companies valued by investors at more than $10 billion each are likely to thunder into the public market next year, raising buckets of cash for themselves and minting new wealth for their investors, executives, and employees on a once-unimaginable scale.

Will it kill the goose that laid the golden egg?

Newly minted hoody-wearing millionaires are about to stampede through my neighborhood once again, buying up everything in sight.

That will make 2019 the biggest year for tech debuts since Facebook’s gargantuan $104 billion initial public offering in 2012. The difference this time: It’s not just one company, and five of them are based in San Francisco, which could see a concentrated injection of wealth as the nouveaux riches buy homes, cars and other big-ticket items.

If this is not ringing a bell with you, remember back to 2000. This is exactly the sort of new issuance tidal wave that popped the notorious Dotcom Bubble.

And here is the big problem for you. If too much money gets sucked up into the new issue market, there is nothing left for the secondary market, and the major indexes can fall, buy a lot.

The onslaught of IPOs includes ride-sharing firm Uber at $120 billion, home-sharing company Airbnb at $31 billion, data analytics firm Palantir at $20 billion, FinTech company Stripe at $20 billion, another ride-sharing firm Lyft at $15 billion, and social networking firm Pinterest at $12 billion.

Just these six names alone look to absorb an eye-popping $218 billion, and that does not include hundreds of other smaller firms waiting on the sidelines looking to tap the public market soon.

The fear of an imminent recession starting sometime in 2019 or 2020 is the principal factor causing the unicorn stampede. Once the economy slows and the markets fall, the new issue market slams shut, sometimes for years as they did after 2000. That starves rapidly growing companies of capital and can drive them under.

For many of these companies, it is now or never. The initial venture capital firms that have had their money tied up here for a decade or more want to cash out now and roll the proceeds into the “next big thing,” such as blockchain, health care, or artificial in intelligence. The founders may also want to raise some pocket money to buy that mansion or mega yacht.

Or, perhaps they just want to start another company after a well-earned rest. Serial entrepreneurs like Tesla’s Elon Musk (TSLA) and Netflix’s Reed Hastings (NFLX) are already on their second, third, or fourth startups.

And while a sudden increase in new issues is often terrible for the market, getting multiple IPOs from within the same industry, as is the case with ride-sharing Uber and Lyft, is even worse. Remember the five pet companies that went public in 1999? None survived.

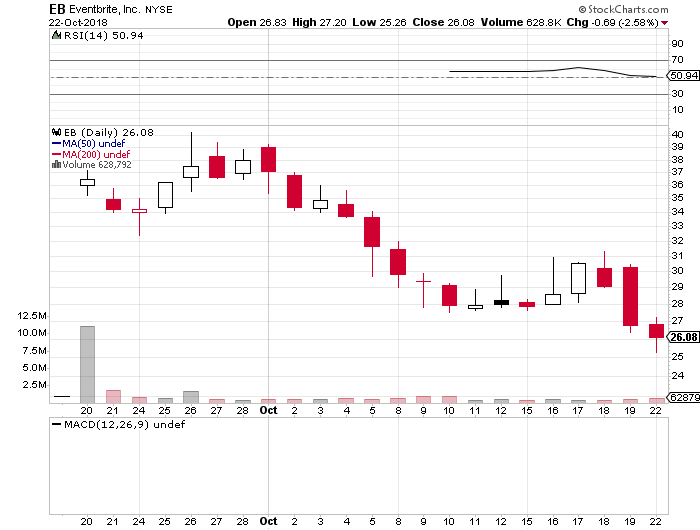

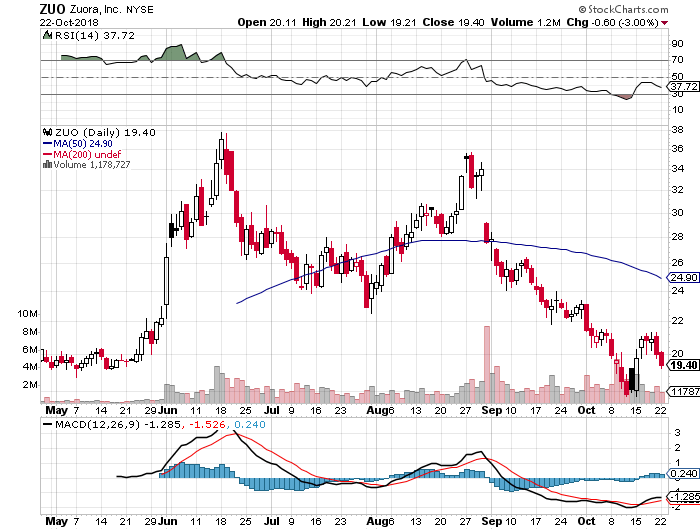

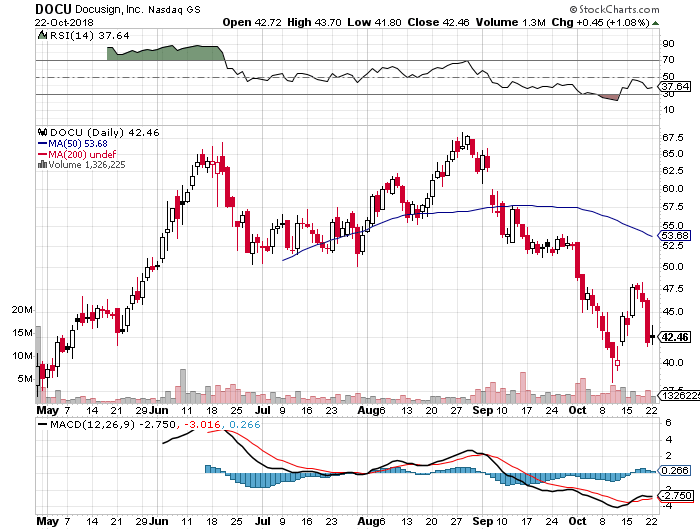

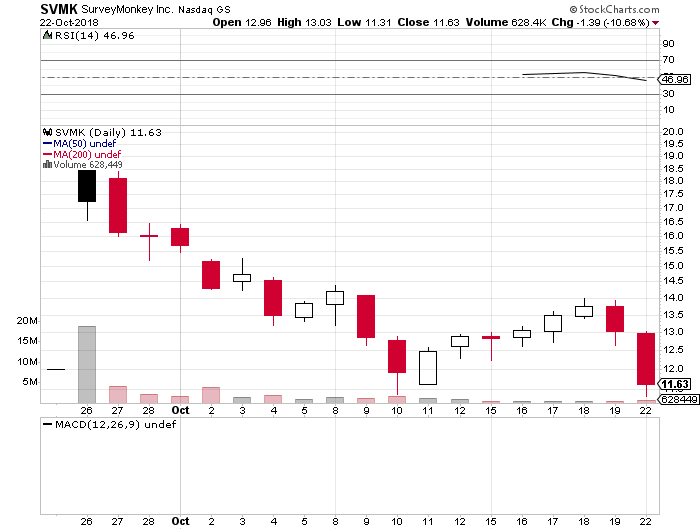

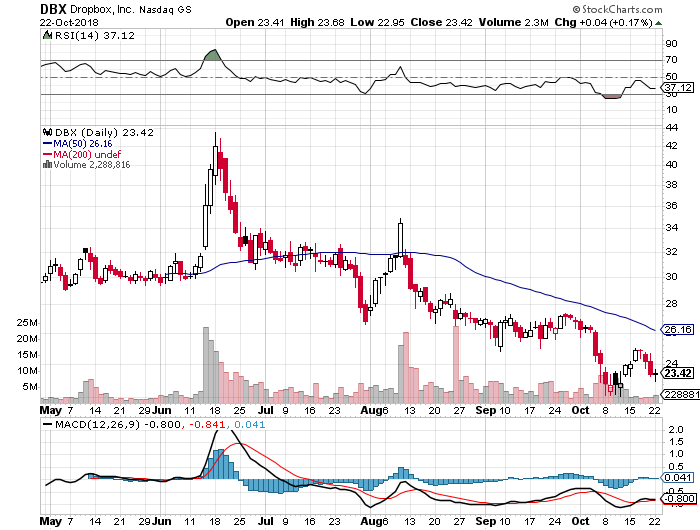

The move comes on the heels of an IPO market in 2018 that was a huge disappointment. While blockbuster issues like Dropbox (DB) and DocuSign (DOCU) initially did well, Eventbrite (EB), SurveyMonkey (SVMK), and Zuora (ZUO) have all been disasters.

Some 80% of all IPOs lost money this year. This was definitely NOT the year to be a golfing partner or fraternity brother with a broker.

What is so unusual in this cycle is that so many firms have left going public to the last possible minute. The desire has been to milk the firms for all they are worth during their high growth phase and then unload them just as they go ex-growth.

The ramp has been obvious for all to see. In the first nine months of 2018, 44 tech IPOs brought in $17 billion, according to Dealogic. That’s more than tech IPOs reaped for all of 2016 and 2017 combined.

Also holding back some firms from launching IPOs is the fear that public markets will assign a lower valuation than the last private valuation. That’s an unwelcome circumstance that can trigger protective clauses that reward early investors and punish employees and founders. That happened to Square (SQ) in its 2015 IPO.

That’s happening less and less frequently: In 2017, one-third of IPOs cut companies’ valuations as they went from private to public. In 2018, that ratio has dropped to one in six.

Also unusual this time around is an effort to bring in more of the “little people” in the IPO. Gig economy companies like Uber and Lyft are lobbying the SEC for changes in new issue rules that will enable their drivers to participate even though they may be financially unqualified.

As a result, when the end comes, this could come as the cruelest bubble top of all.

Mad Hedge Technology Letter

June 11, 2018

Fiat Lux

Featured Trade:

(HERE ARE SOME GREAT SECOND-TIER CLOUD PLAYS TO SALT AWAY),

(DOCU), (ZUO), (ZS), (MSFT), (AMZN)

The year of the cloud has been one of the most successful themes for the Mad Hedge Technology Letter since inception and rightly so.

The heavy hitters are knocking it out of the park with the top gangbuster firms facing no impediment to success.

As these firms crack on, it seems there is not a day that passes by where Amazon (AMZN) or Microsoft (MSFT) do not close up 1% for the day.

If you are feeling nervous and believe the top cloud plays are getting too frothy for your taste, even though they are not, it is time to look at alternative parts of the cloud ecosphere that could tickle your fancy.

The second-tier cloud companies focusing on a particular niche of the market is the perfect place to identify companies that are growing at higher rates than the top cloud companies in terms of revenue expansion.

Amazon, because of its sheer size, will find it harder to double its revenue in the same amount of time as cloud companies with annual revenue of just a few hundred million dollars.

Zscaler (ZS) is a cloud security company that I advised readers to buy on April,16, at $29 and after a blowout quarterly report the stock touched the $42 handle intraday.

This company is a solid buy, especially in light of the General Data Protection Regulation (GDPR) and a newfound, broad-based emphasis on Internet security that will usher in a new injection of cloud security spending.

Zscaler CEO Jay Chaudhry delivered a glorious quarterly performance and the only direction this company is going is up.

All told, Zscaler processes in excess of 45 billion Internet requests per day during peak periods.

It detects and blocks more than 100 million daily threats while performing more than 120,000 unique daily security updates.

The end result is far superior security than traditional outlets. That's the whole point.

The cloud security company was able to inspire business to a 49% YOY pace of growth and calculated billings were up 73% YOY to $54.7 million.

The quarter's success didn't stop there with operating margins gaining 9% YOY helping Zscaler go cash free positive for the quarter.

The type of security products it offers is part of an annual $17.7 billion market and rapidly expanding.

Firms are incentivized to adopt these products because reduced cost on bandwidth and lower network equipment costs benefit the bottom line.

A mobile dominant world is fast approaching, and Zscaler has positioned itself perfectly to take advantage of the new pipeline of business coming its way.

The slew of new signed contracts reinforces this trend.

The most prominent deals were with a Fortune 500 medical equipment company that purchased a bundle including a Cloud Firewall, Sandbox and Data Loss Prevention for 40,000 users.

It followed that up with a deal with a European bank that added the business bundle with SSL inspection and data loss prevention (DLP) for more than 70,000 users driven by the business moving to Office 365.

Zscaler kept going strong with another Fortune 500 tech company joining its lineup, integrating the transformation bundle for 20,000 employees and contractors just six months ago,

They were thrilled with the products, leading them to buy an additional 25,000 seats and now have all 45,000 employees served by Zscaler.

A global 500 IT services and products company in Asia went for the entry level professional bundle covering10,000 users in Q2.

It expanded the next quarter with the same bundle for more than 130,000 users domestically.

Forecasted revenue is expected to be in the range of $184 million to $185 million, substantially larger than the $126 million of revenue in 2017.

Once annual revenues start eclipsing the several billion-dollar mark, growth becomes tougher to grind out.

Zscaler is headed by an old hand and understands the market in detail.

The firm will be in a growth sweet spot for the foreseeable future. Subscribers who do not mind taking on the added risk could expect these investments to pay off many times over.

Another niche cloud company Zuora (ZUO) is performing briskly.

I recommended this stock the same day as Zscaler when it was trading at $20.50. The stock is up big, rocketing to $28.50 at the time of this writing.

Zuora is a company focused on software that helps companies manage their subscriptions business, which has been all the rage for tech companies.

The software as a service (SaaS) model has become the de-facto standard to bill for tech services, and Zuora helps automate and execute.

First quarter revenue surged 60% to $51.7 million.

Zuora's retention rate of 110% increased to 112%, demonstrating that existing customers buy premium add-ons and stick around in its ecosystem.

Zuora increased the numbers of clients with an active contract value greater than $100,000 by 6% to 441, resulting in a net add of 26.

Zscaler and Zuora are around the same size and could experience similar bullish price trajectories in the stock going forward.

DocuSign (DOCU), a digital signature software company, is another niche player whose services have been valuable in the business environment.

Instead of scrawling out your name with a quill and ink, clicking to sign makes the process faster than ever.

The stickiness of its services led Forbes to anoint DocuSign as the fourth best cloud company on the Forbes Cloud 100 list in 2017.

Last year saw DocuSign blow past the half a billion-number bringing in revenue of $518 million, up 36% YOY.

The lion's share of its business comes from its subscription business carving out $484 million in 2017, passing the $348 million in 2016.

DocuSign set an IPO price range between $24 to $26 in April 2018, and the stock has more than doubled to $58 today.

Do not fight against the cloud; embrace it like your lovable pet dog. There is no reason to short these stocks because chances are likely you will get badly burned on these ultimate buy on the dip stocks.

However, DocuSign has seldom even dipped, even in the face of a trade war, crushing dip buyers' dreams.

It has gone up in a straight line.

Only once since its late April IPO has there been a pullback of more than $1.50, and that happened in mid-May when the stock went from $45.50 to $43.

Remember, the trend is your friend.

Zscaler's 37% bump to its share prices after the earnings beat is why you want to get into this stock.

The moves up are legendary.

Zuora's earnings beat earned them a not-too-shabby 20% one-day return as well.

No matter how well Amazon does, there is no 37% up move in one day unless it finds the cure for cancer in a single pill form.

As Amazon and Microsoft grow stronger, so does the appetite for these niche cloud services.

The tide will lift all boats and choosing either a dinghy or a luxury yacht will stand you in good stead.

_________________________________________________________________________________________________

Quote of the Day

"I don't care about revenues," - said Cofounder and Executive Chairman of Alibaba Jack Ma.

Mad Hedge Technology Letter

April 17, 2018

Fiat Lux

Featured Trade:

(WHY THE CLOUD IS WHERE TRADING DREAMS COME TRUE),

(ZS), (ZUO), (SPOT), (DBX), (AMZN), (CSCO), (CRM)