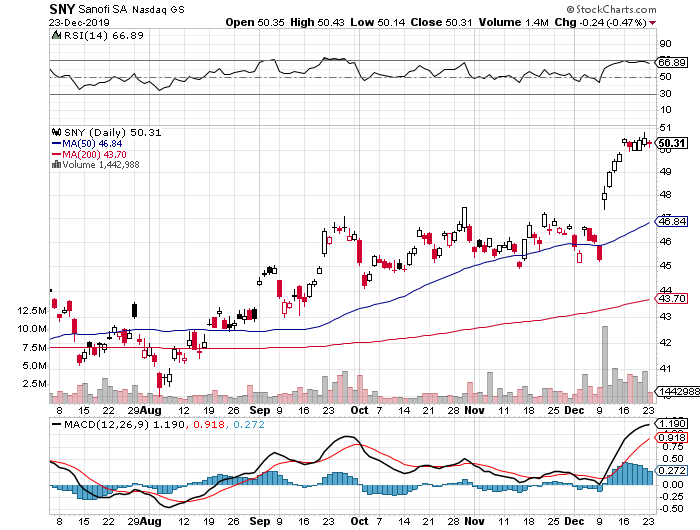

Taking a Second Look at Sanofi

Investors on the lookout for a large-cap biotech investment have several options, with Sanofi SA (SNY) being one of the most interesting companies to consider. The French multinational pharma giant has a diverse drug portfolio which has been attracting attention recently thanks to its focus on the lucrative market of diabetes treatments.

Unfortunately, the diabetes project hasn’t been working as well as Sanofi hoped this year. Earlier in 2019, FDA rejected the company’s new diabetes candidate Zynquista. Despite this setback, the company announced more promising Phase 3 results from another diabetes treatment, Toujeo, which is aimed at children and adolescents with Type 1 diabetes.

Regardless of the roadblocks encountered by Sanofi in its bid to dominate this lucrative market, the company has been insistent in this endeavor -- a determination that’s actually pretty understandable given that the diabetes market covers over 425 million people worldwide.

So far, Sanofi has managed to be one of the leaders in this sector, with insulin injection pen Lantus working as a stable revenue driver for the biopharma for years now.

To offer a clearer perspective on the promising diabetes sector, Lantus raked in $3.95 billion in sales for 2018 alone -- an impressive growth that has been attracting competitors left and right.

In fact, this Sanofi diabetes moneymaker has been experiencing steep competition with sales slipping by over $1.17 billion largely due to the emergence of cheaper and stronger rivals in the market.

Nonetheless, Sanofi wants to maintain its stronghold so new deals are expected to crop up soon in an effort to shore up its declining Lantus revenue. Among the drugs in its portfolio, Toujeo has actually been doing quite well, raking in $930 million in sales in 2018. While this doesn’t really cover the $1.17 billion slip from Lantus sales over the same period, the figure is close enough to bring hope to investors and keep competitors at bay.

Sanofi’s strongest competitor, particularly in the diabetes market, is Novo Nordisk (NVO). The latter’s diabetes drug Tresiba has actually accounted for 84.2% of its overall sales.

While this is definitely daunting for Sanofi, the sales performance of Tresiba can also highlight a key differentiator between the two. That is, Sanofi offers a more diversified portfolio especially in terms of revenue sources. Meanwhile, Novo Nordisk is focused on the diabetes market alone.

Although both Toujeo and Lantus have been remarkable in sales thus far, Sanofi has a number of other top-performing drugs in its portfolio. After all, Sanofi isn’t just about diabetes treatments.

In terms of growth, eczema treatment Dupixent has shown a remarkable 142% jump in sales over the past year. Its revenues rose to $628 million for the third quarter in 2019. In comparison, the overall sales for Sanofi’s diabetes treatments declined by 18% since the third quarter of 2018.

While it’s easy to get distracted by the allure of the lucrative diabetes market, these treatments actually comprise a small portion of the French biopharma’s drug portfolio.

To date, Sanofi has 85 up-and-coming drugs, with 51 of these already sent to early clinical tests and the remaining 34 either in Phase 3 trials or sent for approvals. To provide a more direct comparison, reports show that only two drugs in the pipeline are aimed towards the diabetes market. The rest of Sanofi’s portfolio has 28 oncology candidates and 18 immuno-inflammation drug prospects.

Overall, Sanofi has a stable, well-rounded portfolio to offer its investors. However, stiff competition can prove to be a huge obstacle especially in the high-growth diabetes space. Its revenue growth in this sector isn’t also as remarkable as its competitors.

This doesn’t take away from Sanofi’s other products though. What it means is that it would be a better call to buy Sanofi stock once prices fall at a cheaper valuation.