Tech Option Volume Unhinged

The euphoria in big cap tech shares is the catalyst moving the Nasdaq index recently.

Call option activity is taking the top off of tech shares with usual low beta stocks surging over 5% in single trading sessions.

This unfortunately is causing our options trades to experience heightened stock volatility and the knock-on effect is our strikes getting blown out.

Some of the excess volatility comes down to traders making big bets in the run-up to the election.

Remember when Trump won in 2016, the market exploded higher when many “experts” guaranteed a massive sell-off would ensue.

In the short-term, the unsustainable pace of speculation in derivatives will translate into wild price swings. Monday brought the biggest rally for the Nasdaq 100 Index since April, but measures of volatility rallied as well.

One proxy for the froth still latent in options, the percentage of overall volume represented by single-stock contracts, remains up 19% from a year ago.

Most of the action is concentrated in mega cap technology and momentum-driven shares.

A consensus is coalescing around a few big buyers coming into the options market to corner it with rumors of purchases around $300 million worth of call contracts on tech stocks in a single day.

The Nasdaq 100 Index has gained in all but two sessions this month and just notched its best week since July after last month’s sharp drop.

Whipsawing markets are also possible when liquidity remains thin.

Trading in options showed itself capable of influencing share movement in August and September when dealer hedging (demand from people who sell options for the underlying stock) created feedback loops that helped drive the Nasdaq higher.

That dynamic can also make sell-offs worse than they should be as well as sellers adjust positions.

Big trades in thin markets, especially in technology or momentum trades considered overbought or oversold, increase the potential for exacerbated stock moves as dealers hedge exposure.

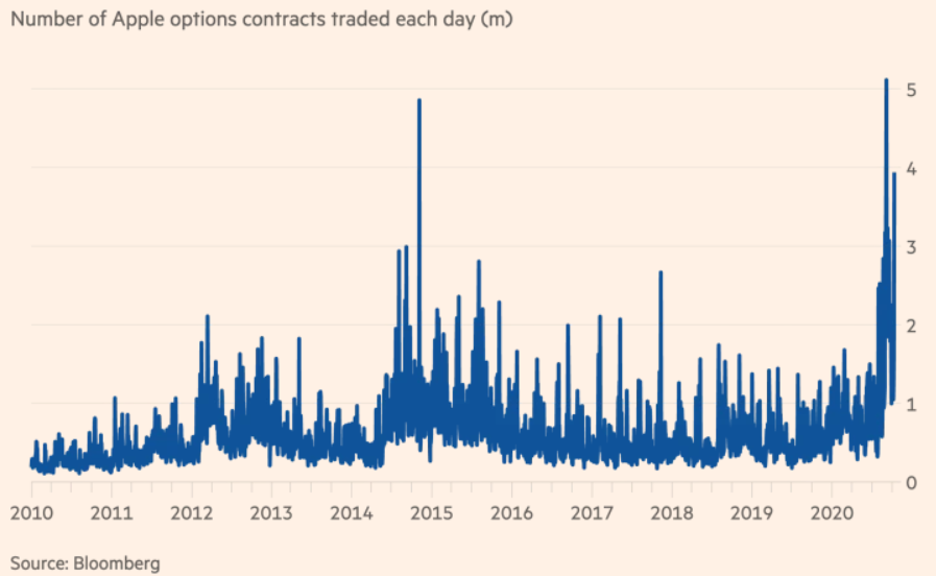

Call open interest in Facebook (FB), Amazon (AMZN), Netflix (NFLX), Alphabet (GOOGL), Apple (APPL) and Microsoft (MSFT) has averaged 12.8 million contracts over the 30 days through Friday, the highest since early 2019.

The tech-heavy Nasdaq index has gyrated an average of 1.8% per day since the beginning of September, while the broader market gauge has fluctuated by 1.2% over that time period.

Recent options activity has been momentum-based, meaning that stocks tend to attract more interest in calls when it’s rallying versus when it trades lower.

Throw in structural forces that are contributing to a sustained high implied volatility environment, and election hedgers have their work cut out for them.

There are fewer short-volatility players as well in the wake of the health crisis.

There’s also less volatility selling by retail investors after the delisting of some popular VIX products earlier this year like the volatility ETF ticker symbol XIV.

It could take a few years for the imbalances to work itself through the system.

Then there’s the resurfacing of an event similar to the “Nasdaq whale” which is reported as Softbank acting like a hedge fund and buying as many big tech call options they could afford.

Softbank CEO has essentially turned his failed hedge fund named the Vision Fund from a start-up investor into a speculative hedge fund in risky option contracts solely betting on the rise of Silicon Valley tech in the age of the coronavirus.

After being burnt by Uber and WeWork, he finally decided to stay out of the messy acquisitions/seed funding and just speculative through derivatives from Tokyo.

The avalanche of options volume will no doubt cause the tech markets to become jittery and it certainly puts a floor under tech implied volatility for a while.

Retail investors have taken notice of this insane volume and largely stayed on the sideline.

At the apex of the madness, retail traders spent more than $511 billion in notional value on call options and that figure was slashed to $343 billion in the first week of October.

Retail traders tend to buy less-expensive short-dated contracts which tend to have greater convexity and ability to exacerbate share movements.

The level of risk-taking occurring in the public markets is at an all-time high.

Just look at America’s most elite university endowments who have slashed their exposure to the stock markets to the lowest levels since before the crash of 1929. And now they’re betting the ranch on secretive, illiquid, and high-risk private-equity funds and hedge funds.

A US teachers’ pension fund has sued Allianz Global Investors, accusing one of the world’s biggest asset managers of employing a “reckless strategy” that cost retirees almost $800m during this year’s market turmoil.

This is just one example of the high-risk strategies taking place with pension money.

In a lawsuit filed on Monday in New York, the Arkansas Teacher Retirement System claims that Alpha Funds, investment vehicles marketed by AllianzGI, had placed bets against an escalation of market volatility in an effort to recover losses they incurred from the same strategy in February.

So here we stand with derivative trading in tech options and general equity strategies leveraged to the hills that are betting on the system not breaking, or at least not breaking yet.

Even if the system reaches breaking point, many of these private investors are betting on governments to come rescue them perpetuating the feedback loop and offers a conundrum to savvy asset managers to miss or partake in the gaps up themselves.